Understanding how home prices fluctuate over time is one of the most intriguing insights gleaned from my post on the reasons behind property bidding wars. Learning how prices change will empower you to make more informed purchases in the future.

I contend that timing the housing market is comparatively simpler than timing the stock market, primarily because home prices tend to change at a slower pace. Given the relatively lower efficiency of the real estate market compared to the stock market, astute real estate investors may find greater potential for profitable investments.

Analyzing four home sale examples allows us to draw conclusions that can benefit prospective homebuyers. Approximately 70% of the homes sold in this area exhibit similar price changes. While the remaining home sales may not be as pronounced, they still show signs of price recovery.

Please note that all real estate is local. What may be happening in San Francisco may not be happening in your city and vice versa. The goal of this post is to use a real life case study to help you make a better buying decision if you feel your housing market is also in an upswing.

To invest in real estate more strategically, check out Fundrise. It is leading private real estate investment firm, manages around $3 billion in assets with a minimum investment of just $10. It focuses on residential and industrial real estate in the Sunbelt region, known for its lower valuations and higher yields.

Home Price Sales Compared To Redfin Estimates

Here are four examples of homes sold on the west side of San Francisco, alongside their Redfin estimates. While I could have utilized Zillow, I prefer Redfin's user interface and have found their valuation estimates to be more accurate.

However, it's worth noting that both Redfin and Zillow often provide incorrect or lagging home valuation estimates. Savvy buyers or sellers can use these bad estimates to make more profitable decisions.

In each chart, the $ sign denotes the sold price, while the dark black line represents Redfin's estimate of the property. What observations do you make?

Key Takeaways From The Charts

Here are the main observations from the charts:

1) The final sales price of each home significantly exceeds the Redfin estimate for each property.

2) There appears to be confusion in the second and third examples, as Redfin indicates a positive dollar figure since the sale, despite the sales prices surpassing the Redfin estimates. This suggests that Redfin may have updated their numerical valuation estimates post-sale without updating the corresponding valuation charts. Once these charts are updated, entirely new historical valuation estimates for each property will be generated, erasing the inaccuracies in Redfin's initial estimates.

3) All price points are well above double the median home price of San Francisco (approximately $1.7 million), indicating strength in the higher-end and median to lower-end segments of the market.

4) Home prices peaked in early 2022 and reached their lowest point in late 2023, representing approximately 18 months of home price weakness.

5) Home prices began rising again in late 2023, experiencing a 15% – 20% increase through April 2024.

6) Home prices demonstrate gradual declines during downturns and rapid increases during upswings.

7) Current home prices have surpassed their previous all-time highs achieved in 2022.

Advice For Buyers Based On These Home Price Charts

If you're considering purchasing a home, it's important to understand that real estate downturns typically span between 1.5 to 4 years. The last extended downturn occurred from mid-2006 to mid-2010, with prices remaining stagnant for a couple of years before rebounding in 2012. In essence, it took six years for home prices to recover.

Therefore, when you observe signs of price weakness in your local real estate market, it's advisable to wait at least a year before making a purchase. After this initial period, you can actively search for potential bargains.

While it's possible to begin bargain hunting at the onset of a downturn by submitting lowball offers based on your projected bottom price, the majority of homesellers are unlikely to accept such offers. It generally takes around a year for homesellers' expectations of receiving top dollar to diminish.

Downturn durations are shrinking

Thanks to advancements in technology and information efficiency, downturns appear to be getting shorter. For instance, the bear market in March 2020 was the fastest on record, rebounding within a couple of months. Similarly, the 2022 bear market lasted just one year before rebounding in 2023 and continuing into 2024.

Below is an example price reference check regarding a home someone purchased in the fall of 2023, at the bottom of the latest real estate downturn. Shortly thereafter, the sales price reset the Redfin estimate higher. Then notice the fade for the rest of the year followed by a surge higher in 2024 as more sales come in.

Waiting Too Long To Buy Has A Risk

When there is a rise in confidence regarding the economy and mortgage rate stability, buyers emerge in large numbers. The longer the period of below-average transaction volume, the greater the buildup of pent-up demand, leading to intense bidding wars.

All four property sale examples mentioned experienced bidding wars that drove the final sale price well above Redfin's estimate and their 2022 valuation peaks. In essence, waiting too long for the housing market to bottom out could mean missing out on significant savings as prices quickly ratchet up.

