Here are are some tips for borrowers of peer-to-peer lending. Peer-to-peer lending has become a popular way for more borrowers to access money beyond going to a traditional bank.

Frankly, I think getting a personal loan from a marketplace like Credible is the most efficient way to borrow money nowadays. Rates have come way down during the pandemic.

Everybody has a different need for borrowing money. Some might want to get a new $5,000 home theatre system. While some might need a $10,000 loan to prevent their small business from going under. It's important to understand that if you are a borrower in P2P lending, you must present yourself in the best light possible.

Treat your P2P lending borrower's profile as if you were about to interview for a job. Your resume needs to exemplify your strengths while deemphasizing your weaknesses. The average employer spends just seven seconds on a resume before making a decision whether to go forward with an interview or boot you to the curb. The same cursory amount of time is spent by a lender, especially one that is investing in over one hundred notes for diversification purposes!

Tips For Borrowers Of Peer-to-Peer Lending

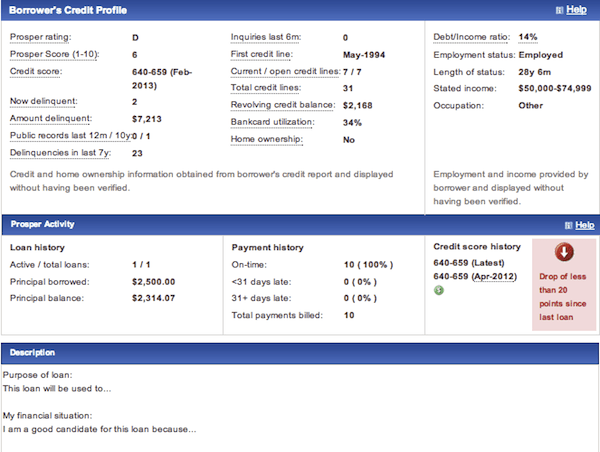

I just spent the past couple hours going through Prosper.com's investment system to deploy $1,000 in new loans. What stood out was how little some borrowers spend filling out their profile. Let's use the below D rated borrower as an example.

The borrower's credit profile is what it is. If you've got 23 delinquencies in the last 7 years, Prosper's system will pick this fact up. There is no escaping or massaging your profile except for when it comes to your employment info such as “Stated Income” and “Occupation.” Stated income is hard to verify. While this borrower doesn't even bother to highlight their occupation. Parking ticket officer perhaps? Just like when you don't put down your GPA, an investor thinks the worst!

As I wrote in a previous article entitled, “P2P Investor Returns By Borrower Rating And Credit Score,” my plan is to disperse funds between AA (top rating) and D, E, and HR (lowest ratings) for a dumbbell approach to achieving 6-9% net returns. This borrower's profile looks alarming, however that's what the estimated 22% expected interest return is for. The borrower's debt to income ratio is low, while the revolving credit balance of $2,168 is not high at all. Alrighty, let's take a chance!

A Low Rating Warning Sign

Not so fast. With a D Prosper rating, a 640-659 credit score and 23 delinquencies in 7 years, I want to know more about this borrower's past. The solution for a borrower is to simply describe the purpose of the loan. Also share why they are a good candidate in the “Description” section below. This is where one can really sell themselves to create a connection with the lender. Again, if you write nothing, investors will think you've got something to hide, like being a bank robber.

Imagine reading a description such as, “The purpose of this loan will be used to help rebuild my house of 28 years after burglars set fire to my kitchen and stole my wedding ring that was given to me by my deceased husband. I'm an excellent candidate for this loan because although I've gone through much hardship in life, I plan on making amends by consolidating my loans and paying off all my debts.“

Instead, the borrower writes NOTHING. As a result, I'm not even going to bother because there are plenty of D rated borrowers in the system. If you are a low rated borrower, it's more important than ever to share your story!

