If you're looking for a car buying rule, let me introduce you to the 1/10th rule for car buying. The 1/10th rule will help you spend responsibly, reduce your car ownership stress, and boost your net worth over time.

If you buy an overpriced car, it is guaranteed to depreciate. If you buy an affordable car based on my 1/10th car-buying rule, on the other hand, then you can invest more cash flow into stocks, real estate, and other investments.

Over time, these investments have the potential to appreciate in value, thereby buying you the most valuable asset of all: time! Having the time and freedom to do what you want is priceless.

The 1/10th rule for car buying is the most followed and most popular car buying rule today. For those of you who want to achieve financial independence soon (FIRE), the 1/10th rule will help you get there.

Americans Spend Way Too Much Money On A Car For Their Financial Health

Back in 2009, I watched in horror as a total of 690,000 new vehicles averaging $24,000 each were sold under the Cash For Clunkers program.

The government's $4,000 rebate for trading in your car ended up hurting hundred of thousands of people's finances instead. With a median household income of only around $50,221 at the time, spending $24,000 on a new car was clearly too much.

Instead of buying a $24,000 car in 2009, you could have invested the $24,000 in the S&P 500. If you did, you would now have over $150,000 today. That's quite an opportunity cost for buying a new car!

Buying too much car is one of the easiest and biggest financial mistakes someone can make. Besides the purchase price of a car, you've got to also pay car insurance, maintenance, parking tickets, and traffic tickets.

When you add everything up, I'm pretty sure you'll be shocked at how much it really costs to own a car and hurl. After more than 10 years, the 1/10th rule for car buying has become the standard car buying rule for financial freedom seekers everywhere.

The Car Buying Rule To Follow: The 1/10th Rule

The #1 car buying rule to follow is my 1/10th Rule for car buying. The rule states that you should spend no more than 1/10th your gross annual income on the purchase price of a car. The car can be new or old. It doesn't matter so long as the car costs 10% of your annual gross income or less.

If you make the median per capita income of ~$42,000 a year, limit your vehicle purchase price to $4,200. If your family earns the median household income of $75,000 a year, then limit your car purchase price to $7,500. Absolutely do not go and spend $49,388, the absurdly high average new car price today!

If you absolutely want to buy a car that costs $49,388, then shoot to make at least $493,880 a year in household income. $493,880 is about the top 1% income threshold today.

You might scoff at the necessity to make such a high amount. However, it takes at least $300,000 a year to live a middle class lifestyle with a family today. Inflation has really made making more money necessary just to run in place.

The last thing you want to do is waste money on a car you don't need.

Minimize Your Financial Stress With A Cheaper Car

If you actually want to save for college, save for retirement, take care of your parents, buy a home, and not stress out about money when you're old, please keep your car purchase to at most 10% of your annual gross income.

Once you buy a car following my 1/10th rule, own your car for at least five years. Better yet, shoot to own it fo 10 years. Don't go selling your car every 2-3 years like most Americans do. If you do, you don't experience the full value of the car. Further, you end up paying wasteful sales taxes each time you buy a new or new used car.

Buying a car you cannot afford is the #1 way to financial mediocrity. One of the biggest benefits of buying a used car is more mental relief. And when you have less stress in your life, you will enjoy it better.

Since Financial Samurai was founded in 2009, my goal is to help readers achieve financial freedom sooner, rather than later. Ideally, I'd like every reader to achieve an above average net worth for their age.

Financial independence is worth it. A car you cannot comfortably afford is a great headwind.

Why You Shouldn't Spend More Than 10% Gross On A Car

If you want to achieve financial freedom, let's go through specific reasons why you should follow my 1/10th rule for car buying.

1) Maintenance costs

The more you drive, the more you will pay to maintain your vehicle. With thousands of parts per car, something will inevitably break or need upgrading. After 10 years of car ownership, everything from your battery to your vacuum pump will need changing.

Not only do you have to pay for maintenance costs, you've also got to pay for insurance, parking tickets, and traffic tickets. Further, the thrill of owning a new or new used car lasts for only several months. However, the pain of paying the same car payment lasts for years.

You might think getting an extended warranty will save you lots of money. But extended warranties are offered because they are more profitable for the issuer, not the car owner. Otherwise, a business wouldn't offer them.

2) Opportunity cost

When you buy a car you lose the opportunity of investing your money in assets that will likely grow and pay you dividends in the future. Everybody knows to save early and often to allow for the effects of compounding. Buying too much car is like negative compounding!

Imagine how much money you would have accumulated if you invested $300-$500 a month in the stock market since 2009 instead of paying for a car? You'd have hundreds of thousands of dollars.

You can dollar-cost average and buy a S&P 500 ETF every month instead of spending money on a car payment. Even better, you could invest just $10 a month in Fundrise, my favorite private real estate investment platform to build more wealth.

Fundrise invests in residential and industrial real estate in the Sunbelt, where valuations are lower and yields are higher. Personally, I've invested $954,000 in a couple private real estate to take advantage of the demographic long-term trend towards lower cost areas of the country. Investing in long-term trends is one of the best ways to build wealth.

3) More Stress

When you pay more than 1/10th your income for a car, you will become more stressed. You'll feel stressed whenever you get a door ding after parking your car at the local grocery store. You'll get stressed whenever you incur wheel rash after parallel parking too close to the curb.

Sometimes when you're driving in traffic, you'll feel more on edge because you don't want anybody damaging your car. If you are within 1/10th of your income, you drive and park stress free. You stop caring about door dings, bumper scrapes, even break ins. Stress kills folks.

In fact, the biggest benefit of driving a cheap old car is less stress. With less stress, your mental health will improve!

Now that my car is nine years old, I don’t care if it gets scratched, or Ding. The other day, I opened my trunk, edit, scraped along a rusty fence. No problem! The older, my car gets, the more I love it. I recommend owning cars for 10 years or more. Then change for better safety features.

4) Makes you want more

The nicer your car, the more you want to spend on other things. You start thinking stupid thoughts like: I've got to buy a matching chronometer watch, driving shoes, and outfit. You start paying $20 for valet because you want people to see you come out of your car instead of park for free.

If you think about it, only the rich or fools buy new cars today. With the average new car price at roughly $50,000, a middle-class household should buy used instead.

5) An expensive car can make you feel stupid

Deep down, you know that if you can't pay cash for your car, you can't afford the car. Each payment you make is a reminder how foolish you are with your money. Why would you want to be reminded every single month of being dumb? The thrill of owning a nice car fades after about six months. But the payment stays the same for years.

Depreciation is intense with new luxury cars especially. I would avoid them at all cost. Instead of buying a $115,000 Range Rover Sport, buy a Toyota Highlander for 1/4th the price instead. Be responsible with your money if you are still on the path to financial freedom.

If You've Already Bought Too Much Car

Look, everybody makes dumb financial moves all the time. The important thing is to recognize your mistake, stop, and fix it! Here are some things you can do if you've bought too much car already.

1) Own your car until it becomes worth 10% of your income or less.

This is the simplest solution if you've spent too much. Drive your car for as long as possible until the market value is worth less than 10% of your gross annual income.

Ideally, you want to get your House-To-Car Ratio up to at least 50 if you want to achieve financial freedom sooner. In other words, the house you own should be worth at least 50 times the value of your car. If you own a car and don't own your primary residence, then you are going to fall farther behind the general public with each passing year.

2) Bite the bullet and sell your car.

If you've spent anything more than 1/5th your gross annual income on a car, I'd sell it. It's making you poor. Even if you have to take a little bit of a hit, I think it's worth getting rid of your vehicle. Don't trade it into the dealer because you'll get railroaded. Instead, try negotiating via Craigslist.

If you have an expensive car lease, here are ways to get out of your car lease. Unfortunately, you will likely be “upside down” on your car lease where you have to pay money to get out of it. Hence, if you can afford the payments, I'd fulfill the lease agreement and swear never to lease another car again.

3) Punish yourself.

Like Silas does in The Da Vinci Code, whip yourself into submission! OK, maybe don't go to that extreme. However, if you don't punish yourself, then you will repeat your mistake and feel fine with what you have now.

