Do you need more incentive to generate passive income in order to give yourself more freedom? Then look no further than the below two charts. They show the 2024 and 2025 capital gains tax rates by income for both short-term and long-term. The capital gains tax rates for 2026 are the same, just that the gains thresholds are slightly higher.

The short-term capital gains tax rate is equivalent to your federal marginal income tax rate. Once you hold your investments for longer than a year, the long-term capital gains tax rate kicks in. The long-term rate is much lower.

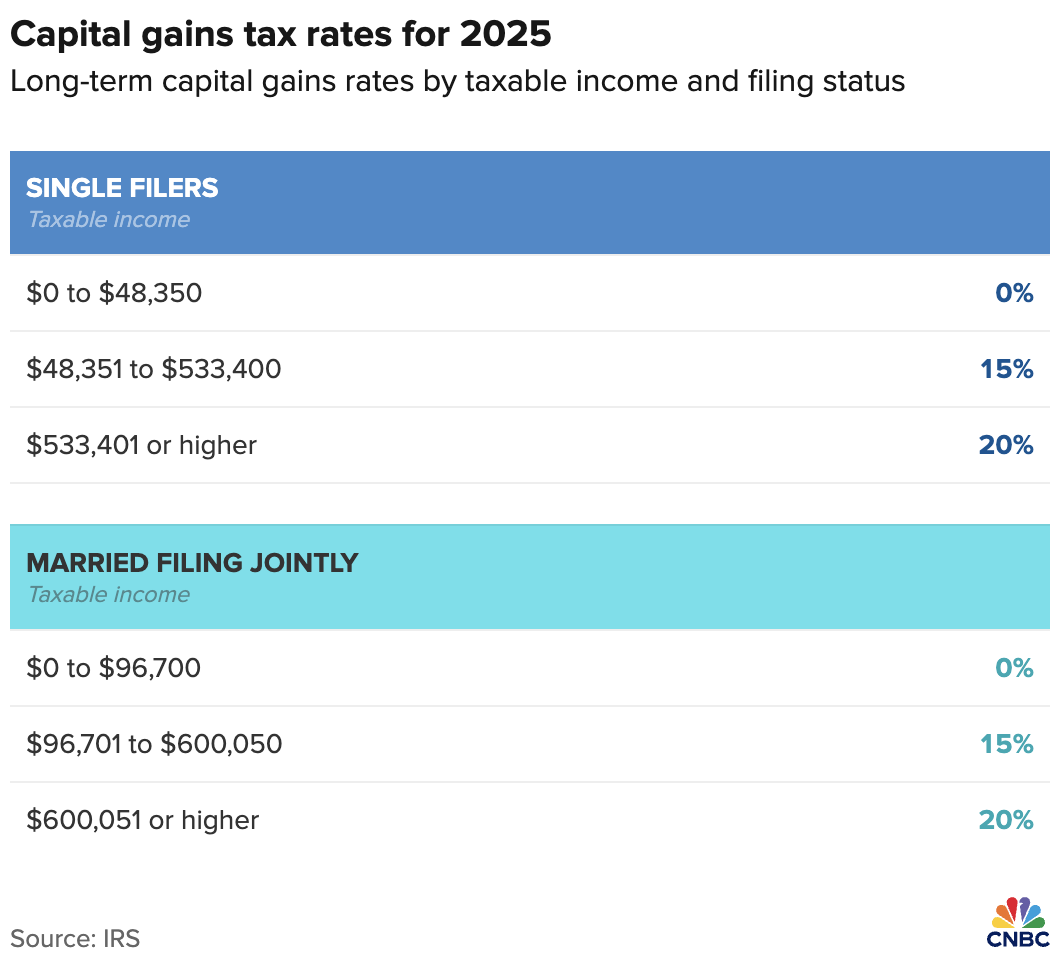

Here are the latest short-term and long-term capital gains tax rates. The income thresholds are slightly higher in 2025. With the passage of The Big Beautiful Bill Act on July 4, 2025, there is a lot of tax relief for Americans going forward.

Capital Gains Tax Rates By Income For Singles

Here the latest 2025 tax brackets and 2025 long term capital gains tax rates. The income thresholds have increased by about 2.7%.

Most Tax-Efficient Passive Income Amount To Make For Singles

If you're single, the largest tax spread difference between short-term and long-term is if you make between $243,728 to $609,350 in taxable income as an individual.

If you make between $243,728 to $609,350 in W2 active income, you are taxed at a 35% marginal rate. However, if you make the same amount in long-term capital gains, you're only paying a 15% rate. In other words, the capital gains tax rate spread is the widest at 20%.

To generate $243,728 to $609,350 you could earn a 4% rate of return on $6,093,200 – $15,233,750 in capital. Or, you could earn qualified dividends at the same rate with the same amount of capital. Or you can take profits on long-term holdings.

Of course, many argue the long-term capital gains tax rate should be lower since we've already paid taxes on our capital. Either way, the most tax-efficient passive income amount to make if you are single is between $243,728 to $609,350 for 2024.

