After Fundrise announced it plans to list its venture product on the NYSE, I decided to do some more research on how different funds actually trade and why float matters more than most investors realize. My main goal was to get a better idea of how the fund may trade compared to its Net Asset Value (NAV).

Most investors assume that if something trades on a stock exchange, it must work the same way as everything else on that exchange. A share is a share, liquidity is liquidity, and price should roughly equal value.

That assumption is wrong.

Two funds can trade on the New York Stock Exchange, show the same ticker format, and update prices every second, yet behave completely differently in terms of pricing, volatility, and long term returns. The reason comes down to one word that rarely gets explained clearly.

Float.

To understand what is happening with Fundrise's venture capital listing and why its potential NYSE listing matters, investors need to understand how different types of funds create shares, eliminate shares, and allow investors to enter or exit.

Once you understand that plumbing, premiums and discounts to NAV stop being mysterious. They become a little more predictable.

In this educational post, I cover:

- How different fund structures actually operate in practice

- The difference between fund strategy and fund structure

- What float is and why it matters for pricing and volatility

- Why permanent capital is critical when investing in private companies

- The main reason why a non-listed open end venture fund would list on an exchange as a close end fund

This article is essential reading if you are an equity fund investor. I know it's long and unexciting, but the more you know, the better capital allocation decisions you can make.

The Three Major Fund Structures

There are three dominant fund structures most investors encounter.

- Exchange traded funds (ETF)

- Open end mutual funds

- Closed end funds

All three may hold similar assets. All three may be regulated. And all three may appear equally liquid at first glance. But only the ETF has a built in mechanism that forces price to equal value.

To summarize: The key difference between ETFs and open end mutual funds is who you trade with and when price is set. ETF investors trade with other investors throughout the day on an exchange, while open end mutual fund investors trade directly with the fund itself once per day at net asset value.

Listed closed end funds also trade between investors, but because their share count is largely fixed and there is no redemption mechanism, market prices are set purely by supply and demand and can diverge meaningfully from NAV for long periods.

Index Funds Are a Strategy, Not a Structure

Before diving into specific fund types, it is important to clear up one of the most common sources of confusion.

An index fund is not a fund structure.

It is a strategy.

An index fund simply aims to track an index such as the S&P 500, the Nasdaq 100, or a bond index. How that index exposure is delivered depends entirely on the structure chosen by the fund sponsor.

This is why index funds sometimes appear to behave very differently from one another even when they track similar assets.

Index Funds as Open End Mutual Funds

The original and still very common form of index investing is the open end mutual fund. An example would be VTSAX, the Vanguard Total Stock Market Index Fund Admiral Shares.

In this structure:

- Investors buy shares directly from the fund at NAV

- Investors redeem shares directly with the fund at NAV

- Transactions occur once per day

- There is no intraday trading

- There are no premiums or discounts

Most index funds inside retirement plans work this way. The fund can easily buy and redeem shares at NAV because its holdings are public and liquid.

When people think of index funds as stable, boring, and always priced correctly, this is usually the structure they are thinking about. The fund itself absorbs inflows and outflows and adjusts holdings accordingly.