Tips For Borrowers Of Peer-to-Peer Lending: AA Rated P2P Borrower

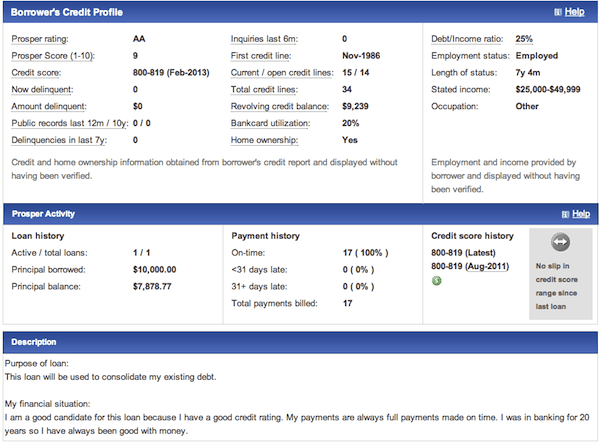

Now let's take a look at an AA rated borrower's profile on Prosper.com. This borrower plans to pay an interest of 6.7% on her loan. This is more than 3X the current risk-free 10-year Treasury yield of 1.9%.

It's obvious from the borrower's credit profile that she is an excellent candidate. She has a Prosper Score of 9, a 800-819 credit score, no delinquencies, and a moderate debt/income ratio of 25%. The only red flag is that she doesn't highlight her occupation. Be proud of your occupation, no matter what it is folks!

What sold me on this loan was her simple financial situation description. “My payments are always full payments made on time. I was in banking for 20 years so I have always been good with money.” Her Prosper Activity information of 17 on-time payments backs up her description nicely. Although my plan was to make 20, $50 loans this round. I decided to invest more heavily in such borrower's whose profiles I really like.

Tips For Borrowers Of P2P Lending To Get That Money!

- Think Like A Lender: The number one thing a lender wants is knowing he can trust you to pay the agreed upon interest rate in the time stated in the contract. The more you can convince a lender you are credible borrower, the higher the chance you will be able to get money.

- Tell The Truth: Remember that social capital carries a lot of weight in the internet world now. As soon as you start to lie or mislead investors, you will be shutout forever. Everybody makes mistakes with their money. Just come clean and get people on your side! As soon as an investor sniffs something fishy, you will be blackballed.

- Describe As Much As Possible: Be as clear and explicit as possible why you need the money. If you need the money to pay this year's college tuition, say so! Saying you need money to achieve “a brighter future” is not good enough. You don't want to leave any doubt in the lender's mind where your money is going. Fill out your application as completely as possible and leave no question unanswered!

- Check Grammar And Punctuation: Nothing turns off a reader or lender than poor grammar and punctuation. You wouldn't send a poorly written application to a college of your choice, nor would you forget to spell check your resume before sending it to your dream employer. The same rules apply for borrowing someone else's hard earned money. The default assumption for applications with poor grammar is low quality, high risk, scammers.

- Expectations: If you're banging a 580 credit score while making $35,000 a year, don't expect to miraculously have people banging down your internet door to fund a $25,000 loan. Prosper will calculate your Debt to Income ratio which limits you to what you can reasonably borrow. Prosper's goal is to keep the marketplace running and to minimize defaults for everyone's good!

- Don't Come Across As Desperate: The more desperate in your application you sound, the less likely an investor will lend you money. You've got to have a confident, matter-of-fact tone in your writing. Have your parents or loved one review your application. Do not whine about why life is unfair. Be as confident as possible that you will utilize the money for a necessity and pay them back.

RESPECT THE CONTRACT

Understand that someone will be lending their hard-earned money to help make your financial situation better. They believe in your story and are therefore taking a leap of faith to help you. The lender is also trying to improve their financial situation. By defaulting on your loan, you are directly hurting someone else as a result.