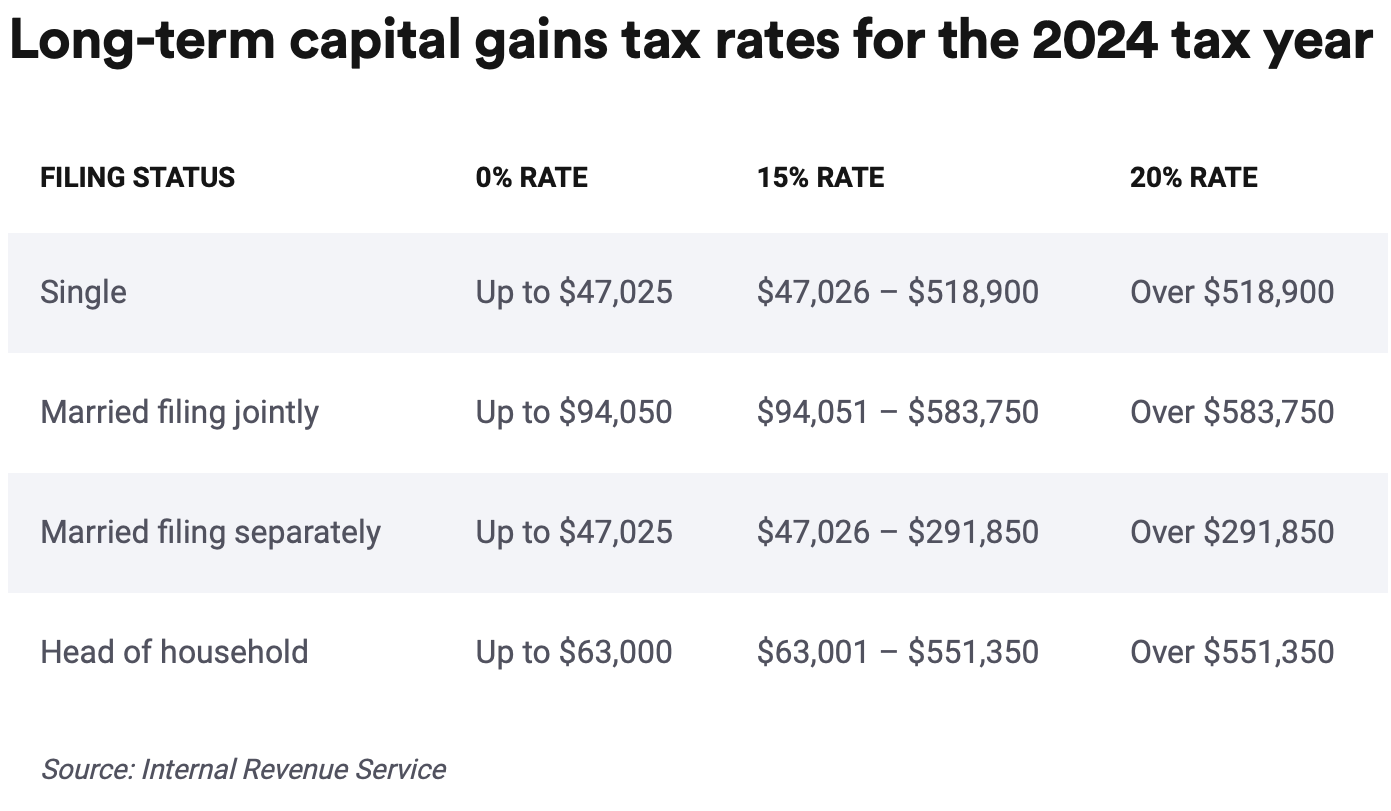

For the 2024 tax year, you will not need to pay any taxes on qualified dividends as long as you have $47,025 or less of ordinary income.

If you have between $47,026 – $518,900 of ordinary income, then you would pay a long-term capital gains tax rate of 15% on qualified dividends. The long-term capital gains tax rate for single filers with taxable income of over $518,900 is 20%.

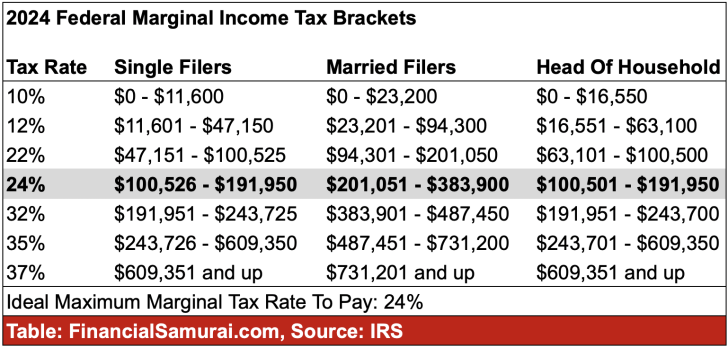

2024 Marginal Income Tax Brackets

Capital Gains Tax Rates By Income For Married Couples

As you can see from the same chart below, the long-term capital gains tax rates for married couples are also 0%, 15%, and 20%. If you are married, you can earn up to $94,050 and pay 0% capital gains tax rates. You pay a 15% capital gains tax rate on income between $94,051 – $583,750, and a 20% capital gains tax rate on income over $583,750.

