If you’re trying to figure out how much to spend on a house, my 30/30/3 home-buying rule is the best guide I can offer. I developed this rule in 2009 during the global financial crisis, and since then, it has gained worldwide recognition from numerous publications and industry experts.

Following the 30/30/3 rule gives you a greater chance of weathering any financial downturn. It keeps you disciplined when buying property in a strong market and minimizes risk in weaker ones. While it may limit your gains during a housing bull market, it ensures peace of mind and steady wealth-building.

Even adopting just one part of the rule can reduce financial stress and help you enjoy your home more. But for the greatest sense of security and balance, I recommend following at least two—ideally all three—principles of the rule. After all, buying a home is likely the largest financial decision of your life.

Too many homebuyers overextended themselves during the global financial crisis, leading to widespread short sales and foreclosures. Even if you managed your finances responsibly, the ripple effects of struggling neighbors could hurt your property value and wealth. The 30/30/3 rule is designed to protect you from such risks and keep you financially sound.

My Real Estate Background And Views

I’ve been investing in real estate since 2003 and currently own multiple rental properties valued at over $5 million. These properties, along with my private real estate investments, generate between $150,000 and $200,000 annually in passive-to-semi-passive income. In 2009, I founded Financial Samurai, now one of the leading personal finance websites in the world, with over 1 million pageviews per month.

My outlook on the housing market over the next decade remains positive. America faces a structural undersupply of 2 million homes per year, while pent-up demand continues to grow. With the Federal Reserve entering a multi-year interest rate cut cycle, combined with the surge in the S&P 500 and advancements in artificial intelligence, real estate prices are poised to catch up.

Ultimately, my goal is to help everyone buy a home responsibly. That’s why I strongly recommend following my 30/30/3 home-buying rule. This rule not only minimizes stress but also helps safeguard our economy. Let's explore my home-buying rule in greater detail with some examples.

Boost your wealth through private real estate: Invest in real estate without the burden of a mortgage or maintenance with Fundrise. With over $3 billion in assets under management and 350,000+ investors, Fundrise specializes in residential and industrial real estate. I’ve personally invested $300,000 with Fundrise to generate more passive income. The investment minimum is only $10, so it's easy for everybody to dollar-cost average in and build exposure.

The 30/30/3 Home-Buying Rule

Here is my 30/30/3 home-buying rule to follow. The goal is to follow each part of the 30/30/3 home-buying rule to be a financially responsible home buyer. If you can’t, you must follow at least one.

Home-Buying Rule #1: Spend no more than 30% of your gross income on a monthly mortgage payment.

Traditionally, the industry says to spend no more than 30% of your gross income on your monthly mortgage payment. However, as mortgage rates continue to decline, more people are tempted to increase the percentage.

When mortgage rates are lower, you can already buy more home if you keep your spending as a percentage of gross income fixed. The danger emerges when you break this home-buying rule percentage to buy an even more expensive home.

The people most at risk of breaking the first rule of home-buying are middle income to lower income people.

Spending 40% of your monthly $50,000 gross income on a mortgage still leaves you with $30,000 in gross income. However, spending 40% of your monthly $5,000 gross income leaves you with a much smaller cushion.

You must be able to take care of your basic needs with the remaining money. Therefore, it is safer to spend less of your monthly gross income on a mortgage the more income challenged you are.

Home-Buying Rule #2: Have at least 30% of the home value saved up in cash or semi-liquid assets.

Before buying a home, you should have at least 30% of the value of the home saved in cash. 20% is for the downpayment to avoid PMI insurance and get the lowest mortgage rate. The other 10% is for a healthy cash buffer just in case you run into financial trouble.

I realize that there are programs that allow you to put down a smaller down payment. However, during times of maximum uncertainty, it's better to have a larger financial cushion.

The homeowners who got blown out the quickest during the previous recession had minimal down payments. With minimal equity, the temptation to walk away from a mortgage is much greater. The thousands who did between 2008 -2012 missed out on one of the largest real estate recoveries ever.

If you are planning on buying a home within the next six months, keep at least the 20% down payment in cash. It is unwise to invest your downpayment in stocks and other risk assets if your home-buying time horizon is so short.

If you don't have at least 30% of the value of the home saved up, it's time to curtail your desires. Eat ramen noodles for the next six months to save money. Start a side hustle to boost your income.

Borrowing the downpayment from the Bank of Mom is pretty common nowadays. However, before you do, you need to ensure that you aren't putting your parents at financial risk.

Home-Buying Rule #3: Limit the value of your target home to no more than 3X your annual household gross income.

The final part of my 30/30/3 rule is great for doing a quick scan at homes you can afford.

Home affordability based on cash flow is a function of the price you pay for the home. If you are able to meet the first two home-buying rules, then you can tie it all together with the final home-buying rule.

Rule #3 is a quick way for homebuyers to screen for homes in an affordable price range. The rule also takes into consideration down payment percentages and prevents one from stretching too much, even with a high down payment.

If you earn $100,000 a year, you can comfortably afford up to a $300,000 home. Or maybe you are lucky enough to earn a top 1% income of $500,000 a year. If so, then you can comfortably afford up to a $1,500,000 home.

If mortgage rates are declining and you're bullish about your income growth, you could stretch the third home-buying rule and extend the home value up to 5X your annual household income.

Just know that 5X a larger salary not only means more absolute debt, but also higher property taxes, maintenance expenses, and so forth. Make sure you run all the numbers before you make any home purchase.

