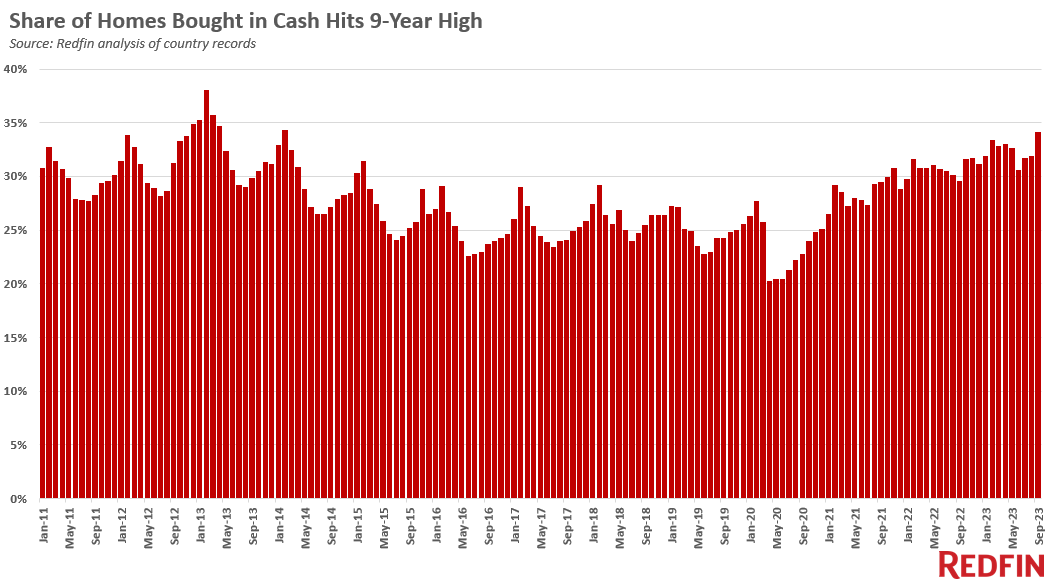

Partially thanks to high mortgage rates, the percentage of homebuyers who pay cash has risen. As of September 2023, according to Redfin, 34.1% of U.S. home purchases were made in cash. This is up from 29.5% in September 2022, when mortgage rates were lower.

In 2025, the percentage of homebuyers who pay cash is likely even higher. Some 46.8% of luxury homes were bought entirely with cash in the three months ended February 29, 2024, according to Redfin. That's the highest share of all-cash luxury home purchases in at least a decade and it's up from 44.1% from a year earlier.

Redfin analyzed county records across 40 of the most populous U.S. metropolitan areas, going back through 2011. An all-cash purchase is one in which there is no mortgage loan information on the deed.

Boost your wealth through private real estate: Invest in real estate without the burden of a mortgage or maintenance with Fundrise. With over $3 billion in assets under management and 350,000+ investors, Fundrise specializes in residential and industrial real estate. I’ve personally invested $300,000 with Fundrise to generate more passive income. The investment minimum is only $10, so it's easy for everybody to dollar-cost average in and build exposure.

The Reasons For Rising All-Cash Home Purchases

Let me share one obvious and several not-so-obvious reasons why all-cash home purchases are rising. There are many psychological aspects that go into paying all cash for a home, in addition to financial ones.

1) Rising mortgage rates.

The most obvious reason why the percentage of homes being purchased with all cash is rising is due to the increase in mortgage rates. The average 30-year fixed-rate mortgage almost tripled from about 2.75% in 2020 to roughly 7.15% in 2024. As a result, fewer homebuyers are taking on debt to buy.

Unfortunately, when you pay all cash for a home in a high-mortgage rate environment, you also give up earning high risk-free income. In this current environment, money market funds and Treasury bonds are paying 4.5% or more. But given mortgage rates are even higher than risk-free income, there is still a net benefit to the all-cash homebuyer.

2) Harder to get a mortgage.

Now for the not-so-obvious reasons why all-cash home purchases are rising.

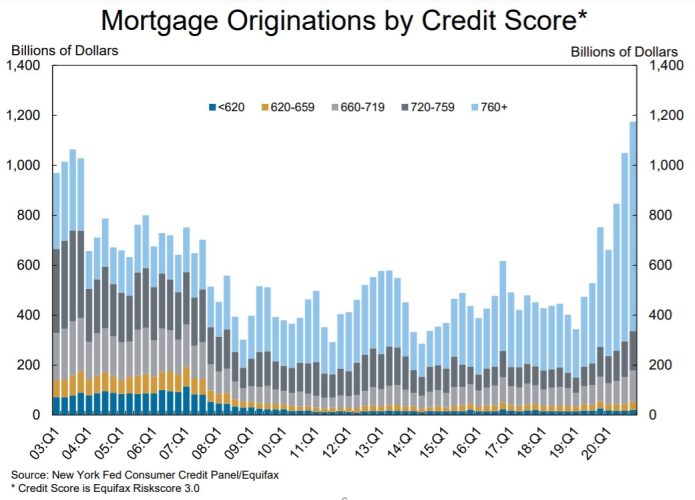

Ever since the 2008 global financial crisis, lending standards to purchase a home have tightened tremendously. The government forced all banks to raise their tier 1 capital ratio to protect banks from insolvency. Banks have also been much more stringent on whom they lend money to.

