Well, we've done it, folks! Despite COVID-19 and tens of millions of Americans unemployed, the NASDAQ and the NASDAQ have successfully completed their V-shaped recovery. At the end of the day, capital, not labor is the best way to build wealth.

In this post, I want to go through some key lessons from this most extraordinary and largely unexpected rebound. We are firmly back to bull markets, despite the economy still in ruins.

I'm not buying into this rally, but I continue to hold my pre-pandemic stock positions with wonderment and bewilderment.

As always, the goal is for all of us to become better investors in order to achieve financial freedom sooner, rather than later.

Key Lessons Learned From A V-Shaped Recovery

1) You might get lucky once, but it's hard to get lucky twice.

In mid-March, I got lucky calling the bottom of the S&P 500 in a post called, How To Predict The Stock Market Bottom Like Nostradamus. The post went through elaborate reasons why I thought buying below 2,400 was a prudent move. Between March 18 – 23, 2020, I invested about $200,000 into the S&P 500 when the index was between 2,300 – 2,500.

By the time the S&P 500 hit 3,000, I had sold 100% of the $200,000 I invested in March. As a result, I left 6% – 15% further gains on the table because I was selling stock on the way up once the S&P 500 hit ~2,800. Further, I took profits on some tech stocks like Tesla at around $850 because it had come back from the dead.

It is extremely difficult to know when to buy, know when to sell, and know when to buy back in. Therefore, don't bother trying to time the market with the majority of your investments!

Related post: Your Wealth Is Mostly Due To Luck: Be Thankful!

2) Limit your speculative money to no more than 20% of your entire portfolio.

You can’t outperform the S&P 500 if you only buy the S&P 500 index. The only way you can outperform (or underperform), is if in addition to your index position, you also pick stocks.

In my perpetual desire to outperform the S&P 500, invest in promising companies, and invest in companies that would never hire me, I've always used at least 10% of my portfolio to invest in individual stocks.

I worked in finance in San Francisco since 2001 and watched the technology sector consistently outperform. Therefore, I hedged by buying tech stocks. It's worked out well so far, but this is mostly due to luck. I've had plenty of examples where I've bought stocks at the wrong time and have lost hundreds of thousands of dollars as a result.

Professional money managers spend all day analyzing stocks and still mostly underperform. Therefore, there is little hope for the rest of us who spend 40+ hours a week doing something else.

If you limit a maximum of 10% – 20% of your overall portfolio to trying to pick winners and time the market, you'll probably be OK. You might outperform with some of your positions or you might end up losing all your money if you're a real buffoon. But even if you lose 100% of your 20%, you still have 80% left. It's the people who risk much more than 20% who end up getting into trouble.

80% or more of your portfolio should be invested in low-cost index funds for as long as possible. Invest the other 10% – 20% how you wish, with no expectation of beating the market.

3) Capital gains tax matters.

If I was smarter, I would have just held onto my ~$200,000 position for longer. The V-shaped recover could easily continue.

The ideal situation would be to hold on for one year, see the S&P 500 go up further, and pay long-term capital gains tax instead of short-term capital gains tax. Alas, I'm not that smart as I'm fearful the stock market has gotten far too ahead of itself.

