In America, we are truly blessed with opportunity to help us chart our own course and grasp success as much as we desire it. Services provided by financial institutions are one of the things that we as American citizens have easy access to, allowing us to utilize financing and credit to further our goals in aspects of our financial strategies on both a personal and business level.

In America, we are truly blessed with opportunity to help us chart our own course and grasp success as much as we desire it. Services provided by financial institutions are one of the things that we as American citizens have easy access to, allowing us to utilize financing and credit to further our goals in aspects of our financial strategies on both a personal and business level.

For many Americans, the idea of not being able to take out a mortgage to purchase a house, obtain student loans for higher education, or receive business loans to pursue business goals would be unfathomable – yet there is a significant portion of the world’s population that simply does not have access to financial services of this nature.

What is microfinance? Kiva explains it well, “Microfinance is a general term to describe financial services to low-income individuals or to those who do not have access to typical banking services. Microfinance is also the idea that low-income individuals are capable of lifting themselves out of poverty if given access to financial services.”

Kiva’s Origins

This is the problem that Matthew Flannery and Jessica Jackley wanted to address when they founded Kiva (named after the word for “unity” in Swahili, as opposed to the North American word for a Hopi religious house). While Jackley was in Africa performing charity work, she and Flannery spoke with business owners in East Africa, and determined that lack of access to the initial seed money to start a business was one of the primary barriers to entrepreneurship in the region.

They returned with the names of seven individuals and a plan. The two of them asked their wedding guests to help finance the loans for the initial borrowers, and in mid-2005 the initial seven loans were funded for a total of $3,500. Shortly after, Flannery and Jackley founded Kiva as a non-profit organization, quickly gaining the attention of Premal Shaw (of PayPal fame) and Reid Hoffman (CEO and founder of LinkedIn) in 2006.

That year also saw Kiva reach its first milestone of $1 million dollars in facilitated loans. Today that total has grown considerably – nearly $673 million has been loaned to financially underserved people around the world with the aid of individual borrowers.

How Does Kiva Work?

So how exactly does this Kiva loan thing work? In short, Kiva works with entities that they term field partners who are tasked with identifying prospective borrowers. The field partners gather the information from the borrowers for Kiva to post, and typically pre-disburse the loan to the borrower. The loan is then posted to the Kiva website to be funded by individuals who are willing to assist that borrower with at least a $25 dollar contribution to the loan. Once the loan is funded the money let is disbursed to the field partner who usually pre-disbursed the loan. As the borrower pays the loan back to Kiva, the lender’s account is credited with the repayments which can then be either withdrawn or lent to another borrower in a subsequent loan.

Lending in this manner means that your dollars can be used not as a one-time handout to the borrowers, but as a method by which they can increase their business potential – much as we would use a business loan in the US. For instance, the loans that I have made on Kiva so far are all in the agricultural sector, and have been used to help agrarian businesses purchase additional land to farm, purchase chickens to increase their production of eggs, purchase additional livestock, or purchase other agricultural inputs to increase the yield of existing crops.

The additional inputs allow these businesses to increase their profits so they can pay back the loan, and hopefully enjoy a longer term increase in business cash flow as well, that may have taken them years or even decades to save for at the local rates. I personally focus on agricultural loans because I believe that it is a necessity to ensure that the basic needs of a human being are met in order to help them realize their potential-and food availability is certainly one of the most basic needs.

Agricultural loans are not the only category that Kiva offers-there are multiple sector classifications on the site, a sample of which include Education, Retail, Transportation, Construction, Health, Housing, Manufacturing, Arts, etc. You can also pick further attributes to narrow down your loan search criteria, such as borrower gender, green technology loans, higher education, start-ups, underfunded areas, and conflict zones, to name a few.

Of course, you can scope out the borrowers that you are looking to lend to by geographic area, and as of this writing Kiva lists 84 countries in their overall list of countries that they are or have been active in (there are some countries that are listed where there are not loans that are in funding at this time). So, if I want to lend to a female farmer using green growing methods in Ecuador, I can query for a list of those specific loans to see what is available.