For example, the average credit score for an approved mortgage applicant is now over 720, an excellent score. Whereas before the financial crisis, the average credit score for an approved mortgage applicant was closer to 680, a good credit score.

Take a look at the chart below for mortgage originations by credit score. Notice how starting around 2009-2010, the light blue section (borrowers with 760+ credit scores) began to increase.

Given it is harder to qualify for a mortgage due to more stringent lending standards, more homebuyers are purchasing homes with cash. One may surmise that more family members are pooling together financial resources to help a family member buy a home. Or maybe people have more wealth than the government realizes due to stealth wealth.

However, on average, homebuyers with lower credit scores are usually less wealthy than those with higher credit scores.

3) The growth of consulting work.

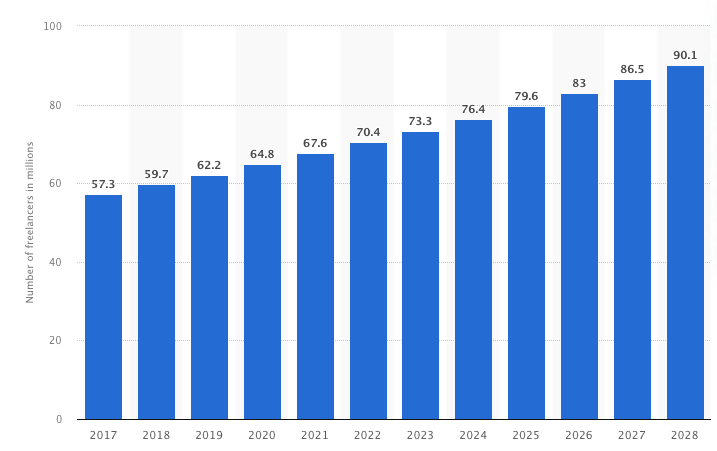

According to Statista, the number of freelancers in America is now around 73.3 million, or over 40% of the American working population. The percentage of American freelancers continues to increase thanks to technology, work-from-home, a lack of retirement benefits, and company disloyalty.

Ever since the global financial crisis, more Americans have realized the importance of having multiple income streams. Millions of people suddenly found themselves unemployed through no fault of their own. And novel ideas such as getting ahead of an impending layoff by negotiating a severance were born.

I've been a proponent of freelance consulting since I left my day job in 2012. If you're highly motivated, you could earn much more as a freelancer than at your day job and have more flexibility in your schedule. You just won't get healthcare and retirement benefits.

Below is a chart that shows the growth of freelance workers in America. The growth looks unstoppable.

Much harder to get a mortgage as a freelancer / consultant.

One problem with being a freelancer or consultant is that it becomes very difficult to qualify for a mortgage loan with only 1099 income. I tried in the past and failed.

Banks view freelancers as much riskier income-earners than people with W2 day jobs. If you don't have at least two years of freelance income, forget about ever getting a mortgage as most banks will want a much longer freelance income track record.

Given the growth of freelancing, the difficulty of getting a mortgage, and the continued increase in Americans desiring to own a home, it's natural that more freelancers are opting to pay cash.

4) Homebuyers are richer today than in the past.

Despite mortgage rates in being near 15-year highs, the percentage of homebuyers who pay cash is NOT at a 15-year high. Instead, the percentage is closer to a 9-year high if you look at the chart above. The last time the share of homes bought with cash was at the current 34% was in 1Q 2014.

