I might have made a significant error by disseminating incorrect information about what constitutes a top 1% net worth in America today. Over the years, I relied on data from the U.S. Survey Of Consumer Finances, released every three years by the Federal Reserve.

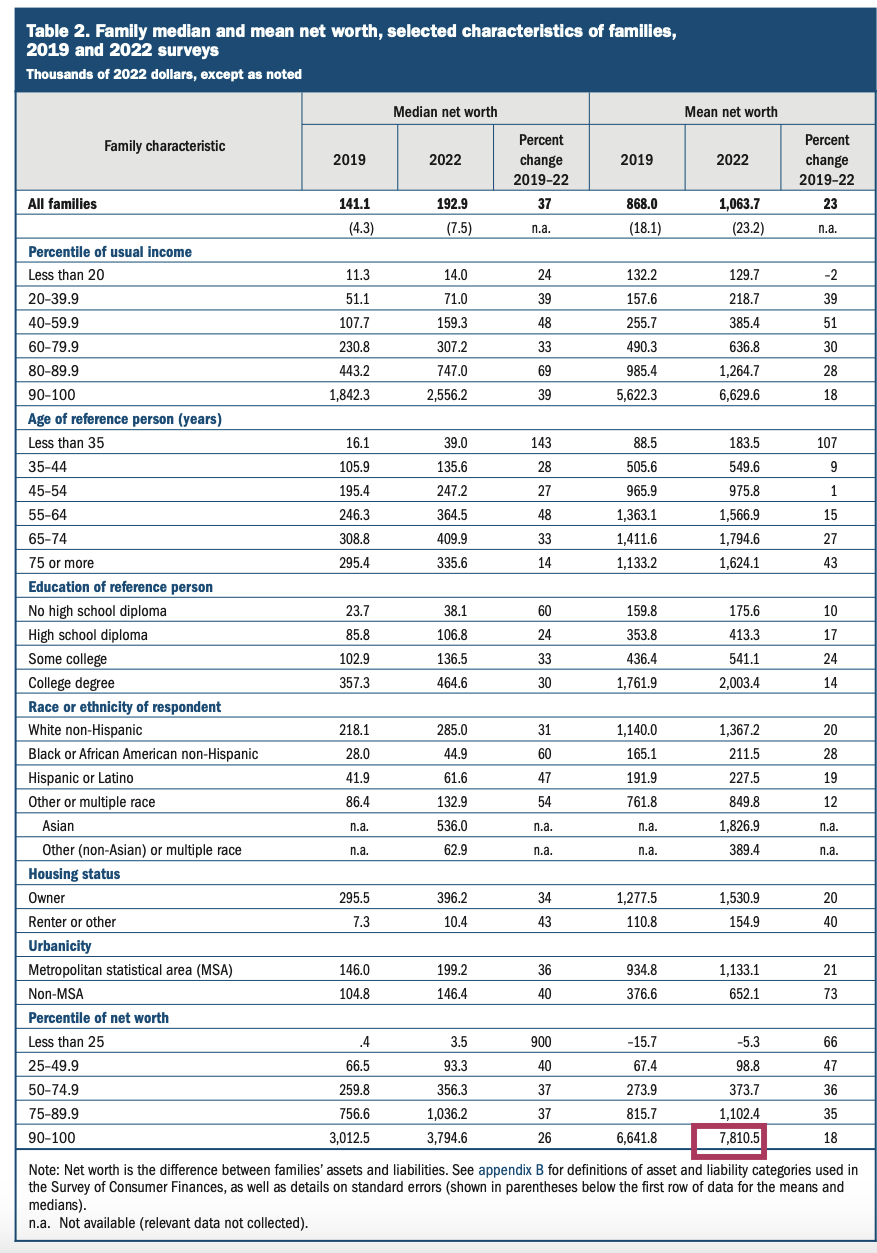

According to a 2023 Survey Of Consumer Finances, a household net worth in the top 10 percent in 2022 was approximately $7.8 million. Consequently, a top 1% net worth would exceed $13 million today.

I considered the data from the Federal Reserve as unquestionable, assuming they wouldn't provide false information. However, a report from Knight Frank, a global real estate research house, has now cast doubt on the Fed's numbers.

Diversify into real estate: If you want to get to a top 1% net worth, consider real estate, my favorite asset class to grow wealth. To invest in real estate without the burden of a mortgage or maintenance, check out Fundrise. With roughly $3 billion in assets under management and 350,000+ investors, Fundrise specializes in residential and industrial real estate. I’ve personally invested $400,000+ with Fundrise to generate more passive income. The investment minimum is only $10.

A Top 1% Net Worth In America According To Knight Frank

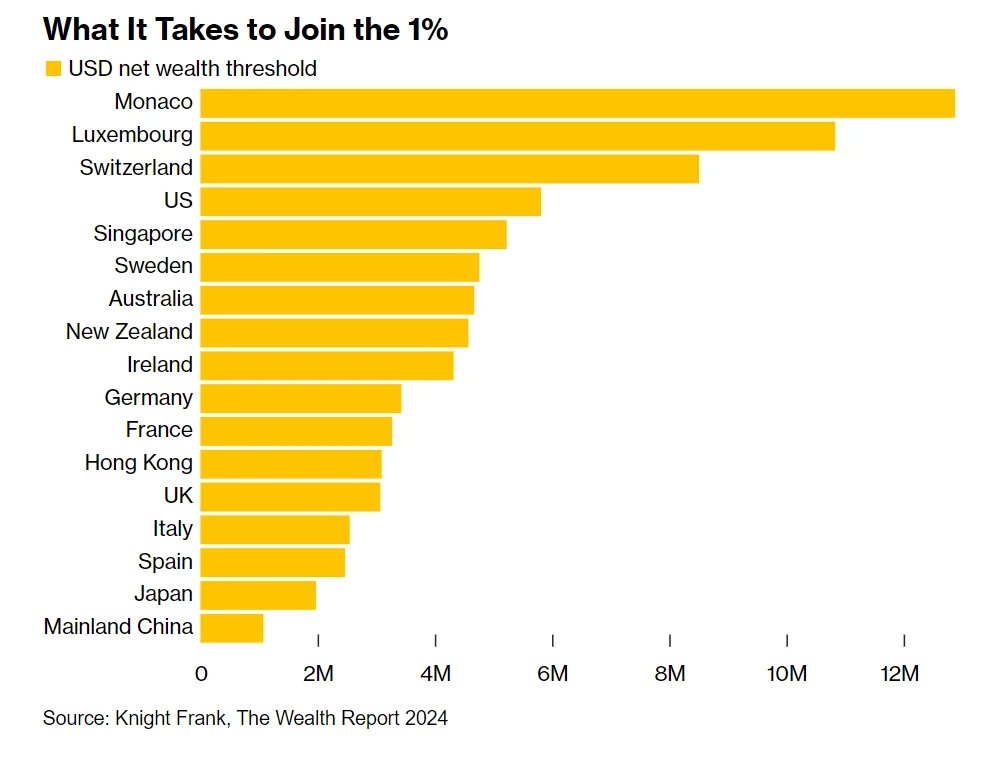

To hold a top 1% net worth in America, according to Knight Frank, a person in 2025 must have a net worth of at least $5.8 million. This amount is at least $7.2 million lower than what the Federal Reserve believes is required to be in the top 1% net worth in America.

