A poor millionaire sounds like an oxymoron, but they definitely exist. Roughly 6% of U.S. households are millionaires, yet many of them still don’t feel rich.

A poor millionaire is someone worth over $1 million but unable to access much of their wealth. In other words, their net worth is highly illiquid. A layoff, bear market, or job loss could quickly put them in peril.

In contrast, a rich millionaire is also worth over $1 million but can easily tap into their wealth. They’re liquid and resilient to financial shocks. Not only are they rich financially, they’re richer mentally. The thought of financial destruction rarely crosses their minds.

The Key Liquidity Zapper for Millionaires

The main culprit behind illiquidity is the primary residence. Owning a nice home is awesome, especially if you get to work from home or are retired. You just have to be careful owning too much home.

If you want to feel comfortable, aim to keep your primary residence below 30% of your net worth. If you want to feel rich, keep it below 20%. That way, at least 80% of your net worth can be in liquid or semi-liquid assets.

In reality, though, maintaining 70%–80% liquidity is tough, and also unnecessary. Millionaires often invest in rental properties, private real estate funds, venture capital, venture debt, and other illiquid alternatives. Decamillionaires and up usually have significant private business equity as well, another illiquid asset class.

That’s why having at least 20% of your net worth in liquid assets—like stocks and bonds—is so valuable. You’ll sleep better knowing you never have to sell illiquid holdings at fire-sale prices and always have dry powder to buy the dip when markets panic.

Recommended Income And Net Worth Chart Before Buying A Home

Below is a handy home-buying chart I put together based on income and net worth minimums. Ideally, you should have both the recommended income and recommended net worth associated with your target home price. If not, you need at least one of the following combinations before proceeding:

- The recommended income + the minimum net worth, OR

- The recommended net worth + the minimum income

Otherwise, you'll likely feel financially strained. And if you're FIRE, with no big paycheck during a bull market, you may feel added deprivation as well since it is in your nature to aggressive save and invest.

My Experience With Liquidity After 27+ Years of Building Wealth After College

My recommendations come from real-life experience, building wealth from nothing in 1999 to financial independence today.

With every home purchase since 2003, I’ve tracked how each one made me feel. My latest home purchase in 2023 was another test of my 20%–30% rule. It was an all-cash deal equal to about 23% of my net worth.

The moment I closed, I felt uncomfortable—house rich and cash poor—hoping nothing bad would happen to our finances in the next year. It was a terrible feeling that I couldn't wait to eliminate.

I even wrote about living paycheck to paycheck after that purchase, which ruffled some feathers. But I was simply being honest about how I felt. From that uncomfortable position, I decided to boost liquidity by negotiating more online business deals and taking on a part-time consulting role at a seed-stage fintech startup. Too bad I could only last four months because I didn’t enjoy the micromanagement.

The experience reaffirmed my belief: to feel truly rich and secure, keep your primary residence to no more than 20% of your net worth. Even though I survived the anxiety, I don’t want to feel that way again.

Thanks to a bull market and continued savings, my home now represents about 19% of my net worth, and I feel great – almost like I got a free lemon meringue pie with my Uber Eats order.

What amplified that feeling was selling my old primary residence in early 2025, after renting it out for a year. Converting that illiquid property equity into public stocks, Treasuries, and an open-ended venture fund that offers quarterly liquidity felt amazing.

As bullish as I am on single-family homes with views on San Francisco’s west side, the peace of mind that comes with liquidity trumps all.