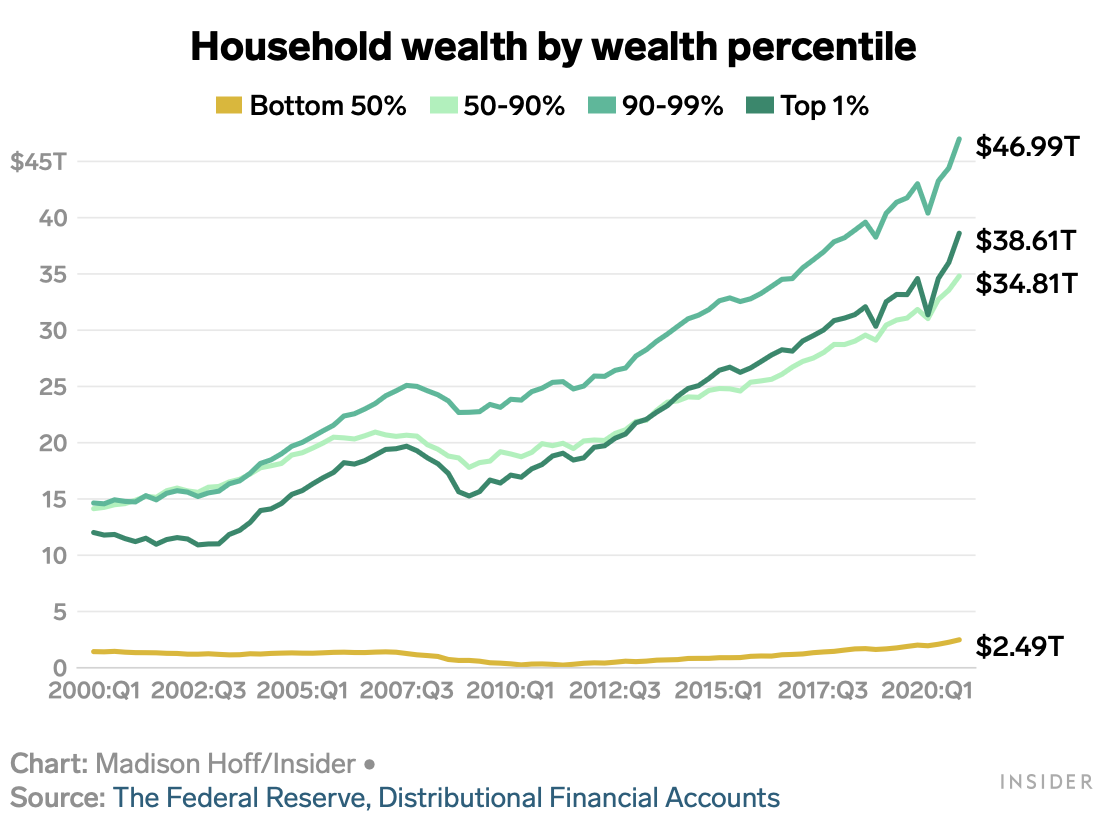

However, back in 2014, the 10-year bond yield was at about 2.7% versus ~4.5% today. This means mortgage rates were about 40% lower in 2014. For the same percentage of Americans to pay cash, despite 66% higher mortgage rates today, implies that cash buyers are relatively richer than before.

Just track the performance of stocks, real estate prices, and other risk assets since 2014. All have appreciated far beyond the pace of inflation. Therefore, Americans who invested in these assets have done well and can more easily pay cash for a house.

Boom In Tech And AI Leading To More Cash Buyers

Now in 2024, investors are richer thanks to robust performance in the S&P 500. Tech workers in the Bay Area are mostly richer thanks to the surge in big tech prices and artificial intelligence. The S&P 500 is near an all-time high again. As a result, more investors are able to sell stocks and pay all cash for a house.

As evidence of greater wealth in America, see the Fed's latest Consumer Finance Survey. The report showed the average net worth of American households is about $1.06 million. Meanwhile, the median net worth of American households is about $192,900. The net worth growth rate for both was about 20% over just three years.

Some buyers are able to make relatively large down payments because they’re using equity from their previous home. However, the share of homes being sold to first-time buyers is declining as it becomes harder to afford a home without selling another one and taking out the equity.

5) Lock in stock market gains and buy real estate before prices surge higher

The final reason why more Americans may be paying all cash for a house is to lock in stock market gains. Selling stocks after a rebound to invest in depressed real estate prices is enticing for those who can. Real estate prices generally lag the stock market by about six to twelve months.

Due to high mortgage rates, real estate prices around many parts of the country are depressed. As a result, homebuyers can get better deals. By paying cash, homebuyers can often get an even better deal because there's more certainty the deal will close once in escrow.

As more investors realize inflation has peaked and mortgage rates will likely go down, there will be increased demand to buy real estate before a potential recovery. We're past the bottom of the real estate market according to Ben Miller, CEO of Fundrise, a private real estate platform with $3.5 billion in assets under management.

The S&P 500 market finished up over 20% in 2023 and 2024. Given over 60% of Americans invest in stocks, over 60% of Americans also see much larger stock investment portfolios. Some of that money is flowing into real estate. Some have even earned enough to pay cash for homes.

More real estate buyers who understand that real estate prices lag the price performance in stocks are buying more prime properties with cash.