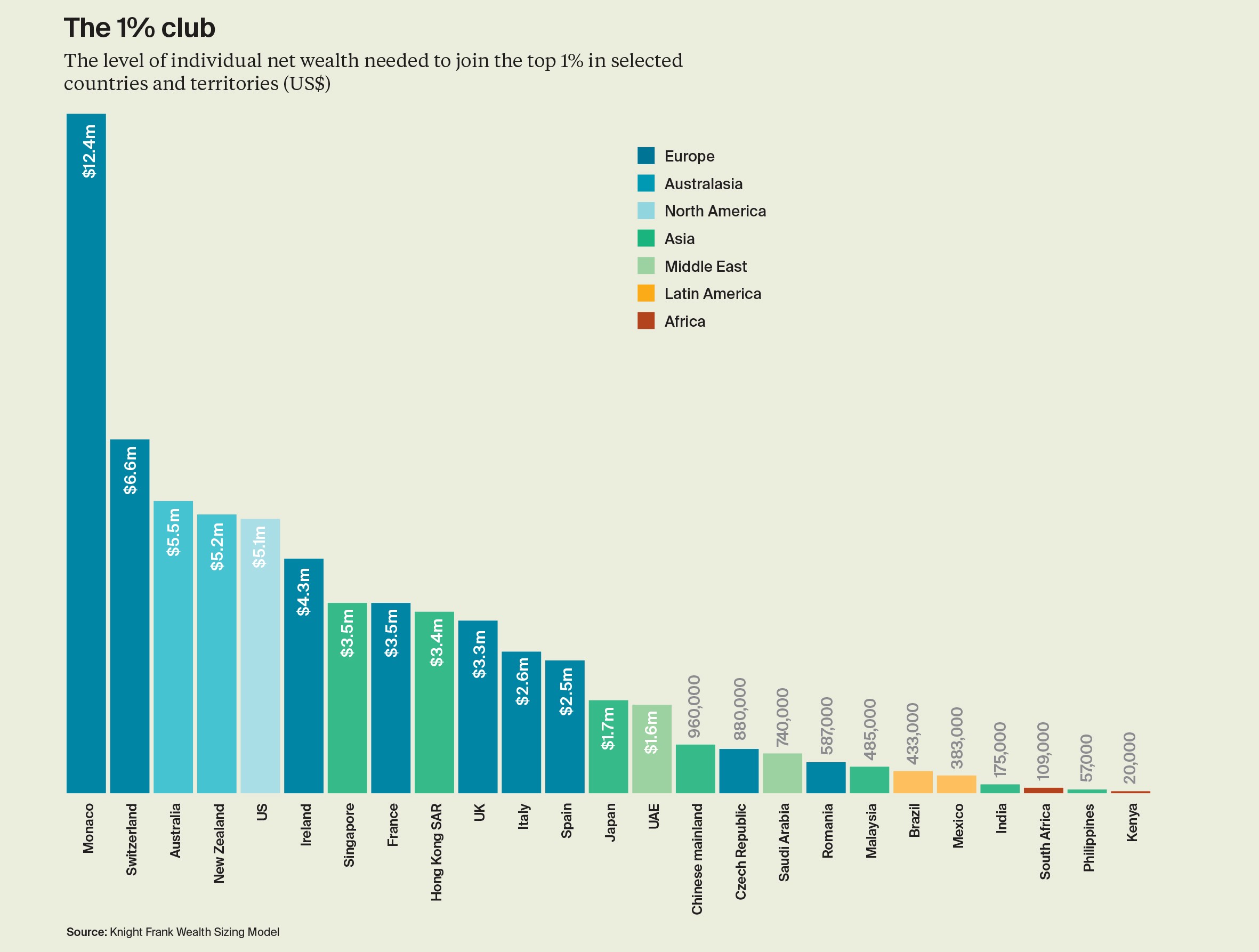

Here's Knight Frank's 2023 post and graph below on what it took to join the 1% net worth club around the world. It showed that in 2023, an American household would need a $5.1 million net worth or greater to be in the top one percent.

After seeing this data, I actually felt a huge sigh of relief! Any stress and anxiety I felt about needing to accumulate generational wealth to live comfortably in this ultra-competitive world went away. After all, I had left work in 2012 with a net worth of $3 million and it has grown along with the stock and real estate market.

I felt a similar level of relief when I read all the success stories from Financial Samurai community college graduates. No longer do I feel it is necessary for me to save $1.5 million for college for two.

A Commitment To Excellence In At Least One Thing

As a Financial Samurai, one of your goals is to strive to be in the top one percent of something, anything. Achieving a top one percent result brings an incredible amount of satisfaction given the amount of time and effort it took for you to get there.

This stretch goal doesn't necessarily have to be financially related; it can be related to sports, playing a musical instrument, earning an investment return, breaking a record, spending time with your children, or any other achievement. The goal is to push yourself to be the best at something for self-actualization purposes.

Although $5.8 million is still a lot of money to reach the top one percent in America, it sure is easier to obtain than $13+ million according to the Fed. There is now less of a need to hustle as hard, work as long, or save and invest as much if you aim to joint the ranks.

I explain the difference in the two numbers down below. Keep on reading.

Recommendation: If you have over $100,000 in investable assets, you can receive a free financial analysis from an Empower advisor by signing up here. An annual review is always worthwhile as your asset allocation can shift significantly over time, and your financial situation may evolve as well. We all have financial blindspots that are worth recognizing to build more future wealth.

Top One Percent Net Worth Levels Around The World

For 2024, Monaco retains the top spot for the highest threshold worldwide at $12.8 million ($12.4 million in 2023). I've never been to Monaco, but it appears small, nice, and perhaps a little boring. But not having to pay income taxes sounds great!

Luxembourg and Switzerland round out the top three, where one needs more than $8 million to make the cut. Switzerland's top one percent net worth threshold was only $6.6 million in 2023, so $8 million is a substantial increase.

Having been to Lucerne and Zurich in Switzerland before, I can attest that prices for food and shelter there are incredibly expensive. Prices were at least 25% more expensive than here in San Francisco, which is perennially considered one of the most expensive cities in America.

Seeing Australia and New Zealand in the top tier of countries with the highest net worth threshold is somewhat surprising. Both countries have strong retirement savings systems, and Australia has a lot of natural resources. However, I'm not sure how New Zealanders are so affluent and can afford some of the world's most expensive real estate.

Best Countries To International Geoarbitrage To Make Your Money Go Farther

Out of all the countries in the above graph, I would consider moving to Spain ($2.5M), Japan ($1.7M), Malaysia ($485K), Brazil ($433K), and The Philippines ($57K) to stretch my dollar farther. Living like a one percenter and raising a family with more financial flexibility than 99% of the population sounds appealing.

I lived in Kobe, Japan, for two years and cherished my time there. When I visit Japan, I appreciate the food, culture, cleanliness, safety, countryside, skiing, and hot springs. Besides Malaysia and Singapore, I'm not sure if there's a country in the world that prepares food better than Japan.

Having also lived in Kuala Lumpur, Malaysia, for four years, I found it to be hot and humid year-round, which may be too uncomfortable for many. However, food and housing costs are inexpensive, and the ocean-side resorts are fantastic. With a $1 million net worth, you can truly live well or spend $5,000 a month.

During business school at Berkeley, I had the time of my life studying abroad in Sao Paulo and Rio de Janeiro. The vibe in Rio felt joyful, with warm beaches, good food, lively dancing, and people who seemed to prioritize working to live.

Let's Appreciate How Good Americans Got It

Out of all the places I've visited and lived, I don't see a better country than America to build your fortune. If you're fortunate enough to live and work in America, seize the opportunity! You don't need a top one percent net worth to live a great life here.