If you're genuinely committed to purchasing a home and intend to reside there for at least five years, it's better to buy one or two years early than even just a month too late. While it may feel uncomfortable to witness comparable homes selling at lower prices than yours for potentially three-to-four years, when the real estate market eventually rebounds, there's potential for bidding wars to drive your home's value back to its all-time highs.

Below is a chart depicting the weekly availability of inventory of single-family homes in America by Altos Research/Housingwire. The years 2018, 2017, and 2019 serve as baseline years for home inventory comparison. Remarkably, 2024 marks the fifth consecutive year with inventory levels below the baseline. Consequently, one should anticipate a backlog of demand among prospective buyers.

The Ideal Strategy For Homebuyers In The Future

Based on this case study, the optimal strategy for buyers is to wait one year after detecting weakness in the housing market, then offer 10% below the asking price for available properties. Waiting just one year for prices to decline minimizes the risk of missing out on a sooner-than-expected robust rebound. Offering 10% below the asking price essentially anticipates potential further price declines over the next one to three years.

Admittedly, convincing most sellers to accept a 10% discount from their asking price one year after the peak may prove challenging. Hence, you'll need to persuasively argue that selling at a discount isn't truly a loss, as it reflects the inevitable direction of their home's price.

While this assertion isn't guaranteed, you and your buyer's agent possess the skills to instill apprehension in the seller by leveraging resources like How To Convince A Seller To Sell To You When They Shouldn't. During downturns, it's easier to persuade sellers that the world is on the brink of collapse and that the market will never rebound. This is because humans are inherently inclined to avoid losses.

A Buyer Should Always Anticipate Further Downside

The challenge with purchasing during a downturn is that it's improbable the real estate market will swiftly recover post-purchase. Instead, it's likely to remain sluggish for another one or two years. This fear of financial loss is the primary reason for buyers' hesitancy to capitalize on lower prices. It can feel akin to stepping in front of a moving train!

However, the old tenant of buying low and selling high remains true in real estate too. Successfully purchasing at any discount off an already reduced price one year from the peak can provide relative protection on the downside.

For context, the worst real estate downturn in recent memory saw home prices decline by 10% – 20% annually for three years, stabilize for one year, then decrease by around 7% for another year before stabilizing once more.

Considering the possibility of shorter downturns, if another severe downturn akin to the global financial crisis were to occur, it's conceivable that its duration might shorten by one or two years. I just don't think we'll ever go through another housing downturn of this magnitude in the future due to stronger consumer balance sheets, more responsible lending, greater home equity, and the growing demand for real estate as an investment.

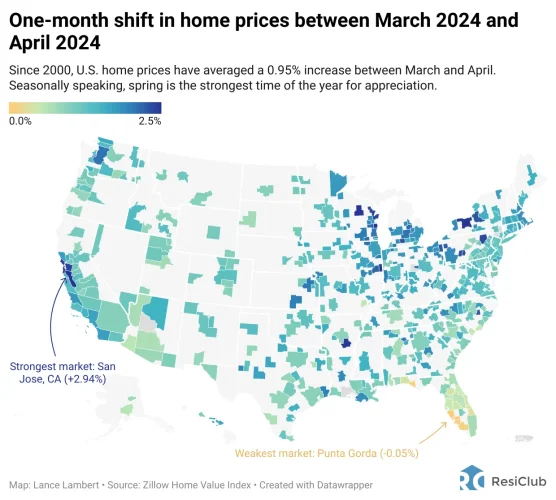

Still Better To Wait Until The Fourth Quarter To Buy (If You Can Find The Ideal House)

So, what should buyers do now that home prices have surged past their previous peaks? The most prudent course of action is to wait until the fourth quarter of the year when the housing market typically cools off. It is the best time of the year to buy property.

Historically, prices have followed a pattern of spiking in the first half of the year, tapering off during the summer months, experiencing a brief resurgence after Labor Day, and then tapering again as the new year approaches. During periods of market growth, the intra-year price decline doesn't typically reach the lows seen in the previous year before rebounding once more in the first half of the year.

The chart below illustrates this trend of higher lows and higher highs. Strategically, buyers aim to purchase during these dips, which occur towards the end of the year.

These price fluctuations within the year are cyclical because buyers tend to be more optimistic at the beginning of the year. With year-end bonuses, New Year's resolutions, and a fresh outlook, they're more inclined to make significant life changes, including purchasing a home.

