One of the reasons I’ve been a long-time supporter and affiliate partner of Fundrise is its willingness to innovate. Since its founding in 2012, shortly after the JOBS Act opened private investments to retail investors, Fundrise has consistently looked for ways to democratize access to institutional-quality investments.

From launching diversified private real estate funds like its Heartland and Income funds, to expanding into venture capital through their venture product, Fundrise has steadily pushed into areas that were once reserved for large institutions and ultra-high-net-worth individuals.

So when I received an email from Fundrise announcing its plans to list its venture product on the New York Stock Exchange, under the ticker VCX, I was intrigued.

I tend to be old-school when it comes to investing. If something isn’t broken, I’m generally reluctant to change it. I’ve been an investor in Fundrise's venture product since 2023 and now have over $770,000 invested across three accounts. My plan is to hold for the next 5–10 years and ride the AI wave with a long-term mindset, largely with my children’s future in mind.

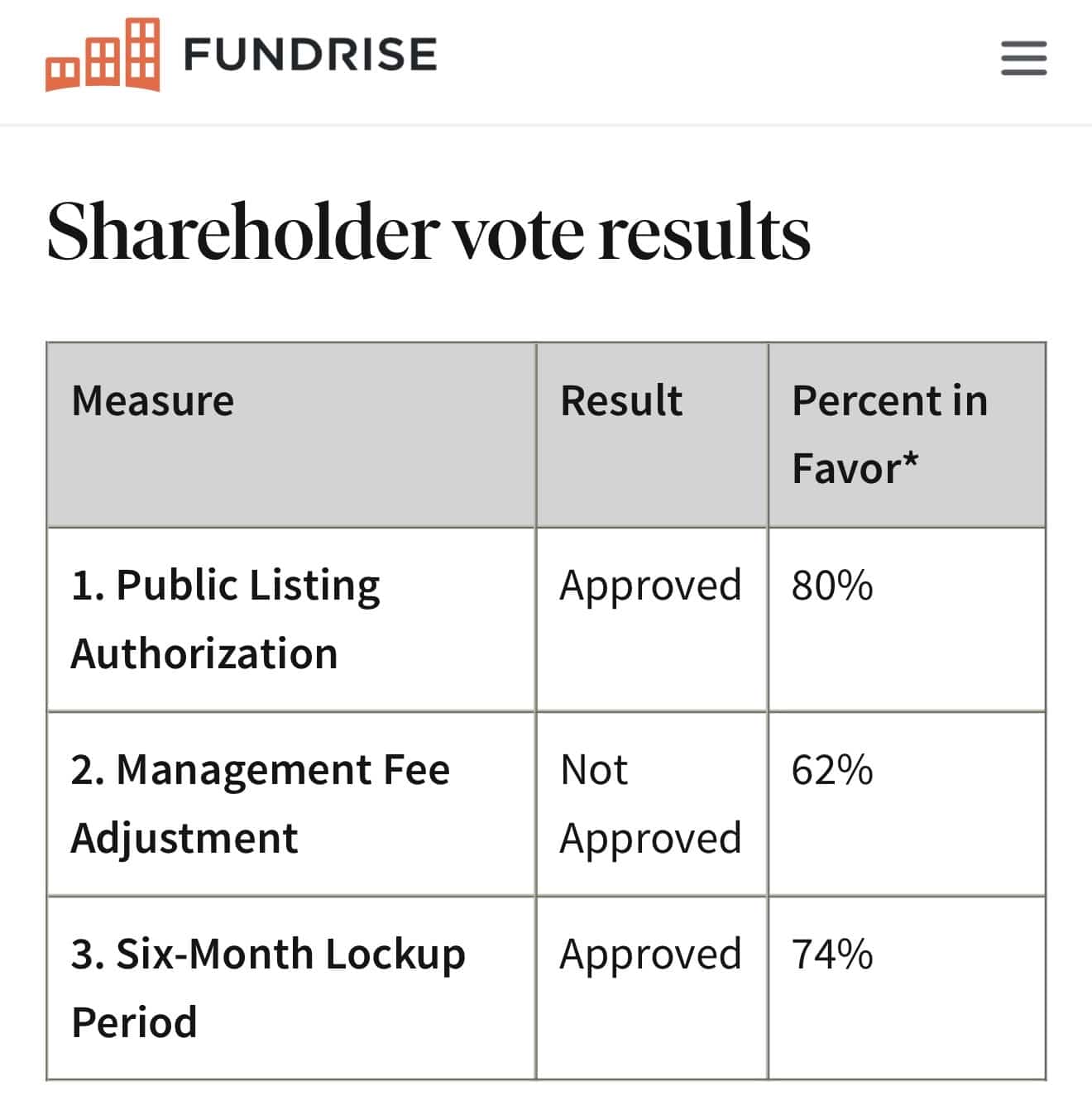

Here are my initial thoughts on the venture product listing on the NYSE. The votes are in and shareholders have approved of the listing.

Update: VCX finally began trading on March 19, 2026 after about a 10 day delay. The listing was a great success for investors and it's important to stay humble after a large investment win. Please do not spend your gains before they are liquid, as there's still a six-month lockup until investors can share their restricted shares.

This post was originally published on February 4, 2026, when Fundrise first announced it was going to list its venture product on the NYSE. I go through my thought process about what might happen. There is a six-month lockup until most shares can be sold.

The Potential For Instant Liquidity In Venture Capital

I’ve invested in traditional venture capital funds for over 15 years. That experience has conditioned me to expect zero liquidity for a long time. When I allocate capital to venture, typically up to about 20% of my investable assets, I assume I won’t see that money again for at least 10 years.

The other 80% of my portfolio provides liquidity. Stocks, bonds, and even cryptocurrencies can be sold if cash is needed or if opportunities arise. Venture capital, by contrast, is meant to be patient capital.

Fundrise already offers quarterly liquidity for its venture product, which is relatively generous by venture standards. But providing that liquidity comes at a cost, one I didn’t fully appreciate at first until I spoke to Ben Miller, CEO of Fundrise.

To meet quarterly redemption requests, roughly up to 25% of the venture product has been allocated to liquid, lower-risk assets such as money market funds and corporate bonds. These assets provide stability and liquidity, but they also dilute returns during strong markets.