We have a vast country brimming with possibilities. If we find one city or state less appealing, there's always the option to relocate to another. Technology has further empowered us to work for higher-paying companies while residing in more cost-effective cities. This ability to move is the main reason why I've been investing in heartland real estate since 2016.

If you want to accumulate a top one percent net worth, it's easier to do so in America than in Monaco, Australia, Switzerland, Luxembourg, and New Zealand, which have higher thresholds. These countries simply don't have the same number of job and business opportunities as we have in America.

Personally, I'm delighted to have arrived in America in 1991 for high school, pursued college, and had the chance to work in finance from 1999 to 2012. I'm even more grateful for being able to leverage the internet to pursue what I enjoy and generate supplemental income.

Who Should We Trust? The Fed Or Knight Frank To Determine Top 1% Net Worth?

It might seem logical to assume that the Federal Reserve possesses more trustworthy financial data on American citizens than Knight Frank, a property broker based in London, England.

However, could it be that the British have insights into American wealth that we don't? Knight Frank might also be less biased than the U.S. Federal Reserve. Or, Knight Frank might be more biased in order to make the British look relatively less poor than the Americans.

Household Wealth vs. Individual Wealth As The Difference Perhaps

Perhaps the difference in top one percent figures lies in the Federal Reserve calculating the net worth of families, whereas Knight Frank calculates the net worth of individuals. After all, two individuals generally have a larger combined net worth than one individual. If a family consists of more than two individuals working from the Fed’s perspective, then the discrepancy between the data would be even larger.

The thing is, very rarely is it 1 + 1 = 2 when it comes to calculating a top one percent net worth. For Knight Frank's top one percent net worth threshold to double from $5.8 million to $11.6 million to more closely match the Federal Reserve's estimate, a person with a top one percent net worth must also marry another person with a top one percent net worth. It happens, but clearly, it's only a small minority of cases.

Alternatively, it's possible that the Federal Reserve reports inflated figures to make more Americans feel insufficient about their financial status. By creating a perception of being poorer than we really are, the Fed could encourage more Americans to work harder and longer, generating more tax revenue.

Personally, I believe in the Fed more given I'm American. In addition, to leave no doubt about obtaining a top 1% net worth, how about shoot for a $20 million net worth!

Best Way To Build A Top One Percent Net Worth

Achieving a top one percent net worth is best accomplished through:

- Entrepreneurship

- Building a real estate portfolio with leverage

- Investing in stocks that dramatically outperform the S&P 500

- Investing in private growth companies that turn out to be multi-baggers

- Working at a high-paying job and saving and investing the majority of your money for decades

- Getting regularly financial checkups by a financial professional who can help you optimize your investments

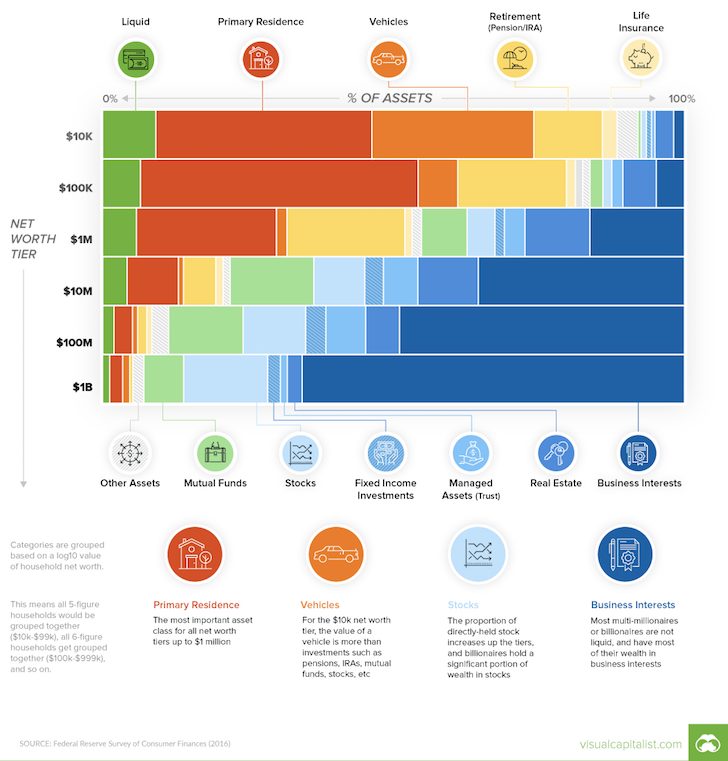

The wealthiest people in the world are almost exclusively entrepreneurs. They took outsized risks, resulting in outsized wealth. While investing in stocks, bonds, and other risk assets contributes to wealth-building, these investments are unlikely to propel you to a top one percent net worth.

To reach the top one percent, you must dramatically outperform the vast majority. This can be achieved through a combination of having a high income, aggressive saving and investing, time, and a willingness to take more risks.

The richest people I know didn't get rich by investing in index funds. Instead, once they got rich, then they invested in index funds as a way to preserve capital.

Below is a chart that shows the net worth allocation by level of wealth. Notice how the richer the individual gets, the greater the percentage of their wealth they have in business interests. This means equity in a public or private company.

The Real Top One Percent Net Worth Threshold In America

For those of you really tuned into personal finance, I suspect your gut instinct tells you that Knight Frank's $5.8 million top one percent threshold in America is too low. After all, the average American household is now a millionaire, although the median net worth is only about $200,000.

So what's the solution since nobody can really say for certain what is the exact threshold to be in the top one percent?

Like most conflicts, compromise is necessary. Therefore, I propose averaging the ongoing top net worth figures from both institutions to arrive at a truer top one percent net worth threshold figure in America.

For 2025, based on the average of the Federal Reserve's data and Knight Frank's data, the top one percent net worth in America begins at about $9.7 million. If you prefer, round up the figure up to $10 million, the ideal net worth to retire with according to thousands of FS readers.

$10+ million for a top one percent net worth in America sounds about right. Best of luck on getting richer than 99% of your fellow citizens. If you get there be sure to share what it's like!

Reader Questions

Why do you think there's such a discrepancy between the top one percent net worth thresholds reported by the Federal Reserve and Knight Frank? Who do you believe and why? What do you think is a top one percent net worth in America? Which countries would you be willing to relocate to for a wealthier life?

Free Financial Analysis Offer From Empower

If you have over $100,000 in investable assets—whether in savings, taxable accounts, 401(k)s, or IRAs—you can get a free financial check-up from an Empower financial professional by signing up here. It’s a no-obligation way to have a seasoned expert, who builds and analyzes portfolios for a living, review your finances.

A fresh set of eyes could uncover hidden fees, inefficient allocations, or opportunities to optimize—giving you greater clarity and confidence in your financial plan. Those who have a top 1% net worth regularly get financial checkups from a financial professional every quarter in order to optimize their finances.

I’ve been using Empower’s free financial tools and speaking with their financial professionals since 2012. From 2013 to 2015, I also consulted part-time at their offices when they were still called Personal Capital. As both a longtime user and affiliate partner, I’m genuinely pleased with the value they’ve consistently delivered over the years. My current net worth is in the multiple eight-figures and I get annual financial checkups.

The statement is provided to you by Financial Samurai (“Promoter”) who has entered into a written referral agreement with Empower Advisory Group, LLC (“EAG”). Click here to learn more.