This is investment income mind you.

Most Tax-Efficient Passive Income Amount To Make For Married Couples

If you're married and file jointly, the largest tax spread difference between short-term and long-term is if you two make between $487,451 to $731,200. The tax rate difference is also 20% (35% vs 15%).

Therefore, the most tax-efficient passive income amount to make for married couples is also between $487,451 to $731,200 for 2024.

Obviously, few couples will generate such large long-term capital gains or passive investment income on a regular basis. At a 4% rate of return, the couple would need $12,186,275 to $18,280,000 in investments to generate $487,451 to $731,200 in passive investment income. At this level, you are clearly Fat FIRE and living it up!

However, one scenario that does could create such large long-term capital gains is when long-term homeowners in high cost of living areas sell their homes.

They'll first earn tax-free profits up to $500,000 if they've lived in their primary residence for two out of the last five years. Whatever profits are left will then face the various long-term capital gains tax rates.

Another scenario may be when a couple cashes in on their long-term stock options. There are plenty of couples who've worked at a private startup for years that finally goes public or gets acquired.

Beware Of The Net Investment Income Tax

The 3.8% Net Investment Income (NII) tax is an additional tax. It applies to whichever is smaller: your net investment income or the amount by which your modified adjusted gross income exceeds the amounts listed below.

Here are the income thresholds that might make investors subject to this additional tax:

- Single or head of household: $200,000

- Married, filing jointly: $250,000

- Married filing separately — $125,000,

- Qualifying widow(er) with a child — $250,000.

In other words, if you earn $250,000 in W2 income as a married couple, and then another $100,000 in investment income, you'll have to pay an additional $3,800 in NII tax on top of a 15% long-term capital gains tax rate in addition to your state income tax, if any.

Given the NII tax thresholds, the ideal income for maximum happiness is $200,000 for singles. For married couples, the ideal income is roughly $250,000, depending on where you live.

The student loan forgiveness income threshold of $125,000 per individual and $250,000 per married couple may also be considered the ideal income as well. The idea is to look at what income levels the government deems worth of free money or reduced tax rates.

Long-Term Capital Gains Tax Examples

Please note the ideal passive income figures above are theoretical exercises. For the most tax-efficient income, it would be best if we earned 100% of our total income from passive investment income. This way, we pay the long-term capital gains tax rate.

In reality, most of us will earn both active income and passive income. It is important to understand that these two types of income are taxed at different rents. Further, it is the total of these two income sources to determine how much you pay in long-term capital gains tax.

Long-Term Capital Gains Tax Example #1

Say you bought ABC stock on March 1, 2010, for $10,000. On May 1, 2022, you sold all the stock for $20,000 (after selling expenses). You now have a $10,000 capital gain ($20,000 – 10,000 = $10,000).

If you’re single and your income was $65,000, you would be in the 15 percent capital gains tax bracket. In this example, that means you pay $1,500 in capital gains tax ($10,000 X 15 percent = $1,500). That amount is in addition to the tax on your ordinary income.

In other words, even if there is a 0% long-term capital gains tax rate on up to $44,625 in long-term capital gains, you still have to pay a long-term capital gains tax on your $10,000 capital gains.

Long-Term Capital Gains Tax Example #2

Financial Samurai Jeff earned $35,000. He pays 10% on the first $10,275 income and 12% on the income he earned beyond that, up to $41,775 (35,000 – $10,275 = $24,725). His total tax liability is $3,994.50 ($1027.50 + $2,967).

If Jeff sells an asset that produced a short-term capital gain of $1,000, then his tax liability rises by another $120 (i.e., 12% x $1,000). However, if Joe waited one year and a day to sell, then he pays 0% on the capital gain.

Hence, before selling any investment held under one year, please calculate the net proceeds after tax considerations. Investments held under one year will be taxed at the short-term capital gains tax rates.

Long-Term Capital Gains Tax Example #3

Financial Samurai readers Claire and Hank, who are married, earn a top 0.1% income of $2,000,000 in 2023. They pay a 37% marginal income tax rate on all income above $693,750 until $2,000,000. They pay the other marginal income tax rates on all income below $693,750.

Claire and Hank also have long-term capital gains of $88,000 from selling stock in 2023. Do they get to pay 0% long-term capital gains on the $40,000 since it is below the $89,250 threshold for 0% long-term capital gains tax for married couples? Unfortunately, no.

Given Claire and Hank are in the highest income tax bracket (37% marginal income tax on income over $693,750), their $88,000 will get taxed at a 20% long-term capital gains tax rate.

The IRS wants its money. The IRS isn't going to let an already top 1% income-earning household then earn tax-free income on up to $89,250 for married couples. If so, that would be an obvious loophole every six-figure or top 1% income-earner would pursue!