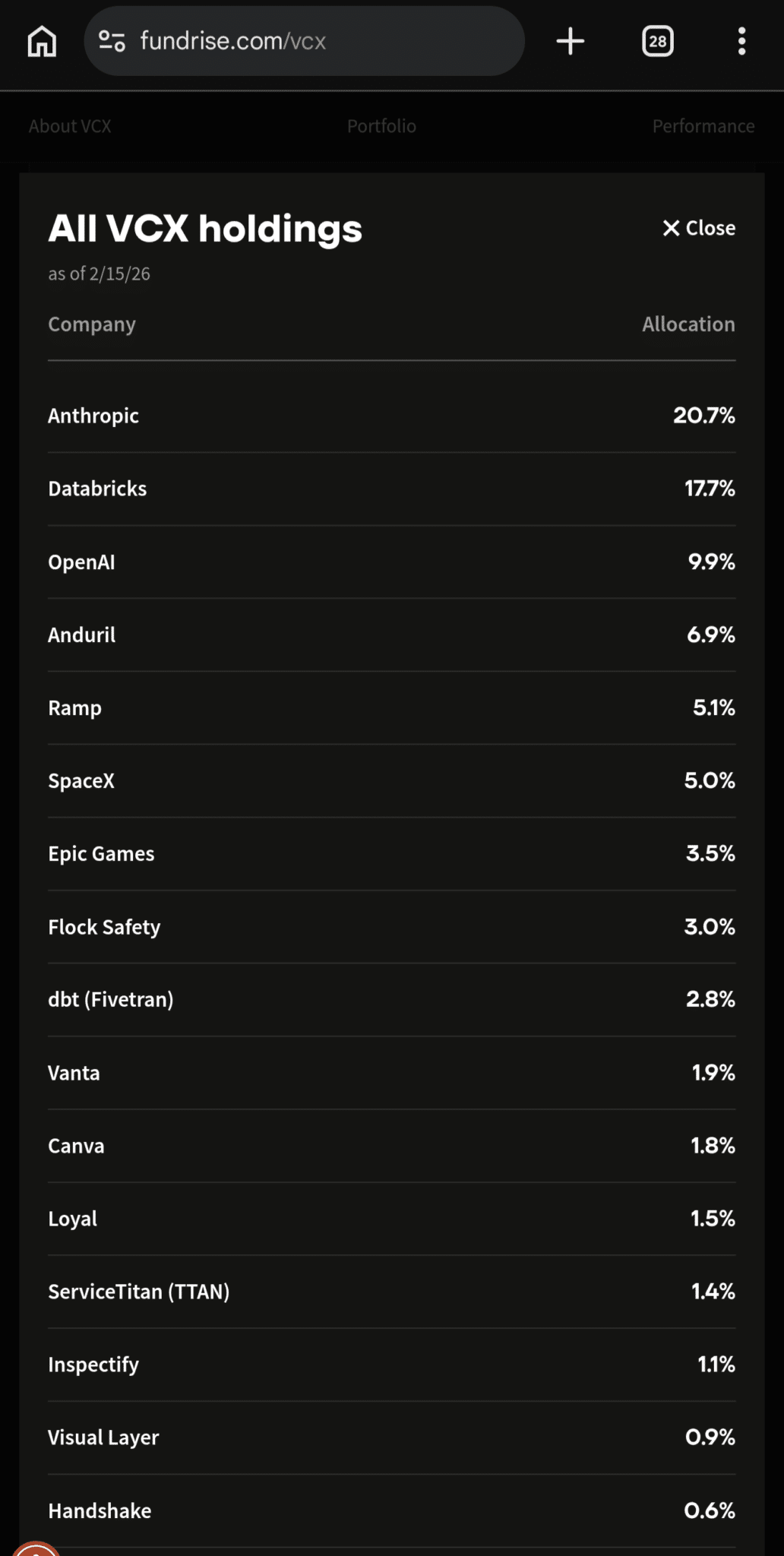

Fundrise's venture product in its previous, unlisted form was an open end fund. Investors buy shares directly from Fundrise, which issues new shares as capital comes in. When redemptions are offered, they are made by the fund itself, not other investors. Transactions occur at or near net asset value, and investors do not trade shares with one another.

But the venture product is not following any index, so it is not following an index fund strategy. It is trying to invest in the top, private growth companies, and it is largely succeeding.

Index Funds as ETFs

Many of the largest ETFs in the world are also index funds. Some of the largest include SPY, the SPDR S&P 500 ETF Trust, VOO, the Vanguard S&P 500 ETF, and IVV, iShares Core S&P 500 ETF.

These funds track an index, but unlike mutual funds, they trade all day on a stock exchange just like stocks. If you are an active trader, or day trader, you can buy and sell these ETFs intraday.

What keeps an ETF’s price very close to its net asset value is a special group of large institutions called authorized participants. These are big banks or market-making firms like Goldman Sachs, JPMorgan, Citadel, or Jane Street.

Authorized participants can exchange ETF shares directly with the fund for the underlying stocks in the index. Ordinary investors cannot do this.

ETF Has A Creation And Redemption Engine

If an ETF starts trading above the value of its underlying holdings, authorized participants can step in, deliver the underlying stocks to the fund, receive newly created ETF shares, and sell those shares in the market. This increases supply and pushes the price back down toward NAV.

If an ETF starts trading below the value of its underlying holdings, authorized participants can buy ETF shares in the market, redeem them with the fund for the underlying stocks, and sell those stocks. This reduces supply and pushes the price back up toward NAV.