Invest Like The Top 1%

The wealthiest people in the world own equity in their own business and equity in other businesses. Index fund investing is a tried and true way to build wealth over time. But it's hard to outperform the masses who invest in index funds.

If you want to outperform, consider investing some of your capital toward private investments that can potentially offer more upside. Private companies are staying private for longer, which dictates investing more of your capital toward private companies to capture more of the upside.

Check out Fundrise Venture, which invests in private companies in the following five sectors:

- Artificial Intelligence & Machine Learning

- Modern Data Infrastructure

- Development Operations (DevOps)

- Financial Technology (FinTech)

- Real Estate & Property Technology (PropTech)

Roughly 65% is invested in artificial intelligence, which I'm bullish about. In 20 years, I don't want my kids wondering why I didn't invest in AI or work in AI.

The investment minimum is also only $10. Most venture capital funds have a $250,000+ minimum. You can see what Fundrise is holding before deciding to invest and how much. Traditional venture capital funds require capital commitment first and then hope the general partners will find great investments.

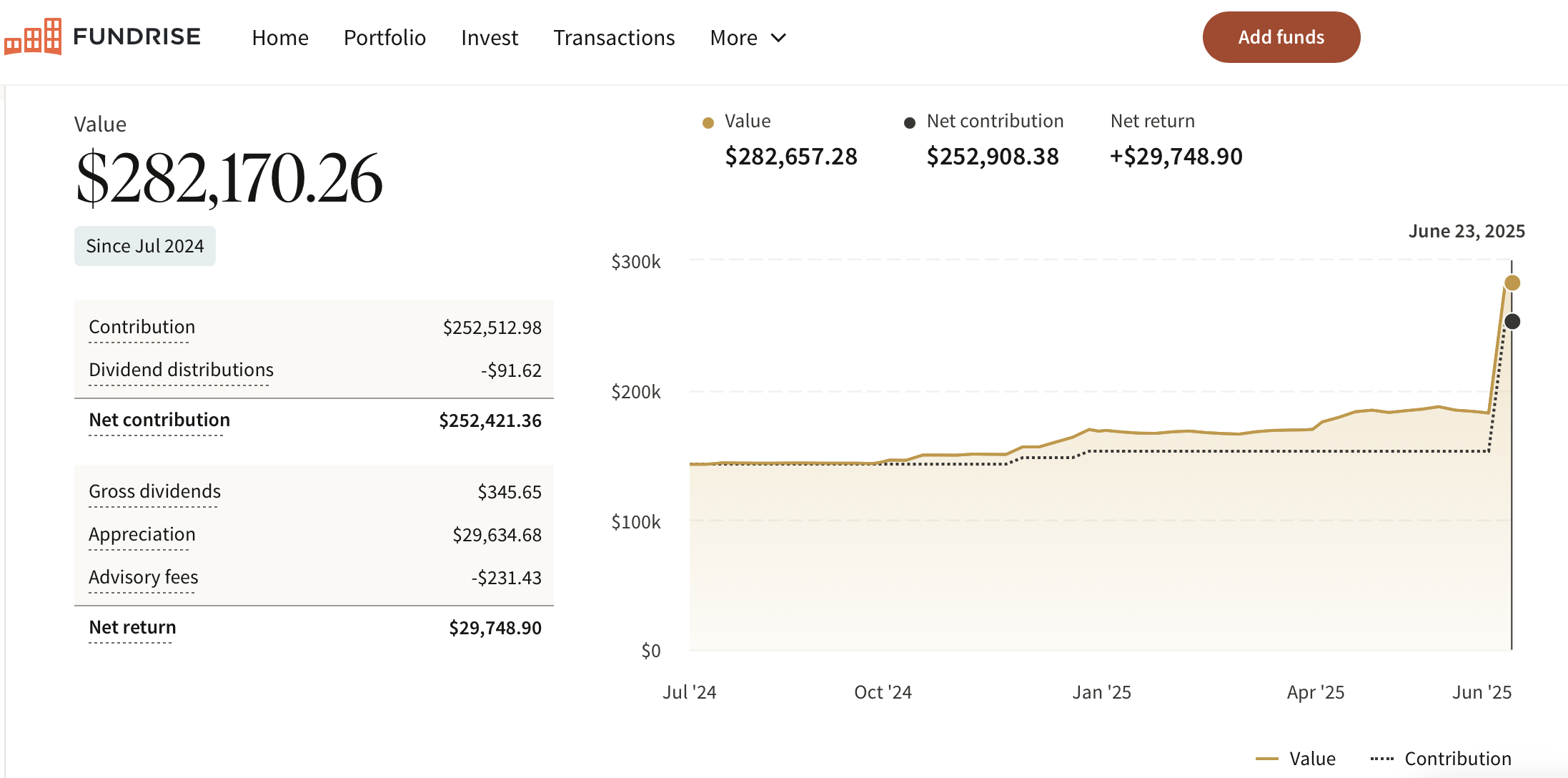

I have invested over $280,000 in the Fundrise venture product as I strive to build a $500,000 position in private AI companies. Fundrise is also a long-time sponsor as our views are aligned in real estate and venture. Below is my Fundrise Venture investment dashboard where I invested another $100,000 in mid-2025.

Order My New USA TODAY Bestseller: Millionaire Milestones

If you’re ready to build more wealth than 90% of the population, grab a copy of my new book, Millionaire Milestones: Simple Steps to Seven Figures. With over 30 years of experience working in, studying, and writing about finance, I’ve distilled everything I know into this practical guide to help you achieve financial success.

Here’s the truth: life gets better when you have money. Financial security gives you the freedom to live on your terms and the peace of mind that your children and loved ones are taken care of.

Millionaire Milestones is your roadmap to building the wealth you need to live the life you’ve always dreamed of. Order your copy today and take the first step toward the financial future you deserve!

Obtaining A Top 1% Net Worth Is Easier Than Ever is a Financial Samurai original post. All rights reserved. I started Financial Samurai in 2009 and it is the leading personal finance website today with over 1 million pageviews a month. Everything is written based off firsthand experience and knowledge. Subscribe to my free weekly newsletter if you want to achieve financial freedom sooner.

Sam, Please consider that the Fed table refers to a “mean” (average) whereas the Knight table ie the entry point (minimum) – these are not remotely comparable. Even the median (50/50 population split) will be well above the entry point. Either I am missing something here or your math is way off.

For those saying that you must need $10 million to be top 1% in the US – are you all from California or Greenwich? Go to the Midwest, southeast, Vermont, etc. – or even western California or New York – and your reality will be reset!

Agree how much does just one Bill Gates household pull up the mean

Bill Gates increases the average not the mean.

Average and mean are the same thing. Median is different.

I’m also confused how one arrives at 13M from the mean of 90-100 being 7.8M. There shouldn’t be enough info to do this.

Having said that: the median of 90-100, p95 = 3.7M, so 5.8M seems kind of low for p99, if you plotted p85, p75, etc, and tried to fit p99, I bet its higher than 5.8M.

Also note that the Knight Report defines HNWI as “… someone with a net worth of US$1 million or more, including their primary residence.” Most definitions count only liquid assets, not non-liquid, like real estate. So there’s some caveats, parsing, and pivoting needed when comparing tangerines and oranges.

My guess is both numbers are right. US Census is about 13.66 million for top 1% for a household, which on average is 2.51 people. Knight is for an adult 5.8 miilion. So majority of the 131 million households have two adults and then kids. So Knight calculated all the net worth for all the households with two adults, and divided by two. then obviously the single household units left as whole. And just leaving off any children.