The P2P lending marketplace is often times a second chance for those who've gone through financial difficulty. Please always honor your borrowing contract on Prosper. If you fail to repay your debt, your credit score will get smashed, and your social capital will be ruined to a point where you will run out of places to ever borrow money again.

If you are interested in investing from Credible click here. They'll ask you for the purpose of the loan, loan size, estimated credit score and basic information to see if you qualify. I encourage you to leverage P2P mainly for consolidating your higher interest loans. Borrowing to go to Hawaii on vacation is not a wise choice, nor is borrowing to buy a new 2013 Mercedes SL550 in the picture above.

If you are interested in being a lender just be warned, investing in P2P lending can get addicting because it is a lot of fun analyzing profiles to make a greater return on your money.

Wealth Building Recommendation

Manage Your Finances In One Place: One of the best way to become financially independent and protect yourself is to get a handle on your finances by signing up with Personal Capital. They are a free online platform which aggregates all your financial accounts in one place so you can see where you can optimize your money. Before Personal Capital, I had to log into eight different systems to track 25+ difference accounts (brokerage, multiple banks, 401K, etc) to manage my finances on an Excel spreadsheet. Now, I can just log into Personal Capital to see how all my accounts are doing, including my net worth. I can also see how much I’m spending and saving every month through their cash flow tool.

A great feature is their Portfolio Fee Analyzer, which runs your investment portfolio(s) through its software in a click of a button to see what you are paying. I found out I was paying $1,700 a year in portfolio fees I had no idea I was hemorrhaging! There is no better financial tool online that has helped me more to achieve financial freedom. It only takes a minute to sign up.

Finally, they recently launched their amazing Retirement Planning Calculator that pulls in your real data and runs a Monte Carlo simulation to give you deep insights into your financial future. Personal Capital is free, and less than one minute to sign up. It's one of the most valuable tools I've found to help achieve financial freedom.

About the Author: Sam began investing his own money ever since he first opened a Charles Schwab brokerage account online in 1995. Sam loved investing so much that he decided to make a career out of investing by spending the next 13 years after college on Wall Street. During this time, Sam received his MBA from UC Berkeley with a focus on finance and real estate. He also became Series 7 and Series 63 registered. In 2012, Sam was able to retire at the age of 35 largely due to his investments that now generate over six figures a year in passive income. Sam now spends his time playing tennis, spending time with family, and writing online to help others achieve financial freedom.

Related posts:

How To Earn 10% A Year From P2P Lending

Ranking The Best Passive Income Investments (P2P is actually ranked the lowest)

Hey Sam,

What are your thoughts on investing with Peer Street?

Pingback: Should I Invest In P2P Lending? Prosper Performance Review | Financial Samurai

Hi there,

I lost my job and need to get unemployment. I owe the state 6k in order to receive 450/wk for up to one year. I have a low credit score and zero income. I have very little overhead at the moment and only three bills. How would I go about making my case to an investor and actually get approved? I am a single mom and have held a job for most of my life, just ran into a tad bit of struggle. How can I get out of this hole? Any suggestions???? djthefiberlady at gmail.com (fiber optics specialist:)