For the life of your car loan, take away a food you love to eat such as chocolate. If you are a coffee addict, swear never to drink that stuff again! Save more of your income after taxes. Feel the squeeze so that you realize how ridiculous your car spending is.

If the amount of money you're saving each month doesn't hurt, you're not saving enough!

Recommended Cars By Income (Tastes May Differ)

The beauty of the 1/10th rule for car buying is that it is tethered to your income. If you want a nicer car, you must make more income! Here are some suggested cars you can buy based on my 1/10th rule.

Cars built in the 1990s and beyond are so much more reliable than those built prior. If you are serious about improving your finances, consider buying a car with less options. The less electronics, the less electrical gremlins too. The more you have loaded in your car, the more maintenance headaches you will have in the future.

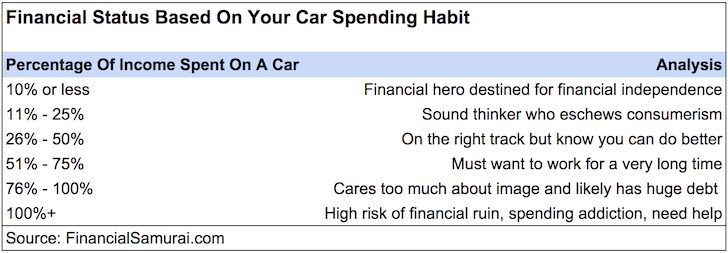

Below is the chart highlighting you financial status based on your car spending as a percentage of household income. The closer you follow my 1/10th rule for car buying, the closer you will get to financial independence.

Please note that there is NO SHAME in owning a car that's worth less than $10,000. I bought a second-hand Land Rover Discovery II for $8,000. Then I drove it for 10 years until it was worth less than $2,000.

The car was great and loads of fun. With the money saved from not buying a more expensive car, I diligently invested the money. A decade later, the money grew by over 160%. But it is important to pay attention to safety.

In fact, the best time to own the nicest car you can afford is when you have kids. This way, you amortize the cost of the car across more heartbeats. Further, you have more valuable cargo which means a safer car is even more important.

But once you've found a safe enough car, put your ego aside so you can have true wealth. All the freedom in the world. Your goal should be to generate enough passive income as possible so you don't have to work. Be a time millionaire or billionaire! Freedom is the true value of wealth.

The Choice For Great Wealth Is Yours

Treat the 1/10th rule of car buying like a game. You will be surprised to find how many different type of cars you can buy with 1/10th your income if you make over $25,000 a year.

If you want a $30,000 car, get motivated by the 1/10th rule to figure out a way to make $300,000 a year. One way is to start a side hustle to generate more income on the side. We're all spending way more time at home now. Might as well try to make some side income online.

If you can't get motivated, then fine. Just don't think you can afford much more. Think about your future and the future of your family. A car is simply there to take you reliably from point A to point B.

If you're thinking about prestige and impressing others, don't be silly. Owning a nice property is way more impressive because at least you can potentially make some money from the asset!

The Worst Combo For Your Finances

One of the worst financial combos is owning a car that you purchased for much more than 1/10th your gross income and renting. You now have two of your largest expenses sucking money away from you every single month.

Think about all the wealthy people you know or the millionaires next door. Chances are high the majority of them own their homes and drive used cars. Their cars likely don't come close to 50% of their gross income.

If you want to achieve financial independence, follow my 1/10th car buying rule. Letting material things stress you out is no way to live.

If you want to detonate your finances and end up working longer than you want for the sake of a nicer ride, then go ahead and spend more than you can comfortably afford. After all, we've only got one life to live.

Buy Real Estate Instead Of An Expensive Car

Keep your car expenses to a minimum and follow my 1/10th rule for car buying. If you do, you will increase your chances of achieving financial freedom given a car is almost guaranteed to lose value over time. Instead of buying a fancy new car, use the money to invest in real estate instead.

To invest in real estate without all the hassle and unexpected costs, check out Fundrise. Fundrise offers funds that mainly invest in residential and industrial properties in the Sunbelt, where valuations are lower and yields are higher. The firm manages over $3.5 billion in assets for over 500,000 investors looking to diversify and earn more passive income. The minimum investment amount is only $10.

Another great private real estate investing platform is Crowdstreet. Crowdstreet offers accredited investors individual deals run by sponsors that have been pre-vetted for strong track records. Many of their deals are in 18-hour cities where there is potentially greater upside due to higher growth rates. You can build your own select real estate portfolio with Fundrise.

I've personally invested $954,000 in private real estate since 2016 to diversify my holdings, take advantage of demographic shifts toward lower-cost areas of the country, and earn more passive income. We're in a multi-decade trend of relocating to the Sunbelt region thanks to technology.

Both platforms are sponsors of Financial Samurai and Financial Samurai is an investor in Fundrise funds.

The 1/10th Rule For Car Buying is a Financial Samurai original post. I came up with the rule in 2009. If you want to build more wealth, join 65,000+ others and sign up for my free weekly newsletter.

Once you get over your ego, you can see that buying TWO $4k crapbox 20-year old Corollas every year would cost you less than buying a new Camry at $37,000 / 7% / 60 months. That’s assuming you just throw the first one away without selling for salvage and buy the second one, and also doesn’t even account for the differential in insurance costs (full coverage and gap insurance would be required for the brand new car).

And that’s just a Camry. It’s more than $10,000 LESS than the average new car cost in the US ($47,244 in 2024).

This concept was interesting until I did the math. It makes no sense at all based on the actual cost of cars today. Not to mention the cost of repairs, associated hassle, and loss of time getting repairs done. It is also theory and makes zero sense in practical terms.

What does your math say? Feel free to share it and some examples.

The solution isn’t to spend more on a car. It’s to spend less.

Make sure your House-To-Car Ratio is as high as possible if you want to achieve financial freedom earlier.

Pardon me if I may come across rather bluntly, but you are absolutely deluded… And I’m saying this after double checking whether there might have been a mistake and you are relating about how things were 5 or 10 years ago – yet it says clearly this was written 02/01/2024!!! Have you actually checked car prices in the past few years before saying one should only pay 10% of one’s yearly salary for car acquisition? I suppose you will also say people shouldn’t spend more than 25% of their income on housing? It begs the question: IN WHAT WORLD ARE YOU LIVING?

I am a pensioner on $20,000 (Canadian) a year and $2,000 cars are simply impossible to find. I just got offered a 2005 Camry for $6,000… My present car is a 2004 at the end of its rope (250,000 km in the rust belt is an achievement by itself) and I should spend 30% of my yearly income on a car that may perhaps last another 5 years, if I’m lucky?

I’m sorry, but advice like yours reeks of the famous “let them eat cake” remark attributed to Marie Antoinette of France before the French Revolution when people with money were like they are today, totally disconnected from the reality of the majority.

No worries. I’ve heard much harsher language before. If you are a pensioner, hopefully you have amassed a large enough net worth over the past 30 or 40+ years working to retire comfortably.

If that is the case, then you can follow my net worth rule for car buying, which used assets as a barometer.

Not everybody is as privileged to have invested and lived through the greatest bull market in history, while having a pension. Something like 14% or less of American workers are eligible for a pension.

For reference, this is the #1 car buying rule for financial freedom seekers. I introduced this rule over 10 years ago (this site started in 2009), and it has been followed by over 10 million people. I update this post every year.

For those of us that make more average incomes you have to almost completely throw out this 10% rule of you want a good car in today’s environment.

I make $66,000 a year and I’m probably going to buy a used 2022 Toyota Prius for around $23,000. Right now I own a 2007 Chevy Impala with 122,000 miles on it that’s burns oil. I live in a Rural area of the Midwest with no public transportation whatsoever, so I drive about 18,000 miles a year. Many of my coworkers drive 25-30,000 miles a year.

I was planning on keeping my Chevy impala forever. Drive your car into the ground baby! Until my mechanic got my car underneath a lift and stabbed a screwdriver straight through a rusted out structural portion of the frame. My vehicles frame could snap on the highway at any time. He told me not to take it out for any interstate driving and he is right.

