Since 1995, I've been a do-it-yourself investor (DIY investing). It all started when I saw my father trading stocks on his Charles Schwab online account. I was hooked and asked him to teach me.

The introduction led me to trade stocks during college. Sometimes I'd win, sometimes I'd lose. Thankfully, my portfolio was only about $3,000 at the time. Therefore, even if I had lost all my money, it wouldn't have been the end of the world.

Throughout my 13 years working in finance, I continued to invest on my own. I found DIY investing to be incredibly fun, especially sitting on the trading floor of a couple of major Wall Street firms. Every day was a new day to potentially make money!

Over time, I gradually started focusing more on asset allocation instead of individual stocks. My career was growing and it was simply too hard trying to consistently outperform the markets.

One time, I was taken into an office and scolded by the lead Managing Director for trading too much. I had whipped around about $12 million worth of trading volume in a month! This incident finally made me realize that trading too much was a career-limiting move.

The more I focused on asset allocation, the easier it was to manage my own money. For me, spending money hiring a financial advisor felt like a waste of money because I worked in finance, got my MBA, and was an investing enthusiast. That said, at 35, one year after retiring early, I did have a free financial consultation with financial advisor that helped illuminate some blind spots I had as a young man.

Ultimately, DIY investing is easier and cheaper than ever. The key is to maintain your discipline.

Traits Required To Be A DIY Investor

I understand not everybody has a finance background or is an investing enthusiast.

Therefore, DIY investing might not be the right way to invest for you. Instead, hiring a financial advisor or going with a robo-advisor like Betterment or a hybrid-advisor like Empower may be better.

However, in the process of writing my book with Penguin Random House, I was made to realize one of Financial Samurai's primary goals is to help empower people to better manage their money on their own. After all, DIY investing can save you a lot of money in financial advisory or management fees over time.

My editor said I've personified DIY investing based on the investing content I've written since 2009. Therefore, if I haven't encouraged people to invest more on their own based on the knowledge they've accumulated, then this site wouldn't have grown.

Note: If you have over $100,000 in investable assets, you can receive a free financial analysis from an Empower advisor by signing up here. An annual review is always worthwhile as your asset allocation can shift significantly over time, and your financial situation may evolve as well. We all have financial blindspots that are worth recognizing to build more future wealth. I've had two free consults with Empower before, and each time, I've received some fascinating insights that have helped me create more wealth.

Traits Needed For Successful DIY Investing

Here are five key traits to have if you want to become a successful DIY investor.

- Discipline. As a DIY investor, you must consistently save and invest your cash flow. You must consistently stay on top of your investments to make sure your capital is properly allocated. If you have a tendency to not pay your bills on time, DIY investing is probably not for you.

- Enthusiasm. Every morning you should be interested in checking the latest financial news. Not only do you enjoy paying attention to the latest economic and government data, but you also like to read about company-specific data. Without enthusiasm, you will eventually lose the discipline to consistently invest your cash flow. You might let your asset allocation go way beyond your risk parameters and blow yourself up.

- Hunger. You don't need to have worked in finance or get an MBA like I did. But as a DIY investor, you need to have an insatiable thirst for knowledge. Your hunger to learn goes hand-in-hand with your enthusiasm for investing. You believe there's always a money-making opportunity out there.

- Humility. As a DIY investor, you will inevitability lose money. The key is to recognize when you are wrong and make adjustments. Staying humble during good times is extremely important to manage your risk exposure. It is the investor who confuses brains with a bull market that often gets destroyed. Being self-aware is huge for DIY investing.

- Optimism. In order to take risks, you need to generally be an optimist who thinks things will work out in the end. Without optimism, you will have a tendency to hoard cash, rent for life, never ask out your crush, or start that company. A DIY investor believes they can make just as much money for themselves as a financial advisor or robs-advisor can.

How To Start DIY Investing

Let's say you've decided DIY investing is for you. You open up an online brokerage account and are ready to make your fortune. Before you put capital to work, you must fill your head with knowledge.

1) Understand risk and reward.

Generally, the greater the potential reward, the greater the risk and vice versa. Hence, you should understand the historical returns for various risk assets. Please read the following two posts:

2) Quantify your risk tolerance.

Now that you know what the historical returns are for the main risk assets, you must try and quantify your risk tolerance. A lot of people think they have a higher risk tolerance than they really do.

