After a long bull market since 2009, all Americans should be rejoicing in their wealth, right? Wrong! No all Americans have benefitted from the rise in stocks and real estate. Let's look at what percentage of Americans own stocks or real estate. It's not as high as you might think.

Roughly 156 million U.S. adults, or 58% of the population, owned stock as of April 2026, according to Gallup, that's down from 62% a year earlier and the first decline since 2016.

Given these figures, the bull market has left a lot of people behind. Due to analysis paralysis and uncertainly, a lot of people have just held cash or invested in Treasuries during the entire bull market. Big mistake.

The Federal Reserve's 2025 Survey of Household Economics and Decision-making found that only 37% of adults hold stocks, bonds, exchange-traded funds, or mutual funds outside a retirement account, meaning most stock owners hold them through a 401(k) or individual retirement account rather than a brokerage account.

Among those who do own stock in any form, the wealthiest 1% hold more equity than the bottom 90% combined, according to Federal Reserve data. Ownership slipped for people in the bottom half of the income distribution.

The top 10 percent of Americans owned an average of $969,000 in stocks. The next 40 percent owned $132,000 on average. For the bottom half of families, it was just under $54,000. With over a 600% rise in the S&P 500 since 2009, the wealth gap has clearly widened.

If you want to achieve financial freedom, you must invest aggressively over a long period of time.

Boost your wealth through private real estate:

Invest in real estate without the burden of a mortgage, tenants or maintenance with Fundrise. With over $3 billion in assets under management and 380,000+ investors, Fundrise specializes in residential and industrial real estate. I’ve personally invested $300,000 with Fundrise to generate more passive income. The investment minimum is only $10, so it's easy for everybody to dollar-cost average in and build exposure.

What Percentage Of Americans Own Stocks Chart

The Federal Reserve's 2025 SHED breaks that ownership down further. 61% of adults hold a retirement savings account such as a 401(k), IRA, or Roth IRA. 37% hold stocks, bonds, ETFs, or mutual funds outside a retirement account.

The Federal Reserve's Survey of Consumer Finances provides a longer-term view of how Americans invest, and the trend is clear: more of us own stocks than ever, but mostly on autopilot.

In 2022, 58% of American families held stock in some form, whether through retirement accounts, mutual funds, ETFs, or direct purchases. But only 21% held individual shares through a brokerage account. Total stock ownership has climbed steadily since the 1980s, while direct ownership has stayed flat at around 20% for three decades.

In other words, most Americans are passive investors by default, gaining their exposure through a 401(k) they rarely check. That's probably a good thing, since the data consistently shows the average stock picker underperforms the S&P 500.

