To gauge performance, you need to have net worth benchmarks. Otherwise, you have no idea whether you are outperforming or underperforming the masses. With net worth benchmarks, you can also retire early for greater happiness if you wish!

Even if your net worth is up 20% one year, it may be not be so great if the S&P 500 is up 28% and you're still young. At the end of the day, everything is relative in personal finance. To achieve financial independence sooner, you must outperform your peers or at least, the average.

Net worth benchmarks will help you stay disciplined in growing your net worth CAGR (compound annual growth rate) over time. Further, net worth benchmarks will change as you age and have different financial objectives.

Recommendation to boost your net worth: Grow your wealth through real estate without the burden of a mortgage or maintenance with Fundrise. With over $3.5 billion in assets under management and nearly 400,000 investors, Fundrise specializes in residential and industrial real estate in the Sunbelt region, where valuations are lower and yields are higher. I’ve personally invested over $700,000 with Fundrise to generate more passive income and diversify into venture capital. The investment minimum is only $10.

Net Worth Goals Change As You Age

When I was in my 20s and early 30s, my net worth goal was to always grow my net worth faster than the S&P 500. This is easier to do the less money you have thanks to aggressive savings.

Now in my late 40s, my goal is to try and earn a return equal to at least 2X the risk-free rate of return. For example, if the 10-year bond yield at 4%, my net worth target return would be about 8%.

The more money you have, the more risk averse you tend to become. At least that's my experience. Further, there's no need to swing for the fences when hitting singles and doubles can provide for a healthy lifestyle.

Be Aggressive Growing Your Net Worth While Young

If you've escaped the rat race, the last thing you want to do is have to get back in, especially if you have young children. Your goal in retirement is capital preservation and steady income. The last thing you want to do is lose a lot of money and have to go back to work!

If you're early on your net worth growth journey, you can be more aggressive. For example, you can invest your entire $300,000 portfolio in the S&P 500 to earn potentially $45,000 (15%) or lose $45,000 one year. Losing $45,000 is not a big deal if you're making a decent salary and are willing to work for many more years.

But if you have a $5,000,000 portfolio and are approaching retirement, shooting for a 15% return is unnecessary. Potentially losing $750,000 in one year would be extremely painful!

If you can comfortably live off $300,000 a year gross, then you only need a 6% return. And shooting for a 6% return (a ~40/60 stock/bond portfolio) will likely protect you from losing more during bad years.

Let's review various net worth benchmarks you can follow to gauge your net worth performance. My hope is for all of you to outperform.

Net Worth Benchmarks To Gauge Performance

Here are the best net worth benchmarks to consider so you know you're on track to achieving financial independent. With the growth of AI, it's more important than ever to learn how to become a competent investor.

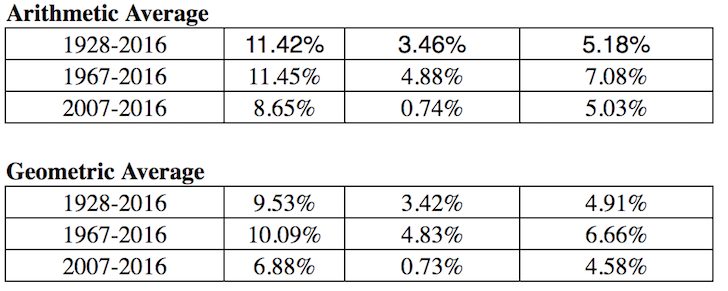

1) The S&P 500 Index. If you live in America, the easiest and most common net worth benchmark is comparing your portfolio's return with the 500 largest stocks in the country. The S&P 500 represents 14 different industries, thereby thoroughly representing the economic health of our nation. Wherever you live, just use your country's largest stock index as a benchmark.

2) Risk Free Rate Of Return Times A Multiple. The risk free rate of return is the 10-year bond yield, which changes every single day. You need to figure out a reasonable multiple on that bond yield because you are guaranteed to return the yield if you put all your money into Treasuries.

What rate of return over the risk free rate (equity risk premium) do you require? My simple formula is to take the latest 10-year bond yield and multiply the figure by 2-to-4.

3) Sector Specific Exchange Traded Funds (ETFs). If you work in the real estate industry and invest in REITs and homebuilders, then you should consider benchmarking your financial performance to a homebuilder ETF such as ITB, XHB, or PKB.

Let's say you work in pharma at Pfizer. Then consider ETFs such as PJP, IHE, XPH. If you work in finance and own your bank's shares as part of your annual bonus, then maybe indexing yourself against XLF is a good idea. Whatever industry you are in, there is an index or an ETF for you to use.

