You might be wondering why rich central bankers remain unrelenting in their desire to raise interest rates. After all, there are plenty of signs individual components of inflation are rolling over.

Given each interest rate hike takes at least six months to have an affect on slowing the economy, the Federal Reserve could easily over tighten, thereby worsening the recession.

American central bankers have the dual goal of maintaining maximum employment and stabilizing inflation. When the labor market is robust, there tends to be inflationary pressure and vice versa.

The NAIRU (Non-Accelerating Inflation Rate of Unemployment) is an estimate of the lowest the unemployment rate can go without leading to rising inflation.

In an ideal scenario, the Federal Reserve would like to see an unemployment rate of between 4%- 5% and an inflation rate of between 2%-3%. In other words, the NAIRU is around 4%, but it changes with the times.

Historically, the Fed has had an inflation rate target of 2%. However, based on where inflation is today, I'm sure they'd be happy if we got to 3%.

The Central Bank's Role And The Power Of Moral Suasion

An important policy strategy is using moral suasion to get consumers and investors to do what rich central bankers want. Moral suasion is the act of persuading a person or group to act in a certain way through rhetorical appeals, persuasion, or implicit and explicit threats—as opposed to the use of outright coercion or physical force.

For example, even if central bankers believe inflation has peaked and is heading down, they won't verbalize their beliefs to the public. Because if they do, the public may end up hiring, buying, and investing aggressively again in anticipation the central bank will slow its rate hikes or cut rates in the future. If this happens, it neutralizes the deflationary effects of the central bank's rate hikes, thereby extending higher inflation for a longer period.

Central bankers are very similar to politicians in that they have a proclivity to say one thing and do another. However, unlike politicians, the effectiveness of a central banker's actions can be more easily measured given both the unemployment and inflation rates are easily tracked.

The farther away the unemployment rate is from 4%-5% and the inflation rate is from 2%-3%, the more the central bank is failing. Instead of creating soft-landing scenarios, the central bank is orchestrating boom-bust scenarios. And during boom-bust scenarios, more people suffer.

Ideally, we want the peaks and troughs of a business cycle to be as close to the long-run real GDP trend as possible. This way, citizens can better plan their future.

Wealthy Fed Board Of Governors

Now that we understand central bankers can't always speak the truth or speak clearly to the public (Alan Greenspan was famous for nonsensical jibber jabber), let's try to understand how central bankers think.

Jerome Powell, makes $203,500, while other Board members make $183,100, amounts set by Congress. In America, these are top 15% salaries. However, their salaries are not too meaningful as all of them are wealthy.

Our seven Board of Governors of the Federal Reserve are already rich. Fed Chair Jerome Powell was a partner at The Carlye Group, a private equity powerhouse. His net worth is easily over $50 million, and more likely over $100 million.

When you are worth tens of millions of dollars, you are obviously financially secure. No matter how poorly the economy performs, you and your family will likely still be fine. You do not need a day job to live a good life. You already have enough assets to generate a large sum of passive investment income.

Further, once you have mega millions, unless you're extremely greedy, your focus shifts more towards service and legacy. Do not underestimate the importance of legacy to a wealthy person.

Legacy is why billionaires donate massive amounts of money to colleges to get a building named after them. Even though these colleges already have huge endowments and continue to charge exorbitant tuition rates, some of the richest people can't help but lust after status and legacy. It’s just human nature.

Banning Of Trading Securities By The Federal Reserve Board

In addition to already being rich, the Board of Governors had a tantalizing advantage other investors did not. It was the ability to trade securities before they made policy statements and decisions.

After many years of public complaining, starting May 1, 2022, members of the Federal Reserve may no longer trade affected stocks beforehand and front-run their decisions. As a result, the opportunity to make millions from this form of insider knowledge has vanished.

The rules “aim to support public confidence in the impartiality and integrity of the Committee’s work by guarding against even the appearance of any conflict of interest,” a statement by the Fed said.

No matter how rich you become, however, it's hard to suppress the allure of making money in a way most others cannot. This is the combination of greed and the thrill of being able to get away with a wrongdoing. When you have power, you sometimes feel very special.

For example, Galleon hedge fund manager Raj Rajarathnam was worth billions. Yet, he was still willing to trade on insider information provided to him by his pal at McKinsey. You would think the risk of going to jail for 10+ years would be enough to deter such illegal activity.

