Wonder how much savings should I hav by age 35? Most financial advisors say you should have 2X your annual income saved up by age 35. In other words, if you make $75,000 a year at 35, you should have at least $150,000 in savings. I don't disagree at all. In fact, I encourage an even higher savings multiple.

At 35, I believe your net worth should be equal to 5X your annual gross income with an ultimate goal of achieving 20X your annual gross income in net worth before declaring financial independence.

Savings is just one part of your net worth. You've really got to come up with a plan to invest your savings so your money can work hard for you, so you don't eventually have to. But savings is the foundation of financial independence, so let's take a look at my guide on how much you should be saving by age.

Age 35 is very important because you should be finally earning good money after 10+-years of work experience post high school or college. With more money comes more temptation to spend. Please focus on saving as much as possible and investing in various passive income streams.

This post provides a savings guide by age.

How Much Savings Should I Have By Age 35?

The below chart shows that the more you make, the more you should save. This is my pre-tax and post-tax savings guide by 35.

I recommend everybody start off with 10% and raise their savings amount by 1% each month until it hurts. If you've ever had braces, you get the idea. Keep that savings rate constant until it no longer hurts, and start raising the rate by 1% a month again. If you make more than $200,000, certainly shoot to save more if you can. You can theoretically achieve a 35%+ savings rate in two short years with this method!

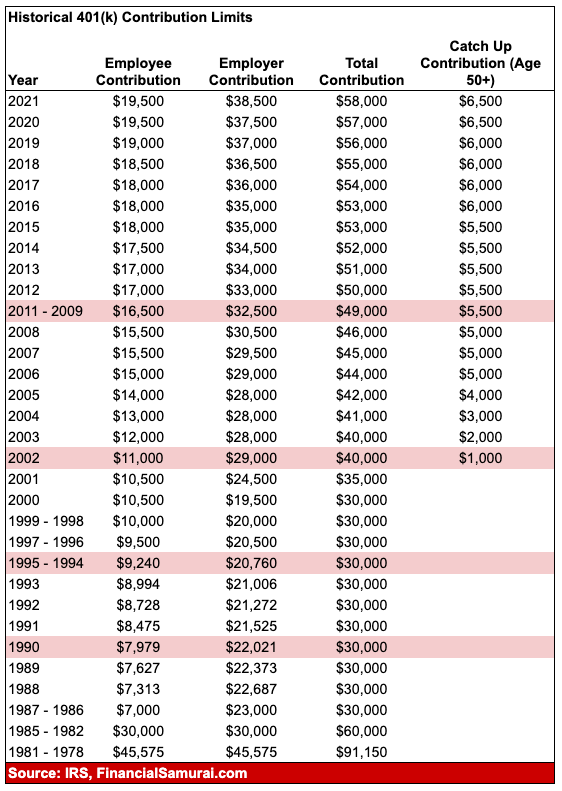

Please note that I am making 401K and IRA contributions a priority over post-tax savings. The reasons are: 1) we have a tendency to raid our post tax savings, 2) tax free growth, 3) untouchable assets in case of litigation or bankruptcy, and 4) company match. Obviously you need some post-tax savings to account for true emergencies. Ideally, my goal for everyone is to contribute as much in their pre-tax savings plans as possible and then save another 10-35% after tax.

The maximum 401k contribution for 2021 is $19,500, and will likely continue increasing by $500 increments every 2-4 years if history is any guidance.

Recommended Expense Coverage Ratio By Age 35

The below chart is an expense coverage ratio chart that follows someone along a normal path of post college graduation until the typical retirement age of 62-67. I assume a 20-35% consistent after tax savings rate for 40+ years with a 0-2% yearly increase in principal due to inflation.

The other assumption is that the saver never loses money given the FDIC insures singles for $250,000 and couples for $500,000. Once you breach those amounts, it's only logical to open up another savings account to get another $250,000-$500,000 FDIC guarantee.

By age 35, you should have between 1X – 4X of your expenses saved. Again, I recommend by age 35 having 5X your income if you want to achieve FIRE sooner. FIRE stands for Financial Independence Retire Early. Financial Samurai is the modern day pioneer of the FIRE movement having launched the site in 2009.

Expense Coverage Ratio = Savings / Annual Expenses

Note: Focus on the ratios, not the absolute dollar amount based on a $65,000 annual income. Take the expense coverage ratio and multiply by your current gross income to get an idea of how much you should have saved.

Your 20s: You're in the accumulation phase of your life. You're looking for a good job that will hopefully pay you a reasonable salary. Not everybody is going to find their dream job right away. In fact, most of you will likely switch jobs several times before settling on something more meaningful. Maybe you are in debt from student loans or a fancy car. Whatever the case, never forget to save at least 10-25% of your after tax income while working and paying off your debt. If you have the ability to save 10-25% after tax, after 401K and IRA contribution up to company match, even better.