More Net Worth Benchmarks To Consider

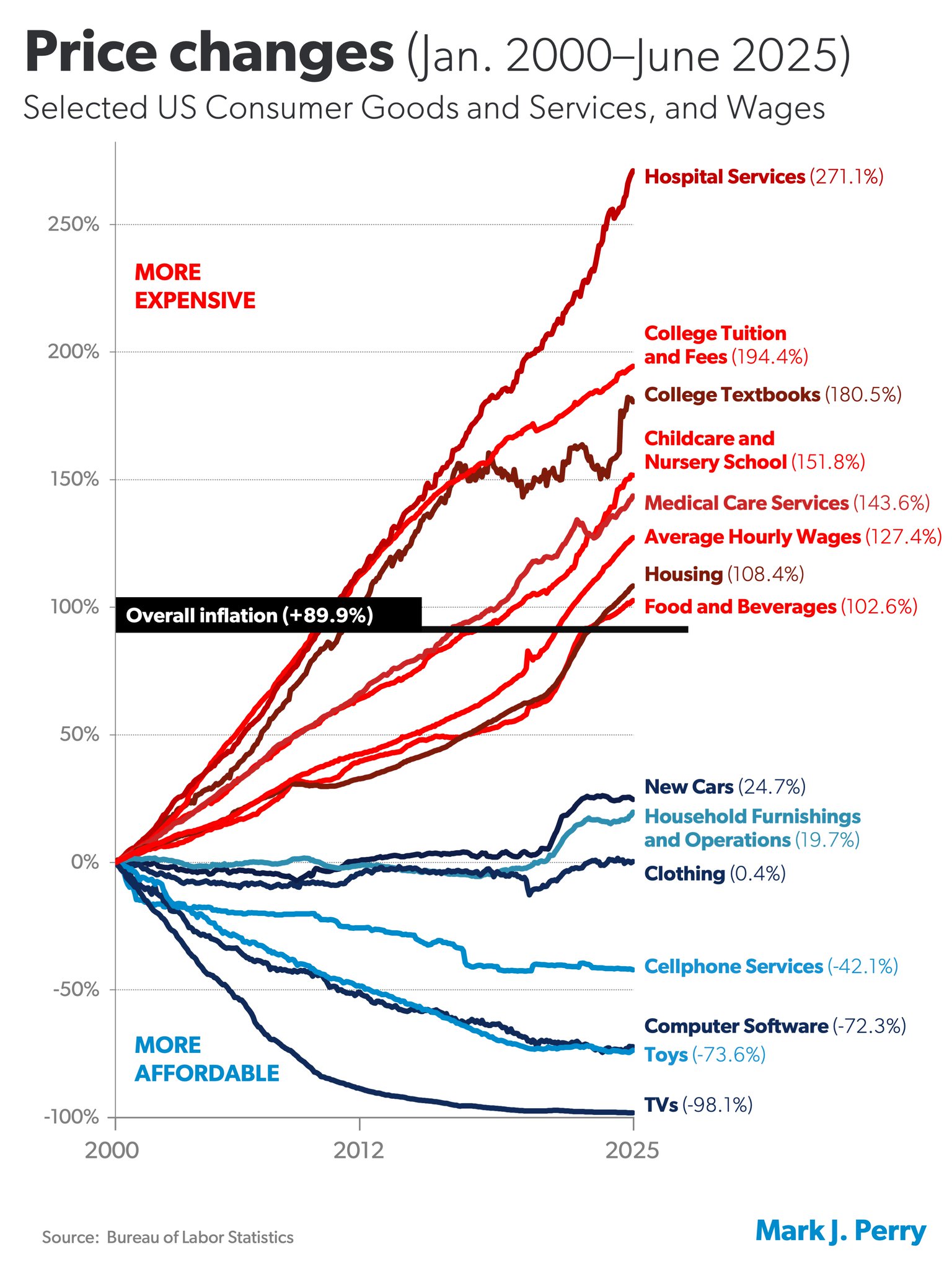

4) Consumer Price Index. The CPI is produced by the Bureau of Labor Statistics and is often maligned as an unrealistic gauge of inflation. The CPI should be considered the base case benchmark for everyone to beat.

In 2022, inflation soared by 9%. As a result, your net worth benchmark had a higher hurdle. Thankfully, inflation is fading again, so your inflation net worth benchmark is lower in 2024 and beyond.