Alternately, if you want to simply donate money to Kiva itself, you can do that either through a direct donation or donation of repayment of your loans. Kiva currently states that each dollar donated directly to the organization enables approximately $7 of lending funds for borrowers. There are other ways that you can assist with the organization as well, which we’ll get too soon.

Kiva Lending Teams

Kiva also allows you to join or create what they refer to as lending teams. The types of these teams vary widely – events like weddings, teams founded in memorium, religious affiliations, countries, universities, US states, and US and foreign city teams can all be found within the team search. There are currently 37,393 lending teams on Kiva with memberships ranging from 1 to 121,879 borrowers that have borrowed between $0 and $19+ million dollars since their inception.

Kiva also allows you to join or create what they refer to as lending teams. The types of these teams vary widely – events like weddings, teams founded in memorium, religious affiliations, countries, universities, US states, and US and foreign city teams can all be found within the team search. There are currently 37,393 lending teams on Kiva with memberships ranging from 1 to 121,879 borrowers that have borrowed between $0 and $19+ million dollars since their inception.

I’ve been lending for a little over a year through Kiva and I formed a lending team soon after creating my account. It was right around Christmas in 2013, and instead of giving material items to family members, I decided that I was going to give Kiva gift cards instead. I reasoned that it was essentially the same as giving cash if they wanted to withdraw the loan after it was paid back, and would be more representative of the season than sending candy or other material gifts to the adults (anyone under the age of 18 still received a gift).

I formed an open common interest team with the stated goals of lending to agriculture, retail, commerce, and education in Eastern Europe, Central America, and South America. Most of the people I sent the Kiva cards to did redeem them and make a loan, although some did not (this is often the fate of regular cash gift cards as well). If you give a Kiva gift card and it isn’t used within a year, it will automatically be donated to Kiva itself to help them cover operating costs.

I found that the process of creating the team and inviting the gift card recipients was relatively easy, although I did end up helping some of the less computer savvy recipients get their accounts created. You can also belong to multiple teams, so if you want to dedicate your loans to fisherman to the “Guys Holding Fish” team and your other loans to a different team, you can do that.

Kiva gives you some nice dashboards to review your lending activity at both a personal and a team level. A trip to your personal portfolio shows your deposits, amount lent, all past loans (active or paid off), as well as your current available credit (funds returned by borrowers typically). A trip to the in depth lending statistics page will show which sectors, countries, activities, and social performance badges you’ve helped with your loans. There’s also a message board where you can communicate, and an overall page of the loans that the team has made.

Kiva Zip Loans

The above lending model is not the only method that you can utilize with Kiva. Recently Kiva has opened Kiva Zip loans, which are 0% interest loans in $5 increments in either the United States or Kenya.

These are assessed based on what Kiva calls Trustees, groups or individuals which vet the character of the borrower, essentially vouching for their reliability in order for the borrower to be listed on the site. Presently that means that these loan types are limited geographically. There are multiple Trustees listed with designee repayment rates less than 50%, so whether or not the vetting process for this is effective is up for interpretation. That said, unlike a Kiva Partner, the trustee never handles the loan or takes repayment, Kiva itself handles both of these.

I haven’t lent through the Zip model myself, but if you are someone who would prefer to keep your charitable giving more local (and by that I mean the US) there are a number of loans available within the United States. Some examples on the site currently range from organic farmers, veterans support businesses, urban mushroom farmers, art galleries, to food trucks.

Kiva Zip is, as noted earlier, a recent addition to the Kiva site, and you’ll see if you go to that area of the site that it is still being referred to as Beta. So far Kiva Zip has loaned $6.3 million to 7,885 small businesses with an 89% repayment rate (lending through the original model boasts an impressive 98.76% repayment rate).

Losses and Tax Considerations

Since this is a financial blog, I think it is necessary to mention the topic of loss of principal and tax considerations when using Kiva. First of all, I’d like to be clear that you are not going to make any money lending on Kiva, that’s simply not the purpose of the site, and if that’s your goal you’re talking about investing instead of charity-in which case you should perhaps be on Lending Club instead.

