At some stage in your investing journey, you may experience a situation where your investment returns surpass your active income (non-investment income, job income). The first time this happens, you may feel excited as you imagine the possibilities. But you likely won't quit your job just in case it was a fluke.

However, after several years of your investment returns surpassing your active income, you will develop a lot more courage to do something new. After all, the S&P 500 shows a positive return ~70% of the years, and the real estate market returns a positive amount an an even higher percentage of the time.

Perhaps you might finally ask for that well-deserved sabbatical without fear of your year-end bonus getting slashed. Or maybe you'll have the guts to start severance negotiation talks so you can pursue a new career.

The power of compound annual returns is why you should save aggressively and invest for the long term. It is also why you need to think twice about splurging on big-ticket items like a car you don't really need.

That $40,000 car you bought 10 years ago would be worth over $160,000 today if it was invested in the S&P 500. Saving and investing aggressively is a must if you want to achieve financial freedom sooner.

Financial freedom starts with informed decisions: Get actionable insights on investing, market updates, and wealth-building delivered straight to your inbox each week by signing up for The Financial Samurai free weekly newsletter. Financial Samurai has been featured in top publications such as the LA Times, The Chicago Tribune, Bloomberg and The Wall Street Journal.

Differentiate Between Investment Returns And Investment Income

Since I began working in finance in 1999, I've always had my mind set on generating investment income to eventually cover my desired living expenses. Getting into work at 5:30 am and leaving after 7:00 pm every day in a high-pressured environment for decades was not sustainable.

When I left in 2012, I had about $80,000 a year in total investment income of a total net worth of about $3 million. Back then, I dared not count on investment returns to pay for my lifestyle. We had just gone through a gut-wrenching recession and there was a chance we could go right back.

Further, counting on investment returns to fund expenses would require withdrawing principal, which I didn't want to do. A decent portion of my investments was in growth stocks that produced no dividends. I was also still in my mid-30s and believed there was further upside to risk assets.

Therefore, I wrote the post, The Ideal Withdrawal Rate In Retirement Touches No Principal. The post helped motivate me to live frugally. I wanted all of my investments to continue compounding during an emerging bull market.

I've followed this strategy since leaving work in 2012, mostly shunning value stocks that take too long to turnaround. As a result, my original retirement nest egg has grown and so has my investment income. Now it might be time to change strategies.

Time To Live Off Investment Principal?

After a 13-year bull run since retiring early, it seems the easy money has already been made.

Even Vanguard is estimating only a 4.02% annual return for U.S. stocks over the next 10 years. The estimate seems low, but it could certainly happen, especially given 2022 was a bear market that showed a 19.6% decline. Stock market valuations are extraordinarily expensive based on all measures. As a result, expected future returns are dampened.

Therefore, it's OK to sell stocks on occasion if you've made enough to buy what you want. Otherwise, you'll never enjoy your stock investments because stocks provide zero utility.

If a stock market crash does happen, you'll be pleased to have utilized your investment returns for things and experiences. Dying with too much money would be such a shame.

Instead of just arbitrarily selling off investments to fund your retirement lifestyle, you could simply raise your safe withdrawal rate. Spent more money so you can enjoy your returns instead of lose it in an inevitable correction.

Case Study On Living Off Investment Returns

Let's say you believe in the Financial Samurai Safe Withdrawal Rate Formula = 10-year bond yield X 80%. As a retiree, your average withdrawal rate over the past five years was 1.5% to ensure that you didn't draw down any principal. With a $3 million portfolio, you were living off $45,000 a year in gross income.

However, during these five years, your investments appreciated from $3 million to $5 million. They did so due to a 10.8% compound annual return. If you continue to withdraw at 1.5%, you will be able to live off $75,000 a year in gross income.

$75,000 is more than enough income to live a comfortable retirement lifestyle. You don't need that much money. But you're older now and feel like you might die with too much.

Given you were confident enough to retire with $3 million, the past five years feel like you've won five consecutive lotteries.

Not only have you been able to do whatever you've wanted for the last five years, but you're also $2 million richer! With five years less life to cover for, your desire to spend more has increased.

Here's another bonus. Risk-free Treasury bond yields are now at ~5%. As a result, if you invested your entire $5 million of investments in Treasury bonds, you'd return $250,000+ a year in state tax free income. Not bad!

The YOLO economy is calling your name. Got out and live the dream.