Perhaps. Nobody will ever know for sure. And there’s still a $2 million gap if you double $5.8 million to the US Census threshold.

I’m impressed if people with top 1% net worths only marry others with top 1% net worths.

The massive variation in top1% figures is indeed frustrating. My best guess is 5.6 gets you in the door and 16.7 million is the average 1% net worth. I suspect the mean 1% would be closer to 8-9 with massive estates pushing the average figure much higher than mean. I wish someone would nail this down

If you’d like to read a more scholarly and in-depth examination of the different means of computing the wealth threshold for the top 1%, I recommend https://economics.princeton.edu/working-papers/top-wealth-in-america-new-estimates-under-heterogenous-returns/

The data is a few years old but the article is illuminating. It comes up with an even lower threshold for the top 1 percent — closer to $4M (when factoring in recent inflation since the data for the study is a little outdated now). As the paper puts it:

“[Prior to this paper, there were] three main approaches for estimating top wealth. The first approach combines estate tax data and mortality statistics to map the wealth of decedents to estimates for the wealth of the living. The second approach uses surveys such as the Federal Reserve’s Survey of Consumer Finances. The third approach scales up, or “capitalizes,” income observed on tax returns to estimate top wealth.”

The paper proposes a 4th method that is arguably similar to the third approach listed above, using administrative tax data, along with well-founded estimates of income rates and pass through business returns, along with some sophisticated analysis of rates of return. In some subsequent back-and-forth I found online, critics of the paper have said that the Survey of Consumer Finances must be more accurate because its an actual survey rather than theory. But the authors have pointed out the the flaws in the survey methodology and the problems with getting accurate samples of the top few percent of wealthy Americans.

Personally, like you, I suspect the truth is somewhere closer to an average of the survey and the other methodologies, which all result in significantly lower thresholds.

I think the boring route of being a professional but saving well offers a better outcome than the CPA calculates. I started as a lawyer at $68,000 at age 25 and still only earned about $135,000 by the time I was 35, $250,000 by 40.

Pretty modest. (I married around 39, but my wife never contributed much due to lower income, plus then having a child.) But I always lived as if my income would peak in the current year, whereas many people spend as if they are on a big upward curve. If the upside happens, save it. I maxed my 401k every year starting at 25.

I made a risky career change and it worked out well, so my income doubled at about age 45. For about 8 years I made $850K-$1.1M annually, but I saved most of the net increase. That body of savings was enough to jump net worth from $2.5M to $7.5M by 2017/age 53, about $6.5M of that investable (the rest house). Then health reasons and career reasons cut my income a lot — but basic S&P500 type equity exposure (plus some pure tech) has brought me to about $9M invested and $2M in one house, at age 60. I still work part time, but I am letting it trail off.

There is nothing miraculous in that trajectory, just never letting expenses grow as my income did.

We have one son in college. I understand the impulse of people NOT to give any money to children–I have never been given anything, BTW. But it came with stress, so I would like to de-stress my son by helping him into a long-term house once he is working. He will ultimately inherit our estate, and I would like him to learn how to appreciate and manage assets.

I had a heart valve defect, which they fixed when I was 55. No big deal. But 2 years ago I was diagnosed with a slow form of leukemia. I’m 60 now. So to your remarks about fear of dying, I need to be prepared to die in the next 5 years. Could be 30, could be 1. Let’s say 10. It does focus one’s mind. I think by the time I die, say in 5-10 years, my wife can be sitting on $15-20M investable.

And finally, on what makes one wealthy? Knowing that you can live comfortably off investments for the rest of your life seems like a good definition. $10M seems good. I think of downsides. What if I need expensive nursing care of $20K a month? At the same time as the market drops. What if my wife needs care, too? $10M should be enough for that, but honestly barely. I feel like we would be bulletproof at more like $15M, so we could spend on care for me without endangering my wife’s ability to live another 30 years after I die.

I know it seems like a bummer to think about death, but it will happen. In the grand scheme, I am very proud of my financial success. I worked hard and stressed a lot, planning and protecting assets. I know it’s an achievement, even though people in the broader society mock and distrust people with wealth.

Some of my many siblings resent me for my success (they can only guess at my wealth, I think they underestimate). We literally grew up in the same busy house, same parents, same food, same shared clothes; and yet I focused better in school and worked 6-7 days a week for 30 years, enduring the stress it takes to make some career leaps and earn well. It’s basically jealousy.

Even my mother, who has a nice stable pension from my dad’s work and her teacher job, and lives as well as she ever has at age 90, is kind of bitchy about me having money. It’s odd that she isn’t proud of my success. But I am proud, so there.

At this point in my life, and to some extent influenced by my failing health, I really don’t have the time for negativity, so I’m afraid I don’t interact much with people who are snarky about my money. I don’t need it. I am focused on enjoying experiences with my son and wife while I’m still alive. Nice international adventures with my teen son. As we all know, money makes those experiences much easier and nicer!

Thanks for sharing! What was the risky career leap that got you to $1 million a year for 8 years?

I hope you will live a much longer life than 5-10 years. Does this prospect make you want to stop working part-time and spend a lot more money since you have so much?

I have a fear of dying with too much, so I took a leap of faith and bought a forever home in 2H2023 that we didn’t need. It cost us a lot of passive income, but it’s my way of decumulating and providing a nice life for my family at age 47 now.

Do you and your wife have life insurance policies? My wife and I got matching 20-year term policies through PolicyGenius in 2022, and felt a huge sigh of relief after. At least we know our kids will be taken care of until their early-to-mid 20s.

I quit my law firm without knowing whether any clients would follow me. Lawyers are not allowed to ask clients in advance, ethically (it is an act of disloyalty and damages the partnership in which you are still a partner), so I didn’t ask until I had resigned. I took the leap and they all followed, and I ended up with more business than I expected, at a profitable place with no legacy costs etc. So that’s where the money came from.

The prospect of dying does make me want to spend money. We decided in a snap move to sell our Chicago house and buy a much nicer house near Seattle. Part of the driver in my head was to move fast while things are still fun. A $2M house definitely takes some money off the table, but it’s a better long-term play on appreciation than Chicago real estate, and we get a nice place to live in the woods with a creek. And closer to my son in college.

I had lots of life insurance when I was younger, but there’s just no way my family will need more money than we have. Plus I was still on board with insurance when my existing insurer denied an increase because of my heart surgery about 5 years ago (my fixed valve), and the agent didn’t really seem to have a plan to seek alternative capacity, and just seemed focused on losing his huge commission. He got all paranoid about whether somebody had “gotten to me” about life insurance. And so I decided fine, I don’t really need the insurance. The investment aspect of my old whole policy was never a good idea.

I could live another 30 years, but my brother died at about my current age from the same cancer. He had other cancers, too, so I’m much better off, but it is still a bit raw. Most of my family doesn’t know my diagnosis because it is too real, too soon. Thanks for your wellwishes and your website.

Bless you my friend. I’m glad you are a great success and that you are able to take care of your family no matter what happens.

Great story. I am pretty much financially and age wise where you are, though just pushing the $10M mark. I agree that $10M makes you comfortable (at least in my area of non-Gold Coast Connecticut) but not ‘rich’. Certainly not bulletproof. I think bulletproof would be somewhere around $20-25M around here.

By the way, when I told my mother what my net worth was a few years ago, she was estatic. She exclaimed “Oh my god, I did it!’ (referring to herself, lol). I grew up in a middle class household and we were probably poorer that most of my friends and our neighbors. My mom always saw it has her mission to give us the tools to be successful, and me telling her that validated all of the work she put in when raising us.