Trying to get away with something illegal can be intoxicating. At a certain level of wealth, you sometimes believe you are above the law.

The irony is, as investors, it was probably preferable for the Board of Governors to continue to be allowed to trade on insider information. This way, the Governors would be more incentivized to adopt polices that boosted their multi-million dollar investment positions!

Just look at how various American stock indices have performed since the proposed ban was announced at the end of 2021. Since the beginning of 2022, the various stock markets have all gone down. Coincidence? I don't think so.

Status Increases If You Hit Your Target Objectives

With no incentive to make money via trading, the Federal Reserve Board of Governors is now focussing on status. Its status in the history books will increase if it can get inflation back down to 2-3% without causing the unemployment rate to go up beyond 5%.

Right now, the Board of Governors has mediocre status. In 2020 and 2021, it cut rates too aggressively and unleashed too much liquidity for too long. Partially due to these decisions, inflation spiraled to 40-year highs.

Now, the Board of Governors wants to rectify its mistakes. It doesn't want to be viewed as the reason for causing so much inflation. But this time, without millions of dollars of personal investments at stake to moderate its decisions, it can now raise rates as aggressively as it wants to and tank the economy and force inflation down.

Central Bankers Can Outperform In A Worsening Economy

As the stock market and housing market decline, the Board of Governors and thousands of Fed agency employees get relatively wealthier. They've got less exposure to risk assets and more cash.

Further, working for the Federal Reserve is a much safer job than working in the private sector. As more private sector jobs are lost due to a recession, employees at the Federal Reserve outperform.

When you don't have as much skin in the game, you naturally don't care as much. Such wealthy people with lots of cash are licking their chops to buy a move-up property at a discount!

I know what I've written sounds cynical, but this is the reality of the world. As long as monetary policy and government policy are run by people, there will always be policy errors. It is very hard for anybody to overcome greed, fear, and the desire for status.

If central bankers were not rich, but mostly made up of middle-class people, perhaps their decisions would be more moderate. Maybe, middle-class central bankers would be more empathetic to the majority of Americans who rely on jobs to survive.

But if you're rich enough where you don't have to work, and narcissistic enough to want a top government job, then you may not care so much about the middle class. Instead, you're more focused on your legacy.

If the Federal Reserve doesn't relent on its rate hikes by the end of 2022, the recession will likely deepen. And because I believe the Board of Governors care about their legacy the most, they will likely become more dovish in 2023. But in case they don't, you need to raise your cash hoard.

The more cash you have in a deepening recession, the better you will feel. And as more assets sell at bargain-basement prices, you can swoop in and take advantage of the Fed-induced carnage.

The Federal Reserve Is Struggling To Govern Properly

If it isn't clear by now, it is dangerous to depend on the government or an individual to survive. You must depend on yourself. Politicians have their own agendas. Further, the good graces of an individual will unlikely last forever.