With the expansion of the multiple up to 5X, you can also name my home-buying rule the 30/30/3-5 rule. But I wouldn't spend much more than 3X your household income on a home if your mortgage rate is over 6%.

Home-Buying Examples Using My 30/30/3 Rule

To help illustrate my home-buying guide, here are some examples. Buying a home is an incredibly emotional process, so it's good to run through the numbers. The last thing you want to do is buy a home and feel stressed every night about your finances.

Two examples of following or closely following the 30/30/3 home-buying rule

You make $100,000 a year and have $120,000 in cash saved. You desire to buy a $300,000 home. After putting 20% down, you have a $240,000 mortgage.

The monthly payment is $1,012 or just 12% of your monthly gross income. With a $60,000 cash buffer left, you have almost five years of mortgage expense covered.

With the same income and cash savings, you decide to live it up a little and buy a $400,000 home instead. After putting 20% down, you have a $320,000 mortgage and still have a good $40,000 cash buffer.

Your monthly payment is $2,022/month at a 6.5% mortgage rate. The payment is still only 24% of your monthly gross income of $8,333. This is good compared to the 30% maximum recommendation.

When mortgage rates are lower, stretching to buy a house worth 4X or even 5X your annual income is possible. However, I do recommended sticking to a 3X multiple if you want that wonderful feeling of financial security.

If America was filled with homebuyers like this, then the 2008-2009 housing crisis would not have been nearly as bad. Unfortunately, too many homebuyers didn't follow the 30/30/3 home-buying rule. Most of us suffered as a result due to foreclosures and short-sales that brought our property values down.

Don't forget, there was once a time when most home buyers bought homes with cash!

An example of someone not following the 30/30/3 home-buying rule

You make $120,000 a year and have $100,000 in cash saved at 32 years old. Not bad. However, you're also salivating for an $850,000 home, which equates to 7X your annual income.

You can't put 20% down so you only put 10% down. This leaves you with only a $15,000 cash buffer and a $765,000 mortgage.

Due to a lower down payment, the best mortgage rate you can get is 6.875%. This is still low by historical standards. However, your monthly payment of $5,025 is 50% of your $10,000 gross income. It’s probably closer to 60% due to PMI. You have now violated all three of my home-buying rules.

If you lose your job, you will run out of cash in three months. You may get lucky holding on with enhanced government unemployment benefits and a couple stimulus checks. However, think about how stressed you will be during this time period.

Instead of buying this home now, first save up another $155,000 to get to $255,000 in cash and semi-liquid investments. With 30% of the home price saved, you can put down 20% and have a nice $85,000 cash cushion.

Further, your mortgage will decline to $680,000. At a 6.5% mortgage rate, your mortgage payment would be $4,298 or 43% of your monthly gross income. If your income increases while you are patiently saving for a larger downpayment, you will eventually get down to my 30% guideline.

Another example of a terrible violation of the 30/30/3 rule

Rule #3 helps prevent a homebuyer from going off the deep end. Sometimes, people confuse their own true buying power with reality. Receiving a windfall can play tricks on some people.

Let’s say you make $70,000 and have a $500,000 down payment due to an inheritance. You feel rich! As a result, you may be tempted to buy a $1 million home since you can put $500,000 down.

If you do, your $2,316 monthly mortgage payment equals 40% of your monthly gross income. But then you get furloughed shortly after purchase with no pay. Three months into furlough, your boss says they won't ever be hiring you back. You are screwed because you have no cash buffer. You thought the $500,000 windfall would be a regular thing. But people only die once.

You end up going into foreclosure. Your credit and finances are ruined. The property values on your block all take a hit thanks to you. Your financial life is over for several years.

Or in one man's case after foreclosing on his home, he went on to get a job at The New York Times as a finance columnist. That's right, even after deciding not pay back his mortgage, he still got a job giving financial advice. Anything is possible folks.

Ways To Get Around The 30/30/3 Home-Buying Rule

Although the 30/30/3 home-buying rule may seem stringent in such a low interest rate environment, just know plenty of people pay all-cash for their homes too. This idea of taking on lots of debt to buy property hasn't always been the norm.

If you want to violate the 30/30/3 home-buying rule, then at least consider the following:

- Rent out a room or a portion of your house

- Create a business on the side to have a legitimate way to deduct a home office and other expenses like internet

