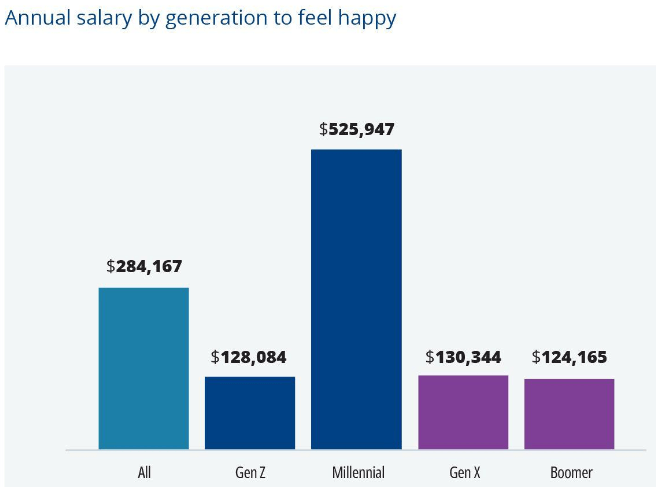

Empower surveyed 2,304 U.S. adults about financial happiness. And one of the most fascinating data points from the survey was that Millennials need to earn $525,000 a year to feel happy!

Obviously, this is just one survey that doesn't reflect all ~73 million Millennials born between 1981 – 1996. However, the income figure needed to be happy by them is still worth noting.

Although $525,000 isn't a top 1% income ($670,000+ is in 2025), it's a top 3% income. And if you need to earn more than 97% of the population to be happy, you might always be sad for the rest of your life!

The income figure across all age groups needed to be happy is $284,167 per year to be happy. Men say they need to earn $381,000 a year while women say they are happy with a much lower income of $183,000. Gen Z $128,000, Gen X $130,000, and Boomers $124,000, are much more realistic about their income needs for happiness.

Where did these surveyed Millennials come up with this $525,000 annual income figure? I think I know the answer.

Struggling To Keep Up On $500,000 A Year

Back in 2015, I wrote a viral post called Scraping By On $500,000 A Year: Why It's So Hard To Escape The Rat Race. The post has been read or seen by just about everybody who is a personal finance enthusiast. We're talking millions of views.

My goal for the post was to showcase how high-income households can often struggle to save for retirement due to lavish lifestyles, high tax rates, high housing costs, and the perceived need to keep up with the Joneses.

Back when I started Financial Samurai in 2009, most personal finance bloggers didn't live in expensive coastal cities like New York or San Francisco. Most still don't. Therefore, I thought it would be worthwhile to provide insights into what potentially half the American population faces.

If you read the 600+ comments, you know the post generated a lot of backlash from readers who live on much less but save much more. They couldn't believe how ridiculous some of the budget line items were. Most of the disgruntled commenters didn't live in an expensive city. Nor did they have children.

However, eight years later, the backlash has died down because more people have realized the veracity of the post.

Raising children in a big city is expensive and energy-sapping. Tuition and housing costs have soared since 2015. Although the top federal marginal tax rate has declined from 39.6% to 37%, that's still a lot, especially once you add on state taxes, city taxes, and FICA taxes.

Dear Millennials, My Bad For Making You Anxious!

My $500K post first created anxiety in readers because it made them fearful that what they are currently making might not be enough to retire comfortably. It doesn't matter how much you make, you will never get ahead financially if you don't control your spending and invest wisely.

My theory is that the post continues to be widely read and has created an expectation in the Millennial generation's minds that earning $500,000+ a year is necessary to be happy.

While I tried to make amends with a new post that incorporated a more frugal budget, A $500,000 Redo: How One Couple Got Their Mojo Back, but by then, it was too late. It seems it wasn't the high spending readers were mad about. Rather, it was their fixation on the $500,000 household income figure that was much harder to achieve.

My bad folks!

I hope you realize by now you don't need to earn $500,000+ to be happy. You also don't need generational wealth to raise a family either.

Instead, what you need is to earn enough to cover your basic living expenses while knowing that you are making financial progress in growing your net worth. Progress = happiness!

Here are the most important factors for financial happiness according to the survey.

