Let's look at the best alternative to peer-to-peer lending. P2P lending ranks last in my best passive income rankings. Therefore, it's best to look for better investments.

Since first writing about my plans to invest more in P2P through LendingClub.com, I've been having a difficult time mobilizing a sizable amount of assets to make a difference in my passive income stream portfolio.

When I say sizable, I mean more than $50,000. The main reason is that I'm just not absolutely comfortable making loans to strangers, no matter how good their credit ratings.

I realize if I invest in over 100 of the highest rated loans, the chances are high that I will be able to earn at least 5% vs. the 7-8% advertised through P2P. But there's something about my desire to invest my money to help someone I personally know that keeps most of my money away from P2P.

The best reason to borrow via P2P is to consolidate your debt into a lower interest rate P2P loan. I also have a soft spot for lending people money over Prosper to pay off medical bills.

Accidents happen all the time, and they are usually not the victim's fault. Every single other reason to borrow money over Prosper does not gel with my lending standards, even if the interest rate is higher.

(Read: The Main Reasons To Borrow Through Peer-To-Peer Lending)

So I'm faced with the dilemma of continuously lending money to strangers at a 5-10% interest rate to consolidate their debts or lend money to a friend who started a hedge fund and is looking to build his assets under management. I'd like for you to weigh in on this decision because $150,000 is at stake.

An Alternative To Peer-To-Peer Lending: Hard Money Lending

I've known my friend for the past 10 years. He was a client of mine when I worked at my last job in finance. He went to Cornell, got his MFE at Cornell, has a CFA, and his articles are published in the CFA magazine.

One of the most important aspects as a CFA Charter Holder is the adherence to the code of ethical financial conduct. Do anything shady, and you will be stripped of your CFA designation which takes three exams and three or more years to achieve.

My friend left his money management job a couple years ago to start his own EAFE focused (Europe, Austrasia, Far East) hedge fund. He's secured $1.4 million in private equity investments for working capital purposes for the next three years.

He's also looking to grow his assets under management and is willing to borrow money at a certain interest rate to reinvest the loan into his fund, essentially creating synthetic leverage. This is where I come in as I'm not quite comfortable enough to invest in his fund just yet.

In 2013, his returns were ~27%, outperforming the EAFE index by over 500 basis points. In retrospect, I should have invested in his fund at the beginning of the year when I had a chance!

There are thousands of hedge funds today, and most of them fail just like any other business. But my lending duration is only for one year at a time, and I have confidence my friend's fund will last for at least three years. (Read: How Do Hedge Funds Make So Much Money)

Don't Lend Money To Friends

Lending money to friends and family is a very delicate situation. I dislike what money can do to relationships. I believe my friend is a financially savvy investor who has integrity. At age 35, he most likely has a net worth of around $1 million dollars thanks to the various convenience stores and rental properties he owns with his wife in the Seattle area.

I assign a 3% chance of him defaulting on my loan or disappearing with my money to Mexico and a 70% chance I will be able to hunt him down and recoup my money if so. His hedge fund could fail, but he still has ample assets to pay me back if so. Despite such a low risk of default, I still have fear because of the amount of money I plan to lend him.

I absolutely HATE having money sitting in a money market fund earning less than 0.5% a year. Inflation is at least 2% a year and I don't want to fall behind. Part of the reason why I've kept the cash in my bank is because I don't want to raise my salary because of the dreaded payroll tax.

If you own your company, you've got to pay the full Social Security and Medicare tax of 12.4% vs. only 6.2% if you are an employee. In case you are wondering, I have already maxed out 25% of my salary in a SEP IRA.

What I'd like to do is invest the $150,000 of my company's funds and only pay taxes on interest or dividends received. This strategy will help keep adjustable gross income low enough so I can pay the lowest marginal tax rates possible while earning a reasonable return.

The $150,000 is also part of the $100,000 I've agreed to not spend as dictated by the community's demands that any spending of such money is deemed immoral, wasteful, and extravagant.

My friend initially offered the following terms for the loan:

* 4% for $100,000 with option for multi-year lockup with 10-year bond index adjustment for 2nd and 3rd year.

* 4.5 for $200,000 with option for multi-year lockup with 10-year bond index adjustment for 2nd and 3rd year.

* 5% for $300,000 with option for multi-year lockup with 10-year bond index adjustment for 2nd and 3rd year.

* 6% for $500,000 no option for beyond a one year lock up.

With only $150,000 liquid to invest, I was stuck at the 4% option, which is OK, but not great. After several rounds of negotiating I got my friend to agree to 5% for $150,000.

I mentioned to him that I've got a wave of liquidity coming due over the next three years thanks to expiring long term CDs. These CDs have been my steady baby, with the majority of them giving off 4.1% interest a year. Unfortunately, the closest interest rate on a 7 year CD is now only 2.3%. (Read: CD Investment Alternatives)

THE BENEFITS OF LENDING TO A FRIEND VIA A PROMISSORY NOTE

My benchmark for a low-risk rate of return has been 4% since 1999. 4% is getting harder to achieve thanks to declining interest rates. The 10-year yield has rebounded to ~2.7% from a low of 1.4%, so that's good for rate seekers. However, 2.7% just doesn't seem like enough in this relatively healthy economic environment.

5% is higher than my benchmark by 1%, and 2.3% higher than the existing risk-free rate of return. In other words, I'm demanding a 2.3% risk premium over the risk-free rate to invest my money in my friend. If my friend were to apply for a loan via P2P lending, he would be rated AAA. Given I've known my friend for 10 years and have a decent idea of his net worth and character, I would rate him an AAA+.

