The following is a guest post from FS sponsor, FarmTogether, a leading farm investing platform. Farmland investing is one way to reduce volatility in your portfolio and generate long-term passive income. Let's look more into investing in 2021.

2020 has been a turbulent year for investors to say the least. On February 19, 2020, the S&P 500 closed at a record high. The following day it began a steep descent, eventually bottoming out on March 23rd, as the COVID-19 pandemic began paralyzing the global economy. This decline officially ended the longest bull market on record.

Despite a strong recovery in the public markets since March 2020, the US economy is still struggling. With rising COVID-19 cases and uncertainty surrounding the outcome of the presidential election in November, investors have become more hesitant about taking risks.

It is more important than ever for investors to have a clear strategy for managing their portfolios in 2021. Let's first go over stock market volatility and valuations. Then we'll discuss three common investing strategies for managing uncertainty in 2021.

Investing In 2021: Volatility On The Horizon

Record-breaking stock prices have been coupled with record-breaking volatility. The CBOE Volatility Index (VIX), a closely watched industry measure of stock market volatility, hit an all-time high of 86.69 on March 16th as many parts of the country entered lock-down in response to COVID-19.

The VIX has been trending down, but is now creeping up again given there's still no second stimulus package and COVID-19 cases are once again surging. It seems likely that volatility will remain elevated as we head into 2021.

Is the Stock Market Overpriced?