Your Finances By Age 35 Are Crucial

Your 30s: This is you right here! You're still in the accumulation phase, but hopefully you've found what you want to do for a living. Perhaps grad school took you out of the workforce for 1-2 years, or perhaps you got married and want to stay at home. Whatever the case may be, by the time you are 31, you need to have at least one years worth of living expenses covered.

If you've saved 25% of your after tax income for four years, you will reach one year of coverage. If you saved 50% of your after tax income a year for five years, you will have reached five years of coverage and so forth. By the time you are 35, you should have 2X – 4X your expenses saved or ideally 5X your annual income.

Your 40s: You're beginning to tire of doing the same old thing. Your soul is itching to take a leap of faith. But wait, you've got dependents counting on you to bring home the bacon! What are you going to do? The fact that you've accumulated 3-10X worth of living expenses in your 40's means that you are coming ever close to being financially free. You've hopefully built up some passive income streams a long the way, and your capital accumulation of 3-10X your annual expenses is also spitting out some income.

Your 50s: You've accumulated 7-13X your annual living expenses as you can see the light at the end of the traditional retirement tunnel! After going through your mid-life crisis of buying a Porsche 911 or 100 pairs of Manolo's, you're back on track to save more than ever before! You are 100% in tune with your spending habits, therefore, you raise your savings rate by another 10% to supercharge your final lap.

Your Traditional Retirement Years

Your 60s: Congrats! You've accumulated 10-20X+ your annual living expenses and no longer have to work! Maybe your knees don't work either, but that's another matter! Your nut has grown large enough where it's providing you hundreds, if not thousands of dollars of income from interest or dividends.

Full Social Security benefits kick in at age 70 now (from 67), but that's OK, since you never expected it to be there when you retired. You're also living debt free since you no longer have a mortgage. Social Security is a bonus of an extra $1,500 a month. You're budgeting a couple thousand a month for health care as you plan to live until 100.

Your 70s and beyond: Sure, you've been spending 65-80% of your annual income every year since you started working. But now it's time to spend 90-100% of all your income to enjoy life! They say the median life expectancy is about 79 for men and 82 for women. Let's just bake in living to 100 just to be safe by taking your nut, and dividing it by 30.

For example, let's say you live off $50,000 on average a year and have accumulated 20X that = $1,000,000. Take $1,000,000 divided by 30 = $33,300. You're getting another $18,000 a year in Social Security, while the $1 million should be throwing off at least $10,000 a year in interest at 1%.

More Aggressive Net Worth Targets By Age 35

Congrats! You've now gone through the basics of how much you should save by age using annual expenses. Here is a more aggressive chart that gives you a net worth target by age based on GROSS annual income multiples.

Like I said earlier, at age 35, you should target 5X your gross annual income for your net worth.

But what about what to invest in? Not to worry, here is a post I wrote highlighting the best passive income investments for your financial future. Each investor's risk tolerance is different, so it is up to you to learn and understand what type of investment is best for you.

Favorite Passive Investment Today

My personal favorite passive income investment is real estate crowdfunding. I've invested money with Fundrise after selling my expensive SF property in 2017 for 30X annual gross rent, or $2,740,000. I basically reinvested money earning a lousy 3% a year to the heartland of America where net rental yields are closer to 10%.

With inflation picking up post pandemic by age 35, you should at least own your primary residence. This way, you are neutral real estate. I do recommend going long real estate through real estate crowdfunding or owing a publicly-traded REIT. I'm bullish on real estate over the next three years at least. I don't think the housing market will crash any time soon

Save And Save Some More

The only way to reach financial independence is if you save and learn to live within your means.

Finally, it's important to then track your investments to make sure you're comfortable with your positions. I highly recommend signing up for Personal Capital, a free online wealth management tool that let's you easily monitor your finances.

Before Personal Capital, I had to log into eight different systems to track 28 different accounts (brokerage, multiple banks, 401K, etc) to manage my finances. Now, I can just log into one place to see how my stock accounts, how my net worth is progressing, and whether my spending is within budget.

One of their best features is their 401K Fee Analyzer which is now saving me more than $1,700 in portfolio fees I had no idea I was paying. They also have a fantastic Investment Checkup feature that screens your portfolios for risk.

Finally, they came out with their incredible Retirement Planning Calculator that uses your linked accounts to run a Monte Carlo simulation to figure out your financial future. You can input various income and expense variables to see the outcomes. Definitely check to see how your finances are shaping up as it's free.

About the Author: Sam worked in investing banking for 13 years at GS and CS. He received his undergraduate degree in Economics from The College of William & Mary and got his MBA from UC Berkeley. In 2012, Sam was able to retire at the age of 34 largely due to his investments that now generate roughly $250,000 a year in passive income boosted by his investments in real estate crowdfunding. Financial Samurai was started in 2009 and is one of the most trusted personal finance sites on the web with over 1.5 million pageviews a month.