Cost To Fund New Initiatives

First, you want to use your lottery winnings to superfund four 529 plans to the amount of $300,000. The idea of using a 529 plan for generational wealth transfer purposes sounds like a no-brainer.

Next, you want to rent the Symphony Of The Seas Ultimate Family Suite for an around-the-world cruise. The cost? $20,000 a week for 10 weeks!

Although $200,000 is a lot of money, the suite is 1,346 square feet and large enough to comfortably accommodate your four grandkids. It would be the time of all your lives!

The total cost to fund these two items is $500,000, for a one-time withdrawal rate of 10% ($500K / $5 Million). If you consider taxes, then perhaps you really need to withdraw closer to $700,000. But let's just use $500,000 for simplicity's sake.

Still A Lot Of Money Left Over After YOLOing

After the adventure is over, you're now left with $4.5 million, or still $1.5 million more than you need.

You decide after spending so much money so quickly, you should take a break and go back to normal. Therefore, you adopt the FS safe withdrawal rate formula again and withdraw at 1.1% since the 10-year bond yield has declined.

With $4.5 million left, you get to live off $49,500, which is still $4,500 a year more than you were living off five years ago. All hail the benefits of a glorious bull market!

When people say the stock market isn't the economy, they are wrong. The stock market is the economy because people turn stock market wealth into spending. And spending is the largest portion that makes up GDP.

At What Point Does Work No Longer Matter Due To Investment Returns?

As I transition back to retirement I've been trying to justify my decision to no longer work so much. As a father of two young children, not working feels like a sin.

However, my investment returns have been greater than my active income returns for the majority of years since I retired in 2012. In addition, the active income I do make doesn't do much to stem any losses.

For example, let's say I lose 10% on a $5 million portfolio. That's a $500,000 loss. Even if I worked really hard for several months to make $50,000 online, I'd still be down $450,000. Losing $450,000 feels the same as losing $500,000. Terrible. Therefore, spending precious time to make $50,000 would make the situation even worse.

On the flip side, let's say I return 20% on a $5 million portfolio in one year. That's a $1,000,000 gain. Even if I take on some consulting projects to make $100,000, a $1,100,000 gain doesn't change our lifestyles one bit.

Work Feels More Painful When You Are Wealthier

After I blew up my passive income to buy a new house I decided to do some part-time consulting work. Working with a micromanager boss, I decided I absolutely do not want to work for anybody again. After four months I quit.

Therefore, there has to be some sort of crossover point where spending any amount of time making active income becomes a waste of time. The only way you would spend time making active income is if you truly loved your work. You don't care how little you get paid because you'd do it for free.

If you're a regular reader of Financial Samurai, I think you can tell I love to write and share my thoughts. Writing posts like, If You Want To Naturally Be Nicer, Get Richer, isn't going to make me money. But human behavior is an interesting topic to me so I write about it anyway.

The Investment Returns Crossover Point

There are two conditions an investor must achieve before they can drop active income due to investment returns. Again, we are differentiating between investment returns and investment income. Once you generate enough investment income to cover your desired lifestyle, you can leave immediately.

Condition #1: At Least Three Years Of Outperformance

If your investment returns are greater than your active income for at least three years in a row or four years out of the last five years, I think you have the green light to take things down a notch.

Three years helps minimize the chances that your investment returns are not a fluke. And given bear markets (-20% sell-offs) tend to happen every 3.5-4 years, I use the benchmark of four years out of five years to account for a couple of bad years.

If your investment returns are greater than your active income for five years in a row or five out of the last seven years, you should be able to completely retire if you want to.

Once you get to an investment portfolio equal to about $250,000, that is when you'll start feeling financially free. From there, you can build a million dollar portfolio and beyond so that your investment returns really start becoming significant.

Condition #2: Investments Equal To At Least 10X Your Annual Active Income

In order for your investment returns to generate more than your active income for three years or longer, you likely need a sizable investment portfolio that is 10X or greater than your annual active income. For example, if you make $100,000 a year, you would likely need at least a $1 million portfolio for a chance to generate $101,000+.

To generate $101,000 in investment returns on a $1 million portfolio would require a 10.1% return. If your entire portfolio is in the S&P 500 and the S&P 500 returns its historical average of 10.2%, then you've got a decent chance of outperforming your active income.