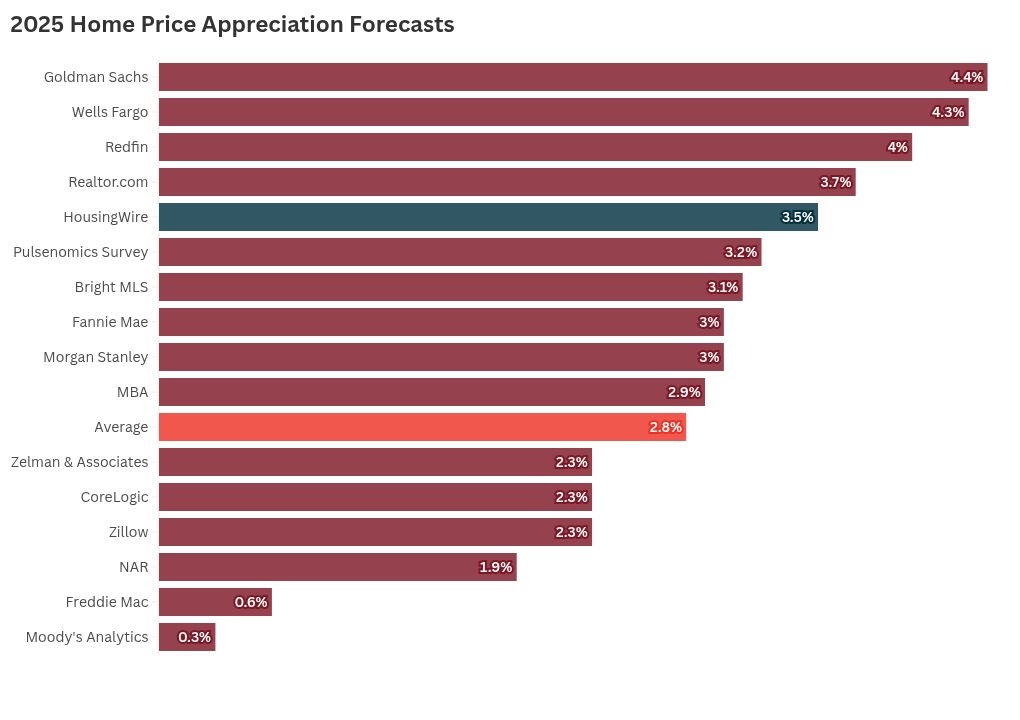

2025 Housing Price Forecasts

The average housing price forecast for 2025 is about 2.8%, after a +4% gain in 2024. With a continued positive outlook in the housing market, more buyers are paying cash as a result. And just in case the housing market doesn't do well, paying cash minimizes risk given there's no mortgage debt.

In most cases, home price forecasts for 2025 and 2026 are inching higher due to the strong labor market and overall strong economy.

Share Of Home Sales Using All Cash By U.S. Metro Area

Here is a fascinating table by Redfin that shows the percentage share of home sales using all cash and more.

In San Francisco, where I live, 26% of home sales were paid with all cash. The metro area with the highest percentage of cash buyers is West Palm Beach, Florida, at an impressive 49%.

| U.S. metro area | Share of home sales using all cash | Share of home sales using all cash, YoY (in percentage points) | Share of mortgaged home sales using FHA loans | Share of mortgaged home sales using FHA loans, YoY (in percentage points) | Share of mortgaged home sales using VA loan | Share of mortgaged home sales using VA loan, YoY (in percentage points) |

| Anaheim, CA | 31.7% | 5.9 pts. | 3.5% | -0.7 pts. | 1.7% | -0.8 pts. |

| Atlanta, GA | 41.0% | 1.1 pts. | 20.4% | 2.7 pts. | 7.5% | 0.5 pts. |

| Baltimore, MD | 41.8% | 11.2 pts. | 18.6% | 0.3 pts. | 8.9% | -1.5 pts. |

| Charlotte, NC | 39.4% | 2.9 pts. | 12.9% | 1.9 pts. | 5.5% | -0.9 pts. |

| Chicago, IL | 26.8% | 3.2 pts. | 15.5% | -2.9 pts. | 2.9% | 0.1 pts. |

| Cincinnati, OH | 45.6% | 6.5 pts. | 15.9% | -0.3 pts. | 6.1% | 0.3 pts. |

| Cleveland, OH | 49.2% | 7.4 pts. | 13.6% | -6.4 pts. | 3.5% | -1.5 pts. |

| Columbus, OH | 32.7% | 3.0 pts. | 14.1% | 2.6 pts. | 4.4% | -1.3 pts. |

| Denver, CO | 36.5% | 10.1 pts. | 14.0% | 1.4 pts. | 6.3% | 0.1 pts. |

| Detroit, MI | 38.0% | 3.9 pts. | 20.3% | -6.5 pts. | 3.1% | 0.1 pts. |

| Fort Lauderdale, FL | 40.5% | -0.5 pts. | 17.2% | 4.0 pts. | 3.8% | -0.5 pts. |