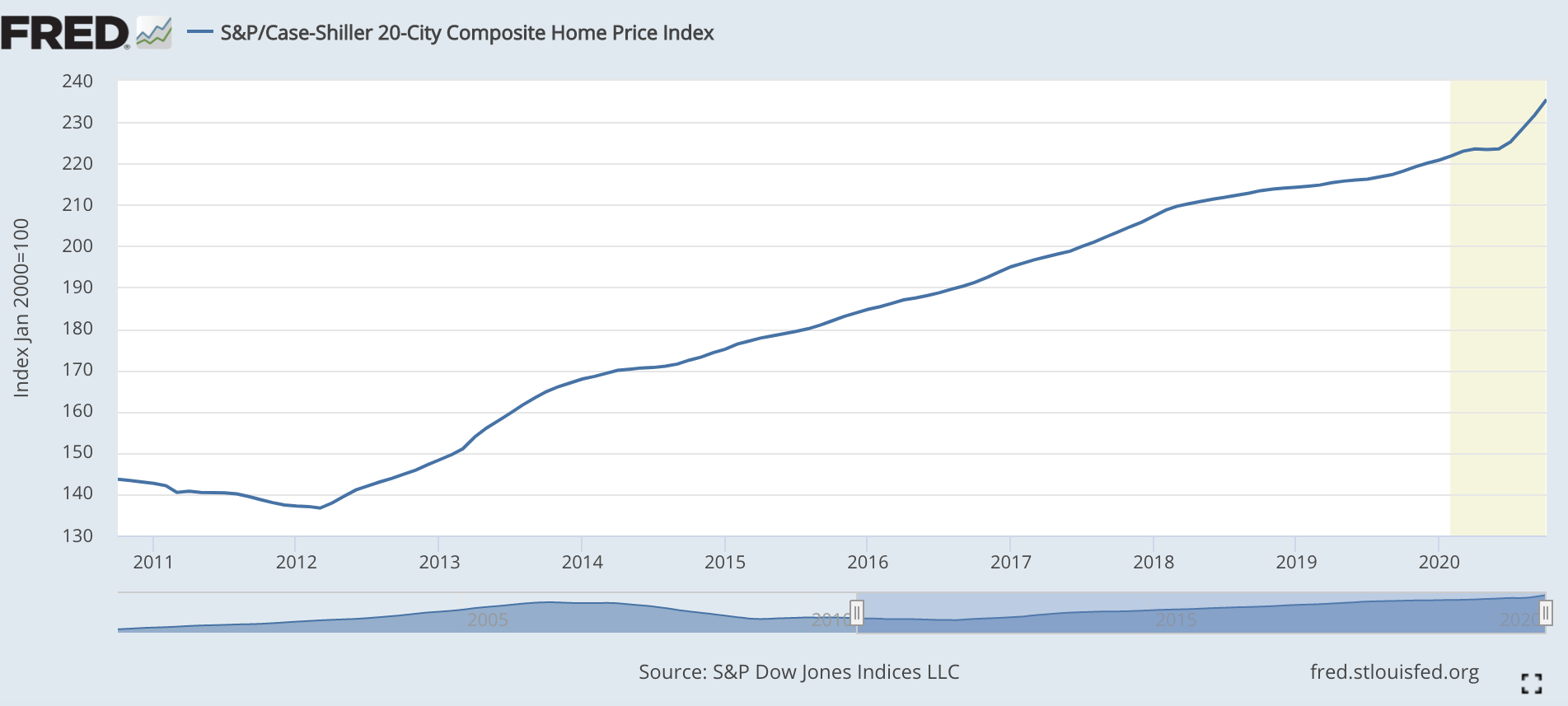

5) The Case-Shiller Home Price Index. The Case-Shiller Home Price Index has risen to be the authoritative benchmark for real estate performance. The Index breaks down home price growth by region.

Given we've discovered that a lion's share of the median net worth in America consists of property, then the Case/Shiller Index should be a relative good barometer for the median American. Home prices have been accelerating during the pandemic.

Coming out of the pandemic, investing in real estate is one of the best moves to make. Inflation is picking up. Therefore, you want to own a real asset that inflates with inflation while the cost of debt whittles away.

My favorite way to invest in real estate is through Fundrise, the pioneer of private eREITs. I've personally invested over $1 million in real estate crowdfunding to diversify and earn income 100% passively. $400,000+ of my investment is in Fundrise.

Owning rental properties and public REITs are also a great way to profit from inflation. However, rental properties require maintenance and time. Publicly traded REITs can often be more volatile than stocks.

6) Hedge Fund Index. Hedge fund managers are supposed to be masters of the universe. Unfortunately, in a bull market they generally lag because of their mandate to hedge. They have absolute return goals where investors expect them to continuously make money even during recessions.

One of the most widely followed hedge fund ETFs is HDG. The HDG is designed to reflect hedge fund industry performance through an equally weighted composite of over 2000 constituent funds. Recently, HDG has performed quite well to many investor's surprise.

It's important to learn how different types of funds trade, including ETFs, open end funds, and closed end funds.

Alternative Net Worth Benchmarks To Track Performance

Besides the above traditional net worth benchmarks, here are more alternatives to consider.

1) Your Parents Financial Situation At Your Age.

Ask your parents what their circumstances were at your age. Did they own a home? A car? What was their savings level, salary, net worth? It may be a fun exercise to have a candid financial conversation with your parents.