That’s awesome. Good for you. That’s what parents should say! I sure want to see my son thrive, and I’d be happy if he has more money than I do. I could see my mother-in-law asking our net worth (we’ve never told her), and she would be proud of her daughter. My wife’s parents worked hard and saved to have about $2M, both starting poor. My mother-in-law would be so happy to know her daughter is well cared for.

Great story of your life and career. I admire your achievements and your attitude and agree wholeheartedly with you. I have managed to accumulate approx. 3.5M net worth at age 58, mostly through hard work and living well within my means. I am looking to retire comfortably in the near term and hopefully live a long and fulfilling retirement doing what I want/when I want/ with the people I want to be with. Best wishes with your condition and I hope you have many more years to enjoy the fruits of your labors.

Oh good grief, there is no way a net worth of only $5.8M puts one in the top 1% in the US. Not. even. close. You best go back to believing the federal reserve numbers.

Let Knight Frank know! Cheers

I’ve also always relied on the Survey of Consumer Finances to track my net worth. However, I have never been able to track down a reliable source of information that breaks down Net Worth Percentiles by state. There are several sources that provide average NW by state, but nothing like the percentile calculator that the Treasury data provides. Are you aware of any sources that break the data down by state?

$5.8M seems way too low for the U.S.. Heck, the average diligent two-income W-2 earner family can amass $2-3 million in their 401ks and home equity by their 50s without breaking a sweat these days. But if that $5.8M number is correct, then 1% means nothing anymore: even if you managed your $5.8 million well, you’d still need to live a middle-class lifestyle to preserve your wealth.

Without breaking a sweat as a stretch. I think you highly overestimate the median net worth in America, which was $192,000, as of 2022, according to the survey of consumer finances.

I have a net worth just north of $6M in my early 60s. I don’t consider myself rich at all, and no where near 1%!!. I live a mid middle class lifestyle and will need to continue to do so so I don’t run out of $. $5.8 really is not much these days. Good grief.

Hi Harry, sorry things are tight for you with a $6 million net worth in your 60s.

Keep fighting the good fight and hang in until Social Security!

If you can share more of your struggles, I’d love to hear more.

Related: Why $5 Million Is Barely Enough To Retire Early With A Family

The number you boxed in the first image is **mean** net worth of top 10% family, which says nothing about the minimum networth of top 1% or 10% households. Using median in the chart (top 5%), which is less than 4mn, indicates that the 13mn estimate may be too high.

The way I read the different studies is that you need $5.8 million to be in the top 1% worldwide and $13 million to be in the top 1% in the USA.

Not according to Knight Frank, hence on the number seems off.

I have always wondered if the net worth numbers for top 1% includes the equity in the house. If so, then for bay area needing a net worth of 13.4M is not surprising given the house prices in this area.

Can you confirm if the equity in the primary residence should be included to calculate ones net worth?

The equity in a primary residence is included. Because it is fungible.

Net of the mortgage liability

I’m 60 years old and married with 1 child in college. No debts and around $10.7M net worth. $9.3 million in savings and retirement accounts, all in treasuries earning 5.2% annually. I have two homes, one a city loft and the other a home in a vacation town a few hours away by car that are both paid off with HELOCs ($0 balance), so I can access available equity if I ever decide to take advantage of any opportunity that presents itself. Value of real estate combined is about $1.2M. The rest of net worth (approximately $200k) is in some hard assets. My daughter was a national merit finalist, so she had a couple of full ride options to colleges but got in to an Ivy League School, so I opted to splurge and do full pay. She has 3 more years to go. I am winding down my business and will pull another $1-3M out of it over the next few years.

I am considering selling both homes and moving overseas to a country like Malaysia (Penang). If assets are throwing off around $480-500k per year, then I could rent a really nice penthouse with a private pool, etc. for around $3-3,500 per month, with really low food and other costs, and lots of travel and entertainment options. English is spoken widely, it’s safer than living in a big city in the US and cost of living is really low. Thus, a very high standard of living, while never touching principal and rolling some of the money back into investments. The other option would be to stay put with my two properties and live off of interest, but it would be more expensive than Malaysia. The only issue I would have is health care, where I will qualify for medicare in the US in under 5 years, where it would probably be challenging to get good health care in Malaysia after 60. The cost is much lower for health care in Malaysia, but if any serious health issue arose, it might be more advantageous to head back to the US.

I really like the idea of going to another country where the cost of living is low and standard of living is high. You are effectively getting 3-5 times for your money. At retirement age, why keep working to try to earn another 3-4 million and take all of the risk, when you go move to another country where your 10-11M is worth 50M? Has anyone here tried this, and if so, how did it work out?

I am similar to you in regards to NW, income and age. Most of it came from a career in finance out in Asia coupled with good investment gains. I lived in Asia solely for 27 years but for the last ten years I have done a roughly 50/50 split of time between the US and Thailand. I have a real estate company there. I have homes in both locales. The one thing I will tell you is that I feel about ten times wealthier when I am in Thailand compared to when I am in the US. I think it is predominantly down to the comparison effect. We tend to compare ourselves to those in our immediate vicinity.

In regards to healthcare, the quality of care I get in Thailand is light years better than what I have experienced in the US. I do carry international health insurance with a high deductible but the cost of care is so much cheaper there that I never meet the annual deductible. I would probably consider the USA if I ever needed highly specialized treatment such as for oncology but for routine care I always get things looked after when I am overseas. It is a much more pleasant experience.

One thing you have to think about if you consider such a move is potential culture shock. It can stressful adjusting to a new culture and to a new locale where you do not know anyone to begin with. However, it can be adventure filled OTOH. With your resources, however, you could take it slowly at first. You could keep your place back in the US and rent a place for a few months out in Asia to test it out. You can do a gradual transition.

$9.8M sounds about right.

My wife and I are 34.

I became a liquid millionaire at 20 starting my second company that I own to this day. I have not yet exited [turned down all offers to date… sometimes a whoops statement though on the long arc, my reason was to learn and be challenged more], though I hope to exit in the next 1-2 years. My liquid net worth is $4.2M (90%+ is after-tax) excluding the value of my company that I own the majority of. In my mid to late 20s, I had to execute a massive pivot and that resulted in some “time lost” as I spent many many millions of dollars a year to execute it rather than take any profits and drew down some of my personal savings in the meantime. I also didn’t invest much of my saved up cash until the pandemic crash [just didn’t know how, then learned and now manage my own portfolio very happily – turns out I love investing/finance], which resulted in muted returns outside of my company.

My wife now makes around $400-$500k/yr in medicine so she’s been a great steady stream/stability to my craziness [absolutely huge years followed by sometimes terrible years], especially when combined with our dividend/passive income and my company income.

While I am not a “huge spender” (I guess some would disagree :D), I have enjoyed my life all the way through. I don’t fly private, or even first/biz class often, but I do what I want, when I want, how I want. I now live in my dream city in SoCal, which was a dream not too long ago. So I’ve probably paid a few million bucks in taxes, spent a few million dollars [including taking care of my parents/family and helping them ditch a poor quality business for a far higher quality cash flowing business doubling their income since], and saved up these few million.

