The IRS allows penalty-free withdrawals from retirement accounts after age 59 1/2 and IRA. The IRS also requires withdrawals after age 70 1/2 (these are called Required Minimum Distributions [RMDs]). There are some exceptions to these rules for 401(k)s and other ‘Qualified Plans.’ However, you only want to withdraw from a 401(k) or IRA if you are in desperate need.

Generally though, if you take a distribution from an IRA or 401k before age 59 ½, you will likely owe both federal income tax (taxed at your marginal tax rate) and a 10% penalty on the amount that you withdraw, in addition to any relevant state income tax.

If you find yourself in a situation where you do need to withdraw funds from your 401k or traditional IRA early, here are the few circumstances in which the 10% penalty might be waived.

When You Can Withdraw From Your 401(k) Or IRA Penalty-Free

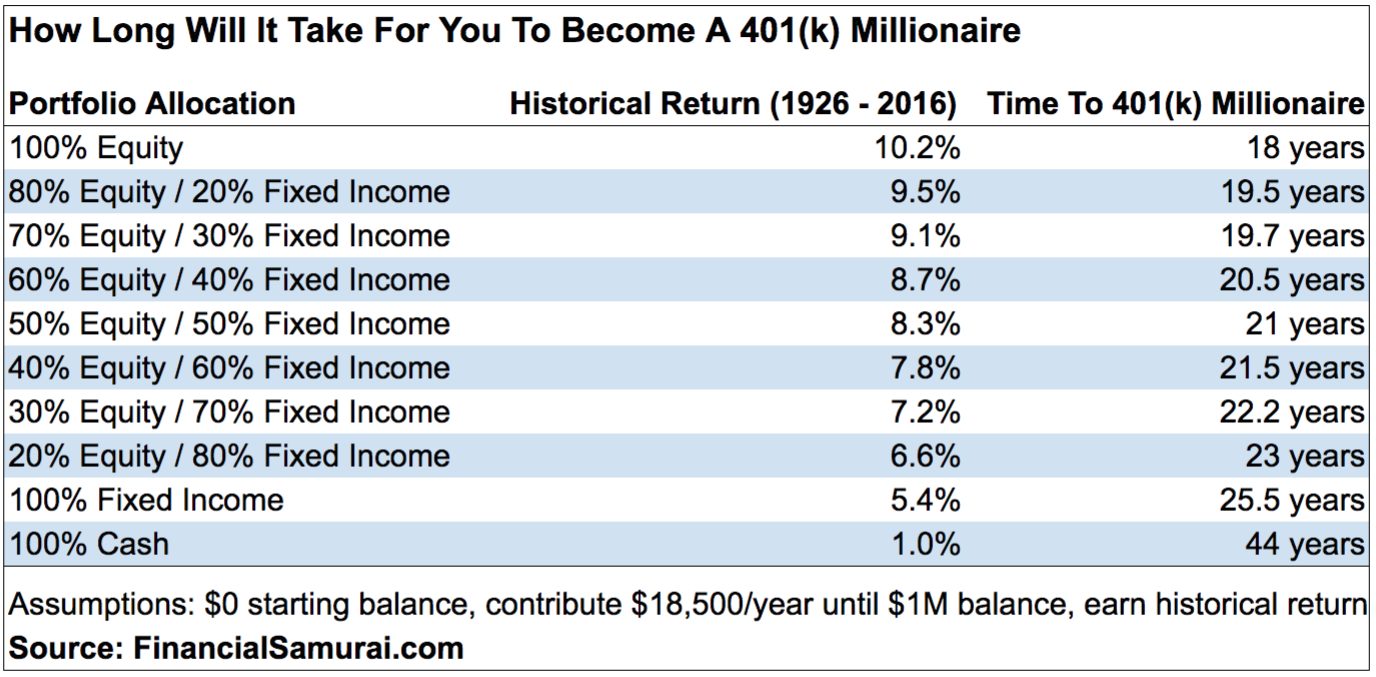

My general recommendation is to ALWAYS max out your 401(k) every year no matter what. In 10 years, you will be amazed at how much you'll accumulate. A 401(k) is one leg of the three-legged retirement stool. The other two legs are after-tax savings and personal hustle.

Let's look at the reasons when you can withdraw from your 401(k) or IRA penalty-free.

Education

You are allowed to take an IRA distribution for qualified higher education expenses, such as tuition, books, fees and supplies. This distribution is still subject to income tax, but there won’t be an additional penalty.

For instance, if you want to get an MBA and you need the money, you can decide to tap your retirement fund for tuition. The rule also allows you to apply this exception to your spouse, children or their descendants as well. Keep in mind this is for IRAs, 401ks or other Qualified Plans are subject to a different ruleset.

Specifically, some 401k plans will allow what is called a “hardship withdrawal,” with education expenses sometimes falling under this clause. It is important to note here that expenses eligible for a hardship withdrawal will vary depending on your 401k plan administrator, so make sure you ask first before withdrawing.

Some providers do not allow hardship withdrawals at all. You’ll also likely be charged the 10% fee for taking funds from your 401k early for most types of hardship withdrawals. There are a few exceptions, but education expenses are usually not one of them.

I strongly recommend not pilfering your 401(k) for an overpriced degree that is rapidly appreciating in value. The internet has made learning free. Instead, work on building specific skills. Learning how to be a good communicator will probably go much farther than whatever you learn in college.

First-Time Home Purchase

You can take up to $10,000 out of your IRA penalty-free for a first-time home purchase. If you are married, your spouse can do the same – and “first-time home” is defined pretty loosely. According to the IRS, the loan has to be for a first-time home and you must not have had ownership interest in a home for the past two years.