Other Reasons For The Huge Income Requirement By Millennials

Why do millennials feel they need to earn 4X more money than Gen Xers ($130,000), Gen Zers ($128,000), and Boomers ($124,000) to feel happy? Besides Financial Samurai creating a warped sense of reality since 2015, here are some other reasons.

1) Perpetual economic crises

Millennials began their careers during the 2008 global financial crisis that resulted in millions of layoffs, a 50% decline in the stock market, and a 30% decline in the real estate market. Graduating during the deepest recession of our lifetimes can cause permanent damage to one's earnings and career potential.

Then the pandemic came along in 2020 for two-to-three years followed by the highest inflation figures seen in decades. Now there is war in Ukraine/Russia and growing conflict in the Middle East. As a result, it's only natural for millennials to feel they need to earn far more than other generations to be happy.

2) Ever-rising housing costs

Once you can fix your housing costs, life gets much easier. Since 2009, I have recommended readers get neutral real estate by owning their primary residence. By owning your primary residence, you get to benefit from housing inflation. By renting, you are hurt by housing inflation due to ever-rising rents and prices.

Those who disagree believe they will be able to consistently “save and invest the difference” in stocks and other risk assets to keep up or outperform. Unfortunately, due to economic leakage and human nature, the vast majority of people are incapable of consistently doing so. Buying a house with a mortgage acts as a forced savings account.

Bidding wars are back, even with high mortgage rates. As a result, those who don't own their primary residence are getting even farther behind. Hence, if you can, try to get neutral housing inflation by owning your home.

If you can't afford to buy a home yet, invest in private real estate so you are hedged. My favorite private real estate investment platform is Fundrise, where you can dollar-cost average with as little as $10. Fundrise invests in residential and industrial real estate, predominantly in the Sunbelt region, where valuations are lower and rental yields tend to be higher.

Financial Samurai is a six-figure investor in Fundrise funds and Fundrise is a long-time sponsor of Financial Samurai as our outlook on real estate is aligned.

An opportunity to buy real estate today

There are essentially two-to-five-year windows of opportunity to buy real estate at more affordable prices every seven-to-ten years. We're in this window of opportunity now, which I think will end in 2025.

If you don't get neutral real estate during this window, I'm pretty sure that in 2035, if you end up taking this survey then, you will cite housing costs as one of your key stressors.

If you can't afford to buy a house today, then you can invest in real estate ETFs, public REITs, or private real estate funds as a way to get neutral the market. While saving for a down payment, if the real estate market rebounds aggressively, you won't fall as far behind.

Roughly 42% of homeowners don't have a mortgage and 80% of mortgage borrowers have a mortgage rate below 5%. Rising rates, although bad for home prices, are not squeezing existing homeowners as much as some might think.

Both Millennial and Gen Z survey respondents say they stress most about high housing costs (67%, 46%) and rising rent prices (62%, 38%).

3) Childcare costs are out of control

As a father of two young children, because I own my primary residence, my greatest concern is the cost of childcare. First, there's the cost of diapers, strollers, food, clothing, medicines, and healthcare costs. Then there's the cost of paying someone to watch your child if you have to work or need a break. Then there's private grade school tuition (if applicable) and college tuition costs.

I've already estimated by the year 2035, the all-in cost of a four-year private university will be about $750,000 per child. I can hope my child gets a scholarship, attends public college, or goes to community college for free. But I can't count on it and neither should you.

Feeling the heat of paying for college tuition

The challenge of paying for my children's education is one of the reasons why I feel I should go back to work once my daughter goes to preschool full time. Not only will I have to pay for her preschool tuition, but I might also have to pay even more than $750,000 for her college in 15 years!

Alas, my master plan is to encourage them to go to community college instead. I've heard a lot of good feedback from readers who went to community college so I don't see why my kids can't go the same route as well and do fine.

If you want one parent to stay at home and raise your children, I can also see why Millennials think they need to earn over $500,000 to be happy.

Why Boomers And Gen Xers Feel More Financially Secure

Boomers ($124,000) and Gen Xers ($130,000) need lower income levels to be happy because they are more financially secure. They've simply had more time to save, invest, and benefit from a bull market.

