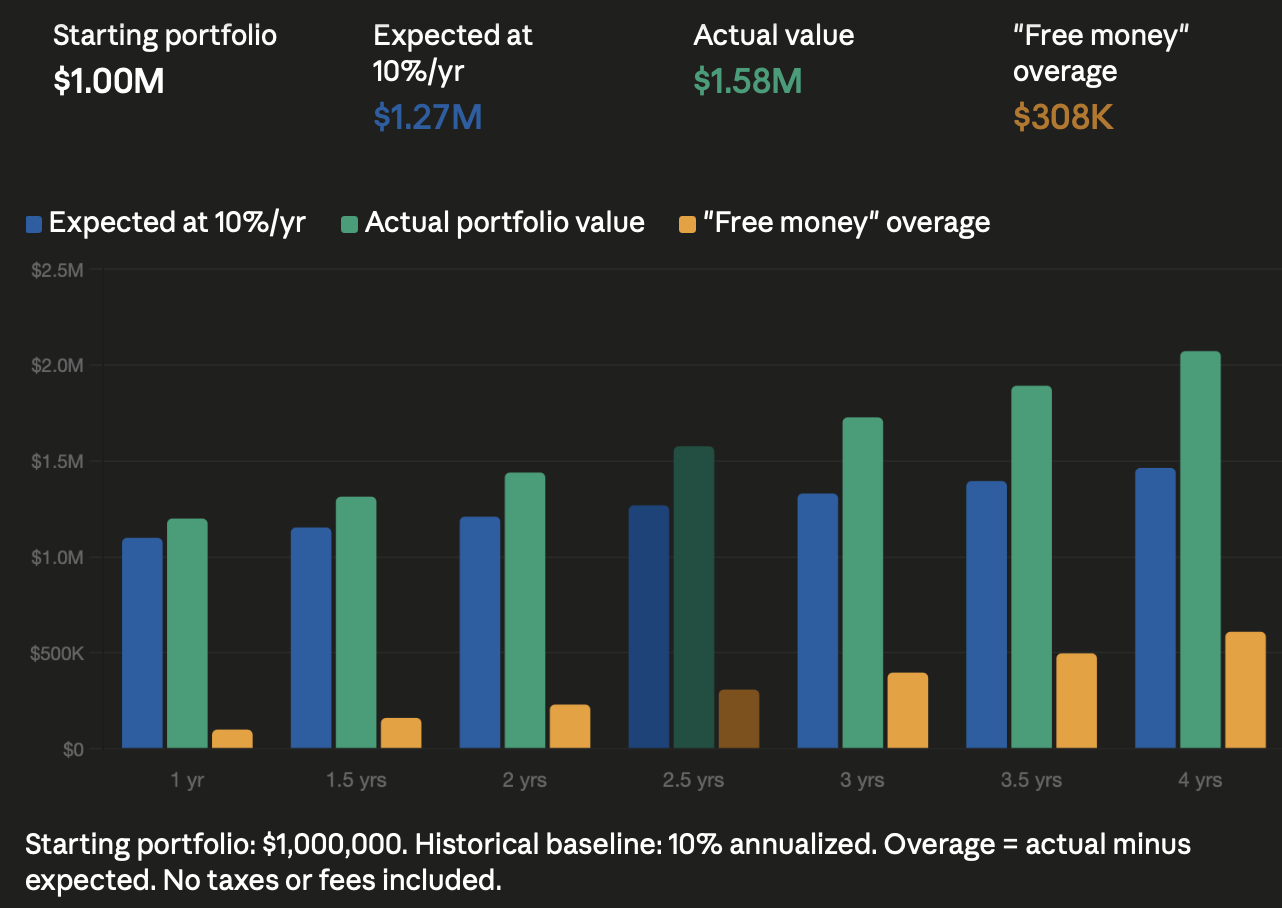

The S&P 500 is up roughly 100% over the past three and a half years. At its historical average annual return of about 10%, you'd expect it to be up closer to 40% over that same stretch. That's an “excess gain” of 60%. I view this excess like free money you find on the street with nobody around.

So why are so many people still grinding like it's 2021? You have five years less to live.

I get it. We're wired to keep pushing, keep saving, keep building, keep wanting more. When the inevitable bear market comes, it'd be nice to have an even bigger buffer.

But at some point, that discipline stops being a virtue and starts being a reflex. The harder you work past the point of necessity, the lower your return on effort. Time is the one asset that doesn't compound. You can always make more money. You cannot make more Sundays.

I want to challenge you to think about what these extraordinary gains actually mean for how you’re living your life. You don’t have to completely upend everything and FIRE like I did in 2012. But there’s a real chance you’re leaving a better lifestyle on the table in the pursuit of more you don’t truly need.