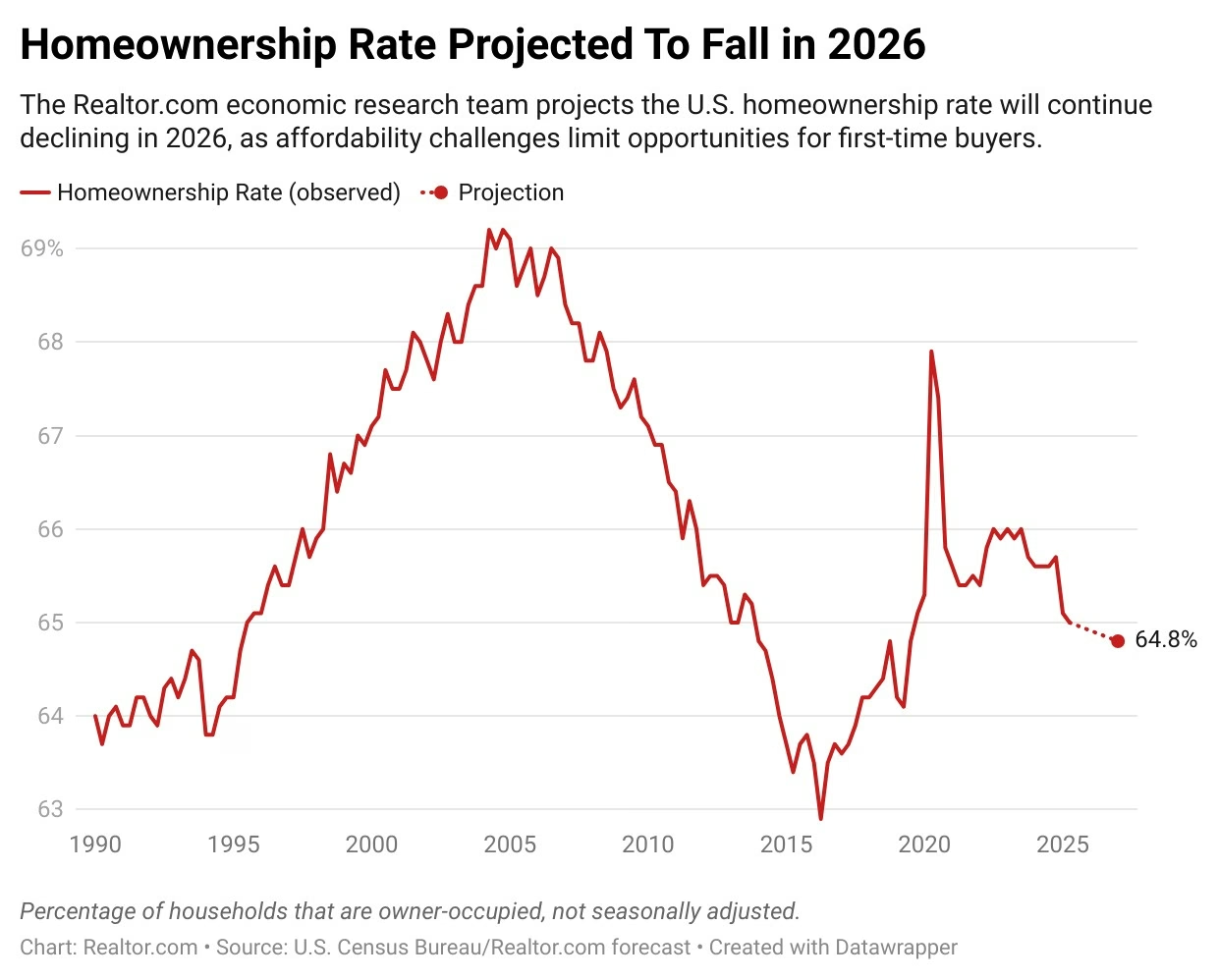

What Percentage Of Americans Own Real Estate Chart

Although the decline in homeownership from 2005-2016 looks steeper than the decline in stock ownership, there was only been a 6.3% move from peak to trough in real estate unlike the 13.5% peak to trough decline for stocks.

The reason has to do with transaction costs, the difficulty to sell, the need for shelter, and the view that a home is a home first and an investment second. And as you can see, homeownership rebounded significantly since 2017.

Roughly 65% of Americans own homes in America. This is good because real estate is my favorite asset class to build wealth. Through forced savings, inflation, and real housing appreciation, real estate will build more wealth for the average American than any other asset.

Although a bull market tends to financially help everyone on the spectrum, there is often more dissatisfaction due to a widening wealth gap. Those families in the 90th percentile have a net worth of almost $1,000,000. Meanwhile, those in the 50th percentile or below have hardly any net worth at all!

The Solution To Greater Financial Security

The obvious solution to greater wealth and financial security is to own stocks and real estate over the long run. You can own one or the other, or preferably both. But certainly don't own nothing. Inflation alone will destroy your wealth over the long term.

Here are some reasons why you might want to own real estate or stocks to help you get started, or help encourage you to own more of either asset class. Personally, I've invested $954,000 in private real estate for more income and less volatility.

Why You May Want To Own Real Estate

Real estate is my favorite asset class to build wealth. For most people, owning real estate is the way to go. The combination of rental income growth and property appreciation are two powerful forces.

1) You are more in control.

Every physical real estate investment you make puts you in charge as CEO. As CEO, you are able to make improvements, cut costs, find better tenants, raise rent, and market accordingly.

Of course you are still at the mercy of the economic cycle, but overall you have much more leeway in making wealth optimizing decisions. When you invest in a public or private company, you are a minority investor who puts his or her faith in management. Nobody cares more about your investment than you.

Personally, I like to buy fixer-uppers and expand the livable square footage. It's one of the easiest ways to make money if you can remodel cheaper than what you can get for sale.

2) Leverage with other people’s money.

Leverage in a rising market is a wonderful thing. Even if real estate only tracks inflation over the long run, a 3% increase on a property where you put 20% down is a 15% cash-on-cash return. In five years you will have more than doubled your equity at this rate.

Stocks, on the other hand, generate roughly 8% – 10% a year including dividends. Leverage also kills on the way down, so remember to always run the worst case numbers before purchase.