When I was 38 years old and wrote the post about scraping by on $500,000 a year, a part of me was wondering if that's how much I really need to feel secure and happy. I didn't have kids yet, so I was carefully planning for when I did. The responsibility to raise children in an expensive city seemed daunting.

As a 46-year-old Gen Xer with two kids, I'm wiser now. I clearly realize earning $500,000 is not necessary for happiness. For a family of four, $300,000 should be good enough! I know some of you are rolling your eyes, but at least that's 40% lower than what these Millennials expect they need to earn to be happy.

I've written follow-on articles such as, Don't Make $400,000+ A Year, Look How Miserable GS Analysts Are, to make my claim explicit. I'd rather earn $100,000 in passive income or $150,000 at a job I love than make $500,000 at a job I hate.

Given Boomers and Gen Xers have had a longer time to save and invest, of course we don't need as high of an income to feel happy. Our net worths are much greater than the average net worth of a Millennial. Millennials only hold less than 5% of the total wealth.

Net Worths Required To Be Happy Don’t Make Sense

What I also find interesting about the survey is the net worth required by generation to be happy. The overall net worth desired is $1.2 million among all age groups. $1.2 million is close to the average American household net worth of $1.06 million according to the latest Consumer Finance Survey.

However, for Millennials, the net worth desired is only $1.7 million. I say “only” because $1.7 million is only 3.23X greater than the $525,000 in annual income required to be happy for Millennials.

If you are to follow my net worth target by age guide, a 35-40-year-old Millennial in 2023 should aim to have a net worth equal to 5X-10X their average annual income. If you want to achieve financial happiness in retirement, you must methodically grow your net worth over time.

Hence, the Millennials in this survey who desire $525,000 in annual income should also strive to have an ideal net worth of $2,625,500 to $5,250,000. But because Millennials say they only need a net worth of $1.7 million to be happy, this implies Millennials aren't thinking properly about their finances.

Or maybe, Millennials have adopted the spending habits of the couple in my scraping by on $500K post and plan to spend almost everything they earn. A double delusion that can only lead to unhappiness!

Having A Financial Plan Brings About Happiness

No matter what your ideal income or net worth is to be happy, 73% of the survey respondents believe having a financial plan can contribute by bringing a sense of security. I agree with this.

Think about how much calmer you feel when you have a list of grocery items when entering the grocery store. Compare this with the constant did I forget something feeling if you didn't have a list.

Having a financial plan for retirement brings a sense of calm. When you know where your money is going and have a purpose for every dollar you earn and save, you will feel happier.

I've used Empower to track my net worth since 2012. As a result, I've felt much more in control of my finances. I got rid of expensive active mutual funds for index funds. I've also mapped out my expected retirement cash flow with its Retirement Planning tool.

Create a plan on your own with the help of technology or seek out a fee-only financial planner. There is no rewind button in life. Hence, do your best to get your money right in the first place.

If you have over $100,000 in investable assets—whether in savings, taxable brokerage accounts, 401(k)s, or IRAs—you can sign up for a FREE financial check-up from a professional at Empower. It’s a no-obligation opportunity to have a seasoned advisor—someone who analyzes portfolios for a living—take a fresh look at your finances.

A professional review can help you identify hidden fees, inefficient allocations, or missed opportunities to grow and protect your wealth. More importantly, it can give you the clarity and confidence to know whether your current savings and investment strategy aligns with your long-term financial goals.

Sample retirement planning calculator results

This offer is provided by Financial Samurai (“Promoter”), who has a referral agreement with Empower Advisory Group, LLC (“EAG”).

Diversify Into High-Quality Private Real Estate

Consider Fundrise, a platform that allows you to 100% passively invest in residential and industrial real estate. With around $3 billion in private real estate assets under management, Fundrise focuses on properties in the Sunbelt region, where valuations are lower, and yields tend to be higher.

I’ve personally invested over $500,000 in Fundrise funds, and they’ve been a trusted partner and long-time sponsor of Financial Samurai. With a $10 investment minimum, diversifying your portfolio has never been easier.