- Be in line for a raise or secure a new job with a raise and promotion

- Build new passive income streams to help pay for your homeownership expenses

- Be really good to your parents and rich relatives

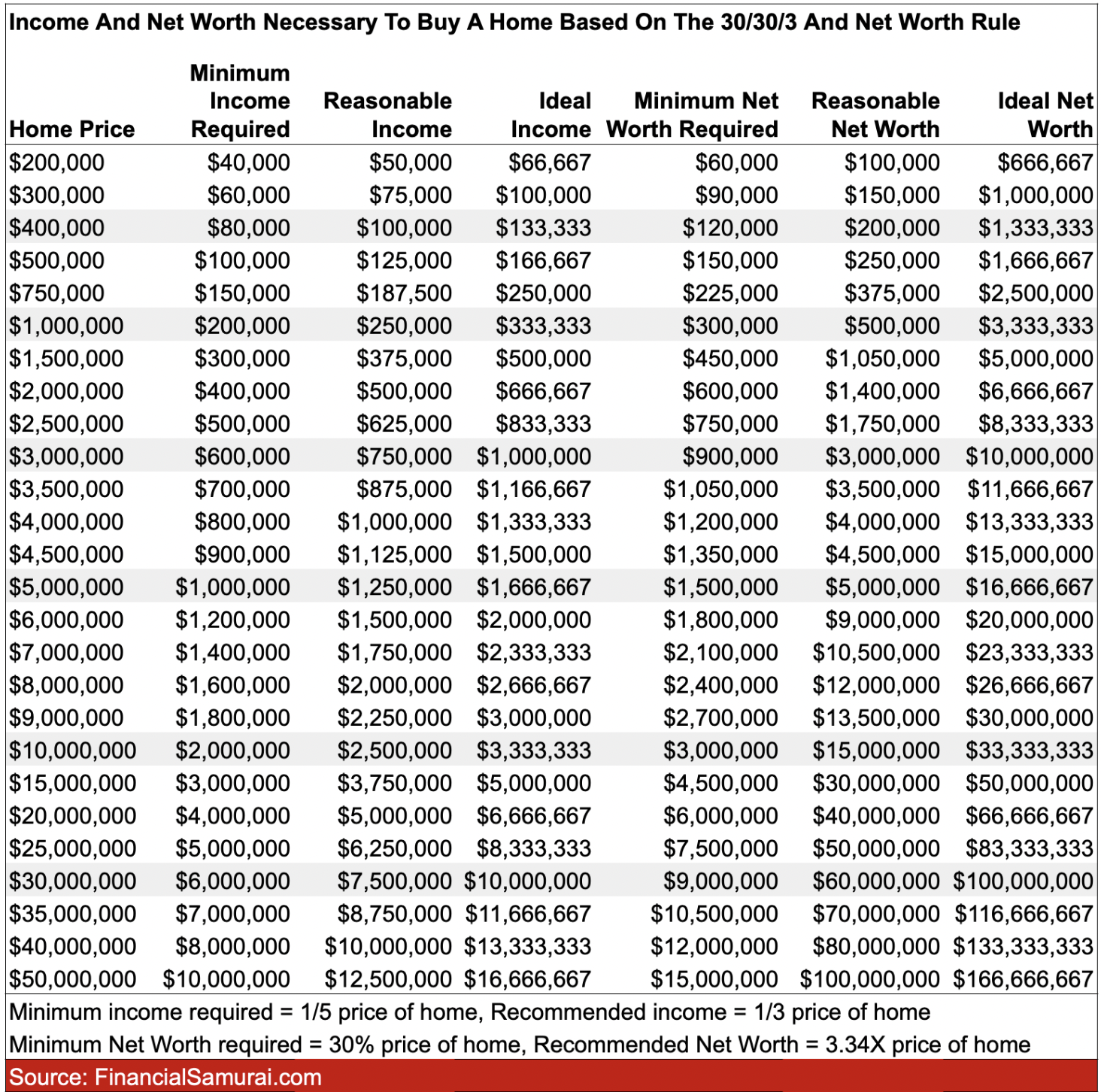

Income And Net Worth Necessary To Buy A Home Using The 30/30/3 Home Buying Rule

For those of you looking for an easy chart, here's one I created that shows how much you should make and what your net worth should be before buying a home. The recommendations follow my 30/30/3 home buying rule.

Have Discipline When Buying A Home

I get your desire to own a nice primary residence (another home buying rule based on net worth). I've been a real estate fanatic since I was in college. We want to live life to the fullest now! What's the point in working so hard if we're just going to hoard our cash right?

A home can be a solid investment. It not only provides shelter, but it can also be rented out. Your home could even appreciate handsomely in value over time. Due to home price appreciation, many people I know have effectively lived for free over the decades.

Further, if your kid graduates with no employment prospects after four years of college and $200,000 in tuition expense, he can live in one of your investment properties. There would be no need for your adult child to live with you. This option may be worth a lot to some investors.

Despite all these benefits of investing in real estate, just don't overextend your finances when buying a home. The stress is not worth it. Here's a podcast episode where I talk to my wife about overcoming the emotional stress of buying a new home.

Keep Housing Expenses To A Minimum For financial Independence

For those of you who are looking to achieve financial independence sooner, follow the FI home-buying rule. This rule recommends you keep your home expense to no more than 10% of your monthly gross income.

If you follow the FI home-buying rule, your path to financial independence will be much swifter. You may even start feeling as light as a bird.

At the very least, please follow my 30/30/3 home-buying rule before making one of the biggest purchases of your life. It'll be good for you in the long run. It'll also be great for your neighbors and the entire financial system as there will be less of a chance you'll be foreclosed.

Best of luck in your house hunt. Please stay disciplined! I expect the real estate market to stay strong for years post-pandemic. But that doesn’t mean you should go overboard when buying a home.

Real Estate Recommendation

If you don't have the downpayment to buy a property, don't want to deal with the hassle of managing real estate, or don't want to tie up your liquidity in physical real estate, take a look at Fundrise. Fundrise is one of the largest real estate crowdfunding companies today with diversified real estate funds focused mainly on Sunbelt real estate, where valuations are lower and yields are higher.

If you like to invest in individual real estate opportunities and are an accredited investor, take a look at CrowdStreet. CrowdStreet focuses mainly on real estate opportunities in 18-hour cities, where valuations tend to be cheaper and growth rates tend to be higher. You can build your own select real estate portfolio with CrowdStreet. Just make sure to diversify and do further due diligence on every sponsor and deal.