Personally, I like investing in private real estate funds offered by Fundrise. Fundrise manages about $3 billion and primarily invests in Sunbelt real estate where valuations are lower and yields are higher. The demographic shift toward lower-cost areas of the country is real thanks to technology and work from home.

I've personally invested $300,000+ in Fundrise to earn more passive income and diversify away from my expensive San Francisco real estate holdings.

3) Tax advantageous.

Not only can you deduct the interest on up to $1 million in mortgage indebtedness on your primary home, you can also sell your primary home for tax free profits up to $250,000 for singles and $500,000 for married couples if you live in the home for the last two of a five year period.

If you are in the 28% or higher tax bracket, it behooves you to own property. All expenses associated with managing your rental properties are also deductible towards your income.

4) Tangible asset

Real estate is something you can see, feel, and utilize. Life is about living, and real estate can provide a higher quality of life while also making you money. Stocks aren’t even pieces of paper anymore, but ticker symbols and numbers. Stocks and other non-tangible assets are considered funny money.

When the world comes to an end, you can seek shelter in your property. Real estate is one of the three pillars for survival, the other two being food and clothing.

5) Easier to analyze and quantify

If you can calculate realistic expenses and rental income that’s all you really need when it comes down to valuing a piece of property. If you can borrow at 3% and rent out for a 7%+ gross yield, you’ve likely found yourself a winner.

Real estate is immediately exploitable if you have the financial means to invest. There’s not only the cash flow component but the underlying equity component that helps investors build wealth.

Take a look online for the latest estimates, comparables, and sales history. Investing in real estate crowdfunding with Fundrise is one of the easiest ways to get started. The investment minimum is only $10.

See: BURL: The Real Estate Investing Rule To Follow

6) Less visible volatility

Your house value could be tanking and you would never know it since there isn’t a daily ticker symbol. During bad times, the utility of your home really helps soften the blow as you enjoy your home and create great memories.

During the 2008-2009 global downturn, I still got to enjoy my vacation property in Lake Tahoe 15-20 days a year even though its value was plunging. Meanwhile, looking at tickers on the TV or computer screen stressed me out sometimes. When your investment is less volatile, it’s much easier to stay the course and not sell at the bottom.

7) Real estate provides a source of pride

Making money for money’s sake feels empty after a while. Every time I drive by my rental properties I feel proud to have made the purchases years ago. I know that my money is working as hard as possible so I don’t have to.

Real estate is a constant reminder that taking calculated risks over time pays off. There is an indescribable feeling nobody tells you once you’ve closed on your property.

Even though the bank probably owns most of it in the beginning, you literally feel like the King or Queen of your castle. When you die, you can pass on your pride to your children or closest companions to let them create their own memories.

8) Real estate is more insulated than stocks

Real estate is local. If you’ve made a good decision to buy in an economically strong region, you will be more insulated from the national economy or the global economy. Spain blowing up is likely not going to affect the rent you can charge in Silicon Valley. Global uncertainty helps drive mortgage rates lower as foreign investors bought safe US Treasury bonds.

Look at prices in superstar cities such as NYC, Hong Kong, Singapore, London, Paris, and San Francisco over the past 20 years. They fall the least, recover the soonest and gain the most.

Of course, industries in your area could suddenly disappear and leave you broke as well. It’s also a good idea to diversify into lower cost regions of the country with much higher yields.

Despite being more insulated than stocks, real estate should benefit from more foreign buyers post COVID restrictions.

Favorite Real Estate Investing Platform

I diversify my real estate holdings through real estate crowdfunding. Fundrise is the best real estate crowdfunding platform today given it is vertically integrated, been around since 2012, and manages around $3 billion in assets for 500,000+ investors.

It's free to sign up and explore. I've personally invested over $400,000 in Fundrise funds, and Fundrise is a long-time sponsor of Financial Samurai.

9) The government is on the real estate investor's side.

Not only do you get generous mortgage interest tax deductions and tax free profits, you get bailouts if you can’t pay your mortgage. The government also aggressively went after banks to force them to extend loan modifications to bad and good creditors. I even got a free loan modification from Bank of America to my surprise (cut my 30-year fixed rate from 5.875% to 4.25% for free).

Programs such as HARP 1.0 and HARP 2.0 are allowing folks to put down a minimal downpayment. There are plenty of non-recourse states such as California and Nevada which don’t go after your other assets if you decide to stop paying your mortgage and squat for months. When was the last time the government bailed individual investors out of their stock investments?