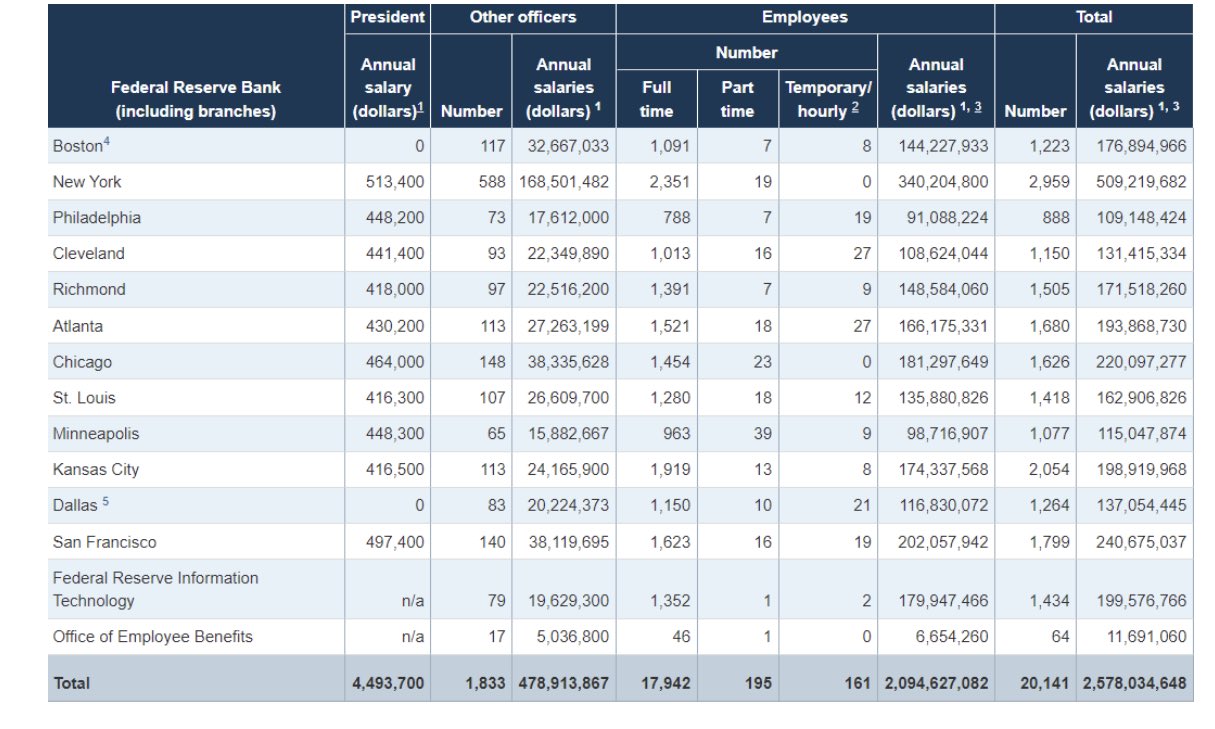

The Federal Reserve Bank literally employs ~400 PhDs and has over 20,000 employees with an annual payroll of over $2.578 BILLION. Yet they still can't properly manage price stability. Maybe economics is a harder topic than it seems given the endless variables.

Or maybe the Federal Reserve spends too much time on bank regulation. According to one reader who used to work at the Fed, around 18k employees work on the ACH system, auditing banks, local programs, plus administrative areas – HR, accounting, IT, etc.

Whatever the case may be, don't fight the Fed and also don't believe the Fed will make the right decisions most of the time. If they really hike the Fed Funds rate to 4% as inflation comes down, we are going to experience a world of pain. Be prepared.

Depend On Nobody Else But Yourself To Survive

Focus on boosting your cash flow to weather the storm. It is more important than a subjective net worth. No matter how well you do at your job or how much market share your company takes, an unrelenting Fed will break the correlation between effort and reward.

As I've recommended in my book, Buy This, Not That, follow an appropriate net worth asset allocation model for your age and risk tolerance. The key is to stick with the framework until the good times eventually return. In the meantime, if you need a job to survive, build your relationships with those who determine your destiny. More layoffs are coming.

Readers, how far do you think the Fed is willing to go to bring inflation back down to 2% – 3%? How much do you think being already rich has to do with how the Fed thinks? Are you raising your cash hoard now, despite inflation still elevated?

If you enjoyed this discussion, pick up a hardcopy of my WSJ bestseller, Buy This, Not That on Amazon. Not only will the book help you build more wealth, but it will also help you tackle some of life’s biggest dilemmas in a logical way.

For more nuanced personal finance content, join 50,000+ others and sign up for the free Financial Samurai newsletter. Financial Samurai is one of the largest independently-owned personal finance sites that started in 2009.

Fed certainly won’t bring inflation down from “8.5%” to 2 or 3% when interest rates are at 2.5 and going to 3.25. At this rate, it will take 6 months to catch up to inflation. All the fed is doing with these tiny moves is damaging economic growth. In order to stop inflation, the interest rates need to at least exceed the stated inflation rate.

The Fed and every so-called Govt Economist refuses to state the truth because it’s political dynamite: the Covid Stimmy handouts created inflation and the only way to curb it is to 1. create painful levels of unemployment or 2. Ask everyone to please give back all that stimulus money.

Guess which is more feasible?

There is no chance in hell the Fed would ever raise the Fed Funds rate above current CPI. We would go into a Great Depression and the Board of Governors and their families would be vilified for generations.