To put things in context, a 5% return on $150,000 is an extra $625 a month or $7,500 a year in passive income. $7,500 is roughly a 7% increase in my existing passive income portfolio and inches me ever closer to the $200,000 a year passive income goal. If I had $500,000 liquid right now, I'd seriously consider lending the money to my friend for 6% to receive $30,000 a year doing nothing! Alas, I've got to wait until the CDs come due.

I've got about 22% of my net worth in CDs which I'd ideally like to mobilize in similar risk, but higher return investments. Originally I was thinking about investing $250,000 – $500,000 into P2P lending, but I just can't get over the $50,000 hump just yet due to unfamiliarity with the borrowers. I see this 5% loan as a viable alternative, even if there is huge concentration risk of investing in just one person.

THE RISKS OF LENDING TO MY FRIEND

My friend could disappear once I cut the check. I'll now no longer have $150,000 but also no longer have a friend. I can take a $150,000 hit, but it will feel like getting uppercut by Mike Tyson with a couple front teeth knocked out.

I'll feel like a fool for being so trusting and will likely go into a month long depression for wasting all the hard work I put into my online company since leaving my job in 2012. I'll also feel embarrassed given I've written this post for all of you.

But if my friend does run, he will ruin his career in finance forever at the age of 35. I will also come after him like a bat out of hell. His hedge fund currently has $15 million AUM, which will therefore produce roughly $300,000 a year in revenue to pay for office rent, salaries, and other business expenses due to a 2% management fee.

The big bucks starts coming in if he performs because he will take roughly 20% of the profits as well. It takes a 3 year track record of performance before he can get to where he wants to be.

The ideal realistic scenario is that he consistently grows assets under management and pays out 5% or more for loans over the next three to five years until he no longer needs working capital funds.

After a consistent track record, I'd also consider investing straight into his fund for what will hopefully be much greater than a 5% return. But then again, most businesses fail after year three.

To clarify, there are three types of investments:

1) Private equity / venture capital investment in his company to make equity money. You must be bullish on my friend's financial acumen, entrepreneurial skills, marketing, and execution. Here's more about about investing in venture capital.

2) To invest money in his hedge fund to make returns based on the fund's performance. You must be bullish on my friend's stock picking abilities.

3) To lend money for synthetic leverage or working capital. You must be bullish on my friend's integrity and ability to pay back the loan. This is where I'm investing. Options 1 and 2 are higher risk investments with higher returns.

Here's how I'd invest $250,000 today. The economic landscape is interesting now with high interest rates.

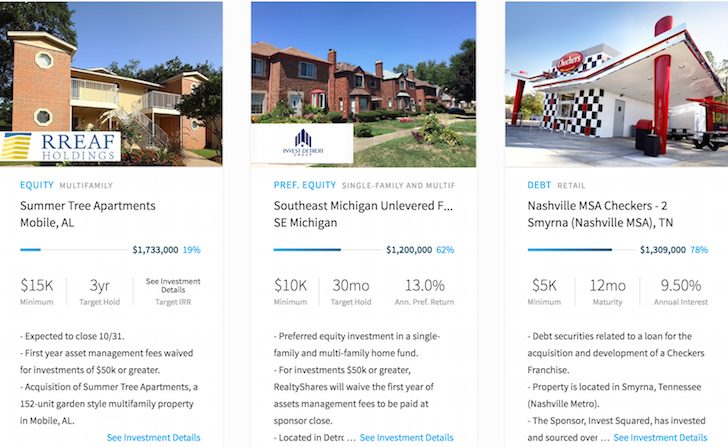

Best Alternative To Peer-to-Peer Lending: Real Estate

The best alternative to peer-to-peer lending is real estate crowdfunding. With real estate crowdfunding, you own a hard asset that inflates with inflation and produces 100% passives incom.

Take a look at Fundrise, one of the largest real estate crowdsourcing companies today founded in 2012. You can invest in higher returning deals around the country for as little as $10.

Historical returns have ranged between 8% – 13%, much higher than the average stock market return. It’s free to explore and they’ve got the best platform around.

Personally, I've invested $954,000 in real estate crowdfunding to diversify my investments and earn income 100% passively. Real estate really is the best alternative to peer-to-peer lending. Hard money lending is not for me.

Best Alternative To P2P Lending: Private Growth Companies

Finally, consider diversifying into private growth companies through an open venture capital fund. Companies are staying private for longer, as a result, more gains are accruing to private company investors. Finding the next Google or Apple before going public can be a life-changing investment.

Check out the Innovation Fund, which invests in the following five sectors:

- Artificial Intelligence & Machine Learning

- Modern Data Infrastructure

- Development Operations (DevOps)

- Financial Technology (FinTech)

- Real Estate & Property Technology (PropTech)

Roughly 35% of the Innovation Fund is invested in artificial intelligence, which I'm extremely bullish about. In 20 years, I don't want my kids wondering why I didn't invest in AI or work in AI!

The investment minimum is also only $10. Most venture capital funds have a $250,000+ minimum. You can see what the Innovation Fund is holding before deciding to invest and how much. Traditional venture capital funds require capital commitment first and then hope the general partners will find great investments.

About the Author:

Sam began investing his own money ever since he first opened a Charles Schwab brokerage account online in 1995. Sam loved investing so much that he decided to make a career out of investing by spending the next 13 years after college on Wall Street. During this time, Sam received his MBA from UC Berkeley with a focus on finance and real estate. He also became Series 7 and Series 63 registered.

In 2012, Sam was able to retire at the age of 35 largely due to his investments that now generate over six figures a year in passive income. Sam now spends his time playing tennis, spending time with family, and writing online to help others achieve financial freedom.

Newbie here. You should invest the $150k with your friend with the caveat that he gives you 5 trade-able investment ideas that you can share with your readers!

Simple question: which do you value more – your money or his friendship?

If you value your money, take the chance, worst case you’re out some money. You have it to lose or you wouldn’t be chasing returns like this.