To take that one step further, I would assign at least a 99% probability that you are going to lose money as you lend it. This shouldn’t be a big deal to you as I assume that your purpose on Kiva is not to retain wealth, but to assist those with less opportunity than we enjoy in the US.

As your loans are paid back over the course of a year or more, you will be losing value to inflation. You may also lose money through currency transaction losses or failure to repay, the former I believe to be more likely than the latter as your loans are often made in the local currency. I was exposed to this with my very first loan on Kiva, where I loaned to a farmer in Ukraine in late 2013. Due to the revolution and extreme unpleasantness that has been happening in that nation, the local currency had lost over half of its value compared to the dollar by the time the final payments on my loan were made, so I was returned the dollar value of that currency at the time each payment was made (the farmer didn’t renege, he paid back 100% of what was owed).

It’s also necessary to point out that unless you are donating money to Kiva itself, which is a 501 (c)(3) non-profit, your loans are not tax deductible as you could withdraw that money after it is paid back. However, you could build up a fund of loan money on the site that could be then donated to Kiva directly to increase your tax deductions in a single year, so it would be possible to employ this as a basic tax reduction strategy if desired.

However, I have found no indication that you can write off a loss due to either currency changes or default, since there is no possibility of a gain occurring and a non-donated loan is therefore not classified as either an investment or a charitable donation if you are returning repayments to your account.

Kiva's Criticisms

We’ve already covered one of the items that have been raised as a criticism of Kiva to some extent, which is the no benefit zone that the lender enters when they accept repayments of the loan in regard to either tax treatment and the inevitable loss of principal value due to inflation. It’s kind of like keeping money in your mattress in a mix of foreign currencies in that regard.

We’ve already covered one of the items that have been raised as a criticism of Kiva to some extent, which is the no benefit zone that the lender enters when they accept repayments of the loan in regard to either tax treatment and the inevitable loss of principal value due to inflation. It’s kind of like keeping money in your mattress in a mix of foreign currencies in that regard.

There have been a few proposals floated by users to pay a low interest rate on loaned funds to allow them to be an “investment.” I’m sure the logistics of this would in no way going to be beneficial to Kiva (government regulations, I’m quite confident, are going to induce prohibitive costs at the least). I expect this to happen never.

If you want the tax break, you can always donate repayments, or donate directly to Kiva itself. If you want to make money, as mentioned earlier, you are on the wrong site. I believe that this essentially renders these criticisms irrelevant.

Then we come to what I like to call the Kiva Kerfluffles. There have been at least two incidents where users and observers have ended up with their underwear in a twist over loans for cultural activities they don’t personally approve of, or other lenders being allowed to lend to people whom other lenders do not approve of. If you want to spend 30 minutes of your life looking at these items query up Kiva cockfighting or Kiva Strathmore University.

I sum these incidents up like this. If you don’t like the business owner’s activities, then you are free to not lend to them despite the fact you may be upset over a cultural norm in their area. If you happen to feel that you don’t like another lender’s ideals and that they should not be allowed to lend, you should probably consider that you are likely overlooking the good that lender is doing (just like you) in trying to help other people improve their lives.

It’s also fair to point out that Kiva did not have anything to do with either of these items except being the connection point between the lenders and the field partners. The field partners evaluate loans, Kiva finds and enables lenders. Banning borrowers based on their culture or banning lenders based on their religious beliefs sounds pretty wrong too-which seemed to be the basic goal of those upset by these events.

There are also some who feel that the Kiva system is in some way dishonest because loans are pre-disbursed and then posted to the Kiva site. I have to take issue with this item as well, mainly because it states clearly on the loan page for each loan when the loan was issued. You do have a direct connection to the borrower in regard to you will receive your payments from that borrower, but the borrower probably will have no idea who you are or that you helped fund the field partner that loaned them money unless they happen to log in to Kiva themselves to look at their loan that was posted.