Be sure to use an inflation multiplier to get a like-for-like comparison. It could be interesting to get some subjective thoughts about their financial situation compared to yours.

2) The Neighbor You Despise.

Comparing yourself to your neighbor is one of the most common, yet worst ways to compare your financial situation. You don't really know exactly how they got their money. So comparing could drive you nuts! Whenever we see a new car in our neighbor's driveway, it's hard not to feel envious. We wonder whether they got a great bonus at work or in my neighbor's case an inheritance.

My neighbor is 26 years old and rides a brand new $10,000 motorbike. He also has a couple sports car because he has no living expenses living at his parent's house. His parents travel back and forth between their two houses. He probably has an embedded net worth of $2,300,000 because he will inherit his parent's house when they pass.

He would be OK if he didn't leave his motorbike running outside every morning, rumbling the entire street with noise. But he still lights firecrackers at night with his other deadbeat friend because he has nothing better to do.

3) Balance Sheet Affluent Formula.

Another net worth benchmark is the balance sheet affluent formula. This formula was created by Dr. Thomas J. Stanley, author of Millionaire Next Door.

The formula is: 10% X Age X Income = Expected Net Worth. In other words, your household’s net worth should equal 10% of the age of the main breadwinner times your household’s annual realized income [adjusted gross income is a good substitute].

If you are in the Balance Sheet Affluent category, also known as prodigious accumulators of wealth, your net worth should be twice the expectation. Hopefully that's all of you Financial Samurai readers!

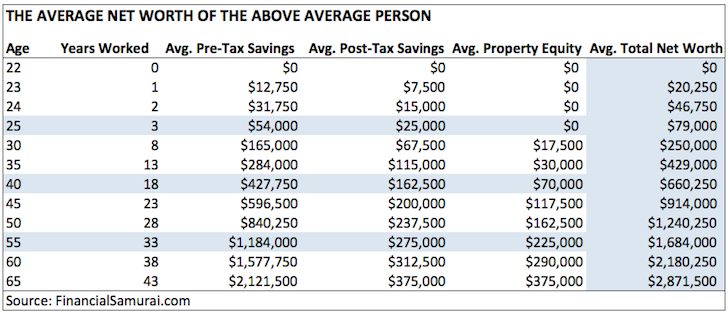

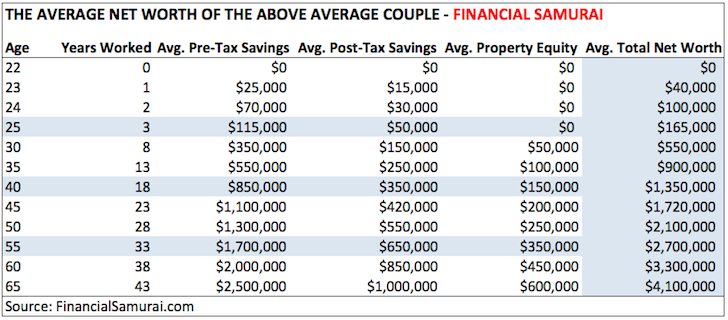

4) The Average Net Worth For The Above Average Person.

I firmly believe many Financial Samurai readers can and will achieve a $1,000,000 net worth by age 50 by aggressively contributing to their pre-tax retirement savings, investing an additional 20% of their after tax savings, owning a primary residence, and working on a side hustle.

5) The Average Net Worth For The Above Average Married Couple.

Another great net worth benchmark combines your finances with your love interest.

Building wealth is generally easier if you have a life partner. Many have wondered whether they should just double the net worth figures in the above average person chart above if they are a couple. That's one way to do it if you believe in equality.

Or, you can take a hybrid approach like I've done below. Read the article about various ways to calculate an above average couple's net worth benchmark.

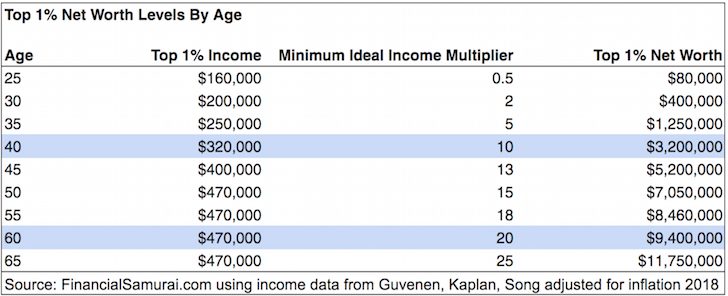

6) The Average Net Worth Of The Top 1% By Age.

If you're really gung ho, then you might want to try and earn a top 1% income level for your age group. Then shoot for a top 1% net worth as well. There are plenty of people who make a lot of money. But they blow it all due to a lack of financial discipline.