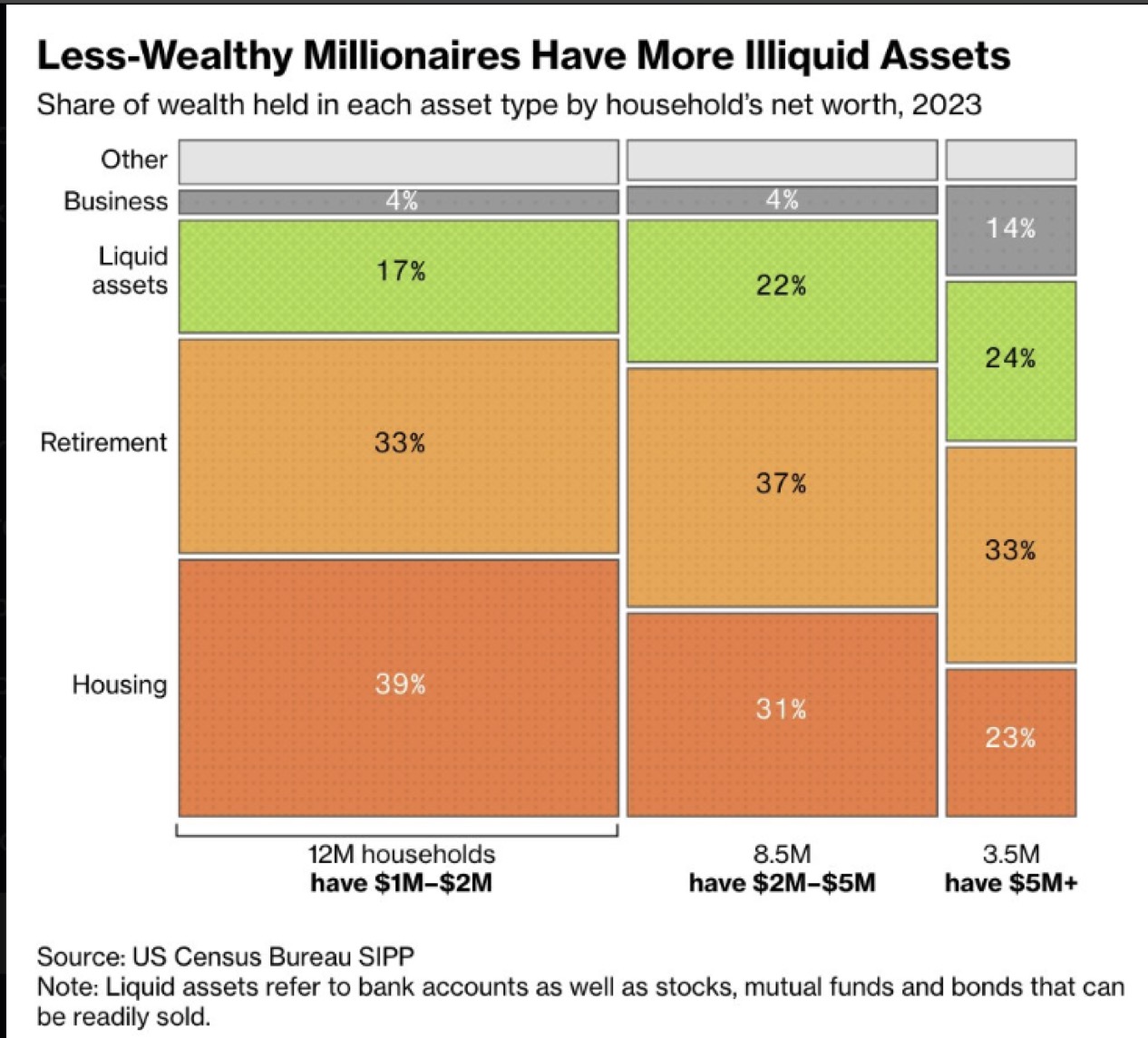

Liquidity by Level of Millionaire

According to the latest U.S. Census Bureau data, millionaire liquidity varies widely.

For the ~12 million households with a $1M–$2M net worth, an aggressive 39% of wealth is tied up in housing. It’s no wonder so many of these “poor millionaires” say they don’t feel rich or feel like they’re just running in place. Thanks to inflation, a millionaire today needs over $3 million to match the purchasing power of a 1990s millionaire.

Meanwhile, for the ~3.5 million households with a net worth above $5M, only 23% is in their primary residence. Roughly 33% comes from retirement accounts, 24% from liquid assets, 14% from business interests, and the rest from miscellaneous assets. Much better.

With the number of mega IPOs from SpaceX, Anthropic, OpenAI, and many more coming, there is going to be a lot of new liquid millionaires. Just be careful being their exit liquidity as these private companies have stayed private for for longer than average. As a result, far more of the wealth has been accrued to private investors.

Based on a Financial Samurai survey, $5 million is the ideal net worth for retirement with $10 million a close second. Once you feel rich enough, you’re willing to act, often by leaving a suboptimal job to pursue something more fulfilling.

I’m pleased to see that the 23% figure for housing among these “rich millionaires” aligns with my 20% guideline. I’m confident that for households worth over $10 million, housing as a share of net worth would fall even lower—likely under 20%.

I’ve written before about how you'll feel reaching various millionaire milestones – $1M, $5M, $10M, and $20M+. And I’ll confidently say: once you have over $10M and your home makes up 20% or less, you’ll unequivocally feel rich, even in expensive cities like San Francisco or New York.