However, if Vanguard's lower return assumptions for stocks and bonds come true, then you will likely need an investment portfolio at least 20X your annual income until you no longer have to work. 20X your annual income is a key metric because it is my recommended net worth target to shoot for before retiring.

A Multiple Of Income Is More Honest Than A Multiple If Expenses

Using a multiple of income is better because it keeps you motivated to save and invest more as you make more money. We all tend to make more the longer we work. Further, using a multiple of income is preferable to using a multiple of expenses because it also keeps you honest. You can't take a shortcut to financial freedom by slashing your expenses.

Once these two conditions are met, you should be able to reduce your work hours or eliminate them altogether. Further, these two conditions are scalable, no matter how much money you have.

Investment Threshold Formula

Finally, after living the work, optional life for 13 years, I’ve come up with the Investment Threshold Formula where work becomes optional. Once your investments have achieved this target, you are free to take it easier at work, find the lower paying job that’s more fun, or even a Retire.

How Long Will It Take Investment Returns To Surpass Active Income?

The length of time it will take your investment returns to surpass your active income will depend on your saving rate and your rate of return. Obviously, the higher your saving rate and rate of return, the greater your chance of succeeding.

Given I believe your capital needs to reach about 10X your annual gross income in order for your investment returns to regularly surpass your active income, let's do some math.

Example #1: 20% Saving Rate

If you start with nothing and save 20% of your annual gross income each year, in 18 years at a 10% compound annual return, you will have accumulated 10X your annual income. In the 19th year, if you continue to get a 10% return, your investment return will have surpassed your static annual income.

If your rate of return is only 5%, then you will accumulate 10X your annual income in 25 years. If a 5% rate of return continues, then unfortunately, you will have to save and work for 36 years to finally see your investment returns surpass your annual income.

Example #2: 50% Saving Rate

If you start with nothing and save 50% of your annual gross income each year, in 11 years at a 10% compound annual return, you will have accumulated a little more than 10X your annual income. In the 12th year, if you continue to get a 10% return, your investment return will surpass your static annual income.

If your rate of return is only 5%, then you will accumulate 10X your annual income in 14 years. If a 5% rate of return continues, then you will have to save and work for 22 years to finally see your investment returns surpass your annual income.

The Likely Time Range

Saving 20% of your annual gross income each year really is the minimum amount I recommend everyone shoot for. Ideally, you will eventually make enough money to get to a 50% saving rate.

With a 20% – 50% saving rate and a 5% – 10% annual return assumption, it will likely take between 11 – 25 years until your investment returns steadily surpass your active income. Of course, if your income declines towards the end, then you can achieve this milestone sooner as well.

For me, it took about 15 years to regularly earn a greater return from my investments than my last year of working.

Thankfully, we can all buy Treasury bonds now and earn over a 5% risk-free return nowadays. That's pretty enticing, especially if you are withdrawing in retirement at less than 4%.

In addition, if you've diligently invested in private funds over the years, you may start seeing surprise capital distributions. These investment returns will come in handy to as you'll undoubtedly have new expenses to cover.