Shoot for a $1,000,000 net worth by 35. At age 50, shoot for a $5,000,000 net worth. And by age 60, shoot for a $7,000,000+ net worth. These numbers are roughly 13% light because nowadays top one percent income is over $400,000 a year.

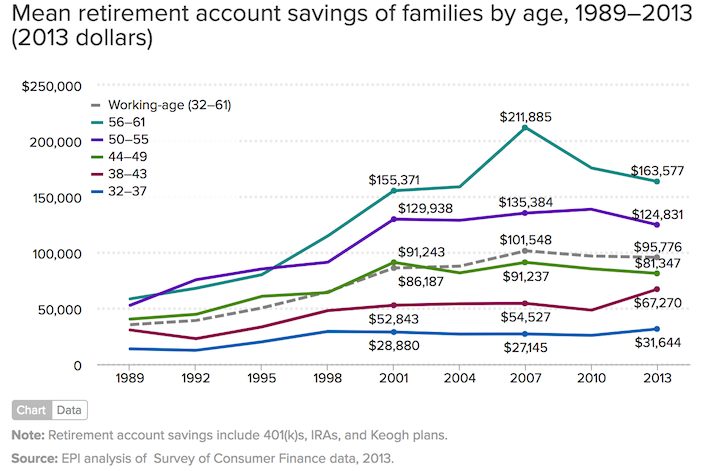

7) The Median Retirement Household Savings In America.

If you're feeling unmotivated, then you can always follow the mean (average) retirement account savings of American families by age based on 2019 data. This is a low net worth benchmark to consider given the median American isn't that wealthy.

The sad part of this chart is that it's much higher than the median retirement account savings of families by age. The median 56 – 61 year old only has $17,000 saved. I hope you guys all agree that the below figures are not very inspiring.

Best Net Worth Benchmark To Follow

Given everything is always changing, you need a dynamic net worth benchmark to follow. Therefore, I think the best net worth benchmark to follow is the annual performance of the S&P 500.

So long as your net worth is growing in line with the S&P 500's performance, you're making progress. During down S&P 500years, hopefully you'll be able to still outperform or still grow your net worth through aggressive savings.

If you are close to retirement or retired, I think the best net worth benchmark to follow is 2X-4X the 10-year bond yield. The 10-year bond yield encapsulates everything from inflation expectations to equity and real estate return expectations. Once you're close to winning the game or have won the game, it's important to dial down risk.

Feel free to take a look at my net worth targets by age as well. It will keep you honest and motivated to always stay on track financially. If you are really enthusiastic, you can see my extreme net worth targets by age as well.

Assign Meaning To Your Numbers

Having more money tends to be better than having less money. But after a certain point, more money means nothing, and can often bring about misery if too much time is spent chasing the almighty buck.

Write out your financial objectives, make a plan, track your net worth, benchmark its growth against your comparison of choice, and go about living as full a life as possible. If the numbers are good enough for your lifestyle, that's all that matters.

Since 2012, my #1 goal has been to earn enough money from my investments and my writing to never have to work a day job again. In order to do this, I had to figure out a way to generate as much passive income as possible.

Today, with two kids and a non-working spouse, my goal is to consistently generate at least $300,000 a year in passive income until my kids graduate from college. This may sound daunting, but that's the challenge I've set for myself!

Invest In Real Estate To Grow Your Net Worth Further

Stocks and bonds are classic staples for retirement investing. However, I also suggest diversifying into real estate—an investment that combines the income stability of bonds with greater upside potential.

Consider Fundrise, a platform that allows you to 100% passively invest in residential and industrial real estate. With over $3 billion in private real estate assets under management, Fundrise focuses on properties in the Sunbelt region, where valuations are lower, and yields tend to be higher. As the Federal Reserve embarks on a multi-year interest rate cut cycle, real estate demand is poised to grow in the coming years.

In addition, you can invest in Fundrise Venture if you want exposure to private AI companies like OpenAI, Anthropic, Anduril, and Databricks. AI is set to revolutionize the labor market, eliminate jobs, and significantly boost productivity. We're still in the early stages of the AI revolution, and I want to ensure I have enough exposure—not just for myself, but for my children’s future as well.

Best Way To Track You Net Worth

The easiest way to track you net worth is with Empower, the best free financial tool online today. I've used Empower to track my net worth, analyze my investments, check for excessive fees, and plan for retirement since 2012.

All you've got to do is sign up, link up your financial accounts, and then you can see everything in one place. There's no rewind button in life. Stay on top of your finances today.

Net Worth Benchmarks To Ensure Proper Growth Over Time is a Financial Samurai original post. Join 65,000+ others and subscribe to my free newsletter if you want to achieve financial independence sooner, rather than later.