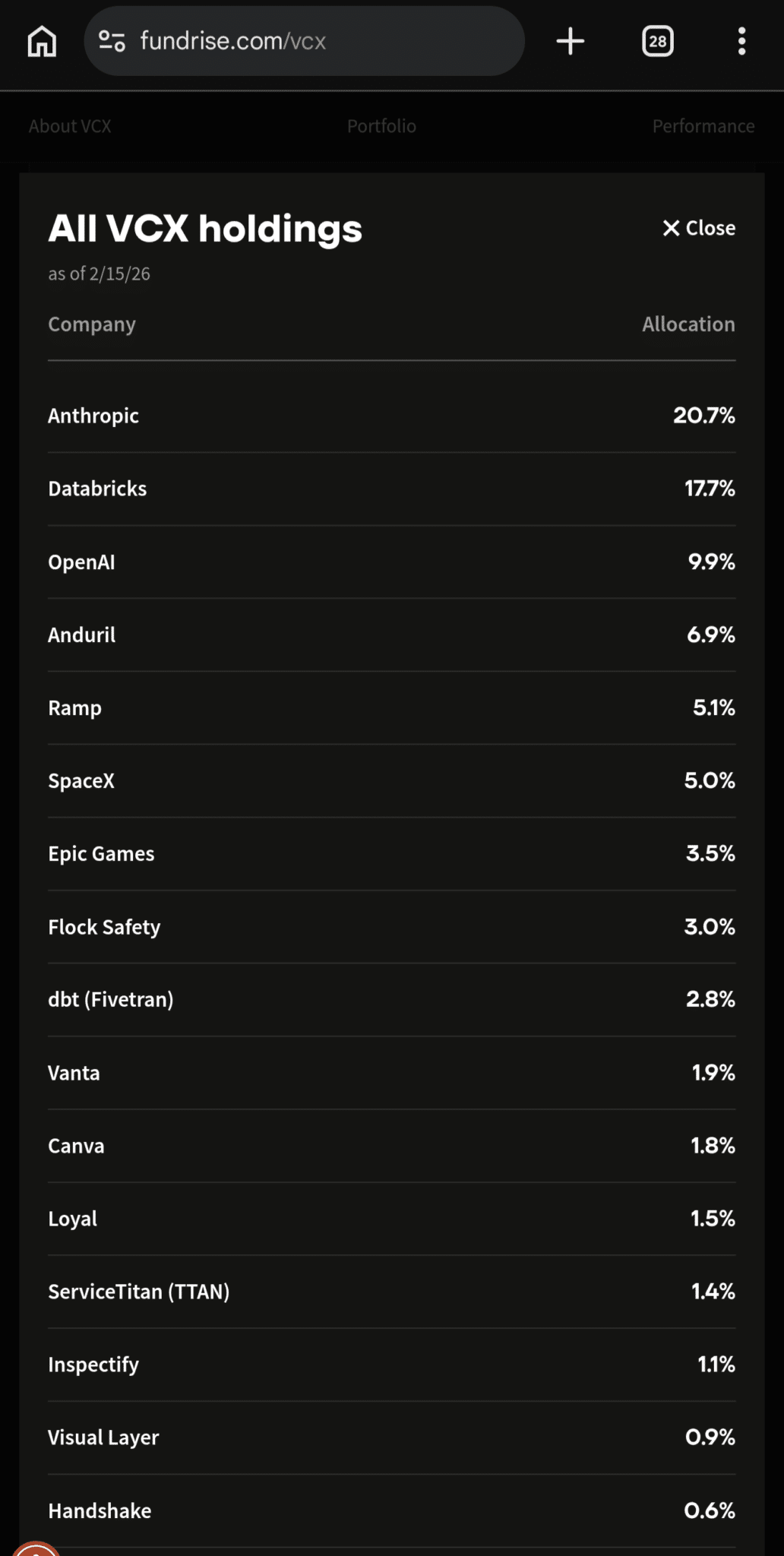

For example, in 2025, the venture product returned about 43.5%, driven largely by exceptional performance from core holdings like OpenAI, Anthropic, Anduril, and Databricks. Meanwhile, money market funds averaged roughly 4% and corporate bonds about 6%.

When 25% of a fund is earning a blended return closer to 5%, that acts as a meaningful drag during bull markets, much like holding excess cash in a rapidly rising portfolio. During strong markets, there was little redemption pressure anyway, as investors wanted to stay invested and often add more.

An NYSE Listing Offers Liquidity And A Potential Boost In Performance

This is where the potential NYSE listing becomes interesting.

If the venture product were publicly listed, the need to hold such a large percentage in low-return liquid assets could be significantly reduced. Liquidity would come from the market itself, not the fund’s balance sheet.

Based on simple back of the envelope math, if that 25% previously held in low-risk assets were instead invested alongside the rest of the portfolio, overall returns would have been close to 55%, instead of 43.5%. In other words, the 25% of the fund earning a low-risk 5% dragged down performance by ~11.5%. That is a significant cost to provide liquidity to shareholders who mostly didn't need liquidity during a bull market.

Of course, markets don’t move in straight lines. Corrections and bear markets are inevitable, especially in highly valued growth sectors like artificial intelligence. When prices fall, investors tend to follow the herd, buying near peaks and selling near troughs.

In a severe AI correction, a privately held fund offering quarterly liquidity could face redemption pressure it cannot immediately meet. That would likely require gating withdrawals, which creates frustration and operational complexity.

A publicly listed fund handles this dynamic differently. During periods of intense selling, the share price simply adjusts to reflect supply and demand. Investors must then decide whether selling at depressed prices makes sense, or whether staying invested aligns better with their long-term belief in the underlying companies.

Better Credentials for Potentially Better Investments

Fundrise has been around for 14 years and now manages over $3.5 billion in assets. While commercial real estate has faced headwinds since the Federal Reserve raised rates aggressively starting in 2022, those challenges are largely cyclical and asset-class specific rather than reputational or operational. I'm hopeful CRE has turned the corner.

Listing the venture product on the NYSE would further enhance Fundrise’s credibility and brand. Getting listed is not trivial. It requires extensive vetting by lawyers, bankers, auditors, and regulators. All this requires time and money.

In some ways, it’s like getting into a top-ranked university. It signals a higher level of scrutiny, transparency, institutional acceptance, and overall standard. As a result, investors may feel more confident about Fundrise's venture product, not more wary. With greater confidence comes greater capital, and thereby more investment opportunities.

Of course, public listings do not guarantee success. Poorly managed public funds still exist. But on balance, a NYSE listing sends a positive signal that Fundrise is serious, durable, and here for the long term.

For startups seeking capital, reputation matters. Founders evaluate investors not just on capital, but on track record, network, and ability to help businesses grow. In fact, one can argue that capital is a commodity because there's so much capital sloshing around.

Fundrise Provides More Than Just Capital

With over 380,000 investors, Fundrise has a distribution advantage that few traditional venture firms can match. Portfolio companies gain visibility, potential customers, and credibility simply by being associated with the platform.