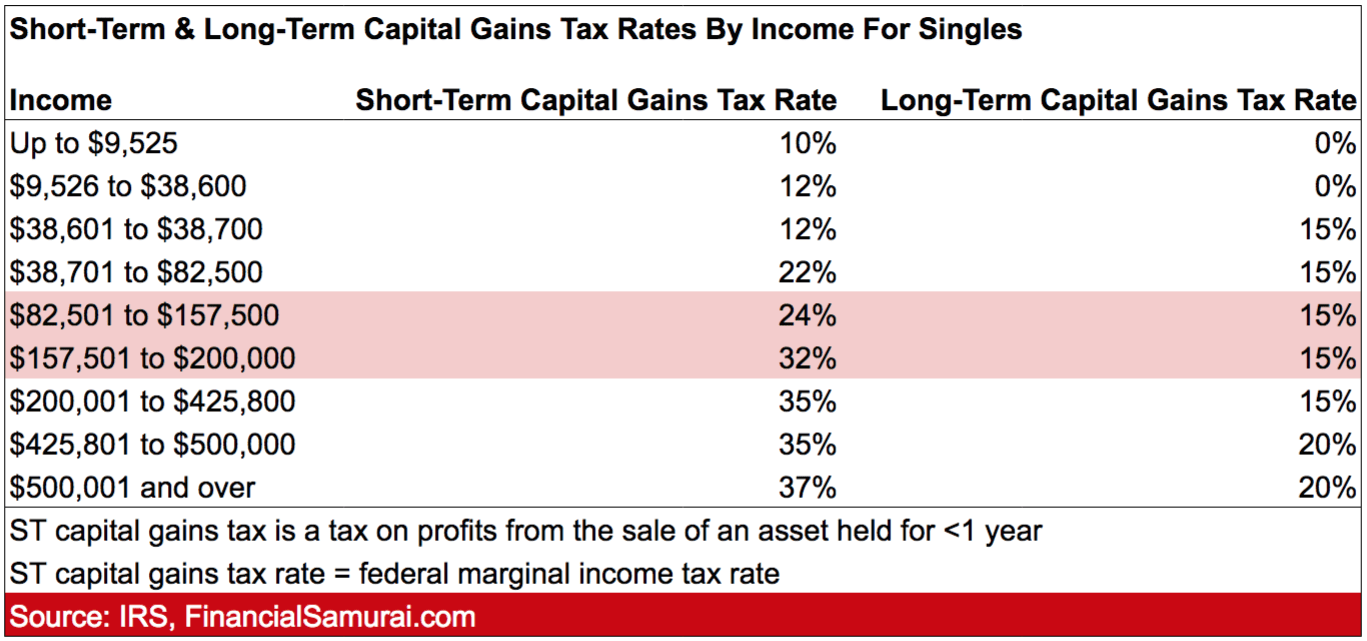

Below is a chart that shows the significant difference between long-term and short-term capital gains tax rates once you start making over ~$157,500 per person. A 17% capital gains tax rate differential (32% – 15%) is huge, and should be avoided.

For those of you who earn more than $200,000 a year and have investment income or gains, it is even more important to hold onto your investments for the long term.

The 3.8% Net Investment Income (NII) tax hits investment income when your combined income and investment income breach $200,000 for individuals and $250,000 for married couples. Then you've got to pay 35% or 37% federal short-term capital gains tax as well as state capital gains tax.

Even if you hold long-term (over a year), your tax bill can still be huge. For example, in California, you would pay 20% federal +3.8% NII + 13.3% state = 37.1% tax if you have huge gains over the statutory threshold. Below are some net investment income tax examples.

4) Check your asset allocation each month to ensure congruency with your risk tolerance.

Losing hundreds of thousands of dollars by March 2020 hurt, but it would have hurt much worse had I lost millions.

If I was down $1 million or more, there would have been a much greater chance that I would have sold some stock near the bottom in order to not lose another $1 million. The S&P 500 had only gone down 32%, whereas, during the previous 2008-2009 financial crisis, the S&P 500 went down about 55%. This V-shaped recovery is a surprise because it is so quick.

By having an asset allocation that closely matches your risk tolerance, you will have a greater ability to not panic sell at the wrong time. Can you imagine selling close to the bottom and then going short? Ouch.

5) Don't fight the Fed.

Despite all the carnage in the economy, if the Fed explicitly says it will be the backstop and use whatever means necessary to prop up the capital markets, believe it.

I have never seen a more open and clear Federal Reserve that has been willing to support every asset class, as this Federal Reserve. During the time of Alan Greenspan, you couldn't figure out anything he was saying. He was a master of saying a lot while saying nothing at all!

Below is a beautiful V-shaped recovery chart of the NASDAQ.

6) Separate your financial situation from the markets.

Just because you got a divorce, lost your job, got a pay cut, or were bullied online doesn't mean the stock market should also suffer like you. The reality is, people are still getting married, finding new jobs, getting pay raises, and joining mobs to bully others every day.

For example, let's say you own a retail store that got forced shut by the government. Your revenue has dried up and you believe the only thing you can do is apply for a PPP loan and set up a GoFundMe page. That's limited thinking. Instead, you should think about who benefits from your demise and buy their stock instead as a hedge.