I really enjoyed this post and found it through your interlinking of other posts. Thanks for all the hard work you put in to make complex topics a lot easier for the rest of us!

Your 2x expectation of the formula is spot on. If you want to be an outlier in retirement age, then you have to be an outlier in wealth accumulation.

A good reminder to check in annually on net worth benchmarks.

Curious to know your thoughts on home equity right now? It seems like a lot of equity has built up these last 5 years +. Do you think home values will continue to increase due to inflation induced by frivolous stimulus spending?

Yes, I’m bullish on real estate over the next 10 years. The demographic home buying trend is very strong with those born in the 80s and 90s.

Mortgage rates will stay low for years. The intrinsic value of a home has gone up as we are all spending more time at home. People want to own real assets with less volatility.

I’m buying more rental property and investing in more private real estate syndications. Cash flow is huge now!

Hi,

Thanks for the website. I enjoy all your stuff. My dream was to become a corporate sell out but was unable to get one of those great jobs. I ended up investing in real estate instead. I will keep expanding my portfolio, However if you have any tips on how to get one of those fancy jobs it would be great.

I know this is a net worth conversation but it leads to a retirement question about how much your net worth is producing each year. I’m 44, and earn more than enough in cap gains and dividends from my net worth, but I don’t have the guts to retire. Mostly just due to my age. It just doesn’t feel right. I went through 2020 and truly looked at what it took to live each month with no constraints, I am also being conservative with my gains and can still be perfectly fine with a 30% reduction in gains. I have zero debt. I wish someone would slap me up abs tell me what to do

It’s the “one more year syndrome” in effect. If you don’t feel fully comfortable leaving, then don’t leave. The key catalyst for me was negotiating a severance. The severance gave me a safety net for at least five years to try something new. If I failed or felt like I was failing within 2 years post work, I would have tried to go back.

Here are two posts worth reading, besides my book on learning how to negotiate a severance.

Overcoming The One More Year Syndrome To Do Something New

If I Could Retire All Over Again, Here Are The Things I’d Do Differently

Here’s hoping your neighbors with the inconsiderate son both live very long, healthy lives into their late 90s, not leaving him any inheritance until he is in his 70s.

Thank you for this informative and well written article.

Hah! Well, my neighbors (the parents) inherited the house and several properties from their parents. Which may be why they haven’t pushed their now 30-year-old son living at home to make his own money.

Always a good idea to set goals and measure them to see progress. With that said, you should measure your real rate of return: gross return less (taxes and inflation). Taxes will not apply to all your investment accounts but inflation will. Speaking of that, you need to determine an applicalbe inflation rate. This is a highly personal decision becuase it is driven where you spend your aftertax money. The CPI is better than nothing but really is not precise enough. For example, if you have high medical or school expenses, I can almost guarantee that the CPI will understate your inflation rate. I would also use a weighted inflation rate so the categories you spend more on, carry more weight. More work but not as much as you think. Just hit the major categories and use the CPI for those of lessor importance.

Finally the S&P 500 is an okay measure. I prefer the total stockmarket index since the S&P500 leaves out about 20-25% of the market. It is a broad measure but not a complete one.

Here’s a little poet by Robert William Service, given to me by my Dad when I was twenty five. It must have made a subconcious impact as it has worked for me. Check it out. Robert William Service “Five-Per-Cent” allpoetry.com/Five-Per-Cent

How do taxes figure in to your net worth calculation. Do you adjust pretax accounts to all be after tax? I have lots of accounts with different levels of tax liability built in plus some tax free Roth accounts. Just adding everything up gives you a mish mash. Would think you would adjust everything to after tax but haven’t seen much written on this. Thanks for the insightful article!

Reduce the gross amount by the estimated taxes / commissions. That would be the best way to calculate true net worth.

While I didn’t set a Networth goal to a specific benchmark, I did establish a 2 year- 5 point goal in December of 2019. Of course, much has transpired since then.

Anyways, my NW goal was to breach the 2 mil. mark by 12/31/21. After a bizarre, and surprisingly profitable 2020, we are sitting about 35k short of our goal.

Barring any unforeseen market events, we should hit our 2 year goal by year end pretty handily. Thanks for continuing to write Sam. Financial Samurai is one of the few places I get much enjoy venturing to online.

Big bucks! Congrats! And fingers crossed we don’t go through another 30%+ violent correction and stay down this year.

Let’s spend more of our money and enjoy life!

Yes, yes, yes. I totally agree with the importance of setting net worth and financial goals relative to benchmarks. So much changes all the time and we need to adapt and improve constantly. With so many rising vital expenses like medical care, hospital services, childcare, and education increasing faster than wages, we have to be creative. Working outside the box to generate passive income, diversify, try alternative investments, and protect our assets is more important than ever. The last 11 months sure has taught us that the whole world can change practically overnight and nothing in life is certain. I still think it’s so important to think positively, but we also have to be prepared for the worst and hope it never comes to that. I always prefer to be more prepared than less.