I’ve discussed this before with Ben Miller, Fundrise’s founder and CEO, including how partnerships like the one with Ramp helped drive meaningful adoption through cross-promotion. Ramp (Fundrise holding)) mentioned to Ben it was one of the most successful campaigns they had run. Now Ramp has zoomed ahead of BREX, its closest competitor that started two years earlier, and was recently sold to Capital One.

As a Fundrise venture product investor, I obviously want the portfolio companies to succeed. I’m one example of an investor who can help amplify awareness, and there are many others who can as well across the platform.

Compare that with traditional venture firms like Sequoia. They have elite reputations and exceptional partners, but access is limited to institutions, insiders, and a small circle of founders. They also cannot instantly reach hundreds of thousands of engaged retail investors the way Fundrise can.

Fundrise is also a private company operator itself, using and testing products from its own portfolio. For startups evaluating potential investors, that combination of capital, platform, and operational insight is compelling.

Listing on the NYSE further legitimizes that proposition.

Here’s my podcast episode where I discuss the accelerating adoption of AI and the Ramp partnership with Ben Miller, CEO of Fundrise.

The X-Factor: Premium or Discount to Net Asset Value (NAV)

Before going further, it’s worth clarifying what net asset value, or NAV, actually means in this context.

NAV represents the per-share value of the fund’s underlying assets minus liabilities. In simple terms, it’s the estimated value of all the companies and assets a fund owns, divided by the number of shares outstanding. When a fund is private, investors typically transact at or very close to NAV.

Once a fund is publicly listed, however, a second force comes into play: market supply and demand for the fund’s shares.

While NAV continues to be driven by the performance and valuation of the underlying portfolio companies, the trading price of the fund can move above or below NAV depending on investor sentiment, liquidity preferences, and scarcity. This difference shows up as a premium or discount to NAV.

Historically, many closed-end funds, especially those invested in illiquid assets like real estate that’s more difficult to sell, have traded at discounts to NAV, often in the 5% to 10% range.

The reasons are usually practical rather than dramatic, ranging from liquidity preferences and valuation uncertainty to skepticism about management or the inconvenience of owning a fund instead of the assets themselves. These closed end funds also don't hold highly coveted private AI company investments either.

That said, scarcity can flip the equation.

If demand for exposure to a particular set of private companies far exceeds the available float of shares, the fund’s market price can trade meaningfully above NAV. In those cases, price movements are driven less by changes in the underlying company valuations and more by supply / demand imbalances in the public market.

This dynamic already exists in pockets of the market. Some publicly traded vehicles with concentrated exposure to hard-to-access private companies have traded at sustained premiums, sometimes well above the value of their underlying holdings.

For Fundrise's venture product, this creates an additional variable for investors. Returns would no longer be driven solely by how well the portfolio companies perform, but also by how the market prices access to those companies at a given moment in time.

In other words, the value of the underlying assets still determines NAV, but the market’s appetite for exposure determines whether investors can buy or sell shares at a discount or premium to that NAV. The harder to gain access to the portfolio companies, potentially, the higher the premium to NAV.

As a long-term investor, I assume the fund will trade roughly around NAV, possibly at a modest discount. But because the venture product owns scarce private assets and could have limited public float (perhaps only around 8%), there is also a plausible scenario where demand drives the share price to a premium, at least for periods of time.

That additional layer of supply and demand cuts both ways. It introduces volatility, but it also creates upside optionality that doesn’t exist in a purely private structure.

Example Of A Closed-end Fund Trading At A Premium To NAV: DXYZ

There is clear precedent for publicly traded funds trading at premiums to NAV. One notable example is DXYZ, or the Destiny Tech100 Inc. fund, which has traded at anywhere from a 100% to 1000% premium to its net asset value. Back in November 2025, the fund’s NAV was roughly $7 per share. Today, it is closer to around $19, but with ~40% of the fund in cash. Based on its latest $29/share trading price, DXYZ is trading at a ~55% premium to NAV.

SpaceX accounts for approximately half of DXYZ’s holdings, which offers a strong indication of just how much demand there is for hard-to-access SpaceX exposure. Investors are effectively paying a substantial premium for convenience, scarcity, and perceived long-term optionality.

As a savvy investor, it’s reasonable to look at DXYZ and ask whether something similar could happen if the venture product were to become publicly traded.

According to Fundrise's latest announcement, OpenAI, SpaceX, Anthropic, Databricks, Anduril, Ramp, and Stripe account for about 75% of the fund. Meanwhile, Anthropic has been in the news frequently in 2026 for disrupting industry after industry. OpenAI also announced on February 27, 2026, that it has raised another round of funding at a $760 billion valuation. Anduril just raised in March at double its previous round valuation as well.

These are the top private growth companies today. Personally, I’d much rather own this basket of companies than half the fund in SpaceX at a $1.25 – $1.5 trillion valuation.

One could argue that the Fundrise venture product offers a more diversified mix of private growth companies with less concentration risk than DXYZ, which I prefer. If that’s the case, it’s not unreasonable to imagine a scenario where the venture product could trade at a meaningful premium as well, especially given how difficult it is for most investors to gain exposure to these companies directly.

A Discount To NAV Could Also Appear

That said, premiums to NAV are not guaranteed and can be volatile. Investor sentiment can shift quickly, particularly during market corrections or periods of rising interest rates.

Premiums can compress just as fast as they expand, even if the underlying companies continue to perform well. Once the 6-month lockup period expires, it is rational to expect any NAV premium to disappear and a discount to emerge. It will be up to Fundrise to properly manage the float as a closed-end listed fund.

In addition, a more diversified portfolio may reduce concentration risk but can also dilute the scarcity effect that drives extreme premiums. Unlike DXYZ, where SpaceX dominates the narrative, Fundrise's venture product's broader exposure could lead the market to value it more conservatively.

All of the private companies held in the Fundrise venture product remain scarce and difficult to access, even for well-connected investors. Meanwhile, ServiceTitan, now publicly traded under the ticker TTAN, represents less than 2% of the fund, reinforcing that the portfolio remains focused on private growth opportunities rather than public market exposure.

Taken together, a premium is plausible, but it should be viewed as optional upside rather than a base-case assumption. For long-term investors, the primary driver of returns should still be the performance of the underlying companies, with any premium to NAV treated as a bonus rather than a guarantee.

Let's Make A Realistic Assumption Of NAV Potential For VCX

Let’s assume there’s a 50% chance the fund trades at a 10% discount to NAV, a 20% chance it trades at par, and a 30% chance it trades at a 50% premium (not 100% – 500% premium like DXYZ, which I wouldn't buy). Under those assumptions, the expected value of a $100,000 investment made before listing would be about $110,000.

Even with a higher probability of trading at a discount, that kind of asymmetric payoff is still the type of risk I’m comfortable taking as a long-term investor. You should play with the assumptions yourself to figure out multiple realistic scenarios.