Personally, I've invested $954,000 in private real estate, $300,000+ of which is in Fundrise, to diversify my real estate exposure, take advantage of lower valuations and higher rental yields across the country. As I get older, I also want to simplify life and earn income more passively. The spreading out of America is a permanent trend post-pandemic.

Both platforms are sponsors of Financial Samurai and Financial Samurai has invested over $300,000 in Fundrise so far.

The 30/30/3 Home-Buying Rule is a FS original post. FS has been around since 2009 and is one of the largest independently owned personal finance sites in the world. Everything is based off firsthand experience. You can join 60,000+ others and sign up for my free weekly newsletter here.

Hey Sam, How do you factor in RSUs and bonuses into income? My income has steadily increased in the last 3 years, but that is mostly due to refresher stock grants and price appreciation. But it has reliably increased. Do you discount bonus and stock?

I’d include it, but try and take an average over the past three years. Good to be conservative as stock prices can easily go down.

This rule doesn’t work in california

You can stretch from 3 to 5 times your household income, but you need to be bullish on your career prospects and income growth.

You can also put a larger down payment up down.

But ultimately, the best solution is to make more money before you buy that home.

Hi FS, I think I can say I’ve read alot of your posts over the years v and to be honest after going from link to link trying to find this one thing. I think you’ve never mentioned it so I’ll figure I’ll finally comment.

How do you decide on how much income to buy an investment property?

In my view this is somewhat a tough one, especially buying in today’s time. Sure, the tenant pays for the house, but if u’re vacant you’d have to be the one paying for it. So now should I think about this? Thank you

Depends on how you want your passive income streams diversified (the more the better in my opinion as I have 5) and what type of liquidity you want. For investment purposes RE should depend on the cash flow after expenses, CAP rate. So if you think a cap rate of 5%(the higher the better) is good then do it if the RE market in the area has a long-term in demand area for appreciation sake. Buying a single home or property lacks diversification and usually requires your participation in managing the property while FundRise and EquityMultiple gives you diversification and minimal effort on your part to manage the asset(s).

So if you buy a house for $500,000 cash then you would want to be cash flowing 5% after all expenses including saving for future maintenance costs, =$25,000/yr + appreciation of the property. Having a mortgage will increase your expenses but give you more leverage on appreciating your equity in the property. Buying a rental property at a destination will allow you to deduct travel expenses and if the property is rented thru Airbnb or VRBO then you can use the house up to 2 weeks per year without the property being reclassified as a 2nd private home.Basically a vacation destination with expenses being deductible against income. A good time to perform maintenance on the property if needed.

While I’m all for financial responsibility and discipline, I’m going to present a counter to your advice here. I think these ratios have utility for someone who makes a decent salary and is debating “do I buy house A at $X or house B at $Y?” While the guiding principles of buying what you can most reasonably afford and saving as much as you can before buying still apply, I think the 30/30/3 numbers lose their helpfulness when they do not compare the fully loaded cost of renting into the mix. A detailed example follows.

In a real-world scenario, lets say Sam lives in the same Mid-atlantic metro area I live in. He is not privileged but is a hard worker, got an associates degree and after a few raises now makes $48k. (in my region I don’t think this scenario is far off from a good percentage of the workforce although admittedly there are many who make dramatically more). He diligently puts aside money and has saved up $20k for a house. He looks at these “rules”, sees the “average” 3 bed starter home sells here for $400k, a less desirable neighborhood or smaller home maybe in the high $300’s but for $250k he can likely buy a smaller 2 bedroom fixer-upper in bad shape. It isn’t pretty (shag orange carpet with who-knows-what stains, pink toilet, odd paneling in the living room, overgrown yard and other quirks) but he can live with it and put sweat equity in each weekend to slowly fix it up. He’s competing with cash buyers looking to flip but lets say he actually has a shot at his offer being accepted.

He gets excited about the possibility and does the math under these rules: 30/30/3.

Rule 1 – 30% of gross income – $4k/mo means he can afford $1,333 in monthly housing payments. Nope, that’s not happening w/ a $240k mortgage at today’s interest rates. P+I alone is almost $1300 at 5%, $1400 at 6% and if he adds taxes of $2k/year, insurance of $1k/year and mortgage insurance he’d be at/over $1600/mo, well over the 30%.

(Assume the $20k he saved went $10k towards closing costs and $10k towards the principal purchase price).

Rule 2 – 30% down. He’s nowhere near this. In fact, he feels downhearted when he realizes his $20k savings, dramatically more than 90% of his co-workers who live paycheck to paycheck, doesn’t even tip 10%.

Rule 3 – 3x income. By this rule, he could afford $144k, and even the cheapest handyman’s special in the county is going for $100k more than that.

If Sam looked at the 30/30/3 rules he’d assume he should NEVER buy. But let us please consider the alternative – he’s got to live SOMEWHERE so lets say he rents. Again, he’s in my real-life Metro area. A 2 bedroom apartment goes for $2,000 – $2,500 /mo if he’s staying modest, nothing fancy. He goes for a tiny 1 bedroom at $1,400-$1500/mo. Sam resigns himself to renting… he gets another raise to $50k, still can’t buy with this ratios, but rent goes up. As it has in this area for as long as I’ve been living, rent goes up every year at 3-5%.