Therefore, I've been able to quantify risk tolerance in terms of how much time is required to work to make up for potential losses. Read:

3) Decide on your financial objectives.

Once you get a good understanding of your risk tolerance, you must then decide on your financial objectives. Common objectives include saving for a down payment, paying for college, and retiring with a large enough nest egg. Your financial objectives will give you the reasons for investing. They will give you the motivation to take risks.

Before our son was born in 2017, my financial objective was to generate enough passive income to provide for my wife and me. She had engineered her layoff in 2015. I wasn't very motivated to make more money because my wife and I lived relatively frugally.

Once our son was born, my motivation to provide shot through the roof. To earn greater returns I took more risks. Four years later, we've been able to boost our consistent passive investment income by about $100,000.

4) Understand your investment options.

There are so many investment options to choose from, it can be very overwhelming. However, as a DIY investor focused on asset allocation, you can narrow your investment options to a handful of ETFs, index funds, and REITs. You can also allocate a small percentage to individual stocks if you are an investing enthusiast. Here are the most common ETFs.

S&P 500: SPY, IVV, SPLG, VOO, VTI

NASDAQ: QQQ

Treasury Bond: IEF, TLT

Municipal Bond: MUB

REITs or Real Estate ETFs: VNQ, IYR, AMT, SPG, PSA, EQR, DRL

For 80%+ of investors, investing in these low-cost ETFs should be good enough.

One good way to help construct your portfolio is to sign up for any robo-advisor for free. Fill out a short questionnaire about your goals, risk-tolerance, age, and so forth. From there, the robo-advisor will spit out a recommended model portfolio based on your situation.

You can also play around with the assumptions. Below is an example where I dialed back my risk tolerance from 10 to 2 to see how the portfolio would differ. As you can see in the New % column, the allocation to TIPS and Municipal Bonds increases by 43%.

Ultimately, I decided my risk tolerance was closer to a 7. Robo-advisors are a great sanity check for DIY investors. The models are based on Modern Portfolio Theory. Of course, you can always let the robo-advisor do all the work for you for a small fee.

5) Allocate your assets according to your age, work experience, or financial objectives.

Now that you have listed out specific reasons for investing, it's time to put money to work. The easiest way to start investing is by following an asset allocation model by age or work experience. Therefore, please read the following:

- Recommended Net Worth Allocation By Age Or Work Experience (takes into account real estate and X factors)

These two posts have been painstakingly revised over the years to help DIY investors allocate their capital in a risk-appropriate manner. These models won't be solutions for everyone. But they should work well for ~80% of the DIY-investing public.

For example, at age 30, you might decide on a 70% stock and 30% bond allocation. Therefore, you could easily construct a two-ETF portfolio comprised of 70% SPY and 30% IEF.

By age 35, you may decide that you want to buy a house. You also believe a house does a good enough job in diversifying your public investment portfolio.

Therefore, you sell your entire bond ETF exposure to help come up with the down payment of your first home. From there, you resume investing more of your cash flow into stocks and bonds.

Again, you can use a robo-advisor's recommendations to help you construct your model. However, I've found robo-advisors tend to stick strictly to stocks and bonds. If you're interested in real estate or alternative assets, you won't find any guidance there.

6) Decide your percentage between passive and active investing.

Over time, you may really get the hang of DIY investing. Or, you may simply have an incredible amount of enthusiasm for investing. With more confidence, you decide to allocate a portion of your capital towards individual stocks, REITs, private eREITs, alternatives, commodities, and active funds.