If you value his friendship, don’t loan him the money under any circumstances. Odds are it will ruin your friendship no matter how it turns out.

I’ve loaned large sums of money twice, one worked out, one didn’t but in both cases it soured the friendship. I won’t loan a friend money ever again, at least not anyone I care about.

Trust strangers. You won’t be emotionally involved, and it will be easier if you ever have to go after them to collect.

Not so simple answer though. I’d like to have a return on my money and a continued friendship. I don’t see why we can’t have both as this is mutually beneficial.

I would be nervous investing that much money with one friend. At least with Prosper you can spread out the amount you lend to many people.

Why can’t you just invest in munis or dividend paying stocks? Can’t you get around 5% that way? And the munis will be tax free to boot!

Let me know if you can find some 5% dividend yielding stocks and munis and I’ll have a look.

I’m afraid to lose principal with this portion of my assets.

This is really interesting. My intuition tells me to not to mix money and friendship… if any of my family or friends really need help, I gift them the money (well, in amounts much less than that though!). If I get it back, that’s great… if not, well it was a gift.

But perhaps my intuition is wrong. We’re talking about two very successful people here, so I’m guessing the rules might be different.

Right now, I’ve quit pumping money into Lending Club for a variety of reasons that I’ve recently posted about, but I’m still reinvesting there. I’m still pumping money into Prosper though, which I prefer to LC.

I think you mentioned to me at one point that I will go crazy waiting for my assets to grow… I think you’re right. It just isn’t happening fast enough! 2014 must be the year of finding even more monthly income!

Nice post Sam!

Sam, sounds like the perfect guy and the perfect deal! I only have one major concern and that is that he is a long-time friend. Money and the exchange of it, tends to dissolve friendships. Other than that, you’re good to go!

You mentioned that you are in hawaii for a few weeks and by ‘hawaii’, I assume you mean kona. I live in kona, so when we see each other in town, be sure and say ‘hello’! You can thank me for the advice then! ;)

Oahu #1! :) still here for another week.

FS – you keep saying the same thing in response over and over…..I know the character, he has a $1M net worth, invested $350k into his hedge fund, gets 2% fees, has $1.5M of working capital, will get collateral, etc.

I think your judgment is being clouded by your friendship.

1. You don’t know character, even your friends, until you see them go through a tough spell. How they handle themselves in the bad times is about the best indicator, and still nowhere near perfect.

2. His net worth can fluctate, quite a bit if it includes the $350k he put in his hedge fund, so $150k is a big deal to him…..and it is also a big deal against a $1M net worth that is likely leveraged (my guess is that his net worth is mostly personal/investment real estate with mortgages – i.e. you won’t be able to touch it). If the hedge fund fails, as you worried about given lack of track record, then the $350k, the mangement fees, the working capital all go down with it. After excluding all of that is there any net worth left.

3. 27% return on a hedge fund is not that impressive in the last year – an index investor achieved that. Rising tide raises all ships…….

4. You keep saying that you will get collateral – what does this mean to you. Collateral means having a perfected lien on a specific asset. Lending directly to him does not mean you have collateral……and if you do figure out what collateral you have then you better understand it (see #2 above).

For 5% it is not worth it and your risk return parameters are way out of whack here. First, if he had a house or rental property with equity and kept the LTV below 80% he could get a 3year home equity loan for $150k 3.5-4%. My guess is he doesn’t. Second, if professional institutional lenders will not lend him the money or will not lend it too him at the rate you will, why in the world do you think you can magage risk better.

Not that you have shared it all, but his profile in no way supports a $150k personal unsecured loan especially at 5%.

You may be satisfied with a 5% absolute return but don’t be fooled to in think that it comes anywhere close to an acceptable “risk adjusted” return.

“15k short term debt to be paid off next month. I will be first in line”

– Sorry I may have read that wrong in terms of you would be getting 15K right after the other short term debt is going to be paid off…meaning he is paying down debt 15K at a time, so that’s why I asked if he is paying 15K off in 30 or 60 days why not borrow less from you.

Here in Texas they don’t allow most of the P2P lending because the regulation has fallen behind the times. I’m hoping they get it open soon because I would be very interested in investing in P2P to further diversify my portfolio.

What I find so interesting is that people love to give advice on how someone else should spend money. I’m convinced that all of the advice comes from a truly good place but how relevant is the advice? I’m not sure how many of your readers are in the same financial situation as you are. Views are highly varied and skewed to their own situation. For example your article about spending 100k. The vast majority of people said not to spend it of such frivolous things. My view is if it makes you happy and you can afford it do it. Tomorrow you may not be around to enjoy your hard work but I digress…

In regards to this article and investing money NOTHING and I mean NOTHING is a guarantee in investing. That is reflected in the return you get etc BUT the fact of the matter is that you have to take a risk to build wealth. One of the hardest lessons that I have learned is that you can’t live another person’s life. They make their own choices. Sam is an intelligent person and I have no doubt he will make the right choice whatever it is. It will be right for him. I only caution him to not put a huge amount of weight on the opinions on his online readers. I’m all for discussion and it’s a fun exercise but to lead a life dictated by others is not something that I would find enjoyable.

Sam I’m sure you understand what I’m saying.

I do and I appreciate it.

I like to be thorough and I often find great nuggets of wisdom from the readership community. For example, one email subscriber replied, “What if he dies?” Never thought of that! Contingencies will now be set in place for such an event.

I have an upcoming post entitled, “If you want greater returns why aren’t you willing to take more risk?” Seems logical no?