| Jacksonville, FL | 46.2% | 3.2 pts. | 15.7% | 0.3 pts. | 16.6% | -2.3 pts. |

| Las Vegas, NV | 33.1% | 0.7 pts. | 22.9% | 2.5 pts. | 9.7% | -2.7 pts. |

| Los Angeles, CA | 22.7% | 3.2 pts. | 15.2% | 1.7 pts. | 2.6% | unchanged |

| Miami, FL | 40.7% | 2.0 pts. | 17.5% | 3.9 pts. | 2.0% | -0.7 pts. |

| Milwaukee, WI | 33.0% | unchanged | 10.6% | 0.3 pts. | 3.6% | -1.1 pts. |

| Minneapolis, MN | 29.7% | 6.5 pts. | 8.8% | -0.5 pts. | 3.4% | -1.0 pts. |

| Montgomery County, PA | 35.0% | 7.6 pts. | 7.6% | -0.7 pts. | 3.0% | -0.8 pts. |

| Nashville, TN | 40.1% | 6.6 pts. | 19.3% | 9.0 pts. | 6.7% | 0.1 pts. |

| New Brunswick, NJ | 33.4% | 6.5 pts. | 12.5% | 0.8 pts. | 2.7% | 0.7 pts. |

| New York, NY | 36.9% | 8.6 pts. | 10.2% | 0.1 pts. | 0.9% | -0.6 pts. |

| Newark, NJ | 26.8% | 7.6 pts. | 14.8% | -2.6 pts. | 2.9% | -0.2 pts. |

| Oakland, CA | 18.0% | 3.9 pts. | 9.3% | 2.7 pts. | 1.7% | -0.5 pts. |

| Orlando, FL | 40.0% | 0.6 pts. | 21.5% | 3.5 pts. | 6.5% | -0.4 pts. |

| Philadelphia, PA | 41.1% | 6.7 pts. | 17.6% | -2.5 pts. | 3.3% | 0.2 pts. |

| Phoenix, AZ | 30.0% | 1.2 pts. | 20.8% | 4.6 pts. | 7.2% | -1.1 pts. |

| Pittsburgh, PA | 41.2% | 13.3 pts. | 17.5% | 2.8 pts. | 4.1% | -1.3 pts. |

| Portland, OR | 24.3% | -0.3 pts. | 13.9% | 3.0 pts. | 4.2% | -1.7 pts. |

| Providence, RI | 24.6% | -2.5 pts. | 25.0% | 2.6 pts. | 6.2% | 0.1 pts. |

| Riverside, CA | 40.7% | 6.0 pts. | 29.6% | 3.6 pts. | 6.5% | 0.6 pts. |

| Sacramento, CA | 26.0% | 5.9 pts. | 15.0% | -0.4 pts. | 5.4% | -1.1 pts. |

| San Diego, CA | 24.9% | 7.0 pts. | 9.6% | 3.3 pts. | 12.0% | -5.6 pts. |

| San Francisco, CA | 26.0% | 5.2 pts. | 1.4% | 0.4 pts. | 0.2% | -0.2 pts. |

| San Jose, CA | 18.2% | 6.3 pts. | 2.4% | 0.1 pts. | 0.9% | 0.4 pts. |

| Seattle, WA | 20.3% | 2.6 pts. | 6.6% | 1.1 pts. | 3.2% | unchanged |

| Tampa, FL | 38.2% | 0.2 pts. | 20.7% | 5.2 pts. | 9.8% | -1.6 pts. |

| Virginia Beach, VA | 23.4% | 2.0 pts. | 14.3% | -0.4 pts. | 41.0% | -0.6 pts. |

| Warren, MI | 35.8% | 4.9 pts. | 9.3% | -4.2 pts. | 4.5% | -0.2 pts. |

| Washington, DC | 26.2% | 5.7 pts. | 13.9% | 0.6 pts. | 15.2% | 0.7 pts. |

| West Palm Beach, FL | 49.0% | 0.8 pts. | 15.5% | 1.4 pts. | 3.0% | -1.8 pts. |

The Median Down Payment Amount In Various U.S. Metros

Here's another fantastic data table from Redfin that shows the median down payments in dollars and percentages by U.S. metro area. More expensive metro areas have higher down payments and vice versa.

With only a $75,000 median down payment in West Palm Beach, Florida, maybe the 49% of homebuyers who pay all cash is not that impressive after all. While the median down payment of $400,000 is.