For example, let's say you owned a $2 million home with a mortgage, but had $4 million in a taxable brokerage account, $1 million in Treasury bonds, $2.5 million in a IRA, and $500,000 in cash. There is no doubt in my mind you will feel rich.

This may sound obvious to you, but I cannot tell you how many expensive-city residents have asked me what that magic number and ratio is so that they can finally get off the treadmill grind.

Housing Builds Foundational Wealth, Everything Else Gets You Richer

The Census Bureau data reinforces one key truth: housing is the foundation of wealth-building.

Thanks to chronic undersupply, population growth, inflation, leverage, forced savings, and government incentives, owning your primary residence is generally a wise financial move. You might not build wealth at the fastest pace, but after a decade of homeownership, you’ll likely see substantial equity gains.

The combination of paying down your mortgage and enjoying long-term appreciation is a powerful force. Of course, there will be more opportune time than others to buy your primary residence. However, long-term, you want to get neutral housing so inflation doesn’t bludgeon you to despair.

Renting Temporarily Is Fine, But Not Long Term (7+ Years)

Some renters say they’ll “save and invest the difference,” but a minority actually do consistently. Discipline over decades is hard. In a way, owning a home with a mortgage protects you from yourself, forcing you to save and build wealth automatically.

If everyone had perfect discipline, we’d all be in peak financial shape with four-pack abs. Yet over 60% of Americans are overweight despite knowing the health risks.

I’m helping manage one of my relative’s investments for free. She’s in her 50s and has rented in New York City for over 30 years. Sadly, she’s now under pressure to move because her income hasn’t kept pace with the city’s relentless rent increases.

I am feeling the uncomfortable financial pressure through her and it truly stinks. If only she had bought a place 10 or 20 years ago, as an illustrator, her life would be so much easier today.

The Cycle Repeats Once Housing Gets To Be a Small Enough Percentage

Once you own your primary residence, achieving “neutral” real estate exposure, you can invest aggressively in other asset classes. Your foundation is set. From there other asset classes can all help expand your wealth. Over time, as these other investments grow, your primary residence will naturally become a smaller percentage of your total net worth.

Ironically, once your home drops below 10% of your net worth, you might feel too frugal. At that point, you’re likely earning far more than you can spend from passive and active income.

So don’t be afraid to upgrade your lifestyle. Buy a home worth up to 20% of your net worth, maybe even 30% again if you wish. Enjoy the fruits of your discipline, then work that ratio back down to feel another great sense of achievement.

Housing builds your foundation, but liquidity builds your freedom. The rich millionaire doesn’t just own wealth, they can use it when it matters most.

So, readers, are you a rich millionaire or a poor millionaire? How much of your net worth is tied up in illiquid assets versus easily accessible cash or investments? And in your view, what’s the ideal level of liquidity to truly feel wealthy and free?

Invest In Real Estate Without Draining Liquidity

If you’re interested in investing in real estate without taking on a mortgage, consider checking out Fundrise. The platform manages over $3 billion in assets, with a focus on residential and commercial real estate in the Sunbelt.

With interest rates gradually declining and limited new construction since 2022, I anticipate upward pressure on rents in the coming years, an environment that could support stronger passive income.

I’ve personally invested over $500,000 in Fundrise funds, and they’ve been a long-time sponsor of Financial Samurai as our investment philosophies are aligned.

If You Want To Be A Millionaire

Pick up a copy of my USA TODAY national bestseller, Millionaire Milestones: Simple Steps to Seven Figures. I’ve distilled over 30 years of financial experience to help you build more wealth and break free sooner. Amazon is having a great sale right now.

For more nuanced personal finance content, join 60,000+ others and sign up for the free Financial Samurai newsletter and posts via e-mail. My goal is to help you achieve financial freedom sooner.

The larger allocation to housing for those in the $1-2M net worth range makes sense given that most people are building their non-housing wealth alongside their housing wealth. The non-housing wealth tends to outpace once the house is paid off.

Yes, I agree. The goal is to try and get your primary residence as a percentage of your total net worth to below 30% to feel more secure. And once you get to 20% or less, you start feeling rich based on my experience and research.

Thanks, Sam — great article! I completely agree with your main points.

My net worth is approximately $5.5 million, with only 13% tied to my fully paid primary residence. While we don’t have individual retirement accounts where I live, pensions are provided through social security. Over 80% of my net worth is invested in liquid assets — primarily stocks and bonds — with a 60/40 allocation.