Given my own history, I would never, ever mix money and friends/family again. 15 years ago, I would have sworn my family would never screw me over. Then I cosigned a $25,000 private student loan for my younger sister, which my Mom agreed to back, should anything happen. Long story short, sister hid the default, Mom got seriously ill, and by the time I knew what was going on, I was on the hook for $42,000. During the financial meltdown. Just after quitting my job. It destroyed me. Several years later, I let my older sister add a line on my cell phone plan, with the idea we’d both save money by splitting the cost. Yeah, that idea cost me over $1,000. To say it puts a strain on relationships when things go bad, or the unexpected happens, is an understatement!

Not everyone will screw you over. Just walk into it with the idea that anything might happen. You never really know if someone will screw you over until they actually do. Of course, like you said, losing the money wouldn’t destroy you, it would just take a few years to make back. That makes a big difference.

Oh my…. sorry to hear about this Cindy!

I don’t get it though.. is your sister just refusing to pay you back the money you lent her for her tuition? Even a slow repayment plan would do no? I don’t get how she wouldn’t split the cell phone plan either, or keep to a budget.

Does she lack guilt, discipline, integrity or all three? I will literally chop off my hand before I ever not pay someone back!

I would definitely say the younger sister lacks all three. She’s taken the attitude of “It’s not my fault you didn’t know better”, and has never made any effort to do anything. It took several years, but eventually my Mom got better, and was able to make things right by me. She lost a kidney and a half to tumors, so I really don’t blame her for what happened. She holds out hope that my sister will someday pay her back, but it’s unlikely to ever happen. If you had told me when she was 20 what she would be like at 31, I would have said you were insane. That definitely was NOT the person I knew.

My older sister made several promises about paying me back for the phone plan, then eventually decided to pretend it never happened. For the sake of relationships, I’ve decided to let things go. I’m working on the forgiving (or at least pretending!), but I’ll never be able to forget.

Seems so wrong and so sad.

Yeah, for the sake of relationships id just forget about the money and never help her financially again unless it’s a life or death situation. Just say you are still trying to make back the money you lost lending to her if she asks again.

I don’t think it’s reasonable, A.) For him to ask and B.) For you to entertain, certainly not @ 5%??!! That’s crazy man, its a huge risk you might as well get some upside, say 15% or an equity stake, 4-5% is an insult where I come from. How do you know he has $15MM under management? All I know is every person on American Greed, who gets taken, says the same thing “But he seemed so trustworthy”

Nobody really knows everything. Lending and investing always has a degree of risk. We don’t know that Apple has over $100 billion in cash, but we believe so b/c that’s what the CEO and CFO have told us.

I would be more worried if he was offering 10% instead of a more reasonable 5%.

I’ve been interested in loaning to the P2P industry because it’s a better return than a savings account (though not necessarily better or less riskier than stocks or mutual funds.) However, I’m still not sure about it. As for lending money to friends, most of the time my response would be “do so at your own risk and the risk of that friendship.” However, your friend seems like he has plenty of assests, a strong business sense, and the abilty to pay it back. But…are you okay with not getting your money back in case his business/investment fails? I think that would be the only way I’d lend the money, being OKAY with the possibility I wouldn’t get the money back, even if it is a slim possibility.

You speak quite a bit about his character, yet very little about the business case of the hedge fund’s chance of being successful. It’s nothing personal, just business. Unless the hedge fund offers something unique (which I doubt it does), I’d pass.

Because it is a loan, I focus mostly in character. If it was a direct investment in his business then is emphasize business analysis. If it was an investment in his fund, if emphasize his financial track record and acumen etc.

Do you have the details of how much he plans on investing into the fund in total of his personal assets? What strategy is the fund? There is a difference between raising funds for the working capital and leveraging OPM.

Of the 15mm how much is going to be his and in the event of a stock market tumble (5-10%?) and a fixed income rout as the Fed raises rates – how much does he stand to lose if his fund is down 10, 15, 20%? How much of that was leveraged and does he have the liquidity to pay all his ‘lenders’ back w/out having to reach into hard sales of personal assets?

Net worth of $1.5mm is less important than how much he has in liquid assets as you will not want to go down the path of asking him to sell his businesses, houses or cars…

@MP

Also what was his track record prior to 2013? 2013 as we all know was a very atypical year – simply buying nearly any equity market with no skill would have netted 30%. Having a small allocation to Japanese stocks, financials, could easily have produced that return.

Even though you are not invested in the fund, I would ask to look at the deck for the hedge fund. Are his returns simply exagerations (beta) of the daily/weekly/monthly return for his benchmark? If his returns are simply a function of beta, then even more reason to be weary as in a down market, his down would be even more.

This all goes back to how liquid is he really after his investments because as stated by someone else, there is a significant cost/downside associated w/ a only marginal return.

I think he’s invested $350,000 of his own money into the fund and company. If the stock market tumbles 10%, he would lose ~$35,000 and his investors would lose ~$1.35 million.

There is no FDIC insurance on investing in a HF, mutual fund, index fund, or stocks. He actually only has $15K in short term debt. The $1.4 million is private equity money for working capital and investing in his company, while the rest is invested in his fund to be managed by him. Hope that makes sense.

Is the 350 including the 150 you propose lending? Are there any other arrangements of this sort? Shoot me a note if you want to discuss more or discuss his fund relative to my beta comments – I’ve been at a startup fund that went the wrong way.

Also – Not sure where my comments went – but I had posted that you look at his returns and prior to this year’s performance. Many long only investors are able to be up 20-30-40 pct this year given the stock markets climb especially in some markets like japan. If his returns are simply exaggerations of the market gyrations, then a serious downturn would result in his losses being a multiple (1.2, 1.3, 1.5 times) of the market return. Again – goes back to how liquid he is and what is his plan to create liquidity in such an event.

I would consider asking him to map out a full personal financial plan if his fund was to be down 20%. This should be something he has already done and if he hasn’t, if approached properly, it will be something that helps him.