The Upswing Will Likely Last Longer Than The Downswing

It's unsurprising to witness a roughly two-year downturn in the real estate market following the Federal Reserve's decision to raise rates 11 times since early 2022. This rate hike cycle was the fastest and largest on record. However, with the economy thriving and mortgage rates gradually declining, we may be poised for another prolonged upturn in the housing market.

The previous upcycle spanned from approximately 2012 through 2017, followed by a slowdown in 2018 until mid-2020. Subsequently, there was a resurgence for two years before the recent two-year slowdown from early 2022 through 2023.

It wouldn't be unexpected to see national median home prices resume their upward trajectory for the next four to six years before encountering another slowdown lasting between two to four years. The Fed has finally embarked on its multi-year interest rate cut cycle starting in September 2024. By the middle of 2026, it's conceivable the Fed Funds rate could be down by 2%, helping pressure mortgage rates downward.

An Important Development That Affects Future Home Prices

Indeed, while affordability may be low, there has been a notable shift in perception regarding real estate as an investment. This shift has led to an increase in the number of individuals purchasing multiple homes for investment and retirement purposes instead of just one. Perhaps, largely due to inflation, there is especially a growing fear among parents that if they don’t buy property today, their children will be priced out in the future.

Moreover, the growing recognition of real estate as a potentially lucrative investment has prompted institutional investors to raise more capital for home acquisitions. However, the most significant surge in demand stems from individual investors seeking to establish additional sources of semi-passive income.

Housing analysts often highlight the undersupply of homes as a key factor driving up prices. While this is undoubtedly true, I believe that the substantial impact on price appreciation stems from the millions of people choosing to build portfolios of rental properties alongside their primary residence, thereby significantly increasing demand.

Home Prices By City Compared To Their Peak Prices

While the future remains uncertain, I believe we have likely passed the bottom of the latest real estate downturn. Consequently, buying real estate today is likely less risky than it was in 2022 or 2023 because prices looked to have stopped declining.

Buying today is more akin to being a growth investor in stocks during a recovery. The chances of you buying a property and then seeing prices go down soon after are lower now. The key is not to get carried away and pay so far above fair market value that you need to wait a long time for the market to catch up to your purchase price.

Ideally, you should aim to identify and purchase properties in markets that have not already experienced significant price increases. Here's some trailing data from the Residential Club newsletter that may offer some insights.

Within each city, various neighborhoods may be experiencing different fluctuations in prices. Additionally, consider supply factors. Cities like Dallas, Houston, and Austin have a substantial amount of new housing supply entering the market, which may take longer to be absorbed compared to cities like Portland, Seattle, and San Francisco.

Stay Disciplined When Buying The Most Expensive Asset In Your Life

The aim of this post is to assist you in analyzing current trends and becoming a more discerning thinker when it comes to property purchases. Property is likely the most significant investment you'll make in your lifetime. Further, there is no guarantee it will go up in value. Thus, it's crucial to become as informed as possible about the current market and familiarize yourself with various buying strategies.

All these charts and data provide snapshots in time, subject to change from month to month. But I also see the data over this time period as a great example to help us become better buyers in the future.

Good luck with your property search! I'll be updating this post every six months to maintain the spirit of this case study. I expect bidding wars to emerge in 2025 thanks to a strong economy and a continued bull market in stocks.

Invest In Real Estate More Strategically

Considering the potential for a multi-year upcycle in real estate, investing now could be advantageous. Fundrise, a leading private real estate investment firm, manages around $3 billion in assets with a minimum investment of just $10. It focuses on residential and industrial real estate in the Sunbelt region, known for its lower valuations and higher yields.

Personally, I've allocated over $1m to private real estate funds, predominantly targeting properties in the Sunbelt. With remote work becoming more prevalent, there's a growing trend towards lower-cost areas of the country.

Fundrise is a long-time sponsor of Financial Samurai, and Financial Samurai is a six-figure investor in Fundrise funds. Analyzing Home Price Dynamics: A Guide To Smarter Purchases is a Financial Samurai original post.

Hey, great post! Understanding how home prices fluctuate is so important. I agree that timing the housing market is easier than the stock market because of the slower pace. Your examples from San Francisco really highlight the value of holding onto property for the long term. It’s fascinating to see how real estate can be a powerful tool for wealth building. Thanks for the insights!