Personally, I don’t plan to sell for at least another five years, and ideally ten. My goal is to invest until my kids graduate college in about 16 years to hedge against a potentially bleak labor market due to AI. Time and compounding are on my side. So the 6-month lockup post a successful VCX listing is not a concern.

Given the tax implications of selling, I would need a significant premium to NAV to be tempted. If I believe the fund can compound at 20% annually for five years, that’s roughly a 150% gain just by holding.

In that case, selling only makes sense at a large premium and with confidence I could redeploy the after-tax proceeds just as effectively. Otherwise, like many wealthy investors, I’d rather borrow against assets than sell them and pay taxes.

The Dream Trading Scenario

If the fund were to trade at an extreme premium, say 100%+ above NAV after the 6-month lockup, I might sell 20% of my position to lock in gains and let the remaining 80% ride. That would be a miraculous ~$770,000 appreciation on my ~$770,000 total position just through a listing. Taking some profits balances prudence with long-term conviction.

And if VCX trades at a discount to NAV, my base case scenario, I'll just hold like originally planned with the expectation the discount will narrow as visibility of VCX improves and Fundrise better manages the operations of the fund.

Before VCX lists, we'll get a glimpse at how the Robinhood Venture Fund I (RVI) trades first on March 6, 2026. The funds are similar in structure, but different in holdings. If RVI trades up, then the chances of VCX trading up as well increases and vice versa. However, I'd much rather own the companies VCX holds than RVI does, which is heavily fintech payment companies.

Unfortunately, RVI trade down 16% initially, but has clawed its way back to trade down ~6.8% as of March 13, 2026. Its listing timing was unfortunately given bombs started flying soon after. However, given Fundrise gained position over Robinhood, it wisely chose to delay its listing from the week of March 9, 2026 until a later date.

As of March 26, VCX is publicly listed to strong demand, and RVI is now trading at a 30%+ premium to NAV. So as you can see, anything can happen. Expect the unexpected as these products remain volatile.

Building Transparency, Liquidity, and a Brand

Having built Financial Samurai since 2009, I understand how difficult it is to grow a business and a brand. Sometimes momentum builds quickly. Other times you get dragged through the mud and suffer. That volatility is simply part of building something meaningful.

Fundrise’s attempt to list its venture product on the NYSE represents a step toward greater transparency, liquidity, and brand durability. It may also improve access to higher-quality deals over time, which is the main goal for both Fundrise and its investors.

The fee structure remains highly attractive. Being able to invest in private growth companies of this quality without paying a 20% carry is rare. One closed-end venture fund I invest in charges 3% management fees and 35% of profits. By comparison, Fundrise’s new 2.5% fee with no carry is compelling.

The main challenge for investors, myself included, will be staying disciplined through public listing volatility. Greater liquidity makes it easier to sell during downturns and to justify poor timing decisions with convincing narratives. I can make both a bull and bear case for almost any position I hold, having trained myself to look at both sides in an effort to avoid being blindsided.

And there will be a correction in AI private companies at some point. The real test will be whether investors can hold through volatility or even buy the dip if they believe, as I do, that AI is at least a decade-long trend.

Investing In AI For The Long-Term

Overall, I’m excited to see what happens. I ended up voting yes to all three conditions proposed after deliberating for five days. Ultimately, I like the asymmetric risk/reward scenario of VCX potentially trading at a large premium to NAV compared to a potential 5% – 10% discount.

Along with my yes vote, I invested an additional $12,000 on top of my $1,000 monthly auto-investment in my personal account with over $265,000. For over a year, I’ve been reinvesting a portion of my rental income into the fund. I was also pleasantly surprised to receive a $2,537.48 year-end dividend.

Readers, what do you think about Fundrise's venture product potentially listing on the NYSE? Do you expect it to trade at a premium or a discount to NAV over time? And would you consider investing before a listing to potentially benefit from any NAV expansion driven by supply and demand?

Fundrise has been a long-time sponsor of Financial Samurai, and I’m also an investor in Fundrise products. I’ve spoken with and met Ben Miller, Fundrise’s co-founder and CEO, many times over the years, and our long-term investment philosophies are closely aligned.

As with all risk assets, there are no guarantees. Please invest only what you can afford to lose and ensure your overall asset allocation allows you to stay disciplined through market cycles.

If you want more real-time thoughts on markets, real estate, the economy, and investment opportunities throughout the week, join 60,000 other subscribers and sign up for my free weekly newsletter. I have published three times a week since July 2009, when I helped kickstart the modern-day FIRE movement. Everything I write is based on firsthand experience.

Hi everyone, congrats on the successful launch of VCX. I encourage everyone to stay humble and don’t do any extra spending without first getting liquidity. Anything can and will happen from now until lockup.

Read: https://www.financialsamurai.com/stay-humble-after-a-large-investment-win/

Good advice..don’t count the chickens til they hatch!

jeeez… i’m speechless. I shoulda held those liquid shares a bit longer.

Mr Samurai, unrelated to VCX, there are a bunch of alternative products coming to market for smaller investors. I am highly skeptical of the overall push, primarily due to concerns about quality and suitability. We’re obviously seeing issues with interval funds. But, there have to be some decent offerings. Have you found any platforms or products that have caught the Samurai’s eye in PE/RA to research further? Platforms where they aren’t just trying to dump their garbage on retail investors?

I was able to sell the shares I purchased on 2/22 today, which was 44% of my VCX holding. Figured better than waiting 6 months for a potential drop, and I still have 56% to sell after lock-up.

someone is impersonating FatThor….these comments complaining about the listing are not the real FatThor

The should have sent the following information out when they announced the listing. I thought existing shares could be transferred to a brokerage account once VCX was listed, but locked. I also thought we couldn’t buy any additional shares after the vote occurred.

“Innovation Fund holders are able to transfer shares to their brokerage accounts. However, this currently applies only to investors who hold unrestricted shares – specifically those purchased after February 20th as part of the pre-listing window.

Regarding the email notifications, not all investors may have received the “Managing Your Unrestricted Shares” email or Newsfeed update yet. These notices are generated and delivered in batches based on when shares fully settle. If you own unrestricted shares, you should receive the email and corresponding Newsfeed update shortly once the notice becomes available.

For most Innovation Fund shareholders who hold restricted shares (the standard shares held before the pre-listing window), those shares remain subject to a six-month lockup period following the listing and cannot be transferred until that period ends. During the lockup, your shares will be held at Computershare (our transfer agent) and will be “view only.”

Once your lockup period ends, you should receive detailed instructions on how to transfer your shares from Computershare to any brokerage account of your choice.”

When do we think VCX will actually list? It was supposed to be 3/9 but that has come and gone.