In my opinion, Kiva and the field partners are doing exactly what is needed. Imagine if one of the farmers I lent to had to wait for myself and the others who funded their loans. What if that stretched halfway through the growing season before their funds got disbursed? This could actually create additional hardship for the borrowers if funds were not pre-disbursed, by burdening them with a loan repayment when they would not have been able to employ the funds loaned in a timely fashion.

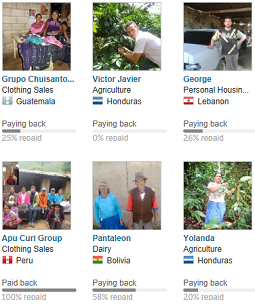

The last item that you’ll see come up is interest rates on the loans. This is something that you may want to pay some attention to if you really want to do a great deal of due diligence as you select your loans. When you look at a loan page, you’ll see an item in the loan description that is called Average Cost to Borrower, along with a figure for Profitability. I’m looking at a loan right now in Guatemala with a 26% PY (Portfolio Yield) and .7% Profitability figure. Portfolio Yield is not a direct measurement of the interest rates that the borrower is going to pay, but it is representative of the average cost to borrowers for that field partner.

Let’s look at a couple of other field partners-a loan in Uganda, 77% PY, 2.4% Profitability figure, and one in Vietnam 6% PY and an N/A for Profitability. As you can see these figures vary quite a bit. I would also say that the figure you may want to consider more important is profitability, which since this is charitable lending perhaps should be on the lower side. You can type in #Low-profitFP in the search bar on the lending page to return only low profit partners. You may also want to consider that if a field partner is posting negative returns, they may not be operating for very long. Understand that when you’re looking at the PY number you cannot apply the logic of our current low interest rate environment in the US. The country you are looking at likely does not have that same environment.

Why Choose Kiva?

Kiva is one of many choices that you have when it comes to charity. When I initially looked at this organization, the things that appealed to me were the facts that my charitable loans would be able to be plowed back in to additional borrowers after repayment, it gave me additional control over where the money was going, and most important, was providing a financial service that would empower the borrowers and improve their local economy instead of making them dependent and/or potentially disrupting their local economy, as often occurs with what I call the hand-out style of charity.

Not to mention, Kiva has been the recipient of multiple awards recognizing the value and effectiveness of their charitable impact worldwide. Here’s a list of some of these awards.

- org recognized Kiva with its Global Impact Award in 2013

- Philanthropedia awarded Kiva it’s Top Non-Profit Award in 2012

- Charity Navigator rates Kiva 4 stars as of 2012 (the highest rating in the most recent year evaluated) with an overall score of 98.76/100 and 100/100 in accountability & transparency

- The Economist gave Kiva its Innovation Award in 2011

- The Omidyar Network granted Kiva $5 Million in 2010 to improve Kiva’s charitable impact

- The Skoll Foundation recognized Kiva with the Skoll Award for Social Entrepreneurship in 2008

More Options to Help Others

There are additional options you can pursue to assist Kiva in its mission beyond becoming a Kiva lender or donating to the organization directly. If you’re one of those with spare time on their hands, you could become a Kiva Fellow, or volunteer your time as an intern at the Headquarters in San Francisco or New York City.

Are you an experienced editor or have a background in technical writing or journalism? You can volunteer as an editor. Do you speak a foreign language at a high level of proficiency? You can volunteer your time to translate loan profiles in the languages that you are skilled in to English. If you’re a skilled programmer, you can drop by build.kiva.org and volunteer to share your knowledge by building applications to assist with Kiva’s mission. Want to help start-ups in your local area take advantage of the new Zip loans? Apply to become a Kiva Trustee.

I’d like to provide a little more context for a couple of these items, specifically the Kiva Fellows and Kiva Interns, as they can be more of a commitment from a time perspective. In order to become a Kiva Fellow or Kiva Intern, you should be prepared to invest 4-12 months or 5 months of your time respectively in volunteer positions with Kiva.

