If you want to get smarter financially, it helps to think in extremes. Thinking in extremes makes financial concepts easier to understand.

Since 2009, I've been using my background in finance to help readers and listeners achieve financial freedom sooner. However, before I graduated from business school in 2006, my confidence in understanding financial concepts was tenuous. I was an economics major who thought about macroeconomic and microeconomic events.

Finance, economics, and investing can be intimidating. As a result, many people don't bother to learn them. Some even think finance is the language of the elite, which it is not. If a public school kid who got a mediocre SAT score can understand finance, so can you.

Out Of Consensus Call On Interest Rates

Because I enjoy reading and writing about economics and finance, the Twitter algorithm shows me related posts. Below is a post by Jim Bianco, a veteran financial research strategist who started his own firm 25 years ago. Jim is about 57 years old and I respect his viewpoints.

Jim goes on to write, “Yes, the Cleveland Fed has overstated CPI in recent months. But it has been by 0.1% or 0.2%. So, even factoring in an overstate again, August and September CPI are looking at relatively large numbers unless you want to make the case that they will massively overstate now, I cannot.

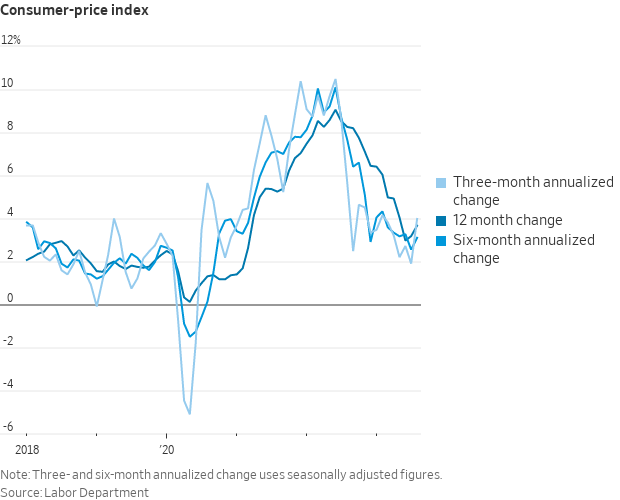

YoY CPI bottomed at 3.0% in June. If YoY CPI is pushing 4.0% by September (reported in mid-October), I cannot see how the Fed pauses from raising rates, and any 2024 rate cut is out of the question.”