IMO…I would not lend to a friend (or family member). It is not worth losing them. Just give them the money or go invest it elsewhere. Your relationship is likely to change during this payback period, even if all goes as expected.

Personally, I avoid these kinds of things because it can create problems.

If the choice is between lending to your friend or P2P, I would lend to the friend. I agree with Sam on the P2P. Not comfortable lending to those that I don’t know and are unregulated. As far as lending to the friend – what about staging the funds whereby, for example, you provide him $50K every 6 months such that you can get a feel for how things are progressing without putting the full $150K at risk from day 1? Just a thought.

Legging in is probably the wiser way. It all comes down to size as he’s already secured $1.4 mil in private equity money. He would rather I invest in the fund directly to have my money managed. I’m thinking maybe I will. But he doesn’t mind paying 5% and reinvesting the money into his fund bc he believes he will beat 5%. That’s money in his pocket.

How is the loan being secured? Is he pledging some of his assets as collateral? I would definitely want some collateral and/or a personal guaranty. You mentioned he has other assets. How do you know you won’t be 2nd, 3rd, 4th in line for his other assets if he defaults? Echoing some of the comments, why is he coming to you for this? He should be able to get institutional money with his track record and qualifications. Also I don’t know much about hedge funds, but 5% sounds way too low considering the risk you are taking on.

Bottom line, I would never do this. I have lent money to friends in the past and gotten burned. The small monetary upside is not even close to the disastrous emotional and financial consequences this could have.

Yes, will pledge collateral. 15k short term debt to be paid off next month. I will be first in line. Lending direct to him not his LLC.

Then why not borrow 135K?

Not sure I understand. How do you know how much he needs to borrow? He offered 6% for $500,000+.

Honestly, for me, it would probably depend on the friend, what they need the funds for, and how much (both $$ and as a % of my net worth). In almost all cases, I would probably turn them down, due to my personal risk preferences.

Though, I am curious where you would fall in the debt hierarchy, as it sounds like he also has $1.5 million of other debt related to this venture. Do the others have personal guarantees? As a PG would be one of my must haves for such a venture (preferably from signed by both him and his wife). Though it does sound like if he defaults it could destroy him professionally (assuming that you took that route and go after him), due to the loss of the designation.

How long would you do the note for? As it seems like you are also interested in investing in his fund, have you considered crafting some sort of unique security with some equity bumper?

Sorry, the LLC has $1.4 million in private equity money locked up for 3 years to fund working capital. This is a riskier investment for these investors as the fund might never take off. His fund only had 15k in ST debt and I’m lending to him as a person not the LLC.

Any way you could get some security for your loan? It sounds like your friend is a stand up guy and trustworthy. He sounds like a good credit risk generally speaking.

My concern would be stepping into the front of the line should he ever end up in bankruptcy. This may be through no fault of his own. For example, another 2008-2009 market crash hits us, his fund is caught in a tough spot and he ends up losing all his investors’ money and facing personal lawsuits (breach of fiduciary duty or some other baseless allegations). Having a secured interest in houses, cars, or businesses might at least limit your downside potential if things go south.

And if he really wants the money and knows he’ll be able to pay it back, he shouldn’t mind pledging his assets to make good on his promise.

Otherwise, I wouldn’t be too concerned about concentration of risk if I were in your shoes. It sounds like $150k is around 5% or less of your net worth. Losing part or all of it isn’t exactly something that would change your daily life at all (other than that month long depression bout you’ll face in the event of a default and the 2nd month you’ll spend chasing your friend down).

Would I do it for 5% of my NW? Not unsecured for 5%. If I wanted to juice my yield, I would probably look for hard money lending with security interests for local real estate investors. I could probably get 5-6% for a 3 year balloon note with decent 70-80% LTV. Not that I’m interested in doing that for a little more yield. :)

The contract is yet to be finalized but I am certainly going to ask him to put on a collateral clause equaling $150k. I’m lending to him directly, not his LLC. He is worth more than the LLC I am presuming. The LLC can go BL but he would still be OK.

He will borrow directly from me to create synthetic leverage and reinvest my money into his fund. He has only 15k ST debt, $350k in principal in the company and $1.4 million in private equity money locked up for 3 years for working capital.

If I could get some real collateral with a perfected security interest and 5% annual with options to extend at a significant premium to the risk free 10 yr bond rate, it would certianly be tempting. Having collateral means a lot, since you’re not dependent on the full faith and credit of your friend.

It’s just that good people can do bad things when the $hit hits the fan. He might start liquidating assets at fire sale prices to raise cash to keep his hedge fund operating if he’s caught in a liquidity crunch. I think you were in IB back during the 2008-2009 crunch, so you probably have more horror stories than I do.

A perfected senior security interest would at least protect you against others if there were ever BK proceedings. Plan for the worst, hope for the best, right?

I’m curious whether you do the deal and what the terms are.

Sam, In your article you state that your friend has over a million in assets, which is one of your comfort factors on lending him the money. My questions is, why doesn’t he go to a bank and borrow on those assets. If he is AAA+ he can borrow money against those assets at 5.5%. Also, if he is not willing to put his skin in the game, why are you?

Because I don’t think he can get anything for under 6%. He’s a new business so lacks a track record. For example, I got a $50,000 unsecured line of credit from citi this summer just because they offered. But that’s it and it costs 6.25% to use and I have been a client of theirs for 12 years.

He was offering 4% and 4.5% for my levels but came up to 5% as a friend with potentially a lot more behind.

FS, a thought to share as I read this. In another life, I had some lending experience for an institution. The two points we had to consider were 1) willingness to pay (your friend clearly has that); and 2) ability to pay. Nobody who fails in business ever plans to screw over their partners, lending institutions, employees who may have left a solid worklife to join, etc. It just happens. His operating expenses are fixed, and that money is going to burn no matter what unexpected things happen in the market, with his results, his businessplan, etc.