| Median down payments, in dollars and percentages | ||||

| U.S. metro area | Median down payment (dollars) | Median down payment (dollars), YoY | Median down payment (percentage) | Median down payment (percentage), YoY, in percentage points |

| Anaheim, CA | $255,000 | 17.0% | 25.0% | 5.0 pts. |

| Atlanta, GA | $38,041 | 22.7% | 10.0% | unchanged |

| Baltimore, MD | $31,295 | 27.3% | 10.0% | 4.1 pts. |

| Charlotte, NC | $57,000 | 48.8% | 15.0% | 5.0 pts. |

| Chicago, IL | $35,775 | 14.6% | 10.0% | unchanged |

| Cincinnati, OH | $21,998 | -2.7% | 10.0% | unchanged |

| Cleveland, OH | $24,250 | 36.2% | 10.0% | 0.6 pts. |

| Columbus, OH | $35,874 | 23.1% | 10.0% | unchanged |

| Denver, CO | $80,000 | -3.0% | 15.8% | 0.8 pts. |

| Detroit, MI | $16,250 | 61.5% | 7.4% | 2.4 pts. |

| Fort Lauderdale, FL | $60,000 | 1.7% | 20.0% | unchanged |

| Jacksonville, FL | $40,032 | 50.8% | 10.0% | 1.2 pts. |

| Las Vegas, NV | $38,000 | 8.6% | 10.0% | unchanged |

| Los Angeles, CA | $169,375 | 6.3% | 20.0% | unchanged |

| Miami, FL | $80,000 | 9.8% | 20.0% | unchanged |

| Milwaukee, WI | $33,029 | 10.1% | 11.9% | 1.9 pts. |

| Minneapolis, MN | $44,985 | 22.6% | 13.0% | 3.0 pts. |

| Montgomery County, PA | $80,000 | 28.0% | 20.0% | 0.7 pts. |

| Nashville, TN | $49,287 | -8.7% | 12.2% | -2.5 pts. |

| New Brunswick, NJ | $100,000 | 15.9% | 20.0% | unchanged |

| New York, NY | $189,900 | 15.1% | 20.4% | 0.4 pts. |

| Newark, NJ | $95,096 | 37.5% | 20.0% | 5.0 pts. |

| Oakland, CA | $210,000 | 9.3% | 20.0% | unchanged |

| Orlando, FL | $45,000 | 1.6% | 11.0% | 0.8 pts. |

| Philadelphia, PA | $21,000 | 1.8% | 8.9% | 3.3 pts. |

| Phoenix, AZ | $46,500 | 1.6% | 10.0% | unchanged |

| Pittsburgh, PA | $16,940 | -12.9% | 10.0% | unchanged |

| Portland, OR | $90,159 | 12.3% | 20.0% | 4.3 pts. |

| Providence, RI | $40,000 | 0.0% | 10.0% | unchanged |

| Riverside, CA | $43,800 | -12.4% | 10.0% | unchanged |

| Sacramento, CA | $91,900 | 25.4% | 20.0% | 5.0 pts. |

| San Diego, CA | $170,000 | 25.9% | 20.0% | unchanged |

| San Francisco, CA | $400,000 | 7.3% | 25.1% | 0.1 pts. |

| San Jose, CA | $378,500 | 18.3% | 25.0% | 5.0 pts. |

| Seattle, WA | $167,172 | 11.4% | 20.0% | unchanged |

| Tampa, FL | $40,330 | 4.3% | 10.0% | unchanged |

| Virginia Beach, VA | $7,380 | 5.4% | 3.0% | unchanged |

| Warren, MI | $33,000 | 34.7% | 10.6% | 0.6 pts. |

| Washington, DC | $54,800 | 49.6% | 10.0% | 1.6 pts. |

| West Palm Beach, FL | $75,000 | 8.7% | 20.0% | unchanged |

Never Thought Of Paying All-Cash For A House Until My 40s

I have now twice paid all cash for a house, once in 2019 and once in 2023. In 2019, at age 42, I purchased a fixer and spent a couple of years remodeling it. It is now a rental.

I will never do another gut remodel in my life! Too painful.

In 2023, I bought the nicest home I could afford after selling stocks and bonds. Since a few years prior, the home I wanted to buy went down in price by 14% and my stocks rebounded by over 20%. Therefore, I figured paying cash for a home was a decent trade.

Here are the main reasons why I paid cash for two homes:

- Got me a better deal (lower purchase price)

- Enjoy turning funny money stocks and venture capital investments into real assets

- Hate going through the painful mortgage application process and paying a fee to borrow money

- Stocks felt fairly valued when I sold each time, although stocks continue to go up long term

- Finally accumulated a large enough net worth to do so

In my 20s and 30s, I was grinding hard to build my financial nut. Of course I couldn't pay all-cash for a home. Getting a mortgage was the only way I could get on the property ladder.

Once I accumulated a large enough net worth, investing became more about capital preservation rather than maximum net worth growth. I didn't want to lose what I had spent 13 years building.

Paying a $10,000 mortgage application fee and then getting a financial lobotomy to qualify was no longer appealing. By paying cash, I dramatically simplified the home-buying process, which also reduced stress.

In addition, you don't need to pay for home insurance if you pay all cash for a home. Home insurance can costs thousands a year and add up over time. In my 20+ years of homeownership, I've not once had to file a home insurance claim. As a result, over $100,000 in home insurance premiums I paid was wasted.