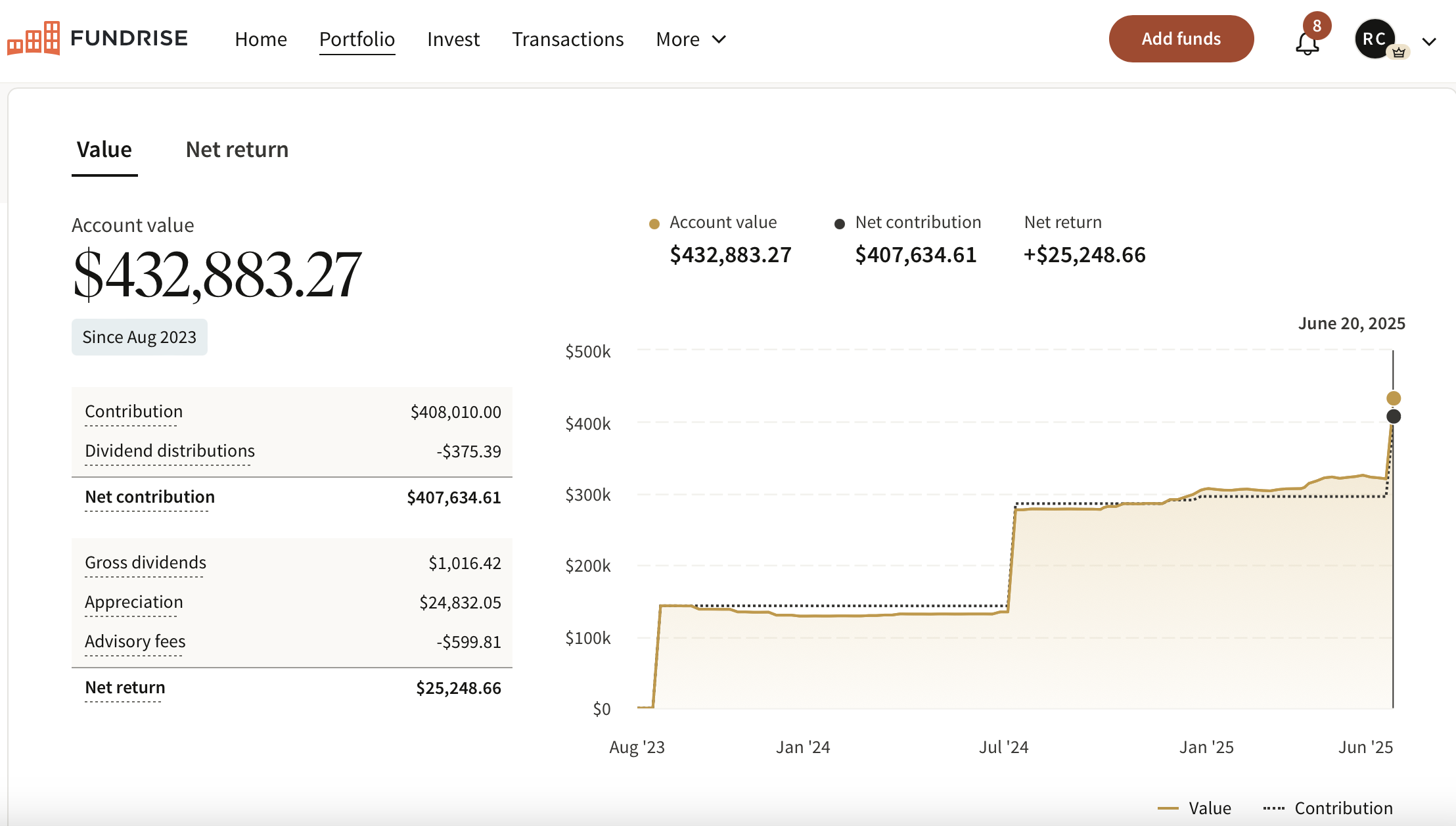

Here's an example of a much needed capital distribution I received from a private real estate fund I started investing in, in late 2016. I will keep the funds mostly liquid, but also continue to dollar-cost average into the S&P 500, private real estate and venture capital.

Living Off Investment Income May Be Harder In Normal Times

Generating enough investment income to cover your desired living expenses may be harder than generating high enough investment returns to cover your living expenses.

For one thing, you need to accumulate a lot more capital given interest rates are lower. You've also got to be disciplined enough to not touch principal. Finally, you may have to shun many growth stocks and equity real estate investments that produce no income, but may provide a greater return.

In contrast, if there is a raging bull market, then living off investment returns may be much easier. You won't need as much capital to fund your lifestyle if your $1 million portfolio is returning 25% a year. But to generate $250,000 a year in investment income will require a $12.5 million portfolio with a 2% yield.

The reality is investment income and investment returns are intricately tied together. The logical thing many people do who no longer want to work is change their investment composition towards less risky, more stable, income-producing investments once they've reached their ideal number for retirement.

Sample Net Worth Composition In Retirement

For example, ~50% of my net worth is in real estate versus ~35% in stocks. I want less volatility and more passive income. I've also got another 5% or so in individual AA-rated municipal bonds. The rest of my net worth is in private equity and private real estate investments.

When I was in my 20s and 30s, stocks accounted for 50% – 90% of my net worth. Losing 30% of my net worth in six months was OK. I could easily make up for my losses with my income. Today, not so much. Time is much more precious now that I'm older.

There Is A Level Of Capital Where Nothing Matters

Let me end by sharing a warning. There is a level of capital where you may lose all motivation to do anything.

In 2012, I was starting to get apathetic about making more money, which is one of the reasons why I left banking. At the time, my net worth equaled about 10X annual income and 40X annual expenses.