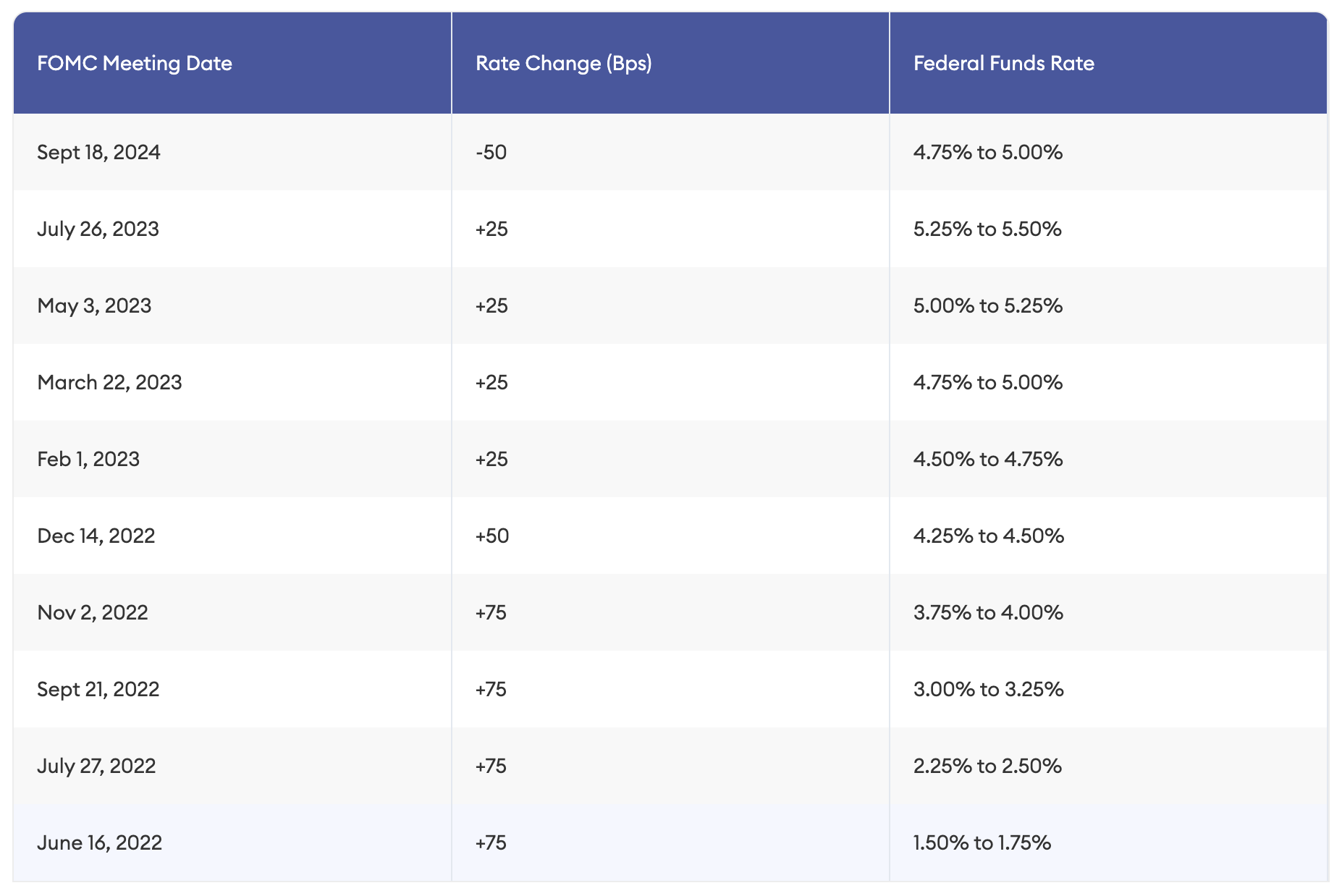

I appreciate Jim's point of view because it is not part of the majority. At the time of his tweet, the majority of economists, strategists, and researchers believed the Fed was done hiking rates for 2023, and would cut sometime in 2024. To be specific, only about 10%, 28%, 20% of traders believed the Fed would hike rates in September, November, or December, respectively. So if you were a betting person, you would bet on no rate hikes in 2023.

Take a look at what actually happened. The Fed did not raise rates in Q4 2023 and it did finally start to cut rates in Q3 2024.

Think In Extremes To Improve Critical Thinking

For anybody who drives, it was evident in fall 2023 that gasoline prices rebounded since the summer. Therefore, given gasoline prices are part of CPI, it shouldn't be a surprise if September CPI ticked up, when reported in October.

However, is it logical to assume the rise in gasoline prices would spur the Fed to hike rates more in 2023 and not cut in 2024? Not to me.

This is where thinking in extremes can provide some financial clarity.

What If Gasoline Prices Went To $20/Gallon?

To help understand this scenario better, we'll apply extremes. Let's say gasoline prices rise from $5/gallon to $20/gallon, an extreme move. It now costs $264 to fill up your empty Toyota Corolla tank. If you have a Range Rover Sport, it will now cost $492 to fill up your tank. Holy cannoli!

Given a large portion of the population can't live without a car for work or school, there will be a large reduction in disposable income. Of course a lot of people will switch to public transportation, car pooling, walking, biking, and scootering. But some will simply have to take the pain of rising gasoline costs.

With a significant consumption slowdown due to higher gasoline prices, is the Fed more inclined to raise rates or lower rates? Consumption (C) is the largest component of GDP. If gasoline prices stay at these elevated levels for months, another recession is all but inevitable.