The more you can see the other side of the coin, the more rational you will be. The reality is that someone is always winning when someone is losing.

The people who shouted the loudest that the world was coming to an end near the bottom were probably short the stock market, missed out on huge gains until the correction, or were going through some very difficult times in their lives.

It's good to minimize social media and traditional media consumption during times of chaos.

7) Capital, not labor, is the way to go.

With tens of millions unemployed, it is clearer than ever that depending on labor as your main source of income is very risky. Everybody must do everything they can to build more income sources with their capital.

Ideally, you want to build your capital large enough where it is generating more passive income than your day job. In this situation, you have reached financial nirvana and no longer have to work if you don't want.

In order to build your capital large enough, however, you must of course save aggressively and invest prudently for a very long time. Shoot to save 50% of your after-tax, after 401(k) maximum contributions for 10 years. If you do, I promise you will feel more freedom than ever before.

Stop thinking the only way to provide for your family is to labor endlessly. Expand the way you think about generating wealth. Once you have your debt under control and have multiple income streams, you will have more courage to take advantage of a downturn and buy.

8) The stock market doesn't reflect the present economy.

To get rich, we must actively try to predict the future. By the time the future is known, the opportunity to profit will be too late. Trying to get an edge reading media headlines is not the way to go. Media headlines are always lagging indicators.

The stock market is a reflection of the economy 6+ months into the future. The V-shaped recovery is saying this will get better. On the one hand, we should all find solace knowing the stock market is predicting everything will be much better in the economy if we can just hold on. Expectations are high!

On the other hand, the stock market has been wrong in the past and black swan events do happen. Again, do not confuse your current financial situation with stock market performance.

9) You'll never lose if you lock in a gain.

Even if you don't time the bottom or the top correctly for maximum profits, so long as you're winning, you're winning. Greed has caused many investors to ride their winners back into the ground.

And if you take those less-than-spectacular winnings to pay for your child's education, buy a house, help fund your parent's retirement, or donate to a charitable cause, then you're going to keep on winning.

V-Shaped Recovery Is Still Undetermined

Investing in the stock market should be boring. All you've got to do is find your appropriate stock and bond allocation, invest accordingly, and hold for the long term. The longer you hold on, the richer you'll likely become.

But it's hard to hold on forever due to three reasons:

- Emotion, mainly fear and greed

- The desire to use profits to pay for life

- The fact that we can't live forever

With stocks, you are a passive investor, which is great and why dividend investing is my current #1 ranked passive income investment.

However, if you are like me and enjoy the process of actively creating more value, then investing in real estate and building a business feel more rewarding. There's no reason why you can't do all three.

Let's all be thankful there's so far been a V-shaped recover. It's possible the V turns into a U, but for now, let's enjoy things. Now it's time to get the economy back on track too.

Readers, what are some lessons you've learned from this incredible V-shaped stock market recovery?

I didn’t expect the markets to bounce back so quickly and didn’t make any stock purchases while it was low. Now that it’s back up, do you recommend buying now or waiting to see if they’ll go back down? I know you can’t “time the market” but everything is higher than before COVID! What do you think I should do? Wait or just invest? I’m a brand new investor so I don’t have many holdings.

I’m personally not investing new money into the stock market and am focused on buying any real estate laggards out there.

But I would contribute to your 401k/IRA as usual for your long term retirement.

See this related post: https://www.financialsamurai.com/buying-stocks-after-a-huge-rebound-arguments-for-why-you-should/

Hi Sam,

Great post on staying calm and reaping the benefits of the market swings, thanks for the guidance. It would be great to hear from you, and the community, what the top dividend stock positions are. Looking to build that beautiful passive income.

Love this article Sam. I’m glad you found your motivation again and are back at it. I don’t even know why, maybe it’s because the sun is shining, maybe it’s because I didn’t even know about the NII (need to crunch numbers…hope it doesn’t bite me after selling some long-term holding this year), maybe it’s because I’m realizing how fortunate I am, but this one really made me feel good.

Love your work, thank you!

Maybe I don’t understand the stock market enough in general. I understand it looks six months ahead, but what would make it shoot past old highs to new highs given the current/expected environment?