Plusses And Minuses Of Paying All Cash For A Home

Although the percentage of homebuyers pay all cash is growing, there are also some downsides to paying all cash for a home.

I may not grow my net worth as fast as I could have had I purchased with a mortgage, but I'm OK with that. I've got too much responsibility with a family to be chasing fortunes I don't need.

In addition, I put myself in greater financial risk by having much less liquidity. If I need to come up with some cash to pay for an emergency, I will be forced to sell other assets.

There’s one final benefit to paying cash for a home I didn’t think about until after re-reading this post. That is saving myself from myself. By locking up cash in my new primary residence, I prevent myself from doing something irresponsible with the money. Hooray!

Real estate is a real asset. As a result, real estate will likely last long after we're gone. For those of us who want to make our wealth last, real estate is my favorite asset class to build and maintain our wealth.

Recommendations

If you want to dollar-cost average into the housing market, check out Fundrise. Fundrise manages around $3 billion for over 350,000 investors investing in the Sunbelt region where valuations are lower and yields are higher. We're past the bottom of the real estate cycle and the investment minimum at Fundrise is only $10.

Financial Samurai is a six-figure investor in Fundrise funds and Fundrise is a sponsor of Financial Samurai. I've invested $300,000+ in Fundrise to diversify into real estate and venture capital.

For more nuanced personal finance content, join 60,000+ others and sign up for the free Financial Samurai newsletter. Financial Samurai is one of the largest independently-owned personal finance sites that started in 2009. The Percentage Of Homebuyers Who Pay Cash And Why They Do is a Financial Samurai original post. All rights reserved.

What an inspiring, touching read! I paid for my 2022 3 bed, 2.5 bath townhouse with HOA in cash in Fairburn, GA 30 min south of Atlanta fully and don’t have to worry of stinkin debt…yay! Happy to hear any tips from people. Proud homeowner here who prays all goes well with home till next few decades.

Congrats! You’ll enjoy this post: the intricate psychology of paying all cash for a home.

I’ve always paid cash, raised by selling appreciated stocks, mostly mutual funds. Income hasn’t been high enough for a tax liability, so there are no tax returns for lenders, even though credit ratings and debt to income ratios are better than many successful mortgage applicants. Also an irrevocable trust, due to the settlor’s death, and Florida land trusts, account for all ownership entities, which breaks many deals. Difficult and expensive insurance in Florida is why I’m in year 40 without it, but lenders don’t care, even though a complete destruction of a home would still yield a 20% loan to value, first position, just on the lot, for a $25k h-e-l-o-c. Underwriters check boxes, and can’t understand, or won’t submit, highly secure loans. A hard money lender understands, but asks for 25% closing costs. New to me is a factoring loan based on future rent for the income property, but proposed interest rates are about 14%.

So I’ll plod along with a $1 million free and clear portfolio, trying to borrow $25k, to pay property taxes and repair leaking roofs before the Florida rainy season begins in two or three months.

By the way, we haven’t gotten the nationally anticipated price pullback in the past year in close to the beach Florida homes. We’re still generally within 3% of all time highs from the spring of 2022.

Wow, not a lot of posts on this topic. Guess jealous Janice can’t pay a house in cash. Interesting to see the chart of the % of people who do buy houses in cash. Guess not too many people who read you want to buy houses in cash. Seems like they’re mostly interested in your stock tips. I have my money in Fidelity, hate stocks, and barely look at them. My son can inherit that.

I bought my house in cash in 2018 when I moved to PA because I could after selling my overpriced Old Town house, which I paid off early at 14 yrs. I moved from VA because I wanted the big house for cheap in a nice safe area with good school district, beautiful scenery & nature, and good health care. My house in Alexandria got broken into, packages were stolen, and the school district was bad. I didn’t want my son to go to private school and possibly be molested by a priest.

Now we live in a neighborhood of my dreams. It is peaceful and I don’t need a gun. Looks like it could be Mulholland Dr in LA. Gorgeous and safe without wildfire risks so my insurance is dirt cheap. My neighbors are executives, a local news anchor, my husband’s surgeon, bank VP, Harvard grads, lawyers, etc. I did not have these type of neighbors in VA, only CIA, lawyers, NASA. These people here paid so cheap for their homes that they can afford the G Wagons, Lamborghinis, Maseratis. You could get a mansion that looks like the one in Dynasty for $1.5 million. When I walk my dog it’s like I’m in a movie scene. It’s so gorgeous here. The bad thing about living here is the overpriced remodeling estimates. These contractors think we’re all rich.

Buying a house in full is awesome. We also don’t pay property taxes because husband gets VA benefits. Therefore,my highest expense house wise is the internet/cable bill. I don’t have a fancy spreadsheet or budget like you do, but I never worry about bills. Life with no mortgage in a gorgeous area is a dream. I feel sorry for the people who can not afford the American Dream or who live check to check. When I was a pharmacist, I never lived check to check but I spent a lot. I’m saving more money now than I did when I was working because there is no mortgage. No one in our family or relatives know anything about our true assets. They just look confused when I say I choose not to work. It’s better for people to not know. I could get kidnapped or robbed.