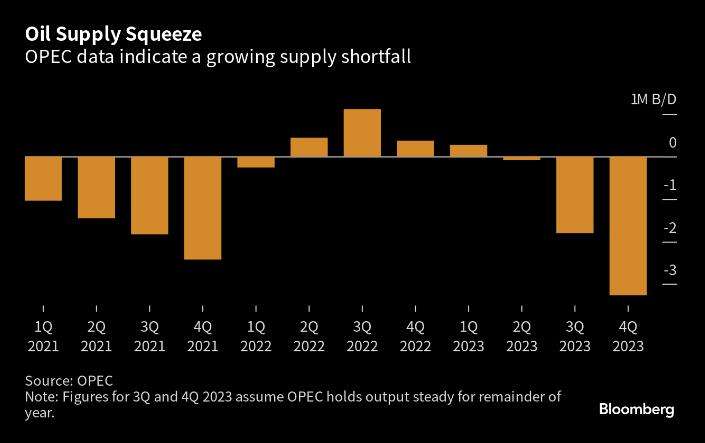

But maybe what Jim is saying is that higher gasoline prices are due to strengthening demand. Although what’s also plausible are production cuts by Saudi Arabia and OPEC and extreme heat shutting down supply as the main drivers of higher gas prices. See chart below.

Rising Gasoline Prices Help Do The Fed's Job

The Fed hiked rates aggressively in 2022 and 2023 to try and tame inflation. The higher borrowing costs go, the less people borrow and buy things they don't need.

Higher interest rates also crowd out private investment spending, given investors can now earn higher risk-free rates of return in money market funds, CDs, and Treasury bonds.

Higher gasoline prices are also a tax on the average consumer. But in this case, many people have no choice but to pay the higher gasoline prices.

With higher interest rates, on the other hand, not everybody will feel the same brunt. After all, roughly 40% of American homeowners don't have mortgages. And nobody is forcing anybody to take out debt to buy something they don't need.

In fact, for savers and investors, high interest rates are great! But unless you buy oil stocks or own oil fields, it's harder to benefit from higher gasoline prices.

Higher gasoline prices help the Fed do its job of slowing down the economy. Therefore, higher gasoline prices would be more of a reason to keep rates steady or even cut rates, not hike rates.

The Fed Could Still Hike Rates

Of course, the Fed could have still hiked the Fed Funds rate in Q4 2023 for a plethora of reasons. However, I don't think rising gasoline prices would be one of them.

More logical reasons would include a continued robust labor market, a re-acceleration in rents and home price appreciation, greater-than-expected increase in borrowing demand, and a return of speculative frenzy in the stock market. After the September 20, 2023 FOMC meeting, Chairman Powell opened the door for one more rate hike by year end. But that didn't end up happening.

12-month CPI rose to 3.7% in August from 3.2% in July, largely driven by gas prices up 0.6% in August.

Why You Need To Understand Finance

At the end of the day, the reason why you want to get smarter financially is so that you can make more optimal financial decisions based on your goals and risk tolerance. The more you can understand, the more you can prepare your finances for potential surprises.

Do not think finance is only the language of the elite. Everybody can learn finance to make better financial decisions. I've been trying to educate people about personal finance since 2009. So far, so good for subscribers of Financial Samurai.

Not only should you know finance, so should your children and all your loved ones. When you know something, it's up to you to teach it to others.

How I Plan To Invest

For me, if the Fed were to hike again in 2023, I was prepared for a potential sell-off in the stock market as a hike was not expected. I'd probably do some buying if the sell-off got bad enough, which is one of the reasons why I have dry powder.

If the Fed were to keep the Fed Funds rate the same for all of 2024, my plan was to invest more of my free cash flow into Treasuries and relax. Earning ~5.5% risk-free is wonderful given the income can pay for more than double our living expenses. Inflation remained relatively sticky in 2024 and the market expected a delay in rate cuts.

It wasn't until September 18, 2024 that the Fed finally cut rates by 50 bps. Therefore, Jim Bianco and all the other pundits who were talking about more rate hikes in Q3 2023 were wrong.

It's hard to be a great investor. But I say you don't have to be one to build great wealth. All you've got to be is a good-enough investor who asset allocates appropriately over the long term.

The more you can understand finance, the more confident you will feel about your money. The ebbs and flows of the world will also be easier to handle. Having a strong mind is one of the best sources of financial security.

Other Examples Of Thinking In Extremes To Help Better Understand

Maybe you're not convinced by my gasoline prices going to $20/gallon example. Here are three more examples of how thinking in extremes help you learn.

Example #1: Housing Contract

You don't understand why buying a home with contingencies is like getting a free call option. Think in extremes.

Instead of having a 30-day contingency, imagine having a 20-year contingency. In 20 years, you have the option to buy the house at today's contract purchase price if everything checks out. Therefore, having this option is worth a lot! As such, your goal as a buyer is to have as long of a contingency as possible.