Why You May Rather Own Stocks

1) Higher rate of return. Stocks have historically returned ~10% a year compared to 3-5% for real estate over the past 60 years. You can also go on margin to boost your returns, however, I don’t recommend this strategy given your brokerage account will force you to liquidate holdings to come up with cash when things go the other way. Your bank can’t force you to come up with cash or move out so long as you are paying your mortgage.

2) Much more liquid. If you don’t like a stock or need immediate cash, you can easily sell your stock holdings. If you need to cash out of real estate you could potentially take out a home equity line of credit, but it’s costly and takes at least a month.

3) Lower transaction costs. Online transaction costs are under $10 a trade no matter how much you have to buy or sell. The real estate industry is still an oligopoly and fixes commissions at a ridiculously high level of 5-6%. You would think the invention of Zillow would lower transaction costs, but unfortunately they’ve done very little to help lower expenses. They are in cahoots with the National Association of Realtors because they are their source of advertising revenue.

More Reasons To Own Stocks Over Real Estate

4) Less work. Real estate takes constant managing due to maintenance, conflicts with neighbors, and tenant rotation. Stocks can literally be left alone forever and pay out dividends to investors. Without maintenance you’re able to focus your attention elsewhere such as spending time with family, your business, or traveling the world.

You can easily pay a mutual fund manager 0.5% a year to pick stocks for you or hire a financial advisor at 1% a year. Or you can just track and analyze your portfolio yourself due to so many free financial tools online like the ones by Personal Capital, my favorite.

5) More variety. Unless you are super rich, you can’t own properties in Honolulu, San Francisco, Rio, Amsterdam and all the other great cities of the world. With stocks you can not only invest in different countries, you can also invest in various sectors. A well diversified stock portfolio could very well be less volatile than a property portfolio.

6) Invest in what you use. One of the most fun aspects about the stock market is that you can invest in what you use. Let’s say you are a huge fan of Apple products, McDonald’s cheeseburgers, and Lululemon yoga pants. You can simply buy AAPL, MCD, and LULU. It’s a great feeling to not only use the products you invest in, but make money off your investments.

Even More Reasons To Own Stocks Over Real Estate

7) Tax benefits. Long term capital gains and dividend income are taxed at lower rates (15% and 20%) than the top four W2 income rates (28%, 33%, 35%, 39.6%). If you can build your financial nut large enough so that the majority of your income comes from dividends, you could lower your marginal tax rate by as much as 20% or so, depending on the current legislation.

8) Hedging is easier. You can protect your real estate investments through insurance. If disaster strikes, it’s often a pain to get your insurance company to pay for damages because the burden is on you to prove your claim. With stocks, you can easily short stocks or buy inverse ETFs to protect your portfolio from downside risk.

9) Potentially less ongoing taxes and fees. Holding property requires paying property taxes usually equal to 1-3% of the value of the property each year. Then there’s maintenance costs, insurance costs, and property management costs. You can build your own portfolio of individual stocks and bonds for just ~$5 a trade. Or you can have a digital wealth advisor like Empower build and maintain your investment portfolio for just 0.25% a year.

Characteristics Most Suitable For RE Or Stocks

People Who Should Own More Real Estate

- Believe wealth is made up of real assets not paper funny money.

- Know where you want to live for at least five years.

- Do not like volatility.

- Easily spooked by downturns.Tend to buy and sell too often. High transaction costs ironically keep you from trading too often

- Enjoy interacting with people

- Takes pride in ownership.

- Likes to feel more in control.

People Who Should Own More Stocks

- Likes to invest passively and happy to give up control

- Is fine with sudden drops and volatility

- Has discipline in not chasing fads or selling when things are imploding.

- Likes to trade or has no problem being an active investor

- Doesn't like to be tied down.

- Have a limited amount of capital to invest.

The Key Is To Invest For The Long Term

The choice between investing in real estate or stocks is like choosing between eating a seven layer chocolate cake or a homemade lemon meringue pie. Both are good provided you don’t go overboard and can hold on for the long term.

When you are younger, investing in stocks is easier and makes more sense. Younger people have less money and want to be more mobile for job opportunities. As you get older you probably want to set some roots so owning at least your primary residence is beneficial.

With stocks, it’s nice to see portfolio values go up. But after a while, it becomes unsatisfying to see more money accumulate in your brokerage account. Money needs to be spent on something, otherwise, what’s the point of saving and investing?