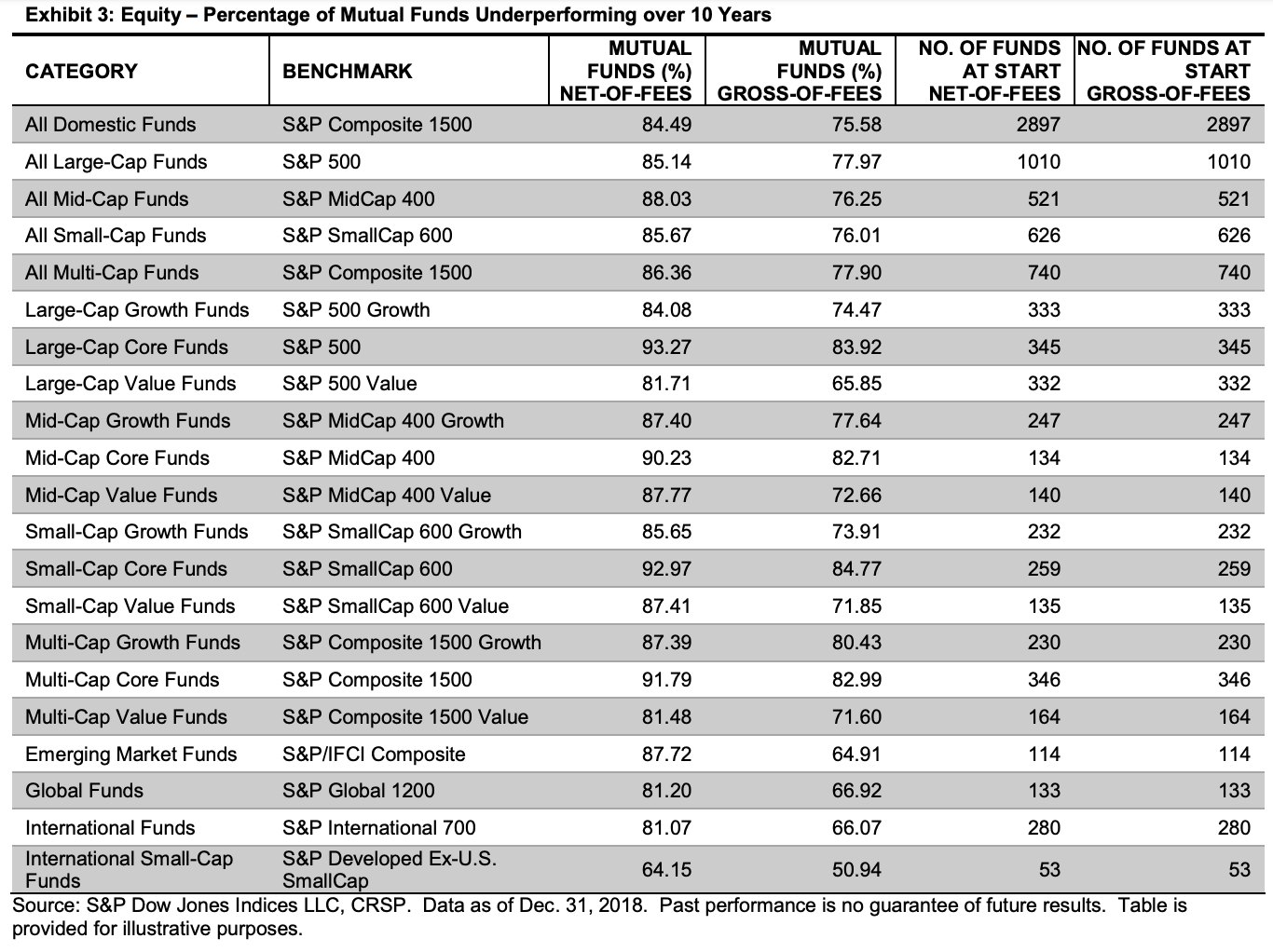

You may outperform the broader market in the short run with your active investments. However, you understand the odds are against you in the long run given most active fund managers underperform their respective indices. But you try anyway because you have hope. You also see people getting rich every day.

The maximum percentage of capital allocated towards active investing I recommend is 50%. 50% is for people who invest professionally for a living. For the majority of DIY investing enthusiasts, I recommend allocating no more than 20% of your investment portfolio to active investing. Please read:

DIY Investing Is Easier During A Bull Market

Back in 1999, I remember getting interviewed by some guy who worked at Arthur Andersen. He asked me what I was interested in. I told him I loved investing in the stock market. Then I naively started blabbing about some recent investment wins.

He immediately responded, “Bulls make money. Pigs make money. Pigs get slaughtered.” He then got up and thanked me for my time.

I must have come across as a know-it-all 22-year-old for him to say this to me. Obviously, I didn't get the job. I was bummed as Arthur Andersen was one of the most desirable companies that recruited at William & Mary at the time.

In a way getting rejected was a blessing in disguise because Arthur Andersen started going bust in 2002 after it was convicted of obstruction of justice during the Enron accounting scandal. Phew.

