As a FIRE parents raising two children in San Francisco, we rely heavily on our investments to remain free. If we significantly misjudge returns, we increase the probability of having to go back to work.

Going back to work is not the end of the world. Ideally, however, we would like to avoid it until our kids no longer want to hang out with us all the time. Based on observation, that likely happens around age 12, which puts us in the years 2028 and 2031.

For background, I'm 48, and worked in the equities departments of two major investment banks from 1999 to 2012. Roughly 35% of our net worth is in public equities. About 40% of our net worth is in real estate, which is the main source of our passive income. About 15% of our net worth is allocated to venture capital, venture debt, and crypto.

I don’t have the luxury of working at a venture capital firm while espousing the virtues of index investing. Nor do I have a cushy Wall Street strategist job that pays well regardless of whether my calls are right or wrong. I try to stay consistent in what I say and what I do because this is real money and real life. There are no mulligans.

Disclaimer: This is not investment advice for you. I'm sharing my thoughts and what I plan to do with my own money. Owning stocks carries risks with no guaranteed returns. Please do your own due diligence and invest according to your risk tolerance and financial goals.

Investment Outlook For Public Stocks

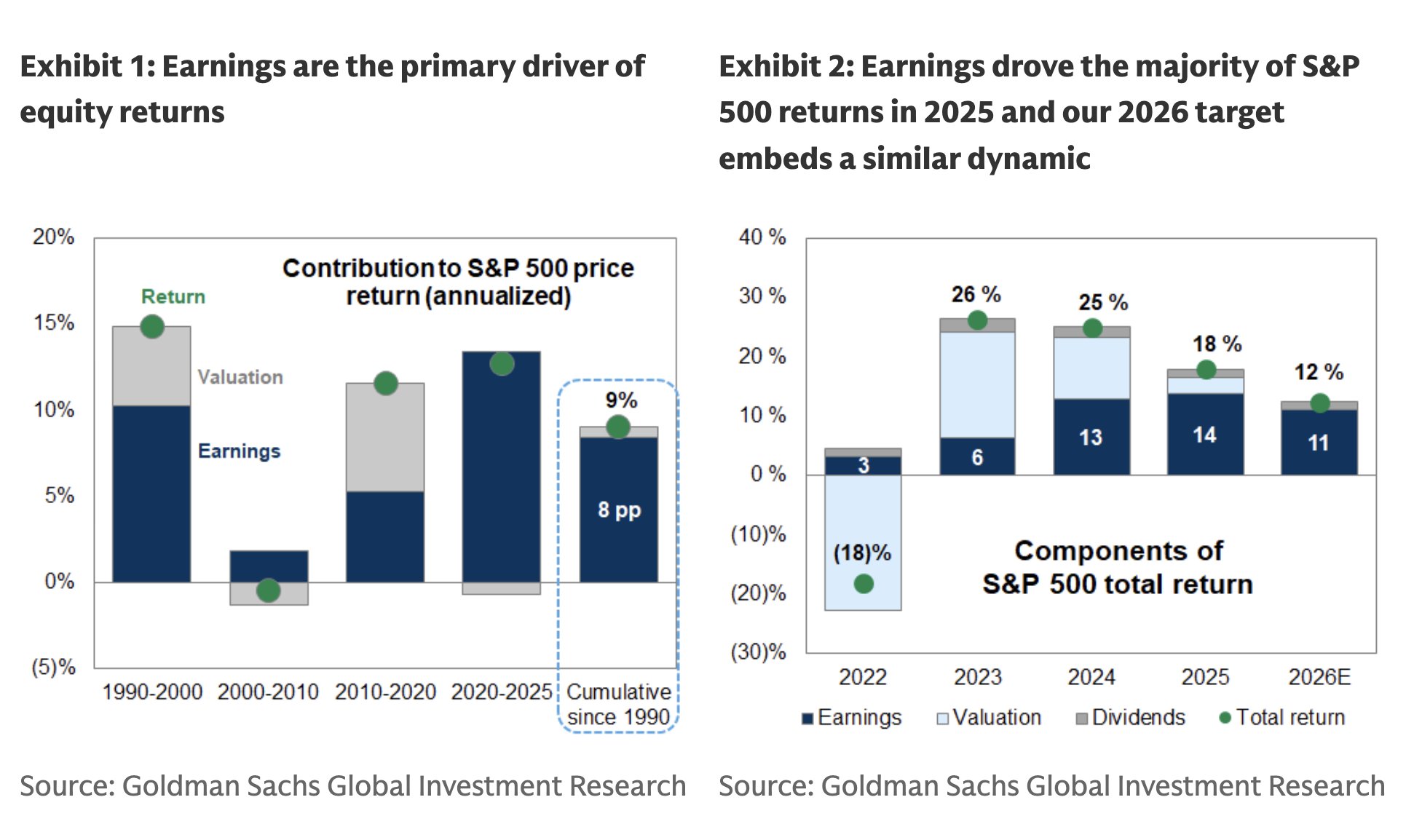

Earnings are the primary driver of stock prices, accounting for 70%+ of long term returns. The remaining 30% comes from valuation changes, macroeconomic forces, and political events. Therefore, the key question is where earnings are headed in 2026 followed by valuations.

The most likely answer is higher, perhaps in the range of 8 to 12% growth. We can arrive at this estimate by aggregating earnings forecasts for the largest S&P 500 constituents and layering in reasonable assumptions for margins, capital spending, and economic growth.

Once we have an earnings range, the next step is deciding what valuation multiple the market is willing to assign. Historically, the S&P 500 has traded around 18 times forward earnings, with peaks approaching 27 times during periods of optimism and technological transformation. That gives us a rough valuation band, assuming nothing breaks badly enough to push multiples below historical norms.

If we believe artificial intelligence represents a once in a generation transformation, comparable to the internet in the 1990s, then it is reasonable to focus on the upper end of historical valuation ranges. A forward multiple of 22 to 27 times earnings would place us in roughly the top quintile of historical valuations, but not in uncharted territory.

