Let's look at the best time of the month or year to refinance a mortgage. If you can refinance at a better time of the year, you might be able to get a lower mortgage rate and save.

The best time of the month to refinance your mortgage is the last two weeks of the month. The best time of the quarter to refinance your mortgage is the last month of the quarter: March, June, September, December.

Finally, the best time of the year to refinance your mortgage is when rates are declining and lenders are hungry for business.

Rates change all the time and one key concept you need to grasp is that the Fed doesn't control mortgage rates, the market does. How can you check what the latest rates are? First, you can look at mortgage rate charts on sites like the FRED. You can also check with local banks and online mortgage rate marketplaces. Another thing to consider is to pay down some extra principal to quality for a refinance if mortgage rates go down further.

Build wealth one better decision at a time: Join 60,000+ others and sign up for The Financial Samurai free weekly newsletter for insights on the markets, investing strategies, and learn how to make better money decisions. Financial Samurai has been featured in top publications such as the LA Times, The Chicago Tribune, Bloomberg and The Wall Street Journal.

Car Buying And Mortgage Borrowing Similarities

As I was getting harassed at the car dealership the other day, something dawned on me. There are optimal times throughout the month and year to refinance a mortgage due to human nature. Timing makes a difference when you want to save money.

Dropping by the car dealership every other week is one of my favorite hobbies. I get to go for test drives and soak up that wonderful new car smell. Plus, I can curiously practice my negotiation skills all for free! Try it some time.

My Mortgage Refinancing Experience

I've refinanced my primary mortgage five times. And, have refinanced my other rental properties by a combined 10 times in the past 10 years.

With each refinance, I get better at negotiating. I learn where I can press for credits and when I can no longer squeeze blood from stone. I've also learned there is a best time of the month to refinance a mortgage. And a best time of the year as well.

One mortgage officer called and yelled at me when I asked for another $250 credit at closing given he promised a no out of pocket refi. I got him to own up to our agreement, but we never did business again.

I've gotten to know five mortgage loan officers across various traditional banks such as Citibank, Bank Of America, and Chase.

They've all shared with me some of their motivational points, which are all the same. One also shared with me why it's so hard to get a mortgage nowadays.

I have extensive experience in refinancing, working in finance, car dealing, and building personal relationships with people in the mortgage business. Let me share with you some discoveries I've found to get the best mortgage rates possible.

The Best Time To Refinance A Mortgage

What banks recommend: If it's up to the loan officer, the best time to refinance a mortgage is always! This is because they are paid through transaction volume. The more mortgages they refinance or originate, the greater they get paid.

In this current interest rate environment, you could do well to look at rates. If you have not refinanced or checked rates in the last 6-12 months, I'm pretty sure you'll be pleasantly surprised. You may be able to get a similar mortgage at least 0.375% lower than your existing rate. I know I did.

What I recommend: I only recommend homeowners refinance their mortgage if they can lock down a similar mortgage at least 37.5 basis points (0.375%) or lower AND break even within 24 months. If you can do this, refinancing now is a no-brainer.

Here are some additional refinance tips to reference to help you with the process.

Figure Out Your Mortgage Fee Break Even Point

When you want to determine the best time of the month to refinance a mortgage, or year, always figure out your break even point.

If you can break even within 36 months, that's OK provided you KNOW you plan on staying in the house for another five years. A break even point longer than 36 months is just not worth the time or effort because nobody knows the future for sure. The median homeownership duration is only 5.9 years to give you a point of reference.

In a shaky economic recovery, investors tend to pile into US Treasuries. So, in other words, investors would rather invest in a risk-free asset that barely keeps up with inflation instead of buying Apple stock.

In a bull market, investors tend to sell treasuries (gov't bonds) and buy stocks or other instruments because they feel the risk reward ratio is better.

Even if The Federal Reserve is raising rates, that doesn't necessarily mean mortgage rates are going up. The market determines rates, not the fed.

Slow economic recovery + government intervention means everybody should be refinancing their mortgages regardless of what time of month or year. But, now it's time to strategize when to refinance to get an even lower rate at the margin. It's all about understanding a person's motivation and understanding the spread.

Related: Should I Do A Cash-IN Refinance? The Benefits And Risks Of Paying Down A Mortgage For A Lower Rate

The Best Time Of The Month To Refinance A Mortgage

Each mortgage loan officer has either a monthly or quarterly target to reach. Practically every single sales department has monthly and quarterly quotas. This is especially true for publicly listed companies given they have to report results every quarter.