Hi Sam – thanks for the illuminating post.

In terms of Zillow pricing, I’ll share my story. I was renting a lovely contemporary home in Santa Fe, NM at the beginning of the pandemic (for $4,200/month), with every intention of buying it from the owner (which we had discussed). Zillow estimated the home value to be $1.2M, and I had two appraisers confirm that estimate. But the owner thought he could get $2M, which I thought was an absurd figure.

Sure enough, before my lease had even ended, he managed to sell the property for $2M to a couple from Chicago. Immediately the Zillow appraisal shifted from $1.2M to $2M, where it still stands.

The story ends well, in that I recently bought and moved into a contemporary home (including a pool) in Placitas, NM for a little over $1M that would go for double in Santa Fe. It’s not necessarily my “forever home,” but much better than dealing with the vagaries of renting.

The lesson is that Zillow just watches where the wind is blowing rather than reflecting any true property value.

“ Zillow just watches where the wind is blowing rather than reflecting any true property value.”

I agree with this. Basically, it’s all lagging indicator and buyers and sellers need to be aware of the direction in which the local property market is going. Congrats on your new home.

“Current home prices have surpassed their previous all-time highs achieved in 2022.”

Honestly, I skimmed the article. However, if this was stated as fact without additional context it’s certainly not the case in my part of NorCal. Sub 3% rates had things cooking in spring ‘22. I would say about 100K off peak for a million dollars home.

I’m talking about west side San Francisco single-family homes. Everything is local when it comes to real estate.

What part of NorCal are you talking about?

Placer Couty

Gotcha. Yeah, the work from home craze has faded as people hear back to hit cities.

I’ve got my 2/2 condo in Placer County, Palisades.

After reading your newsletter I wanted to comment on it here since I know you read these!

(I’m a computer scientist BSc, if credentials matter.)

Wanted to say be careful of the allure of the promises that AI companies make. There will be some massive shifts in the coming years as AI is a powerful tool, but there are some things that AI will do well, and some things it isn’t meant to do well so that you can better align your investments with reality.

AI will never be good at any task that requires 100% exactness, and 100% repeatability unless that task can have hard programmed guiderails. A good example: Driving while staying in lanes for cruise control. The hard programmed guiderails are the road lines which can be defined with classic methods. Anything inside that boundary is fine. The difference between Tesla’s version and other carmakers is that Tesla doesn’t seem to have hard boundaries which is why I’ve used their features and had it suddenly try to veer off the road. The reason is AI is a big statistics machine looking at its data and coming up with the most likely choice based on its input. Any statistical model with a finite level of variance when run infinite numbers of times, is guaranteed to do all possible iterations. This means there will always be chance for error. It’s a logical conclusion stemming of the law of large numbers and central limit theorem in statistics.

A perfect example of where AI changes the game, and a good use case is Adobe photoshop’s content aware fill. It seems like a small use of AI, however, anyone who uses photoshop can tell you just how much time it has saved them. The guardrails are the selected section of the image, coupled with the prompt. The AI is free to experiment within those bounds.

Another example is live voice changing. As scary as it is, it does not have to be perfect because humans don’t always speak the same all the time. So if it makes some weird errors, it’s unlikely to be noticed, and would in many cases make it sound more human. (Our voices squeak, change cadence suddenly, etc).

The commonality of these use cases is that it is free to make errors within those bounds.

If you knew all this already, then I apologize for wasting your time. Otherwise, I hope it helps in your search for companies that will change the shape of society.

i have found zillow and redfin greatly over estimate home values, by at least 5-10%.

Fascinating. Which city? Curious how they have understated by 5-20% for about so examples I’ve seen.

Perhaps your city is going through a downturn so Zillow and Redfin estimates lagging?

I’ve noticed Zillow and Redfin overestimate values in LCOL and MCOL areas and underestimate them in HCOL and VHCOL areas. It’s not an exact science but it’s largely consistent.

Interesting. Specific examples would be great!

I have been in NVA for 30 years – HCOL. Its been a very hot housing market like others in the country for many years. It is mostly personal experience with these software estimates.

I sold a house in 2000 that they had about 920k and I couldn’t get more than 850k for sale. And that was in Arlington, VA, where multiple bids in one day on the market common. Tax assessed value was 825k. NOthing odd about the house or location.