Reader Questions And Suggestions

Why do you think Millennials think they need to earn way more money than other generations to feel happy? What do you think is the ideal income to be happy? What about the ideal net worth?

Listen and subscribe to The Financial Samurai podcast on Apple or Spotify. I interview experts in their respective fields and discuss some of the most interesting topics on this site. Please share, rate, and review!

For more nuanced personal finance content, join 60,000+ others and sign up for the free Financial Samurai newsletter and posts via e-mail. Financial Samurai is one of the largest independently-owned personal finance sites that started in 2009.

Or maybe millennials need to dig themselves out of student debt for a degree that left them worse off than if they never went to college. If you enter the workforce with a net worth of -300k or more, you definitely need to earn more to get to that 1.7 million.

Sure, that’s a valid point. Thanks

This assumes that Millenials aren’t aware of the fact that their assets would only be 3.5x greater than the annual income.

Maybe they just want to work for fewer years.

My take away….Only Millenials turned to the interent to get the answer to the question, “How much income do you need to be happy?”

Every other group got up, went to school, got a job, earned, and then spent, and then made an informed answer based on actual experience.

In my experience, Millenials as a group, know everything, and have actually done nothing.

And based on recent standardized test scores, I awould not trust a Millenial to tell you anything about mathematics.

A useless group as a whole, perhaps someday they will grow up and move out of Mommy’s basement and into the real world, until then, their opinions offer nothing.

Where do you think your contempt is coming from? There are around 72 million millennials.

A typical boomer opinion that maligns a whole generation and offers nothing. Based on your gross generalizations, I wouldn’t trust anything you have to say.

Let’s use Sam as an example:

1. Makes top 10% income PASSIVELY

2. Stay at home dad

3. Lives in SF

Despite the above, Sam only has 2 children below replacement children. If everyone in the whole world did this, given enough time, humans would go extinct.

While this could be a personal choice, Sam makes comments such as the need to send kids to community college which indicates money is a factor. One could easily conclude that someone similar to Sam living in a major city would actually need to make around 500k to have above replacement levels kids.

Could be! There’s just one problem with your hypothesis, I am telling you straight up. I am happy earning about $350,000 a year. That’s good enough to take care of a family of four.

How many children do you have and how much do you think you need to earn to be happy?

I’d love to know more about you and other reader’s stories.

Thx

What level of income would be good enough to send 4 children to private university for college vs community college?

I think 100k is enough to be happy (single). However, sending 4 kids to college (not community) would be 400k+ in the USA.

I’ll also add Catholic priests are a good baseline. In the Northeast a priest makes ~50k. Free housing at 2k/month post tax is worth another 30k. That’s 80k for a single man dedicated to a life of service. Therefore I’m not really suprised by the millennials numbers anymore

Interesting point! I’d add that, like teachers and social workers, that’s also a job that involves people who put in massive unpaid hours – and churches expect it because they are celibate and don’t have to attend their kids’ games, etc.

Similar to another comment: college costs can come down a lot with dedication and planning. Aside from being academically gifted or an athlete or band/music skills, etc. to get a scholarship, there are ways to make it cheaper.

My nieces and nephews have each graduated from high school with either AP credits and/or taking community college classes while in high school. Lots of schools are allowing this now. My niece might actually graduate with her associates degree from community college prior to receiving her high school diploma due to her credits. She’s taken advantage of sprint sessions between college semesters like in winter break and summer classes from community college as well as taking classes during the school year. I think because the high school has a relationship with the college the credit hours are something like $75/each rather than the $500-900/credit hour (or more) for most college credits.

Anyway something to think about while budgeting the college planning.

As far as the the $500k I don’t think it’s a must, but if you are asking people on a survey what kind of life they would want to have, that probably hits the mark. An interesting question would have been asking if they are happy currently somewhere in the survey and what their current income was. Like other posters I’d imagine most people are happy with what they have – but money does ease stress so long as you have good health with it.

My W2 income combined with wife is close to $500k now and growing. Thinking about it at times, I’m not sure if I’m happier now or years back when we had half that. Our house is larger and we have a lot of nice things, but sometimes I look around and just see stuff. Our kids sure have fun, and we have to focus to keep them grounded, just because we can buy something doesn’t mean we will.