If you've ever been to a car dealership, you can sense they are much hungrier the last week of the month vs. the first week of the month!

Very few people can keep up their selling intensity every single day without burning out. Thus, most people save their energy for the last two weeks of the month and the last month of each quarter.

You can see from plenty of organizational behavior charts how effort really drops off after a particular deadline. Everybody knows what it's like to relax after studying so hard for a mid-term or final!

Conclusion: The best time of the month to refinance your mortgage is the last two weeks of the month. The best time of the quarter to refinance your mortgage is the last month of the quarter: March, June, September, December. Finally, the best time of the year to refinance your mortgage is when rates are declining and lenders are hungry for business.

The Best Time Of The Year To Refinance A Mortgage

Year-end bonuses make up a large portion of one's total annual income in the financial services industry. There are plenty of cases where a year end bonus can be 2X-3X your base salary if you are a star performer. As a result, driving revenue for the firm matters when bonus decisions are being made.

Nobody, and I mean nobody, remembers much of what you did the first quarter of the year. That's why when it comes time to pay your year-end bonus you need to remind your boss of your accomplishments. There is asymmetric emphasis on what you did in the second half of the year. And more importantly what you did in the 4th quarter!

Another important thing to know is when each firm's fiscal year (as opposed to calendar year) ends. It would be nice if all companies' fiscal years were the same as their calendar years. That is starting on Jan 1 and ending on Dec 31, but this is not the case. Some companies have fiscal years that end on June 30th!

In other words, their fiscal year for accounting purposes, which includes paying bonuses starts on July 1 and ends on June 30. Thankfully, most banks have fiscal years ending on Dec 31.

Get The Lowest Mortgage Rates During 4th Quarter

Assuming books close on Dec 31, bonuses for the fiscal year must be determined at least two weeks before i.e. Dec 15 or sooner. Hence, mortgage loan officers know to be the most aggressive in closing loans in the 4th quarter of the year.

The idea is to finish the year strong. Make amends for a bad first half, get paid a handsome bonus sometime in January. Then, cruise for the first half of the new year and repeat!

Conclusion: The best time of the year to refinance your mortgage is in the 4th quarter: October, November, December. The best time to refinance during the 4th quarter are the last two weeks of October and November, and the first two weeks of December.

Why Does Timing Within Timing Matter For Getting A Lower Mortgage Rate?

Banks work on spreads. For example, if they can pay 1.5% for $1 million in capital (deposits) and lend out at 3%, they make $15,000 a year provided you honor pay back the loan.

If banks can earn a 1% spread on billions of dollars of loans, you can see how they'll make lots of money!

Mortgage loan officers have wiggle room as to how much spread they want to make off your loan. For their best customers, such as those who provide consistent referrals, banks will often charge a tiny spread or no spread just to retain the relationship.

Such clients might have multiple different product accounts open which are more lucrative for the bank. Relationship pricing for mortgages is a big thing. For new customers who don't have a lot of assets, the spreads are wider.

When mortgage loan officers are aggressively trying to hit their quotas, they will give you more wiggle room. They do this by narrowing their spread or providing more credits.

Not only is generating revenue important, loan officers like to show a large number of loan originations or refinances. There is a customer lifetime value for every customer as chances are there will be future refinances and healthy referrals.