In a bear market, DIY investing can feel much more stressful. If you are also investing family money, you will feel the stress even more. You may feel like you are letting your partner and children down as their portfolio's sink in value.

The only good thing about investing during a bear market and rising rates is that it's actually easier to generate more passive income. For example, you can buy Treasury bonds yielding 5%+. Your dividend stocks will also have to pay higher dividends to stay competitive.

Be Careful To Not Go Overboard As A DIY Investor

As a DIY investor, I have lost money many times before because I bought too soon, bought too late, or sold too late. In the past, I also invested a much larger percentage of my portfolio than appropriate in individual names that sometimes went sour.

Today, I am a grizzled veteran who continues to invest my own money. I recommend focusing on asset allocation first and foremost. A proper asset allocation is what will determine most of your gains.

You don't have to be a great investor as a DIY investor. You just need to be a good-enough investor with the appropriate risk metrics.

If you decide to be a DIY investor, please remember the saying the Andersen Consulting guy told me. Don't confuse brains with a bull market. DIY investing is much easier during good times. It is during massive corrections, like the one we saw in March 2020, where a great DIY investor shines.

Further, are you really a great investor if all you're doing is performing inline with the broader market? I say no. You're a responsible investor, but not a great investor.

To be a great investor, you need to consistently outperform. After all, if everybody is getting rich at the same pace as you, you're just running in place. Here is my latest stock market forecast.

DIY Investing Is Scalable, But A Price

One last thing about DIY investing. If you learn how to invest your own money, you can then proceed to help invest your partner's money and other people's money. In other words, your investing skills has scale.

Just know that managing multiple portfolios takes time. And if there is a market meltdown, you will feel more stressed given other people are depending on you. If you underperform too greatly, you will also feel pressure.

The more money you manage for a loved one, the more stressful DIY investing will be during turbulent times. Therefore, I suggest keeping your DIY investing services within your household.

Recommended DIY Investor Free Tool

Finally, if you want to be a DIY investor, stay on top of your investments with Empower's free financial tools. It analyzes your portfolio's composition, highlights where you can reduce fees, and points out issues you might not suspect.

For example, below is a snapshot after I ran the Investment Checkup feature on my old 401(k). It identified the Fidelity Blue Chip Growth Fund had a high expense ratio of 0.74%, which I wasn't aware of. As a result, I swapped it out for a similar Vanguard fund to save ~$700/year in fees.

Empower's free tools have come a long way since I first started using them in 2012. The better you can track your finances, the better you can optimize.

Free Financial Analysis Offer From Empower

If you have over $100,000 in investable assets—whether in savings, taxable accounts, 401(k)s, or IRAs—you can get a free financial check-up from an Empower financial professional by signing up here. It’s a no-obligation way to have a seasoned expert, who builds and analyzes portfolios for a living, review your finances.

A fresh set of eyes could uncover hidden fees, inefficient allocations, or opportunities to optimize—giving you greater clarity and confidence in your financial plan.

The statement is provided to you by Financial Samurai (“Promoter”) who has entered into a written referral agreement with Empower Advisory Group, LLC (“EAG”). Click here to learn more.

Diversify Your Retirement Investments

Stocks and bonds are classic staples for retirement investing. However, I also suggest diversifying into real estate—an investment that combines the income stability of bonds with greater upside potential.

Consider Fundrise, a platform that allows you to 100% passively invest in residential and industrial real estate. With over $3 billion in private real estate assets under management, Fundrise focuses on properties in the Sunbelt region, where valuations are lower, and yields tend to be higher. As the Federal Reserve embarks on a multi-year interest rate cut cycle, real estate demand is poised to grow in the coming years.

In addition, you can invest in Fundrise Venture if you want exposure to private AI companies like OpenAI, Anthropic, Anduril, and Databricks. AI is set to revolutionize the labor market, eliminate jobs, and significantly boost productivity. We're still in the early stages of the AI revolution, and I want to ensure I have enough exposure—not just for myself, but for my children’s future as well.

I’ve personally invested over $500,000 with Fundrise (above is my investment dashboard), and they’ve been a trusted partner and long-time sponsor of Financial Samurai. With a $10 investment minimum, diversifying your portfolio has never been easier.