Just like the education exclusion, you can also tap this option for the benefit of your family. Your children, parents or other qualified relatives may receive the same $10,000 for their purchases, even if you’ve used this benefit for yourself previously or already own a home.

First-time home purchases or new builds may also be considered eligible for a “hardship withdrawal” from your 401k, but again, the 10% penalty will still likely apply here.

I do not recommend borrowing from your 401(k) or IRA to borrow money from the bank to buy your first home. You're much better off building your after-tax savings and investments for a 20% downpayment. If you don't have at least a 20% downpayment in cash plus a 10% buffer, you probably cannot afford to buy that home.

Medical Expenses Or Insurance

If you incur unreimbursed medical expenses that are greater than 10% of your adjusted gross income in that year, you are able to pay for them out of an IRA without incurring a penalty.

For a 401k withdrawal, if your unreimbursed medical expenses exceed 7.5% of your adjusted gross income for the year then the penalty will likely be waived.

A medical expense is the only legitimate reason for withdrawing early from a 401(k) or an IRA. Medical expenses are often unforeseeable, and can get extraordinarily expense without proper insurance.

Family Circumstances

If you are required by a court to provide funds to a divorced spouse, children, or dependents, the 10% penalty can be waived.

Series of Substantially Equal Payments

If none of the above exceptions fit your individual circumstances, you can begin taking distributions from your IRA or 401k without penalty at any age before 59 ½ by taking a 72t early distribution. It is named for the tax code which describes it and allows you to take a series of specified payments every year.

The amount of these payments is based on a calculation involving your current age and the size of your retirement account. Visit the IRS’ website for more ore details here.

The catch is that once you start, you have to continue taking the periodic payments for five years, or until you reach age 59 ½, whichever is longer. Also, you will not be allowed to take more or less than the calculated distribution, even if you no longer need the money. So be careful with this one!

The 401(k) Loan: Better, But Not Ideal

The IRS allows you to borrow against your 401k, provided your employer permits it. It’s important to note that not all employer plans allow loans, and they are not required to do so. If your plan does allow loans, your employer will set the terms.

The maximum loan amount permitted by the IRS is $50,000 or half of your 401k’s vested account balance, whichever is less. During the loan, you pay principle and interest to yourself at a couple points above the prime rate, which comes out of your paycheck on an after-tax basis.

Generally, the maximum term is five years, but if you use the loan as a down-payment on a principal residence, it can be as long as 15 years. Sometimes, employers will require a minimum loan amount of $1,000.

The benefits of borrowing from your 401(k) are as follows: you do not need a credit check, nothing appears on your credit report, and interest is paid to you instead of a bank or credit card company. The interest rates are usually lower than what you could receive elsewhere, and the paperwork is not complex. At least you're paying yourself back in interest.

Related: What’s the Best Way To Save And Invest For Retirement?

The Negatives Of Borrowing From Your 401(k)

If you leave your leave your employer (or are laid off), your loan is generally due right away, usually within 60 to 90 days. If you can’t pay it back, you will be assessed a penalty by the IRS.

You are also not able to borrow from an IRA if you transferred your 401k funds to an IRA. Also, taking a 401k loan depletes your retirement principal and will cost you any compounding that your borrowed funds would have received.

Related: Only A Petulant Fool Borrows From A 401(k)

IRA Rollover Bridge Loan

There is one final way to “borrow” from your 401k or IRA on a short-term basis, and that is to roll it over into a different IRA. You are allowed to do this once in a 12-month period. When you roll an account over, the money is not due into the new retirement account for 60 days. During that period, you can do whatever you want with the cash.

However, if it’s not safely deposited in an IRA when time is up, the IRS will consider it an early distribution and you will be subject to penalties in the full amount. This is a risky move and is not generally recommended, but if you want an interest-free bridge loan and are sure you can pay it back, it’s an option.

Try Not To Touch Your 401(k) Or IRA

It is best not to withdraw from your 401(k) or IRA. Leave them alone to fund your retirement.

The people who get in trouble are the ones who are always withdrawing from their 401(k) or an IRA for whatever reason they can think of. It's like constantly picking at a scab. The more you do, the slower your wound will heal.

Treat your 401(k) and IRA like a vault where money only goes in, and never comes out. Then work to build your after-tax investment accounts in order to generate passive income. You will be amazed by how much you will amass in your 401(k) after 10 years.

If you absolutely need money beyond what your insurance policies can cover, then first attack your savings account, then your after-tax investment accounts, and then your pre-tax retirement accounts. Ideally, your emergency won't be greater than your savings amount.

For 2021, the CARES Act is allowing more people to tap their 401(k) and IRA without penalty to take care of any hardships. Just be careful. Once you start withdrawing from your 401(k) or IRA, you could go down a slippery and addicting slope that may put your retirement at risk.

Related: Explaining From Real People Why The Median 401(k) Balance Is So Pathetically Low

Recommendation To Build Wealth

Sign up for Personal Capital, the web’s #1 free wealth management tool to get a better handle on your finances. In addition to better money oversight, run your investments through their award-winning Investment Checkup tool to see exactly how much you are paying in fees. I was paying $1,700 a year in 401(k) fees I had no idea I was paying. As a result, I shifted my investments to low cost index funds.

After you link all your accounts, use their Retirement Planning calculator that pulls your real data to give you as pure an estimation of your financial future as possible using Monte Carlo simulation algorithms. Definitely run your numbers to see how you’re doing. I’ve been using Personal Capital since 2012 and have seen my net worth skyrocket during this time thanks to better money management.