Dear Financial Samurai,

Every year, more than 60,000 Europeans die from summer heat. When I first heard that statistic, I assumed it was a demographics story, and it mostly is. Over 85% of the victims are age 65 or older.

But here’s the conundrum. The over-65 crowd also has the most money to spend on not dying. I believe people are mostly rational, and nobody rationally chooses to roast in a hot apartment to save a few bucks on electricity.

Then I spent an afternoon taking my parents to lunch in Honolulu’s blazing heat, and I finally understood. It’s not just frugality. It’s stubborn habits, unawareness, and the sheer activation energy required to change anything after a certain age.

If your parents are getting up there, please read this post. It might just save their lives: In Praise Of Unnecessary Suffering (Until It Does You In)

Speaking of taking care of the people you love, if anybody depends on your income, you need life insurance. My wife and I finally got matching 20-year term policies through Policygenius during the pandemic, and the relief was immediate. Policygenius lets you compare real quotes from top carriers side by side in minutes, for free. Check your rates with Policygenius here and stop procrastinating like our parents do.

Marshmallow Test Times 10

I bought my first stock in 1996. After 30 years of investing, my main conclusion for building great wealth is boring: buy low-cost index funds, hold them for decades, and stop touching your portfolio. I’m certain 90% of you who try day trading for more than a year will lose money or make so little it wasn’t worth your time.

The problem is temptation. It’s too easy to log into your brokerage account and panic sell after a collapse (March 2020) or FOMO buy after a ramp (semiconductors), right before everything reverses. And the longer you invest and the more capital you accumulate, the more turbulence you’ll face, and the louder the temptation gets.

This temptation is one reason why I happily invest up to 20% of my capital in traditional venture capital and private real estate. I can’t sell even if I want to. Illiquidity has saved me many times from selling at the wrong time.

But this year, I finally experienced maximum investing emotion, the kind where life-changing sums are at stake: holding an asset I’m locked up from selling for six months. There’s nothing to do except make some imperfect hedges that cost money and wait. It’s been quite an emotional ride that has tested my discipline for not spending on unnecessary things.

If you’re thinking of joining a promising pre-IPO startup or getting into venture or angel investing, this post is for you: What It’s Like Waiting Out A 6-Month Lockup.

Doing The Math For Sanity’s Sake

The asset in question is VCX, Fundrise’s Innovation Fund, which listed on the NYSE on March 19, 2026. I purposely waited four months to write about the experience so the initial mania could die down and I could think clearly again.

To keep the FOMO and daydreaming at bay, I did a rigorous analysis of what VCX’s NAV is truly worth. The share price is simply NAV plus a premium or discount, and so far the premium has been doing most of the driving.

If you’re a VCX shareholder or want to learn how to value a closed-end fund, this post walks through everything. Once I finished the analysis, I could set realistic expectations for the shares at lockup expiration and model out different future scenarios.

I don’t think you’ll find a more comprehensive analysis out there, which briefly made me wonder if I should go back to working on Wall Street. Then I remembered I’m on summer vacation and I value my freedom too much. This post took forever, with some great feedback from the community as well.

Stock Market Stuck Back In Neutral

I was hopeful the worst was behind us in equities. Unfortunately, the war in Iran is reescalating, oil prices are shooting up again (+21% in a week), Google’s bloat is showing with a delay in its latest Gemini model, SpaceX is under IPO price, and momentum names in the semis and DRAM sectors are correcting.

Two benign inflation prints last week did little to bring the 10-year yield down. At least the market is no longer pricing in a Fed rate hike this year, which it was just a week prior. But I’m not sure the Fed matters much when the bond market keeps doing its job for it.

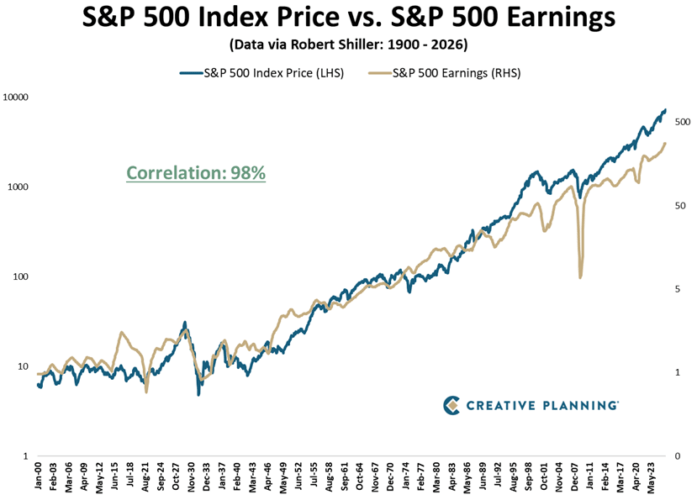

What keeps me hopeful: earnings. S&P 500 EPS is now expected to grow about 24% year over year ($275 to ~$341), while the index is only up single digits so far. That means the market is actually cheaper today than it was in January, which lowers the odds of a bigger correction. And if we get one anyway, I’ll be buying the dip again.

Notice how the gap between the blue line and the gold line is widening since the 2008-2009 global financial crisis. That’s comforting for long-term investors.

One way I’ve dampened all this stock market whipsaw is by allocating to private real estate and private credit through Fundrise. Real estate is my favorite asset class for building wealth because it’s less volatile, generates income, and you can’t panic sell it at 2 am. With the 10-year yield stubbornly high, private credit is also paying attractive income. You can invest with Fundrise starting with as little as $10. Financial Samurai is an investor in Fundrise, and Fundrise is a longtime sponsor of Financial Samurai.

To your financial freedom,

Sam

Keep In Touch

If a friend forwarded you this newsletter, join 60,000+ readers and subscribe at financialsamurai.com/news. You can also sign up at financialsamurai.com/email to get every new post the moment it’s published and read it ad-free for the first few hours.

Money is too important to be left up to pontification. Everything I write is based on firsthand experience, since I started Financial Samurai in 2009.