I’m glad it didn’t list on March 9. Perhaps end of the month or once there’s more stability in geopolitics and the market. There is no rush, unlike Robinhood’s RVI.

Did you buy unrestricted pre-listing shares? If so, have you been able to successful transfer your shares over to your brokerage account?

There’s no rush?! Our shares are sitting idle! Stability in geopolitics and the market is not happening for many months.

An expedited rush to market and this happens LOL. What a joke.

Wouldn’t delaying the listing be the opposite of expediting to market?

With a $38 million net worth, how much did you invest in the innovation fund? I would think it would be no big deal whether it less now or later for you. It’s not a big deal to me.

March 17.

They were supposed to list March 9 or March 10. No communication from them about transferring existing shares.

Where is VCX? It was supposed list on March 9 or March 10. Today is March 12 and no word from Fundrise. What is going on?

Working through backend operations to get all investors who bought the unrestricted pre-listing shares squared away. We just got our set up and transferred to our online brokerage.

Then there’s waiting on more favorable time to list with all the uncertainty going on. Smart on them. No rush.

Did you buy unrestricted pre-listing shares? If so, have you been able to successful transfer your shares over to your brokerage account?

I already had shares. No email from them about a transfer.

Bad opening for RVI. Terrible timing + sentiment. But, it’s just one day.

Hi Sam, very interesting article. Thank you.

I do believe VCX will trade at a good premium on its first week (probably not as high as DXYZ because, like you said, the fund is much more diversified), maybe over 50%, but that premium would rapidly go down and likely turn into a slight discount as the end of the lock-up period approaches.

However, despite the high diversification, the top 3 holdings (Anthropic, Databricks and OpenAI — in addition to SpaceX) are all expected to go public themselves in 2026 or early 2027. If this happens, in my opinion the ”pop” they will generate will be huge given their valuation and own lock-up periods their employees will face, which might lead VCX to trade at a premium as high or even higher than DXYZ later this year or early 2027. Would you agree ?

On a side note, do you think what the Trump administration is doing with Anthropic could significantly affect its valuation ? Thank you!

Hi Joel – I think the default thinking is once Anthropic, Databricks, OpenAI, and SpaceX go public, depending on how they do, the premium to NAV for VCX would decline since investors can just own the shares directly.

However, you could be right in that if they all surge higher, then VCX will naturally rise with them. Further, during the own employee lockup period, there could be an expansion in premium to VCX temporarily. But of course, hard to say.

As I wrote in this weekend’s freely weekly Financial Samurai newsletter, the government snafu with Anthropic is likely to be a bump in the road that will actually lead to more user signups but to a divided country and all the media coverage it is now getting. Claud by Anthropic is now #1 on the Apple App Store.

Nice stance on Anthropic!

What’s pretty unique with VCX is that all of these main holdings might go public concurrently, or almost simultaneously one might say. Given that OpenAI is expected to be the largest IPO in US history and Anthropic the second one (and SpaceX in the top 5 – top 10) this could well be a once in a lifetime event.

I suspect the own employee lock-up period could be really beneficial to us. I also agree the expansion in premium would be very temporary. I have about half of what you have in the Innovation Fund but I plan on cashing out at least half of it if that kind of ”pop”happens. I totally believe in the underlying long-term growth potential but I’m one of those people who prefer to redeploy in less risky / more tangible assets like real estate if the opportunity comes.

Let’s see what the future holds. Any large premium to NAV, if it happens, is a temptation that’s hard not to take advantage of. But we can all run our models to make a determination of what premium is worth selling at compared to the compound growth of the NAV.

My goal is to asset allocate and invest for the long term (5-10 more years). I actually don’t want the temptation to sell, as the AI move is clearly a 10+ year trend IMO that is only going to grow.

What percentage of your investment assets is in the fund and where are you on your financial independence journey? For reference, I left finance in 2012 and have been FIRE or unemployed since.

It’s very true that the core question here is what premium is worth selling at, compared to the compound growth of the NAV.

Personally I just hope any large premium to NAV happens soon enough to be able to take the tangible benefits and get priceless peace of mind.

I think it’s not disputed that AI will turn into a bubble at some point, the question on everybody’s mind is ”when”. Like you and like people at Fundrise I think the 5+ year mark is pretty safe (but who knows for sure?). The 10 year mark, though, comes dangerously close in my opinion. Not worth the headache or procrastination for me.

I only graduated from college 4 years ago so I’m still working full time as a software engineer. The Innovation Fund is about 25% of my investment asset. Redeploying in real estate and for increased diversification was (and still is) my main goal.

Hi Joel, I think you may enjoy this follow up post: https://www.financialsamurai.com/theres-no-need-to-escape-the-permanent-underclass-after-all/

Sam- Here’s one for ya. Now that we know VCX will be listed, will you include the fund in your “stocks & bond” allocation, or your “alternatives” allocation bucket? Thinking through for my own diversification strategy and curious your thoughts. Thanks!

It’s a good question. Probably more towards my public stock allocation now, as a public venture fund. At the same time, I will have it as a specific allocation towards venture capital as well.

Let’s hope for the best! I’m glad Anthropic is the largest holding, as it bulldozes its way across industries.

Thanks Sam, So, for example within your diversification framework/strategy you will likely mark 50% of the total capital invested in the VCX fund to public stocks, and then keep 50% marked to alternative/venture. I think that is a good way to think about it as well. Or am i misunderstanding and you would weight differently? Thanks!

That’s one way to do it. Overall, I have a target and a limit of investing up to 20% of my total capital into alternatives, which includes venture capital.

The key is to stay disciplined, and stick to your asset allocation targets as they should be based on your goals and risk tolerance. It’s when investors go far outside their targets where they can sometimes get hurt.

Yes, definitely appreciate your goal posts and strategy around diversification and have taken action on that which is where these questions are coming from :)

I’m 38 w/2M net worth and have around $150k invested in the fund that is split between Roth and Brokerage.

Currently have around $100k cash to invest and looks like i will need to look at refilling the alternative bucket if i mark 50% of my assets in the fund toward public stock exposure now. Today like many, Gold/Bitcoin/Energy/Oil is on my mind.

I’m 26 and looking to diversify in this nasty market. I’m at $38M net worth and have around $6.5M invested in the VCX fund. I have about $4.6M cash to invest and thinking of just putting it in monthly dividend ETFs until the AI IPOs.

That’s awesome. You are worth so much so young. How did you amass $38 million just eight years out of high school?

Options trading on a few “tips”

Cool. Hope you grow it to $100 million!

Insider trading doesn’t appeal to everyone.

looks like you doubled your net worth yesterday with the ~$30M gain on your VCX today. congrats!

Hi Sam, what are your thoughts on the pre-ipo shares being offered?