Medical expenses are outrageous! Especially ambulance expenses! Grr. Total racket.

I change my net worth goal to +10%/year. That’s an easy number to remember and benchmark. Some years I’ll do fine and some years I won’t. The other benchmarks change too much from year to year. It’s easier for me to just track my result.

Anyway, if we average 10% gains, we’ll have a lot more money than we ever need.

I agree. 10% is a good easy goal to have. Also aligns well with the historical S&P 500 annual return average.

I’m interested in exploring more conservative investments as I head towards retirement. Do you have a list of which munis/bonds you prefer to invest? What other investments do you consider conservative enough to meet your needs? Do you generally need a broker to buy munis? I’ve looked into Vanguard funds for munis and treasury notes, but I have enough cash after the run up to buy direct if there’s an advantage to doing it that way.

Thanks for another fact filled post!

There’s CMF for California and MUB for national muni bond funds. I also buy individual CA muni bonds as well. You can find a list of them from your brokerage and go through the ratings.

Thanks

Thanks for updating this as I had asked you about your net worth growth benchmark. I’m approaching 50 and am happy with my absolute net worth and growth. I try to match the S&P 500 which isn’t easy since real people need to have a cash reserve at all times.

I remember you positing your goal of 3x risk free rate some time back, but it seems you have seriously modified your target given you’ve outperformed in the last few years. How have you evolved your investment portfolio/strategy to account for the higher returns? I think that would be an interesting post to contrast the more conservative portfolio vs the more aggressive portfolio. I know you keep us updated on where you are investing at any given time but a historical vs current snapshot might be helpful.

I just realized I’ve ben too conservative and with the 10-year bond yield at only 1.1%, a 3.3% annual net worth growth target seems overly conservative. However, if we enter a bear market, a 3.3% return is great.

The other thing is, Financial Samurai is a cash cow now. So just saving online earnings will help grow net worth, by 1-2% a year.

My wife and I feel fortunate to have had a 32% increase in net worth in 2020. We definitely benefitted from staying invested, and even increasing contributions, during the COVID crash. It will be difficult to hit that again without another “opportunity”, but 30% is a stretch goal.

Our net worth is just about 3x our combined gross salaries at this point, so we will likely continue to see large increases in the next few years simply by having a decently high savings rate. We also own our home, so it’s nice to see a good portion of our living expenses having a positive impact on our net worth. With that said, 20% is our goal for this year.

I just began executing my father’s estate and have learned that I am much better at money than he ever was. He was meticulous in record-keeping, but not as devoted to paying his bills. It’s been fascinating. I also began beating his best salary year in 2013. I am working hard to continue improving my salary for the next few years. Once I get where I’ve set my goal, I will likely “coast” on that enormous salary. I have no children and the goal is to establish my financial life so that I can do the less-financially fulfilling business I’ve been growing. I think I can continue loving my business if I don’t need to expect personal and financial gain from it.

Great content Sam. When I was in my 20’s I wanted to earn 12% returns every year. It was the roaring 90’s and that seemed like reasonable growth. A few recessions and decades later, I am very comfortable earning a 7% annual return. By knowing the combination of how much I can save and what rate of return I need makes establishing a portfolio to meet my needs a straight forward task.

I think its interesting how the human dynamic operates when you generate a sufficient return, but jealousy enters the mix when someone else generates a return higher than yours. It’s great that you have eliminated that emotional element from your finances. I think that’s tough for most people to do, which leads to unnecessary risk taking. Richard Thaler actually just won the Nobel Prize for his research in this area (Behavioral Economics). This is the first year I’ve underperformed the market, which has been frustrating, but I also understand that investing is a long-term game. I think the main point in the article you mentioned was setting a reasonable return target that you feel comfortable with and not to worry about other peoples affairs.

Interesting post. It is always interesting to me that people focus on absolute returns and not real returns (right up there with non logarithmic charts….ie the visual representation of a stock going from 10-20 and then 20-30 is the same when it not…..maybe a future post topic for you). I prefer to stick to a goal over inflation (no real good measure so have to use CPI…..open to others) of 4x inflation. I realize that the risk free rate and inflation rate generally move in the same direction but the idea works better for me. Will be interesting to see if people’s targets move when inflation picks up (10yr treasury and CPI in the 80’s would be tough to beat 2-4x)

Hi Sam. Is this one (partially quoted below) correctly state?

“10% X Age X Income = Expected Net Worth. In other words, your household’s net worth should equal 10% of the age of the main breadwinner times your household’s annual realized income”

It just seems like it produces a fairly low number, especially for older people. Take a guy making a modest $100K at age 50.

