In an attempt to better understand the potential discount or premium to NAV for the Fundrise Venture product (VCX), I wanted to examine Pershing Square Holdings, ticker PSHZF, listed on the London Stock Exchange.

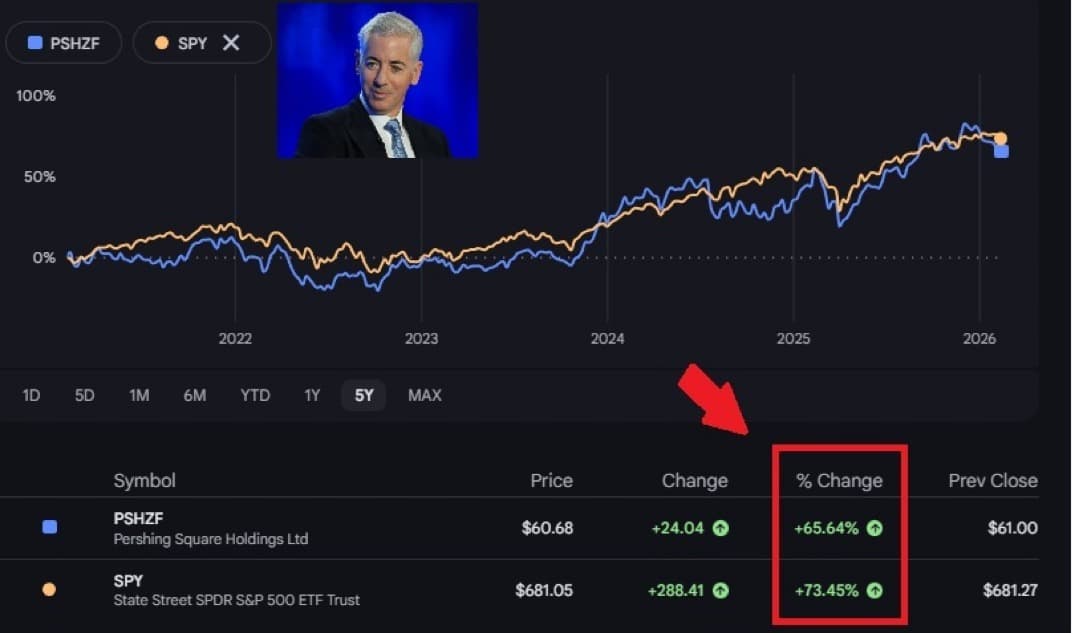

Pershing Square manages over $18 billion and is run by American, Bill Ackman. Meanwhile, the fund currently trades at about a 25% discount to its NAV. When it first listed in 2014, it traded at as small as a 9% discount. The NAV discount widened to about 40% in 2022, and then traded at a 30%–35% discount in 2023 and 2024.

As an investor, you can take this -9% to 40% historical discount-to-NAV range as a datapoint for when to invest. Obviously, the greater the discount to NAV, the better value you are getting. Not only could the NAV rise in value if Ackman invests in winners, but the discount to NAV could narrow as well.

When the Fundrise Venture product lists on the NYSE, could it trade at a similar discount to NAV as Pershing Square? It’s possible, but I highly doubt it for the reasons I highlight in this post.

Update: VCX listed on Thursday, March 19, 2026, after an initial target day launch of March 9, 2026. The listing was a success, with the shares opening at around $42 (+120%), and rising even more. For pre-listing investors, it's important to stay humble after a large investment win. Please do not spend your gains before they are liquid, as there's still a six-month lockup until investors can share their restricted shares and anything can happen. This article tries to see if there is a potential relationship between Pershing Square and VCX.

Why Does The Pershing Square Fund Trade At Such A Large Discount?

Here are four main reasons for such a persistent discount to NAV.

1) Core Holdings Are Public Equities

Pershing takes concentrated positions in 8–12 holdings and actively engages with management to effect change. Past holdings include Chipotle, Restaurant Brands International, Hilton Worldwide, Alphabet, Canadian Pacific Kansas City, and Amazon.

The issue with owning public equities is that you and I can construct the same portfolio ourselves. In other words, there is no barrier to entry to owning public equities. Fund investors must rely on the acumen of Ackman and his analysts on when to buy and sell.