If year end 2025 S&P 500 EPS is approximately $272 and earnings grow by 8 to 12%, we arrive at a 2026 EPS range of roughly $294 to $305. Applying a 22 to 27 times forward earnings multiple yields a year end 2026 S&P 500 target range of approximately 6,500 to 8,200. That is an enormous range, but at least it provides a framework for expectations.

The midpoint of that range is about 7,350, which implies roughly 6% upside from current levels. Earnings growth would be driven by continued AI related capital expenditures, an easing Federal Reserve, and fiscal stimulus tied to the One Big Beautiful Bill Act. The primary downside risk is weakening consumption if job losses accelerate more than expected.

A Likely Lackluster Year For Stocks In 2026

Personally, I have low confidence that stocks will meaningfully beat the risk-free rate in 2026. The current risk free rate, measured by the 10 year Treasury yield, sits around 4.2%. A 4.2% return would place the S&P 500 near 7,200 by year end.

The difference, of course, is that Treasury bonds provide a contractual guaranteed return, while stocks expose you to downside risk. In an environment where valuations are elevated, geopolitical uncertainty is high, and elections loom, that trade off matters more than usual.

I am firmly in the camp that we will see another correction of at least 10% in 2026, so don't buy the dip too often too soon. Rich valuations, persistent geopolitical tension, and political uncertainty tend to make investors more risk averse. Corrections do not require recessions. They only require a repricing of expectations.

As a result, I do not think 2026 is the year to aggressively increase equity exposure or deploy most of your free cash flow into public stocks. Despite the roughly 70 percent historical probability that stocks rise in any given year, the risk reward setup looks less compelling than it did in 2023 or even 2024.

The S&P 500 is up approximately 80 percent since the start of 2023. We should be counting our lucky eggs and nurturing them carefully. After experiencing a 24% decline in 2022 following two strong years, the last thing I want is to give back a large portion of recent gains again. My approach for 2026 will therefore be more defensive.

How I Plan To Invest In Public Stocks In 2026

Specifically, I plan to allocate incremental capital toward Treasury bonds and private commercial real estate, two asset classes that have materially underperformed public equities since 2023. Mean reversion may not happen on schedule, but valuation dispersion matters.

My personal year end 2026 S&P 500 target is 7,280, based on a 24.3 times multiple applied to $300 of earnings. My largest individual stock position remains Google, which I view as a quasi monopoly with enormous free cash flow and optionality across multiple AI driven markets. But I think there should be a broadening out of performance.

Please be aware that around mid-year, there will be new EPS estimates for 2027, and the street will start valuing the market based on those estimates.