Being able sell with no lock up is an attractive option, especially if the shares trade at a premium to NAV.

After the latest holdings was released on February 15, I was pleasantly surprised to see Anthropic as number one at 20%. Given anthropic has been demolishing industry after industry of these past couple of months, I would think that demand for that company is quite high.

What are your thoughts?

Why are your recent contributions so sporadic?

I like to invest in pieces as I do more research and understand more. Because with this investment, once you invest the money, you won’t get it back for at least 7 months due to the 6-month lockup.

After this post, I wrote:

How Do ETFs, Open End, Closed End Funds Trade

Why Does Pershing Square Holdings Trade At A Deep Discount To NAV

After each post written and digested, I ended up investing a little more. That is how I do my due diligence.

How about you? How have you invested in the product and what is your views of the listing’s future?

you should include this in the article. it’s more than “a little of SpaceX”

Thanks. Updated. 5% still isn’t a huge position, but more than the 2% from September 2025.

SpaceX is run by a man with a personality disorder who thinks life on Mars is not only possible but sustainable. Starlink, yes. Mars, not going to happen.

Realize they gotta invest some of the funds that have flown into the fund, but really not a fan of buying more SpaceX at this valuation

I tried to push more cash into my Roth INNOX, but they told me it was closed to new money, and instead they divided it into their two other funds – which I do not want.

Beyond that, between the Fundrise fees and the fees Inspira charges I am not sure I want to deal with this.

Next, regard the ‘vote’ – even though shareholders voted down the fee increase, I have read the management is going to raise the fees regardless of the vote.

Yeah, Fundrise had to shut down new investments on Friday, Feb 20 I believe, in preparation for the launch.

Where have you read management will raise the fee regardless of the vote not receiving 2/3rds majority?

OpenAI Chief Financial Officer Sarah Friar recently said the company’s annualized revenue topped $20 billion in 2025, up from roughly $6 billion the year prior. Also 280B by 2030.

This will make every large pension fund manager rather nervous. The thing troubling them will be ‘what in my current holdings is going to be eaten by AI’?

Ben Miller has publicly stated he regularly received million dollar offers from large funds for some of their positions in VCX. In short since VCX is going to be the public ticker for private tech VCX demand is going to be borderline bonkers. This will lead to a problem; liquidity.

3 solutions, unlock current holders, issue more shares at NAV or sell some of the funds holdings. The latter is impossible. Founders would fume and Fundrise would be doing the exact opposite of their stated reason to be. In sum reputation wrecked. The go to will be unlock in stages as necessary.

‘Bye bye now’ will likely turn into the largest folly of an investor’s lifetime. VCX has a baked in 35% NAV increase before OpenAI’s revelation. They have put their cards on the table and said ‘show us the money’ to the rest of the AI big boys. More NAV boost in the offing. Strap in VCX can literally with SpaceX take you to the moon. The coming Fundrise roadshow will ensure it.

Love your conviction! And I hope everything you say about OpenAI and VCX does come true.

However, I’ve invested long enough and in various venture funds to know that nothing ever goes according to plan.

We cannot count our chickens before they hatch. For example, I thought I was going to get huge returns from Rippling, an HR software company my fund invested in 2018 at around $500 million. But with AI crushing software by 20-30%~ maybe not! It was worth around $16.8 billion in the latest funding round last year May 2025.

Today would suggest our conviction was certified correct!

It is an amazing launch. We just got to stay grounded. But congrats to us for now!

See: https://www.financialsamurai.com/stay-humble-after-a-large-investment-win/

Revenue is not the same an income. According to Fundrise’s most recent SEC filing (CIK 0001640967), in December 2024 they had $21,081,000 in cash and nine months later, in September 2025, they had $10,896,000 in cash — that’s a 50% decrease in 9 months. In addition, the SEC filing states that Fundrise is operating at a loss with negative cash flow.

Fundrise needs cash and taking this fund to market will allow them to increase cash flow, which is greatly needed. It will be interesting to see what happens to their real estate funds after this. Will people still be interested in their poor performing Flagship fund or will they abandon ship (pun intended).

Current private tech funds on the market are not going bonkers. In fact, they are down over the past three months. They will most likely rebound, hopefully, but the AI bubble has to be taken into consideration.

Yeah, the calamity in all these interval funds and public private credit funds (blue owl, etc) illustrates exactly the problem when you mismatch duration of assets and evergreen funds. VCX being a closed end fund will have a fixed amount of capital to work with and will not be subject to the whims of inflows and outlfows anymore…a huge positive.

That said, I am a bit nervous about the negative sentiment out there for software/tech. But, this could pass.

Will be interesting to watch Robinhood Ventures today.

I’m at further odds to the ‘voting with my wallet’ analogies I’m reading about re VCX. In spite of the stated downsides against ‘democratizing the process’ (e.g., nav discount, volatility, floats /spreads, valuation lag and expense ratios), there remains the fact that by creating a ‘lock-up’ period for those choosing to remain loyal to the ‘party’, the process communizes the fund, by restricting their very movements, that which in a publicly traded fund should allow, and only because its ‘better for everyone’. Seems less than the laissez-faire capitalism I was raised with.

I know this is the way its done, but it rips at the very core of the argument.

Anybody???

You may want to ask Phil. He seems to be a genius.

See liquidity problem above. The alternative is trading at a discount to current NAV (practically impossible) but if it did weak hands would rush to exit and dump. That’s why we are locked up, but as I said you should anticipate staged lock release if that assuages your concerns/irritation. It’s the obvious first release valve. However if you believe we are going to compress the Industrial Revolution into 2 decades not 2+ centuries as I do you might wish you were locked up for 6 years not 6 months.

I may not be the sharpest bread knife in the drawer, but at heart, I’d be just as put out as if my ‘Global Asset Management’ solutions provider changed my ‘preferred shares’ into ‘bonds’. It seems a bit off-putting and I guess I can’t explain it correctly.

I just attended the virtual shareholders’ meeting, which lasted four minutes. The Fundrise general counsel read the IPO proposal and voting options, then ended the meeting. That was it! No questions. What a joke.

If the fund goes public, which it appears to be the case since Ben Miller has already scheduled another shareholders’ meeting next week (to be aired live on YouTube) to discuss the IPO, then I will pulling all of my money out of Fundrise. Byeeeee!!!

That’s the beauty of the free markets. Investors can buy and sell as they choose.

But what are the reasons why you would sell besides you being bearish on the growth of companies like OpenAI, Anthropic, and Databricks? Your reasons can help others make better decisions as well.

I’ll be curious to see how Robinhood adventures fund, RVI, does post listing. If it trades at a premium to NAV, then I think VCX can do the same.