The problem is that with our over levered economy, businesses are loaded with debt and won’t be able to handle 4%+ rates. Regardless of where inflation is, do you remember when 2.5% rates froze credit markets and crashed stocks in December 2018? Something similar would happen by 4% currently despite inflation being at 8.5%. Long term rates are a better indicator of what fed funds rates will crash the market and cause a recession, not the inflation rate.

Not sure what all the weeping is about. Decreasing asset prices allows you to catch up to the mega rich. The longer the market stays tanked, the better. Fingers crossed this lasts for years.

You’re not wrong.

Yes, when Warren Buffett was down during the global financial crisis, we were all at least $30 billion closer to his net worth.

Funny! But the point is valid. Assets are cheaper. The question is how do we view them? As income producers – notice Buffett’s fascination with dividends (seems to have paid off); or as stores of wealth.

And I find it disingenuous (not you FS) to say Covid stimulus created inflation – a small bit, but much smaller than QE, supply chan disruptions, and employment disruptions brought about by immigration curbs, women leaving workforce and massive retirement. Or, if we are going to say “stimmy” let’s look at where money went – local govts., businesses, etc. as well as direct payments. Spiked inflation? Yep, but did anyone want a depression? Not seen a soul say yes to that.

I think a Fed Governor last week said inflation wouldn’t be this high if it wasn’t for COVID.

This is only good for people still in the accumulation phase. If you’re already in the retirement phase, higher rates and lower asset prices only hurts you, assuming you aren’t in cash.

Inflation might have peaked, but it is still high. To get closer to 2%, they will have to hike the rate quite a bit, right? I believe Powell when he said there will be more pain. It’s time to batten down the hatches and prepare for the storm. Investors were too optimistic because of the good unemployment rate.

We’ll strengthen our cash flow and try to keep investing. I think next year will be rough.

Thanks for humanizing and on some level exposing the Fed for what it is and isn’t. It is a powerful agency that is supposed to have the best interest of the US economy and people in mind. It isn’t a well oiled organization that always has the best interest of Americans in mind – at least based on your premise.

For me, after nearly 30 years of aggressive investing and riding mostly the ups of a stable American economy with near zero inflation, and astronomical economic growth to excellent personal net worth, I feel like the end of an era is upon us investors. I’m sad for the kids starting out investing who may not experience how successful our economic system can be when all the pumps are primed and running at full capacity. What a beautiful thing capitalism is when done correctly. Unleashing the creativity and inventiveness of American entrepreneurs and rewarding them and their investors with great wealth has been and always will be the only real path to better tech, medical, food, lifestyle etc etc.

I sense a big change in the air and it’s mostly coming from the political world. Yes politicians mostly have incredible wealth, but they no longer seem to believe that the capitalism that made them rich works for average people. I think this is a huge mistake, but I see the signs of this thinking everywhere I travel. Elites in govt and academia have decided that many issues should now be viewed thru a semi-marxist or socialist lens. Things like food distribution, energy production, transportation and even Science should be viewed less thru the lens of facts and the market and more thru the lens of Govt decree and issues of “equitable” distribution of resources. They are smart enough to mostly avoid using those words directly but anyone who’s studied Marxist econ theory sees it plain as day.

It seems to have been ramped up during the Covid pandemic maybe because maybe they thought people traumatized by Covid would be more open to new economic ideas.

Be that as it may, where we stand today is a scenario where the Fed appears to be unable to corral an economy drowning in massive Covid handouts that lit the inflation fuse and led to any number of terrible unintended consequences. the Federal Govts first stab at honest to goodness socialism has caused much more harm than it reduced, which ALWAYS happens when you replace capitalism with socialism.

The delicate balance between low inflation and low unemployment that has made millions of Americans millionaires over the past 20-30 years has been irreparably breached and I don’t see Powell or anyone else at the Federal Reserve having the brains or even desire to get the genie back in the bottle. I hope I’m wrong about all of this but like I said, I sense something in the air…and as Lenin was supposed to have said: the last capitalist we will hang is the one who sold us the rope. Capitalist do have many flaws when it comes to promoting and preserving their philosophy no matter how successfully it has raised millions out of poverty.

Can Fed first reduce its balance sheet first from $8 trillion to $4, pre-pandemic, or $0, like pre-2008? They literally own 30% of all outstanding mortgages and blew up the recent housing and asset bubbles.