Because this process is profitable and happens continuously, ETF prices almost instantaneously adjust back toward the value of what they own. Any discounts or premiums are typically arbitraged away within seconds or minutes in normal market conditions.

Remember, indexing is the strategy. The ETF is the structure.

Because ETFs combine intraday liquidity with strong price discipline, they have become the dominant way investors access index exposure outside of retirement accounts.

Liquidity, not scarcity, defines ETF behavior. Float expands and contracts automatically.

Index Funds as Closed End Funds

Less commonly, an index can be delivered through a closed end fund. Some examples include ADX, the Adams Diversified Equity Fund, KF, the Korea Fund, and MXF, the Mexico Fund. But most closed end funds are not index funds, but active funds where the manager picks individual names.

In this structure:

- The fund holds assets designed to track an index

- Shares trade only between investors

- There is no redemption mechanism

- Premiums and discounts can persist

The portfolio behaves like an index. The trading behavior does not.

This is why closed end structures are generally a poor fit for index strategies. Indexing is designed to remove friction and tracking error. Closed end funds introduce an additional layer of pricing risk that has nothing to do with index performance.

Closed End Funds and Why Price Becomes Untethered

Closed end funds are fundamentally different.

Once launched and listed, the number of shares is largely fixed. Investors do not buy from the fund and do not redeem with the fund. They trade only with each other.

If buyers are enthusiastic, price rises above net asset value (NAV). If sellers dominate, price falls below NAV.

There is no automatic force pulling price back to value (NAV).

This is not a flaw. It is a design choice.

Open end funds always trade at NAV by design, and ETFs trade near NAV because arbitrage enforces it. Closed end funds lack that enforcement, so once listed their prices are set purely by supply and demand and can diverge meaningfully from NAV.

Why Discounts Tend To Be The Default For Closed End Funds

Across the closed end fund universe, many funds trade at a discount to net asset value, often in the range of roughly 5% – 10%. This can occur even when the underlying assets are performing reasonably well. As a result, discounts are common enough to be considered a feature rather than a flaw.

The reasons are largely structural, not a judgment on management quality or asset selection. Closed end funds do not offer investors a guaranteed exit at net asset value, which means prices are set purely by market supply and demand. When demand softens, discounts can emerge and linger.

Further, the vast majority of these closed-end funds hold public equity, public debt, and private loans, like $18+ billion Pershing Square Holdings. Hence, it makes more sense these funds, with a higher fee load and a pool of publicly traded securities, would trade at a discount to NAV.

Why would investors hold the fund when they could hold these same assets directly? Fundrise Venture Capital, on the other hand, holds assets that cannot be easily owned, and are highly coveted.

In a closed end fund, management fees are charged based on net asset value, not the market price of the shares. This means investors continue paying fees on the full value of the underlying assets even when the fund trades at a discount, creating both an economic and psychological drag that can cause discounts to persist over time.

Conversely, when a fund trades at a premium, fees are still charged on NAV, which can make the fee burden feel lighter relative to market price, even though investors have paid more than NAV to own the same assets.

A Discount May Be Required As A Margin Of Safety

In addition, investors do not control the timing of asset realizations, distributions, or liquidity events. That uncertainty can lead some investors to demand a margin of safety in the form of a lower market price.

Without a built in arbitrage mechanism like with ETFs, there is nothing that forces a closed end fund’s price back to net asset value. As a result, discounts can persist for long periods of time, even if performance is solid and distributions are paid consistently.

Premiums do occur, especially when a fund offers a compelling yield, strong recent performance, or exposure to a hard to access asset class. But premiums usually require sustained enthusiasm and a perception of scarcity. Discounts, by contrast, often require nothing more than investor indifference.

What Float Is And Why It Matters

Float refers to the number of shares actually available for trading in the public market. It excludes shares that are locked up, restricted, or held by insiders who are unlikely or unable to sell in the near term.

Float matters because prices are set by supply and demand of tradable shares, not by total shares outstanding. A company or fund can have a large share count but a small float, which means relatively modest buying or selling pressure can move prices sharply.

This is why float plays such an important role during IPOs, lockup expirations, and new fund listings. As float expands through new issuance or the release of restricted shares, price behavior tends to become less volatile and more tied to fundamentals.

When an exchange such as the NYSE is evaluating a listing, they usually want to see a larger float for better price discovery.