Now if I follow this rule above, I’ll have to spend $6,600 on a car. You know what kind of car I can get for $6,600? Basically exactly the same car I have now (minus a bit of rust). So now I’m back to owning another late 2000s car with over 100K miles on it and probably the same engine and transmission issues my current car has. I might as well buy something newer and treat it better this time around.

But Why a Toyota Prius? Because they consistently get 50MPG on both the highway and city driving. Why do you think whenever you go to an airport all the Ubers and taxi cabs are Priuses? Because they have the lowest total cost of ownership over their lifetime. The 2022 Prius uses a single speed planetary gear style transmission, dual port injected 4-cylinder Atkinsons cycle engine, and has no drive belt or alternator that can fail. The head gasket issues and EGR clogging problems have been solved in the 4th Gen Priuses. The toyota Prius also has a bunch of plastic panels on the bottom to protect the hybrid system, but has the added side effect of protecting the undercarriage from corrosion.

I plan to drive this car into the ground as well, and I think this is the only sensible additude to have if you plan on buying a new car. If you plan to buy a newer car, plan ahead that you will own this car for the next 10+ years and purchase accordingly. This time I’ll use cosmoline on some areas known to rust.

Excellent feedback and analysis. In your situation, a reliable car is vital given you drive so much. Hence, relaxing the 1/10th rule makes sense.

I still wouldn’t pay 1/3rd of my income on a car, but that’s just be.

I’m a big fan of driving a car for 10+ years. My car is a 2015, so it will complete 9 years come July 2024. But it only has 51,000 miles.

Enjoy the Prius!

I think your car spending is reasonable as long as you can pay cash for it. You obviously need a reliable car you could drive for the next 8-10 years. For example, Dave Ramsey recommends not to spend more than 50% on annual income on ALL vehicles owned by a household. You are well within this range. The sad truth is that majority of Americans buy cars they can’t afford and that is why 85% of them are bought on credit or leased. Sam’s 10% rule I think is mostly for people with high incomes who pursue the FIRE dream. I personally try not to spend on a car more than my monthly income, which is easy to do if you make $40-50K a month, and pay cash unless I get 0% financing for 36 months. Congrats on you car choice.

The answer to everyone’s doubts/concerns below is a used Lexus ES350 or RX350. I bought my 2011 RX350 in 2015 for $20k cash and my 2014 ES350 this year for $17k cash. RX350 has been flawless and and has 138k miles on it now. The ES350 is flawless (same drivetrain as RX350) and has 66k miles. I make 160k per year and keep my cars till the tires fall off. Both cars will EASILY reach 250k miles (probably 7-8 years for RX350 and 10 years for ES350). A Lexus or Honda product will last the duration and have small maintenance bills. TBH, I would not have to think twice about buying a 2007 ES/RX350 for $5-10k as they are solid cars. I think this post is brilliant and should be followed.

Greetings,

In 2015 my wife and I bought a new Scion xB, 2015 model year, for $18,840. Our previous car had died and I really needed another one for commuting to work. True, we didn’t need a new car, but the price was acceptable considering it’s a reliable Toyota product. Our combined annual income at the time was $203,000. I still drive the same car today. It’s in very good condition, fun to drive, and we never regretted the purchase. And it has never had a mechanical failure. This 10 percent rule can be done successfully. Don’t waste your money on cars. Thank you for the good advice on this web site.

While I understand and can fundamentally agree with the principals behind this rule, it’s laughable how out of touch this is to the reality of most. I’m sure it’s easy to preach one size fits all financial advice when your individual gross income VASTLY exceeds that of whole households across society.

Why is me buying a $8,000 car when my income was over $80,000 out of touch with reality? The second hand car I bought served me well for over 10 years. Then I followed my 1/10th rule for car buying again and bought a $20,000 Honda Fit and traded in my old car for $1,500.

Just because your reality is different from another person’s reality doesn’t make another person’s reality laughable. What’s laughable is the median household of only $75,000 in America buying an average priced car of $49,500. That’s a surefire way to never achieving financial independence.

Being able to invest and watch the money compound over time for more freedom is way more valuable than buying an overpriced car that is guaranteed to depreciate in value. But, to each their own!

I bought a brand new Mazda 3 about 12 years ago that I still drive. I was probably at about 20% car price / income at the time, but I had saved quite a bit of money the previous 2 years not having a car at all. Now with the car value falling and my higher income I’m under 5% in car value / income even with today’s inflated used car prices. A car has generally been more a convenience and luxury for me since I do live in an area with good public transportation.

With current car prices, is the 1/10th salary rule a pipe dream? I think it’s impossible currently and possibly moving forward.

I just sold my 10 year old Hyundai Economy car for $10k to Carvana. It needed atkeast $2500 in maintenance. New tires, brakes, suspension… but had pretty low mileage at 55k miles. Carvana will probably turn around and sell it for $15k. I bought it NEW for $16k in 2013.

1/10th rule for someone making $50k a year is a $5k car. I would fear for my life driving a $5k car in this market.

$2500 is a lot less than a new car

If you’re earning minimum wage you probably shouldn’t even have a car. You’re sore doing more on gas, insurance, parking and repairs than you can afford. Take the bus. Ride a bike. Walk. Fiscally speaking you probably should not own a car unless your household net is more than $80k, and even then you’re throwing away more money than you can really afford.

I agree that as income goes higher the ratio would change. Probably every $50k mark ratio lowers. Nobody is making $200k and then buying a camry. Also to ppl complaining about used cars Toyota is King and Honda is probably second. It’s funny how ppl will buy an American car (ford, Lincoln) complete crap and then blame it on that it’s used.

My Goal is:

making under 50k > buy no car or motorcycle

100k > used Toyota Camry, 10 years old

200k > used Luxury 5-10 years old (Mercedes’ Lexus etc)

300k > buy any car I want: S class or Tesla P100 or rotate every year

I’m making over $250 and still drive a Rav 4 hybrid. Maybe I should scale up for more comfort, but with current economy, it seems foolhardy.

I wonder how this formula translates to EV, with the price premium associated with them (20-30% cost of equivalent class of cars). I guess 1.30/10 of salary, or do we all need to go down a class? We need to take into account the long-term fuel savings and maintenance costs. I hope this article gets updated.

I’d assume you mean 1/10 of your net sal not gross? Well that only leaves me with very high mileage car that would be more in my machanic’s garage then in mine. The cost of used cars have skyrocked due to high demand and inflation with your paycheck not keeping up.

I had an old car for years but I had to junk it because they don’t stock the parts anymore; the fuel pump went (it was replaced six months before) the car would have kept going if I could find another one but that model car was long gone to the crusher in all the junk yards.

So far I’m lucky that I can walk or bike to work but that’s gonna change too since my rent is going to skyrocket which will force me to move farther away from my job. So now I have to look for a car that is dependable/low miles/cheap to insure/good on gas for around 3,500 or less?? Not in this lifetime!

Gross. Sorry if I was not clear in the post. But I will make it more clear now.

For three years, my car was probably worth between $2000-$4000 until I finally traded it in for $1,500. It worked fine.

As I made more money, I bought a nicer car. It’s a good motivator!

does this include insurance or just the purchase price? As a new driver, my insurance premium is worth more than the cars I am looking at.

Definition of lifestyle creep

Indeed. And if done well, it’s great because it feels so good to spend more money as you get wealthier. Otherwise, we end up dying with too much. And that would be a waste.

wow just ignored my question. Great ethics you have. You have all this money but no manners

Curious. Do you think I owe you anything? If so, the entitlement mentality you have might really hurt you over the long term since you’re not paying anything and consuming this post for free. There are over 1,200 comments on this post. It’s hard to keep track of everything.

Please work on your emotional intelligence (EQ) if you want to grow your wealth, build better relationships, and live an easier life.

“does this include insurance or just the purchase price? As a new driver, my insurance premium is worth more than the cars I am looking at.”

To answer your question, just the purchase price.

At some point this rule stops making sense right? Like if you have a household income of $300k you can afford a $50k car easier than someone who makes $60k a year and buys a $6,000 car.