After such a long and relentless bull market, my apathy has returned. Yes, there were two massive spikes of motivation after each of our kids were born. But it has settled down now thanks to excess investment returns way beyond a safe withdrawal rate of 4% – 5%.

If our investment returns were poor since 2012, I would be feeling the opposite. But at the moment, I'm feeling incredible. There is no point in spending any amount of time making money if I don't love the work.

Shoot For A Net Worth Equal To 20X Your Average Annual Income

Once your net worth is over 20X your annual income or 50X your annual expenses, apathy sets in. Once your net worth gets to over 40X your annual income or 100X your annual expenses, that's when you start completely checking out. You may start constantly thinking to yourself, “F this BS!”

Therefore, if you want to stay motivated, you might ironically have to keep inflating your lifestyle! It's either that or give more money away. You can always do both.

If the strong returns in risk assets continue, eventually, productivity will decline. In that case, the only people left to do the work will be non-investors and new graduates.

Get A Free Financial Analysis Offer From Empower

If you have over $100,000 in investable assets—whether in savings, taxable accounts, 401(k)s, or IRAs—you can get a free financial check-up from an Empower financial professional by signing up here. It’s a no-obligation way to have a seasoned expert, who builds and analyzes portfolios for a living, review your finances.

A fresh set of eyes could uncover hidden fees, inefficient allocations, or opportunities to optimize—giving you greater clarity and confidence in your financial plan.

The statement is provided to you by Financial Samurai (“Promoter”) who has entered into a written referral agreement with Empower Advisory Group, LLC (“EAG”). Click here to learn more.

Diversify Your Retirement Investments

Stocks and bonds are classic staples for retirement investing. However, I also suggest diversifying into real estate—an investment that combines the income stability of bonds with greater upside potential. With rising rents and property prices, real estate tends to generate strong investment returns and passive rental income over the long term.

Consider Fundrise, a platform that allows you to 100% passively invest in residential and industrial real estate. With over $3 billion in private real estate assets under management, Fundrise focuses on properties in the Sunbelt region, where valuations are lower, and yields tend to be higher. As the Federal Reserve embarks on a multi-year interest rate cut cycle, real estate demand is poised to grow in the coming years.

In addition, you can invest in Fundrise Venture if you want exposure to private AI companies like OpenAI, Anthropic, Anduril, and Databricks. AI is set to revolutionize the labor market, eliminate jobs, and significantly boost productivity. We're still in the early stages of the AI revolution, and I want to ensure I have enough exposure. In 20 years, I don't want my young kids asking me why I didn't invest in AI near the beginning of the revolution!

I’ve personally invested over $500,000 with Fundrise, and they’ve been a trusted partner and long-time sponsor of Financial Samurai. With a $10 investment minimum to get started, diversifying your portfolio has never been easier.

Thank you. This information is very useful. We’re 41, 2M mostly in PE and 400k one income. It seems silly for the other parent to work and be taxed at 50+%. Fortunately this has given us time to pursue more lucrative and deferred taxed opportunities. Tax policy incentivizes quitting.

Sam: I am a 52 yrs Old Man. I have $40,000 in 401K, I am way behind on retirement. What can I do. I earn $65,000 Yr and am running out of time. Please advise.

Reaching retirement is a 3 legged stool:

-Save more

-Spend less

-Work longer

Unfortunately there is no magic formula here and taking on excessive amounts of risk to catch up is precarious, to say the least. Perhaps coming up with a financial plan so you have a roadmap of what you need to do to achieve your goals would be a good start.

At some point in your life you come to the realization that time is short. You blink and your kids are no longer children. Not to mention your health is a precious blessing.

While investing and transferring wealth to your future generations is an admirable goal, no amount of money can make up for the time you spend with them. There’s some balance to be struck between preparing for tomorrow and enjoying the present.

True. Where are you and your journey? Did you also decide to give up the money to spend more time with your children?

One way to prevent your income from becoming irrelevant is to compound it alongside your investments. This can be done by diversifying take-home income sources as well as growth of an income source ie. business growth, real estate rental increases, stock dividend increases via splits, enhancing income tax deferral/deductions, geographic arbitrage, etc.

My active income now, halfway thru my career, is 10 fold what it was at the start of my career. It still matters as it ups the ante towards the goal of a 25x income NW, albeit less than it once did relative to NW appreciation thru passive income/asset appreciation. My NW is currently over 100x my 6 figure starter income, but it is not yet over 25x my current 7 figure annual active income.