To increase your chances of achieving financial independence, join 60,000+ readers and subscribe to my free Financial Samurai newsletter here. Financial Samurai began in 2009 and is the leading independently-owned personal finance site today. Everything is written based off firsthand experience.

Great article, Sam. I think I have the 5 key traits you outline and decided to give DIY direct indexing a shot. We’ll see over time how this will work out. Maybe you can discuss direct indexing in a future blog, would be interested to hear your comments.

Hi everyone.

For some time I am investing in 4 mutual funds in my ROTH retirement account. (Semi conductor, technology, IT and pharmaceutical). They have been doing alright, no complaints. Along with that I invest in (dividend) stocks myself. These are mainly reputable companies. (Well known, good financial basis, positive outlook…). People have been telling me that 4 mutual funds is too much and I should scale down to only 2. What’s your opinion? I am 50 and I am also contributing to a PSRS retirement. (Lifetime teacher’s retirement package) and I am in no financial distress. Thank you for your sincere input

Loved this article!

Discipline is really the key to long-term success as and investor (as well as some patience). Other than that, I’d also say that it’s best to keep it simple. A lot of newer investors unnecessarily make investing more complicated than it needs to be!

What advice would you have for me regarding my post above?

Sam, great post. In my opinion, everything pertaining to being a successful investor comes down to risk assessment and discipline. If you cannot stick to your plan, you will not succeed. Both discipline and risk assessment are critical to this as improper risk leads to an increased likelihood of irrational behavior and without discipline you cannot properly assess risk.

Hi Sam! Great article as always. I believe I am a “responsible investor”, not a “great investor.” I am keeping up with the market, I don’t try to time things and I invest for the long term in low cost index funds. I keep no more than 5% of my net worth in actively managed individual stocks that I hope will provide significant growth. I find this to be a fun exercise for me, and I find it really exciting to read up on these stocks and try to think about the innovations they may come up with that will fuel a meteoric rise. Since its only 5%, I feel its a safe sandbox. I am a little surprised that you feel OK with a 20% actively managed allocation for a DIY (non-pro) investor.. that seems a little high. Perhaps that is just my personal risk tolerance. I am currently 41 and about 5-8 years away from FI. Thoughts? Am I too conservative?

Without knowing your current net worth composition, passive income, and current income it’s hard to tell.

20% is a meaningful enough amount to make a difference to overall performance, but not enough to significantly derail.

For example, having 20% of your portfolio in Apple, P&G, JP Morgan, Home Depot, and Google doesn’t seem too much riskier than the S&P 500. A lot depends on what your 20% is invested in and how the remaining 80% is invested as well.

Sam –

Thank you for this thoughtful article. I have been a DIY investor for the past 5 years now. Recently i started using two parallel robots advisor (Vanguard Digital and Betterment) to see how they compare , prioritize etc. it has been only 3 months – and due to the bull market, it is hard to tell who is “winning” – but will be interesting to observe and learn.

Do you have any experience with Vanguard Digital Advisor?

Thanks

Unless the portfolios are the exact same, one will “win” whenever you decide to stop the test. The fees are comparable right?

I don’t have direct experience with Vanguard Digital Advisor, but I know they’ve grown massively since launch.

Betterment was built from the ground up as a digital wealth advisor, so my nod is with them. VDA is more like a bolt-on to their hugely successful fund business.

Thanks!

Yes, fees are comparable (Vanguard slightly more competitive). You are absolutely right about the composition: they are similar, but not the same, as I have set it up. Betterment does a better job at the tax loss harvesting I have noticed already. I am keen on seeing the down market signal triggers each of them take with my similar portfolio mix.

I think the notion that you need to outperform the market to be considered a great investor is wrong. It comes from the fact that it is so easy to get market returns these days thanks to low cost index funds and surely greatness doesn’t come so easily.

But consider if these indices didn’t exist. Investor’s who were still able to match the indices would be returns would probably be seen as top notch investors. Just because it’s easy doesn’t mean its not great.

For sure. We all have different standards. If you think being great is performing in-line with the majority, then that helps make investing easier.

One secret to happiness is having lower expectations. The other secret is just wanting less.