Despite most of the positions being public equities, Ackman did use credit protection to hedge downside risk during the early 2020 COVID volatility. So if you are investing in a hedge fund and want downside protection, Pershing can provide that capability. But it usually doesn't seem to, going 90% – 100% long.

2) Closed Structure + European Listing

PSH is a closed-end fund listed in London, not a ETF listed on a U.S. stock exchange.

That creates:

- No daily redemption mechanism to arbitrage price back to NAV

- A limited natural U.S. investor base that doesn't invest in LSE stocks or funds

- Less index inclusion versus U.S. funds

- Some institutional mandates that cannot own foreign-listed Closed-end Funds (CEFs)

If this were a U.S. ETF holding the exact same portfolio, the discount likely would not nearly be as large. Maybe 0-5% instead. Closed-end funds can trade at discounts for decades if there is no catalyst to close the gap.

Unlike an ETF, there is no simple mechanism forcing convergence, as I wrote in my post on how different fund types trade.

3) Fee Structure (1.5% + 16% Performance Fee)

PSH charges:

- 1.5% management fee

- 16% performance fee above a high-water mark

That is cheaper than traditional 2/20 hedge funds, but it is expensive relative to passive equity exposure. Meanwhile, investors mentally discount future returns because fees compound.

When you discount expected future NAV growth by fees, some investors demand a structural discount.

4) Concentration Risk And Volatility

With usually only 8–12 stocks in the portfolio, there is significant concentration risk in PSH that warrants a discount. During good times, returns can be great. But during bad times, like in 2022, returns can be terrible, hence the 40% discount to NAV.

If you are investing in a hedge fund, your goal is usually to reduce volatility and protect downside risk through hedging (shorting some names). But if the fund does not hedge meaningfully or consistently, and instead creates additional volatility for holders who are not suited for it, a discount to NAV is demanded.

With manager risk, key-man risk, and strategy cyclicality, a discount to NAV is only natural.

Fundrise Venture Comparison To Pershing Square Holdings

Trading at a 25% discount to NAV after a NYSE listing would be a terrible scenario for Fundrise Venture product (VCX) holders. However, I do not think it will happen given the following differences compared to Pershing Square Holdings:

1) VCX Owns Private, Hard To Invest In Assets

VCX owns highly coveted private company shares in names such as OpenAI, Anthropic, Databricks, Anduril, SpaceX, Canva, and more. Unlike public equities, very few people can invest directly in these companies during their next private fundraise. As a result, it is logical that investors would pay a premium to own these names, not a discount.

2) VCX Will Trade On A Much Larger U.S. Exchange

VCX will try to list on the NYSE, not the London Stock Exchange. The NYSE is 8–9 times larger than the LSE in terms of total market capitalization. Trading volume on the NYSE is typically $50–$100+ billion per day versus only $5–$10+ billion per day on the LSE.

As a result, the natural demand pool is larger. VCX would be available to every U.S. retail brokerage account and could potentially attract institutional flows.

3) VCX Charges A Much Lower Fee

VCX plans to charge a 2.5% annual management fee and 0% carried interest (a percentage of profits). PSH charges only a 1.5% management fee, but 16% of profits after a high-water mark, which is part of the reason Ackman is so wealthy. I would much rather pay 2.5%–3% of AUM than 1.5% and 16% of profits for companies that have the potential to growth tremendously.

Hypothetically, if your $100,000 position doubles to $200,000 in one year, you would pay an approximately $3,750 fee to VCX and keep $96,250 of the profits. In contrast, you would pay a $2,250 fee to PSH plus 16% of the $100,000 profit, or $16,000, for a combined total fee of $18,250. Clearly, paying a $3,750 fee is preferable to paying an $18,250 fee.

4) VCX Manages A Smaller, More Nimble Fund With More Holdings

VCX is a ~$550 million fund versus PSH at $18+ billion. As a result, it is sometimes harder to outperform with such a large amount of assets under management.

For example, investing $55 million (10% of VCX) in a private growth company that performs well can make a bigger difference to VCX than to PSH (0.3%). Taking a similar 10% position, or $1.8 billion in PSH, would tend to move the stock significantly or even be impossible if Ackman wanted to invest in a smaller company due to limited float.