Who's Actually Benefiting From This Bull Market?

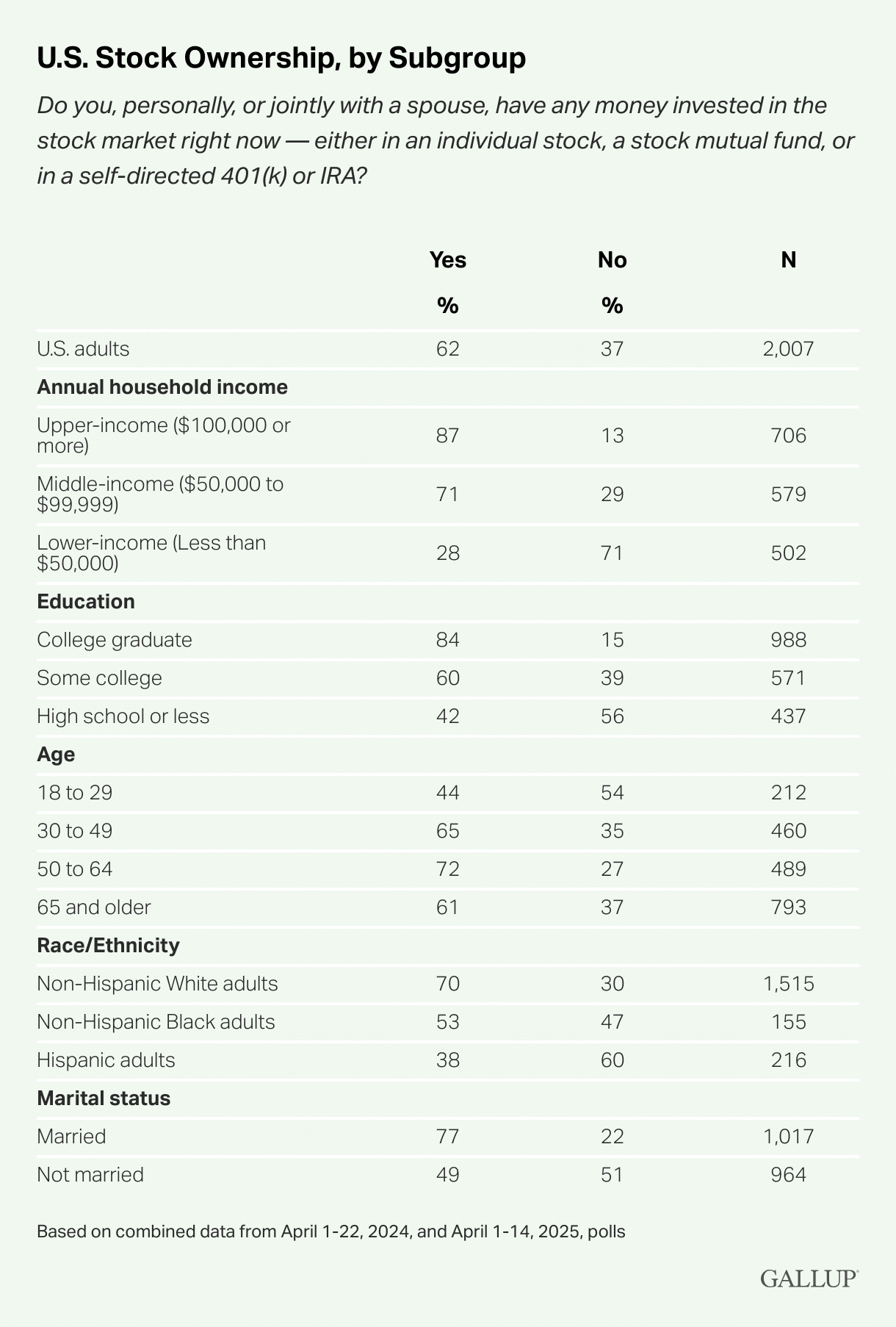

Before diving in, it's worth grounding the numbers. About 62% of Americans report owning stock in 2025, matching the 2024 reading, and the highest sustained level in nearly two decades.That sounds encouraging. But dig a little deeper and the picture gets more unequal.

The wealthiest 1% hold about 50% of all stocks, worth roughly $29 trillion. Expand that to the top 10% and they hold 87% of equities. The bottom 50% of Americans by net worth own just 1% of all stocks.

Stock ownership is highest among adults in households earning $100,000 or more (87%), college graduates (84%), and married adults (77%). I'm assuming that's most of you. Among those earning less than $50,000, ownership drops to just 28%.

The bull market of the past few years has been an extraordinary wealth-creation event , but it's been concentrated. If you're a regular Financial Samurai reader and newsletter subscriber, you're almost certainly in the portion of the population that's been a meaningful beneficiary.