Hey Sam,

One additional selling point for local community colleges: I was “home schooled” during high school and was able to obtain dual credits for both high school and college—while attending a local community college. I started taking college classes at the age of 15–which counted for both high school and college credits. By the time I graduated high school, I was already considered a junior in college (over 63 hours completed). I was able to simply transfer to my college of choice as a junior and never had to take the SAT / ACT.

If I’m paying for my children’s college, I intend to implement the same strategy. It also gives them peace of mind to take a gap year travel & explore—and they’ll still be 1 year ahead of everyone else!

Cheers,

Payton Reid

Sam,

This country simply does not have enough housing, both Republican and Democratic states have issues with homelessness currently that haven’t existed since the 1920s and 30s, back in those times it was farmland that was causing issues for people. Old farmers in the 1920s and 30s refused to open their lands for development and that created land speculation and bubbles that ultimately burst in the Great Depression. We can’t be a healthy country if land is not available for the next generations.

There are simple fixes, but the first one is simple. Stop treating houses as investments and treat like cars instead that depreciate over time. This will cause investment dollars to flow into new construction and lower the value of existing homes. A house is a place to live, not a savings account. When I hear politicians talk about housing as an investment it makes me sick. Houses are an expense and should be treated as such both in tax code and in terms of the types of houses we build. This nation needs millions of small houses for young families or the future for millennials and Gen Z will be very dark indeed.

We need to go back to building houses in the way they were constructed in the 1950s. This country built millions of houses for men returning from World War II and we can do it again if we want. The houses were small, but were adequate for young families and because housing was cheap people had money for retirement savings and buying other luxuries as well. The era of big wasteful houses needs to end and end soon.

Maybe there would be enough housing if there weren’t 15-20 million illegals occupying current housing stock.

I have seen where the immigrants you speak of live and they aren’t living in houses that is for sure, unless you count the rich immigrants from Asia and Europe in the mix, but plenty of Americans move to Europe as well. People in my state have to move to make room for a freeway and they can’t afford a new house in another neighborhood so they are moving to Europe for affordable housing and their family has been in America for over 100 years.

Bottom line in my state in the 1990s you could buy a house with a part time job. My brother did it and so did my uncle. Now there aren’t affordable houses for sell anywhere and they aren’t really building a lot more of them. What they are building is tons of cheap apartments. I can rent an apartment for under $1,000 a month, but a house will cost $5,000 a month in my city at current rates. Again illegal immigrants are not buying houses. That is not thing where I live.

But since we are talking about immigrants maybe this country could build houses for them too! We have plenty of money and space, but houses I guess are for the super rich these days, ordinary folks I guess will have to pay a landlord until the day they die.

Yikes. Worst comment I’ve seen on an article here in a long time. Do better. Be better.

With not enough housing, it’s actually important to invest in more Housing and Land for your family.

Real estate is the one asset that is limited.

Great comment Jake and one that I agree with. I’d be curious to hear thoughts from Sam and others, but I often worry far more about my two young kids being able to afford a house one day than I do about them being able to afford college.

My wife and I own 40+ acres with a home, and have subdivided the land into two lots and are in the process of building a new home. One of the biggest reasons for doing so is because we have two young boys that will eventually need a place to live, and there’s nothing around here for under $750K. So while we will rent out one of the homes until they’re older, it eventually will become a housing option for our sons if they choose to stay in this area.

I recommend folks buy one property per family member. Not only will they act as an investment, they act as a place to live for each person in the future if needed.

Property is a great hedge against a lot of things.

Totally agree Will. Your primary residence is not an investment. It provides negative cash flow, and only if you sell it decades from now will you make any money off of it. Even then you have to pay hefty commissions to do so, and still have to pay to live somewhere else. A house is a luxury purchase and a place to live.

Just don’t forget the benefit is the rent savings, which tends to go up with inflation, if not faster. While a mortgage or all-cash payment better fixes your living expenses.

Although renters say they will save and invest the difference, the 40X greater net worth differential between owners and renters says a lot. Not 4X, but 40X differential.