I feel very well off, as I believe my actual total net worth is something greater and even if my company were to die in flames tomorrow, I have learned so much that building something new and getting back to where I was and then some seems very probable. I also feel very well off as I’ve always had full control of my schedule. Yes, I’ve worked stupid amounts at different points in my career and dealt with beyond insane acute stress at intervals, but 70% of my career has been sub 40 hours a week. So, quality of life has been very high, even though I’ve likely left plenty of money on the table doing this.

While I’d like to see my liquid net worth (ex my company concentration) grow into the 8 figure range, I don’t think I’d change my lifestyle much from here outside of buying our third home and renting our first (already) and second (to be rented) out. There is not much else I desire financially anymore, nor do I plan to leave anything significant for our future children. I grew up lower middle class with my immigrant parents, and I want my children to carry a fire that the utmost financial security simply can’t provide them.

True rich though? That’s probably something pretty up there – maybe $50M? I just don’t desire it. If it happens, cool.

Having a wife who earns $500K a year is huge! Congrats. No need for you to grind so hard.

Alas, my wife doesn’t have a day job since 2025 and refuses to go back to work, so all the responsibility is on me.

If you have kids, you might feel the need to accumulate a lot more wealth.

It helps a ton! I usually out earn her 1.5-2x in any given year, but 2023 was a bad year for me and 2024 is a recovery year that might just end up really stellar. I’m quite grateful that there is no pressure. That allows our yearly income to generally be above the 7 figure range when optimized, or a bad year like 2023 is still about 650k with her income, our passive/dividend income, and 0 company income.

We are saving at a pretty rapid clip nowadays since I really tightened up our budgets in recent years just to accelerate wealth accumulation and invest.

Selling my company may also bring a decent windfall so we are primed to end up with a 20-30M net worth if we don’t blow it out of the park in 10-15 years. If we do manage to do decently better than we expect (such as the company I’m hoping to start next actually takes off), 30-50M seems reasonable! Not for sharing with our future kids though.

Difference between the 2 data set: median vs mean. Numbers are approx. the same for the first 9 quintiles, only in the last (highest) quintile they differ. This is driven by the spread of wealth in this quintal, skewing the mean. Hope this helps to explain the difference.

Net worth in the survey conducted by the Federal Reserve is measured by an economic unit designated as family. If this parameter is given a similar definition by the Census Bureau, it would appear that the survey gauges the wealth of the population sector with the highest income. The census for 2022 reported the following median incomes:

• All households $74,580

• Family households $95,450

• Nonfamily households $45,440

Of note, results from research aimed at measuring the strength of the correlation between income and net worth are somewhat inconclusive.

Your estimate of $9.7 million is corroborated by the World Inequality Database. As of 2022, Piketty determined that the 1% of equal-split adults (definition provided in portal) with the highest net worth held at least $4.89 million. Assuming that the typical family household comprises two such individuals, the economic unit would own more than $9.8 million.

Sounds good. But the doubling of net worth by combining two individuals only really works of both individuals have top 1% net worths.

We are in our early 60s, and I retired 3 years ago but my spouse is till working and making great money. We both came from lower middle income immagrant families with parents knew nothing about investing.

We are lucky to have professional jobs, and have never worked in banking or high tech, just two w-2 employees for 30+ years in private sector and we are not even good investors and didn’t start investing until in our late 40s. However, we are very frugal and lucky to have been able to achieve financial freedom and are considered UHNW given our net worth as of 12/31/2023.

We live very modestly, drive two 10+ year old Japanese cars, live in a house bought 30 years ago in Bay Area. It is difficult to change our mind set to go from being frugal to lavish live style. We have continued to shop at Costco, Walmart and Target.

We are concerned that we have continued to save too much (55-65%) and really need to spend our hard earned money but we don’t have much material needs these days. Our kids are grown and have professional jobs, and we will help them to purchase their first homes and fund our grandchildren’s (none yet) education when time comes.

We are very fortunate to have accumulated what we have even though we never though it was possible. Live within your means, and continue to save and invest will get you to your financial goal. In addition, having a right life partner definitely helps to achieve the financial goal much more possible.

Thanks for sharing. Can you share your estimated net worth and what you plan to do with any money left over?

We have over $36m+ as of 12/31/2023, and my financial goal is to get to $42m when my husband retires in the next 3 years. Do we need this much? Absoluately not given our life style!

We will be able to live off our passive income once my husband retires, and I don’t expect to touch our assets for a very long time if ever.

We will gift some money to our siblings and also donate a portion to the charities with our estate when time comes.

Wow! That’s huge. I’d love to know how you were able to get to such a high net worth after only starting investing in your 40s. What exactly did you guys do for a living and how much did you make? Getting some numbers and understanding some math going from not much money into over $36 million net worth in 20 years would be very helpful to understand.

Given the amount of frugality, can I assume that both of you really love your jobs? Because I think most people will start to take things down after $10 million if they don’t really love their jobs.

If you have kids, how do you think about giving money to them to help them out while they are most in need and you are still alive?

Thanks for any color you might provide. I have a fear of dying too much and initiated my decumulation phase in 2023 at the age of 45.

Wow! I want to know also Michelle! To accumulate that much without being business owners?? Good for you. You must have saved every penny of your extra income for years!

Our 2024 Net Worth (As of Jan-2024) was around $15M w/investments mostly in blue chip companies. As to what it feels like to be within the top 1%, I’d say nothing special. We lead a normal life (just like millions of American citizens) and shop at stores like Walmart, Home Depot, Rei and pretty much anything in between. However, we avoid spending money on what we consider unnecessary, particularly in entertainment industry (concerts, sporting events, etc.) and the so called charities that use emotional based advertising to deepen their own pockets (St. Jude, Shriners Children, Wounded Warriors, etc.). We do however support our local communities.

Thanks for the feedback. Maybe the age of attaining a top1% net worth has something to do with it too. More exciting achieving 1% when younger than older perhaps.

How old are you?

62

Cool, at 62, are you concerned with dying with too much? This is my concern at 46, which is part of the reason why I bought a nicer house last year. I feel like dying with more than $5 million feels like a waste of time, energy, and stress from when we were younger.

Not really. We have already decided that ALL of our assets will be left for wild life around the globe… and whether we leave $5M or $50M upon our exit, it really doesn’t concern us. We’ve been on all the continents during our multiple foreign assignments… so we have kind of “been there… done that”. Right now, we are happy and content with our life style and really don’t see the need to keep spending for the “sake” of spending…

That’s good. If you have children, what are your thoughts on giving money to them?

Is there a net worth target you’re shooting for before finally calling it quits?

We are “DINKS”… too career oriented! Our company moved us every three to four years so we didn’t focus on have a family as our constant move would have been hard on the kids. Though we didn’t get to have kids, we were enriched with many cultures around the world.

As for the net worth target, nothing in the works in terms of our goal, but suffice to state that our Net “effective” growth is around 10%.

When did you live in Kobe? I happened to live there from 1990-1993 during my high school years.

Now that I live in the SF Bay Area, I wonder what threshold is needed for 1% wealth in this region.

1983 for two years when I was six. My gosh, it was the same age that my son is now and I remember a lot of my time there. I need to take him traveling!

For SF Bay Area, I would say at least $14 million, if not $20+ million.

I had a lot of fun in Kobe. Traveling is great for kids as it teaches them to adjust to change, which can be handy later in life. And you will have great memories to look back on, instead of the regular routines. My eldest is now in college and he is eager to travel, even with his parents. We are hoping to make a trip to Japan this summer.

Fourteen to twenty million is quite a threshold. I think I’ll have to be satisfied with the lower threshold for US top 1% wealth.