Hi Sam – What are you investing your cashed profit from selling the stocks? I have cash to buy real estate but I would rather invest in municipal bonds for tax sheltering or short term bonds in the meantime. I live in Los Angeles. What funds would you recommend if you were in my situation? Thank you!

It’s hard for me to buy municipal bonds here b/c rates are so low. That said, bond interest rates have gone up recently as the 10-year bond yield went from about 0.6% to 0.9%.

I think there’s absolutely nothing wrong with holding good old cash earning 1.25% as we wait for deals. We’re back to all-time highs yet in order to justify all-time highs, the economy has to come back to 100%.

I’m searching for real estate deals.

Thank you, Sam! Like you said I have my money in Markus at the moment earning 1.3%. I will read your post for real estate.

Hi Sam, although not related to your post, I wanted to ask you the following: I am saving to buy a second property to rent out (the first property I also bought for 140k with cash/savings – no debt). Does it make sense to wait for 10 months to save enough money to pay in cash under the current environment? The net return on my first property is +/- 6%, so just wondering if it would make sense to get a mortgage for the second property and use the cash to invest in something else (dividend yield stocks?). I have to say that I am not in your league and only very recently I invested for the first time in the stock market (I bought 10k of SPY at 240 following your advice, thanks much for that!). The only reason I can think of for not getting a mortgage is to avoid the bank fees/financing costs of the transaction (+/-5k) and not worrying of repaying a debt.

Love reading your posts and thanks for all the information and advice you provide.

I would advocate for return to free market. With FED buying MBS and lowering interest rates to zero, of course real estate prices and investments can maintain bubble valuations. Good for current owners but completely manipulated. I hope my children can buy assets at historically normal valuations. Home prices should reflect underlying incomes/ stock price reflect earnings rather that having FED support excessive debt and leverage. FED polices benefit top 10 percent. Other 90 percent representing all races have been left behind

The V recovery is because we are / were in an economic suppression not a real recession. Once people feel the suppression has / will end(ed), most of the economy will return to its prior growth. We just needed assurance that the world as we knew it was not going to end. The curve has been flattened. Hope is restored. Industries will shift, companies will shift, jobs will shift, but the macro economic situation will continue upward. Consumer saving rates will not stay high, but drift back down. And, we’ll likely have some over-spend as people spend some savings on pent-up demand items. As you say, the market looks forward.

p.s. If you want to be the S&P or other indices, use covered calls to increase your capital-based income.

This is pretty much what I am planning/investing for as well. There is still a lot of short term risk but even in retirement I want to stay aggressive with the money I hope not to ever need for a long time, if at all.

I also believe the $5T sitting on the sidelines will act as a floor to the market as those who have waited for a testing of the lows that never came will want to put money back to work and will buy the dips which should smooth out short term declines as a normal part of a strong secular Bull run.

Current protests more about this rather than race Govt/Fed has your back and will ensure your wealth if u are rich. Poor folks might get a 1200 dollar check and a month or two of rent forbearance. Great system

As a parent with three kids in private school, what are some of the things you’re doing to fight the power?

A Universal Basic Income would likely be a good place to start. I’ve become a major proponent of it over the past year as a way to help people participate in the economy and the market without stifling the need to work punishing success. It would also help curtail this system where, yeah as TJH said, the “power elite” (for lack of a better term) and those who are well off get coddled while everyone else gets their own crumbs thrown back at them and told to get back to work.

I think the protests are definitely about more than just race. The anger that underlies the masses of people taking to the streets in large cities and small towns in all 50 states runs deeper than police shooting unarmed black men (not to dismiss that issue). There’s a systemic unfairness—not just a simple “You are more successful than me”—that people know is there that permeates everything, even if they can’t articulate the how and why. And to me, THAT’S why people are out in the streets.

Sincerely,

ARB—Angry Retail Banker

Totally agree wrt “Don’t fight the Fed”. I was Uber bearish. When the Fed dropped rates to zero and reduce reserve requirements I had to scramble back to reverse the position. As Papa Powell said he has an unlimited balance sheet ♂️

Really good points, especially the capital not labor advice. When I was younger, I was very one track minded – my day job was how I was going to earn money and save. That’s all I knew. While having a steady paycheck was crucial to earning my financial independence, it wasn’t the only place I should have been looking to earn income back then. Fortunately thanks to reading your blog for over a decade now, my eyes opened to explore other channels of income.