That’s the goal. To tether your net worth goal to your latest income to keep one motivated and disciplined.

Hi Sam

I’ve been reading your blog for almost 5 years now and have learned so much. Thanks for everything !

Question – Should portfolio withdrawals be included in the 20x income in a semi-retired household? My husband received a considerable sum about 14 years ago (tragic circumstances) and since then we’ve continued to work, but now want to focus on developing income doing what we love. A few years ago he quit his job to start something new and now that his income is up to a healthy amount, I am ready to leave my job and do the same.

Neither of us want to retire in the traditional sense; we just want the freedom to make less money while perusing our interests. We live in an expensive city in Canada and withdraw about 40k annually from our portfolio. Our income, including our rental property, the portfolio withdrawal, and day jobs, is around 180-190K. Net worth is sitting around 3.6-4m including our principal residence which puts us at 20x income. Our net worth growth has also exceeded our income for the last 5 years.

I’m taking the plunge either way, but it I’ve never gone without a paycheck! it’s quite a bizarre experience for me. We have a toddler and another on the way, and thankfully were also able to save up a year of expenses in cash, but giving up a solid paycheck with two young kids sometimes keeps me up at night. We are both mid 30’s.

Kevin

Hi Kevin,

Nice to hear from you. Portfolio withdrawals shouldn’t be considered income. But portfolio income should be considered income (passive income).

It sounds like you guys are living relatively frugally for your net worth. So I wouldn’t have any problems taking a leap of faith and doing something else you enjoy doing that doesn’t pay as much.

Further, to be able to spend more time with your little ones before they go to school full-time is really a blessing. Hard work, but the time goes by quick. I just dropped off my 4 yo at preschool. I asked him whether he wanted to walk around the block and see some garage doors before going in and spend more time with me, and he declined. He was so excited to go to school!

GL!

Sam

Sam: when you say 20x active income, I assume you mean 20x pretax wage/income too? Also a friend recently reminds me that my so-called “net assets” is still subject to ~30% tax when I sell them, so even our liquid portfolio is ~$10M, it’s really $7M because we have to pay 20% long term capital gain, plus ~10% California income tax.

Also our $10M was merely ~$5M 3 years ago thanks to the recent monetary policy. For people who won’t retire in 10-20 years it probably doesn’t matter, but since we’re planning to retire in 1-4 years, I feel at least we need to set aside 2-3 years cash for living expense so we don’t have to sell if the market falls 40%.

I’m experiencing a bit of this apathy already and I don’t have those numbers. I can’t imagine what it will be like when our investment values are high enough to really not care.

I think it really does come down to workers getting more wise to the notion of ‘why am I killing myself for these people?’ at work. I do good work, and we’re short staffed like everyone else. My current apathy stems from the notion of, what are they going to do, fire me? Someone else will certainly want me if that happens. I can’t be bothered to care too much. I’ll just keep doing my job and investing for our future.

Hi Sam, does your savings rate of 30-40% of gross income include mortgage payments since this is in essence saving/contributing to an appreciating asset? If not, how could someone save 40% of their gross income if they have a 15 yr. $750K mortgage which you’ve previously indicated is the ideal mortgage unless they make roughly $1M/yr?

Sam, i really enjoy reading all of your articles. In one of your articles you mentioned that someone could retire comfortably if they had assets that equal 50x annual expenses. Are these only investable assets or could they also includes equity in their personal residence. I am 53 and my investable assets are about 40x annual expenses and my home equity is about 10x annual expenses. Thanks for all the great info.

I relate to this article so much. I actually quit my job recently in my late 20s after the NW hit 20X annual income because I just couldn’t care less about it anymore. Sometimes I wish I kept the job just to have more income to buy more assets, but I also know I’d be hating life a lot more. Grass is always greener syndrome.

What do you plan to do next in your 30s and beyond?

I’m working on a website that will hopefully serve as regular income down the line (altho as I’m sure you know it takes a while before you see much traction). Also watching for new investment opps. Still getting used to not receiving a regular paycheck – it certainly is one of the more addicting things in this world.

