The average credit score for approved mortgages continues to remain high. Banks continue to only lend to borrowers with the highest credit scores.

Before the 2008 – 2009 recession, the average credit score for approved mortgages averaged around 720. 720 is actually the cut-off point between “Good” and “Excellent” credit.

Given the housing market collapsed nationwide anyway, one shouldn't be too impressed with a 720 credit score. A 720 credit score should be viewed as average, at least from this loan officer's perspective.

Average Credit Score For Approved Mortgages Went Up Post Financial Crisis

After the housing bubble burst, the average score for approved mortgages shot up to 769 from 2009 until the end of 2012. A 769 credit score beats out 80% of all other credit scores out of 850. In other words, banks weren't lending to hardly anybody. The upside is that the probability of a similar type of housing crash in the future has declined.

Then by 2020, according to Fannie Mae the average credit score of an approved mortgage applicant went down to 741. During the start of the pandemic, the demand for housing shot through the roof. But it was brutal for even good income earners to get a mortgage back then. Many renters I know have been shut out of the housing market simply because they can't get a loan.

I still see little signs of sub-prime mortgages or negative amortization mortgages returning. But one thing we should be concerned with is the latest Federal Housing Administration initiative to get Boomerang Buyers back in.

Boomerang Buyers Coming Back

The Federal Housing Administration has come out with a new program allowing buyers who lost their home to a foreclosure or short-sale to buy another home. These buyers are dubbed “Boomerang Buyers” because they've come back for more.

The program requires that applicants show they lost at least 20 percent of their income for at least six months, which in turn caused them to lose their home. Boomerang Buyers then must show they recovered from hardship (grey area) and have had clean credit for at least one year.

Clean credit doesn't mean a good credit score mind you. Once borrowers pass the initial tests, they are eligible for regular FHA loans which require just a 3.5 percent down payment – no different from a first time FHA loan applicant who never foreclosed or short-sold a home!

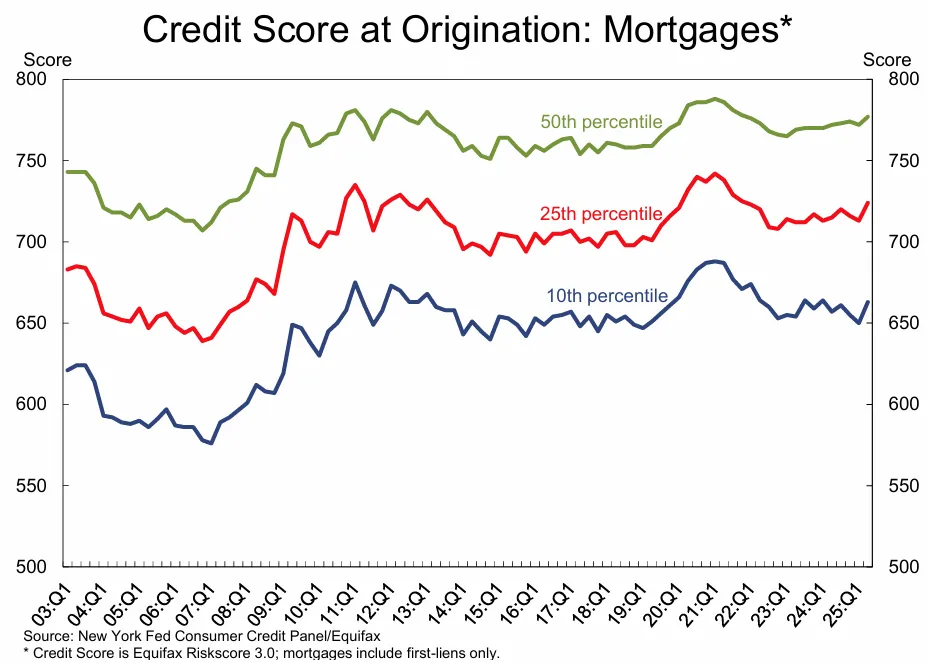

Credit Score At Origination For Mortgages

Below is the latest credit score at origination through 2025. As you can see, it peaked in 2020, scores fell through 2022, and now they are back on the rise to about 780. As a result, it's once again getting harder to get a mortgage to refinance or buy a home.

There is even a high profile case of owner-occupancy mortgage fraud by a Fed Governor, which highlights one way in which borrowers try to lower their interest rates. During elevated mortgage rate environments, borrowers get “creative.”