You are right Sam that it fixes a portion of your housing costs. But many aspects of your ongoing housing costs still do increase – your property taxes, insurance, repairs, maintenance and renovation costs will certainly continue to increase with inflation.

The 40x figure is highly, highly misleading. Correlation does not equal causation. Many people who never own homes do not own them because they never made enough money to afford it. If you factor in the difference in income for those cohorts, it would be nowhere near 40x.

Anybody who tells you the net worth you need to retire comfortably is a factor of your average income is either an idiot, or trying to sell you an investment product. We are all to believe that our expenses in retirement will continue to include the amount we’re saving for retirement during our careers in perpetuity.

If your target should be a multiple of anything at all, choose the amount you spend AFTER taxes and savings and mortgage/debt payments. (You’re going to pay off your debts before retirement, right?)

Millennials thinking they would like a $500k+ salary are thinking about how much money they need to service their debts and how much disposable income that they would like to have after meeting their savings targets. They don’t need to increase their savings targets along with their earnings. If they did, there would be no amount that would ever satisfy them.

Ouch, unkind words, but that’s OK since this is the internet.

The problem with using a multiple of expenses as a net worth target is that you can cheat your way to Financial independence by just slashing your costs to the bare bones.

But by using an average income multiple, it forces you to be disciplined as you make more money, which most people do overtime with experience and expertise.

Plenty of people make more and then end up spending more. And then in 20 years, they wonder why their net worth isn’t larger.

Given your strong feelings, I love to know more about your background and what stage are you at in your financial independence journey? What multiple did you set on if you achieve financial independence. Thanks.

I’m not financially independent and have been working for 12 years.

No idea who these people are. “Needing” 500k a year is psychotic relationship to money. Is it needing or wanting? Of course they ideally want to make more – who doesn’t? Who doesn’t want to travel world and buy what we want without a care. But my sense is they are happy with much less than 500k a year.

I am in a HCOL area (NVA) and employ many millennial engineers who make between 75-150k and are quite content raising families and none are married to lawyers or CEOs – so combined not making more that 200-300k. I make it a point to at least get to know my employees beyond a straight superficial level. And some are only single income. It is a very competitive career, so if they were very unhappy making what they are making they could jump around and boost their income, but few do.

Money and happiness is a tricky thing to measure.

Sam, great post. I liked your post on “Scraping by on 500,000k” I’ve met and are friends with people in NYC, Philly, and DC who make this and the example budget you came up fits them very closely. They are power couples for sure and stressed out with two-three kids. Their income is their spending limit. They are UAWs or under accumulators of wealth. (borrowing from a well known finance book) They tell me about it haha. As a millennial (age 38 wife 36) I don’t think 500k plus is needed for max happiness. Your spot on with progress = happiness. Homeownership certainly helps with seeing and feeling progress along with steady automatic investing every two weeks. When we wanted to buy a house we got out of consumer debt and I got a second job, slashed our spending, and we saved as aggressively as possible ~40% of our income at the time; then bought in 2018. So glad we made the effort. Other friends are living the the rat race or on the hedonic treadmill and it’s pretty obvious they are less happy in life. Again great post, cheers.

Millennials are born between 1981 and 1996 (27-42 years old in 2023). This is a huge range and doesn’t put everyone in the same boat.

Older millennials, such as myself, had a rare opportunity to get ahead. Myself and many of my peers purchased homes during the great recession while still in our later 20s. During the great bull run came an opportunity to upgrade homes on one or two occasions, and also increased affordability with the downward trend of mortgage interest rates.

I can understand those that had student loans, job sector instability, or other situations didn’t have it as easy. For me, however, I often look back and just feel very lucky, because I believe I am, with dumb luck timing. We get by happily in a very HCOL area on just my normal professional salary.

Yes, the Millennial generation is large and diverse. Congrats on being able to buy a house during the GFC. That was an opportunity of a lifetime! Not sure we’ll ever get that opportunity again.

Didn’t realize the Millennial age creeped past 1980. I always thought 1980 was the cutoff.

“I’d rather earn $100,000 in passive income or $150,000 at a job I love than make $500,000 at a job I hate.”