And the justifications in the borrower’s mind will be beyond the lender, as the “Identity Trap” and “Cognitive Egocentrism” come into play. Just look at some of the responses for people who got underwater on their Real Estate investment in your prior posts, and walked away (“the bank takes the loss into account” “the bank can’t pursue me for the money” “I made a business decision” “it isn’t illegal”, etc.) This is what you will be looking at, if things corkscrew into a cornfield.

Another question you may ask him directly, is why won’t a legitimate lending institution lend him this money? Just a guess, but he will be incorporated as an LLC, his personal assets are untouchable, and if they are willing to take a chance on him at all, his rate will be ridic!

It would be fun to read about you going all Dawg The Bounty Hunter on an ex-friend, but if he goes tits-up there won’t be anything to gain. Street Justice is a fun fantasy (and great Chuck Zito reality show), but Legal Justice is how funds are recovered. You may get nothing (except stuck with your legal bill into 5-figures), or pennies on the dollar. This is an entirely different kind of risk.

CIT in Salt Lake City has a 7-yr CD paying 2.7% and a 10-yr CD paying 3.35%. So your true margin is not 5%, but 2.3%/1.65% (on which you will pay taxes). The RISK is 5%. The risk on a friendship is 100%; it is binary. And the risk that his hedge fund not only succeeds but outperforms, is yet another hard-to-quantify consideration. One last thought, for your consideration, is that I hope you do not make this lending decision into a referendum on your ability to judge character. Wishing you well, as you evaluate your options!

Damn…well said JayCreezy, a much more articulate response than mine even though I was thinking the exact same way. I’d prefer Sam buys the range rover…

You make good points as always.

He will borrow directly from me to create synthetic leverage and reinvest my money into his fund. As he has only 15k ST debt, $350k in principal in the company and $1.4 million in private equity money locked up for 3 years for working capital, I’m feeling like this is a good investment.

I am borrowing directly from him with his assets as collateral and not the LLC. As such, this is a better way for me would you agree?

I don’t think he is going to leverage up his own money to the point he has to shut down in a violent downturn. What may happen is investors just flee and he’s left with nothing much to manage and closes shop. Closing shop shuts down his operating expenses + remaining lease. There are no guarantees in investing, so it is unlikely investors will sue of he ends up losing them money, unless there is fraud which I don’t think will be the case.

I’m making a bet on his integrity, not so much on his business. The business could go BK, and he would lose the money he invested on his fund, but the majority of his assets are outside of his fund and that is where my $150k is playing.

Further thoughts mate?

Thx

@ Nbsdmp thanks for the kind words. As I read this, I can’t help but wonder how much of the $15 million AUM is synthetic leverage. This $150K will increase his AUM by just 1%, and is borrowed to attract more clients impressed by a growing AUM. And keep coming back to the idea that Carlo Ponzi’s business model was premised on synthetic leverage.

@FS, sounds like you know the borrower is who he says he is, is willing to repay, you as lender have recourse on specific verifiable assets, and the borrower has the ability to repay. So, just three more thoughts that most likely have occurred to you…

1) Any spouses must also sign, with full right of recourse and obligation to repay.

2) Don’t guess at his NW of $1mm, know it and run a credit check; if you are reluctant to ask for the same thing you require from a renter and/or he is reluctant to provide, you know what to do.

3) if you do the deal, scrub this post of anything you wouldn’t want read back to you in deposition or court, or remove it altogether until the loan is concluded.

Keeping good thoughts for you as you make your decision!

Jay as usually is making some great points. For you it seems like a pretty good deal (although I have a diff idea below) but I really just don’t get why he is doing it. As Jay points out it is 150K into a bucket of 15mil…really isn’t that much. Also as we hit year end and he is up 27% is he taking the standardish 2/20 payout? If so, it seems like he should have PLENTY to roll back into the firm. Seems like he could just refi one of his buildings for a 30 year amortized so payments are next to nothing .

As for another idea (not saying he’d go for it) why not discuss a loan/option deal. Almost like a stock option where at anytime you can decide to forgive principal for money in the fund? He gets his money, you get your 4% floor and unlimited upside should the fund skyrocket.

Nope, no way, not a chance. Maybe I missed some of the details, but why would a guy with a $1M net worth need a loan from you (or anybody else for that matter) for $150k? This wreaks of the guy trying to act/appear bigger or more successful than he really is. What is he using the money for? What are the terms of the loan? Is he giving you a PG backed by hard assets (some of these items might sway my vote btw)? This has a high probability that it will complicate the friendship, and a low probability that it will move the needle in your life from an investment standpoint. My suggestion is if you really believe in this guy, invest the $150k to make the 27% return you believe he is capable of repeating. It is my opinion that a “loan” to friends or family should be considered in your mind a “gift”…with full understanding you may never see it returned and you are 100% ok with that. I’ve had friends ask to borrow money, and when I start walking through the reasons, it is obvious the reasons they need the money are either foolish or their inability to be patient and willing to sacrifice themselves to save the money. Tough/touchy subject for sure…my guess is that 3 years from now the interest rates are back to the point where you can get a safe 4%-5% return and you having $150k with this friend will not look very appealing.

I’m not comfortable letting his fund manage my money yet because of the one year track record only. Id like to wait for 3 years to make sure the first year is not a fluke.

What I am evaluating is not so much his investing acumen but him as a person to pay back the loan. As of now I’m much more comfortable in the latter and will result in accepting only a 5% return as a results.