Seems A Little Risky

Think about this for a little bit. The government, in all its wisdom is allowing those who stopped paying their mortgage for whatever reason to try again with only 3.5% down. Meanwhile, banks who are offering jumbo mortgages (not covered by Fannie or Freddie) are requiring 20% or greater down with ~741 credit scores to buy a home. This is the main reason why jumbo loans have LOWER rates than conforming loans. The borrowers are simply higher quality.

One would think that going through the trauma of foreclosure or a short-sale would produce home-buying scars for at least a decade (takes ~7 years for your credit score to fully recover). One would also think that if you foreclosed on a home before, you should at least be required to put down greater than 3.5%. But I guess the government is so pro-homeownership that they can't help but get people who can't afford a home to try again.

If you only put 3.5% down, you hardly have any skin in the game. The first people to foreclose again during the next downturn are those with the least amount down.

To make a point, if you paid 100% cash for your house, of course you aren't going to foreclose given the cost of ownership is minimal. It would be better for all of our finances to follow the 30/3 rule for home buying.

The Housing Market Is Slowing, But Will Come Back

If you are long the property market, you are relatively sanguine about the current loosening of credit standards. One property I own in Tahoe tanked because nobody could get a condotel mortgage anymore. This was despite the property yielding a net operating profit yield of 8-10%. The only buyers were cash buyers. Things have recovered like everything else, but the mortgage market for condotels is still tight.

If you are short the property market (renter), then you should either take full advantage of an FHA loan or overweight mass market homebuilder stocks until they blow up.

Just like how it's unwise to fight the Federal Reserve when investing in the stock market, it's unwise to fight the Federal Government when investing in the real estate market. The Federal Government is signaling they will do everything in their power to get as many Americans to own a home as possible, regardless of their history.

When it comes to buying property, seek a golden time to buy real estate when the math makes sense and you come across a good deal that checks all the right boxes.

When the average credit score for approved mortgages is declining a little bit, it's also easier to get a mortgage at the margin.

Invest In Real Estate Without A Mortgage

If you don't want to invest in real estate with a mortgage, diversify into private real estate instead.

Consider Fundrise, a platform that allows you to 100% passively invest in residential and industrial real estate. With over $3 billion in private real estate assets under management, Fundrise focuses on properties in the Sunbelt region, where valuations are lower, and yields tend to be higher. As the Federal Reserve embarks on a multi-year interest rate cut cycle, real estate demand is poised to grow in the coming years.

In addition, you can invest in Fundrise Venture if you want exposure to private AI companies like OpenAI, Anthropic, Anduril, and Databricks. AI is set to revolutionize the labor market, eliminate jobs, and significantly boost productivity. We're still in the early stages of the AI revolution, and I want to ensure I have enough exposure—not just for myself, but for my children’s future as well.

I’ve invested over $400,000 with Fundrise, and they’ve been a trusted partner and long-time sponsor of Financial Samurai. With a $10 investment minimum, diversifying your portfolio has never been easier.

To increase your chances of achieving financial independence, join 60,000+ readers and subscribe to my free Financial Samurai newsletter here. Financial Samurai began in 2009 and is the leading independently-owned personal finance site today. Everything is written based off firsthand experience.

I really think that the government should require “boomerang buyers” to have a minimum credit score of 720 and at least a 10% down payment. I’m also curious as to how they will verify these people actually had a decrease in salary of 20% for 6-months. Does that include not getting a raise? I’m only bringing this up b/c my sister-in-law and her husband walked away from their house without any hardship issues, they just felt they had spent too much on their house and “everyone else was doing it” so they did it too. Now, I don’t want to deny them another house, but I think that 3 years isn’t long enough and 3.5% down isn’t an adequate down payment for the boomerang bunch.

However, not to sound hypocritical, I’m hoping to purchase a home as a first-time home buyer probably under the FHA program. I have excellent credit (score over 760), very little debt (I still have student loan debt, but that’s it) and a good income. My down payment won’t be 20%, but I’m okay with that for now.

It doesn’t seem right that your relatives should be able to buy another house with only 3.5% down at all. Letting the house go with no hardship is the exact mentality that leads this nation to economic ruin.

With that credit score, you should not go FHA. Save up an extra 1.5% and go conventional with private mortgage insurance.

FHA charges a 1.75% up front mortgage insurance premium on the loan amount plus 1.35% a month for mortgage insurance. With your credit, you could cut the monthly rate down to 0.6% and have no up front premium.

Oops, the monthly rates are annual. I should have re-read what I was typing before hitting “post”.

We’re in the process of closing on our first house and the financing must have relaxed a lot. I’m lower-mid 700’s on my credit score, and we didn’t have to put down nearly 20% down on the house, requirements were 5% minimum and obviously have to pay for the plethora of other fees that come with it, inspections, appraisals, other closings costs, etc. We do have sufficient income and despite not having an 800 credit score, have almost zero debt and no negatives on credit at all, so I imagine both of those played into it a lot.