VCX owns at least double the number of companies as PSH. However, about 75% of VCX is concentrated in OpenAI, Anthropic, Databricks, Anduril, dbt Labs, Vanta, Canva, and Ramp. So I would say the concentration risk is similar to PSH’s 8–12 companies.

Conclusion About the PSH Case Study

I highly doubt VCX will trade at a similar discount to Pershing Square Holdings. They are fundamentally different vehicles, with different asset bases, fee structures, investor audiences, and structural dynamics. Although both are closed-end funds and lack the redemption mechanism of ETFs, the similarities largely end there.

Pershing’s discount is primarily a function of its public equity exposure, closed-end structure without a redemption mechanism, European listing frictions, performance fees, and concentration risk. VCX, by contrast, provides access to scarce private assets, intends to list in the United States, and does not have a performance fee drag.

While no listed vehicle is immune from trading at a discount, applying Pershing Square’s historical discount range directly to VCX is likely the wrong framework.

Destiny Tech100 (DXYZ) and Robinhood Venture Fund (RVI)

A more appropriate comparison may be DXYZ, which is currently trading at roughly a ~50% premium to its approximately $19.5 NAV, and RVI, the Robinhood Venture Fund, which after an initial 16% drop, now trades at a 30% premium to NAV.

I am doing this work primarily because I have approximately $770,000 invested in the Fundrise Venture product, which could realistically swing down by $150,000 or rise by as much as $385,000 simply based on listing dynamics. Post listing of VCX on March 19, 2026, the performance has been much greater than expected. However, given there's a 6-month lockup, it's good to stay humble and not count any chickens.

Because my wife and I do not have day jobs, we rely heavily on our investments to fund our lifestyle. As a DIY investor, I need to conduct deeper due diligence to improve the odds of making sound, long-term investment decisions.

Anyone here investing in Pershing Square Holdings? If so, what are your thoughts on how to approach the fund given its discount to NAV? Wouldn’t it be better to just invest in an S&P 500 ETF with minimal fees, given that performance has been similar over the past 5–7 years?

Fundrise is a long-time sponsor of Financial Samurai, as our investment philosophies are aligned. Please do your due diligence before making any investment and only invest an amount you can afford to lose. There are no guarantees when investing in risk assets, and you can lose money.

One question I do have and maybe I don’t understand. As a partner in closed ended private funds and SPV’s we get shares of companies as they go public or if they get bought out we get the cash value less our fund or SPV managers carry. Under this model do the owners of this new public entity get shares or larger distributions if a company gets bought out? I view the shares that get distributed as major upside. We get the recommendation of our fund if they are going to sell or hold them, but it’s ours to do what we want after paying the carry. How does it work under this model?

Great question, and you are not misunderstanding anything. You are pointing to a real structural difference between a traditional closed end private fund or SPV, where you may receive distributed shares after an IPO, and a publicly traded fund vehicle, where the fund itself is what you own, not the underlying portfolio company shares directly.

Under the public fund model, investors generally do not receive direct share distributions when a portfolio company goes public or gets acquired. Instead, if a liquidity event happens, the fund owns the IPO shares or receives the cash or stock from the acquisition, and then the manager decides what to do at the fund level, such as hold the newly public shares, gradually sell them, reinvest the proceeds, or in some cases distribute capital if the structure allows. In that setup, your upside usually comes through higher NAV, a potentially higher trading price for the fund shares, possible premium to NAV expansion, and maybe distributions or dividends if the fund policy permits.

That is why it feels different from an SPV or private fund, where you might get your pro rata shares distributed, pay carry, and then decide for yourself whether to hold or sell, which gives you that valuable second bite of upside post IPO.

In a listed fund structure, that discretion typically shifts from you to the fund manager. So your instinct is right, you may be giving up some upside flexibility from direct distributions in exchange for benefits like liquidity, simplicity, and access.

Also, owners of the public fund do not usually get larger distributions automatically if a portfolio company is bought out. A buyout may increase the fund’s NAV, but whether cash gets distributed depends on the legal structure, distribution policy, tax treatment, manager’s reinvestment mandate, and sometimes board decisions.