Kiva Fellows apply to go through Kiva’s Fellow classes, and are subsequently utilized as the boots on the ground for Kiva’s mission in various countries that Kiva works in world wide. Since these are unpaid volunteer positions, they might be an ideal way for someone who is financially independent, adventurous, and adaptable to share their skill set with Kiva while doing good for humanity. If you want to check out the class dates and application process, you can look at the Kiva Fellows Program.

Kiva Interns have a similar scenario, although they are for a period of 5 months. The internships are also unpaid volunteer work that you can apply for either to hone your skills in a non-profit environment, or volunteer your skills to assist with the charity. Intern classes happen 3 times per year, and can be applied for at the Kiva Internship Program.

If Not Kiva, Find Your Way

There are multitudes of ways that you can volunteer your time (perhaps the most valuable thing you have) or money in pursuit of charitable endeavors. Historically, I’ve been far more inclined to donate my time than money to charitable organizations (highly tax inefficient) such as the local Veteran’s Shelter, Food Shelf, or Habitat for Humanity.

Kiva is one of the few charitable organizations that I’ve been willing to trust any money too since I was burned at the early age of 8 donating to a “Save the Rainforest” charity which I later felt had collected my money under false pretenses. I believe that their level of transparency is excellent, and the methodology that they employ to connect lenders and borrowers in need of microfinance lending opportunities is superb. I’ve seen some users go so far as to call it addictive.

If you’d like to join my team on Kiva you are welcome to join the Green Knight Society. While I’ve established some goals for team members, it’s your money, so you should feel free to lend where and how you would prefer. I don’t receive any financial consideration for new team members or their loans, except perhaps some positive karma – so join whatever team you like, or lend individually, it really doesn’t matter how you decide to contribute as long as you do.

Microfinance services like Kiva do have a positive impact globally and do help to level the playing field to some extent, enabling those born into areas that do not have the same sort of financial services available to them as we do in the United States of America. Not to mention the buy-in is a mere $25, not a huge amount of money to an American, but a significant benefit to someone in a country like Guatemala where the average annual income is just over $4,000 USD.

Hopefully this post has given you a better understanding of how Kiva works, so you can determine if this is one of the ways that you want to give back to your fellow man. Thanks for the space on your blog Sam!

-GreenKnight008

Wealth Building Recommendation

Manage Your Finances In One Place: One of the best way to become financially independent and protect yourself is to get a handle on your finances by signing up with Personal Capital. They are a free online platform which aggregates all your financial accounts in one place so you can see where you can optimize your money. Before Personal Capital, I had to log into eight different systems to track 25+ difference accounts (brokerage, multiple banks, 401K, etc) to manage my finances on an Excel spreadsheet. Now, I can just log into Personal Capital to see how all my accounts are doing, including my net worth. I can also see how much I’m spending and saving every month through their cash flow tool.

A great feature is their Portfolio Fee Analyzer, which runs your investment portfolio(s) through its software in a click of a button to see what you are paying. I found out I was paying $1,700 a year in portfolio fees I had no idea I was hemorrhaging! There is no better financial tool online that has helped me more to achieve financial freedom. It only takes a minute to sign up.

Finally, they recently launched their amazing Retirement Planning Calculator that pulls in your real data and runs a Monte Carlo simulation to give you deep insights into your financial future. Personal Capital is free, and less than one minute to sign up. It's one of the most valuable tools I've found to help achieve financial freedom.

About the Author: Sam began investing his own money ever since he first opened a Charles Schwab brokerage account online in 1995. Sam loved investing so much that he decided to make a career out of investing by spending the next 13 years after college on Wall Street. During this time, Sam received his MBA from UC Berkeley with a focus on finance and real estate. He also became Series 7 and Series 63 registered. In 2012, Sam was able to retire at the age of 35 largely due to his investments that now generate over six figures a year in passive income. Sam now spends his time playing tennis, spending time with family, and writing online to help others achieve financial freedom.

Updated for 2018 and beyond.