As you make more money your cost of living doesn’t go up unless you decide it should, but a loaf of bread costs the same regardless of your income.

Great article. My partner and I are a one-car household. We own a car that we purchased for less than 5% of our gross annual income. Pretty good, right?

However, I am starting to look at the total cost of ownership more closely. We’ve been considering getting an EV for some time now. With the higher price of gasoline and extra maintenance costs for ICE vehicles, we would actually save money on an annual basis by trading in our car for an EV that is more expensive on paper (paying cash for the balance, of course).

Hi Jesse – You might enjoy this post on the getting an electrical vehicle might finally be worth it.

Thanks for the link! The only thing holding is back is the recent spike in price of used EVs. Of course, if that gets much worse it will make ICE vehicles look good again.Had we bought a Nissan Leaf a few years ago I’d be sitting pretty right now.

My disability insurance payment is about $2300 per month. I had paid my home off early and inherited around $120k. I want to rent for a year to improve my credit score so I can buy a modest home costing around $150k. I was planning on spending $20k on a car that I intend to keep 10+ years but after reading these articles, I’m second guessing if I should limit the car purchase to under $5k. I have no problem driving a beater; 20 years ago when my terminal illness made it impossible for me to work and make the money I was used to earning I learned really fast that when that hood gets popped open, some cars still say “Toyota”. I then let my high dollar, high payment car go and spent $250 on an older car that lasted 2 years. I haven’t had bought a car via financing since that time. Just wondering what my best strategy would be right now.

Sounds like you need a really reliable car. 10% of $2,300 a month is $230. I would just pay $20,000 cash for Toyota Corolla for something really reliable with the hundred $20,000 inheritance. Keep it simple and minimize car stress.

Hi Sam.

I’m Brazilian. How can I apply and follow this rule living in my country, with a different currency?

Same concept. Spend no more than 10% of your annual gross income on a car, even if it’s in Brazilian real. This may make things even tougher to buy the car you want. But again, a car is a depreciating asset. So you want to allocate the least amount of capital possible to a depreciating asset.

Old used Camry?

One must really love money and hate oneself to do this

Birthing wrong with a used Camry for folks making under $150,000 a year. My dad used to have a 7-year-old one when I was in high school. It ran great. He retired at a regular age and is comfortable.

My wife and I tried this rule. In 2018 we picked up a 2010 Subaru Legacy for $7500 (cash), we were making around $120k at the time. Later on in 2018, we picked up a 2009 Ford Expedition EL for $5000 (cash). Our income has nearly doubled since then. We did the FS and DR approach all in one. It worked well for us to build up savings, but it was a pain in the backside.

The Expedition turned into a headache, leading to us being stranded several times. We learned that the seller disabled the engine light when we bought it, then later found out (assuming) the mileage was rolled back… A LOT. Yes, we did a Carfax on it prior to buying it but the mileage was most likely rolled back 5 years prior. We ended up putting about $8,000 in the car over the 3 years we owned it, not including oil changes. $13,000 in over 3 years, $1,500 back to us on trade-in.

The Subaru did us well for the most part, we ended up having a transmission issue that was going to cost us $6500 to replace, and we had put about $2500 into the car over the 3 years we owned it. It would have been $9,000 repairs over 3 years PLUS the $7500 we bought for it, so we declined and traded it in. We received $3,000 for the trade in for parts, it would have been $5,000 if we replaced the transmission. If we replaced it, that’s $19,000 spent over 3 years on a car that gave us 35,000 miles – it could have gone more had we replaced the transmission but that cost effectiveness just wasn’t there.

We bit the bullet and bought brand new cars.. 2 of them.. we told ourselves we were NEVER going to buy a brand new car. Our financial situation is/was in a good spot; we didn’t follow the 1/10th rule but both cars will be paid off within 36 months. The comparative cars we were looking at were $30-$40k with 100k+ miles, or we spend $40k on a brand new one.

We have 3 kids and live in rain/snow, so we wanted AWD and space. We had PTSD (jokingly) with buying the Expedition and didn’t want to take another chance – too many DIY people out there that don’t know what their doing to their cars. The car loans are sub 2.5% as well. We bought the two new cars thinking that if they last long enough, two of our kids will have them around the 10 year marks.

We paid a “premium” for space, updated safety, reliability and longevity. Even if we have some repairs that are a few grand every 5 years, and we put 200k on the cars before the kids get them, we KNOW the history of the car and we won’t have any surprises.

All that being said… I do like the 1/10th rule and understand it greatly, especially when you’re looking at sling-shotting yourself into a better financial situation. We are also fortunate enough to continue investing/saving/paying off debt with the car payments that will soon be gone.

Cheers.

Much cheaper to buy brand new cars in a long run.

I don’t know who came up with the 1/10th rule, but it was clearly someone who knows nothing about cars. Cheap cars are unreliable money pits, and your story illustrates that. I’d rather spend more for peace of mind.

But I don’t have financial security. At least I have a nice car!

Very interesting article and very informative to many (but not all) people. That being said, not everyone is in the upper 10% wage earners and can waste their hard earned money on such toys costing the majority or more of their income. Those folks that drive BMW’s & Mercedes…all the power to you if you can afford it. But not everyone lives in California, metro-NYC or similar area and has that much disposable income.

The key (as I am in my mid-60’s) after living all over the USA and parts of the world is DON’T LIVE BEYOND YOUR MEANS. Sure, everyone wants to live on the beach with palm trees and great weather year round. I know, I did it from Southern California to the Castles of Edinburgh and everywhere in between. Now I live in the country far from the big cities and related stress due primarily to financial uncertainty. Why uncertainty? Because NOTHING is guaranteed in life except taxes and death. Not your job, income level, health, stock market, vehicle, spouse, home/apartment or anything else. A simple accident or mishap can alter a persons entire life. With all the insanity in today’s “Covid Culture”, things have gone “Bat-S*IT Crazy”.

That being said, after reading many of the comments in this thread, it is interesting to say the least, hearing from both sides of the financial spectrum. What works for someone living in upscale San Francisco is not going to work for someone living in rural Columbus, Mississippi and vice versa.

Personal opinion, if anyone is living paycheck-to-paycheck and spending $60K on a new truck is either trying to impress the girls or over-the-top with testosterone injections. The older guy’s reading this know exactly what I’m talking about…we all have done it to some point. I have seen young people go without eating, live in a dump and work numerous part-time jobs just to make the monthly truck payment on the $60K PU. Insane.

I have always bought high-mileage dependable vehicles. Yes HIGH MILEAGE and if you park them side by side to a new car, you can’t tell the difference. I have read in this thread that a cheaper vehicle will cost $3000+/year in auto maintenance. Yes, if you buy garbage…evidently the guy who wrote that has no idea on how or what type of used vehicle to buy. Remember, in the 1970’s and earlier (specifically up north) cars that made it to 50,000 miles were considered unheard of. The body would rot before the engine failed. No so much today. I’ve seen vehicles past 400,000 miles on the road! You need to have an experienced individual go to the seller and inspect for anything major. The transmission and engine are the biggies. There is no reason you can not have a decent car for around $2500 if you do your homework.

Think about payments. Unless you pay cash (most do not), you can double the amount of the loan if you take it to full term. A $15,000 loan will be like $30,000 when all paid off. Then the REQUIRED FULL-COVERAGE INSURANCE until the loan is paid off in full. If you live in a big city, that is BIG BUCK INSURANCE. Yes, you might save on gas mileage over time and repairs, but, will you be paying $400+/month in auto repairs? I don’t think so.

Bottom line, do what is best for you and your situation as no 2 people have the same variables. What works for me may not work for you. Personally, I don’t have a “Status Class” vehicle to drive around trying to impress others as is unfortunately so common. I’m happy with my 10-year old Jeep Grand Cherokee that is paid off in full ($3000 at the time) that has no body damage, has over 200,000 miles on it, spent only around $300 over the past 2 years in maintenance parts (I repair my own vehicle) and was worth around $40,000+ when it was new. I’ll drive it until it drops. If I bought it new and took out a loan, I would have been a slave to the bank and insurance company for 5+ years. Less stress my way!

