Dear Financial Samurai,

The market looked dicey as it sold off on nosebleed valuations. But then Fed Chair Jerome Powell spoke on Friday, strongly hinting the Fed will cut rates in September as it acknowledges increased weakness in the labor market. The market took his words positively, and here we are—back at all-time highs.

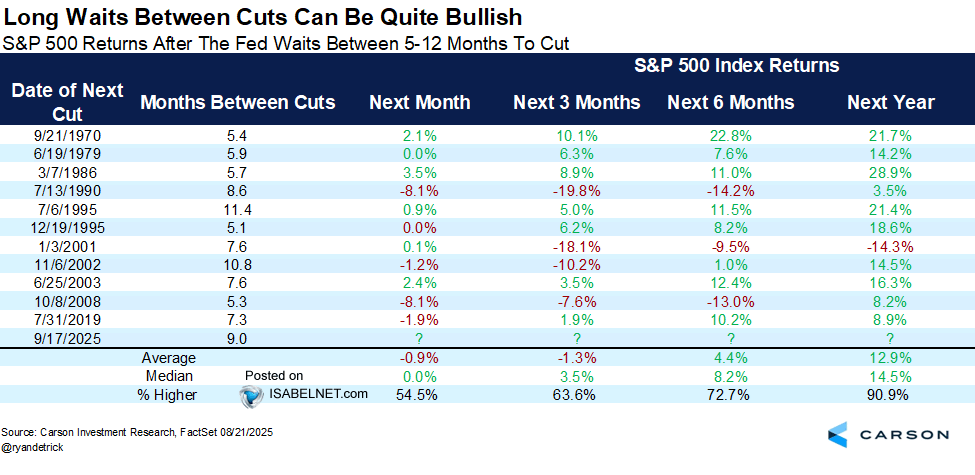

The Fed last cut rates on December 18, 2024, by 25 basis points. If they cut again in September, that would mark a nine-month gap between moves. Based on the data below, the next three months could be volatile, as the market begins to digest signs of a weakening economy—and perhaps even stagflation.

Prepare yourself for a possible 10% pullback so you don’t get shaken out. September and October are historically rough months for stocks, but 12 months later, the S&P 500 has ended up higher 91% of the time.

That FOMO Feeling Returns

Ever since coming back to San Francisco after 36 days in Honolulu, I’ve had this intense FOMO feeling I haven’t felt since 2007. Back then, every asset class was going up and everyone I knew was getting rich. I let that feeling get the better of me and bought a 2/2 vacation condo in Everline Resort, Lake Tahoe, right after a nice bonus. I thought I couldn’t lose. Of course, I ended up losing big over the next three years as the global financial crisis unfolded.

Fast forward to today, and with that same FOMO creeping in, I find myself 98%–100% in equities and growth stocks across all my tax-advantaged portfolios. Part of me wonders if I’m making the same cavalier mistake I did as a 30-year-old. The difference now is I’ve built up a larger taxable brokerage account and have steady, semi-passive income from mostly paid-off real estate.

Still, feeling FOMO is usually a bad sign. If you’re experiencing it too, check out my latest post: How To Eliminate That Intense Financial FOMO You’re Feeling. I wrote it after my fever broke, and re-reading it a couple of times helped me feel more grounded.

More Hooked On Investing Than Spending

The media loves to say Americans aren’t saving enough for retirement. We’re bombarded with consumerism, and the narrative is that we’re weak for overspending. But I think there’s a growing counterculture: people who actually enjoy being frugal and investing more than buying things they don’t need.

After all, we’ve been in a bull market for most of the period since 2009. Many of us have become so accustomed to making money that plowing more into investments feels natural. Over time, it’s easy to get addicted to the process and neglect spending on things that bring joy today.

Financial FOMO also plays a role. Nobody wants to fall too far behind those who’ve gotten extraordinarily wealthy over the past decade. But too much of anything isn’t healthy. If you know you should be spending more—especially if you’re older—perhaps this new article will help: When Investing Is More Alluring Than Spending, Fight Back.

Tax Planning For High-Income, High-Net-Worth Individuals

Finally, one of the headaches of investing in some private funds is that K-1 statements often arrive late. That means doing taxes twice—once by the April deadline, then again by October 15. That’s where my focus will be for the next month.

So when Empower, a long-time affiliate partner, reached out to share that they provide tax services for clients, I was intrigued. I hadn’t realized they did. Together, we put together a helpful post: The Most Common Tax Planning Mistakes High Earners Make.

The key takeaway: the biggest gains come from small, consistent, legal moves repeated year after year. Just like working out, eating well, or investing, the compounding effect adds up.

They’ve structured their service tiers to grow with your assets:

- At $100K+, you get help with tax-optimized investing (loss harvesting, tax location, efficiency).

- At $250K+, you also receive tailored tax planning guidance—analysis and recommendations to plug gaps in your strategy before you file.

- At $1M+, clients get direct access to a CPA at no additional cost (which normally runs $140–$400/hour).

If you’re like me, you probably already have a system in place. But I’ve found that even small tax tweaks can add up to big long-term results. That’s why I’m giving Empower’s free consultation a try next week. I’m curious to hear their perspective on my equity-heavy portfolio, and more importantly, how they’d think about the decumulation phase—spending down while still leaving a legacy.

If you’ve got $100K+ in investable assets, you can sign up for your own free, no-obligation session here. Even if you don’t make a change, a second opinion could surface opportunities you might have missed.

To Your Financial Freedom,

Sam

Disclosure: This statement is provided by Kansei Incorporated (“Promoter”), which has a referral agreement with Empower Advisory Group, LLC (“EAG”).

To expedite your journey to financial freedom, join over 60,000 others and subscribe to the free Financial Samurai newsletter. You can also get my posts in your inbox as soon as they are published by signing up here. Financial Samurai was launched in 2009 and everything is written based off firsthand experience.