If I’m reading the formula right that would suggest a NW of $500K at age 50 is “on-track”, but that seems like a fairly low-end observation.

That’s what Dr S recommends, but for prodigious savers, the number is double.

Ah, okay; thanks for the clarification!

I am generally more risk averse with everything in my life, but with money it’s a little different. I’m not risk-averse at my age (35) because I am majority in stocks, and with stocks it is a gamble.

I do agree that when one gets to a certain point of comfortability in covering their expenses then there is no particular reason to risk one’s money. I’m not there yet, but when I do get there, you better believe I’m not gambling.

I do not believe that, when using sound rational and research, investing in good companies is “gambling.” History has shown that to not be the case.

We are told by the investment world that this is all so complicated and we NEED their wisdom and expertise to succeed. Poppycock.

Common sense, looking at what is going on in and then acting on these things can make one rich.

Further, the self confidence that comes from being self made is priceless.

Thank you for the insightful post. Should a married couple simply double the target numbers? Or is the multiplier less than 2, given that some expenses are usually shared?

You can double the numbers as a couple, or go a hybrid route.

Check it out: https://www.financialsamurai.com/the-average-net-worth-for-the-above-average-married-couple/

I love your site and have been a fan for a very long time. However a slight point of constructive criticism: it’s very obvious that you have a cognitive bias regarding income, taxes and savings based in the area where you are from.

These numbers are extremely different if you for example, live in Western Europe (where I’m from) where taxes alone can be up to 55%. Just something to take into account when you write future articles.

Take care.

I’m most definitely biased towards American readers because I live in America and something like 97% of readers are from America.

However, if you’d like to adjust the charts to your tax rate by reducing the amounts, or using your own countries stock index, by all means. I think the information is quite transferable.

You’ve helped me think about how to produce more relevant content for Wester European readers though! Cheers

I tink 10% YTD is amazing! I’m happy with my 8.5% YTD so far, I think anything about 5% I’m happy with (yes, I’m not aiming very high hah). Your 26 year old neighbour sounds very annoying, especially with the motorbike running loudly and shooting firecrackers with his friend. He sounds very ‘unsupermotivated’.

Hmmm. Very interesting, Sam. Other than the Mustachean Threshold (net worth greater than 25 times your annual living expenses), I never really pondered this. We’re retired now, so my simple goal is to have our portfolio return more than our annual living expenses by a comfortable margin. Right now, Mrs. Groovy and I are on track to spend around $37K in 2017. So far this year our portfolio has returned $126K. And the best part about this is that our portfolio allocation is 35% stocks and 65% bonds. We do have one individual stock–a lithium concern–and that stock has accounted for roughly half of our market returns. It looks like a lot of people are excited about the electric car push in Europe, China, and here. Anyway, thanks for the great read. You made me think.

Now that coverage of $126K/37K is impressive! That sounds truly rich to me.

I don’t see how the “mustachean threshold” can be a net worth growth benchmark though b/c the only way you know your net worth is growing properly is if your annual living expenses are also growing.

In other words, this threshold is a scarcity mindset threshold, and not a growth mindset. But that makes sense because they are focused on frugality and savings, whereas I’m much more focused on aggressively growing the pie. It’s harder to do, hence why less people do it, but it is infinitely more fun to write about and try!

Damn it, Sam. You’re making me think again. I never considered the “Mustachean Threshold” as coming from a scarcity mindset. Very insightful, my friend.

I just follow your chart as my benchmark. Currently working on getting to top 1%. Already there income wise. The side hustle that I started after reading this blog enabled me to make more than my day job. Working on getting networth to top 1%. 44 years old at 2.5M. Hoping to get to 6M by 50. To get there I would need 20% returns plus savings in the next 6 years. It is going to be tough, but that would be a major achievement for me. Hopefully by 55 I should be in the top 1%.

Now that is amazing. Great job on the side hustle! Can you share what it is?

The thing with stretch goals is, even if you don’t get there, you’ll have gone much farther than those who didn’t push themselves.

I became a realtor. I was already quite interested in real estate and I buy property every couple of years. Then I read something you mentioned in your blog post about side hustle. So I figured there was no harm in trying. I could at least save some money on buying selling my own properties. First year I did 3 deals then 15 and this year I am at 20! I gave up my full time job and opted for PT consulting because its a LOT OF WORK. The worst thing about being a busy Realtor is that your weekends are pretty much gone. Thats a lot of valuable time with my boys. I try to make time during the weekdays but it is hard.

Being a realtor instead of being a w2 employee, you have a lot more leeways to deduct your business expenses and hence you could substantially reduce your AGI. You could even deduct your business expenses of your luxury vehicle for your realtor business. This is definitely one big advantage on working for yourself. I can’t do the luxury vehicles deductions for being an active investor and trader.