Given my muted enthusiasm for public stocks, I plan to focus primarily on maxing out tax advantaged accounts such as my Solo 401(k), SEP IRA, and my children’s custodial investment accounts. I do not plan to aggressively build my taxable brokerage account, the third rule of financial independence, especially since a significant portion of our house sale proceeds in early 2025 was already reinvested into equities.

Venture Capital May Outperform The S&P 500

After the exuberance of 2020 and 2021, private company valuations collapsed in 2022, with many private companies seeing markdowns of 50 percent or more. That washout, however, created healthier entry points for investors willing to endure illiquidity. 2022 is also the time when Fundrise launched its venture capital product.

Companies that survived 2022, or were founded during that period and raised capital at reasonable valuations, are often in much stronger positions today. They are leaner, more disciplined, and better aligned with customer demand.

I am confident that private AI companies will outperform the S&P 500 in 2026. The reason is simple. While the S&P 500 may grow earnings by 8 to 12 percent annually, certain private growth companies are growing revenues and earnings by that amount monthly.

The challenge, of course, lies in valuation methodology. Early stage growth companies are often valued on revenue multiples rather than earnings. A company generating $10 billion in revenue and growing at 200 percent annually may appear attractive at a 15 times revenue multiple. But once profitability emerges, the market often shifts valuation frameworks, sometimes abruptly.

Figma is a useful example. After a high profile IPO, its valuation was sharply repriced in the public markets, with shares declining roughly 80% from peak levels. While early venture investors still achieved extraordinary returns, later stage public investors learned that valuation regimes can change quickly.

This dynamic reinforces the importance of diversification across private and public markets. Metrics of success evolve as companies mature, and what looks expensive or cheap depends heavily on context.

How I Plan To Invest In Venture Capital In 2026

My goal is to build a $500,000 position in Fundrise Venture within my corporate account and a $300,000 position in my personal account earmarked for my children by end of year. I am roughly 75% of the way toward both goals and plan to contribute an additional $100,000 and $50,000 respectively.

I also have commitments to two closed end venture capital funds that may draw an additional $50,000 to $100,000 in 2026. Meeting these capital calls is a must, otherwise, I'll get blacklisted from future offerings.

Again, overall, I will limit my alternative investments to 20% of all investable capital. However, since companies are staying private for longer, I certainly want to have meaningful exposure to select names to capture more of the upside as well.

Slightly Up In 2026 Will Be A Win

Nobody knows where markets are headed. All we know is that stocks have historically risen about 70 percent of the time in any given year. Four consecutive years of double digit gains are rare, but not unprecedented. The mid to late 1990s provide a useful reminder:

1995: +34.11 percent

1996: +20.26 percent

1997: +31.01 percent

1998: +26.67 percent

1999: +19.53 percent

That run was driven by falling interest rates, rapid technological adoption, and strong economic growth. In some respects, today’s environment rhymes, particularly with solid GDP growth and moderating inflation. My hope is that there's a blowoff the top, like we saw in early 2000.

What matters is remembering what followed:

2000: −9.1 percent

2001: −11.9 percent

2002: −22.1 percent

The first rule of financial independence is simple. Do not lose a lot of money. Losing tons capital costs time, and time is the most valuable asset of all. I am deeply grateful that the stocks I owned since January 1, 2023 are up over 100 percent. My primary financial goal for 2026 is to preserve those gains.

That goal will require luck, but it will also require intentional risk management. For me, that means reducing exposure to public equities at the margin and diversifying incremental capital elsewhere.

Readers, what do you expect for the S&P 500 and for public and private markets in 2026?

Start 2026 With Clarity, Not Guesswork

If 2026 is going to reward discipline over blind optimism, then knowing exactly where you stand matters more than ever.

One tool I’ve consistently relied on since leaving my day job in 2012 is Empower’s free financial dashboard. It remains a core part of how I track net worth, monitor investment performance, and keep cash flow honest.

If you haven’t taken a hard look at your portfolio in the past 6 months, this is a sensible time to do so. Through Empower, you can also get a complimentary portfolio review and analysis if you have more than $100,000 in investable assets linked. You’ll gain clearer insight into your asset allocation, risk exposure, and whether your investments truly match your goals for the years ahead.