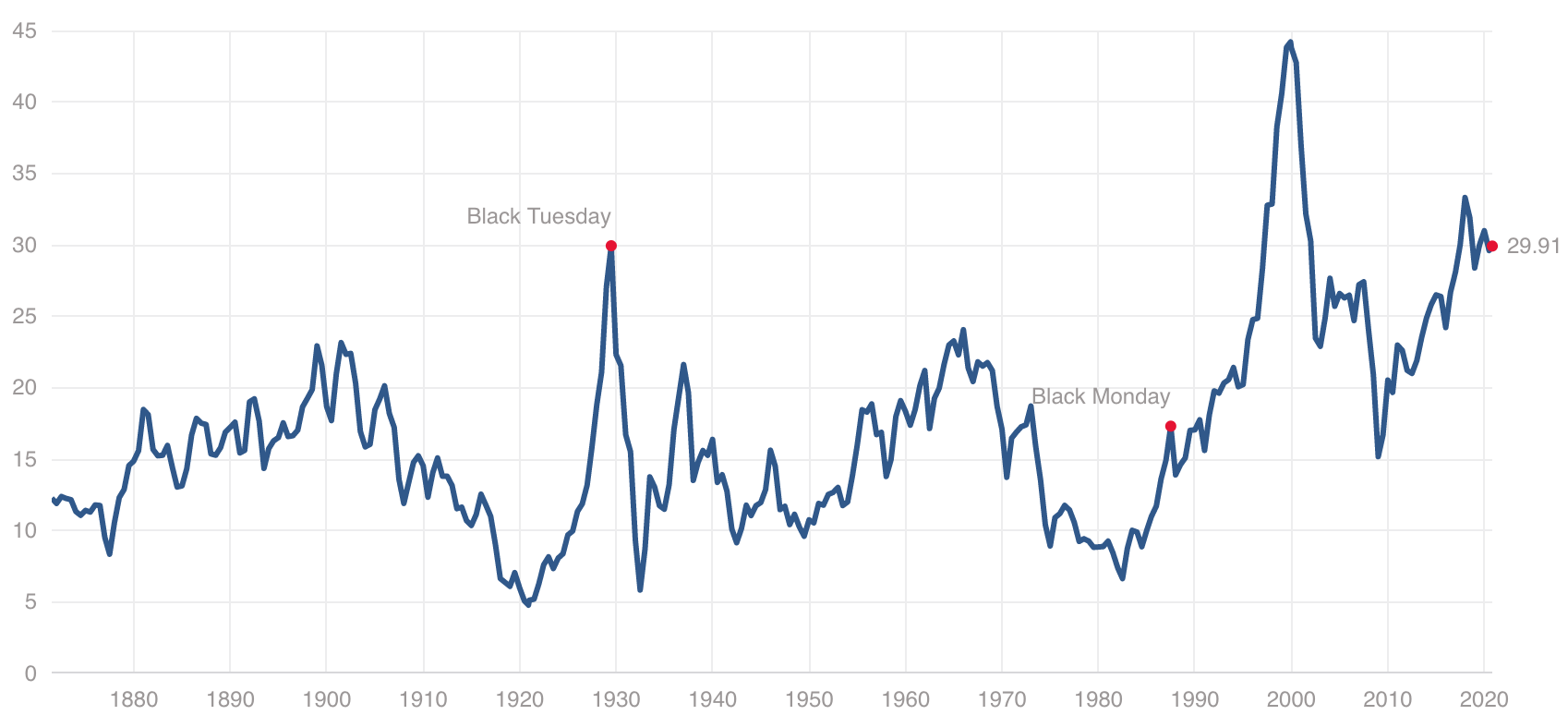

The S&P 500 Shiller PE currently stands at about 30X versus a median Shiller PE of 16X. Therefore, from a historical standpoint, the stock market is overpriced. With so much uncertainty on the horizon, it is very hard to accurately predict future earnings.

For example, Bank of America's equity strategist, Savita Subramanian, raised her S&P 500 EPS estimate from $115 to $125, which would represent a 23% decline from 2019 levels. She then initiated a $155 2021 EPS estimate, which is still slightly below 2019 levels of $163.

If there is a viable vaccine introduced to the masses in 1H2021, Subramanian believes her 2021 EPS estimate has $5 upside. But even with a blue sky 2021 EPS estimate of $160, a 28% YoY rebound in earnings, the S&P 500 is still trading at 20X 1-year forward earnings, which is expensive compared to the median of about 15X.

In September, the Federal Reserve projected that the economy would shrink 3.7% by the end of the year. Some Wall Street economists predict GDP growth will rebound by more than 5% in 2021, but only time will tell. Investing in 2021 will require properly forecasting both corporate earnings and economic figures.

Why Are Valuations And Stock Prices So High?

Stock valuations are so high because earnings remain depressed. Investors are always forward-looking. Investors hope there will be government stimulus and a coronavirus vaccine in the near-term.

Additionally, the Fed’s decision to keep interest rates low for longer means that the stock market is one of the few places where investors can seek potentially higher returns given the opportunity cost is so low.