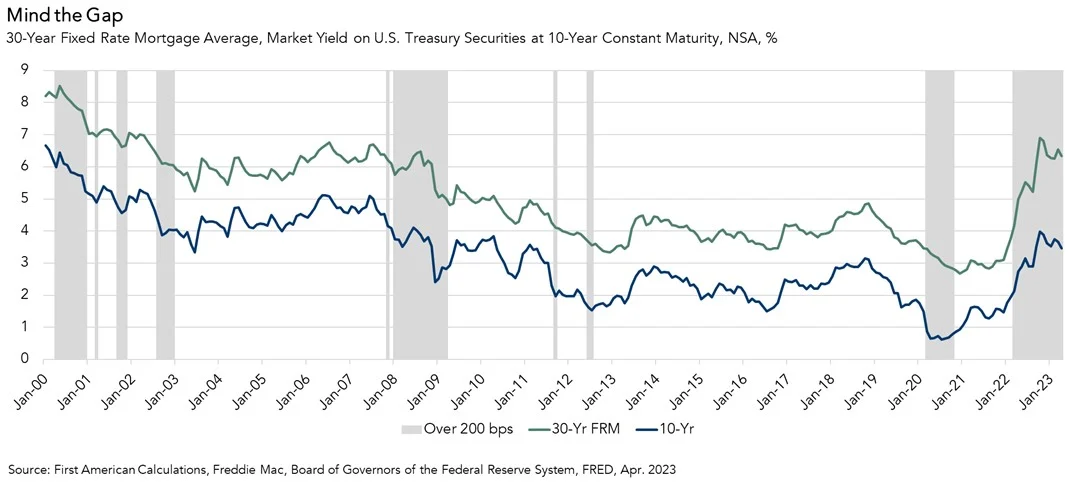

When Will The Spread Between Treasury Yields And Mortgage Rates Narrow?

According to Odeta Kushi, an economist from First American,

“If the spread returned to historic norms, the average 30-year, fixed mortgage rate in April would have been 5.2 percent instead of 6.3 percent. On the one hand, it’s possible that we’ll see a narrowing spread when the Fed finishes its monetary tightening. If the spread narrows, there may be some downward pressure on mortgage rates.

On the other hand, the Fed is unlikely to become an MBS buyer again and slower prepayment rates and longer duration are here to stay. It’s reasonable to assume that the spread and, therefore, mortgage rates will retreat in the second half of the year if the Fed takes its foot off the monetary tightening pedal and provides investors with more certainty. However, it’s unlikely that the spread will return to its historical average of 170 basis points, as some risks are here to stay.

Knowledge + Action Creates Wealth

It's important to understand how systems work. Now you understand how mortgage loan officers are incentivized. As a result, you can use this knowledge to get yourself the incrementally best rate possible.

Now you know the best time to refinance a mortgage. Thus, you should also know how to get the best mortgage rate possible.

Check the latest mortgage rates online with an online lending marketplace. You'll get real quotes from pre-vetted, qualified lenders in under three minutes. The more free mortgage rate quotes you can get, the better.

This way, you feel confident knowing you're getting the lowest rate for your situation. Further, you can make lenders compete for your business.

Build Wealth Through Passive Real Estate Investing

Real estate has always been my favorite asset class for long-term wealth building. With the powerful combination of rising property values and rental income, disciplined investors can steadily grow their net worth over time.

If you want to invest in real estate without the headaches of being a landlord, consider Fundrise—my preferred private real estate investment platform. Since 2012, Fundrise has grown to manage over $3 billion for more than 380,000 investors, focusing on residential and industrial properties in high-growth Sunbelt markets where valuations remain attractive. And the best part? You can get started with as little as $10.

Fundrise has been a long-time sponsor of Financial Samurai because we share the same philosophy: making institutional-quality investments accessible to everyday investors. I’ve met with CEO and co-founder Ben Miller several times, and you can hear our conversations about the markets on the Financial Samurai podcast.

For more nuanced personal finance content, join 60,000+ others and sign up for the free Financial Samurai newsletter. Financial Samurai is one of the largest independently-owned personal finance sites that started in 2009. Everything is written based off firsthand experience.

Great article! So helpful!

I’m about to refi my investment property. Would you trust the Loan depot?

Thanks.

Great article!

When you are talking about the best time to refi – does this mean to actually close? Meaning I will want to apply in early-mid September if I’d like to close in late October for the best deal? Or apply in late October?

Thanks!

The start of the conversation/negotiation.

Requesting clarification, please. You state that yr-end bonuses are usually set based on the numbers (on the book) by Dec. 15th. Yet, you recommend that the first 2 weeks of Dec is an ideal time to ‘start the conversation/negotiation’. Does that provide enough time to complete the Refi? (so the loan officer can get those numbers on the books by Dec. 15). IOW, are you implying that the Refi process is likely to go ‘faster’ during the first 2 wks of Dec.? That there is more ‘urgency & motivation’ during those 2 wks (to get it done)? I am planning for a Refi this 4th quarter. Thanks!!! P.S. great stuff!

How do you navigate the “credit check”?

Most lenders won’t even give you a rate to start negotiations until doing a hard credit check.

Obviously you can’t keep receiving separate credit inquiries, only to walk away.

Lenders have an obvious leverage here.

When you talk about “break even” do you mean recover the cost of refinancing through the savings you’re getting on your loan? Or is this something else I’m totally unaware of?

Great article!