The house I am in now they have at 940k estimate, and doubt it would fetch more than 850 based on the market, which is very solid. I bought in 2021 for 750k so appreciation to 850k I think is very solid in that timeframe and in this market. Assessment value 827k. I have just noticed that it jumps around lot. Through Feb of 2024 it was estimated at 880 by Redfin/Zillow, then in like a week it was adjusted to 940k, which is not realistic.

I just think they do seasonal adjustments and use too few house sales similar to you in the general area to make large adjustments. Nothing that you or I couldn’t do with common sense (housing market hotter in the spring) and a little online research into recent sales. I don’t feel they have any special sauce in their estimates.

It appears that January is the best time to buy based on the chart.

What would be interesting to understand is the 1-yr, 3-yr and 5-yr CAGR of the properties you listed – as that’s the only way for us to compare investment opportunities between asset classes. Otherwise, we are eyeballing a few charts and drawing conclusions from them.

Real-estate growth is lumpy, some of the gains were pulled forward during the pandemic and we are just now touching those previous peaks. If you look at the 5-year CAGR of those properties, you’d probably end up in the 5%-7% range, which is lower than the S&P500 (without leverage). With leverage, you’re likely in the 10% range – which is where you’d be with the index

Moving forward, we’re not going to see 7% growth in real estate, it’s likely to return to long-term average of about 4% in the bay area. At 6% interest rates, the math simply doesn’t work as investment.

You can make the rough IRR calculation with each. This is just a case study and snapshot in time, as prices and economic conditions are always changing.

“If you look at the 5-year CAGR of those properties, you’d probably end up in the 5%-7% range, which is lower than the S&P500 (without leverage). With leverage, you’re likely in the 10% range – which is where you’d be with the index”

How did you get 10% with leverage given most people who buy with a mortgage out less than 50% down?

Do you rent or own? And do you have as much invested in stocks and other risk assets as you do the house you own or the property you might buy?

Thanks

Horrible start and great finish in this article.

It would be very interesting to see the analysis above (closing cost vs estimate) for condos in San Francisco. I have seen exactly the opposite trend that you describe in the article (continued price cuts, condos unsold for >3months, transactions well below Redfin/Zillow estimates)

Single family homes in SF is a niche market as there is no more permits will be ever granted. Sorry for being blunt, but all your readers know you are biassed here as a homeowner in SF yourself.

Real estate is about location location location, and single family homes in SF are really scarce…it is difficult to project this analysis to the rest of the city or the nation.

Please look at what is going on in Texas or Florida, with prices collapsing left and right and all transaction closing below estimates.

No problem! The more blunt and harsh the better IMO. It’s important to see both sides in order to build more wealth and avoid land mines. We also don’t want to miss out on great opportunities like somehow over the past 10 to 20 years.

I’m totally biased, but I’m also looking at the data and home sales.

To understand your point of view, do you own or rent? If you rent, how long have you been a renter? And when do you expect to buy, if ever? Where are you on your financial journey? Understanding your back, and will be very helpful.

Feel free to send specific examples of sales and some data. It’s easy to say prices are collapsing or rising without any data. I did mention to be careful about buying in cities were supply can be endless.

I also welcome a negative gas post about real estate if you want to write one.

I have been renting for the past 14 years and have completely missed the boat. As a result, I will probably have to rent for life.

It’s not fair other people have been able to buy property in Build Wealth while I have not.

I wonder if your view is influenced by your position? I’m not sure how highlighting real life sales examples and doing an analysis on these examples to come up with better buying strategies as a bad start. Instead, it’s both enlightening and insightful as we transition to potentially lower mortgage rates in the future.

Have you been renting for a while? So many people I know who’ve rented for the past 10 years are frustrated and angry about the housing market.

Nacho, I own a condo and I’m seeing the same thing. I’m wondering what gives. HOA fees have gone up considerably with inflation, so I’m wondering if that’s part of it. I would love to see some data. I’m looking to sell next year or the year after. I’m wondering if a lot I’m wondering if a lot of condos are under capitalized like mine is. Mine is definitely due for a special assessment and I know it’s really difficult to sell when there is one and there are special rules surrounding the sale. Definitely not buying another condo again.

So incredibly fascinating! Love your deep dive analysis. If I ever need to buy a property I definitely want to hunt off peak in end of Q3 to Q4. Sometimes there’s not a huge range of inventory to choose from but there’s always something. It’s a fun and exciting process nonetheless.