Sam, great post as always. It left me wondering at what net worth level is it smart to pay cash for a $2M+ home on the coasts (think SF or NYC metro or Boston). My guess is north of $10M which would put one in the top 1% wealth in the U.S. so out of reach for 99% and probably 98% of your readera. My assumption is that $2M is about right to live in a nicer neighborhood in a nice but not extravagant home that has modern updates for family of four. All cash in these areas of the country which are economic hubs would be a stretch for most with net worth below $10M. Would you agree?

The house is less than 20% of what our portfolio is currently worth and we have enough passive income that we won’t need to draw on the portfolio when we retire. Owning the house outright is just one less thing to worry about and the (relative) peace of mind seems a worthwhile swap for the opportunity cost of not pulling out the equity and investing it, especially considering the hassles of the first and the concerns of the second.

Yes I paid cash for my condo because at the time, it was the only way to actually buy a low price property in 2016 in the Bay Area. I had to compete with seven other all cash offers, as is sale, no contingencies, 10 days to close which came in hours after the listing posted. No way a seller is going to wait for financing to come through. I didn’t go see the property until after I bought it lol. People thought I was crazy but obviously that was the only alternative. It worked out just fine I’m still living here in 2023. It was a fantastic purchase.

Here is another angle to consider- Owning a home with no mortgage allows me and my wife, as retirees, to draw less income from our investments, which lowers our taxes. We will convert the maximum in the tax bracket to Roth each year- by the time RMD’s kick in we will hopefully have spent/ converted all of our Tax defered accounts.

Which bracket are you maxing out to the top of? 12%?

Being a dividend investor with 6 figures a year coming from there, it would be deleterious to give up that yearly income. However, I do agree with a certain net worth your money becomes more liquid especially if you have a good portion in “Magnificent 7” type stocks. Those are very little income for me but provide great growth and that is where I would “pinch” the gains for an all cash deal! Great article…

Seems a decent portion of the increase might be from the explosion in businesses advertising to buy houses as is with quick settlement. This is a popular option for kids wanting to unload the homes of their decreased Boomer parents. As in all things, as Boomers have aged thru the economy, what happens to them causes waves.

One of these low-ball investors named their company “probate real estate.” The average discount to fair market value seems to be 25% to 30%.

I didn’t realize that cash purchases have been on the rise recently. Your reasons all make clear sense though. I wish I had enough cash to buy my current home in the past, but things have worked out ok. My mortgage is almost paid off thankfully. I can’t wait to be rid of that.

I can see how it might be a tough decision to pay cash and give up dividend or interest income on such a large dollar amount. But personally I think I’d prefer having my equity in a house and not have to worry about how the stock market is treating my money or remembering to reinvest expired fixed income investments. Those are still fairly simple “problems” to have though. Anyway, thanks for writing!

paid all cash when we moved in 2021. love it! no mortgage hassle/cost. no payments. got house slightly cheaper than listing and other bidders. no regrets about not putting money elsewhere! highly recommend to all and definitely think benefits outweigh opportunity loss.

Hi Sam, great article and interesting and somewhat surprising supporting data. I’m wondering what your opinion is on maintaining homeowners insurance on paid off properties? Perhaps if on the coast where hurricanes are an issue e.g., Florida it still makes sense, but not sure about most areas where natural disasters are low risk.

Good question! Given it’s such a big investment, I’d still get home insurance, at least actual cash value home insurance in case disaster strikes.

See the two types:

https://www.financialsamurai.com/replacement-cost-value-versus-actual-cash-value-home-insurance/

Should clarify you need to insure the building’s value. No need to insure the value of the land baked into the house’s market value.

It will be interesting to see if the insurance company can let you just focus on the building insurance.

Here is the post: Home Insurance Needs For Paid Off Properties

Made an all cash offer in 2021 but ultimately my banker made the process so easy – and rate was so cheap – that I ended up getting a 10y I/O

I would absolutely do all cash offer – and will likely do such when I buy a place over the next 1-2 years as a second home.

Hi Sam. We have not paid cash for a house, but the last house we bought in 2015 we got a 10 year note and paid it off in 3.5 years. I know a lot of people would say we were dumb b/c interest rates were so low then, but we don’t care. We wanted to be debt free before we retired, and we achieved our goal. It felt so good to write that last check. Congratulations to you and your wife for buying your last 2 houses with cash. I think that is a wonderful thing and am happy for you.

Congrats! Feels good right? I’ve never regretted paying off a mortgage and I don’t regret paying for my 2019 fixer in cash. The price was good and the cash flow is solid.

Not having to deal with a bank is nice.