You have to total the ordinary income and capital gains and then pay the respective capital gains taxes accordingly. Your ordinary income is taxed first, then your capital gains is taxed taxed second.

How To Minimize Capital Gains Tax

Even though long-term capital gains tax rates are more favorable, they are essentially a double taxation on money that was already taxed. Therefore, I wouldn't get too excited about paying lower tax rates.

What you should get excited about is not having to pay as high a tax rate while not having to actively work for your income if you generate enough passive income.

We've discussed the difference between active and passive income to avoid confusion. We've also discussed the best combination between active and passive income to live the ideal lifestyle.

Now let's discuss some ways to minimize capital gains tax.

1) Hold forever your asset forever like a billionaire

The best strategy for minimizing capital gains tax is to hold onto your assets forever. If you can't hold on forever, then try and hold on for at least one year. After one year, your investments will qualify for the long-term capital gains tax rate.

During your decision to hold or sell, it's very important to calculate the tax implication between your short-term and long-term tax rate. It's generally better to buy and hold for the long-term. But, when you're young or in a lower income tax bracket, taxes are less of a drag on your returns.

As you get wealthier, you become much more incentivized to hold. Think about the single person making $800,000 a year. If he takes a short-term profit on a $200,000 gain, he'll pay a whopping 37% short-term capital gains tax. If he held for more than one year, he would only pay 20%.

The only logical reason for him to sell is if he felt his investment would lose more than 17% or more than $34,000 in value if he didn't sell within a year. Be like a billionaire and never sell your assets and borrow from them instead.

Just make sure you are holding onto your investments for the right reasons. In my case, the pain of owning my SF rental property outweighed the cash flow it provided. I sold and invested a third of the proceeds in stocks, a third in bonds, and a third in real estate crowdfunding.

As a father of two young children, I don't have the time to deal with tenants anymore. My kids are growing up fast. I don't want to miss a thing.

2) Max out tax-advantaged accounts

These include the 401(k), IRA, Roth IRA, SEP IRA, Solo 401(k), and 529 college savings plan. These plans either allow investments to grow tax-free or tax-deferred.

Qualified distributions from Roth IRAs and 529 plans are tax-free. In other words, you don’t pay any taxes on investment earnings. With traditional IRAs and 401(k)s, you’ll pay taxes when you take distributions from the accounts.

3) Rebalance with dividends instead of selling assets

Rather than reinvest dividends in the investments that paid them, use the dividends to invest in underweighted investments. Typically, you’d rebalance by selling the securities that now take up a higher percentage weighting than your target. You would then reinvest the proceeds into those securities that have a lower percentage weighting than your target.

But by using dividends to invest in underweight assets, you can avoid selling strong performers and the capital gains tax that goes with selling. Rebalancing with dividends will just take longer to get to your ideal asset allocation.

4) Carry losses over

When it comes to capital gains on stocks and bonds, you can use investment capital losses to offset gains. Here's an example. Let's say you sold a stock for a $20,000 profit this year and sold another at a $15,000 loss. You'd be taxed on capital gains of $5,000.

This difference is called your “net capital gain.” If your losses exceed your gains, you can deduct the difference on your tax return, and carry over up to $3,000 per year.

If you have $200,000 in long-term capital gains one year, you can “use up” $200,000 in capital losses in a previous year to offset the gains and pay no taxes. Before the $200,000 in capital gains, your $200,000 in capital losses were just sitting there waiting to be used beyond the $3,000 capital losses allowed a year.

5) Look into a robo-advisor for tax-loss harvesting.

Robo-advisors like Empower are online services that manage your investments for you automatically. It deploys tax-loss harvesting, which involves the selling of losing investments to offset the gains from winners.

To do tax-loss harvesting manually could be very cumbersome, especially if you have a lot of trades. Therefore, using a robs-advisor to automate can be very helpful.

Minimum Passive Income And Invested Capital Targets

For those just getting started, minimum targets are helpful to stay motivated.

If you are single and retired with no active income, your goal should be to generate at least $47,025 in annual passive income. If you are married and retired with no active income, your goal should be to earn $94,050 in annual passive income.

Why? Because at these passive investment income levels, all the capital gains are tax free! At a 4% rate of return, we're talking about having $1,175,625 and $2,351,250 in invested capital, respectively.

For simplicity's sake, let's just round these figures to $1.2 million for individuals and $2.4 million for couples. Once you get to these passive investment income amounts, depending on your relationship and living situation, you should be able to reach a minimal level of financial freedom.

Know The Standard Deduction Levels For More Tax-Free Income

If you want to make more than $47,025 for singles and $94,050 for married couples, here's the next passive income strategy to consider.

For 2024, the standard deduction increases by $900 to $14,600 for singles and $29,200 for married couples. The standard deduction limit will generally go up every year. For 2026, the standard deduction is $16,100 for singles, $32,200 for couples. It keeps going up every year.