I’m getting ready to go to a Credit Union for refinance information. I personally have never tried this on my own. My husband has been the responsible partner of our finances, but recently had a medical incident which affects his thinking process at times. Do you think this is a good time to try refinancing?

HI Financial Samurai,

Can I send you the current refi estimates a lender has sent me and you take a look at them. I need someone objective and smart to review. I don’t know how to haggle with this kind of information. I can haggle at a farmer’s market bit that’s as good as it gets.

So… speaking of mortgages. Curious to know your thoughts on Mortgage REITs. WSJ had an interesting article on them recently…

FYI I’m going to re-fi soon! I’m @ a 3.99% rate on a 5/1 ARM… looks like I can easily get a loan over 100 basis points lower (with no fees). No brainer…

Thanks for the great information Sam. I always refinanced when I’ve noticed a 0.5% decrease in the rates. I’ll have to look more closely at the 0.375% rule. Shopping around is really important. I’ve found a loan officer in my area that I can almost always get great rates through and the closing costs are next to nothing (around $1k). I also refer a lot of people to him, so I’m betting this is why I always get a great deal.

0.5% decrease is just as well. I just start really looking when I see rates below 0.375% b/c of my own mortgage amounts. Everyone is in a different scenario.

What I’ve found is that once rates are at 0.375% below what I’ve got, I can often haggle to get down to 0.5%, or the markets will push them lower for me.

This is great info! We have refinanced several times too, but only when it made sense. It’s crazy to believe that we had a mortgage at 6.5% before!

Ah yes… the good old days when 6.5% was a great rate… but also real estate prices were going gangbusters! It’s coming again, we just have to be patient.

How do you expect to learn how to deal with salespeople and work your negotiation skills if you never go to the car dealership for practice?! It is the lion’s den!

Great points! I think this is true for all negotiation. If you know the other party’s motivation, you can be more successful.

Lovely post Sam!

I’m one of those who has been on the fence whether I want to start negotiating early or wait a few months before the mortgage is up. Personally I have 1.5 yrs left on this mortgage, the rate is not bad at 3.6%, because even if I chose variable I’d only get it at around 2.99% roughly. More importantly, I don’t want to pay any $$ on the penalty, and I’m certain one would exist if I broke the term earlier.

You sure about the pre-pay penalty? If not, double check with your mortgage loan officer. I’ve never had one, and I’ve refinanced 15+ times already. Perhaps b/c I explicitly tell them no pre-payment penalty.

A 0.6% spread sounds like it’s worth refinancing. I don’t wait until expiration. I act when the spread is wide enough.

I’m pretty certain about the penalty, however for shits-and-giggles, I should look into it and how much the penalty would actually end up being.

Also I think we’re talking about two different penalties. There is no pre-pay penalty, but there is a penalty for early termination of your mortgage agreement, even if you’re resigning again.

This post made me send a note to the person who originally financed my mortgage to see if it is worth considering. It is much more difficult for me though because my principal balance is so low.

Great to know. My bank also has “sales” during a month, where they don’t charge any fee to refinance. Don’t remember when that was last, I think near the end of the tax year, i.e. March (UK).

Very interesting article! These are information people who have mortgages to pay should know about in order to make their financial difficulties less strained.

I do. Anybody who cannot wait until after the holidays, and during better whether to list their property is a much more motivated seller imo. Gems can be found! Right before New Year is when I found my current house.

This is a genius post. I love how you’ve refinanced so much and enjoy the art of negotiation. Getting my mother to refinance is like pulling teeth and it drives me crazy.

Timing can make a difference like you’ve said and I certainly see cycles in my own job when I’m more willing to go the extra mile for someone. Tapping into that is a smart tactic!

Help yo mama! It’s interesting how some people are so reluctant to save money. Go through a little elbow grease, lock in a lower rate, and save money for years to come sounds worth it to me!

When I refinanced earlier this year I couldn’t find a lender that would offer no closing costs. While it makes sense to refinance in conjunction with rates that are dropping, the closing costs will keep pushing back the years you need to stay in your home to reach break-even.

What are the best tactics to use to get a lender to waive closing costs?

Ask during the best times of the month and year per this article’s suggest! And be prepared to walk away and keep on shopping.

That’s great information. Usually anything sales driven always gets attention at the month/quarter/year end, so that’s a good thing to have. You have to start the process a bit earlier since it takes a while from when the application until it actually closes.