I didn’t say I would sell. It’s too late for me to do anything with my Innovation Fund shares because Fundrise intentionally blocked share removal/purchase the same day as the end of the vote, prohibiting people from making a decision based on the outcome of the vote. (By the way, investors can buy and sell as they choose within Fundrise.)

What I meant was I will pull the rest of my money out of the remaining funds (i.e. Flagship, Income) and close my account. Flagship has been a disaster, and I didn’t like getting blindsided by the Innovation Fund announcement. The fact that they have expedited the vote in a matter of days is a red flag. The fact they did not allow questions during the shareholder call is another red flag.

This is a money grab by Fundrise. They are increasing their fee rate by 35% by putting it on the exchange. For a company losing money, it’s what they have to do to survive.

Why didn’t you comment on the shareholder meeting portion of my original post? What’s the point in holding a shareholder meeting if all your going to do is read the email you sent to your clients? Pathetic.

The beauty of Fundrise is “investors can buy and sell as they choose” — it’s not a closed fund. I didn’t say I was going to sell. Besides, I can’t sell because Fundrise set the liquidation date and voting deadline date on the same day, prohibiting investors to make a decision after the voting results.

What I meant was I will liquidate my real estate funds (i.e. Flagship, Income). Flagship has been a disaster. I don’t like getting blindsiding by FR with this IPO announcement with only a couple of weeks notice.

It’s an obvious cash grab for FR because they are increasing their management fee by 35% once the fund hits the market. FR is losing money, so it’s in their best interest to take the Innovation Fund public. If FR was doing well, then why don’t they go public? They sold “IPO” shares in the company several years ago, but nobody knows what the NAV is now.

Maybe Richard is one of those retail investors who doesn’t really understand that equity in a company is different from client investments in a fund where there is a separate LLC from Fundrise the company and the fund investors.

Richard‘s assumption is common for unsophisticated investors. Which is actually a risk and why Fundrise and other funds would best have investors like Richard out. This listing helps.

There’s a reason why traditional venture capital firms require accredited investors to be limited partners.

Maybe Phil is one of those investors who doesn’t care if he loses money in the market.

Btw, even though the “management fee increase” vote failed to pass, Fundrise states in their response to that they will do whatever they believe is in the best interest of the shareholders. I take this to mean they intend to increase the management fee.

I got the impression they had to do it per some SEC regulation. I was surprised it was so short. Clearly, Ben knew the vote would pass based on the number holders with large share positions. I did find it ironic that the management fee increase failed to pass, which means the people who voted in favor of going public didn’t want to pay the higher fee. That’s like people wanting to get into heaven, but they don’t want to die.

Currently between 3 listings/potential listings (DXYZ, VCX and PWRL) and one closed end fund ARKVX total AUM ~ 2 Billion. Market Valuation of just Anthropic and OpenAI is ~1.5 Trillion, not even counting SpaceX and Databricks etc. I don’t see it moving the needle much. Out of the three VCX if anything should have a better premium since they didn’t pull any tricks like insider allocations ( I mention that in my post). My thesis is that demand is real and it should trade at a premium. Why do I say that? DXYZ is trading at a 50% premium today. Tickers like DXYZ, VCX and PWRL will be well correlated (because they have similar holdings, though not exact but a majority of their stake is in the same companies). This makes them good candidates for stat-arb strategies. If one is trading at 80% premium and the other at a 20 percent discount some Quant in a Hedge Fund is going to turn on a strategy to buy one and sell the other to bring them in line. So yeah they can trade 20 vs 40 premium but not 80 and -20. And with VCX having better reputation than DXYZ and PWRL it should ideally be the one trading at a higher premium.

The NAV of DXYZ is actually around $11.5 now. So it’s trading close to a 145% premium.

I’m biased and believe Fundrise has a better reputation than Destiny, and a better portfolio of names too. But bias gets me in trouble, so I want to stay level-headed here.

Good point about arbitrage with premiums and discounts, although not perfect, I can see how a quant hedge one would do that.

I can’t invest in Cathie Wood’s funds. She has lost so much of invrstor’s money since Covid with ARK; and her target prices for Tesla and Bitcoin are widely optimistic and dead wrong so far. Great marketer, it a great investor. It is shocking how bad her performance is.

I recently received an email from Robinhood with the following:

private markets have been closed to everyday investors for too long. Robinhood Ventures Fund I is changing that by expanding access to private companies at the frontiers of their industries. Be there for the unveiling.

Date & time: February 17 at 10 AM PT / 1 PM ET

Date & time: February 17 at 10 AM PT / 1 PM ET

This sounds very similar to what Fundrise is already doing. Do you think more competition in this marketplace will be good or bad for the Innovation Fund?

I think there are two things at play. One, a rising tide lifts all boats as RobinHood is one of the largest brokerage platforms today. As a resolved, there will be a lot more interest in such funds, and that’s still over affect will flow to Fundrise, as investors look for alternatives, especially ones with better value or better portfolio compositions are larger discounts to NAV.

On the other side, if there are enough of these products on the market, the supply gets mopped up, and there may be a greater discount to NAV for these funds. But where are things stand now, the demand is so much greater than the available supply of these private AI companies that 50 new Funds launching I don’t think will do enough to soak up demand.

Of course, there’s no guarantee with anything here. But this is my thought process.

well, that sure explains the timing/urgency

I understand the pros/cons but not the impact or mechanics. Say I have $100K and they move forward Does that mean I get stock worth $100K? In the future if I want to invest another $50K do I just buy it on the market? So if the NAV if 10% premium I now pay 10% more? That seems to me to be a one time benefit for what I already have invested. Future investments would just be buying stock and possibly having to now pay a premium? I was thinking of investing more but now I don’t see why I would. I relatively new to investing in the fund so I wouldn’t gain much. Appreciate any comments on advance how it specifically impacts those that invested once this happens.

If you think they will trade at a premium to NAV, and you want to invest more, then do it now, before they list through Fundrise. Right before listing if I read it correctly Fundrise will stop accepting new purchases. I think trying to suss out where it trades premium/discount etc. to NAV is too hard. If you like the holdings and want more exposure to AI, software etc. Just DCA (dollar cost average) into the fund until you get the allocation you want.

I’m writing another post that shares my thought process on NAV discount or premium based on research on Pershing Square Holdings and the Robinhood Venture Fund I upcoming listing. Stay tuned for that post, out on February 19, 2026.

Bottom line, I think there’s a 65% chance the Innovation Fund trades at a premium. And if RVI, the Robinhood Venture fund, trades at a premium, that probability goes up for VCX based on the similar structure and holdings.