In our experience, just getting a bid accepted on a house has been the most difficult part, fingers still crossed everything keeps going smoothly. The housing values here never really went down, just stagnated, but it has been absolutely ridiculous from a financing first time home buyers perspective. The first 5 houses we put an offer on sold in under 48 hours and every single one was paid in cash, and there have been at least 10 that we were really interested in that sold too fast to even get a bid in. Was getting a bit discouraged that we couldn’t get an offer accepted in 7 months as it was just nearly impossible to compete against cash buyers even when bidding over asking.

Anyway, I don’t think it would be wise to return to the practices of the 90’s but it’s absolutely a great thing to get more people that want to own homes and have the means to purchase one, the opportunity to.

I really have to question what the long term outcome of the massive corporate property purchasing that going on is going to be. I’m sick of seeing home rentals in my area for well over the mortgage cost which is a direct result of all the cash buyers that we were battling against. On the other hand, if I had the cash means to get in on that business model, I’d be all over it. They’re easily getting an equivalent 8 – 9% return to what a bank would be making on a 4.3% mortgage on the same property, and they have the luxury of being able to increase the rent every year.

Congrats on getting your offer accepted! Where are you located?

With no debt and a clean credit report and high credit score, you are doing well. I’ve got all sorts of debt since I have multiple properties and different streams of income. Lots more investigation as a result!

Well, the housing market only got as high as it did because of a confluence of subsidization and overly loose lending. Just because we made a speculative bubble once, doesn’t mean we should do it again. I agree that current lending standards are probably too high, though. I wouldn’t quite qualify, and I’m the most fiscally sound person my age I know, apart from a close friend from college who started earning 6 figures right out the gate and has panic attacks about money whenever anything goes even slightly imperfectly. When I think about some of the other people I know who own houses, I find the notion that I’m less capable of handling that responsibility than them to be a pretty shaky proposition.

I know you are very pro-home ownership/building a portfolio of rental income and that’s great. But lets be real here, a lot of people are better off renting though. Not everyone should buy up property and have a significant amount of their net worth tied up in real estate. A lot of people are not capable nor do they want to spend the time to being landlords. I just seen too many people get crushed because of buying a property and possibly move soon after. They then find out being a landlord long distance is a job itself plus their full time jobs.

A lot of people these days, especially the newer generation like myself. We are constantly moving places, taking on new jobs, our careers can force us to move locations for that next promotion/pay raise. Its not like before were it was the norm for most people to spend 30 years plus at one employer, get a pension and retire in the same location.

Al though I really do feel like I am missing out by not owning. But its probably not ideal for me right now being overseas and not knowing when I’ll be back in states.

I have moved at least 5 times in the past 11 years(spending no more than 2 to 3 years in one location). If I did not have the flexibility to move to different states and overseas on 2 of the occasions. I would of left a lot of money on the table and my net worth would of been about half of what it is today, if I couldn’t make a move quickly.

For those of us are in situations that want to be in the real estate game but can’t due to distance and circumstances. What are some alternatives? I have looked into property managers, REITS, crowd funding real estate projects etc. But yet to actually talk to some one who has done it first hand… any one have any more information on this?

My credit score is just fine. I currently have a 793, 797 and a 805 from all three major credit monitoring companies. I have never even had a car loan, personal loan, or mortgage in my name either. Just built that up purely by using several credit cards regularly and paying them off in full every month.

5 moves in 11 years is A LOT of moving. I wouldn’t buy property either until I knew with 80%+ certainty I would be in one place for at least five years.

Save your expat money like crazy and enjoy the adventure!

Great analysis. This is valuable information if you are making plans and checking out the market. I think its also quite useful if you are working on building your own credit score. Its use knowing that attitudes about what you need from your schore change over time.

Sam, I’ve seen you write about how hard it is to get a mortgage, but this must be for primary residences only. My credit score is constantly slammed by opening up new mortgages (it’s only in the mid-700s) but any mortgage I apply for goes through very quickly.

I’m not sure who or what is greasing the rails. Maybe it’s because I can only use brokers now rather than traditional banks? Does that make a difference?

If you don’t mind me asking Jason, how many properties do you own now?

PS-I’m in contract for #4 as we speak and I noticed the bank (USAA-all my mortgages through them) is being strangely more demanding for additional documents this go around.

Chris

I love USAA but they were the most difficult bank I have ever used to purchase a rental property. I have also used a broker which was difficult as well. Currently using a large well known bank and closed last rental within 3 weeks. closed a refi within 4.