Fast forward 10 years. Sam if he followed the “rules” is still stuck renting. His rent just increases & increases each year and he has absolutely NOTHING to show for the $200,000 or so he’s paid in rent for 10 years (assuming he’s kept the tiny 1 bedroom).

Now what would Sam’s position be likely if he would’ve instead bought the fixer upper for $250k despite the fact it didn’t quite fit in the ratios? 10 years into a 30 year mortgage, he’d now owe somewhere between $180,000 – $200,000 on the loan. But with his DIY work on the weekends and increase in housing costs in the intervening decade, his home is now very realistically worth $350,000.00 or more. So he’s increased his net worth by $150,000. He talks to a former buddy who rented the cheap 1 bedroom apartment he was considering all those years ago at $1500/mo rent and realizes that with an annual rent increase of 3% each yeare, his buddy now pays $1,957/mo in rent. Meanwhile Sam is still only paying $1,600/mo. for his house.

If mortgage rates have dipped in those 10 years, or if Sam would benefit itemizing deductions his financial picture is even better. And this is just 10 years in. After 30 years, Sam is ready to retire in a fully paid-off house while he (or his buddy) rented his whole working life, he might be panicking, realizing he just cannot afford to retire.

Anyway, that is pretty close to several real-life people I know. Granted, if Sam was irresponsible and spent beyond what he could afford in other areas, say buying new cars every few years (or didn’t curtail other expenses in the first years after buying) he might very well face foreclosure and lose his house. But he wouldn’t have had cushion if he rented and lived that way either.

I hope that summary explains, respectfully, why I feel these ratios do not adequately take into account a fuller picture when it comes to renting vs. buying for people who are looking to buy the cheapest house they could possibly get vs. renting at market rates. Generally, the wisdom to 1) keep monthly costs low 2) save as much as you possibly can to put down and 3) buy the lowest price house in your budget/range is wise. And I think that is what your ratios intend to convey. So I’m not bashing them, just respectfully suggesting they should be considered AFTER comparing renting vs. owning at the base level in one’s region. If one concludes that fair market for the most affordable rentals would cost close to the monthly expense for the contemplated purchase it is still likely prudent to buy, even if all the “rules” are broken.

I realize that is very long-winded, hope though that the thoughts help someone reading this.

Fair points. I have stretched the 3X to 5X your salary if you’re confident about the growth of your income.

And yes, taking on huge leverage and stretching to buy the most expensive house a bank will allow you to buy can play out handsomely in a BULL MARKET.

But don’t forget two things.

The first thing is that bear markets do happen. Do you remember where you were in 2008-2012? Plenty of people went into foreclosure, or had to do a short sale, because they lost their jobs, or didn’t make as much as they anticipated, or their mortgage went up.

The other thing to know is that renters are not helpless. They can invest their free cash flow into stocks, public REITs, and private real estate funds like the ones offered by Fundrise during this hypothetical 10-year period. They will likely not make as much in a bull market given the lack of leverage. However, they will still build their wealth in a risk-appropriate way.

At the end of the day, my 30/30/3-5 home-buying rule is just a guide. Nobody’s gonna get fined or go to jail if they violate my rule. If you want to use my experience and expertise to feel great after a home purchase, then feel free to follow it. If you want to roll the dice more aggressively, ignore it. Everything is rational in the end.

Related post: I climbed to the top of the property letter and feel no happier.

What advice would you give to someone like me who has a net worth of about 700k but a relatively low income of around 40k? Homes less than 120k simply don’t exist where I live, so how do I follow rule #3? If I do need to bend it to afford a home, what home price do you think would be reasonable for me? Would you recommend using some of those savings to put a higher percentage down payment or another path?

Sam,

Appreciate the informative article and reference chart. I’m 59 years old, retired at 55 and have approximately $7 million in retirement savings (not including home equity). My wife and I are exploring options for a retirement destination/home and found several possible locations; however, the home prices are around $1 million. We have always been prudent savers and lived below our means. The thought of spending $1 million for a home is frightening! With the exception of our current mortgage, we do not have any debt and should have $300K in equity with the sale of our current home. We would appreciate your insight on the following:

– The purchase of a $1 million home a risky move for our financial future?

– If we purchase a home in that price range, what is a recommended financing strategy assuming our retirement income withdrawals are taxed as normal income?

We do not live a lavish lifestyle, enjoy playing golf and travelling. If possible, we pan to leave our two children with a decent inheritance and provide for charitable donations.

Thanks for your time.

Walter

Hi Walt,

Check out my net worth home buying guide given you are retired. $1 million is under the maximum threshold for your net worth, especially if you pay cash.

Enjoy!

Sam

How about an updated rule given current high mortgage rates?

No change to the rule. It stands whatever the mortgage rate is. The 3 is discretionary between 3-5X household income = price of house purchase.

Isn’t the maximum mortgage to income ratio that traditional lenders will lend on 28%? If so, rule #1 wouldn’t be possible at 30%. However, the 3X rule (#3) would keep people well below 30% on rule #1 unless mortgage rates were over 10%, so maybe that is a moot point as long as we don’t return to 1980.

Yes, lenders usually require the PITI (principle, interest, taxes, and insurance), or your housing expenses, to be less than or equal to 25% to 28% of monthly gross income. Lenders call this the “front-end” ratio.

However, during boom times or undisciplined times, some lenders lend more and some borrowers fudge their incomes in ways to get to below 30%, when the real percentage is actually higher.

Hello Sam,

I’ve been following your blog for a while and I know you generally like real estate.