I hear ya, I would say you are probably correct that this will work out but this is not where I would put my money. I’m sitting on a lot of powder right now and I’m sure a nice deal will turn up for me, until then I’m o.k. with miniscule returns. Like JayCreezy said in his post, the spread on what you are looking for to get 5% vs. a much safer bet such as a high quality municipal bond you buy directly that gives you 4% tax free is a better way to go IMO. I just don’t like the complication of friendships with money. A lot of people knew Bernie Madoff personally too and gave him a ton of money to invest…just sayin’. Keep it simple.

I wonder if Bernie Madoff has caused the lending risk premium, or money management risk premium to go up. It must have since the scandal was so great and for so long.

I think he did for sure…I think we are in a unique low interest rate bubble right now, that is why I’m not in a rush to deploy a whole bunch of capital in marginal investments. Reminds me of the Old Bull, Young Bull story I tell all the time. (even though I’m not that much older than you!)

Please tell me the story wise one.

I’d never heard of lending via a promissory note before, so thanks for the education. My state doesn’t allow P2P lending so Propser/Lending Club are out, but I wonder if such a personal loan might be allowable. Intriguing stuff, Sam.

Ask around. You might have some friends in need!

Is there any particular reason why your friend is turning to you for such a loan? Based on your description, he has all the right credentials (CFA’s are hard to get!) and is qualified enough. I’m just wondering if he’s seeking you out for the liquidity injection because he can’t obtain funding elsewhere? Or maybe you terms are just better?

I get squeamish about the idea of lending money to family or friends. The risk is more than just monetary. If you move forward, be sure to get a personal guarantee (since it sounds like you’d be lending to the hedge fund investment management company he has created) and, if possible, have him put up some of this other assets as collateral.

If this loan proves to be satisfactory and remains in good standing, then perhaps you’ll be open to similar opportunities? Before you know it, you’ll have a whole portfolio. I can see it now, the Bank of Financial Samurai will soon have a branch office near you!

In an IDEAL world, I would loan my liquidity to ALL my friends and family at a 5% rate of return if I knew there would be no complications b/c I’d rather lend money to someone I care about vs. a strange.

I’ve often thought about lending money to blogger friends in the Yakezie because they were going to P2P and paying 8%+. I’d happily accept 6% instead but I never went through with it b/c I’m scared of money messing up relationships. I could create a public ledger so everybody knows how much I’m lending to whom so that it puts pressure on my friends to pay back, but I also need to respect people’s privacy.

Social capital is HUGE nowadays.

My friend turned to me 2 years ago for advice on raising money and starting the business. I gave him lots of advice, but never invested b/c there was no track record. Now that he has operations up and a one year track record with other investors that I know, and I now have the liquidity (1.5 years ago I was leaving my firm and dumped all I had in the markets via structured notes) through diligent saving and hard work, I pinged him again for the opportunity. 5% is cheaper than he’d have to pay elsewhere, and the $150K is easier to obtain from a friend or acquaintance. I think the regulations are that you can only have a limited number of investors/clients/lenders in a fund.

I think the loan is a first step into potentially actually letting him run my money. In other words, if he makes due on his loans promises and grows his fund, he knows there is more behind.

I’ve had luck lending money to friends. It has never been that large of a sum and granted I’ve only done it 4 times. I lent a friend $5,000 at 19% interest, he declared bankruptcy but still felt obligated to pay me back outside of the court. I don’t lend sums I do not feel like losing I also usually try to get a larger return but the people I lend to are not as credit worthy as your friend.

Are you sure your friend is a friend by charging him a 19% interest? How long was the loan duration for? I would feel really bad charging someone more than 10%, and definitely more than the average credit card rate of 15%.

Perhaps the 19% interest was warranted due to him going bankrupt, but still.. that is kind of scary and I couldn’t loan more than $5K with that kind of loan either.

I didn’t come up with the interest rate, he offered. I paid off a car loan he had and that was the rate he was already paying. Its not like I told him that’s the going rate.

I think I missed somewhere what the loan is for? Also, I’m more familiar with Venture Capital and not as much with Hedge Funds – when is he launching his next fund and is he taking on partners to disperse the work? I know that’s how the balls roll with VC’s – need to keep that 2% rolling in.

Anyway – what is the loan for? For his fund? Or for him personally?

He will borrow directly from me to create synthetic leverage and reinvest my money into his fund. As he has only 15k ST debt, $350k in principal in the company and $1.4 million in private equity money locked up for 3 years for working capital, I’m feeling like this is a good investment, but am totally open to hearing the pitfalls.

I’d be curious to know how you would paper this loan up. Surely it wouldn’t be a handshake deal. Unless you’re working off of a form you feel comfortable with I suppose you’d have to factor legal fees into your return.

Promissory note with about 10 points to it on one page. He has about $1.7 million in private equity investment for working capital already. I can add requirements into the contract without cost. The loan is directly to him, not the LLC for him to reinvest into the fund eg synthetic leverage. He’d rather I just kindest directly into the fund, but believes in his ability to outperform the 5% and pocket the difference.

At the end of the day, it is just a sheet of paper with his and my signature agreeing to terms like all contracts.

To clarify, there are three types if investments:

* private equity investment into the equity growth of the fund

* investing in the fund for him to manage

* lending to the LLC or him personally for synthetic leverage

I’ll clarify in the post

Normally I’m against lending friends money. Then again, I don’t have any friends that manage $15MM in assets for a hedge fund they founded. I guess my main questions here are: who is the final obligor for the promissory note? I’d typically structure this with the management firm for the Hedge Fund (managing partner of the partnership, etc) and then have it be personally guaranteed by your friend. This is small ticket lending and it’s a pretty risky business, even though your friend is an A rated credit for that space.

My advice: just make sure that you have all the correct legal entities on the hook. Him, his company, any trust where he keeps his actual assets. I don’t want you to be left holding air at the end of this!