Staying proactive isn’t about over-optimizing, it’s about avoiding preventable mistakes. Small improvements today can meaningfully compound into greater financial freedom over time.

Empower is a long-time affiliate partner of Financial Samurai. I’ve personally used their free tools since 2012 to help manage my finances and investments. Further, I did some part-time consulting for them in person from 2013-2015. Click here to learn more.

Sam, thanks for the suggestion but what I really like about Empower is the Income and Expense tracking from all of my accounts. That’s why it’s so frustrating when there are big holes in the collection and reporting pieces.

Having been retired since 2000 and having been lucky with investments, including some money from my parents, I don’t really need the Investment analysis portion. I do actually work with Schwab’s Private Client group and find the 50bp charge to be manageable.

I thought you might like this little investing tidbit. In the 1980’s my mother was in a women’s investment club where she worked in a suburb of Seattle. In 1987 the advisor warned them to “watch out for this guy” -the guy was Bill Gates. They had never owned stock before but invested $10,000 in Microsoft in 1988 and always reinvested all income. In 2021 when my Dad died my mom got a step-up in basis and the stock was then worth over $5M. Today it is up an additional 66%. Washington state has an estate tax exemption of $2.193M and we put that amount of MSFT in trust for my mother. It is now worth $3.813M. In addition my mother has gifted MSFT stock to my 2 brother’s and I, our 5 children, and her 6 great-children. Is that not an amazing 4 generation legacy? My dad’s advisor at Schwab always wanted him to diversify and sell, but in addition to his other “Seattle stocks”-Costco, Starbucks, Boeing, & Amgen he just let them sit.

All the best. Keep up the great work that you do.

Karen

Do you invest in venture capital and venture debt using Fundrise? Do you have venture investments outside of Fundrise? I’ve not looked into Fundrise. Every time I’ve invested in private equity, it’s done poorly. I have a $100K in one fund right now where I think the fund manager may have absconded with the money–no reports or updates, a scant K-1 issued each year.

My kids are about to enter college. Their 529s are fully funded. I have 37% of my NW in real estate (not funds) including my primary residence. 59% in public traded equities. 4% in cash which now I’m thinking might be low if you’ve got 10% in cash. BTW my 4% cash includes short-term bonds.

I have minimal cash to invest because what I have may need to go into cash-in refi’s. I have one apartment loan that adjusted from 4.25% to 7% in October. I need to bring $65K to the table to get a loan at 5.3%. These are all ARMs. More refis are on the horizon. Lower interest rates cannot come soon enough.

I’m currently invested in three venture debt funds and five closed end traditional venture capital funds beyond Fundrise. Personally, I like to invest in these funds because they forced me to continue investing over their initial through your time. Period. I also don’t have to think about the money and trust that the general partners are looking for the best investment as possible.

As my absolute dollar amount invested in public equities gets larger, the swings get much larger as well, which can feel disturbing. So when my money is out of sight, it’s also out of mind and it provides relief.

It sounds like things are going well with you! Congrats!

I know you don’t write about commodities very much (?), but do you have any thoughts on silver being up 213.01% year over year? Is this being driven by demand (AI / datacenters), FOMO, dollar collapse, ? Is this cause for concern?

Good question. You’re right that I don’t focus much on commodities because they aren’t productive assets and don’t generate cash flow like stocks, real estate, or private investments. That said, a 213% year over year move in silver is eye catching. A large part of the rally appears to be driven by momentum, speculative flows, and narrative chasing rather than a sudden step change in fundamentals. Commodities, especially silver, tend to attract FOMO once prices break out because positioning and liquidity can amplify moves quickly.

There is real industrial demand for silver in electronics, solar, and potentially AI related infrastructure, but that demand is incremental, not exponential. It does not fully explain a 200%+ move in such a short time. At the same time, silver often trades as a leveraged play on gold when investors worry about inflation, currency debasement, or fiscal excess. When those macro narratives gain traction, silver can overshoot in both directions.

Is it a cause for concern? I’d say it’s something to be aware of, not something to panic over. Big commodity moves often mean higher volatility and a greater risk of mean reversion. For long term FIRE investors, silver works better as a small, speculative allocation or a trade rather than a core holding. I still prefer assets with cash flow and intrinsic value drivers, but sharp moves like this are a reminder of how quickly sentiment can shift when liquidity and psychology take over.