The question is what you're actually doing with it.

The “Free Money” Math

At a 10% annual return over 3.5 years, a $500,000 portfolio grows to roughly $695,000, a gain of about $195,000. Instead, with a 100% total return, that same portfolio becomes $1,000,000.

That’s slightly over $300,000 in extra, above-expectation gains. Not because you worked harder. Not because you made brilliant stock picks. Just because you held.

This matters for how you think about your next year of your life. That excess return, roughly $150,000 per $500,000 invested at the most basic calculation, represents significant spending for most.

It also represents freedom bought cheaply by simply staying invested. And yet most people will let that number sit in a brokerage account and continue showing up Monday morning to a job they'd quietly quit if they felt they could afford to.

They can at least leave to do something more enjoyable, regardless of lower pay. They just haven't run the math yet.

Let's do it for a few different situations.

From $50,000 to $100,000: The Young Grinder

You started working at McDonald's at 16, saving and investing 80% of your paycheck while living at home. By 24, you had $50,000 in a taxable brokerage account, an impressive feat of discipline. Three and a half years later, the market has doubled it to $100,000.

You're now the associate manager making $60,000 a year. It's a real job, with real responsibility. But it's not the life you imagined.

At this stage, $100,000 isn't “retire early” money, but it's “bet on yourself” money. The historical 4% withdrawal rate gives you about $4,000 a year in passive income, which doesn't move the needle much on its own. But what it does is buy you courage.

Instead of grinding toward a $85,000-a-year management track, you go part-time and enroll in community college to study filmmaking. You write and direct short films. Maybe you become the next Sean Wang, whose semi-autobiographical indie film Didi premiered at Sundance. Maybe you don't.

But you gave yourself the shot, and your $100,000, quietly compounding in the background, gave you the cushion to try. Every year you wait, the gap between “who you are” and “who you want to be” gets a little harder to close.

The extra $30,000 in above-historical gains you just received didn't require anything from you. Use it to buy one year of going all-in on something you actually care about.

From $100,000 to $200,000: The Idealist Trapped in Consulting

You're 26, three years into a soul-draining job in management consulting. In your college application essay, you wrote about building a nonprofit to bring clean water to communities in Somalia. Unlike your classmates who virtue-signaled their way into elite schools and then straight into consulting, you actually went to Somalia and did the work.

But you got into Yale, partly on merit, partly because your grandfather's name is on a building, and the path of least resistance was consulting. The pay was good. The prestige of working at McKinsey was intoxicating. And now here you are, two years in, wondering how you got so far from who you were at 17.

Your portfolio has doubled from $100,000 to $200,000. At a 4% withdrawal rate, that's $8,000 a year, not enough to live on, but enough to cover modest expenses in a low-cost part of the world. Combined with grant funding and the nonprofit connections you still have, it's enough to go back.

You quit. You move. Your heart is full. And the $200,000 still growing in index funds acts as a permanent backstop, a financial floor that means you'll never truly be stuck again. (It also doesn't hurt that your parents set up a $5 million trust, but that's a separate essay.)

From $800,000 to $1,600,000: The Finance Lifer Ready to Escape

You're 30, with $300,000 in your 401(k) and $500,000 in a taxable account after some great bonuses and consistent frugal living. That's $800,000 total after eight years in finance. Not bad. Three and a half years later, you're sitting on $1,600,000.

Seven figures. A number that felt abstract at 22 now has your name on it.

But you hate the long hours. You hate the constant pressure. The most interesting thing you did last week was a pitch deck for a deal you don't actually believe in. So you raise your hand to get laid off, a move that, done right, gets you a severance package worth six months of salary while preserving your eligibility for unemployment benefits.

At 33, you decide it's not too late to reinvent yourself. You go back to school for an MBA at Berkeley. You take the job in China you passed on at 22, the one in business development that felt too risky at the time. Now, with $1,600,000 in assets compounding at 6% – 10% annually, you can afford to take a job for the experience rather than purely for the salary.

The “free money” in this scenario, the $500,000 – $600,000, above what historical returns would have generated isn't just a number. It's the psychological permission slip to walk away from something good but wrong, and toward something uncertain but right.

From $3,000,000 to $6,000,000: The Tech Burnout Who Keeps Delaying

Twenty years in tech. You rode the wave well, $3,000,000 in equities, a home worth $3,000,000 with $2,000,000 in equity, and a 3% fixed-rate mortgage that now looks like a work of art in hindsight.

You've been burned out for two years. You feel genuinely bad about building products designed to maximize doomscrolling time among people who'd be better off closing the app. But you have two kids in private school for a total cost of $125,000 a year after tax.

Your husband works part-time at the science museum for $24 an hour because it's meaningful to him. Yes, you'd love for him to get a well-paying full-time job so you can retire early, but he loves the “WiFI lifestyle” as he constantly jokes with his buddies.