Example #2: Bond Prices

You don't understand why bond prices go down when interest rates and inflation go up and vice versa.

Let's say a one-year bond costs $100 and pays a $3 annual coupon (3% yield) in a 2% inflation environment. How much would you pay for the $100 bond if inflation goes up to 100% a year? Probably no more than $50, or down 50%.

Even if you get all your money back ($100) in a year plus $3, due to 100% inflation, your $103 is worth only about $51.50 in real terms (can only buy $51.50 worth of stuff versus $103 last year).

In a 100% inflationary environment, there will be new bonds issued with a 100%+ yield to attract enough demand. Therefore, your 3%-yielding coupon is worth much less.

Example #3: Looking For Love

A girl rejects you and you don't know why. You're fit, good looking, and kind.

Your current occupation is unemployed after a five-year run at a big tech company. As a computer engineer, you're confident you'll find another job soon. She, not so much.

The girl is afraid you will end up living at home with your parents. After five years, you might spiral down a dark hole of despair because you still haven't found a job or purpose.

She doesn't want to risk getting dragged down in your misery because she grew up in a poor single-parent household. Her father was also once kind, but turned violent after the money disappeared.

Hence, by thinking in extremes, your solution is to move on or try again once you have a stable job.

Also Think In Probabilities

The more you can think in extremes, the easier it is to understand why things are the way they are.

Complimentary to thinking in extremes is thinking in probabilities, as I write in my bestseller, Buy This Not That. The more you can extend your thinking while mixing in probability analysis, the better critical thinker you will become.

Thinking in probabilities helps you accept your chances of being wrong and mute its impact if you are. Conversely, thinking in absolutes will make each error feel more devastating because you didn't prepare appropriately.

Finance, investing, and economics are complicated subjects. But over time you'll get more comfortable understanding everything you read by thinking in extremes and probabilities.

Subscribe To Financial Samurai

Listen and subscribe to The Financial Samurai podcast on Apple or Spotify. I interview experts in their respective fields and discuss some of the most interesting topics on this site. Please share, rate, and review!

Join 65,000+ others and sign up for the free Financial Samurai newsletter. Financial Samurai is one of the largest independently-owned personal finance sites that started in 2009.

Please comment on the Government’s Fed Now digital

Banking program to control our

Money! How do we protect our funds from the Feds taking it?

On the note of looking at extremes….I do this is my retirement planning.

I have a section called “Game Theory” below my expenses, ROI expectations, income and so on.

Basically, that section of my spreadsheet has (8) sub sections. I figure out the NPV for each event…THEN (this is the ambiguous yet helpful part for me) the probability of that event. I omit any event with under a 5% chance of happening.

1.) Events with large positive ROI IN my control.

Sample Events: things like will increase 401k contribution 10k starting in 2025. NPV of 10k more for 12 years, 200k, 80% chance of happening, risk adjusted NPV is 160k

Sample Events: buy a 2 unit and live 1 unit when the kids go to college in 2037. NPV of 500k … 20% chance of happening (wife has mixed thoughts on the idea lol). Risk adjusted positive NPV of 100k

2.) Events with small positive ROI IN my control.

Sample event: things like get a small raise / bonus / side hustle / reduce expenses

3.) Events with large positive ROI IN NOT my control.

Sample Events : If my investment returns are 1% higher than my conservative estimates. If inflation is lower. Medical costs dont inflate as much as I think they will.

4.) Events with small positive ROI IN NOT my control.

Sample Event: technology makes some daily life item cheaper, social security payments arent delayed as much or reduced as much as I am planning on. 1 spouse dies earlier than planned (morbid…but reduces expenses).

Then I add up the risk adjusted positive NPV’s

5.) Events with large negative ROI IN my control.

Sample: let adult children or grand children live with us. Decide to take a lower paying job

6.) Events with small negative ROI IN my control.

Sample: provide financial assistance to parent or family member for a short duration

7.) Events with large negative ROI IN NOT my control.

Sample: have a large unreimbursed medical expense, ss payments reduced more than expected, 1 spouse becomes disabled,

8.) Events with small negative ROI IN NOT my control.

Sample events: lose a job for a year and stop contributing to retirement savings, dollar loses value and all my imported goods go up in cost, water shortage and water 3x-es in price.