Small Float Does Not Automatically Mean Higher Value

A small float does not mean a company or fund is undervalued or destined to rise. It simply means fewer shares are available for trading, which amplifies price movements in both directions. Scarcity increases volatility, not value.

When sentiment is positive, a small float can push prices higher as buyers compete for limited supply. But the same dynamic works in reverse. If confidence fades or a few holders decide to sell, prices can fall quickly because there are not enough natural buyers.

This is why small float assets often trade away from intrinsic value. They overshoot on optimism and undershoot on fear. Float magnifies emotion more than it reflects asset quality.

Over time, what matters is whether demand is durable and whether the float stays constrained. If additional shares are released or lockups expire, the scarcity effect can fade fast. A small float accelerates price movement, but it cannot sustain value on its own.

How Float Interacts With Closed End Fund Pricing

This is where float and fund structure intersect. Closed end funds typically have a fixed number of shares outstanding, creating a stable float. That limited float can support premiums when demand is strong, but it also allows discounts to persist when interest fades.

Because closed end funds lack a redemption mechanism, excess supply is not absorbed at net asset value. Pricing becomes driven more by investor sentiment interacting with float than by changes in underlying asset values.

In other words, closed end fund prices are shaped as much by psychology as by fundamentals. When enthusiasm rises, a fixed float magnifies upside. When indifference sets in, the same float can trap prices below net asset value for long stretches, even if performance is solid.

Related: Venture Capital Terms You Should Know: MOIC, TVPI, & More

Growth Assets and the Role of Narrative

Funds that hold high growth assets behave differently from traditional income oriented closed end funds.

Narrative matters.

When a fund offers exposure to assets that retail investors cannot otherwise access, demand can overwhelm structure, at least temporarily. This is especially true for late stage private technology and AI companies.

Growth focused closed end funds have historically traded at significant premiums during hype cycles. These premiums are real, but they are also fragile.

Once sentiment cools, the same structure that allowed the premium also allows it to disappear.

Currently, DXYZ, a closed end venture fund, still trades at a huge premium to NAV, with high volatility since its listing on March 2024. Given the long duration of DXYZ trading at a premium to NAV, it gives me more confidence Fundrise's venture product will as well, as I like the Fundrise's holdings even more.

How Float Is Created in a Closed End Fund Listing

When a private fund transitions to a publicly listed closed end structure, float does not appear automatically.

There are only three ways to create float:

- Allow existing holders to sell immediately

- Organize secondary selling by existing holders

- Issue new shares

In practice, issuing new shares is the cleanest solution.

Lockups often prevent early investors from selling. Without new shares, trading volume would be minimal and the listing would struggle to function as a real market.

Issuing new shares creates tradable supply, raises capital, and improves liquidity. If done near NAV, it does not meaningfully disadvantage existing investors.

Fundrise Venture Capital In Context

Fundrise's venture capital product sits at the intersection of several powerful forces shaping markets today. It holds private growth assets that retail investors want exposure to, it is actively managed rather than index based, and it wants to transition toward a publicly traded closed end structure.

That combination creates opportunity as well as complexity. If the fund lists with a relatively small float and a compelling narrative, it could trade at a premium in the early months, especially during any lockup period when supply is constrained and interest is high.

Over time, structure still matters. Without active tools such as buybacks, disciplined issuance, or frequent asset realizations, the natural gravitational pull for most closed end funds is toward net asset value or a modest discount. However, starting with strong demand and differentiated assets can make that path smoother than average.

This does not make the fund risky by default. It simply means it should be evaluated differently than an ETF or an open end index fund, where structure quietly does more of the work.

Why Structure Matters More Than Most Investors Think

Most investors naturally focus almost entirely on what a fund owns. Far fewer spend enough time thinking about how that fund actually trades.

Yet structure determines whether growth in net asset value reliably translates into market returns. ETFs generally deliver NAV performance, while open end mutual funds deliver NAV by definition. Closed end funds deliver NAV only if the market cooperates.

When sentiment weakens or attention shifts, price and asset value can diverge for reasons unrelated to fundamentals. Understanding this difference helps investors size positions appropriately, manage expectations, and remain patient when price action temporarily disconnects from asset quality.

In the case of Fundrise Venture, investors are not just buying exposure to AI and private innovation. They are buying into a specific trading structure with known strengths and manageable limitations.

Why A Closed End Structure Exists: Capital Permanence

It is fair to ask why a sponsor would choose a closed end structure given the tendency for discounts.