Neither do I! The loan is with him directly to reinvest in his fund and not a loan to his LLC.

You strike me as a very risk averse person due to your preference for fixed income securities. Based on what I have read of your blog I imagine you wouldn’t be happy with that amount of capital in one basket. Even posting this shows you are seriously on the fence.

Also, 2% management fee and he is paying interest on loans? That is a lot of hurdles to overcome. I would picture a situation where he lags the market by 5% for 2 years and see how you feel about it. If you could sleep knowing he was lagging badly, then do it.

You are right. I am risk averse b/c it’s important to protect the nut at all cost in retirement. At the same time, I have a $200K/yr passive income goal that I’m set on achieving. This $150K loan would bring me $7,500/yr closer.

A 2% management fee on assets, and 20% of profits is pretty standard in the hedge fund industry. It’s also 1% and 10% as well for many startups. To be clear, I’m NOT investing in his fund. This is a loan for working capital purposes as he scales up and builds a 3 year track record.

Good luck! I’m sure you know what you’re doing. The only problem I see is that when he default he’ll have a bunch of creditor, not just you. Everyone will try to get a portion of their money back and there’s probably not enough to go around. If business goes well, I’m sure you’ll get your money back.

My dad lends money, but he take collateral. If someone default, he can sell and get some money back. People default all the time. It might not be their fault at all.

True. He only had $15k in short term loans that will be paid off next month. Has $350k principal and will use my $150k to invest in the fund eg synthetic leverage.

You are wise to be cautious! I haven’t lent any large sums of money to friends before. Definitely get a contract if you move forward. I suppose one thing to consider is how much does he really need this money? And would a bank lend him that much (sounds like yes) and at what rate range.

I have a small Prosper account myself. I’ve stuck with the higher rated borrowers for the most part since they tend to get approved faster. A lot of the borrowers I’ve seen are indeed refinancing or doing home improvement projects.

I think he can do fine without the money. But when it comes to a hedge fund, more money to manage in the beginning to gain momentum, and attract other clients, the better.

Sam, why are you even looking at the loan details? That’s crazy! As a numbers guy you should know that unless you have some special verifiable skill at determining who will default, you should just automate it based on the historic returns of your filter. You must have tons of time in retirement to slog through all those prosper loans. Way too much effort for me.

I do have a lot more time in retirement. That happens when you don’t have to work and commute 12 hours a day.

Lending money is a very personal decision for me.

Do you think you’re adding actual value with your review (i.e. you are making more money) or do you think you’re just making yourself feel better about the loan? Not saying one is wrong, just asking.

As for me, I tagged the loans that I thought would be great and flagged the ones I thought were questionable. I wasn’t able to predict bad loans. So I stopped looking and just let the filter take care of it. My problem with P2P lending is I can’t get a decent volume given my tight filters.

Not sure what you mean. The article suggests cutting out the middle man if possible to lend directly to someone you know as an alternative to P2P. I provide a personal example to allow discussion. Would you like me to be more generic? Bc this is what I’ve been considering doing for a while now. Thx

I am interested a lot on P2P lending but I am a little afraid of the variable returns. I have to say I would feel very uncomfortable about lending to a friend as I would not the friendship to be ruined if they didn’t pay. It sounds like you trust your friend a lot and thats great. I think if you make the proper precautions, it can be great for both parties.

Sam, I must say I got very excited when I read the title of the post. Both P2P lending and other alternative means of investment are quite fascinating and desirable to me. The highlight of the post was of course, “…and a 70% chance I will be able to hunt him down and recoup my money…”

As for your situation, if you’re confident in your assessment with your friend, than I would proceed with the 5% on the $150k. Prior to putting any additional funds in this arrangement I would wait until the $150k and the interest has been earned, plus an updated review of his hedge funds financial and growth situation. Provided he is making progress, I would then feel more comfortable loaning additional funds.

It goes without saying that personal guarantees should be included in the loan contract if at all possible. Provided he does have a net worth of 1MM+ than this should provide you with some additional security should he decide to bail.

As for me, I would invest in this deal, at the 5% rate up to $150k. I would not invest in the hedge fund simultaneously as providing any loan, now, or in the future. I would not be interested in the double dip of exposure. Since my overall financial picture does not mimic yours, I will be sticking to my P2P lending investments until I have the capital to start doing private money deals.

No hesitation though due to concentration risk on one person, even though this one person would be a AAA+ rated borrower on Prosper or Lending Club?

Essentially I’m cutting out the middle man and going directly to a peer of my choosing to lend money. I guess I should have more confidence in the contract we sign up vs. the application process that a borrow goes through with one of the two P2P lenders.

I can make up the $150K in cash if he skips town, but it’s probably going to take another year to two. I can’t stop seeing clips of American Greed on CNBC where cons get retirees to fork over lots of their money for great returns only to disappear.

Someone of his credit wouldn’t waste his time with Lending Club or Prosper as capital can be found much cheaper elsewhere, as you’re demonstrating with your potential loan to him. Additionally, unlike with Lending Club or Prosper, you have a face, an identity, and the means to extract your pound of flesh should it be required. The P2P lending companies don’t offer that to investors.

Given the nature of the contract (get it reviewed by your attorney, obviously), it is absolutely cutting out the middle man while mitigating some of the risk (see above). Given your overall financial picture, the $150k isn’t pennies, but your overall portfolio risk is already relieved somewhat by your existing diversification.

And I couldn’t help but laugh at your comparison to naïve seniors on TV. While the risk cannot be discounted in this investment, you aren’t handing over your personal information to an unknown con you haven’t met before or someone you haven’t had the full opportunity to research and do your due diligence on.

Like I said before, if it were I in your situation, I would probably move forward with the investment, but hold off on additional investments with him until performance is proven.