Then I add up the risk adjusted negative NPVs

***This is key*** I add extra value to the risk adjusted NPVs…..why….because there are risks beyond my comprehension. I add 1% for EVERY YEAR between now and retirement and 0.5% for ever year between retirement and death to account for “adverse events beyond imagination”. I explain WHY below.

Then…add up the positive NPV events, negative NPV events, your negative NPV adjustments (explained below) and that is how you should adjust your target retirement number up or down.

WHAT IS COOL about this:

1.) allows your to account for ALL the “what ifs” in your head. Just come up with an NPV for the event and weight it for how likely you think/feel it is.

2.) the extra percentage points for the negative event NPV’s….REDUCE over time as you near retirement….giving you more option to retire earlier WHILE having enough for most any event.

3.) helps plans for the changes in life. Each year I can remove events or change probabilities. For example….once my kids have 100% lived outside of my house for a couple years, I will feel confident they are gone for good and will 100% remove that event…which will push me to retirement even faster….ONCE and ONLY after that risk is “neutralized”. Of course…the same can be true for factoring in positive NPV events like planning to save more in 2025 (when I no longer pay for daycare).

4.) the 1% of negative event NPV I add before retirement and 0.5% between retirement and death…..also reduce the older I get. The older I get….the shorter the window for negative events to occur and the more comfortable I can be retiring sooner.

A little more deep dive on the negative event adjustments:

Mechanics: I add 1% to my total negative NPV value for every year BEFORE my estimate retirement date. I am 39, and plan to “soft retire”….go to part time consulting at age 54. So I adjust my negative NPV value up 15%.

THEN I increase my negative NPV up 0.5% for every year I estimate me/my wife being retired before death (which I estimate at 98 for us to be conservative). Retirement of 44 years (98-54) times .5% is 22%. So I increase my negative NPV by another 22%. All in…my negative event NPV gets inflated 37%. BUT….lets ASSUME all the my negative risks are STILL risks by time I am 54 (they wont be) …. at 54….my “inflation” of negative events will simply be 22%….thus REDUCING the amount of money I need to a safe retirement…..as you approach retirement….your “RE” number falls faster and faster.

Why do I increase pre retirement more than post retirement? 1) The affects of a negative event will be felt much longer if it were to occur preretirement. Don’t forget…I am planning for unknown events with unknow consequential severity 2) My whole financial model is built on taking more risks and getting more return preretirement…then unrisking (to a degree), post retirement. So I have somewhat less downside in unimagined, negative NPV financial/investment events.

Why not just increase negative NPV events by a flat percentage?

Here is the cool part…..the older I get….the lower the chance events will happen before my retirement date or before my death. So….as I age….I will naturally (from this method) need a slightly smaller nest egg each year because I “over saved” when I accounted for these unknown events. IF an unknown events comes up … I am also covered (either wholey or to some degree…that is arguable based on the event/severity.

Also as I age….uncertain events and certain events….fall off. So I can factor in things that will help me down the road….things that could hurt me….and things I cant imagine. Could I factor in unimagined events that benefit me…I could….but I am more a sceptic than an optimist.

Can this be adapted for you….sure…..first…my game theory is super granular…you could just separate things that benefit you and are adverse to you….instead of separating by how much. You could/should adjust the negative event NPV adjustment percentages. Admittedly….I just went with percentages that felt palpable to me.

ALSO….worth noting….to young people….this game theory WILL distort your retirement amounts higher far more than someone in their 40, 50s or closer to retirement. That is by design. As you age and uncertainties in life before certain….you get a more accurate FIRE number. I dont think this is a bad thing though….it helps motivate younger people to save more (when they are less experienced at life) and have more money for when life settles and they are more mature to decide to either spend and enjoy more, retire earlier or help others more.