Hi Guys, Interesting information that you have here. I have a few questions. I am looking for funding to help with business start up costs, help to pay bills, debt consolidation, ETC.. I need a mini miracle in short terms. I have poor credit. I’m looking for anywhere from funding between $25,000-$100,000. Depending on which route you want to look at. $25,000 would help with business costs, and bills. $100,000 would help acquire and accomplish my goals and pay off all my debts. My Situation: I was married 10 years to a man who made me lose every job I ever had while we were together, and is currently in prison for CSC (if you need more details e-mail me). Things that weren’t down hill went down hill(half my debt was acquired during the marriage, part was acquired before the marriage due to another situation which if you want details email me, and part of the debt was acquired after he went to prison) . I am currently still trying to get the divorce finalized, but the courts keep losing my paperwork. CPS was involved which made matters worse and not better, I’d still have my job if it weren’t for CPS(email for explanation). I’d Tried different online money making methods, spent money on them, turns out most of them were scams. Things got worse. I ended up seeing someone, we will call him my ex-boyfriend. He seemed so sweet and caring and supportive. I was helping him with his automotive business. Things were ok for a while. He got involved with drugs and alcohol. I didn’t want it around my kids (raising 4 kids by yourself isn’t easy). He threatened to kill us. I got a PPO. He Violated the PPO. Domestic violence here we go. To say the least, Things haven’t always been easy, or nice, or peaches and cream. I’ve been through a lot, and my credits bad, very bad. Things could be worse. On a Positive aspect, The ex-husbands in prison for what he did, the ex-boyfriends in jail for another DV on his new GF, I still have the house that my ex-BF and I were buying which im trying to get out of foreclosure, I started an E-Commerce web store which I’m trying to grow, And my bank accounts are still open. Those are some positives with all the negatives. Now, onto the business aspects of things. It is a small web store with lots of potential. I intend to grow the website, as well as have open stores around the country eventually. It will Eventually go Global. I’m not willing to give up on my Dreams, and I’m tired of everything failing and for once in my life I’m not going to let anything or anyone stop me from achieving my Goals. I’m just stuck in a bad situation right now that I’m working to get out of and just need some help. I help other’s when i can, if they need something and I can provide help I do. My business proceeds would Also help to Build a foundation for a better future, not just for me and my family but for others as well. One of my goals is to Build a self-sufficient community of people helping people, taking the homeless and providing jobs and shelter, rescuing animals, helping victims of violence get out of thier situations and into better ones, helping family’s grow. It takes one person in small steps and acts of kindness to make a difference and change a life, but it takes a good heart to change the world and make it a better place one step at a time. I’m just trying to Achieve my goals a little quicker, and with some help I could.

Now, My Questions:

Due to my situation, Is there any way for me to get the help I need?

What are the steps that I need to take to acquire the funding i need?

Am I Just one of the ones falling through the cracks, and there is no hope of getting the help I need?

What exactly, do I need to do to get the funds that I need to move foreward?

I can say this, anyone willing to invest thier time, patience, and money in me will receive more back than what they invest.. Right now I just feel stuck, and frustrated, but all of this I will overcome to just like I have everything else in my life. I believe in miracles, this too will get better.

Hello. My name is Dustin, and reading this article continues to frustrate me beyond belief! At the same time i gives me a shimmer of hope. The reason it gives me hope is because it provided an answer to one thing i was looking for which is that some lenders do actually look at the borrowers situation and look deeper into the score, however I recently applied to prosper in search of a peer to peer lender and immediately declined. My info was ran through an automated system and in two seconds got a no. How can i get in touch with said lenders? my credit score is at 640, and im in the military so for the past six years i have made just about every payment in full and on time. I had multiple small loans in the amount of 1,000-1,500 that were paid/ closed never late, but i cannot for the life of me get a personal or debt consolidation loan in the amount of or around $6,000. I am currently going through a separation/ divorce and the switch from dual income to single with a forced move into a new apartment, has killed me financially. for the past six years i have worked very hard to better my credit and maintain debts well. Now i am starting to slip and need help but cannot find it anywhere. I have applied numerous times, which i know hurts my credit, but i have to apply. And i keep getting denied. One bank even told me they would approve me if i had another loan for that amount that i had payed off. How will this happen if no one will accept me? Well i apologize for making this so long, but i guess my question is where can i find a place to put my situation out there and have lenders go over it themselves and decide on the loan? Or any help at all would be greatly appreciated.

Thank you all for your time.

Dustin M.

I have been investing in Prosper for about 3 years now with great success. (I currently stand at over 30% APY over the past 12 months). I have a relatively small stake and would love to increase it, but I am nervous because of the company’s financials.