Hence, hold enough bonds (non-tax exempt) to use up the $14,600 / $29,200 standard deduction with the interest income, and then generate $47,025 / $94,050 in dividends or long-term capital gains from equities or other investments.

The single person will make $61,625 and the married couple will make $123,250 of income and not pay any federal tax (you will owe state taxes though depending on where you live). If you want to make more tax-free income, then you'll simply have to buy and hold municipal bonds from your state.

Adjust Your Income According To Your Cost Of Living

$1 million to $2 million in invested capital to earn tax-free capital gains may not be enough. If you are raising a family in a higher cost of living area, then you may want to accumulate at least $5 million in after-tax investments instead. Do the math.

The beauty of the long-term capital gains tax rate is that even if you end up generating more income, you still get the first $47,025 / $94,050 in gains tax-free depending if you are single or married.

Therefore, to the extent you can generate more, you might as well keep going until you find your optimal level for financial freedom. For most investors, paying a 15% – 20% long-term capital gains tax rate is reasonable.

Our Passive Income Target Compared To The Ideal

Upon writing this post, I realize our long-term passive investment income target of $400,000 is still below the ideal income range for married couples. This range is where the tax rate difference between active income and passive income is largest at 20% (35% vs. 15%).

Therefore, I guess I should work harder to accumulate another ~$1,600,000 in capital! But I'm not going to because I'm tired as hell. We already live on less than the ideal tax-efficient passive income range above.

Take these ideal passive income and invested capital targets as guides. They will help you think about how much to work, how much to relax, and how to construct your total income composition.

At the end of the day, you want to feel fairly taxed for the income you earn. The government also wants you to stay motivated to work. Otherwise, society would collapse if all us sat around and depended on others to pay for everything.

Earning tax-free long term capital gains of $47,025 for singles and $94,050 for married couples seems generous. So does earning tax-free active income equal to the latest standard deduction. I'd shoot for these income targets and then reassess.

Personally, it has felt wonderful to take things down during a difficult year. A bear market in 2022 and the potential for higher tax rates make grinding less appealing.

For those of you who are tired, take a load off! Analyze your income composition and adjust your effort accordingly.

Free Financial Analysis Offer From Empower

If you have over $100,000 in investable assets—whether in savings, taxable accounts, 401(k)s, or IRAs—you can get a free financial check-up from an Empower financial professional by signing up here. It’s a no-obligation way to have a seasoned expert, who builds and analyzes portfolios for a living, review your finances.

A fresh set of eyes could uncover hidden fees, inefficient allocations, or opportunities to optimize—giving you greater clarity and confidence in your financial plan. Everyone has a financial blindspot, and an Empower professional can help you recognize what you're missing. Further, Empower provides tax planning services if you decide to use them to manage your investments.

The statement is provided to you by Financial Samurai (“Promoter”) who has entered into a written referral agreement with Empower Advisory Group, LLC (“EAG”).

Diversify Your Retirement Investments

Stocks and bonds are classic staples for retirement investing. However, I also suggest diversifying into real estate—an investment that combines the income stability of bonds with greater upside potential.

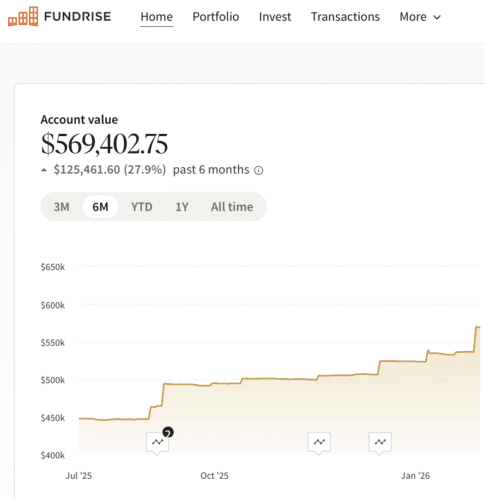

Consider Fundrise, a platform that allows you to 100% passively invest in residential and industrial real estate. With over $3 billion in private real estate assets under management, Fundrise focuses on properties in the Sunbelt region, where valuations are lower, and yields tend to be higher. As the Federal Reserve embarks on a multi-year interest rate cut cycle, real estate demand is poised to grow in the coming years.

I’ve invested over $400,000 with Fundrise, and they’ve been a trusted partner and long-time sponsor of Financial Samurai. With a $10 investment minimum, diversifying your portfolio has never been easier.

Subscribe To Financial Samurai

Listen and subscribe to The Financial Samurai podcast on Apple or Spotify. I interview experts in their respective fields and discuss some of the most interesting topics on this site. Please share, rate, and review!

For more nuanced personal finance content, join 65,000+ others and sign up for the free Financial Samurai newsletter and posts via e-mail. Financial Samurai is one of the largest independently-owned personal finance sites that started in 2009.

I didn’t realise how much of a tax advantage long-term capital gains offer, especially when total taxable income is managed well. The example showing how someone can earn up to ~$44K in long-term gains and pay no tax really puts things in perspective. It’s a good reminder to hold assets longer when possible and structure income across brackets smartly. Thanks for making it so clear!