Extreme thinking situation. Radiology, at the time I graduated Med school (1996) was being viewed as a poison branch of medicine to get into. It was at a time when the government wanted to save money, so they decided Internal care or primary doctors were going to be the ones deciding whether or not to order expensive Radiology imaging studies. Primary care docs were incentivized to save money by restricting access to specialty imaging. This put a huge damper on smart med school graduates to go into Radiology. Not so many Radiology exams ordered, not so much money to be made. Until that point, Radiology was one of the toughest training positions to get into, because of the money to be made for not a hard day. To get a spot in Southern California, or anywhere in California, was impossible for anyone but the cream of the crop with connections. I figured that the “Gatekeeper to Radiology studies” fear was overblown. I applied to several SoCal spots, had several interviews, and chose Loma Linda in Redlands, Inland Empire, one of the prettiest places to me, in a gorgeous hospital. It was like the seas parted to make room for me. A couple of years later CT scans were gaining in popularity throughout medicine, especially in the Emergency Department, where “Get a CT” helped ER docs move patients expeditiously to the correct next stop…surgery, medical internist, or home with meds. The gatekeepers died a quick death. I did have a successful career for 17 years.

Now, the profession is so extremely busy. CT and MRI’s are ordered profusely, for the expediency and partly because fear of lawsuits. “Oh doctor, the patient had a headache and you didn’t get a head CT?”

Yes! So true and super helpful. I’ve done something a little similar to this with big, round numbers when trying to understand new things in the tax code.

I’ll also be curious to see what happens with the fed the rest of the year.

Sam,

In the article you stated:

“To be specific, only about 10%, 28%, 20% of traders believe the Fed will hike rates in September, November, or December, respectively. So if you were a betting person, you would bet on no rate hikes in 2023.”

But don’t you think the key to winning a bet is about exploiting the margin between expectations and reality? If 10% of traders think the Fed will hike rates in September, but the actual (though of course un-knowable) reality is that there is a 20% chance they hike rates – can’t you make the best money by betting against the majority in this case? I only mention this because I find that sometimes people suffer from groupthink, and that when a lot of people think a thing, the expectation that the thing will be true is often actually higher than the reality-based probability.

Now I’m not so sure in this case, and I’m not some hyperactive day trader looking to exploit every small advantage. But I thought I’d get your thoughts on this if you care to reply/elaborate.

Thanks much!

Absolutely. There are derivative investments you can invest in that can capture these differences. One of the keys would be to sell BEFORE the actual event, but after the appreciation in the investment. Because if the Fed does hike in September, for example, 10% to 20% chance doesn’t matter. It is an absolute result.

Mr Sam, have you considered suggesting your readers to under spend their income, budgeting and indexing. You can get rid of all your other posts. Sure,they do carry some entertainment value, but how about some sound financial advice .

I’m a poor guy and need to learn the basics. Not only do I lack financial intelligence, I also lack emotional intelligence.

Sorry to hear about your difficulties Ram. It does help to be a nice person. So I’d start with that. I’d also reach out to a financial advisor who can look over your situation thoroughly.

See:

How To Develop Emotional Intelligence

Your Lack Of Emotional Intelligence Is Costing You A Fortune

The Recommended Split Between Active And Passive Investing

Hey Ram – I was a loser once. And the only way I got out of it was to take control of my own destiny. Insulting other people, telling people what to do, and complaining why life isn’t fair isn’t going to help you.

You must blame your lack of financial intelligence on your lack of studying. Same thing if you have no friends, don’t have a promising job, and are struggling financially. If you want to get better, you’ve got to put in the work.

Good luck to you! At the end of the day, it’s your life to live and nobody else’s.

Hi Jerry , you are still are a narc . The great Warren buffet has advices to put his money in index funds after he is gone , 99% of the actively managed funds don’t beat an index over the long run . What have you done champ .

Sam has helped my clarify my investment approach. I budget and invest in index funds, but I also purchsed 3 condos in the sunbelt due to insights gained from this site. I am less nervous about the movements of the market, and more diversified. So please dont be a prick. As someone with zero background in finance, Sam explained many things to me and for that I am gratful. Without this site, there is no way I would have had the confidence put most of my into idexes and also diversify into RE. I am gratful.

Appreciate the note! Once one has a better understanding of the finance language, confidence follows. And this confidence brings about more peace of mind during rocky times.

Fight on!

You might enjoy my podcast on Apple and Spotify too if you don’t know I have one. I’m trying to record more regularly for the next 10 years.

Exactly why I’m having such a hard time pulling the trigger

Uncertainty for next 40 years feels much greater than the past 40 years.

Pulling the trigger on what though?

Hey Sam!

Great exercise in thinking of the extremes. Too often we are worried about the little things when we should really be using the extremes to change our perspective.