In many growth oriented vehicles, the manager may prefer to recycle proceeds rather than distribute them. So in the listed fund model, you are really betting less on direct distributed shares and more on manager capital allocation skill, NAV growth, market perception of the fund, discount or premium to NAV, and the liquidity and tradability of the fund shares.

It can still be a great setup, but it is a different type of upside. A simple analogy is that with an SPV, you may eventually get the fish, meaning the underlying shares or cash, while with a listed fund, you own the fishing boat, and the manager decides when to sell the fish, keep the fish, or buy more gear.

To know exactly how this specific model works, the key thing to review is the fund’s prospectus or offering circular, distribution policy, liquidity and redemption terms, any language on in kind distributions, and the manager’s discretion after portfolio company IPOs or exits, because that is where it will spell out whether they can or will distribute underlying shares, distribute cash, or retain and reinvest proceeds.

Thanks for the info. I have been piling in private investments and will watch this

I am investor in PSH, and mentioned it here, which I think is where you got the idea to investigate it. I have investments in closed end funds in Australia too. Some of them trade at a premium currently – GLS.AX and WAM.AX and others at a discount e.g. CDO.AX. GLS – stands for Global Long Short – is a listed hedge fund that so far is performing very strongly. It’s hard to explain the premium for WAM which invests in Australian small cap stocks. It pays very high dividends and the manager does a lot to promote it. All these have performance fees. I think the discount at PSH is mainly an overhang of the Herballife debacle and the London listing. In 2019 and 2020 the fund did 58% and 70% after fees. In 2021 it matched the S&P 500. Then in 2022 it did -9%, which was half the downside of the S&P 500. In 2023 it again matched the S&P 500.and outperformed by 3% in 2025. Only in 2024 did it under-perform the S&P. The fund is buying back shares and the discount is narrowing recently. So, I am hopeful it will get closer to NAV.

“ In 2019 and 2020 the fund did 58% and 70% after fees.” That’s huge!

Hopefully it can recreate that magic again. Thanks for sharing your thoughts.

Looked into buying a chunk of Pershing Square but the PFIC makes it nearly un-holdable in the United States. Almost like Ackman didn’t want US investors. Probably explains a lot of the discount

Great write-up. Didn’t realize Robinhood is on their road show w/ their own fund! Good to know.

After looking at some of the holdings in the prospectus, I do like where VCX is at w/ the portfolio company mix. I would think side-by-side VCX has the bigger brand names that people want exposure too.

It’ll be interesting to see how these funds do in the public markets.

From a valuation/size standpoint, they’re just so small & this is going to be great exposure for FundRise as whole.

PS – Wanted to add more to Innovation Fund but missed the cutoff w/ a t-bill rolling off on the 27th! Back to lower yields I go!

Sam thank you for going through these analysis for me. My friend and I who are both retail investors didn’t fully understand the listing and primarily focused on the increase in mgmt fee so voted no. However I am reconsidering this after the mutiple anlysis and case study you have put together. I have increased my contribution to the Innovation fund as I wanted to buy an entry level employee exposure to the AI companies and I will be okay whichever way the shareholders decide. Thanks again for all your detailed thoughts, you definately don’t get enough credit!

You’re welcome! I’m trying my best to figure everything out and understand everything as well. So this has been an educational process for me as well.

I just got a notification from Fundrise that investors are no longer able to invest in the Innovation Fund as it tries to establish its shareholders and capitalization before listing.

Best of luck to us!

For sure – yes my final tranche cleared yesterday to hit my target exposure so best of luck to all of us!

I also voted against primarily due to the increase in management. I would have thought they could have lowered the fee since they no longer will have to maintain a portion in cash to permit withdrawals. I know they give a few reasons why they believe the listing will benefit us but I cannot help but thnk they will benefit more.

I invested in their IPO long ago and I wish they would focus more on that.

Well said.Thank you for the insight!

Wow such insightful comparison analysis. Thanks for highlighting the differences in the fee structure. It really helps to see an example and to also look at the differences in holdings and exchange. It’s also a good reminder to me just how vast the investment sphere is. This was quite helpful thanks!

Enjoyed this series of articles! How would you categorize Berkshire? While not a CEF per-se, it seems like the price to NAV would behave similarly.