Couldn’t agree more.

IMO, I think it would be best to “grin and bear it” for X years at the $500K job you hate and then transfer to a lesser paying job that you enjoy much more. As long as you are strategic about it, those years at the high paying job will set up you for high NW and early retirement. Being resilient and tolerating a certain amount of professional work discomfort for long term financial security is a lost art for most in society. An added benefit to slaving away at the high paying job that you hate is that once you leave, you will be eternally grateful you are no longer at that job and that sense of relativity you gain will help keep you happy for years to come. That was Sam’s path and to a certain extent, mine as well.

In what world is $150K per year for job you love somehow a compromise?! I have a doctorate and still struggle to make $60K per year as adjunct faculty at several different universities (no benefits at any of them, either!). My husband earns a little over $110K per year, and that’s after almost 20 years in his field. Doubling our current household income for doing jobs that we (mostly) enjoy sure sounds like a nice compromise to me….

First year college graduates, working in technology, finance, consulting, all make over $120,000 nowadays.

Millennial here. Living in a High-er cost of living area of the country.

We will probably come in at about $350K income this year. Have been working for a decade in our professions that is HH income. A $550K income is not needed to be happy but another $200k a year would no doubt lift off pressure.

Could guilt free do whatever you want during the year within reason and save even more each year.

With a family of 4 now a lot of the increase in income goes to daycare $4K a month. We live a good lifestyle currently though and have saved more then the average for our age so no complaints.

We for sure do not feel like we can leave our jobs anytime soon however…$550K a year would speed that up.

$350K is almost at the ideal taxable income level based on 2024 tax rates (~$380,000), so enjoy!

$525,000 is nice, but it often requires more work and more taxes. Nice to have, but not required.

A few factors in play. 1) dating now needs to be 6’+ with $300k for the average girl. 2) Entry level homes are half a million dollars in the midwest (unless you’re in a town of 8k where there’s no jobs). 3) student loans are six figures. 4) cars cost 50k. 5) inflation is at like 27% compared to pre pandemic. 6) we’re about to hit another great depression.

Hmm, think for item 1, that might be less than 1% of the male population.

High expectations, so life could be tough!

According to google napkin math:

14.5% of men are > 6′ tall in the USA.

27% of men age 30-49 are single.

A 35 year old man with a 300k income is in the top 2%.

2% * 14.5% * 27% = 0.08%.

About .08% of men who would fall into this range, or about one in 1,250.

Who said “single” was on their list?

So you’re saying they’ve got a chance!

But the funny thing is, there are plenty of men like that in NYC, LA, Boston, and San Francisco. So it’s surely higher than 1,250.

Certainly it’s higher in areas of the country with higher where the bulk of the $300k+ jobs exist.

In areas where those jobs don’t exist, probably closer to 1/5000

Raises hand, 6’2″, so I’m even more “special”

Well done. And are you also making over $300,000 and living the dream?

Some millennials are still carrying high student loan debts while also trying to save for their own kids college, paying for expensive day care while also helping their parents, and paying 8% interest on their mortgage for a house that was already too expensive. There are a lot of reasons that come to mind when I consider why many of my generational cohorts feel they need to make $500k to be happy.

I don’t think a single household is paying an 8% mortgage. That was a brief average for several weeks this year and we’re 0.7% below that average now. And nobody pays the average, funny enough, much lower.

But yes, without fixing housing, building wealth gets harder.

True. I know more than one millennial with floating rate HELOCs at over 8%. In both cases, they used the HELOCs for needed home improvements. As an older millennial, I don’t relate personally because I bought my first house during the Great Recession, traded up, and refinanced when rates were below 3%. But, I can see how younger millennials who have student loan debt and high childcare costs who entered the housing market later and who pitch in with their parents as we do for one set of ours need to gross $500,000, not to feel pinched. These things quickly add up in some parts of the country.

Great post as always Sam. To be clear, are the numbers ($525K = happy) per individual or per HH?

HH, which includes singles.