As a CPA in Massachusetts (one of the highest income states) I knew that data was incorrect and reported it to you maybe four years ago. Oh well live and learn good for you. There is inherited wealth to consider but the $13M number meant pretty much no one making around the 1% (592K 2023) US AGI income (a real known number) for twenty years and saving a great deal would ever enter the 1%. That math makes no sense to me. Also say if $13M was the true threshold and it only yielded 5% the AGI threshold would be about $650k instead. No one new would ever enter the 1% meanwhile we know there is turnover. One can conclude there is indeed a strong correlation between long term 1% income and those who are 1%ers.

What exactly did you report 4 years ago and what was the situation then?

You don’t think you could achieve a top 1% net worth with a top 1% income after 15-20 years?

Hi Sam, Math would not support it if it was $13 plus.

Modeled Current last report AGI $592k *.70 (Low average tax effect) $414K less $100k likely living costs = $314K. contribute for 20 year the $314K at $26K a month even with 7% compounding its only $12.8M and we know the 1% threshold for the AGI over the last 20 years average is much lower than $592K. So the 5.8M makes a lot more sense Cheers

How did you come up with 7%? The S&P 500 has returned on average 10%, and top 1% income people might have the ability to outperform the average S&P 500 growth rate over a 20 year period.

There’s entrepreneurship, investing in real estate with leverage, investing in individual stocks, working at a growth company, getting paid more than the 1% threshold over time, etc.

Related: Net worth growth targets to shoot for

Most high worth individuals I deal with have a mix of assets which return 5 or 7%. They’re generally not too flashy in life either. Watch out is that S&P ripe to fall??? Look at Shiller’s PE it’s at 34.5, you can guess what happened every time it was over 20 in the past. I know AI and this is different this time. :)

Did the high net worth people get there by growing their net worth by 5-7% a year? If so, how old are they and did they start off with a lot of money to begin with?

I would say mostly professionals or self-employed who worked long careers, raised families in the suburbs and didn’t hit home runs. They are concerned about wealth protection and generally prefer to reduce their risk profile. Too much risk and sooner or later the gambles don’t pay off.

My wife and I share all our accounts and income. I’ve often wondered, when referencing data on net worth, are these values interpreted as “household net worth”, or should I be dividing our account values in half when assessing how we stand? Is there an industry consensus on this?

There isn’t. Household in America is generally a catch all for all number of people in a household.

So with the Knight Frank data, you can shoot for $5.8 million per person given it says “individual.”

Everything I read says HNWI applies acrossed a shared home. So read it as “household.” And that’s the sense I get when talking to financial people. They’re not going to sit across from a couple living in the same household and ask, “So who’s the actual HWNI here?”

I would argue that the Fed’s indication appears closer to reality especially with asset prices at all time highs. For instance a high earning millennial professional like myself would struggle to purchase a home on the coast of California even though I am in my early 40’s and have a top 1-2% net worth with ~9.5 million in liquid investable assets, but I will continue to build assets and “Buy Utility and Rent luxury” like a wise man said. Have a great day!

Hi Keith,

How much of a home are you looking to buy? Surely with a $9.5 million net worth, you can buy a $2.8 million home no problem no?

Or are you talking about buying a $10+ million home on the water? If so, read: The problem with beach front property.

Ocean view property instead for the win!

Looking in the 3-3.5 million range, my concern is my income, net worth and down payment can meet all 3 FS requirement’s but I worry my income (own vet practice) can’t keep up with this new fancy lifestyle

Gotcha. If you buy that house, I’m pretty sure you’ll find a way to make things work. We are rational beings, and will take appropriate action to solve discomfort.

You’ve got so far already!

Sam here is what i am curious about:

1. How fast is top 5% growing their wealth each year on average? is this 3-4%?

2. How fast is top 1% growing their wealth each year?

3. How fast does the top 0.1% grow their wealth each year?

The strategy to reach those levels will depend on how fast the wealth group is breaking away from the masses which i call “the escape velocity”. Say for example top 1% wealth is 10M$, if they are compounding by say 10% each year, someone say with 6M$ and 500K$ net income added each year to their wealth compounding at the same rate may only catch up to the group in 15 years unless they can compound faster. My gut feel based the graph your provided in “two levels of rich” is that top 0.1% compounds at around 8% while the 1% compounded historically at a lower rate (perhaps 3-4%) which may perhaps have changed in the recent years as they may have gotten financially smarter. As those groups break away, the wealth gap will increase further making it unachievable even if you added 1M$ a year to investments and compounded at the same rate…

The gap will only continue to widen, which is why I encourage people to continue saving and investing as much as possible.

The good thing is, thanks to modern technology, medicine, and stable civilizations, life is as good as never before, without needing to be super rich.

Reading the comments and reflecting more on this topic, I am left with the thought of why we are fascinated with the top “1%?” I’m not exactly sure. I hope a previously very happy person with their 2mill NW is not now stressed out…LOL. I have no idea of the NW of anyone outside of my own household, including my family and closest friends. So it is very hard to understand or add meaning to these statistics. Also, top 1% sounds like it is so broad as to be someone irrelevant anyway – from 5-10m NW to Warren Buffet 100B NW. The idea of “being great at something” being defined by reaching top 1% NW doesn’t really resonate with me.

I think the more interesting point this brings up for readers of this blog is that if a “comfortable” retirement requires 10mill, which solidly puts one in or close to 1% top net worth, what does that say?

I read a number of financial blogs and it does seem like this one is more geared to the affluent and becoming very affluent, not so much FIRE. For FIRE absolute NW numbers are somewhat meaningless, what makes one comfortable/happy in retirement more simply comes down to lifestyle.

When it comes to building above average wealth, it’s good to know what to shoot for. And in general, it’s good to have specific targets for better focus.

Then once you have enough; accumulating more becomes more of a game. A middle class lifestyle today is as good as a top 1% lifestyle from 50 years ago.

LOOK LETS STOP KIDDING OURSELVES HERE: JUST GO TO

WWW.

BLOOMBERGBILLIONAIRE

INDEX.COM

SCROLL ALL THE WAY DOWN TILL YOUR FINGERS HURT…

GET THIS PICTURE YEARLY THEN U WILL UNDERSTAND

CAPITALISM BETTER AND THE

5% WHO CONTROLS THE 95%

WITH THE GOVTS IN BETWEEN

THERE IS A REASON FOR FORTUNE 500 OR THE FORTUNE 1000

jb

Why did you say this?

“Any stress and anxiety I felt about needing to accumulate generational wealth to live comfortably in this ultra-competitive world went away.”

Why did you have a need previously?

Fun challenge. Always good to have a little stress and anxiety. What are some stretch goals you have?

See the post: The Desire For Generational WealthAnd The Angst Of The Not Rich Enough Class

Well, after making some amateur mistakes, I decided to de-market for a while. Now I think 10% a year is more than sufficient. More specifically, I feel one shouldn’t have to use the market —their day/night job should be enough. In that respect, I’ve tried to stop poring over the market’s internals. It’s kind of obsessive and life was simpler before I started bothering with it. It’s easy for greed to take over (for me) so had to back off.

Growing your net worth 10% a year is great. It will double every 7.2 years.

A day job is enough if you’re happy working forever. Most are not, hence the importance of passive income.

Definitely will be working forever if I don’t get on a higher ladder of a job – that for sure. Last year just made it over expenses. So, based on your article, to be comfortable I’ll have to find a job(or set of them) that pays about 50% more. It was like for that for a couple years but the position ended so had to take something less, just gotta keep trucking.