I should have written more. It is incredible easy to get SP 500 returns, yet the overwhelming majority of people get far lower returns. These numbers are according to Vanguard for the 5 year period ending 12/31/2020

SP 500 – 15.2%

5% of investors returned: >16.3%

75% of investors returned: <13.1%

Median Investor: 11.6%

It's simply not true to say getting market returns puts you in line with the majority of investors.

Source:https://institutional.vanguard.com/content/dam/inst/vanguard-has/insights-pdfs/21_CIR_HAS21_HAS_FSreport.pdf (page 91)

Got it. Thanks for clarifying. Personally, I compare myself to investors, not the overall average population. And I benchmark my returns to the S&P 500 and other indices, which anybody can return by buying a respective index fund.

What do you benchmark to? And how have your returns been?

Related posts: https://www.financialsamurai.com/net-worth-benchmarks-to-ensure-proper-growth/

https://www.financialsamurai.com/how-much-have-americans-saved-for-retirement/

What do you use to compare yourself to investors and not the overall population?

I am relatively young at 30, so since I started investing in 2013 it’s been almost entirely a bull market. I am entirely invested in index funds. About 15% SP 500 and overweight small cap and value. I am .2% below SP 500, so below average and woefully below what you would consider an investor.

On the plus side I have made up for my poor investing skills with consistency and dedication so I am slightly ahead of your above average net worth of the above average person, or aanwotaap for short.

I’ve been a long time ready but first time poster. Congrats on all your success. You are the American Dream.

The S&P 500 is a great benchmark. It’s hard to be a great investor who consistently outperforms. I certainly do not. But I’m happy being a good or average investor by focusing on capital allocation.

We are all at different stages of our financial lives. Don’t let comparison be the thief of joy! Congrats on your progress.

I was happy with what I had when I left in 2012. Otherwise, I would have kept working. The past 9 years have felt almost like a nonstop gravy train.

Well, not to nitpick but the quote here was: “To be a great investor, you need to consistently outperform. After all, if everybody is getting rich at the same pace as you, you’re just running in place.”

The second line is problematic.

Everybody will never get rich at the same rate as you. While almost everyone invests, half the population does not invest in much more than buying a home or collecting comics or some such, or else they invest in depreciating assets (a trailer home, a non-collectible vehicle, clothes, shoes, etc.).

It’s hard not to outperform them if you have any sort of portfolio, even if your investments are not quite up to the market average. That may not make you great, but it is certainly better than running in place with everyone.

How cool is it that we’re nitpicking about this one particular line in the entire post? It shows how much we all care about outperforming.

All of us are free to benchmark our finances, our health, our fitness, or happiness on whatever we want. Don’t let anybody tell you otherwise!

Sam,

You say in your post “You may outperform the broader market in the short run with your active investments. However, you understand the odds are against you in the long run given most active fund managers underperform their respective indices.” Your statement, of course, agrees with virtually every financial advisor including some very smart and successful investors such as Buffett and Bogle.

What are the specific characteristics of the market or perhaps even the behavior of smart investors that makes it nearly impossible to beat the market?

Since you and I are a tennis players, here’s another example. The average tennis player cannot hit a 100 mph serve. In fact, the average 4.5 rated player cannot hit a 100 mph serve. However, with the right level of instruction, practice and yes, some degree of talent, many players can learn to hit a 100 mph serve.

I guess I just hate the idea of settling for average. So, again, why is investing inherently different?

Overanalysis and analysis paralysis. A lot of active investors are smart, but somethings they think they are smarter than they really are.

It’s much better to focus on asset allocation and long-term investment themes. Allocate your capital towards a long-term theme and you’re likely good to go.

See: Focus On Trends: Why I’m Investing In The Heartland Of America

Remind me what level USTA player you are? I’m still stuck at 5.0 after 5 years, trying to get down. But 2020 I did not play. I should be able to appeal down to 4.5 next year. Too old!

I used to be 5.0+, played in college and was in top 10 in South but haven’t played much in a long time. I will be in SF from Aug 28 to Sept 13 if you have any interest in meeting up.

Jim

Ah very cool! Shoot me an email and maybe we can go to a public park somewhere.

I prefer the DIY investing route myself too. I started out investing in single name stocks but quickly blew myself up luckily with just a small balance. So now I stick to ETFs for the most part.

I did sign up for Personal Capital’s free tools and got their free financial advisor meeting analysis. That was interesting to see and gave me some good ideas of how to improve. But ultimately I’m happy with DIY as I am with a lot of other things. Great article thanks!