I’ve rarely had short term capital gains with my portfolio because I tend to just buy and hold for the long term. I didn’t realize the spread on tax rates was that big between short and long term capital gains. Wow!

Sam – you are wrong about the NII tax.

It doesn’t work like most other taxes.

First, it only applies when your “net investment income” (generally income from interest, dividends, stock transactions) exceeds $200,000 (or $250,000 if you’re married). Ordinary income (wages) does *NOT* count towards the threshold so you’re statement about those who “earn” more than $200,000 is incorrect.

Second, it only applies to the amount in excess of the applicable threshold. So, for example, if you have dividends of $201,000, and you’re single, you only pay NIIT on $1,000. Not such a big deal.

Obviously, if you have a huge capital gain, NIIT could be a bigger deal, but even then it’s only 3.8% of the excess. So, if you have a capital gain of $300,000 and you’re single you pay 3.8% on $100,000, which is $3,800, or 1.26% effective NIIT.

Ok, I guess we have different interpretations of what the IRS says here https://www.irs.gov/newsroom/questions-and-answers-on-the-net-investment-income-tax

Section 3:

Individuals will owe the tax if they have Net Investment Income AND also have modified adjusted gross income over the following thresholds:

Filing Status

Threshold Amount

Married filing jointly

$250,000

Married filing separately

$125,000

Single

$200,000

Head of household (with qualifying person)

$200,000

Qualifying widow(er) with dependent child

$250,000

If you have been earning more than $200,000 in income and not having to pay the NIIT on your capital gains, income, dividends, etc, I guess a congrats is in order. Perhaps set aside some money just in case you are wrong. I should also look back at my taxes and see if I can get lots of Tax refunds if you are right.

Here is also a NII tax example for you to check out: https://www.financialsamurai.com/calculating-net-investment-income-tax-properly/

Yes, you only pay the 3.8% NII tax on investment income once you’re above the $200k/$250K threshold based on income AND investment income. However, let’s say you make $500K a year and have a $1 million capital gain. Paying 3.8% on top of all the other capital gains taxes adds up.

This isn’t a NIIT post, but I will add further clarification and encourage more people to click the NIIT post linked in this post if they want to learn more.

It’s interesting that after reading about lessons from a V-shaped recovery, the only thing you focus on is the NIIT.

The NIIT does include income (MAGI) in order to calculate the statutory threshold where any investment income will then be taxed an additional 3.8%.

I’m a CPA. Who does your taxes? If you haven’t been paying the NIIT as a single based on your logic, you’ve essentially been failing to pay at least $7,600 a year in NIIT tax. The penalties and interest are high.

My suspicion is that you’ve never paid NIIT b/c your income + your investment gains have never exceeded the statutory threshold. Therefore, you are confused and don’t understand what you are talking about.

Please clarify if my suspicions are true.

Sam – Thank you. As always you are a gentleman and I stand (somewhat) corrected.

Jeff – I am not a CPA, and you are correct that I was incorrectly excluding MAGI because, in my retirement scenario, I am *not* planning on having MAGI above the threshold (i.e., my SE income and dividends will be less than $200K, and the rest is municipal bond income, not included in MAGI). So, for me, NIIT will not be an issue whatsoever absent a change in the law — but you are right that MAGI will typically trigger some amount of NIIT for people with MAGI and NII that, together, pushes them over the threshold and my explanation was wrong in that regard.

Even still, that amount will not be 3.8% of their total NII, but 3.8% of the total NII + MAGI over the threshold. Am I wrong? Educate me.

Sam’s post on NIIT is a very good one and I learned from it. You could be a little less harsh, as this tax stuff if monstrously complicated to non-CPAs.

As for the V-shaped recovery–what more is there to say? Maybe it sticks, maybe it won’t. I’m not trading (any longer, anyway) and simply use excess cash to buy anytime the market is down 10% or more. That’s worked out nicely for me, so far, but I’m interested in the tax issues and learning about how they work.

Dunning Kruger syndrome? So confident, yet so wrong!