The 2% inflation target was also a hoax too. Paul Voclker said in his memoir it was invented by some central banker from NZ in the 90s, for whatever reason even he didn’t know and never committed to either. However, 2% got repeated often enough to become central bankers group-think and sowed the seed of crypto (BTC was by design deflationary), not to mention it caused the real wages to stagnate since the 90s in spite of the productivity increase. Just look at how much we can accomplish nowadays thanks to the internet revolution and how little our wage income grew compared to our parents.

When I looked at our YE 2021 Net Worth in January, I realized we were at our peak Net Worth. We had a nice 3 year run up and I decided I wanted to de-risk a bit. I took all of my wife’s 401K money (~$1.8M) and moved it from equity funds to stable value funds. At the same time, I did want to keep new money going into equity funds. Even in a declining market, I could dollar cost average our purchases at lower prices knowing this money would eventually rise as the market turned around at some point in the future. We have the ability to defer 50% of my wife’s salary into a plan that also has a company match over and above the company 401K contributions so this new money continues to get invested in equity funds, along with new 401K and HSA contributions.

Making these moves helped us go from 90% equities to about 70% equities and gives us money to buy the dips and reap some longer-term gains down the road while we wait for this market to stabilize. I am retired and all of my funds are mostly in equity funds so this de-leveraging of my wife’s retirement funds seemed to make sense on a number of fronts.

As always, the trick will be to make sure I get her retirement money back into the market without waiting too long and missing too much of the eventual recovery.

I have decided to move my wife’s current 401K money from the company plan to Fidelity and purchase some short-term CDs until we decide to put that money back to work in equities. I don’t plan to move this money until we see signs that the Fed may be ready to pause their Fed Fund increases.

Fed should go ahead and hike 100 basis points in Sept and fall on its sword. QE created this monster, So tired of hearing the Shock and Awe commentary from the Too Big Too Fail Bankers on Wall St. Doom and Gloom. “ Just this week, Fannie Mae, the government-sponsored buyer of home mortgages, predicted the rate on the 30-year fixed mortgage will fall to an average 4.5 percent in 2023. The agency forecast average rates on the 30-year fixed at: 4.74 in Q1 2023, 4.54 in Q2 and 4.44 in both Q3 and Q4.” I wonder how/where they are getting their optimistic numbers? Thick as Thieves as Sam has so eloquently not stated. I don’t see Walmart, Amazon, Apple , UPS, Fed Ex marching 5 to 10,000 EE’s to the door before XMAS. $11.2 trillion in tappable home equity, and post COVID pent up Demand for travel, entertainment, new vehicles, New Apple I-phone, etc. Labor market for our service and consumption economy is already fragile.

i have been building cash since mid 2021. now 10% of net worth (500k or so) and growing each month. but i’ll tell you it is hard with inflation eating at it. SPY now down 22% and wonder if i should start layering back in. i already am 60% in stocks and at age 58 not sure where to turn. i have no significant bond holdings but YTD they aren’t much better and not yielding much better than aapl stock. tough environ.

Got to love your cash! Especially if inflation begins to drop. Much better to have cash lose value to inflation than lose to a loss.

I don’t think the Fed can get “official” inflation (see shadowstats.com for the real story) to 2%-3%. I think the world will be forced to re-benchmark inflation in general in the 3% to 4% range in a new normal that will produce supply issues for the rest of the decade. Moronic government policy around energy and Covid is indelible. The Fed will do as they do however, and hike until they break something. Like Sam says, cash up.

Fed doesn’t have as many options to manage or control supply side. Trying to beat down demand is not the best strategy when it is really the lack of supply or perceived/fear of lack of supply which is causing the problem. Government and agencies should be more focused on securing manufacturing and clearing up major shipping and trucking/transport issues which are the main reason why so many prices are going up…

Yes, good point. The Fed can raise rates all they want, it can’t improve supply chain issues and increase oil production.

Good thing shipping and trucking prices are collapsing again.

Nor can it eliminate all of the 7 trillion we printed in stimulus and handout bills in the last 3 years. now another 500b for student loans

The problem is factory in Asia will close down within next few months, and once we need more product there will no enough factories to produce it. We probably will experience another inflation wave next year.