The answer is capital permanence.

Capital permanence means the manager gets to keep capital invested until they decide to sell assets, not until investors ask for their money back. It is the difference between running a long term project with committed funding and managing a checking account where withdrawals can happen at any time.

In an open end mutual fund, investors can redeem shares at net asset value whenever they want. If enough money leaves, the manager must sell assets, even if it is the worst possible time. The investor controls the timing.

ETFs are more flexible, but large investors can still force creations or redemptions that influence what the fund must buy or sell. Investor behavior still shapes portfolio decisions, especially during stress.

In a closed end fund, once capital is raised, it stays put. Investors can sell shares to someone else, but the fund itself does not have to return cash or liquidate assets. The capital remains intact.

That difference matters.

Better Match To Be Long-Term Investors In Private Companies

Because managers are not worried about withdrawals, they can invest in assets that take time to mature. Private companies, venture investments, real estate, infrastructure, and private credit all benefit from patience and stable capital. And given private companies are staying private for longer, they need more permanent capital as investors.

When markets panic, a closed end fund does not have to sell assets at depressed prices. Managers can wait for fundamentals to play out instead of reacting to investor fear. This is why closed end structures are often used for strategies that do not fit inside ETFs or open end mutual funds, which demand liquidity.

The tradeoff is straightforward. Investors give up control over when capital comes back at net asset value. You can sell your shares, but you may not like the market price.

In exchange, the investment strategy gets better odds of success because it is not forced to make bad decisions at bad times. Capital permanence is not about protecting investors from volatility. It is about protecting the investment process from suboptimal investor behavior.

Think about how many investors panic sold in 2009, 2018, March 2020, 2022, and April 2025? In a way, a closed end fund can protect an investor from themselves.

This is why Fundrise is using a closed end structure for its venture capital product. The strategy requires long duration capital and the freedom to invest without worrying about forced selling. Investors are relying on management to stay calm and strategic.

Hard To Invest In Venture Without Permanent Capital

Capital permanence also allows asset realizations to occur when conditions are favorable, not when markets are stressed. Over time, that flexibility can improve asset level outcomes, even if market prices drift around net asset value.

The structure also supports operational stability. Fees are predictable, teams can be built for the long haul, and decisions can be made based on opportunity rather than redemption risk.

Most importantly, many of the private innovation assets investors want exposure to cannot live inside an ETF or open end mutual fund. A closed end fund is often the most practical way to offer access while preserving the investment process.

Putting It All Together

VCX is not designed to behave like an ETF. It is designed to maximize asset level outcomes over time with permanent capital.

Understanding both what the fund owns and how it trades sets the right expectations. Early enthusiasm combined with a constrained float may support premiums. Over time, price will likely gravitate toward net asset value or a modest discount.

That does not make the investment good or bad. It makes it knowable.

And in investing, knowing how something works matters. When structure and psychology are understood upfront, investors are far more likely to hold through volatility and let the long term thesis play out.

Voted Yes For The NYSE Listing

After five days of deliberation, including spending over five hours writing this post and another three hours writing the other one, I've decided to vote yes on all three proposals.

Ultimately, I like the asymmetric risk/reward scenario of VCX potentially trading at a large premium to NAV compared to a potential 5% – 10% discount. A 5% – 10% discount is nothing for the benefit of liquidity and less cash drag. But potentially trading at a hefty premium even after the lockup is a bet I'm willing to make.

If the listing doesn’t materialize, I’m happy with the status quo. With a minimum investment amount of only $10, gaining exposure to Fundrise Venture Capital is easy. I will look forward to investing in future venture capital offerings if they materialize.

Along with my yes vote, I invested an additional $3,000 + $2,000 on top of my $1,000 monthly auto-investment in my personal account with over $265,000 invested. For over a year, I’ve been reinvesting a portion of my rental income into the fund. I was also pleasantly surprised to receive a $2,537.48 year-end dividend.

Update: VCX listed on Thursday, March 19, 2026, after an initial target day launch of March 9, 2026. The listing was a great success, with the shares opening at around $42 (+120%), and rising even more. For pre-listing investors, it's important to stay humble after a large investment win. Please do not spend your gains before they are liquid, as there's still a six-month lockup until investors can share their restricted shares.