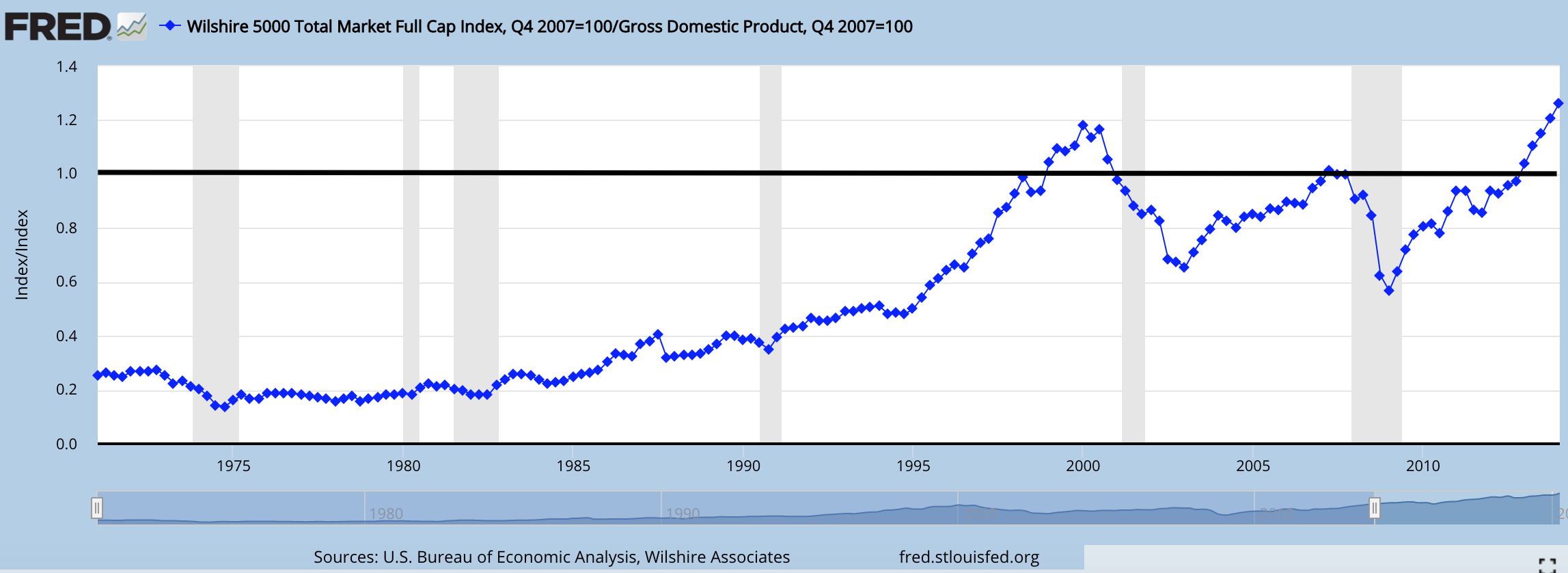

Buffett Indicator

With that being said, the stock market is also currently overvalued according to the “Buffett Indicator,” which is at levels not seen since the dot com bubble in 2000.

The “Buffett Indicator” is calculated as the ratio of the combined market cap of a country’s publicly traded companies to the country’s GDP. Any value over 100% implies that the market is too hot. In August 2020, the Buffett Indicator reached an impressive 183%.

Bearishness From C-Level Executives

Economic metrics aside, many C-suite executives are also concerned that the stock market is too hot. According to an August survey by Deloitte, 84% of Fortune 500 CFOs believe that the stock market is overvalued, the second-highest level on record. Only 2% of CFOs believe that the stock market is undervalued.

Which such beliefs, it's hard to see publicly-traded companies resume stock buybacks once it's socially correct to do so. Stock buybacks have also been a catalyst for higher stock prices in the past.

Further, Deloitte’s survey also found that 60% of CFOs rated the US economy as “bad” or “very bad,” and only 43% expect better conditions in a year.

Political Uncertainty

The presidential election in November adds additional uncertainty. It could take weeks to count all the mail-in ballots. Even after the counting is done, there might be a contested election that could be left up to the courts to decide. A contested election will likely lead to increased market volatility.

Perhaps there will be a Blue Wave or a Red Wave that will create much more certainty about economic policy in 2021 and beyond. With continued tremendous support from the Federal Reserve, 2021 could turn out to be a fantastic year.

No one can say for certain whether this level of volatility is the new normal.

Investing In 2021: Three Ways To Cope With Uncertainty

With all this uncertainty on the horizon, it is more important than ever for investors to be prepared for more vertigo-inducing stock dips. In order to protect wealth and continue to achieve long-term goals, we suggest three things.

1) Keep Diversified

Diversification is critical for building a portfolio that is resilient to market shocks. By adding multiple uncorrelated asset classes to your portfolio, you reduce losses in the event of a downturn in the stock market. Depending on the mix of investments, a diversified portfolio can also deliver above-market returns.

Diversification doesn’t need to stop at stocks or bonds – there are a number of alternative investments that offer benefits to investors. For example, farmland is a low-volatility asset class that is well-suited for long-term investors.

Over the past ten years, the value of farmland has risen over 6% each year. US farmland averaged 10% total annual returns from 1992 to 2018. Unlike some other alternative assets such as gold, farmland offers investors the benefit of passive income in the form of periodic cash dividends in addition to appreciation of the underlying asset.

2) Don't Try And Time The Market

With the stock market as heated and volatile as it is currently, it can be tempting for investors to try and wait for the “right” moment to invest. This is often a mistake. It is impossible to consistently time the right time to buy or sell.

While it’s clear now, that March 2020 was an excellent time to invest, hindsight is always 20/20. A good investor always has to try and forecast the future.

A better investing strategy is to dollar cost average. Invest sums at regular intervals instead of waiting to put all your money into the stock market at once. This is a natural way of ensuring that even when you’re buying high, you’re also able to take advantage of some of the market dips.