“Once your net worth is over 20X your annual income or 50X your annual expenses, tremendous apathy begins to take over.” I’m close with my investments= 18x annual income, 45x annual expenses. I wouldn’t say tremendous apathy, but I do know that if I told most at work how much money I had they would absolutely say, ‘what the hell are you doing here dealing with this crap.” Part of my answer is mental stimulation. I like the challenge of the work and I haven’t quite found anything compelling to replace it, at least not yet. Only thing right now that would compel me to retire is the freedom to travel more, but you know Covid, not impossible but more inconvenient. But im also realisitc, there is only so much travel I can do before I’d be back home and then “what next?”. I don’t have the what next figured out so I keep working.

Check back once you hit 20X income.

What is it you do that brings you so much mental stimulation.

Really love this post and very timely as I was just bringing this subject up with my wife during one of our nightly walks. Including this year we will have made more in investment returns over the last 4 of 5 years. The last 3 being the biggest.

Current NW is about 30X expenses. Time to think about changing gears… :)

I agree with the 20X income and 40X expense rule. It just feels right and let’s me sleep at night if I retired. We’re around that level right now but are still allocating 85% in risk assets. In the bad scenario, we can live off of half of what we have. Hoping for sufficient upside in the next 5-10 years that we can buy a house as nice as yours, Sam, and vacation first class all the time.

I have 20 times income and 60 times expenses in investment accounts excluding equity in residences. But a huge chunk of that money is in pretax/ deferred accounts that will be taxed. Not feeling secure enough to retire quite yet as a result. Came from nothing and NW over $30M but still worried. Crazy.

If you’re still worried, then you’ve just got to keep grinding, especially if your work provides meaning.

At what level net worth do you think you’d stop worrying? How old are the kids now?

Wait a sec Jeff, I slept on your post to make sure it was what I thought I read the night before…, so based on your ratio your income is 1.5M, expenses is 500k on your NW of 30M?

Unless mine or your math is incorrect you need to take a serious look at your lifestyle and spend requirements to live very comfortably anywhere in the world. Perhaps you are supporting several families, maybe you need your 8k sq ft house in Newport Harbor and 6 cars to be happy. 1 vacation home isn’t enough, you need 3 at a 3M price tag each.

Anyway I slice your numbers, you’re ready financially. Perhaps reevaluate yourself not your finances…

Don’t disagree. Annual spending not quite $500k because NW number includes personal residences. So closer to $400k. Clearly have a nice but not crazy extravagant lifestyle. All expenses for 2 admittedly nice homes runs $100k. 2 newer German luxury cars, a horse that runs close to $30k, dining out a lot, 3-4 luxury vacations a year, helping out the kids etc. All adds up. We pretty much always fly coach, don’t own any toys like a boat, and i shop at Costco for clothes. Yes my wife does like nicer clothes. Not complaining and realize i spend way more than most but if you met me you’d never guess. Consider myself a regular guy who’s done ok. But not filthy rich. I guess if i lived in the midwest i might feel that way. But fit in with my friends and know plenty who have more.

Don’t be afraid to quit while you’re ahead. I’ve known folks who have bought RVs and boats just because they felt like they were the only ones on the street who didn’t have one and wanted to fit in. There’s a lot to be said for deciding that you’ve got enough and that you want to spend time with friends and family, or working somewhere you couldn’t have otherwise.

Sam, thank you for all you do, I appreciate your work and really value these posts.

My NW is currently greater than 50x annual expenses based on an average of the last four years of expense tracking. That said, I like your advice of using income rather than expenses as a NW target.

As a small biz owner, my income has varied over the years. This year I’ll make half of what I did last year. What I am struggling with is how to determine an appropriate income baseline with such variable income amounts:

For example, my current NW is:

• 16x this year’s projected income from work

• 8x last year’s

• 12x the average of the last 5 years

• 9x the average of the last 13 years

• 48x my base salary (before profits)

• 32x what anyone else would pay me to work for them (if I’m lucky)

My investment returns have not exceeded my income from work once in the last five years, though it’s ahead so far this year. My average income returns since 2017 have been 2x expenses.

I plan to keep working, but start slowing down more, and just doing what I enjoy more, so the big earning years are likely behind me.

Any advice would be appreciated.

Hi MD,

Best to make a best guesstimate for what your income will be over the next three years. Using the average of the last 5 years is good. But I would also forecast a realistic estimate income for the next 3 years too.

How many years have you be earning income and what business are you in? Can you save and invest more given your multiples are pretty strong right now?

It took me about 15 years to get to the regular Investment Returns Crossover Point. And I was VERY aggressive in saving and investing.