Since stock selling will trigger short term or long term gain, would you sell stocks just to balance portfolio (i.e if your portfolio is not balanced and mostly stocks and would like to rebalance into bonds/ real estate)? Or would you just invest future capital into other areas and this would not trigger tax impact?

Question so for dividend income tax-free married file jointly I can make up to

$89,250 in dividends and pay no tax. My question is let’s say I make 99,250.

do I get taxed now at 15% on the entire 99k or is the first 89k free and the 15% comes on that 10k that was over

Another question would say i earn 150k and then 80k in dividends. ? do I get taxes normally on the 150k and get the income earned on dividends tax-free since it’s under 89k?

Great post and breakdown, Sam. I recently read a book by Lance Belline called More Wealth, Less Taxes. In short, if you structure your investments in three baskets (deferred, ROTH and brokerage) you can draw nearly $120k or so a year across the three baskets and pay nearly no / negligible taxes.

FS, I don’t see how this is double taxation. Seems disingenuous to call it such.

First, we pay taxes such as sale, excise etc. out of taxed income, and

Second, and more importantly how can you claim it’s double taxation when it’s only taxes on gains?

If anything, these taxes are unbearably too low relative to income taxes. What is the rationale for allowing investors to “underinvest” in govt. and get a break for money they didn’t earn? All the while getting a tax break for capital losses, too?

Because they take risk? Well, going to work is risky, and so are many actual jobs. And if one loses money, no tax breaks…

TBH, hearing folks like you and me whine about Cap Gains tax isn’t far off from whining about salty caviar!

Ah, nobody is whining. We just have to understand the tax code, and accept the way things are, and change our behavior accordingly to what we believe in that is fair.

100% double taxation. You use post tax money to invest, taking risk, and all the government can do is take more. There should be no such thing as capital gains taxes.

You’re getting taxed on the income you are earning from your investment, not the investment funding itself, which has already been taxed assuming it’s an after-tax account.

That’s like saying we shouldn’t be taxed on rental income because we bought the property using money that was already taxed once.

Well, I think all tax is theft, so….

First FS, you are nothing if not prodigious.

Second. I look to minimize my tax bill too.

Third, I accept that what I owe I should pay.

Timothy claims to believe all tax is theft. Hyperbole? Don’t know but it only makes sense if we live in a world without government – yeah, that’s called communism.

I had a lot of short-term gains in 2020 COVID year when I was swing trading for a few months.

Now it’s all about buying and holding for the most part. I like the idea of using the dividend income to buy in under-weighted holdings or just put into a diversified ETF.

I think paying long-term capital gains tax is better than being over-weighted within your asset allocation which could create more risk.

I’m not sure I understand, but would it be better to take a short term capital loss rather than a long term capital loss, or does the period held not matter?

Nice article.

One thing to point out: these are the tax rates on taxable income not on income. So at a bare minimum you should be adding $13,850 or $27,700 (standard deduction amounts) to the incomes posted before the tax brackets start to take effect.

Yes. Take a look at the bottom third of the post where I discuss standard deductions. Thanks.

I’m a little embarrassed, I wasn’t aware how favorable the brackets were for smaller long term gains. Mentally I always just thought of the long term cap gains rate at 20% (top of the range). It never occurred to me that I could take up to a $44k gain while paying nothing. Wild. I live modestly, $44k is actually a big majority of the funding that I need annually!

The more I read your posts -the more I get humbled…. I’m glad I found you

I think you’re slightly confused. I was initially confused myself too. The 44k gain at $0 taxes is only if you had no other taxable income for that year. If you have non cap gains taxable income like w2 day-job income, you have to look at your total taxable income in the ranges above to figure out your cap gains tax rate.

Thanks Jamie. Correct me if I’m wrong, but I think the $44k long term capital gain would effect the marginal tax rate for my earned income -but the capital gain still wouldn’t be taxed. Does that sound right to you?

Ohhh, now I see what you’re saying. Thank you

Here’s an example: Say you bought ABC stock on March 1, 2010, for $10,000. On May 1, 2022, you sold all the stock for $20,000 (after selling expenses). You now have a $10,000 capital gain ($20,000 – 10,000 = $10,000).

If you’re single and your income was $65,000 for 2022, you would be in the 15 percent capital gains tax bracket. In this example, that means you pay $1,500 in capital gains tax ($10,000 X 15 percent = $1,500). That amount is in addition to the tax on your ordinary income.

Another example:

Joe Taxpayer earned $35,000 in 2022. He pays 10% on the first $10,275 income and 12% on the income he earned beyond that, up to $41,775 (35,000 – $10,275 = $24,725). His total tax liability is $3,994.50 ($1027.50 + $2,967).

If Joe sells an asset that produced a short-term capital gain of $1,000, then his tax liability rises by another $120 (i.e., 12% x $1,000). However, if Joe waits one year and a day to sell, then he pays 0% on the capital gain.

Gotta total the income and capital gains and then pay the respective taxes accordingly.