Hence, my bias is towards real estate. With real estate, not only get to enjoy the asset, there's also a good chance you can make a profit over the long run as well.

Own assets that rise with inflation such as stocks and real estate. Even if there's a 20% correction, 10 years from now you'll likely be happy you invested today.

Own More Assets, Build More Wealth

If there's one takeaway from this post, it's that the wealth gap is really an ownership gap. The top 1% own more stocks than the bottom 90% combined, not because they're smarter, but because they consistently own income-producing assets while everyone else hesitates.

If you want to build wealth beyond stocks, check out Fundrise, a platform that lets you invest in private real estate without the burden of a mortgage, tenants, or maintenance. Fundrise manages over $3 billion for 500,000+ investors, focusing on Sunbelt residential and industrial properties where valuations are lower and yields are higher.

With a $10 investment minimum, there's no excuse to remain part of the ownership statistics you don't want to belong to. Dollar-cost average in and let time do the heavy lifting.

I've personally invested over $500,000 with Fundrise to generate passive income and diversify away from my concentrated San Francisco real estate holdings. Fundrise is a long-time sponsor of Financial Samurai, and our investment philosophies are closely aligned.

What Percentage Of Americans Own Stocks or Real Estate is a Financial Samurai original post. All rights reserved. Financial Samurai began in 2009 and is the top independently-owned personal finance site today with over 1 million organic pageviews a month. Join 60,000+ others building wealth by signing up for the free weekly FS newsletter here.

Great article to give the big picture, however if investors are just starting out, mutual funds from a place like Betterment or AXOS Invest is best. There are a lot of stocks (some mutual funds as well) individuals can’t purchase because they can’t afford the minimum purchase.

My opinion is that most people fail to really grasp and understand that “stock” ownership is the actual REAL ownership of very tiny fractions of much bigger (hopefully profitable) business enterprises. And as such, they should attempt to understand WHAT it is that the business does to make its money. After which they need to determine what a “fair” and rational PRICE is to pay for each share of ownership. Very similar to what Sam does when evaluating potential real estate candidates for cashflow and investment purposes. No matter how awesome a particular business (stock) is or how great a piece of property is, if one grossly overpays for that ownership, they will be greatly disappointed in their longterm “returns”. Most people get stuck on watching daily stock market quotations of all these businesses and have no idea whether that represents a rational price for the business (and its earnings) or not. All they see is that the “market” is up or the “market” is down or they just claim that everything is rigged. It is not….. at least not in regards to the straight up, fractional ownership of publicly traded equities. Even if you identify a great business and buy shares of it a reasonable price, the business can still suffer problems and cause you investment pain. There is never a guarantee with anything in life. However, as long as capitalistic markets remain intact, and you own assets (stocks/property/etc) that are truly of any value to society and were purchased at reasonable prices (not based on speculation), you are most likely to do reasonably well over the long run with regard to wealth building. Time horizon is everything and Millennials certainly have that aspect going for them.

Very well said. Heed this.

The average Joe doesn’t know much about either asset class. They have heard they need to invest to stay ahead of inflation. However, just because they know they have to invest doesn’t mean they know how to do it. Warren Buffett believes that people should keep putting their money in a low-cost S&P fund. This takes away the pressure of knowing which stocks to pick.

With real estate, you need to keep your property in good shape which often requires outlays of cash. This eats into your returns, especially if there are major repairs required.

Both asset classes are worthy as long as people know what they are getting involved in.

You wonder why the gap between the rich and the poor only widens?

Sometimes I feel people at the bottom of the food chain have a much harder time to build meaningful assets consider they could hardly get by. But I believe with hard work and dedication they can still participate in the market even real estate through REITs.

The key I think Sam says it right is to invest for the long run.

Hi Sam,

You made me google for questions like:

1. What % of Americans have ANY college degree?

2. What % of Americans have access to Internet?

3. What % of Americans own a computer or smart device?

Hmm.

The truth is – US is #1 developed country in the world. But it only means that Americans have access to top infrastructure, highways, public schools.

Beyond that, general populace is struggling to visit a doctor for a simple fever, to pay for college. Education is commercialized in US. Most middle income families cannot afford to send their kids to college any more. The costs have increased at a higher rate than this bullish stock market.