Sam

Thanks Sam. I appreciate it. I’ll use my past 5-year average as a starting point and also think about my 3-year projection and factor that in. I’ve been working in tech since 98 and after 13 years of running a business my energy level is dwindling. Still, there is more I can do to save and invest, and hope to get to the crossover point too some day. Thanks again!

When it comes to the 40x annual expenses rule of thumb, do you count healthcare costs post retirement? Makes a big difference because if I assume an annual cost of about 24k, that would come out to an additional $1M needed.

All costs. If you have to pay for it, you must include.

What I find amazing and concerning, is those on here who are well off are concerned about healthcare costs. What does that say for the average Joe’s and Jane’s out there?

The average person can get subsidized healthcare. Those who make over four times the federal poverty limit pay full price to help subsidize those who do not.

I believe Scott is referencing cost in general, regardless of subsidized healthcare. An individual can “afford” a subsidized healthcare plan (or various Medicare plan(s)) and still not be able to afford their copays, coinsurance, deductibles and/or out-of-pocket maximums. In those events, there is sometimes charity care coverage at an institutional level depending on the individual’s/family’s finances. Otherwise, inability to pay will result in enrollment payment plans or being sent to collections.

As someone who is still a bit away from my FIRE goals, I definitely am looking forward to the day of “apathy” where I get to 40X my annual income.

At that point, I feel like I wouldn’t be “apathetic” per se, but I’d probably attack new hobbies (whether they make money or not).

Hi Sam – I’ve been a long time reader but this is my first time posting. Very interesting article. I’m wondering what you think about our situation. My wife and I are 41 and we’re striving to retire by 45 (though I’ll probably work longer because I really enjoy my job, at least I do now). Our current net worth is only 7x income but 30x expenses (2.1M, 300K p.a., 70K p.a.). We have no debt, no kids and have good incomes so our expenses are low compared to income.

Hi Justin, I would shoot for at least 10X income if you plan to have no kids and keep expenses the same or less.

But I would really encourage everyone to get to 20X income, like stated in the article.

Justin,

Medical will cost about $1,200-1,500 per month, so your expenses may go up. Plus this is a high deductible plan that comes with, well, high deductibles and high out of pocket.

Usually I answer your questions at the end but I can’t resist a different angle. If you haven’t yet (or maybe I missed it in the article) maybe you should book the Symphony Of The Seas Ultimate Family Suite. :)

I noticed many of your recent articles encourage us to spend more. It’s hard to do that given most of us have a save and invest first mindset. Whenever people like us think about dropping a lot of money somewhere, we like to check all aspects of that expense first and afterwards may (or may not) have a feeling of remorse if the product, service or experience wasn’t as we’d imagined it to be.

I still have a long way to go and am hoping growth assets can continue to fly (realistically maybe not as high as times past).

The way I see it, if we aren’t going to spend money during a pandemic and a raging bull market, when will we ever spend money? Now is the time to spend money on a better life.

How have your investment returns been compared to income?

Yeah, we’re planning to go to Puerto Rico for a few days this fall – much needed!

They’ve exceeding my our joint income, no question year to year has been crazy, an anomaly one could argue.

This post made me feel better. I’ve been stressed at work recently, but when I step back and think about it I’m already at 20x income in terms of my NW (more if I count home equity and 529). So why stress… especially about stuff that i have no control over.

Yep, been getting more in the portfolio than we collect in wages from work for several years now, but these have been unusual years so I don’t trust that too much.

Also, my wife and I can’t begin collecting our pensions (without a big penalty) for a few more years. At that point, so far as I can tell (unless one considers the end of any further retirement plan contributions), continuing to work would actually cost us money. Time to hit the road and see (more of) the world.

The only thing is that, after decades of building my skills and knowledge in a very technical field (has to do with programming and databases) it will feel strange to just walk away from it. Especially as those skills will begin to become obsolete the moment I stop keeping them up.

It’s hard to leave, even if you hate your job. So if you feel fulfilled at your job, it makes a lot of sense to keep working IMO. It’s a bull market where returns are massive and innovation is good.

Sam, is your place in Tahoe safe from the fire?

It is Randy. Thanks. Thoughts on investment returns versus active income?

Thanks for the great article. Can you clarify how you calculate Net Worth in the context of this article? Does it include pretax 401K and real estate equity as well?

Absolutely. Anything that has value than can be monetized.