Prosper is currently hemorrhaging cash at a rate of $12M per year and shows no signs of reversing this trend. In fact, their cash flow has grown steadily more negative with each year! Even with the $20M from Sequoia Capital, this spells bankruptcy by the end of 2014.

As Prosper lenders, we actually have no direct claim to the promissory notes that bind the repayment of the original borrower loans. They are owned by Prosper Funding LLC which is a wholly owned subsidiary of Prosper Marketplace Inc. In the event of a bankruptcy, we would simply be another creditor with claims against Prosper’s assets. It is unclear how a bankruptcy court would distribute the proceeds from repayment of notes even given the formation of Prosper Funding LLC which theoretically protects payments due lenders.

Mr. Samurai, as an experienced investing professional, I welcome your take on this situation and how it factors into your increasing stake in Prosper notes.

Jeremy, I’d recommend you check out (not my site). Peter has a tremendous amount of research and can point you in various directions to help focus your investment strategy!

Good luck!

Sure, do what works for you and makes you feel comfortable I say. Making these investments is a leap of faith in each person to honor the contract.

I agree that it’s very important to acknowledge why you have any negative items in your profile and take responsibility for them. Those who blame everyone else for their failures will find a reason why they can’t pay you back if it comes to it. I can’t believe you would not have some sort of description for why you want money, although I have had resumes turned in that had our town name spelled incorrectly, so there isn’t much that surprises me anymore.

Hello Sam,

I arrived at this post while doing research on P2P lending, and specifically on Prosper.com, since I too live in the Bay Area and I used to work for ELOAN, which was founded by the same person that founded Prosper.com, Chris Larsen.

Have you any knowledge on a possible bankruptcy filling by Prosper.com; or technology issues plaguing the company? I ask because I also found the following post: yesiamcheap.com/2012/12/im-leaving-prosper-com-due-to-technology-problems/

Everything is so far pretty good here with my experience with Prosper.com. They recently got a $25 million+ capital investment from Sequoia Capital and a new CEO, so I don’t think Prosper is going anywhere anytime soon. I will highlight if there are problems though.

I would second Sam’s comment here. Prosper is not in jeopardy of bankruptcy at this time, and with Sequoia’s investment and the new management, I would expect to see some significant improvements at Prosper over the next few months.

Sam, great job summarizing your tips for what might help a borrower become more attractive to lenders. However, in today’s peer-to-peer lending market with nearly all the available loans getting fully funded prior to expiration does a borrower really need to take these steps?

Additionally, from a study done in 2011, strong borrowers with a good credit profile might benefit from have no description, while those of a slightly lower grade would benefit from a well-written description. Google the study: Is Silence Golden? – How Non-Verifiable Information Influences Funding Outcomes On Peer-to-Peer Lending Platforms

Personally, I do not look at the descriptions. While that might have assisted in founding the original “spirit” of “peer-to-peer” lending, I find it overly time consuming and a very inexact science. Further analysis in a couple guest posts at LendAcademy in December demonstrate that having a description or not isn’t a good indicator of default (see the revised chart at the bottom: )

So without a tangible benefit, and loans getting fully funded provided they make it through Prosper or Lending Club’s review process, does the description ultimately matter in getting their money? Food for thought!

Thanks for your thoughts. Your comment is from the angle of the investor, which is good. This post’s angle is for the borrower who wants to improve their chances of getting funded.

I read descriptions b/c I enjoy the process and want to feel some connection with the borrowers I’m lending to. I’m sure Prosper’s “Quick Invest” system works pretty well if one is diversified. I just enjoy the process so much. It’s half the reason why I invest in P2P lending.

Of course! I love the process of investing tremendously like yourself, but perhaps am currently taking a less subjective approach! ‘To each their own’ which is part of the reason why I love peer-to-peer lending!

As far as the borrowers go, I think my main point above was the first one in that borrowers who meet Prosper or Lending Club’s criteria are pretty much getting 100% funded at this point. I’m not sure that the actual impact a better description will have would represent a significant effect on a loan’s funding at the end of the day.