PS – Don’t get credit cards unless you pay it off 100% each month either. The 20% interest will eat your soul if left to pay out over time!

I do somewhat agree with the objective and reasoning of the goal, with one caveat. The rule is certainly achievable IF you can perform some car repairs yourself.

I make about average household income, and I own a 2001 Honda Civic and 1991 Toyota. By that metric, I am meeting the 1/10 rule. But for these cars have repaired them myself. The timing belts, faulty camshaft sensor, replacing brake pads. If you can do the work yourself, buying a Civic, Corolla or Camry, you can reliably get by paying very little for a functioning car.

Also, I don’t stress things like dings in parking lots, thieves targeting my cars, or any other damaging element.

I will say I agree with the author’s sentiment, but I do not think it is a make or break law. If someone does 1/5 instead, but sacrifices other areas, they can still accumulate respectable wealth. But the author already made a table for that anyways.

This post didn’t age well at all considering what’s going on with used car market. Used cars cost like new

That’s because you’re not thinking about the opportunity cost of investing in the stock market, real estate market, crypto, etc.

A poor person thinks only about the cost of the car. A rich person thinks about opportunity cost.

I will share a personal example of opportunity costs. We bought a new Tesla Model S in March of 2015 for $108k and sold Apple stock to pay cash for it. At the time, we were living in NorCal and where Teslas were common in our neighborhood. One of my buddies who ran a large body shop group that was one of the few authorized Tesla collision reapair centers and had toured the Tesla plant in Feemont. He was super impressed with Elon and their business model and was encouraging me to buy at least $100k of Tesla stock as he had just bought $150k. I didn’t buy any but if I would have taken his advice that $100k in TSLA would now be worth $2,545,000. I think about it often as I still use that 2015 Tesla with 126,000 miles on it as my daily driver. It’s worth about $32k now, lol.

How do you spell stupid? W-A-R-R-E-N… And that’s for buying a $105,000 Tesla. People like you are so obsessed with others think that you feel you have to live up their expectations, drive what they drive, go whete go etc. Living in the same neighborhood with the Filthy rich wasn’t going enough. You could of went and bought 2- used Honda’s a couple years old or even just 1 and banked the $75,000. Why Honda over other imports. Because of the reliability factor. That Honda will last you forever in some cases as long as you service it appropriately. My next choice would be a usedLexus. They have good engines and are the cheapest to maintain according to many. If you have to hide your Lexus from your neighbors view then you need to move to a different neighborhood as it seems you probably do quite often. Not listening to your friends investment advice may of cost you in terms of paper wealth but hell we all have made that mistake. If someone told me 20 years ago to put my money into bottled water as it’s going to be a huge money maker in years to come I’d a thought he list his mind. Don’t believe in the market either. Many have gone bankrupt and to jail in that corrupt thinking. Ask Martha Stewart. Playing the stock market is like horse racing. Cheat to win, cheat to lose then cheat again to recoup the losses. Life is too short. And if a Lexus isn’t good enough for ya then you might plan on working til you die. You can’t take that Tesla with ya figuratively although some might opt to be buried in theirs, but you can keep making monthly payments for it til you do die. That’s essentially what one is doing by wasting their savings or inheritance on an expensive vehicles. I’d give anything to have a new Raptor. I’m just not willing to pay $100,000 for one that will lose half its value in few years. Crazy stupid there.

Reading this now as I currently need to purchase a car…and I don’t understand FS’s response. The purchase price of a used car now seems to EXCEED the purchase price of a new one of the same model. If the new and used car both drain $30K, where’s the difference except for the lack of warranty, higher maintenance cost, existing wear/tear, and greater uncertainty in buying used? Without a lower sticker price, I fail to see the value in the current market.

I’m not sure what else to say. Feel free to buy whatever you want for whatever price.

If you are OK with forsaking any potential future investment returns, that’s probably a good thing. B/c it means you are already saving and investing enough for your future.

The YOLO economy is here!

This article seems like another hot take. While I definitely agree with the main sentiment (i.e. people spend too much money on cars), 1/10 is way too restrictive. When I didn’t earn as much, I used to drive real beaters, but it got to the point where the hassle of going to the shop all the time just wasn’t worth it. I now drive a Subaru that I bought new in 2015 for 19k. Given that I make about 170k per year, I’m not even adhering to this rule despite being what I consider to be quite frugal.

Wealth serves to fund consumption and enhance quality of life, but people need to be sufficiently conservative to plan for a lifetime of purchases and “what-ifs”. As noted in the article, it’s also important to be cognizant of opportunity costs. Thus, the article’s main point is well-taken, but (as usual) it’s taken to an extreme.

My car buying rule is actually not a hot take. I presented it to the world over 10 years ago and millions of people have take into account.

Over the past 10 years, we’ve had a incredible bull market in stocks, bonds, real estate, and many other asset classes. I really hope that a lot of people during this time Invested more than spend less money on the a car they really didn’t need.

But this is just my recommendation and guide. People are free to do whatever they want their money. Everything is rational in the end!

Yes this is absolutely a hot take. To apply a 1/10 rule you should be applying yearly. Especially in today’s market, if you go out and buy a $4000 car and it has problems on you throughout the year and then the next year or two or breaks down on you then what’s the difference between that and buying a new car which is reliable and paying $3000-$4000 on it yearly? To apply this one 10th rule you will also have to understand some thing about cars in order to buy used, which not everybody does. I find this article just an extra add to confusion, not a solution. It doesn’t add any value or understanding to the costs of buying an old car or how to even go about it. You don’t just spend 1/10 of your salary on a used car and be done with it for even one year. And under these guild lines you could be missing out on a reliable used car over an extra $1000. This article doesn’t guide you in anyway, it’s pointless. It should be revised or deleted.

Sure. If you don’t like the rule, presumably because you don’t come close to following it, do your own thing. No big deal. Nobody is judging you.

Everything is rational. If you love your car and you are happy with your financial situation, great.

Personally, I am happy to not spend so much on cars over the years so I could invest the money fully into the stock market and real estate market.

I just enjoy making more money so I don’t have to work as much to take care of my family. Earning passive income is something I enjoy more than owning my car.

But after such a massive bull market since 2009, I’m thinking of upgrading and living it up more. Once my Range Rover Sport gets to be 10 years old I’m 2025, it’ll be time to change.

I think the ideal length of time to own a car is about 10 years or until it is about 10 years old.

See: https://www.financialsamurai.com/the-ideal-length-of-time-to-own-a-car/

Wow wow wow car buying advices from a Range Rover owner. Interesting.

Pretty cool right? The 1/10 rule doesn’t discriminate between the type of car you buy. It provides a guidance for how much to spend based on income.

Would you rather read car-buying advice from a bicyclist who doesn’t need or want or can’t afford a car?

It’s really up to you whatever you want to spend. At the end of the day, it’s your money and you can live the way you wan. This article was more for people who artist friend we can arrange to help them achieve financial freedom sooner.

If you want to buy a nicer car, make more money. Making 10 times its value.

And on top of everything I said which you may or may not approve. Is that you drive half of the national average. The cost of you owning a used car which you do not let us privy to it’s cut in half for the average person. And again not sure if you do any of you own work On cars or not.

The cost of driving a used car is not that much higher than that of driving a new car, unless that new car is a hybrid. In fact, in most cases, it’s lower, if you take the cost of insurance and depreciation into consideration.