If anybody is wondering about the profitability and Portfolio yield definition, here is GreenKnight’s response:

Portfolio yield as I understand it is the interest rate charged on average for borrowers from that field partner. That does not equate to the money that the field partner clears, which is the profitability figure. The field partners aren’t necessarily charitable organizations, although many of them are. The field partners can and do make money off of the loans, which is why I mentioned that the profitability figure may be the more important one. While they should have some profitability in my estimation (to ensure they don’t collapse) high profitability numbers may be indicative of gouging on the interest rates.

The numbers can be a bit tricky, because in order to understand if the field partner is giving a competitive rate, you’d really have to understand the specific country’s economic situation, and the relationship and perhaps geography between the lender and the recipient. A country with high inflation should have a higher PY figure for instance, so one of the problems that people often have with this is they look at the PY and think to themselves “Well, I can get a loan for 6% here in America, so obviously that field partner in Uganda charging 77% PY is lending at predatory rates.” That may well not be the case and that 77% might be the actual rate the Uganda field partner needs to charge to stay even or turn a small profit to expand their operations.

Both of those statistics are measures of the field partner though. This tripped me up initially when I looked at the site too, as I had the impression that this was a return that the charitable money would be getting, but it’s not.

Back in college, we were asked to write a persuasive speech to convince the class they should donate to our cause. Instead of donating money, I thought it would be better for everyone to lend the money – through Kiva.org. Annoyingly, the class decided to donate to some random flavor-of-the-month charity. Nevertheless, I think Kiva rocks. Heffer rocks as well. I’m all for helping people help themselves.

Hi. My name is Larry. I am very concerned about our children. My children live in Arizona. I live in Washongton state. Poverty is a fact for our children in divorced familys here in America. Lawyers, courts, and personal self interests of survival all deal into the melting pot.

I am special and need some sort of consultations here.

I am 51, just took retirement from a larger corporation…. taking my pension, and have/am

(of course split the pension fund in half) in the process of moving my money to my new companies (a huge company with astranomical aspirations) at which I was just employed at within two years ago. I have not done my taxes this year and am in great fear. Poverty is coming to all who have not informed themselves of our worldly governmental systems.

i.e. (Just my opinion}

I love to donate to causes of worth. I am a w-2 worker who enjoys making money on the side but have not set up a business here (I have made my living in auto repair/manufacturing/mechanical/autobody/cusom/RV repair/etc) because I have move to a new state of residence.

Currently I have 60k roling over into a 401 k. I am taking 40k to keep me going for another 15 years (buy a harley) and to try to repair my financial situation. I would prefer a whole new blog spot for people like me….. because there are many of us coming your way. I am on the cutting edge of american workers wealth/poverty and I do not want to make a mistake right here right now.

Larry, I think the biggest mistake you can make is to use some of your retirement funds to buy a Harley. And I say this as a motorcycle rider myself. Keep as much as you can in your retirement fund, and through discipline, dig yourself out of your financial problems. Start actively setting financial goals for yourself, and only reward yourself (with smaller rewards than a Harley) AFTER you have met those goals.

I see so many people struggling their way through life, headed close to retirement, who blow money that they really don’t have to spend on a Harley, or a big new SUV, or an RV or some other toy. Trust me, it’s a huge mistake. Get your financial affairs in order first, and then if you’re getting ahead of the game, you can splurge a little, and in a smart way. I.e., not a brand-new Road King, but maybe a used Harley that’s 5-8 years old.

Just so you don’t think I’m blowing smoke here: I’m 35 years old, I earn about $160,000 a year as an attorney and have a net worth of a bit over $1 million. I don’t get to buy anything fun until my retirement account is funded for the year, and I always make sure my savings account is big enough to cover emergencies. Even with that income and balance sheet, I drive a car that is currently worth about $13,000 (it’s 6 years old now and I plan to keep driving it for at least 2 more years). I wanted to buy a Suzuki Hayabusa, and I wanted one REALLY bad for years before I finally got one. When I finally got one, I bought one that was 7 years old and had only about 4,500 miles on it. For motorcycles, it’s pretty common to find them in about that age range with low mileage, because lots of people get them and hardly ride them, or get them and then scare the crap out of themselves with a near-accident and then sell them. A brand-new Busa would have cost me around $12,500, and my used one cost me $4,200. Totally worth it. (But only because I could afford it. It wouldn’t have been worth it if I had to pull money from my retirement account to buy it.)