I was curious what your opinion is on this article which argues in favor of renting (at least if you only have one residence). It’s a bit of a long read, but I would really appreciate it if you could provide your opinion. Thank you for all your great articles!

moneywithkatie.com/blog/when-the-math-supports-buying-your-primary-residence-instead-of-renting?format=amp

Hi Thomas – When you’re younger and don’t own a home, there is a tendency to argue for why renting is better. The reality is, inflation, population growth, capitalism, are too hard to go against long term. You want to ride the inflation wave long term, not get beat up by it.

If you rent, you are short the real estate market. Just like shorting the S&P 500 long term isn’t a good idea, shorting the real estate market and being a price taker by renting isn’t the best idea.

I encourage you to understand the background of the authors and those profiles in the article. It’s totally fine to rent. But the investment return on rent is always negative 100%. One of the featured people has been negative on housing since at least 2016. Since then, Canadian real estate (she lives in Canada) has skyrocketed.

Another related post: My Favorite Asset Class To Build Wealth

At the end of the day, do the math! It’s your money. And everything is rational in the end.

Sam

Hi Sam,

Wow, I did not expect such a detailed response so fast! Thank you so much.

“At the end of the day, do the math!”

I like this tip. After all, everyone’s situation is different. Personally, I’m young, single, and can’t afford a house anyway at the moment. However, I see the value in owning at least one home and want to own a home in the future.

While you’re here, I just want to say I appreciate your blog and it has been very helpful to me. Although some of your rules seem a bit extreme at first, I like the fresh perspective that you offer compared to more mainstream financial advice.

Keep up the good work!

Hi Sam, great content! Great rules for home buying. I love your book too ☺️

I was wondering what your thoughts are on breaking a mortgage (4.7%) with 450k remaining in expensive Vancouver and taking the equity (approx 900-950k gained from appreciation) to another Canadian heartland market, like Calgary or Alberta. Would you consider paying cash for a house up to 800k in the new cheaper market?

Thank you!

Hi Scott,

Thanks! If you don’t leaving a review on Amazon, I’d appreciate it!

As per selling and relocating, tough to sell and pay taxes. As a result, I tend to buy, hold, rent out, and buy another place. But if the lifestyle in Calgary or Alberta suits you, then go for it. Locking in gains for a cheaper place is nice.

Sam

When you say gross income do you mean before tax? For example if I earn a salary do you mean gross income is before personal income tax deducted?

Yes. Gross income = before tax. Net income or after-tax income is after tax.

I don’t see how these three rules agree with each other. For simplicity’s sake, let’s assume you earn $100k per year. Thirty percent of that comes out to $2.5k per month. If you assume 4% continuously compounding interest, a 30 year term, and 20% down, we’re looking at a home value of ~$650k (albeit including all of the other fees in the home value itself), which is a 6.5x multiple of your salary, a far cry from the 3x or even 5x rule.

It seems to me that the third rule is just a stricter version of the first rule, except stated slightly differently. Unless this article was written at a time when 2.5% interest was available, in which case you could get the multiple down to 5x with payments at 30% of your gross income if you conservatively went with a 15 year term and 25% down. But it seems to me that to do this is to give up the key advantage of a mortgage, which is all in the leverage.

As far as the net worth rule goes, are we talking about home value as a percentage of net worth or home equity as a percentage of net worth. Because let’s say you have $150k in net financial assets and sell $100k of them to spend on a down payment on a $500k house. Your home value is now 3.33x your net worth whereas your home equity is now two thirds of your net worth. Are these rules meant to be about overspending on a house or overall exposure to real estate vs stocks?

Anyway, it seems like there are a lot of interesting moving parts here relating to:

-Over vs under spending on home value and luxury relative to your income

-Tolerance for leverage

-Outlook on inflation/deflation

-Speculation on the price vs value of what you’re getting, as well as the future price of the property

-Speculating on your own income growth

-Preference for exposure to real estate vs financial securities, or using them to hedge against each other

With all of these in mind, I think it might be smart to think less about the rules you propose and more about (1) getting a lot of value relative to the price you pay and (2) minimizing the interest rate, especially since the first of these is something you can’t ever change. But if the need ever arises, you COULD simply sell and buy something smaller, perhaps even at a profit. The name of the game might be to look for value (generally location more than luxury per se) and leverage it heavily.

As a side note, home expenditure is really the only thing I can see growing infinitely with my income and wealth. At a certain point and not really that wealthy, expenditures on cars, clothes, food, travel, and whatever else stay the same even with more income/wealth. But I could spend arbitrarily much on an UES townhouse or alpine ski chalet or what have you and not feel like I was wasting the money.

You should include taxes and insurance in the 30% of your gross income number. A $650k home might have $13k taxes and $2k property insurance. That means it’s not $2,500/mo it’s $3,750/mo which is $45,000/yr or 45% of your gross income.

Thanks for the article! The last rule “limit price of house to 3x annual gross income” seems too conservative though.

In your example: “You make $120,000 a year and have $100,000 in cash saved at 32 years old. Not bad. However, you’re also salivating for an $850,000 home, which equates to 7X your annual income.

Instead of buying this home now, first save up another $155,000 to get to $255,000 in cash and semi-liquid investments. With 30% of the home price saved, you can put down 20% and have a nice $85,000 cash cushion.”

Isn’t this person still violating the 3x annual income part of the rule, though? What’s the point at which having 30% of the price saved compensates for the house being worth >3x annual income?