I respect your opinion but I still think this is way overkill. To get straight to the point, not everyone is sitting on a goldmine of money to pay 10% of their annual paycheck on a car and then end up racking up thousands more in repair bills. Case in point myself. My first car was a 2002 VW Passat which I picked up for $2500 but ended up spending $4000 more over two years, along with sleepless nights before I finally bit the bullet and got a certified pre owned 2017 Nissan Altima that came with an extended warranty. Fast forward to today and I just bought my second CPO vehicle, simply because of the stellar ownership experience I had. Did I lose on opportunity cost. Yes, but I could sleep well at night knowing any unforeseen expense (Like a $1200 wheel bearing replacement I did two years ago) would be covered by my warranty, but also the fact that I had a smile on my face every time I got behind the wheel of that car. Cars are my passion, and I have zero regrets spending on one. I will add that I do save/invest at least what I pay each month for my car loan, so I make up a little of what I lose in depreciation. This is also personal opinion but someone buying a 10 year old Land Rover really shouldn’t be advising others on cars. Those things are so unreliable, I wouldn’t go near one with a 10 foot pole. I did have the option of a 2016 Land Rover when I bought my latest car, but even an extended warranty couldn’t convince me to buy one knowing that parts and maintenance would make me broke, even though a vehicle like a Land Rover is perfect for my outdoor lifestyle. To put things in perspective, I’m 29, just having finished graduate school with a PhD, with near zero college debt, so I can afford to lose a little opportunity cost if it means living a little. Also, the idea of passive income doesn’t really appeal to me, simply because I’d be down to working till I’m 85 if it means doing what I love and making an impact on my field of work. This article has a target audience, like my buddy who’s investing to build passive income and follows the 10% rule to a T. But for someone like me who’s got a game plan in place for owning a nice car while at the same time saving sufficient for retirement, I think it just kills the fun out of life.

I will say though that I am not adverse to risks, so spending on a car and investing in higher risk stocks and ETF’s is my thing, and should not be a thumb rule for anyone else to follow. It’s worked well for me, but I can’t guarantee it’s going to work for you.

I think you are missing the point. The point is that the more expensive the car, the more other costs are (typically insurance). Warranties run out and parts wear out on all cars. Also, we can assume you rent and drive an expensive car.

It is fine to justify the expense. That is not the question, but it is not a smart financial choice. And I drive a 10-year-old Grand Caravan that cost just over $6 grand two years ago.

I don’t agree with the ‘not a smart financial choice’ argument. I don’t think there’s a one size fits all financial gameplan for every person. The 10% rule works well if you are already rich or have a large chunk of money in savings, that way the car you get is actually reliable and comes with a warranty in the case of the former or you have disposable cash that you could put in to fixing the car.

In my case, I bought a certified pre owned Nissan Altima for $16k in 2016. This June, my transmission started giving out and I was at 98k miles, just two shy of the end of my extended warranty, and the dealership couldn’t ‘find’ the problem because shutting off the car and starting it up again temporarily made the problem go away. Now I could bite the bullet, dip into my year old savings(I graduated with a PhD last year so I’m 29 and in my first actual job) or do the smart thing and dump the car while the used car market is skyrocketing and get almost the same amount as I put in when I bought the Altima 5 years ago. I shopped around and found a great deal on a 2018 Equinox with AWD, the premium package and the pano sunroof for $24k. With my trade in value, I’m paying just $50 more for the Equinox each month. I also invest/save around that much so it’s not like I’m living beyond my means. And this is my first transition job post a PhD, so I’m fairly confident I’ll pay off the car sooner than my loan term and still save enough for a comfortable retirement. Now I ‘could’ have saved the $$ I’m paying for the Equinox and invested it but at that point it’s money I probably won’t live to use(unless I live past 100). There’s a good saying: You never see a UHaul behind a hearse. You can’t take that extra $$$ with you when your time is up. I can both enjoy my passion for cars and save for a comfy retirement at the same time with my current trajectory.

This smacks of special pleading.

The rule is a good guideline, and yes, it means many people wouldn’t even have a car if they followed it. But if you want to be like most people, then you will end up like them – which is living paycheck-to-paycheck.

Not sure why you keep mentioning you have a PhD, as it’s irrelevant to the point and only shows that having a PhD is no certainty of financial literacy…

I think a PhD is a bigger investment than putting $500 in the stock market each year for the 6 years you’d spend to get the degree. Education is never a waste of money. I’m not talking about most people, I’m taking about peers with a PhD in my field. My professor with a PhD in my field makes about $250k a year with his wife and they own an Audi E-tron and a Chevy Traverse, they buy new cars every 3 years and are building a new house so I doubt he lives paycheck to paycheck. I also think he’s smarter than someone who makes $250k a year and drives a Toyota Camry because they feel guilty about spending more on a car when they love driving. If you can’t enjoy the money you earn, you need to question your life choices.

I think you just reinforced my point above. And your example professor (if real) is almost certainly living paycheck-to-paycheck if they live anywhere near SF or in any HCOL area.

No I haven’t. I’m saying you can enjoy spending money and save if you make enough money. Even with a temporary post doc position, I still save money despite renting and paying off a car loan. I know that once I move to a full time professor position in academia, I’d probably save even more. Assuming I work till I’m 70-75, I’d have plenty of money to enjoy retirement and then some. You’d need to be splurging on a lot more than a car to live paycheck to paycheck with a $250k salary, so it’s all relative to someone’s lifestyle.

I think this article works well for someone like my sister and brother in law who view work as a chore and want to retire early like the OP. Otherwise, you’d essentially be making money you’d never really end up spending unless you somehow live way past 100.

Well, if you’re a postdoc now, you *might* be a full professor in 10-20 years. Academia is brutal. Why you need to save now.

This has to be the stupidest take I’ve ever seen. If you make $60k/yr only buy a car that is worth 6k… wtf logic is that?!

I deserve a nicer car if I make $60K/year. Why can’t I drive a $50,000 BMW if I want to?

Just because I didn’t do well in school or go to a good college and land some high paying job, I should be able to afford the same luxuries as those who have done those things!

A $50k BMW is overkill, just like this article. You’d be better off with a much more reliable $30k car. Word of advice, don’t buy European vehicles, the maintenance cost will get you eventually. For comparison, a Camry XSE costing ~$30k will hold its own and then some against a BMW 5 series in terms of equipment and features and will give you more than 200k miles of use. You’d be lucky if that 5 series makes it to 100k miles without major mechanical issues.

I believe the person you are responding to was being sarcastic. Read the last bit again…

I can’t even get on board with the 1/10 rule. I don’t want to spend more than $2,500 period, I don’t care if other people think I’m poor because of the car I drive, I would prefer to insure I’m not poor because of the car I drive. The new car flavor wears off way too soon I could never justify paying a car note, the car serves the same function, get you from point a to point b. I’m not paying a premium for that. I’ve seen countless friends take on car notes from $300 to $500 a month, it’s a colossal waste of money. Many of them trade up every 3 to 5 years. I can’t understand that desire to be in perpetual debt, it’s like they don’t even care what the total cost is, they just say “It’s only $300 a month” I’ve never had a car note and never will, I was never able to understand why so much commitment must be given to what gets you to and from work when cheaper options were always available. A $2,000 car that is well taken care of can get you to work or the store just like a $50,000 car. The cost of a car note would have to equate to the cost of extended basic cable in the 1990s for me to justify it and I’d even have a problem with that because it’s recurrent. That was $40 a month. Of course on my income level, this guide also says I should basically be getting around on a skate board or a scooter.

I admire your aim, however at $2,500 I would be concerned about the car’s reliability. Especially nowadays with the inflated car prices. A cheap car is no good if you need it to commute to work and run the risk of not being able to get there.

Hi there! Really enjoyed this article, thank you. Before I get to my financial/car question may I suggest you put a more user friendly “Leave A Reply” / Comment area… I had to scroll an insane amount past all your 1000+ comments until I found the comment box at the very end. Why not install at the end of your article?!

Your 1/10th advice, are you suggesting 1/10th of one years costs per vehicle? So we make about 130k /year, 10% would be 13k. Would that be our budget for vehicle costs per year? Or total cost/life of the vehicle? If it’s just the budget for the year, that’d be estimated about $1083 per month or less.

We bought a car new in 2006, total costs about $25k, paid it off and still driving it today June of 2021. Definitely have gotten our value out of it! We’re keeping this but need another vehicle and want to stay under 30k, well under if we can find the smaller suv needs we are looking for. Looking at your advice, it’d make sense if you’re saying don’t spend more than 10% of your income on a car yearly… but if you’re speaking 10% total life of car, seems very extreme and not a lot of options with that?

Another question, We’ve saved up money and can buy with cash or at least part of it but don’t want to tie up cash in a vehicle IF we’re able to get a very low interest rate? What’s your take on cash vs. loans etc?