This is a done deal. If you read the Fundrise update dated 12/2/2026 I would suggest the shareholder meeting will be a ‘reveal’ not we need your vote. They got my vote anyway days ago. The window to buy now will close sooner rather than later. I’m sure Sam will be more circumspect when he comments but Mr. Miller is speaking as plainly as he can

I’ve come to expect nothing is a done deal until the deal is done.

The volatility now and the public markets is extremely high. Yet, with Anthropic raising another $30 billion at a $380 billion evaluation, the demand for private AI companies has never been higher.

So in a way, if the fund list and existing shareholders, want to sell at a discount NAV, the larger the discount, the greater the demand will be for me and others to buy. So that Discount should narrow. And of course, if it trays at a huge premium to NAV, we will kick ourselves for not buying more now.

I support anyone’s opinion on all this as everyone has their own motivations for investing. But, I think some people are misreading the benefits of the current setup vs the listing, which is understandable. An evergreen private fund is very different from a drawdown fund. Currently, the Innovation fund is evergreen and allows quarterly liquidity. Sure, it’s private, but the inflow and outflow of funds is massively disruptive to the management of funds and realized returns. For example, if there is a large outflow, for whatever reason, then Fundrise has to sell ILlIQUID assets at whatever price the can get to fund those withdrawals, unless they put up a gate. On the flip side, if there is a massive inflow of funds, it dilutes the existing holders returns. That is the major flaw of an evergreen fund having illiquid assets, but shorter term cash flows. Moving to a closed end fund would fix the AUM (capital base is locked in, unless new shares are issued or retired) and they would not have to sell assets based on capital flows but only when they want to for valuation purposes. Yes, there is daily market volatility, but, ironically, it is a FAR better alignment of long term capital base matched with long term underlying holding.

Yes, the key point is the mismatch between illiquid underlying assets and ongoing investor inflows and outflows in an evergreen structure. Not good when there’s suddenly a lot of panic too.

The key concern initially is how it trades to NAV. If there was some type of sweetener or minimum NAV discount guarantee or promise Fundrise would buy back any shares post listing at NAV for a short time after lock up, then the vote would overwhelmingly pass to list. Bc there’s also a chance for a premium to NAV as well.

Ben Miller stated in a reddit post 4 days ago that if the stock was trading at a large discount to NAV (he says 20% in the post) that fundrise “would very likely look to do a share buyback”. I dont know if a reddit post can be considered a promise but its at least something

Thanks for sharing! And that would be great if Fundrise did. If Fundrise could signal intention of doing a share buyback if the discount hits 10%, that would allay a lot of worries.

As investors, we are relying on Fundrise to do the right thing post listing, which I think they will.

That’s a good sign! Still adding to my position this month.

Sam, do you think it would help or hurt VCX if some of the main holdings (OpenAI, Anthropic, DataBricks) start to IPO prior to lock up expiring? My guess it just depends on where it trades relative to NAV at that specific timeframe.♂️

If scarcity is a big factor for it to trade at a premium to NAV, perhaps it’s better for these names to stay private for longer for pre-IPO holders.

Yes, if they IPO, it’s no longer scarce as everybody can buy. So we depend on management to rebalance accordingly. Just look at the Figma IPO and its performance.

Indeed. My thoughts exactly!

LOL!!! Figma has tanked!!!

? Figma did tank after, which is why I mentioned it.

Are you an investor in the Innovation Fund?

Why so much disrespect in your comments?

Yes, I’m investor. Why else would I post? And why are you censoring my comments? I see you didn’t post my main comment about the supposed scheduled call tomorrow for investors.

What comment? I don’t see anything. Did you include links and disrespectful language? If so, it’s automatically filtered outs

Only investors got the invite.

I do like the emotion from your comment though, so keep it up. What do you think is driving your emotional response as an investor?

Don’t think Jane understands. Looks like reading comprehension problem. Wouldn’t bother responding as Jane is low class, comes from Reddit, and probably only has a couple thousand invested. Got to keep the uneducated lowlifes away.

Wow. Even if Jane does only have a couple thousand invested, doesn’t mean you should launch an ad hominem attack (considering you “wouldn’t bother responding” yet you did). I’m surprised FS allowed your misogynistic comment to be posted. It’s comments like yours that breeds cruelty.

You obviously are not aware of Fundrise’s financial problems, which seems to be the reason for the fund’s IPO. Perhaps you should do some due diligence (see SEC) before commenting about the “uneducated lowlifes.”

You comment is in poor taste and rather immature.

Why fix it if it ain’t broke? I voted against going public because the fund is doing great and the stock market isn’t. Fundrise is not telling us something about going public, and it makes me uncomfortable. The Innovation Fund was appealing to me because it was private; otherwise, I could invest in publicly traded ETFs that hold private AI companies (i.e. AGIX, ARKVX, GPZ). I don’t understand the rush to the market except for the possibility the Fundrise C-suite is looking to exploit the situation by cashing in. The original prospectus makes no mention of going public or even possibly going public. I don’t like it when investment companies change their behavior on a dime. It’s unsettling, which is not a positive look with personal investments. Is Fundrise taking their best performing fund public because they are having debt problems with their real estate investments? Ever since they combined their plethora of real estate funds into the Flagship fund, it’s been a losing fund for multiple years now. Do they need capital to bail out their real estate investments? Are they running low on cash? According to their most recent SEC filing (CIK 0001640967), in December 2024 they had $21,081,000 in cash and nine months later, in September 2025, they had $10,896,000 in cash — that’s a 50% decrease in 9 months. In addition, the SEC filing states that Fundrise is operating at a loss with negative cash flow. — It looks like we have our answer.

I agree. Your argument makes sense, but I’m not surprised Fundrise is taking the fund public for selfish reasons. Since when do financial institutions ever do anything for the sole benefit of their clients?

At least on the market you will be able to sell your shares. If your shares were to stay with Fundrise, there’s no guarantee that you could even get your money out. If Fundrise were to go bankrupt, everyone would lose their investment or get pennies on the dollar.

What Samurai says about technicalities is only part of the picture. There are other points, some – market related, some – people related. CGPT easily finds multiple failure points – ask yourselves, it’s lengthy, but the bottom line to me is that now the link between my money and DaBigAi company is more direct, perhaps much more, than if it were to become Yet Another Index Fund.

Please chime in. Thank you!

Nope. I already voted against it. I chose to invest in Fundrise to AVOID the market — that was the appeal. It is disappointing that they want to take this fund public because it reflects poorly on their integrity.

Can you expand on why it reflects poorly on their integrity? Do you feel that other closed end funds and other funds that list have questionable integrity too? If so, why?

Can you confirm what the new fee structure would be? I read that the SEC filing included… Page 10 (and the surrounding sections) of the filing describes the shift from the current 1.85% flat fee to the proposed 2.0% management fee and the 20% incentive fee (carried interest) above an 8% hurdle.