Subscribe To Financial Samurai

To achieve financial freedom sooner, join 60,000+ others and sign up for my free weekly newsletter subscribe here. I started Financial Samurai in 2009 and everything written is based on first-hand experience. For background, I worked in investment banking from 1999- 2012 and gave up making max money to be free at age 34.

Fundrise is a long time sponsor of Financial Samurai because our investment philosophies are aligned. Before making any investment decisions in risk assets, please take time to read more of my posts and listen to my podcast interviews with Ben Miller, the CEO of Fundrise.

If you want more real-time thoughts on markets, real estate, the economy, and investment opportunities throughout the week, join 60,000 other subscribers and sign up for my free weekly newsletter. I have published three times a week since July 2009, when I helped kickstart the modern-day FIRE movement. Everything I write is based on firsthand experience.

thanks Sam, for the thoughts. do you think NAV for innovation fund will trade at a discount once listed?

It depends on the market conditions, the time of listing. But a normal market conditions, I think there is a 70% chance it trades at a premium for the first six months. And then once the lockup expires, fundamentally speaking, it should gravitate towards the NAV or a slight discount of 5-10% OK. Something else

However, if the underlying assets, like anthropic, continues to grow rapidly, the overall NAV should continue to increase.

Of course, there is no guarantee at all. Which is why having a proper asset allocation is important. I keep my venture capital and alternative investments to know more than 20% of my investment capital.

thanks Sam, appreciate the response. I believe existing investors like us are locked in for the first 6 months? also, what is yourr strategy to wait and buy or buy now?

What are your thoughts on how the fund will trade after listing and after the lockup?

Hi Sam, thanks for spending time and energy on this topic. Just to confirm, by continuing to invest in your “new” dollars in the fund with your contributions over the weekend – you are anticipating the collective value of these companies to keep growing in the future, correct? I ask because with the flurry of funding rounds last year, my understanding is that every dollar now invested in the fund moving forward is buying in at these current valuations – and therefore is assuming significant future growth when one could potentially argue the current valuations are pretty rich/speculative?

That’s my hope! But of course, there are no guarantees. I’m investing for at LEAST another 5 years, but more like 15-20 years for my 6-year old.

wow great stuff Sam. I know you aren’t really focusing on advantages of on over the others but one thing that has impacted me is using ETFs allow you to take advantage of intraday volatility of the markets. Not daytrading but juicing your long term returns with entries that you can’t make with public open-end funds. it can really impact even long term results. I remember last April during tariff tantrum, after a few days of selloff the market opened around 5100 sold off to 4800 intraday, then closed back where it opened at 5100ish. So if you entered a buy for an open end mutual fund when SPY say 4850, you actually purchased at the end of day price 5100. Meanwhile you could buy the ETF SPY intraday at or near the lows in real time and would mean an annual return 5-6% more than buying something like VTSAX the same day. That half day extra return represents some good annual returns. Pretty amazing. I get if you are going to dollar cost average with VTSAX frequently during the year it may pretty much average out, but thats why I like to juice my returns on major volatility days with SPY and VOO and VTI.

Yes, definitely a benefit if you can time the intraday purchase well. It’s hard to do, but certainly possible!

Wow I learned so much from this. I’ve heard of float before, but there’s no way I could have told you what it meant before reading this article. Thanks for explaining such a complicated topic in a way that makes it easy to understand!

In theory, if the fund manager grows NAV + Distributions faster than the average stock market rate of return (for assets with similar beta), then a closed end fund should trade higher than NAV and vice versa. This should be the equilibrium so that investors don’t get a free lunch of a higher than average return. If the average fund manager performs the same as the market before fees then on average after fees they’ll under-perform so the typical closed end fund will trade at a discount to NAV.

Of course, actual prices often deviate from this equilibrium for a long time! Pershing Square Holdings, which trades on the LSE, is a classic case. It has either outperformed or matched S&P 500 performance over the last few years while investing mainly in large cap US stocks but trades at a massive discount to NAV. As an investor, one of my reasons for investing was this massive discount. We’ve experienced good returns but not much closing of the discount.

Wrt Pershing Square, has the discount widened or narrowed since purchase? Because if you purchased at a discount of X, and it still trades at a discount of X, then all is good if it’s performed well or outperformed no?

Note: Pershing Square just came out with their performance versus the S&P 500 and they have underperformed over the past eight years, while Bill Achman has earned something like three to $500 million a year or something.