I would not be high on your horses yet. 40 Million plus out of the workforce and many underemployed as well as Americans not protecting themselves might lead to a second wave and further disruption. It all seems FISHY to me with what has happened and the sp500 at January 1 Levels. The govt cannot keep pissing away $$$$

A certain someone has the Fed in his pocket and badly wants the stock market to look good to help his re-election prospects. That’s a corrupt but powerful motive lacking any checks or balances from leadership at the moment.

Thanks again for the analysis on calling the bottom! I was in 75% bonds from late June 2019 until March mid March. I’m up 23% YTD today.

I have no idea what set off the market rally on Friday but it was incredible.

I too believe there is a disconnect between market valuation and the current state of affairs and can only explain this because of what the federal reserve has done which is quite remarkable.

The amount of new money being printed is staggering and I worry about the long term effects such as potential for hyperinflation. But hopefully there are people far smarter than me that are able to balance on this knife’s edge.

I am glad I did not sell off my positions during this time but rather did strategic rebalancing which now in hindsight looks like a genius move. I specifically went into sectors that were depressed (picked up REITs and energy sectors) and they have rebounded like I predicted, just a lot quicker than I thought.

It was the May new jobs report that surprised the market on the upside. The market was expecting more job losses. Check out one of the job charts I published in this post.

The data from the Bureau of Labor Statistics revealed that 2.5 million new jobs were created. That marks the reversal of widespread job losses in April (20.5 million jobs shed) and March (700,000 jobs shed). Across the board, most industries saw an increase in employment.

The job data coming out is worrisome. I’d be curious to see numbers adjusted for PPP loans that have allowed companies to bring back workers at full time, despite lackluster revenue or even still being closed.

I have a concerning feeling jobless claims may be an issue the next 8-12 months as companies figure out the new normal and slowly realize they cannot turn a profit. We might see a lot of smaller businesses die a slow death, unfortunately rather than an abrupt never open again like some.

Thanks to the PPP loans a lot of people are going to give opening a try, but for those who already function at minimal margins, things could turn ugly, real quick.

I know of several people who are off unemployment because the Owners received PPP loans and were convinced they needed to use the money to pay them, so despite still sitting at home, they are being paid via their employer whose doors are still shut. They are no more employed in May then they were in April, but the Government is showing charts and graphs pretending they are.

There are some concerning data in the report such as “…the number of permanent job losers continued to rise, increasing by 295,000 in May to 2.3 million. (See table A-11.)”

What have I learned or realized during the last couple months? The government will try anything at any cost, which worries me for the future as we figure out how to navigate and address the giant hole we continue to dig.

100% agree Space

PPP loans took people off the unemployment rolls. Three card monty played by Government. Cant see how all this stimulus doesn’t end in a disaster at some point ( 20 to 30 years?).

Completely agree that the PPP is skewing the numbers and is going to cause major problems to businesses long term.

This is especially the case for the ones making minimal margins as you’ve highlighted. There have been a number of sources highlighting the complexity of the loans and how qualifying for forgiveness on the loan may be very difficult. So not only were they making minimal margins before this crisis, now they’ll be lumbered with debt repayment if they even manage to survive.

Definitely raises the question if this is the best use of funds to artificially keep many businesses alive that were already on the verge of collapse. Do agree that these are unprecedented times and a large percentage of businesses do need the support, although think a focus should also be given to job creation too, instead of just job preservation.

In a way, the PPP loan is going to help the low margin business the most, if it can survive because that means the PPP money is paying for a higher percentage of what it costs to run the business i.e. a much bigger difference.

In comparison, PPP money to a super high margin business is really just more money in the business’ pocket and doesn’t really move the needle as much.

Very good point! I suppose there’s an ideal segment of the market where the loan doesn’t artificially keep already failing businesses afloat and also doesn’t line the pockets of high margin businesses.

Although in reality I imagine trying to isolate that specific segment successfully will be practically impossible.

Great post once again, they’re always appreciated! Thanks Sam!

Sam, great post. You did “call” the bottom. Stating when you’d buy, that you were and why. Black swan aside,

you also called this recesssion. 2/2 on the the biggest moneymakers of the past year.

I cannot say I have down as well (heavily invested in Intl and Small Cap) but I appreciate the read and the read on the tea leaves. Let us hope the economy pulls out like the market – and benefits all. I am skeptical of the fall when the virus could resurge in areas. But what do I know you see where my money is.