Take any other poor emerging country. Lets say, India. The folks there do not enjoy the best infrastructure, or highways. But they can at least get their fever treated by a qualified doctor for a $2 visit. Or send their kids to college for under $2000 per year on merit. Middle/Upper middle class can afford to have a driver, a few maids to clean/cook on a daily basis. The folks who cannot afford a BMW but can afford all of this.

When my dad visited me earlier this year, he scratched his head as to why standard of living in US is considered higher for a college graduate.

Food for thought.

A lot of people think stocks are like lottery tickets. It’s all based on the fear that there are always big market drops and flash crashes. They have no idea that stocks represent the perceived future value of a business.

It’s more than that. I think the 2008 chaos left its mark on the younger folk. I’m an older millennial and it seems to me we’re the inheritors of bad times and hardships. We know because of 2008, we’re never going to be alright and it’s going to be a struggle to just survive and pay for housing and basic necessities.

We didn’t have the financial education or financial means to buy into the stock market in 2008 and we don’t have the “safety of jobs” like the previous generations, we’re hired and fired at the company’s whim. Before 2008, company’s were working to improve employee life and experience at work, now they just think employees are items to be used and discarded.

It’s nearly a decade later and we’re still struggling to recover over here (admittedly we’ve also got other issues compounding the problem). To me, the stock market looks like one big rigged casino where the payouts favour certain individuals. What makes it worse in my case, is that to buy in is hugely expensive and the low success rate of businesses over here.

I have a friend who is deep in stocks (been in it for about 20 years) and he has tried to get me to buy in (it has worked and I did buy one). But he still has to work because the stock dividends can’t cover him financially. And then on top of that he tells me that so many businesses have folded and he has lost stock/money.

I feel better/safer knowing my hard earned blood, sweat and tears (and believe me it feels like a pound of flesh) is earning little but dependable interest at the banks. So what if my house will be a little smaller and I’ll have fewer holidays and knick-knacks, at least I’ll be able to afford the basics (food, water, lights).

Sounds like you’re making my point! I am an older millennial too. It’s not all doom and gloom for us. If you had invested your money continuously before and after 2008 you would not be so bitter. Also the stock market is not a “rigged casino.” It is a market like any other. The big difference is how the flow of news and earnings influence stocks daily.

The big trick is you need to buy diversified, good companies that you like that are valued fairly. Too many people chase penny stocks or overvalued companies. If you buy good companies you will beat the market over the long term. If you don’t want to do that, invest with an S&P 500 index fund. Warren Buffett even said that his advice for his wife when he is gone is to keep her money in an S&P 500 index fund.

I’m bitter at the chaos of the finance world caused by the idiot bankers and the state of employers because let’s be honest here, I was raised like a dutiful worker bee and I expected my employer to take care of me if I was loyal, hard working and respectful until I retired. I was sold on the once you get a job, everything will be ok – the work hard, play hard ploy. Then I had a rude awakening that it’s a dog eat dog world.

When 2008 hit, I had been working a little over a year, so not a lot of time to accumulate funds to invest while taking care of my family (who by the way know little in the way of finances). And when I saw how my tiny retirement fund became tinier, I got freaked out and completely put off the stock market. But I did know enough of the stock market (Thanks Suze Orman!) to keep putting money in my retirement fund because I knew that we were buying low with my monthly instalment! (Yay me!)

But the returns haven’t impressed me yet. It’s a yearly average of 8%. Interest from the banks over here provide a guaranteed 8% return on a 5 year fixed deposit. I know the brokers are making solid choices when compared to the performance of other retirement funds. I have wondered how much is the stock market and how much is the economy causing a return less than 10% ?

It is all doom and gloom when you live in a banana republic (junk status with the bonus of abominable crime) and you see the cost in US dollars to buy citizenship elsewhere (investing your way out) but I’m not bitter at the stock market or not putting money in the stock market. I had/have no business being in the stock market with the zero financial expertise I had/have. I’m smart enough to know that!

Thanks to the insights on Sam’s blog and my research into how to buy stocks, I now understand that they’re assets that you buy with a view that they will appreciate over years with dividends making up for the initial investment and have been encouraged to try. But buying in is going slow because it’s so expensive and it takes time to research stocks. And not to mention feeling as overwhelmed as a guppy swimming with sharks because I feel I’m learning all of this so late in life and wondering how much of it is rigged (Apologies but you haven’t convinced me that it’s completely free and fair). And not to forget I have an example of someone being in the stock market for 20 years and still not being financially ok.