They’re crazy. I guess the Millennials are entering their prime earning years. They have to aim high. Also, the cost of housing is crazy for them. They feel like they need such a high income to afford a house. Lastly, I think high income Millennials are spending a lot. This generation highly value experience. They spend to enjoy life. Hence, the need for high income. Once they’re a bit older, they’ll probably get more realistic. Not many people can earn $500,000 per year.

I wonder if a few people didn’t just enter “$20M/yr” and skew the results. You usually see something like 2x current income as the hypothetical “wow, what a life changing salary that would be”, not 10x. You also don’t usually see this extreme of outlier behavior in polls around financial expectations between demographics. Given it’s one online-only survey I’d take the result with a pretty big grain of salt.

Maybe! And you’re right, it’s just one survey. But it’s an interesting one at that.

I love seeing massive differences between perception and reality and figuring out why.

This generation has grown up with 24/7 social media where everyone looks like a millionaire. So it shouldn’t be a surprise that they think half a million dollars a year is what they need to be happy. Because that’s what it looks like.

But the most interesting part of this post is the piece about only desiring $1.7 million in net worth compared to annual income of $525K. It says to me that the millennial generation is only worried about the here and now. I think there’s a mental aspect to it. Net worth is for retirement. Annual salary is for spending on things that allow you to keep up with the Joneses.

A high paying job creates a false sense of security and an inflated lifestyle. When you’re making a lot of money, you spend a lot of money. And the only way things get better is to make more money. It’s only after leaving a high paying job do you realize how excessive it was, and how happy you can be with less.

I’ve been amazed at how my view of money has changed since I stopped working five years ago. I have more net worth now (about 3 – 4x) than I did when I was working (I benefited from a company acquisition when I left), but without W2 income, every dollar spent is scrutinized in a way that it wasn’t before. I want to get the most value out of every dollar earned. It’s made me really appreciate what I have and how recklessly I spent when working.

I’ll just say one more thing. If life is too expensive on the coast, move somewhere else. A lot of what the coastal cities “offer” in happiness, isn’t really worth the investment. I know, I grew up in New York and lived in Los Angeles.

Cheers.

“But the most interesting part of this post is the piece about only desiring $1.7 million in net worth compared to annual income of $525K. It says to me that the millennial generation is only worried about the here and now. I think there’s a mental aspect to it. Net worth is for retirement. Annual salary is for spending on things that allow you to keep up with the Joneses.”

Yes, only $1.7 million was quite interesting to me as well. Maybe it’s a desire to YOLO all your income today for tomorrow is not guaranteed.

Or maybe there’s a disconnect due to a lack of financial education about the level worth needed to generate $525,000 into perpetuity ($13.125 million at a 4% rate of return).

Where do you live now? And why is it better than where you did live?

James, so true re the millennials living for here and now. My kids, besides maxing out their 401s, will not do anything else.

Well put James!

“It’s only after leaving a high paying job do you realize how excessive it was, and how happy you can be with less. I’ve been amazed at how my view of money has changed since I stopped working five years ago.”

I have exactly the same experience. Once you stop living of your salary and start living of your capital, the perspective fundamentally changes. You want to put as much money as possible to work, you scrutinize your expenses and realize what really makes you happy and what is just a ballast.

You certainly do have an influence on us Sam! And your insights and logic on the expensive costs of raising kids is spot on especially for those of us on the coasts. It can get out of control so quickly without intentional discipline to harness expenses. And yes even the cost of childcare, which is necessary to work since a lot of coastal families don’t have extended families locally to lean on for help, is super expensive.

And housing too. It’s no joke there are dozens and dozens and dozens of RVs on the rise in places like Lake Merced in SF because so many of the residents can’t afford anything else.

With economic uncertainty a new norm and job security out the window, we really have to make a conscious effort to avoid lifestyle creep, invest wisely, and proactively build passive income and net worth.

Quick reminder:

As a parent, you are not obligated to allow your children to go to a $750k all-in institution. You can say hey pal this is what we have saved or can cash flow. Here are your school options. Pick one and no I will not allow you to take out students loans.

Thank you,

Mgmt

Love it! If my kids don’t get straight As and a scholarship that brings the cost of college down to at most the cost of a top 20 public university, they ain’t going!

Community college and a grade school education with parental guidance rocks.