You have to adjust your expectations based on what works for you, and take care of the important stuff first. You can’t buy the Harley now and then decide, 15 years later, that you really want to un-make that decision and get the money back in your bank account, with interest. Once it’s gone, it’s gone.

Don’t fall into the trap of telling yourself that you deserve a Harley because of the years of hard work you’ve already put in. My mom taught me at age 12 that no one “deserves” anything. You have to bust your butt, make smart decisions, and then when you can afford something, you can buy it. A sense of entitlement never paid anyone’s bills.

Hang in there, Larry.

Ok. I can do that, but what should I do with the 30k(after taxes) I took in my split distribution? I owe my attorney in Arizona just over 20k, but I am going to try to settle out on some of that. (I don’t want to give them anything really) I was going to spend 8k on a motorcycle. I want to buy a house too, (my landlord wants to sell me the house I am in now and I could get a steal on it) but maybe its too late for me and I should just start slamming money in my 401k instead.

My life has been in utter ruins since 2006 when I divorced. Now, I have a great job that’ll pay me 80k for a starting wage.

I can wait a few years on the motorcycle, but the lawyer? I just want her off my butt. I claimed bankruptcy last year so lawyer is about my only bill. Anybody ?

Sorry to hear about the divorce. Those can be brutal, for sure. Paying off the lawyer is a good idea, especially if you can negotiate the bill down a little. Maybe you should tell her something like “If you’re willing to reduce your fee to [pick a number — $15,000?], I can take some money out of my retirement fund to pay you off in one lump sum. Otherwise, I will need to continue making payments for a long time.” She might take you up on the offer to get paid quickly.

After paying off the lawyer, I think putting the money toward the purchase of your current house is a great idea. At age 51, it’s definitely not too late to buy real estate. Be sure to document the sale appropriately. It might be tempting because you have a history with your landlord to be loosey-goosey with the documentation, but you could get burned badly by doing that, so protect yourself.

I would pay it into real estate instead of putting the additional amount in your 401k. Your house can operate as a pretty decent retirement investment, and you will have diversified your holdings by putting some in real estate and some in the stock market.

Also, if/when you buy your house, consider accelerating the repayment of the loan to the extent you can afford it. Additional principal payments of even a few hundred bucks a month can drastically accelerate the repayment of the loan. If you’re familiar with amortization schedules, you might run a couple of comparable scenarios to see how fast you can pay off the house and be living mortgage-free. There are online calculators for that sort of thing, or you can download a template for Microsoft Excel.

Thanks for sharing so much about Kiva. This is the first I’ve heard of them. That is very cool that there are agricultural, education, and health loans. And wow that’s neat that they are helping borrowers in so many countries! Given the way it’s structured I think I would probably make an actual donation straight to Kiva so I could get the tax write-off.

Wow, a huge amount of detail here, but thanks for sharing and giving a detailed insight into how Kiva works. I think microfinance is a brilliant idea for encouraging less fortunate people and countries to grow and develop, and definitely something I’d love to be involved in further one way or another.

Cheers,

Jason

Kiva is cool, especially when you bring kids into the mix. I received a gift of $25 on Kiva and decided to have my (at the time) 5 y.o. help decide whom to loan money.

It was pretty funny when later, in his kindergarten class, the teacher asked where people most wanted to go on vacation. My son said he wanted to drive our car to Tajikistan so the guy we loaned money for his car wash business could give us a wash…

We’ve ended up loaning to a lot of interesting places, and I’ve been able to teach my son a lot about the world and entrepreneurship, while, of course, trying to help some folks out.

It’s an especially good idea for a gift to someone, as an alternative to just buying more stuff.

That’s a great idea! A wonderful way to help someone while also learning more about the world ourselves, teaching our kids about other people and their lives, and also remembering/showing our kids how fortunate we are to have everything that we do. Keep it up!