Interestingly, even though I really love our current home, I often feel a subtle urge to upgrade. In theory, we could afford it, but I genuinely enjoy the financial flexibility we currently have — it makes me feel wealthy. That’s why I try to quiet the voice in my head suggesting an upgrade, even though this flexibility sometimes tempts us to spend more freely. Ironically, I suspect we’d actually cut back on our spending if we had a more expensive home.

Very interesting article and thoughts! Timely too, as I just moved a fair amount of money around. I sold a few rental properties earlier this year, still have a few left. I was sitting on a fair amount of cash, and with a 10 month old, and a wife who wants to transition from corporate America to consulting, I actually reduced some liquidity in favor of lower debt, and cash flow.

I just put another 100k in a private equity deal, increasing my total investment to about 300k. 100k of that is in a RE Development Deal, 200k in another fund that has been kicking out 10% a year returns consistently.

Then, I did the unthinkable, threw an additional 170k at our primary residence, which has an insanely low rate, and recasted the mortgage. Why?

This will allow me to sleep at night as my wife makes the transition to consulting but more importantly being a full time mom. We have been paying a lot for our nanny (who is amazing, but between a high rate and payroll taxes, it adds up). We still come out ahead, as my wife has a great income, plus amazing benefits, but it’s not always about money, right?

We will only owe 550k on our primary, worth ~2.3 (paid 1.2, put another 150k in remodeling). At a 23% LTV, I feel good about it.

Liquidity? We have a 600k HELOC with a 0 balance. I have used this over the years to buy rentals cash, then refi them, but allowing me to get deals done quickly when needed.

In addition I keep 250k in a HYSA at all times.

This reduced mortgage debt, will allow us to cash flow more monthly, and me mentally to DCA stocks with little stress. Our private equity deals pay all our property taxes, etc, so our $2500 mortgage takes me back to 15 years ago expense wise in regards to housing.

38 years old, low to mid 3m total NW, yes, quite a bit locked up in our primary, however with 545k in 401ks, (2) Rental Properties, 50k in a taxable brokerage, 300k in private equity deals, and 250k in HYSA, we aren’t too far behind the 8 ball.

Oh plus, I bought our daughter 10k worth of NVIDIA when she was born. Wonder where I got that idea from? :)

Off to taxable brokerage accounts so someday we can enjoy true FIRE, thank you for all the lessons the past decade. I have learned a lot, followed some advise (missed out on some stock gains), but maximized proper leverage and real estate investments to help get to where we are at.

Goal is 10m NW, though it sounds high, I do see the path.

thank you for sharing your journey.

Very interesting article and thoughts! Timely too, as I just moved a fair amount of money around. We sold a few rental properties earlier this year, still have a few left. I was sitting on a fair amount of cash, and with a 10 month old, and a wife who wants to transition from corporate America to consulting, I actually reduced some liquidity in favor of lower debt, and cash flow.

I just put another 100k in a private equity deal, increasing our total investment to about 300k. 100k of that is in a RE Development Deal, 200k in another fund that has been kicking out 10% a year returns consistently.

Then, I did the unthinkable, threw an additional 170k at our primary residence, which has an insanely low rate, and recasted the mortgage.

Why?

This will allow me to sleep at night as my wife makes the transition to consulting but more importantly being a full time mom. We have been paying a lot for our nanny (who is amazing, but between a high rate and payroll taxes, it adds up). We still come out ahead, as my wife has a great income, plus amazing benefits, but it’s not always about money, right?

We only owe 550k on our primary, worth ~2.3 (paid 1.2, put another 150k in remodeling). At a 23% LTV, I feel good about it.

Liquidity? We have a 600k HELOC with a 0 balance. I have used this over the years to buy rentals cash, then refi them, but allowing me to get deals done quickly when needed. Nice to know it’s there as a back up emergency. Housing can go down 50% before I have to worry about this even being capped.

In addition I keep 250k in a HYSA at all times.

This reduced mortgage debt, will allow us to cash flow more monthly, and me mentally to DCA stocks with little stress. Our private equity deals pay all our property taxes, HOAs, so our $2500 mortgage takes me back to 15 years ago expense wise in regards to housing.

Focus for us moving forward is after tax brokerages, allowing true FIRE someday.

38 years old, low to mid 3m total NW, yes, quite a bit locked up in our primary, but not doing too bad with a couple rentals, 540k in 401k accounts, 300k in private equity deals, 50k in a taxable brokerage and another 250k in HYSA. (Plus when our daughter was born I bought her 10k worth of Nvidia as a gift)

Much of this is a huge thank you to everything I have learned reading this over the years. On to the stock account……..