3) Maintain A Clear, Long-Term Strategy

The further you can stretch your investment goals, the easier it is to look past short-term volatility. Too many investors get spooked and sell when the market takes a downturn. This is a sure-fire way of losing money in the long run. Instead, the best approach is to understand your risk tolerance, allocate your portfolio in a risk-appropriate manner, and ride out the dips in the market.

Having a long-term plan helps take the emotion out of investing. And emotion is an investor's biggest enemy. By keeping your money in the market through the dips, you’re able to grow your savings with compounded interest.

Sam here. One of the tricks that has helped me stay the course is to think about investing for my children. In 20+ years, the long-term trend should smooth out and these short-term sell-offs will just be tiny blips.

Finally, remember that the market is more likely to go up than down. Over the past 40 years, markets ended up with positive returns ~75% of the time.

Consider Alternative Investments

If you dislike the day-to-day volatility of the stock market, consider investing in alternative investments like real estate, venture debt, private equity, and farmland.

Long-duration alternative assets like farmland have numerous benefits, including reducing overall portfolio volatility, mitigating risks, and providing passive income.

Learn more about FarmTogether’s investment opportunities in farmland or sign-up for an account today. It's free to sign up and explore.

Sam's Thoughts

Thanks to FarmTogether for sharing their thoughts on managing uncertainty and thinking about the future. Personally, I've been slowly allocating more of my investable capital to alternative investments. I really dislike volatility, and would rather invest in a private investment that doesn't have a daily price update.

Ideally, my private investments generate a positive IRR over a number of years and surprise me with a nice balloon payment. Once you start regularly investing in long-term alternative investments, these surprises become much more regular.

One of the goals of having money is to be able to stop thinking about money. I want to live my life with minimal financial distraction. Investing in long-term alternative investments helps me achieve this goal.

My rough investment allocation is 40% real estate, 25% stocks, 20% bonds, 10% alternatives, and 5% risk-free. My goal is to increase alternatives to 15% and slightly reduce real estate to 35% in 2021 by growing my overall investment pie.

Stocks and bonds are expensive. Meanwhile, the return on cash is so low because interest rates have been slashed. Therefore, the most promising investment opportunity in 2021 is real estate or real estate alternative investments in my opinion.

Related posts:

The Definitive Guide To Farmland Investing

Financial Samurai 2021 Stock And Real Estate Outlook

Readers, what are some of your thoughts for investing in 2021? What type of opportunities do you see? How do you plan to position your investment portfolio? Is the stock market rally year-to-date setting us up for disappointment? Or do you think investments could really perform well in 2021?

I live in california and have 50k in fidelity brokerage- other 125k already invested in etf’s- the 50k is earning no interest- what is your suggesting so I can make the money “work”- have 20k in checking and savings

Regarding your question about investing in 2021 and if the markets should be good, I think they will be. If things hold on the political front and we have a divided government then there is a higher likelihood the policies that would have been very unfriendly to the market do not get enacted. If we start to see some vaccines that can be widely distributed in the 1H of 2021 and we get some kind of stimulus in Q1, then we should see a positive environment for investors. Comparables next year should be very favorable, contributing to the positive momentum.

From what I have read, historically speaking, the best returns have come when we have a Democratic President and a divided congress. Right now, that appears to be what we are going to have.

Thanks Sam. Definitely agree dollar-cost averaging is the way to go, it’s also a lot more accessible for the average person that doesn’t have the time or desire to continually monitor investments.

Also think another point to note on diversification is to periodically rebalance. Know you have specific allocations that you aim to stick to, however I think a lot of people adopt a set it and forget it strategy, even more so now with employment pension contributions. Think this is leaving a lot of people with more risk that they think, especially now bonds don’t have stock market de-risk benefits they once did.

Do you have any recommendations on how often to rebalance? Do you do it at set times or when a certain asset class becomes X% off the target etc?

I think continuing to dollar-cost average into index funds is diverse enough for me, but I would definitely like to add some real estate to the portfolio to help weather any potential market storms. I’ve always heard that by investing in the S&P you do have some exposure to the real estate that those companies hold, since that is factored in as a part of their valuation. Where do you stand on that theory?