I’m curious, what tool are you showing in #4? I’ve never seen that tool before. Also, thank you for continuing to write great content!

You can just sign up for Betterment or Wealthfront, answer a few questions, and the platforms will produce a model for you.

I started following Jussi Askola on Seeking Alpha to understand REITs better. It helped me tremendously to find high quality REITs instead of garden variety REIT ETF like VNQ.I invested in high quality REITs and they have been up YTD. Because they are liquid, one can get in and out at will.

I invested in FundRise as well. I see so far 3-4% Cash on Cash and 3-4% appreciation of investments. For some reason, it didn’t click for me. I am not sure I like the private eREIT model from FundRise. Others in crowdfunding market (like RealtyMogul) let you invest directly in each investment with higher projected cash on cash and IRR. After Fundrise experience, I am not leaning towards crowdfunding model.

Joe…I felt the same way about Fundrise, but I have stuck with it for 3 years now and I have seen a total return all time at about 8.2%.

I started with $10k and added another $10k 6 months later I believe. I feel its CAGR is somewhere between 5-7% (Cash on Cash and Appreciation together). I have been with them for around two years.

This is a solid start for Financial Samurai, I’m glad to see he’s providing coverage to stocks, bonds, and some alternative assets. Still yet to see any coverage on commodities and precision medals though. A well diversified portfolio would include at least 10% allocation in gold as an inflation hedge.

Thanks Dan. I could write a book about this entire topic. See Section #6 in the post. People are free to invest what they want. But hopefully, they invest in what they understand.

Given your belief on investing in gold, commodities, and precious metals, how do you reconcile your beliefs with this recent comment you made the other week?

“I sold my stock in 2019 as I saw a correction coming, Since then I’ve been in cash and renting.”

Thanks

Technically American gold Eagles are considered legal tender (e.g cash), about 0.25% of my face value are in gold coins. How much physical gold do you have in your portfolio?

My DIY portfolio return has consistently been below S&P’s average. But I enjoy DIY investing. It keeps me engaged, it keeps me reading…

With DIY, I feel like one of the most important trait is to remain humble after a big win. Investing DIY style and winning big makes it feel like a casino tbh. Left unchecked, sizing may increase too much after a big win and with one “bad” luck, your portfolio can be 0 or in some cases, negative. I hedge a lot to never be in that position, but that’s also probably why my DIY portfolio is below 8% (annualized).

But my main portfolio is all automated. No active management there. Just DCAs every two weeks to a target fund that reallocates itself. That portfolio has consistently beaten the S&P average thus far.

Is your DIY portfolio 100% stocks? If not, then it’s not a fair comparison.

But yes, if the underperformance is too great for too long, the money can really add up. After a couple years of underperformance, I would check out the robos and speak to a financial advisor and see if they can help.

DIY is much easier in an everything bull market. I like your caution about that. Most diy investors have the hardest time physiologically with the drawdowns. I know I do. We haven’t seen a prolonged drawdown in a while, except specific asset classes.

And that’s where knowing your limits of risk is important. It’s for your peace of mind, not just a mathematical equation. Our monkey brains don’t think with math. They think with emotions.

I got a quick tip for anyone who uses or is thinking of hiring a financial advisor. Go to the FINRA website and type in your advisor’s name. It shows you if they’ve had any complaints and what the complaint is. It’s basically a background check on their professional life. I had a broker who had 6 complaints logged against him in a 3 year period!

With index funds and ETF’s the only use I have for an advisor is to double check my asset allocation. Other than that I’ll never use an advisor again.

Good tip! Thanks for sharing.

The hired investing advisor is pretty funny to me, as in most cases the hired person is likely picking a target fund and rebalancing on occasion. People paying others to do that for them is crazy to me. In fact I had a friend try and convince me to use his advisor, he said he only charges $5k, a one time fee, and then sets you up. I finally asked him to show me some of his major set up and found that surprise, surprise, he was in a target date like retirement fund. It’s insane what people don’t know.

We are currently living in a world where the knowledge about any topic in the world is a couple keyboard and/or mouse clicks away. Truly. Better yet, you can just verbally ask your favorite App to educate you on nearly any topic. Why people don’t want to learn more is beyond me.