Thanks so much for your time and help!!

Hi Sam, I appreciate you writing this, I think it points a lot of people in the right direction, especially those that view cars as a utility. I assume that if someone was to view cars as a hobby and spend the money they have allocated for hobbies as well as 1/10th their income they have on a car, you’d see no problem with it?

My main gripe, however, is that a lot of the reasons you brought up for not overspending on a car (maintenance, insurance, life-style creep) are more closely tied to the make a model of a car than to its purchase price (whether new or used). For example, if someone made 120k, using the 1/10th rule, they could buy a 12-year old BMW 7-series for 12k and it would be better decision than a used 2-year old camry for 20k. The problem is that the aforementioned problems, (especially maintenance), are going to be way worse on the BMW and cost way more in the long run, making it a worse decision, despite the lower purchase price.

My point is that I think a car’s affordability has a lot more nuance to it than simply the purchase price of the vehicle. I’m interested to hear your thoughts on this. Thanks!

If income 120k, according to 1/10 rule one should get 12k Camry, which for sure less maintenance than a 12k BMW 7.. Nuance is that with same budget you still need to look for less mainenance and less insurance car, but that apply to new or used car.

If you can justify how newer 20k Camry cost less than a 12k Camry after maintenance, insurance…etc then yes 20K Camry will make more sense than 12k BMW.

How does this rule apply to households that need 2 cars? Also we already own one car flat out and will need to buy a new car later this year.

It’s the same. 1/10th rule applies to total household income for as many cars as you want to buy. $200,000 household income, perhaps buy two $10,000 cars.

The car buying rule is to encourage families to either be disciplined spenders are encourage families to try and make more money from a day job or at home.

My income is around a million, I owe 150k on my house. No other debt.

I just dropped 150k on a new Mercedes G wagon.

I understand your 1/10 rule, but i think as the income goes up, the 1/10 ratio can change.

I don’t feel guilty, irresponsible, or foolish for spending 150k on a car in my situation….I have no boats, no cabin, toys, no kids and and a conservative wife.

But I realize you are providing general advice…

Nice! I had a MB G500 before as well, when I was 25 years old and only making about $200,000. But mistake. But it was fun while it lasted! Bought a condo in 2003 soon after I got rid of it.

THANK YOU for writing this! I have been on my sister about this for a solid year. She has a couple of kids and keeps talking about needing a minivan. She and her husband are both teachers and make around $60k combined. I told her she needs to focus her search on something in the $6k range. She keeps trying to tell me that is unrealistic and she needs something reliable, which will cost at least $15k to $20k. I have told her she is absolutely crazy to even think about spending that much given their income. I completely agree with you that if she and her husband want a vehicle that costs that much, then they need to figure out a way to make $150k to $200k. As you said, they should easily be able to get a side hustle that adds $100k or so per year. Just drive an Uber or sell stuff on Etsy or something. It’s not THAT difficult!

It definitely was a great idea having a couple of kids while making $60K combined.

Agreed! And don’t have even get me started on that. From the time she was pregnant, I told her that she needs to look into adoption. Give those kids a chance. They are now 6 and 4 3 and I continue to plead with her to look out for her (and their) financial well-being and look into giving her kids up to a family that can afford to give them a good, financially stable life. I can tell that she doesn’t like me to bring it up, but I’m going to continue to do so as long as she and her husband are basically “working poor”.

Okay depending on the area, 60k is not poor, it’s middle class. I think trying to convince someone to give up their kids is horrible thing to do, unless they are mistreating the kids. As long as the kids have food, shelter, and supportive parents, they’re better off than they would be in foster care. I can almost promise you those kids, if given up, would not end up in a well off family, since well off families mainly want to adopt kids. If you really wants what’s best for your sister and her kids, sit her down and explain to her the math behind saving and her spending decisions, instead of harassing her to give up her own kids!

I never reply, but dude, you are completely nuts for this post. There are plenty of ways to raise kids on $60k/yr and “give them a chance.” I do not think $15k on a car at their income is not a fantastic choice, but it isn’t gonna ruin their lives. Of course she doesn’t like you bringing this up you sound like a complete nutter for telling her to give her kids up for adoption because you think $60k/yr is poverty. Seriously consider seeking treatment. I’m surprised your sister still talks to you if you have done the psychotic things your post claims.

Wow! Are you not familiar with the power and depth of the love between a parent and child? Are you really that superficial or are you just joking?

This post reads as sarcasm or satire. I think the posted is calling out the fact that this guidance only makes sense when presented with choices. Some people don’t have the luxury of a good choice vs a bad choice only bad choices with different degrees of consequence and risk.

Buying an old sh&*t box will save money but it comes with other risks – like that of safety. One needs to weigh the likelihood of occurrence against the impact of the risk.

I really like Financial Samurai for financial rules of thumb but come on – it is not possible to buy safe reliable transportation for 3 kids for under 15k (unless your a mechanic)

That said – I WISH I could bring myself to buy a new car. I have 0 debt (mine and wife college, grad school, 2 cars and house all paid off) off) 45 years old. $1.5MM net worth. $200K cash in emergency fund. 2 kids. 50K saved so far for college.

When is it ok for me to spend $40K on a new car without the guilt?

When household income reaches $400,000+ :)

I actually just wrote about saving for college in a 529 plan and for generational wealth transfer purposes.

$50K for two kids is not enough unless then are both under 5. I don’t think we parents should count on our kids being genius or being prudent enough to go to public school.

What if you’ve managed to build up that Net worth on only $150,000 a year at your age, that is really well done. And I would say splurge a little and shoot for a $25,000 a year car, not $15,000.

That said, I drove an $8000 car the depreciated to $3000 for 10 years and it was great. It was a Land Rover discovery 2 and could gave transported 4 no problem.

How much did you spend on repairs on a very unreliable rover?

And don’t say nothing because I’ll know your fucking full o shit.

Anything not Toyota is not reliable. The end.

Why so much anger? When I drove a Toyota FX16 hatchback, I was proud of it. Be proud of yours!

It’s a great stealth wealth car.

Since owning my RR since 2016, I’ve had to replace the big fan in front of my engine. It stopped worked in 2019. Just out of warranty so the cost was $675 I believe. Replaced a fuel sensor recently as well. That was $300.

Not bad.

You are the one that needs help, not your sister. You clearly don’t understand the bond between parent and child. If they want a reliable ride, so be it. I don’t believe anyone’s financial status is set in stone for their lifetime. For all you know, they might be making more than you in a few years, what then? And have you even considered the cost of maintaining a $6k vehicle, and all the mechanical breakdowns, not to mention the lack of safety features they would have to deal with. Cars are no longer a luxury, but rather a necessity. If they can take out a loan for a 20k vehicle, stretch it out longer for the sake of low payments now and pay it off faster when they make more money, that would be a wise choice.

I am trying to understand where they teach? Do they both have a full time assignment? $60K combined seems to be very low and unless they teach at some rural private school, most teachers in any public school make more than $30K. As far as the minivan is concerned, it is better to spend a little more and get a good van that will last a decade instead of buying a car that is going to give trouble few years down the road. I don’t consider $10K a lot for a minivan regardless of income. It’s 2021, not 1990

So basically by the logic of this ‘1%er mentality’ article, the majority of Americans can only afford very high mileage used clunkers and my experience with older clunkers is that there is hidden cost of both time and money that goes beyond just the face value sale price. Paying someone to fix your car adds up real fast. Then, the after effect would be that no dealerships will be able to sell any new vehicles and only the 5% of top wage earners will have dope rides while everyone else ride bicycles around. Way to keep the bar unattainable, but then that is the end goal of capitalism, the few get it all in the end.

Yes, the amount of money people spend on not just cars but *options* on their cars is completely f’ing insane. I understand why. Car culture is a religion and an obsession for many men. But imagine someone adding $10k in options to their $1k phone or laptop. You’d think they were completely insane. And it doesn’t matter that it’s a more expensive base price. For a given level of income/wealth the amount you spend on unneeded options on *anything* should be relative only to your wealth not to the base price of the thing. Having said that, I know the rule is simply stated for the purposes of a lowest common denominator (i assume) but where you live makes a big difference. Since cars cost the same nationally, but houses and other costs of living don’t.

