Dear Financial Samurai,

A couple of things stood out this week. The first is that the U.S. personal saving rate is back down close to a record low, according to St. Louis FRED data. I used to think a low saving rate was pathetic and somewhat alarming. At a 3% saving rate, for example, you'd have to work 33.4 years just to cover one year of living expenses. So FIRE would be out of the question.

However, after the personal saving rate shot up to about 31-32% at the onset of COVID, and then again to about 26% during the COVID rebound, I realized Americans can save more if we WANT to. Americans are in much better financial shape than the bears think.

This second chart buttresses my point about a healthier than expected consumer. It shows a similar decline in the saving rate, but an uptick in net worth to disposable income. That uptick signals Americans are spending more and saving less because they are richer.

The wealth effect of a rising stock market is influencing consumer behavior. And if you're in a strong housing market, the positive wealth effect from real estate is even stronger. You have something tangible you can enjoy, and when a neighbor's place sells for more, the gain feels concrete.

With stocks, it's a little less real given they have no utility, which is one argument for why some people with $10+ million mostly in stocks still don't feel like it's enough. What if their portfolio drops 50%?

In my latest post, I talk about the importance of suffering now for a better life tomorrow. The thing is, this rampant bull market is rewarding the aggressive saver and investor. So if you can make some sacrifices and build that capital base, you could one day see an extraordinary run in capital gains that makes work completely unnecessary.

Just think: +23% in 2023, +22% in 2024, +16% in 2025, and +10% so far in 2026. That is a phenomenal run for the S&P 500 that has made investors a fortune. So the suffering you endured in the past may grow more and more worthwhile over time thanks to compounding.

Increased Breadth Is Positive

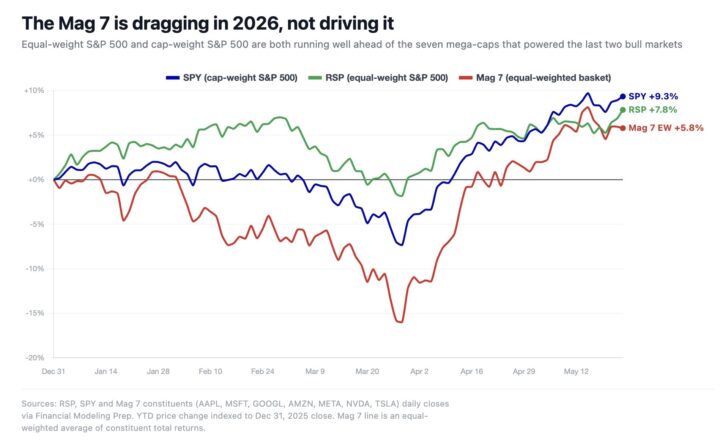

The second thing that caught my attention is this chart showing how the Mag 7 stocks are actually dragging down the S&P 500's performance this year. New leadership is generally welcome, and the chart argues for slowly declining concentration risk, which is a net positive for bulls.

I ended up buying back some Microsoft and Amazon after the dip, and more recently Google on Friday, which has been sucking wind since hitting $400. So I've inched back to an ~80/20 weighting. My hope is they mean-revert. But I'm still concerned about another correction, so I refuse to hold a 100% equity weighting any longer.

Optimizing For Peace Of Mind After FIRE

In my post on how $10 million should be more than enough to retire early, a reader left this comment on my budget.

At first I was taken aback by how much life insurance you had. I'd think if you are FIRE, you'd be leaving enough money behind. However, being FIRE suggests there are a lot of things you do for your family that would still cost a good deal of money to replace. Wondering about the level of insurance you think you need to accomplish this. Having younger kids likely factors in a lot.

This comment reminded me of the constant pushback against life insurance. The logic goes that if you are truly financially independent, you can simply self-insure.

While yes, that is true, what the critics miss is that when you are FIRE, you put a greater value on peace of mind. For example, you don't mind paying up for a MacBook because you appreciate being able to walk into the Genius Bar whenever something breaks. You no longer care so much about optimizing every line item in your budget the way folks still on the journey do.

The life insurance debate is almost as heated as the debate over whether to pay off your mortgage early. I'm not sure why. But to me, the relief of having life insurance is at least 5X more valuable than the cost of the premiums. I imagine I'll feel differently once my kids are independent adults. Right now, though, I want as little disruption for my family as possible if I were to die prematurely.

If you have young kids or anyone leaning on your income and you haven't priced a policy lately, go compare quotes before life gets in the way again. I like using Policygenius because you can shop a bunch of insurers in one place and get an apples-to-apples view, instead of letting one commissioned agent call you 14 times until you cave. It took me far less time than I expected to lock in a term policy that actually fit.

Check out: Why Every Rich Person I Know Has Life Insurance

Time For Some Positive Negativity

Finally, based on comments and emails, I guess I wasn't critical enough of people who think $10 million isn't enough to live free. One person said he was upset that every time he visits Financial Samurai, it seems it's only for the top 1%.

Well, yes. Running this newsletter and website for 17 years does take a top 1% amount of grit and consistency. But the content is geared toward everybody who wants to improve their financial situation. The vast majority of people I know are not as obsessed with their personal finances as everyone here is.

But to take the criticism to heart, my last post of the week focuses on negativity: How To Overcome Financial Despair For Good. Frankly, things have been so good for stock investors that we might forget nothing good lasts forever. We should mentally prepare for bad times again.

To your financial freedom,

Sam

If you want to read my posts ad-free for the first three to six hours after publishing, sign up for my email list. You'll get every post the moment it goes out. If someone forwarded you this newsletter, you can subscribe here. My goal is to help you achieve financial freedom sooner rather than later.