Another excellent article Sam.

Back in 2006 I figured out that adding a LIQUID ASSETS row to my Net Worth spreadsheet did wonders for my ability to sleep. After 20 years of quarterly tracking this second most important data point…my average “Liquid Accounts” has been 22.4% of Total Net Worth. It was as low as 9.2% and as high as 37.4%, today it sits at 27.1%. I have found this ~20% ballpark to be shockingly consistent for me. I can report that 9.2% “feels” like a constant pucker and 37.4% “feels” like time to move onto a yacht anchored off some exotic beach.

I own several pieces of investment real estate (15% residential + 85% commercial), which requires a lot of maintenance, and I feel the need to keep extra reserves in order feel strong & confident. As a result, I find 25% liquidity is really my sweet spot to “feel rich”. The percentage of my primary res is not a factor and never has been because my wife & I decided to do the “overreach thing” once and then have lived in that house for 25yrs. All my “feeling rich” seems related to current liquidity vs. my perceived short term cash needs vs. catastrophe fears vs. trying to figure out how to optimize time & quality of life. Time & quality of life, of course, being the only things that matter…smh…

Buckets as % of Net Worth (~50yo,DINKs):

Primary Res (free & clear) = 7.0%

Taxable Accts = 29.5%

Retirement Accts = 26.0%

Investment Real Estate = 40.0%

Misc (Vehicles/Equipment) = 2.5%

Debt = -5.0%

Great feedback. Thank you for sharing! It sounds to me like it’s time to overreach again, maybe!

25 years is a long time to live in a house and that has probably helped you build a tremendous amount of wealth by investing, your excess cash, and feeling more and more secure as each year goes by as the house as a percentage of your net worth grow smaller

25 years that went by in the blink of an eye, I remember buying our house like it was yesterday. Fortunately, we bought the right primary for us, in our city, in 2001. I always thought we would “upgrade”. Instead, we have found our 2,800sqft is already too large for 2 people. So, an “upgrade” never happened. It is actually very difficult to find a very nice, very high-end house that is not also big square footage in our market’s top locations. No-one ever builds a 2bed/2bath, 2,000sqft “Carrara marble & oak” palace on a 5,000-10,000sqft lot w/ a pool is what I am saying. 3,000-4,000+sqft is just more house to maintain with zero additional benefits to us. In fact, bigger house really just means bigger property taxes, and all that money that could have gone to more house & more taxes has been saved & invested, just as you predicted.

100% the key to building wealth is to start early and stay focused. Easiest thing we ever did, but it took 15-20 years to do! We decided (at ages 27 & 29) that my wife stay focused on paying our monthly bills and I stay focused on building our total net worth. This dual focus approach really made it happen much faster than I ever imagined it could. So, step one, most importantly, marry the correct person!

Hear, hear!

You’re totally right about not needing an even bigger house as well. In fact, the offset is more true.

The best time to own the nicest house you can afford is when the kids are still at home. It’s not like you’ll want to upgrade to an even bigger house with just the one or two of you.

The time is truly gone by so quickly. I was asked by Business insider to include some childhood pictures and Mang, going down memory line really was a bit melancholy. I remember 30 years ago like it was yesterday.

This is such great advice! We rolled some equity we had with our first home to purchase a $300k home we live in now in Charleston sc in 2017, borrowed just $160k and owe $110k now and the house is worth around $650k. If is small but in a good neighborhood and we love it! Our Net worth in our late 40’s is $1.8M and we are so glad more of that net worth is in investments and not in home equity. If we bought a house to our income we would have much more home equity but far less invested assets in other areas like stocks and precious metals. Thanks for all the great advice over the years, Sam! Your the best!

Excellent point Sam! This is the classic distinction between liquid net worth and net worth. LNW is what matters to feeling rich. How much do you have, in a matter of days, not weeks or months, after paying related fees/taxes/penalties? This is what is really crucial for the “feeling”.

I also like your 20% rule, it means I should find a much larger house!

You plug Fundrise a lot, I’ve been concerned it’s not the same as owning shares and won’t see any similar gains. This research I did on the Innovation Fund looks encouraging, I might dip into this fund gradually with some skepticism.

Top private firms like OpenAI, Anthropic, and SpaceX worry that certain investment structures—such as SPVs or tokenized vehicles—could unintentionally make them “public” under SEC rules by pushing them over the 2,000-shareholder limit set by Section 12(g) of the 1934 Act.