Hi Sam, while your point has merit, I don’t think we can underestimate the power of peer pressure.

All the rich central bankers have rich friends that rely a fair bit on the stock market for personal investments, the companies they run and the big stock-linked bonuses they will receive.

As you highlighted in your article, central bankers’ performance is measurable and easily tracked. As soon as we see a clearer trend emerging, interest rates will be coming down gradually. I do agree that they want to postpone this for some more time mainly through hawkish interviews. But I am sure that in casual talks with peers they have a different tone and message.

“The last duty of a central banker is to tell the public the truth.”-Federal Reserve Board Vice Chairman Alan Blinder, Nightly Business Report, 1994

Yes, for sure. Rich people have many rich friends. Hence, I think the Fed HAS to relent in its insistence on hiking the Fed Funds rate beyond 3.5%, especially if the 10-year bond yield remains below 3.5%.

Let’s hope! Otherwise, this will be one of the most vilified Feds ever!

One other compounding factor is that Powell seemed to let Trump back himself down in Q4 2018’, and I suspect he knows it. Personally, I think we’re almost done. I do appreciate how hard Powell is jaw boning right now though. Just wish it started nine months ago

Fascinating topic! Yes it sure does seem ironic that it likely would be preferable for them to have kept ability to act on insider trading info.

I’ve been saving up a lot of cash this year, some partly due to getting less disciplined about putting my cash into the market, but also due to the desire not to lose money in this crazy volatile environment.

We haven’t seen a rate situation like this in many decades. Fortunately a few are still around that lived through Volker and the 70s. All the newbies in financial services and financial planning will be going to school for the next few years. Think about that.

agreed!

This is one of the best write ups I’ve seen about the Federal Reserve. I think you are spot on about the Fed protecting their legacy. 40 years later we still credit Voelker for bringing down inflation in the early eighties. I’m using history as a guide and say the Fed will probably overshoot. I haven’t been buying my normal amount of stocks on this down turn. I’m using 2023 earnings of $240 a share, ($10.00 below current estimates) and a 15X multiple as my line. S&P 3600. That’s when I’ll really get aggressive. If it doesn’t get down to 3600 that means I’m doing better than I thought.

Thank you for a great article, Bill

Bill,

3,600 is a solid threshold for when to start backing up the truck. I do think 3666 was the bottom for the S&P 500 in this cycle. So if it gets below that, I will be aggressively buying as well.

In my newsletter, I did say I would start buying more regularly below 3900 when the S&P 500 rebounded to 4300. So we’re close again and I have been nibbling. But my cash board is growing and I love it.

Let’s hope the Fed realizes they don’t need to overtighten as inflation drops.

Sam

Thanks for following up Sam…after reading your newsletter today, I came back here to make sure I hadn’t misread your post on Friday.

may I ask what factors indicate to you that inflation will drop?

Check out the first chart in the post. Gas prices have come down for over two months in a row. Freight rates from Asia have halved. Housing market is softening. The stock market is down over 15%. Deflationary signs are all over.

Are you not seeing the deflationary signs out there?

“The irony is, as investors, it was probably preferable for the Board of Governors to continue to be allowed to trade on insider information. This way, the Governors would be more incentivized to adopt polices that boosted their multi-million dollar investment positions!” This actually blew my mind because it’s so true.

I’m stuffing away as many ibonds as possible. Holding for at least a year, so no worries on penalties. T-bills also look delicious and are more liquid than Ibonds, but I can’t resist the interest rates on ibonds. Once you hit your limits on ibonds, I think T-bills will do just fine for cash positions.

Thanks for the article Sam.

I did not know about the recent stock trading restrictions for the Fed. I would still like to see their real estate holdings, though.

If they own lots of real estate and have little cash, then they may have no real interest in raising rates by a substantial amount to reduce inflation.

Even if they held all cash, they would then be tempted to cause deflation to benefit their cash position. Still a conflict of interest either way!

With great power comes greater responsibility. I like to believe that the Fed has the general public’s interest first. Maybe that makes me naïve. People may not remember you as well when times are good but will definitely not forget if you’re the one/group of people that made them suffer.

I’m saving up some cash and continuing to invest some (50/50) in Vanguard ETFs.