Maybe you are just buying way lower than you can afford? Feel free to share more details about your income, purchase price, area of purchase if you’d like! thx

Ok, so I just did a sale a few months ago and I’m down to 7 doors. But once I figure out how much taxes I owe for ’13, I’m hoping to get another 2 if I can.

I’ve successfully applied for 9 mortgages since ’09 (including my personal home) and I also did about 3 refi’s when the rates started dropping. Three of these mortgages were under 100k. Five of the mortgages were in California and the other four were out-of-state. All of my investment loans were under 200k.

Interestingly, I’ve found the lower-cost mortgages were actually the most trouble. I think it’s because no-one actually makes that much money on them, so there’s not that much incentive to give good customer service. Plus, because of the low amount, it’s more costly to refi to take advantage of a rate drop.

My advice is to get the most bang-for-the-buck on each mortgage, so as long as your cash-on-cash return remains about the same, borrow more. My last couple of slots will be for larger amounts against small multifamilies.

3.5%! Wow I’d certainly take advantage of that if I lived in the US. Ha!

When I read your articles I do have a tendency of looking up facts/figures. Good side effect. :)

Like check this out:

https://en.wikipedia.org/wiki/List_of_countries_by_home_ownership_rate

Home ownership rate of United States is only 65.2%. Canada at 69% (although the data is 2 years older).

Considering that someone who foreclosed could walk away again.. How big of a mortgage would they be approved for? Are they at least looking at debt to income ratio?

This is an interesting article:

https://www.citylab.com/housing/2013/09/why-us-needs-fall-out-love-homeownership/6517/#disqus_thread

Should we be trying that hard to get people into houses? Americans have other means of acquiring wealth. Like stocks, The Lending Club (which we Canadians don’t have! boo!), ETFs (safer than stocks!), mutual funds (your grandfather’s ETF), and good old fashioned savings accounts (but who uses those anymore??).

And a higher paying job you can get by moving can offset any “wealth” acquired by owning a house. Or paying really cheap rent while you divert your money to more education.

However if you can buy a really cheap house, that’s usually better than renting..

I hope Canada has a nice soft landing, and no hard crash like the US. Your real estate charts are looking a little scary!

Interesting article! I think the banks are loosening credit because they need the business or higher profit business. Either way, it is for their own self interests. After all banks are in for the money, profit and their shareholders.

I will freely admit that I am a huge cynic and perhaps I even border on the edge of conspiracy theory. But I sincerely believe that the ill-advised move toward allowing lower credit score people have another shot is two pronged. First the administration had a vested interest in “helping” lower income people. When it is election time, guess who these people will vote for? The people who say “buck up, old chap. Work to get a larger down payment, pay your bills on time and get your credit in shape. Then we’ll consider giving you a loan.” Or will they vote for whoever says “You poor thing. Everyone is against you. Wall street doesn’t deserve its riches so we are going to let you have some by giving you this great deal. Only 3.5% down instead of 20.” I’ll let you ponder the response to that. The second prong is that when the housing market tanked, many jobs were lost. Mortgage loan officers lost jobs, construction workers lost jobs, etc. And when people lost (or didn’t buy homes) municipalities lost tax revenue. They desperately need this revenue to fund operations and pensions. So it is in their best interest to get more people back to paying into the municipal coffers.

Property taxes = Oh how sweet it is for the government.

One city government official reached out over e-mail and said they are trying their hardest to get renters to pay more taxes. The only way is to get renters to become homeowners.

Politicians are awesome!

This is great news for potential new buyers and for people who lost their homes due to the recession. My mother almost had to sell her house a few years back when she lost her job, but my siblings and I helped out for a while and she was lucky to have found another job. Other families weren’t so lucky and had to lose their house. This “boomerang buyer” program will allow them to once again be home owners.

Is it really a good idea to allow for only 3.5% down for boomerang buyers who foreclosed or short-saled the last time around? The cascade of defaults crushed homeowners who continued to pay their mortgages on time all throughout.

What’s wrong with just renting or buying until one has 20-50% down?

This is fascinating. I think I commented in one of your other real estate posts that friends of ours with very high incomes– well over $200K annually– were treated like children (a letter from this place, a letter from this employer, verification of this, etc.) went they went to borrow money for a new home, despite high credit and well over a 20% down payment. Once again, it seems like the broad middle is being pummeled by new regulation, while the very wealthy (cash buyers) and the credit unworthy (boomerang buyers) are off to the races!

Gotta love Big Government! Resistance is futile. So you might as well try and take advantage of all the government programs as much as possible to the extend of the law right?