Whether it’s a job interview or a loan, if you want money from someone bring your A game and then some. This greatly increases your chance of walking away with the check in hand.

I’m still a little leery of P2P lending. Part of me wants to try it if my State allows it. And part of me says better off not.

Like any new investment. Start small, keep diversified, and build your way up if it’s working for you.

Wow, Sam…this was such an incredible dichotomy in case study! I have yet to look into P2P. I kind of need a loan in 10 months or so (even though I would rather pay cash…fingers crossed) for home renovation. I am scared to try this out, but why not!?!? I need to check it out as an investment opportunity as well. So great you posted this!

Tony, p2p is not a bad option, especially if you can borrow at a lower rate than alternatives.

Just spend time writing your description and answering the who and the why. You will beat out 90% of other borrowers who have little to no description.

Oh man, sometimes I can’t believe that folks don’t leave descriptions when they are asking for a loan. I’ve said before that I don’t need an extensive detailed background, just a simple explanation of why they want the loan and why they are a good candidate. It would take only a few minutes to do this. I have passed on loans before because of a lack of description. I see a lot of similarities in how you scrutinize a loan with myself.

Yes, it seems like such a no brainer to spend 5 min to write a description. If a borrower doesn’t bother, I’m not bothering either!

Sam, I just can’t imagine applying that amount of scrutiny to my loans on Lending Club. I’m closing on my $10,000 investment amount there before I start doing the same with Prosper, but I have a quick series of filters I apply and then I lend. I screen purely for debt consolidation, 36-month loans, and a few other criteria (including only buying $25 of each loan), but it still takes weeks to get large amounts of money invested. If I scrutinized any more, it would take even longer to find a substantive amount of loans. In fact, I’m still trying to get the last $3500 I put into LC last month to get through their process!

I find the process fun and very addicting. At $50-500 a loan, I can find homes for $10,000 within a couple hours no problem. I love to get involved in the decision making. It’s like betting on people’s ability to succeed.

What kind of interest rate would he have to pay? He seems too risky for me! I would want some evidence he has changed in order to consider lending to him.

22%+

I guess that says it all. Very risky and priced appropriately. I think I would still stay away from unless he can show he has changed.

Everything has a price. Just ironic those who may have the most difficult time paying back their loan get the highest debt interest to make the payback even harder.

That’s a crazy amount of delinquencies! I have to admit that is part of the reason why I have not pulled the trigger with P2P lending, though I freely admit that is somewhat irrational. My state allows it, though I just not have taken the time to study up on it more and give it a try. With the way rates are (or aren’t) these days, you have to find other options to try and earn some income.

You can find a lot of borrowers with zero to minimal delinquencies in 3 years at all ratings. There’s something for everyone and interest rates vary accordingly. It is an amazing lenders market place.

This is great advice for borrowers. As a P2P investor I am MUCH more likely to invest in loans where the borrower has taken the time to describe their financial situation and purpose of the loan in detail no matter what their “rating” may be.

I don’t know if it is the same way on Prosper, but with Lending Club investors can ask questions to the borrowers. Answering those honestly and completely will also significantly increase your chances of getting your loan funded.

Hi Sam – I ended up opening a $1,000 balance with Prosper about a month ago and using their quick invest option to see how it works. Chose mostly B and C rated folks with debt consolidation. Still getting comfortable with it.

Wow that’s a lot of delinquencies in the first example. This reminds me of interviewing. I ask candidates the same amount of questions yet the interviews constantly range widely in length. Even if someone looks good on paper, if they only give me short 1-10 word answers I lose interest quickly and move on. Someone with a less impressive resume who presents themself well and gives thorough, well constructed answers will keep my attention. And of course someone who looks great on paper and also presents well in person comes out on top.

Yeah, perhaps the first example is too extreme. Makes me wonder even with a decent description, why bother taking the chance when there are others with much less delinquency.