Based on various campaigning I’ve been hearing, I’m going to be watching closely for new rules for 2021, especially those concerning retirement planning, as they could completely change the playing field, starting as early as driving me to do some things this year.

If the tax exemption on 401k contributions is changed to a 26% refundable tax credit, that will end my contributions. I don’t have any employer matching and only avoiding state taxes makes it worthwhile now, double taxation on contributions for people with a marginal tax rate greater than 20.5% would make 401k investments a thing of the past, even as, for a lot of them, loss of the exemption would also make them ineligible for Roth contributions. And almost no one with a working spreadsheet program is going to want to be double taxed on 401k contributions, just so they can then roll or convert them into a Roth.

Changing long term capital gains to be at income tax rates when income is over 1 million is also likely to create a lot more consternation, even for folks that make no way near that normally, if it is paired with the “step up” provision being eliminated. Raising the top rate back to 39.6% could also make the pain go just a bit deeper.

If the “step-up” provision at death is eliminated then, as the executor for some of the folks in my family’s older generation, we will have to seriously reevaluate some estate planning.

Further, at least one of them is probably going to need some additional changes if estate tax exemptions are being cut in half, planning that wouldn’t have been needed until at least 2026, if ever, otherwise.

How do you classify RE syndication investments (like CrowdStreet)? Do you count them as real estate equity or alternative assets?

How would you classify RE notes or income syndications (since these operate like a REIT)? Not as safe as a bond, but typically not as risky as a growth fund.

I ask since we have about 35% of our overall wealth in real estate we own directly. I want to diversity our remaining portfolio into syndications and other alternative investments, and am curious to know how you would classify growth versus income plays in these areas.

I classify real estate crowdfunding as a type of alternative investment. My real estate asset allocation is physical real estate that I either manage, live in, or simply own.

My hope is that my real estate crowdfunding investments outperform my physical real estate holdings. They have since 2016, but now I’m concerned since heartland positivity rates are so much higher now.

Farmland is interesting bc it doesn’t really care about covid-19. Everybody still has to eat and the returns are less dependent on economic variables.

The goal for investing in alternative investments is for diversification and less visible volatility. I really love getting surprise passive income win falls and balloon payments. For example, just a week ago, I got a $35,000 distribution from one of my alternative investments. It was a nice surprise.

It’s fun actually not thinking about money and just focusing on living your life. What example, with the stock market melting down now, it’s no fun to spend any type of energy wondering how low it will go and portfolio composition etc.

Buying: I plan to buy (most likely in total or S&P index fund) when the overall market dips by 2% or more in small increments. I suspect this will happen numerous times over the next few months.

Selling: I plan to slowly sell some winning positions since the stock prices seem to be inflated, thus realizing gains. I’ve offset this by some losers I held for many years in hopes of reducing my tax liability!

Does this sound reasonable?

Sounds reasonable, and then it sounds a little bit counterproductive. What will the end equities acid allocation be and what is it now?

I think it’s important that Investors focus on asset allocation. Run the numbers regarding the potential returns, and stick to it. Ideally, and Investor will adjust his or her acid allocation by being able to focus more dollars on under allocated assets.

I’ve kept most of my long term portfolio holdings alone this year. I was also building up my cash for the last six months or so and just put some of it to use in the last couple days. But I still have a fair amount left in cash that I’ll maybe deploy bit by bit over the next six months.

I agree with staying diversified and not stress about trying to time the market. I like to buy when there are dips but don’t get frazzled on trying getting the timing perfect. I also like to keep my eye on the long game.

Maybe there is upside to the markets with companies that make it through COVID who are leaner along with the backdrop of low rates, low oil, and growing technological efficiencies. Maybe…

Hi Sam,

Thanks for sharing your rough asset allocation. When I think about my personal asset allocation, should I be thinking about it including my 401K? Or should I be thinking about asset allocation for after-tax investments? Do you have asset allocation recommendations for each (401K vs after-tax)?

Hi Sawyer, I include my equity allocation in my 401K in my overall equity asset allocation. Just have a note that I won’t be withdrawing from my 401K until after 60.

Understood and makes sense. Thank you!