Thanks for the feedback!

You’re my favourite financial writer! I like how you did the math for all these life plans!

Thanks Lana! I appreciate you.

Hi, greetings from long time reader from eastern europe! I always value your optimistic pov and seeing bright side. How do you diversify or insure from geo risks for US?

I frequently hear comparisons to the situation in the late 90’s, with tech stocks potentially over-valued on the hype. To me there is a significant difference between that situation and what we may see in the near future. The dot-com bubble happened largely due to myriad startups with vaporware and no intrinsic value to offer. When the bubble burst, the equity that people had invested in these companies simply disappeared. This time, the “bubble” stocks are the likes of NVIDIA, Meta, Google, Microsoft, etc. Even if the AI bubble bursts spectacularly, these companies have other successful, profitable business lines that would keep them afloat. It’d be a significant loss for investors, but not a wipeout. Or am I just trying to convince myself that the risk is lower now?

Balance sheets and earnings are far stronger today than in the late 1990s. However, Meta still declined over 50% in 2022 alone.

So I would say the volatility is worse, faster, and more violent (March 2020 and March/April 2025).

Your comments about 2000-02 really resonated with me. It’s inevitable that a period like that returns. I started saving in late 2008 so I have not really experienced any meaningful prolonged downturn in the market. I have about $12.1mm now (95% of which is invested in public equities and 5% in real estate). 70% of the money is in the S&P and the remaining 30% is in 5 stocks (Google, Amazon, Apple, Berkshire, and my company stock). I have under $100k of cash and no bonds. Given the inevitable downturn in the market and losses I would experience in absolute terms given the size of my portfolio, how does someone like me manage this risk? The Simple Path to Wealth suggests letting it ride. Empower and other advisors suggest selling the index funds and buying 150+ individual stocks they can churn if prices fall and generate tax benefits. Thoughts?

Direct index investing works well but u have to add capital to it or its loses its utility over time (and therefor paying a higher AUM fee for the benefit)

With approximately 11.5M in stocks and only 100k in cash, if I was in your situation, I would be focused on asset reallocation. You have more than enough to live a very very cush life. I personally favor a dumbbell approach. I would sell some of the stocks and purchase treasuries and have that represent at 10-20% of your net worth. Then if there is a repeat of the financial crisis you’ll have a couple million that is secure no matter what happens and you’ll be primed to take advantage of a significant downturn. Plus, materially will your life change if you have 11.5M in stocks vs 9.5M? At those valuations, it’s just a number. You have won the game, at this point it’s more about asset protection than optimized accumulation.

11.5 is more than half way to 20mm. Sty focused

Diversification is key and there is always a bull market somewhere, so far this year dividend paying stocks have outperformed tech and growth stocks and if rates decline further they have more room to run.

The BBB bill legislation is going to have a big one time stimulus for consumers when massive refund checks arrive in the Spring. People have been overpaying on their taxes since the bill passed and those that did not adjust their withholding to reflect the new rates will receive a refund for those tax over payments. This is a one time thing, but it will help consumer discretionary stocks and maybe juice the markets a bit.

This might be a year when Mega cap tech under performs, but that is okay. I own a ton of stocks that aren’t tech that are undervalued. They will do well going forward.

It does feel like mega cap tech will underperform this year doesn’t it? I think the S&P 500 broadens out and banks and consumer discretionary may outperform.

Tax relief would be nice!

Top banks have a full IPO pipeline and M&A is back. Lower interest rates will create some interesting opportunities, but leverage will be back in vogue… so more risk for the return.

I wish I was back in banking and making banking money then! This year should be better than the last for M&A and IPOs.

I just played golf with a husband, whose wife is a Managing Director tech Banker. She is already secured $50 million in banking fees this year for her group. Not bad!

As someone in the industry, comp was good this year and expectations are favorable this year. And the deferreds have done well with the stock appreciating significantly….

Thanks for writing and sharing your investment thoughts. I certainly do hope that this will be an up year and I feel cautiously optimistic about that. I expect that my cash flow will be lower this year due to some personal changes. However, I still have a goal to pay closer attention to my allocation and increase its diversification.

I’m very heavy US equities and have a bunch of treasuries coming due next month. So I have a lot to think about between now and then on how I want to re-deploy that capital and possibly some of my long US exposure as well.