Overall great article. One thing that jumped out though: “Even though long-term capital gains tax rates are more favorable, they are essentially a double taxation on money that was already taxed.”

Well, actually, the money being taxed as capital gains (long-term or short) is the money that was made by the principal you had invested, and while this principal is money you had already made, and was taxed when you were paid it, that principal is not taxed a second time (until you die, if then). It is only the new money earned by the principal that is subject to capital gains taxes.

Granted, it would be great not to have to pay any kind of capital gains tax on earnings. Which still makes getting as much as possible into a Roth IRA a good thing as, once there, the earnings due to increases in values, and to dividends paid, are not taxed, even when you initially draw them from the Roth IRA.

Since it never get any tax on this income, this is why the federal government has limits on how much money can be invested there each year.

All of which means any money held in a Roth IRA should be the last money the owner would ever want to touch, especially since there there is no required minimum drawing (RMD) required from a Roth (at least, not yet) making it the solid foundation, whatever its size, of almost any personal accumulation of wealth and savings.

Potato potatoe! :)

Yes, good point. Endless taxation makes earning up to the 0% LT capital gains tax threshold attractive.

Thanks for posting the 2023 rates! The income brackets went up a decent amount compared to 2022. I rarely have short-term cap gains these days but usually have some long-term gains when I file taxes. Speaking of which I need to tally up how much I had last year now that it’s tax filing season. Taxes used to make me feel so overwhelmed because I didn’t understand how they worked. But each year I try to learn something new and it’s really made a big difference in my understanding and strategies to save.

Thanks for the article, there’s a good amount of summary points. One issue though: The article shows being updated in Nov 2021 but the charts don’t seem to reflect 2021 info correctly…

There are many sources, this is just one that seems to match the IRS data:

putnam.com/literature/pdf/II985.pdf

No problem. My rates are for 2022. The link you provide is for 2021.

As a new subscriber, I feel kind of foolish asking, but……Under the heading, “Action Item For All To Strive For”……….How is it that a couple can make $77,200 in capital gains income and OWE NO FEDERAL TAXES ON THE L/T CAPITAL GAINS?? What did I miss?

Also, can one somehow convert real estate holdings into L/T capital gains for this purpose?

Thank you for helping me understand.

Pretty cool huh? It’s just the tax law for long term capital gains. You can actually earn about $100,000 and not have to pay federal income tax b/c the standard deduction for a married couple is $24,400. So, $77,200 + $24,400 = $101,600

The key is to accumulate a sizable taxable investment portfolio to generate such income.

Sam-

Thank you for the quick reply. I sincerely appreciate the response, as well as the incredible content you and your readers put into your site.

I know the standard deduction is $24,000.

Under the Action Item to Strive For, you state “Everybody should figure out how to generate at least $38,600 in annual passive income if you are single or $77,200 in annual passive income if you are married given the income is all capital gains tax free.”

Where in the article does it show you can have $77,200 in LT cap gains and not pay federal tax? I do not see a reference or a calculation for it anywhere.

Sorry if I’m missing something obvious….I just don’t see it anywhere in the article.

Thanks for bearing with this newbie :)

Yeah no problem. It’s in the chart. Sorry for not being more clear.

Sam-

No problem. I just missed seeing it in the chart.

There is so much information out there that it’s a bit bewildering at first.

Thanks again!!

This article sings to me. I am working on getting our passive, dividend income up as high as possible. It’s fun to be in a position where we are buying things that will help us buy more things. I am of course talking about financial instruments.

I had not considered a robo-advisor, and I need to take a look at that. I also need to verify that we are not getting taxed on that income, but I suspect the tax software I use does it right.

State municiple bonds are also something I am currently looking into. I got some great suggestions in a comment here, when I asked them a question about it.

My goal is about $200,000 in investment income. I’m at about 1/3 of that now, and we will see how the next few years help that along.

I retired at 46 and am going back to college for the first time. My net worth is only about 1.5 mil and I only owe 180k. My passive income from my rentals is around 65k per year. In Orlando that is more than enough to live a very comfortable lifestyle. I liked the article, and it reflects my reality. Life is very good and looking forward to whatever is next in life.

Exchange Funds are another way of delaying capital gains if you have a large chunk of stock that has grown. My wife and I recently used this strategy to diversify our portfolio and delay the taxes until we are considered Florida residents in another 5 years. That way we avoid the 9.85% state income tax of our current residence.

We want to be Florida residents in 3 years. Great information! What is your current state of residence? Our taxes here in IL are killing us! Plus being misspent.

Hi Sam

Thanks for the interesting article

Where is the real estate (rental) income in this scenario if someone have rental properties?

Thanks

Rental property is special b/c it can be shield from income taxes due to amortization, a non-cash expense. Any profits from rental property is treated as short-term income though.

yYou guys are all very financially savvy and I am a novice so bear with me. I listen to your podcast Sam and I appreciate your take on things. I am learning a lot but have a lot to learn. I have a question: I am selling an investment property and it will have a long term capital gains but I have a loss carry forward that hasn’t been used yet so we are going to use it against this sale. My question is: where do I safely save the cash until I am ready to purchase my next primary residence? We want to probably buy in a year but maybe less than a year if we score a deal in our (expensive coastal) neighborhood.