It is. Hence why I highlight it as a suboptimal decision and the need to come up with a larger downpayment and buffer.

I discuss stretching to pay up to 5X your household income for your home in a low-interest rate environment. But that’s the limit. I wouldn’t go over that.

While building up your downpayment, I would be investing in real estate in other ways, such as in public REITs or private real estate funds. The idea is you want to ride with the real estate market so if it explodes higher, you won’t get too far left behind.

Hi Sam –

I’m looking at a 650k house with annual taxes of 14k. We have 340k in cash. 200k in 401ks. 26k of debt. With the rate hike, I’m nervous. My annual salary has increased YoY, but I’m usually a conservative person. So let’s say it’s 180k combined. Can we afford it? Would you recommend a larger 40% down to lower the monthly rate due to cash flow concerns?

Yes, you can afford it. Just bargain harder with rates up. Putting $240K down and leaving yourself with $100K will let you sleep very well at night.

I think now is finally one of the better times for buyers. Froth has faded.

Hi sam,

I agree to your method.however,how bout someone who dont have same amount of income every year.

Currently my net worth is around 2,6 mills( 700k in my current house,and the rest are in stock and gold).

In 2019,i paid all my debt included business debt.

In 2020,my net income is 350k,while last year my net income is 850k.The fluctuation is a lot.I am not sure this incoming year net income yet.

My plan is to purchase a land with 800k-1 mills in value.i am gonna save 300k before i proceed with the plan.i will also build the land much later on,prob within 3-5 years.

Thanks,

Denny

Samurai,

I was wondering if you think my situation is worth breaking rule #2 for you…

I make 95k gross, single guy, 25 years old. I have 15k saved for a down payment, and am looking at maximum 300k in the Tampa Bay area. I am planning on renting 2 of the 3 bedrooms to my brother and a friend. I am trying not to count on them in case things change, who knows when someone decides to move out, but I can at least count on them for a year or two. I could also likely find others to room with if that time comes. I have 30k left of student loans, but no other debt. Including my student debt, 401k, misc. assets, and additional cash savings, my net worth is still quite a ways shy of your minimum at 15k. I need a place to live relatively soon, and If I am paying this little for a mortgage with today’s rates, it seems much better than renting for more money monthly and no equity. By the time I could save 20% of the down payment, I would spend thousands in rent that could have gone towards building equity. Another pro is the tax breaks I would get for owning a home. What do you think? I appreciate your advice,

John

I do exactly this, John. Buy a single family home with a 5% down payment, rent the spare bedrooms, then ask for the PMI to be dropped if the house appreciates.

I don’t understand the logic to use gross income to calculate how much someone can afford for a monthly mortgage payment. Doesn’t it make more sense to use after tax monthly income? If a couple has a gross income of $150,000 and they max 401k and HSA , they are left with roughly $7100 after taxes and all deductions…. But you’re saying 30% of gross income would leave someone with a payment of $3750 per month… $7100 – $3750 does not leave a family with hardly any money left over per month.. why don’t we calculate mortgage payments based of what someone can afford after all deductions? That makes way more logical sense.

You can do either. Gross is a way to make an easier apples-to-apples comparison given everybody has different tax rates and tax-advantaged retirement contribution amounts.

A percent of gross income is also what lenders use, so it is consistent.

Ok, fair enough. Thanks for input.

Honestly, the 3x gross income for a house is spot on. That’s the best advice for sure….

Hey Sam!

Great article, I wanted to see your thoughts if you think these rules still apply if you plan to house hack (i.e. Rent by the room, live in one of them) which covers your mortage and allows to live for free.

Best,

Adrian

I actually missed the rent bullet, which makes sense to me, what rules(if any) do you think still apply with the rent by the room?

I would view renting out rooms for income as an insurance policy first. Don’t include the income when using the 30/30/3 rule.

However, renting out extra rooms for income is definitely a great idea and one I did in my late 20s and early 30s for several years. We had a garden room we rented out that was separate from the main house.

Hi Sam,

Great article. For the first rule, what about closing costs? Property taxes, homeowners insurance? How do you factor all of that into it?

Thank you

I like your formula and it’s easy to understand. Thank you. We are wanting to purchase for sometime now (dying to buy already) we can do Rule #1 and Rule#3 and in 6-8 months time I’m sure we can do Rule #2 but I’m afraid the housing market may get worse for us buyers. Should I buy now??

I do believe the housing market will continue to do well over the next three years. There are pockets of opportunity to buy. This summer is one as people go travel and kids have time off.

The other opportunity is during the winter holidays.

See this post for a thorough analysis: https://www.financialsamurai.com/why-the-housing-market-wont-crash/

Thanks for the article, Sam.

Your article made me realized I haven’t been spending ENOUGH on my primary. I essentially live free because I live in one unit of the duplex and own a short-term rental.

The YOLO mentality has creeped in due to the pandemic years, my wife and I are looking to spend more. With recent promotions, run up on real estate and stocks, we are feeling comfortable. However, we don’t feel “rich” yet even though we are now 40% to our fat FIRE number. We, too, don’t know how to spend money.

Now we are thinking of converting the duplex to a SFH. Why? Duplexes are cheaper than SFH with by sq footage when you compare fixers and full-remodeled properties. Or we could buy a 3rd house, not sure yet.