I came across a quote the other day…

“The man who does not read has no advantage over the man who cannot read”

You are in a great spot and possess more knowledge and discipline than the average investor if a financial advisor would only provide marginal, or negative, value for you. That’s great!

The benefit of an advisor for many is a measured investment approach, and the ability to buffer or prevent bad financial decisions. Finance is like a foreign language to many people, and like other things that don’t make sense to them, it tends to get avoided.

I only type all this to say it truly is different strokes for different folks. Some are financially capable and interested in money, and some are not!

Your last point is valid for sure. My previous point was that all of the information is out there, and easy to grasp with small efforts. If most people read a few articles, or even a book on occasion rather than binge watching TV shows, they could be further ahead.

There really isn’t all that much magic to investing consistently over the long haul. And for most people as FS said, buy and index set it and forget it. Eventually the time in the market wins over timing the market anyway. So, why people feel obligated to pay someone else to tell them the same thing is confusing to me.

Just as a relevant example…

If people just read this very post, and nothing else. The information provided within could set them up for life. Sure, there could be some minor deltas in capital growth with some coaching, but why pay the fee?

Make a plan, and execute. That’s all it really takes. Jumping in and out and all over, is going to give nominal gains. Being consistent for decades will be dominate always.

As noted in the post, you should still always look for a unicorn from time to time. I recently bagged one that netted an additional $2M for me. Surely lucky position to be in no doubt. But without this gain, I would still be trending to the same place in the future.

We enjoy your thinking and writing, Dogen. If you would ever consider putting yourself up for adoption, Rosemary would be willing to look into it for you. She’s very good with paperwork and documents and stuff.

We started the investing journey quite awhile back with a large bank’s preferred customer mutual fund offerings (etfs weren’t available back then) and very quickly found ourselves chafing under the restrictive allocation formulas our investment advisor was forced to abide by.

So we branched out with a small online brokerage account. And we have never looked back. We really love it. We read constantly. We love making our own investment decisions. And following news about the companies we have chosen to include. Can’t wait for the market to open each Monday. Walk with the wise and try to imitate the behaviors/choices of successful investors with a few of our own selections sprinkled in. But wear our tap shoes because some dancing is usually required. Feel we know how to behave in an up market. Always keep some powder dry so we can react prudently when there is a dip, no matter for how long the market stays down. History says its coming back up eventually.

We love companies that are growing AND that pay an acceptable dividend.

Neither one of us feel comfortable with a hammer in our hand, so the only real estate we own is our vacation home, and the Reits included in our online brokerage account.

The 2nd grade concepts of “more than or less than” have served us well. Just about the only math concepts we have truly needed thus far.

Could we do better by indexing. Sure. But not by a whole lot. And being bored out of our minds would be an unacceptable price to pay.

This is a more or less typical example of our investing. After some initial ipo euphoria, BYND has settled into a.little up, a little down ennui. No dividend of course. No Impossible Foods ipo yet. Maybe Spring 2022, but we’re not holding our breath. We did want to get some sustainable and “veggie” exposure so we looked around and invested in: CAG/Gardein div. 3.74%, GIS/Good Catch div. 3.49%, K/Incogmeato div. 3.61%, KR Simple Truth and Emerge lines div.1.96%, and TSN/First Pride and Raised and Rooted lines div. 2.24%. We don’t feel the need to go “beyond” these selections on some “impossible” search to fill out our “veggie” sustainable exposure.

Keep up the good work. We’re fans. :) :)

We also read/follow Neil Dutta, head of research at RenMac. Look him up. You’ll be amazed how well the guy can think.

finally the post we’ve been waiting for! I think what’s really important to see here is asset allocation… it’s very pre-mature to just shoot for the most gains or most profitable investment vehicles, you must first ask yourself what are you trying to achieve by investing? because saving for a car vs. saving for retirement are completely different goals thus there will be different investment vehicles that are more suitable for the goal

Love the post and love the idea of being a DIY investor. Especially liked the part about not spending money hiring a financial advisor. Though I am a CPA, I feel that I am capable of learning as much about the market to DIY invest. After paying off student loan debt (contributing to my company’s 401(k) match right now), I plan to max out my 401(k) and open a brokerage account to invest. Though I may have a little bit of FOMO, I am just learning so much about the market and it is exciting.