I would suggest a high interest savings account in an internet bank like ally bank at 1.9%. Although there is a maximum amount u can save in each of the accounts, ~200-250k. A lit of these banks have no issues with quick withdrawals.

I believe Vanguard does not have a limit on the Money Market max and it is at 2%+ with easy add and withdrawal.

Thanks for the Vanguard advice!!

Check out Treasury Direct

The math is eye opening isn’t it? Our tax system clearly favors early retirees.

The sweet spot is to hold enough bonds (non tax exempt) to use up the $24,000 standard deduction with the interest income and then generate $77,200 in dividends or LT capital gains from equities. You’ll make 100k of income and not pay any federal tax (you will owe state taxes though depending on where you live).

God bless America!

Great addition! And if you want to make more tax-free income, just buy and hold municipal bonds from your state.

sorry, but would the higher income from the muni’s raise your AGI and bump you out of the lower bracket?

Good question. I don’t think so because muni bond income is exempt from state and federal taxes, so the income it generates should count as part of your long term capital gains. I’ll double check.

I have a question…Let’s say I have one stock and earn dividend of $38,600 every year. I finally decide to sell the stock because it’s high and let’s say I make $300,000 in capital gain. Are you saying I don’t have to pay any tax on the $300,000 because my income is $38,600? I’m single and I’m in CA.

Thanks

No. You have to pay tax as the numbers are based off total income.

If all your income is from a $300,000 long-term capital gain, then you would pay a 15% marginal capital gains tax rate + a 3.8% tax on gains above $200K/$250K + any marginal state income tax.

If you have active income of let’s say $1,000,000, your $1,000,000 will face a 37% federal marginal income tax rate and your $300,000 will face a 20% LT capital gains tax rate + +.

For the first two tables on the long term gains tax and your income bracket, is that bracket your total income on your w2 for the year or your adjusted income after your deductions? I’ve had people tell me it’s one and not the other and then vice versa. Thanks!

Aren’t the gains rate brackets based on all income, not just the capital gains themselves?

Good point to clarify. I was looking at the long-term capital gains tax rate from an early retirement point of you with no active income.

Active income is taxed as short-term income. LT capital gains tax kicks in on capital gains income, but the active income portion lowers the level in whichever LT capital gains starts.

Eg. if you have $0 active income + $30,000 LT gains, you pay 0% LT capital gains tax. If you have $1M active income + $30,000 LT capital gains, you pay 20% LT gains tax + state + 3.8% NII.

Great post Sam.

Rookie questions: If you had $20,000 active income after deductions, and $20,000 capital gains, would you pay $0 on the active income, and 15% of ($40,000 – $38,700)? i.e. 1) are you still only paying the marginal rate for capital gains, and 2) is the threshold at which your marginal rate is calculated based on LT capital gains alone, or is it based on the sum of LT capital gains and your active income?

Along those lines, would it make sense for someone who is, say, transitioning between jobs and taking an entire calendar year off from work, and who has $35,000 in capital gains that she could realize in that year, to “realize” those capital gains during such a year, even if she intended to immediately reinvest but subsequently with a higher cost basis and a (hopefully) lower tax burden down the road?

For the past three years, Mrs. Groovy and I have had annual living expenses of $36K. We have a substantial capital gain in our one lone stock holding (a lithium mine), but the gain isn’t big enough to offset the loss of our Obamacare subsidy. Our Obamacare subsidy in 2018 is $27K. To have an effective capital gain tax in the 15% vicinity, my capital gain on our lithium stock would have to be somewhere in the low two hundred thousands. We’re not there yet. Perhaps in a couple years. C’mon electric cars!

Capital gains is a pita. I’m trying the hold forever option 1 and option 2 as much as possible. I used to have some turnover in my stock accounts with both gains and some losses but lately I’ve been trying not to have any sales to keep holding and avoid cap gains taxes. Great read!

I am looking forward to having the problem of figuring out what to do with my future mountain of long term capital gains. As a member of a young high earning couple, with positive cash flow (after all our savings, expenses of daily living and taxes) from our jobs, I am interested in getting the forum’s thoughts about using appreciated assets as collateral for loans to make further investments.

For example, say I have a long held index fund with 250k in unrealized cap gains yielding 4%. Rather than paying ~24% in capital gains tax, why not borrow 50k (assume borrowing cost 5-6%/year ) using stock portfolio as collateral and put that money to use and use yield from investment and your 4% dividend yield to service the debt and continue to grow your net worth without taking the tax hit? Your existing dividend income could service a loan up to 20% interest rate or >50% drop in value of index before you’d need to use outside funds to service the 50k of debt, which you have hopefully put to use in a productive investment that will generate income and hopefully appreciate as well.

-ECS