Several years ago, he read the post, How To Get Your Spouse To Work Longer So You Can Retire Earlier, and the concept stuck. He sees other men online living a life of leisure while their wives work, so he figures why not him too.

New Target Age To Retire: 7 More Years

Your family's expenses are $260,000 a year. Retiring at 43 feels reckless, so you set a target: 50, assuming 7% annual returns. By then, $3,000,000 should grow to around $4,800,000. Good enough!

Except three years later, you're 46 and your portfolio is worth $6,000,000. Not $4,800,000. Six million.

You are three and a half years ahead of schedule. The above-expectation gains alone, roughly $750,000 to $1,000,000 above what historical returns would have produced, represents almost three years of your annual expenses. Your home has also quietly appreciated from $3 million to $3.8 million, boosting your home equity by another $800,000.

At a 4.5% withdrawal rate on $6,000,000, you generate $270,000 a year gross, almost enough to cover your $260,000 annual spend after taxes. The only thing keeping you at your desk is inertia and identity.

Your kids are 14 and 16. In four years, they'll both be gone from the house. When they were first born, you had an excuse to send them to daycare and preschool early. But that guilt has always stayed with you. So you negotiate a severance and make up for lost time.

Although your husband starts to panic that he might not be able to play golf and poker with his buddies in the middle of the day, you reassure him that everything will be OK. You’ve done more than enough to support the family, and you need a well-deserved break.

Once the kids leave for college, you might even just leave his lazy ass.

From $7,500,000 to $15,000,000: To Your Health

You're 53. Thirty years of 55-hour weeks. You built something from scratch and genuinely helped people, a free health product that improved lives. Your philosophy was simple: the more you give, the more you receive.

But you're noticing the uptick in customer complaints, and they have started to outweigh the ones who are grateful. Why aren't features being added faster? Why won't you respond to every email? How dare you partner with sponsors to pay the bills on a product you give away for free?

But worst of all, your health is deteriorating. The childhood asthma that once sent you to the hospital multiple times has returned with a vengeance. You’re constantly aware of your breathing because it feels so labored. Meanwhile, your hip pops with every step, a reminder of creeping arthritis and the likelihood of a future replacement.

Your entrepreneurial pursuits have come at a real cost to your well-being.

You had $7,500,000 in stocks in September 2022. Today, your equity portfolio has doubled to roughly $15,000,000. Your real estate holdings also went from about $6,000,000 to $8,000,000. Your total net worth is somewhere around $23,000,000, give or take a million.

The above-historical gains on your equity portfolio alone, roughly $3,000,000 to $4,000,000, represent more money than most people accumulate in a lifetime. But you only realized these excess returns until you talked to a financial professional who made you realize how lucky you are.

For the first time, you have the clarity to admit that you've been staying in the game not because you need to, but because you don't know who you'd be if you stopped. You finally start focusing on your help and sell your company to a long-time employee.

Buy Yourself Time and Happiness With Your Excess Stock Market Gains

Making 100% in stocks in three and a half years is not normal. It's not what history suggests you should expect. And if you don't use these fortuitous gains to meaningfully improve your life, you risk missing the entire point of investing in the first place.

Here's your permission slip.

With returns this far above expectation, it makes no sense to endure a job you dislike for even one more year. It makes no sense to stay with a partner you've outgrown, or to keep grinding through obligations that no longer reflect who you are or what you value.

Change is hard. Giving up the pursuit of maximum money is genuinely difficult when status and income have become part of your identity.

But if your portfolio has doubled in three and a half years while you were busy working 60 hours a week, something worth examining is happening. At some point, continuing to trade irreplaceable time for incremental gains you don't need is just habit, not strategy.

You owe it to yourself, your partner, and your children to actually use what you've built. Because if you don't, you'll simply get richer, but won't feel quite right.

Have you done the math on how much “free excess money” the bull market has generated for your portfolio? If your portfolio has doubled in the past three and a half years, what is actually stopping you from making a major life change? And if you've already crossed that number, why are you still there?

Free Financial Analysis Offer From Empower

Stay on top of your net worth with Empower, the web's #1 free financial app. Track your cash flow, x-ray your investment portfolio for excessive fees and inappropriate risk exposure, and use their retirement calculator to plan for the future. The more you understand your finances, the more confident you will be when a correction inevitably returns.

I'm mailing out signed copies of Millionaire Milestones for those who take advantage of Empower's free financial check-up this year. You can read about my experience and the promotion instructions in this post. I've taken advantage of three free consultations with Empower over the past decade and each session has helped me better understand my finances.

Financial Samurai is a promoter of the Empower Advisory Group, LLC (“EAG”), and is not currently a client.