It amazes me how easy people spend $5 on Starbucks latte’s and $10 on a banana split at an ice cream parlour. If you buy a new car with the desired options and you then drive the car for the next decade, so what? For a lot of people, a dependable car is a MUST. I think this 10% cut-off is very conservative and not working for a lot of people.

Just for perspective though… I’m considering going back to school for a PHD which would in no way increase my salary and I’d only be doing it for the experience (I.e. lifelong dream). The opportunity cost will be about $300k which is MORE than my annual income and it’s purely a luxury. But if I die without it I’ll deeply regret it. Life is ultimately about experiences and minimizing regret. Finances factor INTO that but if finances become the dominant factor in your life, you’re missing the point.

Exactly! I just graduated with a PhD and I’m working on my Post Doc with an annual income of ~$55k and I just got a 2018 Equinox for $25k. I have next to no student loan debt, and I’m looking at a great career moving forward. I’m not going to buy a $5000 clunker and end up paying $5000 in repairs over the next 5 years just because of a 10% rule. My first car was a $2000 VW Passat when I was making $25000 as a graduate research assistant during my grad school days and I ended up putting almost 5k down on repairs, not to mention the sleepless nights worrying about what would break next. I had enough and financed a certified pre owned Nissan Altima for $16k that put a smile on my face every time I drove it for the next couple of years and helped me sleep better at night. A sub $10k car is not worth the hassle. Not everyone can afford to wipe off their hard earned savings on repair bills.

Also on a side note, go get the PhD! It’s really going to boost your career for the future! It’s huge future investment if you ask me

I think that in 2020, 10% of your annual income is on the way too cheap side for an entire car. For one, that leaves the average consumer in the $4,000-$7,000 range which anyone who has ever shopped used cars knows that’s the “Goldilocks Zone”, as in the supply just doesn’t exist. I can also tell you that for that price you aren’t getting anything under 100,000 miles. I can also tell you as someone who has owned many cars in that price range and mileage that your WILL have expensive fixes to handle. In fact, any car over 100k miles needs to have the timing belt, water pump, serpentine belt, pulleys, fuel filter, spark plugs, and probably struts swapped out immediately to continue operating, which adds an extra $1000 at least. I’m someone who has to drive 300 miles a week commuting. That means you’re suggesting over 15,000 miles a year on a beater car for 10 straight years. Yeah, screw that buddy, I’ll spend a couple extra thousand and get a warranted car with a few lower miles. 25% of income seems more reasonable for people who aren’t Mr.Krabs. I spent that much about 4 years ago and now I make almost twice as much so it works out well. The car still hasn’t crossed 100k and it’s still worth about 10% of my yearly income. Nothing horrible happened and my car is better than yours.

I guess the problem is your concern is about the lifespan and maintenance add up the real cost and that make sense. But once it is raised to 25% people start to talk about brand and luxury car and not most economical Japanese car. Also this rule applies to new and used car. As for used car it is possible to better off spending 25% on a Japanese car than 10% on a used Range Rover.

You obviously haven’t heard of Tesla. Cheap cost to operate, very little maintenance, and with full self driving coming it is an appreciating asset.

I’ve heard of Tesla. I’ve been an investor in the company since 2018 and am very happy. I actually know a couple people who could have invested in Tesla in 2018, but bought a Tesla instead. Ouch. They’d have over $500,000 in gains today.

Exactly. Instead, they sad and poor today. If they had only thought about how much happier and better than other they could have been if they had purchased the stock instead.

I bought a Tesla. Yes. I would have been better off financially if in invested the money paid for the Tesla, in Tesla stock. However, getting to know the car and see how awesome it was made me decide to invest in Tesla too. Not so many stock but still. So, buying the Tesla was a sound investment. After three years it is still a joy to drive and I don’t regret anything. Life is too short for that.

I bought A a tesla model X and a model S and I have never had an issue with money. It might also be that I make over 500,000$ in anual household income A year. I agree that tesla’s are amazing and I still love to drive them. my other car’s were BMW and audis but I say that tesla is way better! I saw up there the cars you should buy but I say if you can afford that car and it’s what you like there is no problem buying it! So I say tesla 100% all the way.

What if my company pays for car worth 25% of my Gross annual income , and, every 4 years I am entitled for new car ? Company pays for insurance also every year.

If I don’t buy the car then amount of car is paid to me in 48 installments, after 30% tax deduction.

Will this 10% Rule will have relaxation to 25 % ?

Why are there so many replies here looking to cheat. I remember in school where teachers would discourage cheating in an exam by say, “If you cheat you only fool yourself.” That didn’t necessarily seem to be the case though.

But this is like dieting: cheating will only postpone the goal of becoming independently wealthy, and being able to retire early if desired. You can spend it now, or save and invest and have much more later.

Putting some numbers on this: we’ll assume an income of $100K. The company will pay $25K toward the cost of a car over 4-years. And I’m not really clear what Dinkar was saying, so I’m going to assume it means that he can opt to get cash of $6,250 per year, plus insurance ($750) and buy whatever car he wants, or use a bus or bike. So Dinkar’s income for the purpose of this column is $107K, and therefore he can afford a car valued at $10.7K, which he should drive for as long as he can.

So the rule gets relaxed from 10% to 10.7%!

(Note, this really all goes out of the window in the face of the pandemic, and if there is a real societal and cultural shift in how we approach work and heading to the daily office, we may change our approach and fully be on board with your 10% rule if cars become kind of useless and collect dust in our garages).

In the old days before 2020, we treated our cars almost like a sanctuary to how we treat our home, with respect and care, as it’s a place where we spend at minimum one hour a day, and at *least* 8 hours a week in. That’s around 400 hours a year in our vehicles at the very lowest range, without factoring road trips or longer drives for site visits and other business needs. I really don’t think someone making 200k a year should be schlepping it in a 10k car (if a family of two vehicles to get around) under your guidelines.

Where I live, browsing on Autotrader, that’s a really low bar unless you love working on vehicles or are best friends with a mechanic. You’re getting maybe a beat up 7 year old Corolla, a 10 year old RAV4 or 8 year old Nissan Rogue. *Generally* speaking you do not want to keep a vehicle much beyond 15 years of its life, so in the best case scenario, someone would own a 2013 Corolla and a 2012 Rogue (which by the way is way too small for a family of four, especially with car seats), in 2020! For a couple that makes *200K* a year! Frankly I think that is ridiculous and selling yourself short unless you live within minutes to rapid transit and can easily get around without a vehicle. Maybe applies if you’re in downtown Manhattan with a 5k mortgage I suppose, or right in the heart of San Francisco.

Spend 8 hours in a 2018 Acura and spend 8 hours in a 2012 Nissan and you can decide for yourself if it’s worth it, but to me it’s a no-brainer if it doesn’t significantly impact the rest of my life and my monetary allocation. The comfort, enjoyment and smile on my face – and I’m not a gearhead or a mechanic – is well worth buying a few less electronics or a marginally smaller home in my life. I’ve owned 20 year old Toyotas and have owned a 1 year old Lexus and it’s a complete world of difference when commuting.

I think a 25% rule is much more sensible and practical, and aligns better with most life stages if you have superb financial sense and management abilities. A family pulling in 120k can pick up 30k worth of car, maybe a single newish mid tier SUV like a RAV4, or CRV and a used Civic. Totally makes sense, is reasonable, fits their incomes compared to the rest of the country. 200k income – 50k of car, can go up to an almost new Honda Pilot and a lightly used Acura TLX. Again, very reasonable, great vehicles. No way this family should be driving 10 year old Corollas if they care at all about comfort and where they got to in life!

300K and you should be totally fine getting a brand new BMW 3 series and a Nissan Murano or used Lexus RX. And anyone who lives in a household with an income of 500k can pretty much own whatever Tesla, Range Rover and Jaguar models suit their fancy in their garage honestly unless they’re horrible with their money.