So it actually makes sense for the fun to trade at a large discount of NAV due to the under performance and due to the fact the fund just owns publicly traded stocks that anybody can own.

It’s exactly the same 25% discount to NAV in 2021 and now (we began buying in 2018 and got up to the current position in 2021). Yes, we have done very well with an IRR of 20% p.a. Which is why it’s crazy that it trades at such a huge discount, which hasn’t narrowed.

Good to know. Let’s see how much capital it raises and whether it lists this year. https://stocks.apple.com/AAqCTtKSYTeGwffpS-bi3Aw

“Scarcity increases volatility, not value.”

This is very true and not understanding this has created a lot of investment losses that were avoidable because of acting on a flawed thesis (looking at you, Crypto Bros and Goldbugs).

A gold standard is not the same thing as gold having an intrinsic value, as governments are required for the former and scarcity plays a role in the latter.

Thx for sharing. Long time reader of your articles. Curious – could you expand on the taxation difference between the ETF vs Mutual fund structure? ie long term capital gain thx you

Thanks for reading for so long — I really appreciate that.

On taxes, the key difference is how capital gains are realized and passed through.

ETFs are generally more tax-efficient because of the in-kind creation and redemption process. When investors sell, the ETF can hand off low-cost-basis shares to authorized participants instead of selling securities in the market. That means fewer realized capital gains, so long-term holders often pay little to no capital gains tax until they sell their own shares.

Open-end mutual funds work differently. When investors redeem, the fund may have to sell underlying holdings to raise cash. Those sales can trigger capital gains, which are distributed to all shareholders, even if you didn’t sell anything yourself. That’s why people sometimes get surprise year-end capital gains distributions in taxable accounts.

For long-term investors in taxable accounts, this structural difference alone often makes ETFs more tax-efficient. In tax-advantaged accounts like IRAs or 401(k)s, the distinction matters much less.

I sent an email to Fundrise IR last week asking if they could confirm the float of VCX and if they could confirm no at the money new share issuances for at least the first 6 months. Still waiting to hear back. Curious if anyone else had already confirmed these few points. I’m a no on the proxy vote pending their answers.

They are working on the float size with the NYSE and what should be ideal. NYSE wants an ~8% float, so that has to be created. The larger the float, the better from the NYSE’s perspective.

Interesting do you know if the float will come from new share issuances issued by Fundrise? Fundrise IR confirmed they can’t give a number on float and there wont be any restrictions on new issuances. All things being equal, hard to see how there wouldn’t be a premium shortly out of the gates with a 8% float, but we’re in the dark on the exact figure.

Trying to come up with incremental buying demand in the Innovation Fund since 12/31/24-1/31/26.

NAV was ~$190m on 12/31/24 with a share price of ~$11.37 and NAV was $524m with a ~$18.12 share price on 1/31/26. Looks like incremental demand for Innovation Fund shares over the past 13 months was $524m – ($18.12/$11.37)*$190m =221.2m or ~$17m/month in net inflows. A float of 8% would be about $42 million in tradable shares.

I suppose there’s always a fog of war in investing, but would be nice to eliminate known unknowns before voting.

I don’t think even Fundrise knows what the float will be for sure.

I hope they just issue new shares and raise more capital to invest and create a reasonable float. Investor appetite should be high, but nobody knows for sure.

I think we’re just a TINY subset of the human population who cares like crazy about personal finances, cares about AI disruption, and invests as a hedge and as a potential profit. I strongly feel most of America is not like us as I’ve been doing this since 2009 and the everyday people I speak to aren’t not personal finance enthusiasts.

I also note that they want to increase their management fees as part of any listing. Is there a valid reason for this apart from increasing their profit? If the current fund is working well for us, then why risk higher fees for an unknown outcome.

Fundrise isn’t making money after marketing and operation expenses with no carry. Raising the management fee helps them break even and earn a profit. Based on recent returns, the fee is insignificant and I don’t even notice.

One simply cannot get into these companies. If you can via tradition VC, it’s 2-3% and 20%-35% of profits. I know everybody wants free nowadays, but eventually, creators will stop providing value if they can’t turn a profit.

Good article. I would add that over time you need to track activist investors in the closed end space e.g. SABA. They sometimes drive change. Whether it is a longterm improvement or not is an open question.

Thanks for the info. Activists should be good, but their timing may be misaligned for what management is trying to do.

So who knows best? Management or investors trying to make what’s usually a quicker return?