I was going to buy in the S&P 500 index fund (a bank here was offering it) but while researching, I came across Sam’s blog about the S&P at a record high (Thanks Sam! You saved me!). It seems to me the trick is to research, research and research and to have patience and not freak out and even when you’ve done all of that, you’re not guaranteed results. And I crave security and guarantees.

I own 12 rental properties in Central Tokyo and it has been a very good business for me. It took me about 20 years to acquire and build up. It prints money for me and I just put that into the stock market where the dividends have continued to turn over and over as well. My spaces are all in the best locations in Shibuya so I never really need or want to sell anything because it is all profits on profits on profits…and I really love living in Tokyo

I always think I am done with real estate but there are always deals out there and financing is so cheap in Tokyo that I am thinking of getting another place recently.

I am retired from everyday business and I am quite handy and enjoy working on the spaces and I enjoy taking my kids with me as I think it is great education for them too.

I have started fashion and handmade computer businesses as offshoots of the real estate/construction business and I have a site/company called shibuyarepublic.org

I am also partnered in a small real estate firm as well if anyone here is interested in a Tokyo purchase…

Thank you for your site I find it quite enjoyable and have enjoyed reading about your personal journey.

I own stocks, and not real estate. I don’t like the hassle of real estate for myself or as investment. I worked as a property manager for some time and tenants were such a PITA. I also learned I just prefer to have someone else to call if the roof is leaking. I think I can get a higher value (not necessarily a higher return) in stocks. It suits my temperament.

I think people should own both. Owning your principal residence is first and foremost a place to live. Real Estate as an investment asset is much easier to acquire now thanks to platforms like Fundrise, RealtyShares, Peer Street, etc….

You can own real estate without the headaches. True, you will never get the 200% return but you will get a more reliable and steady return without the endless headaches if directly owning real estate for investment purposes.

I have stocks/ETFs. And REITs in my IRAs. But I totally agree with investing in companies you always used like Mickey Ds, Coca Cola etc.

What would you say to to a young buck who doesn’t have enough capital for real estate but wants to get in the game?

Fantastic article that got me thinking, Sam, as always. Thanks.

As a Gen Xer who got a later start (went to professional school), I like stocks. I’m a little wary of real estate in far away places, but could see myself investing in REITs or crowdfunding (local real estate in northern Virginia is extremely expensive, and, running the numbers, doesn’t make sense right now). Our primary home is within 3 years of being paid off, and that security makes me more comfortable.

I’d like to take the real estate plunge, but may just wait for my parents’ home to become mine– then, I could rent out the home I’m living in now, or theirs.

I wonder where the 2-4% real estate return comes from. That seems awfully low. Is that for the asset itself (i.e. home price index) ignoring the rental income? With the rental yield, real estate can pretty easily return more than 2-4%, especially when some moderate leverage is involved.

Great post. About a year ago, we sold a rental property we’d owned in Vancouver for 10 years (we also own our primary residence). I’m very happy with the decision as we did very well on the investment and I foresee expensive maintenance ahead the aging condo complex.

That said, I’m itching to get back into real estate investments. It seems near impossible to find something in the Vancouver area with a suitable Cap rate though, and going further a field would be complicated. I think we’ll stick with stocks until the real-estate market takes a dip here.

Can you share what your purchase price and sale price was in Vancouver? That must’ve been pretty darn good.

I like your stock ownership down from 2007 number. It sort of validates what I’m already thinking.

Home ownership historically has screwed up the black community therefore never really liked it as much. I plan to probably take some money out of stocks and buy a second home, at some point, if I ever feel stocks are too high. Don’t think we are there yet. Maybe in a couple of years. I think AR in the next iPhone is going to start a whole different kind of frenzy in the tech space. Then there will be a AR/VR tech arms race driving the Nasdaq higher. Will monitor the situation over the coming years and see if we get back to that 2007 stock ownership number you mentioned earlier in the article.

Sam, it was interesting to see the ratio of people who preferred stocks over real estate. I definitely like both, but my preference is real estate.

A great piece of real estate can pay you time and time again if acquired properly. And, I do feel there’s more control involved with real estate which I like. :)

Kind of scary stats to thumb through. I’m a big proponent of owning both “paper” assets as well as “tangible” assets such as real estate. It’s a diversification I’m very comfortable with. While I haven’t experienced a downturn yet, I merely graduated college during, I think that I will be perfectly content in sticking with this strategy even in the face of any sort of correction.