What you’ve done is very smart, living in one unit and renting out the other. That is actually what I wrote I should have done instead of buy a single family home in SF in 2005. More efficient and better returns for sure.

The thing is, if you don’t have kids yet, the extra space really won’t be used.

Hi Sam, great article! My husband and I bought a house in LA this past Apr 2021. For those who think your 30/30/3 rule is impossible to follow in a high cost of living market; it’s tough, but doable!

During our search, it was so hard to stay disciplined. We make 250K annual combined and it was too easy to increase our budget and justify it to ourselves because we live in LA. Our budget was at 750K but we could have stretched it to 1M…. We’d almost given up and joined the crowd, then we found our current house. It was listed for $825K, our offer was accepted at $820K and ultimately negotiated down to $795K during escrow. We shopped around at SO MANY banks and ultimately locked in a 2.75% 30yr fixed rate.

Rule #1 – Our monthly mortgage is about 14% of our gross. Rule #2 – We put down 20% and have 10% saved in liquid assets. Rule #3 – The house is 3.18 (0.18 over rule #3) but we have a tenant in an adu that brings in monthly income, which we think makes up for it!

I share my story in hopes of inspiring others in high cost of living areas to stay the course. It’s hard; but don’t join the crowd and keep your eyes open for opportunity! I recognize that this transaction would not have been possible on one income alone. If I was home buying by myself, I’d scale down to a smaller size property, maybe a condo vs a SFH, or look in areas where my budget would have still worked 1 hour outside of LA. Best of luck!

Nice work! And isn’t it great to own a home that doesn’t financially stress you out? Times are good now. But sometimes, things turn south. To be able to comfortably afford a home over the long term is what it’s all about.

Hi Sam,

Thanks for this article and read. I realize all situations are different but we are a dual income household making 290k a year before large commission checks. I am basing our household income sans commission and am not comfortable assuming differntly. We are in the market and have the 20% downpayment and are currently in escrow on a 1.38 million dollar home, with a 3.1% interest rate. We certainly do not adhere to the 3% suggestion (although we live in CA and see you can go up to 5X), but adhere to the 30% Gross income rule (you are referring to Gross correct?) and 30% savings IF you taking into account our 401ks and stocks/index funds (which we hope to never touch). My question to you is how often do you think people still fail when they are very close/ hit the mjaority of your rules? This is stemming from an impeding doom feeling financially after we have already entered into the escrow process. Our numbers/budget at up, but the cost seems to ludicrous and irresponsible. ADditionally we do not have children yet and are currently auto saving about 1,500k a month under our budget mode. Which DOES not feel like enough since we are used to packing away about 40% of our income into savings to hit the money for the down payment. In summary, not that we have what we need, we are still feeling doubts. Kindly advise on if the numbers above sound fiscally responsible.Thank you!

Sam, love your newsletter, BUT your 30/30/ 3 rule is way too restrictive for the middle income people in a high cost areas like LA, OC, SF, etc. I have owned my own mortgage company for 40 years now. The average mid income earner in a high cost area cannot save very much money. It would take them 10 years+ to save 20% down. The money lost in just the utility value of real estate without any appreciation is devastating. Lastly, in 2004 I did 13 media interviews of the upcoming financial disaster. It was very predictable because the lending guidelines were gone. 100% financing, stated income, etc. Today it is tough to qualify for loans. I do consumer educational events, one speaks on this topic it is titled “Build Wealth & Retire WITHOUT Saving Money thru RE.” I teach a real world solution to the enormous number of people that cannot save money on how they too can become financially secure and retire. Keep up the good work! MP

Agreed. There is absolutely no way for the 30/30/3 rule to work in the SF Bay Area.

By your logic, people/families with 300k income shouldn’t buy more than 900k home. That doesn’t exist here.

Or 400k income: a tiny number of 1.2m condos perhaps, but they wouldn’t be big enough to have even a small family.

The entry level home price in San Mateo or Santa Clara Counties is just about 2m which would require 666k annual income. That’s top 1% range. So only the top 1% can buy in these counties, and only a starter home at that.

The rule clearly doesn’t work here.

Hence why I’ve suggested you can stretch to 5X your household income. But that’s it. I wouldn’t go beyond that.

But you’ll be surprised that ~20% of Bay Area homebuyers pay CASH. So they clearly stick to the 30/30/3 rule.

See: Income And Net Worth Recommendations To Buy A Home At Every Price Point

And How Much Should You Make To Afford A $5 Million Home

Thanks!

Those 20% that paid cash are among the lucky with huge stock payouts, usually from Tech. Clearly in the top 1% for the area. Can’t base general financial advice on this segment of the population.

That’s the wacko bay area market. Only the top ~ 5-10% of earners can buy ANYTHING because the supply/demand curve is so out of balance. Yes, there are exceptions, but it’s basically now the rule. Haves and have-nots. Which will play out over the generations. People that bought 10, 20, 30+ years ago are golden, and anyone coming of age now has to leave to buy anything.

How will this 30/30/3 rule work in current Bay area market ?

1. You mentioned mortgage spending 30% of income, is it after tax?

2. Rates are already a bit high now, so getting 3% on 30 years is difficult, wont 10 arm be a good idea?

3. Even if someone can afford it, I am not clear – if it is wise to pay almost 30K in yearly property tax on a 2M+ value?

4. As a general rule – how much growth in the property value one should count for – 4 to 5% appreciation in 10 years in Bay Area CA for 2M property? or much less ?

Thanks,