Thanks for compiling!

Good stuff Sam,

I have so many people in my workplace that are millennials that want nothing to do with either real estate or the stock market. They figure they will ‘adult’ at a later time. Also I believe the bank of mom and dad will eventually help them out when inheritance rolls around (which you have written about before).

I think it will take time but eventually millennials will leg into stock ownership. I have read where most think it is an old white man’s game, but stocks like SNAP and others that millennials use will eventually bring them to the market, whether informed or not.

I have wanted to get into real estate investing, hopefully one day on the commercial side, as it seems to be better suited for my taste of not dealing with individual tenants in a single family home. As far as homes though, I love the idea of Realtyshares or other new companies coming to the market for home investing.

Good stuff as always!

Entertaining site. I guess you are trying to stir up some controversy with this post, so I’ll bite.

How is not knowing what your asset is worth a positive? You may get your MBA revoked for that one!

RE in major cities like NYC is hugely impacted by foreign capital and the world economy. Those high rise apartments going up in front of Central Park are filled with foreign investors. Foreign capital flooding into NYC as a place to park capital is a huge part of price inflation there.

Easier to price and quantify is as much a negative as a positive. If every simpleton knows what something is worth, it is a complete commodity, and therefore almost impossible to generate the mythical alpha.

Being in control is only a good thing if you know what you are doing!

I agree with the tax and leverage being potential great advantages over stocks.

Again, very nice site and interesting post!

One of my favorite things about these surveys is the differences they reveal between those who read sites like FS, and the populace at large (or at least those who took the initial survey).

I get the feeling that people would invest quite a bit less into RE and retirement accounts if not for hefty incentives, often provided via our tax code. Some, like us personal finance nerds, would still invest. But without things like a 401k match, income tax deferral, or mortgage interest deduction, my assumption is that we’d collectively own far fewer assets.

My question for readers out there that rent…does it feel like “home” when you do not own your place of residence? I love my home and love doing work around the house & improving it. What does it feel like when you rent? I’m curious- because we’ve talked about selling our home and renting given our suburb of Chicago market is not appreciating at all any more!

Wow. This is a great article. Perhaps this would should that the next correction, wouldn’t really be a big one solely basing on the stock ownership factor amongst various income groups?

Playing the game by not being in the game is really not playing the game. You gotta be the player to be in the game and to beat the game.

If 20% less Americans own stock (down to 52% from a high of 65%), then who is going to panic and sell the next time around.

How can they sell in a panic and crash the market if they haven’t bought the market yet?

These people need to read a book by Felix Dennis entitled “How to Get Rich.” He talks about how ownership is everything, and if his own brother came to him asking for a single share, he wouldn’t give it up. As I write this your poll indicates that there are 1% of poll takers who do not own real estate or stocks. If you fall in that general category, please do yourself a favor and get some ownership. If I can do it on honestly and on minimum wage, then most people can do it.

(Yeah I know Financial Samurai’s readers may own businesses or be rich instead of owing stocks/real estate, its not the point of my comment).

Because stocks have a small float. It doesn’t take a lot to cause a panic, just like it doesn’t take a lot to cause a bank run and have the banks close their doors and run out of cash.

Oh I get the concept now. Thanks for taking the time to point out what must have seemed obvious to you, I appreciate it.

We play in both markets, but have a strong preference for stocks over real estate (the only real estate we own, partially because it isn’t paid off, is our primary home). I prefer to have to no back chat from my investments, and that is where stocks really shine when compared to tenants.

Wage stagnation. Hard to buy stocks or real estate when both their values have artificially grown due to serious policy flaws and your paycheck remains flat.

https://www.epi.org/publication/charting-wage-stagnation/

The market going up is a redistribution of wealth that has gone upward. Stock buyback programs, huge stock based compensation packages that companies now get to report “Non-GAAP earnings” without this piece factored in, allowing foreign investors to buy up properties in major coastal markets, massive student debt loads, major run ups in health care costs, college graduates earning almost exactly what they earned 15 years ago in real terms.

Most would like to invest, but the opportunities for far too many remain out of reach. Policies that made the already well off incredibly rich need to be fixed.

I have roughly $850K in stocks and $250K or so in real estate (ell equity in my primary home). I’ve always wanted to buy more real estate, but reading some of your posts Sam, about nightmare scenarios with tenants, really makes me squeamish about the whole thing. Thank you for reinforcing some of the principles behind the two. Both roads lead to Rome.