The Fundrise Innovation Fund avoids this issue because it is a publicly registered investment company under the 1940 Act (similar to a mutual fund). For legal purposes, it counts as one shareholder of record on a company’s cap table, no matter how many individuals invest in the Fund.

Additionally, it is structured as a Regulated Investment Company (RIC) that must stay diversified—no single investment can exceed 25% of its assets. This ensures it isn’t treated as if its investors directly hold shares in any one company.

In short: the Innovation Fund, unlike SPVs or tokenized vehicles,

does not increase a private company’s shareholder count,

does not threaten its 12(g) exemption, and

is not designed to concentrate ownership in a single issuer—

so it avoids the regulatory risks that concern companies like OpenAI.

Indeed. I’ve been very focused since 2023 to figure out a way to invest in private AI companies to ride the AI investment thesis and to protect my children from AI taking away their jobs in the future.

I’m thankful that Fundrise has been a long-time supporter of Financial Samurai and that they launched the Innovation Fund at the end of 2022 as a way to gain access to such companies. Until then, I was only an investor in closed-end private funds with usually $200,000+ minimums and zero liquidity.

So far in 2025, I’ve invested about $400,000 in Fundrise’s venture capital product, and plan to continue dollar-cost averaging. I don’t see why OpenAI, for example, can’t double in valuation to $1 trillion in the next 2-4 years. Databricks, Anduril, same thing. But of course, there are no guarantees.

I will not miss this AI investment trend, mainly for the sake of my children. I will allocate about 20% of my investable capital to various private funds, including Fundrise.

Here’s my conversation with Ben Miller, CEO of Fundrise, about the acceleration of AI on Apple if interested.

Someone who is in his early 50s and has $2M in primary residence equity and $1M in liquid investments. Due to unforeseen circumstances, I am unemployed with only a small gig paying $30K a year. Given the circumstances, is it better to sell and rent for now till the finances are stabilized?

Depends on the carrying cost. Once you sell, you probably won’t be able to get back (or not to the same value home at least). And if you struggle to get a full paying job again (the risk for us in our 50s), you might not qualify for a new mortgage.

How optimistic are you about prospects in your profession, perhaps after the tariff uncertainty settles down? I’m in tech, so a job loss might effectively translate to retirement, so I will plan accordingly.

Thank you for your response. I am not very optimistic about my profession (not in tech). I am fine with renting for the rest of my life if that is needed to be able to keep paying the bills until I’m 100.

Another option could be selling and buying a much cheaper property. If, for example, you bought a $500-600k house that would likely make you feel a lot better about your circumstances.

Yes, that’s an option too. I will need to do the math to determine how much I can generate in returns from the remaining deployed cash and whether that’s sufficient to cover my bills.

I’m often puzzled by the “20% of net worth” guideline for homeownership. I understand the basic idea, but does it refer to the home’s total value being limited to 20% of your net worth—for instance, a $2 million house if your net worth is $10 million? Or is it about capping your equity in the home at 20%, so you could own a $5 million property with a $3 million mortgage (leaving $2 million in equity) and still align with the rule for a $10 million net worth?

Home’s value. $2 million home, $10 million net worth provides comfort, with or without a mortgage.

A long time ago, this entire concept was simple explained by one word: “farmers.”

Many of our ancestors were land rich, yet dirt poor, because the only thing America had was space, and lots of it. What people don’t understand is that money is only worth what it can buy. You can’t eat it! And without real skills, physical goods, a way to produce anything…the money isn’t worth anything.

Good insights! Reminds me of this post: The Best Way To Stay Rich: Turn Funny Money Into Real Assets

Only about 5% of our net worth is liquid. The rest is tied up in real estate (primary home (20%) + lot for future home build (25%), retirements accounts, 529s, and HSA. This keeps our backs against the wall. However, we don’t feel poor. That’s all mindset. As we stand now, at 20% for our primary, it feels like that’s living too small and keeping things too close to the vest. At completion next year, the new build will be around 66% of total net worth, or 46% of total (if you go by equity). I will look forward to getting that down over time. We’re 46 and 40. Hopefully, in 20 years the home is worth 4M out of 15M+ NW. That would still be 26%, though. Oh well. We’ll suffer through.

Let us know how you’ll feel once your home is done! What is your net worth now?

Almost 3M. I’ll never feel poor, since I only compare myself to the 25-year old me that had a negative 185,000 net worth.

Nice work climbing out of that hole!

If you will never feel poor, you might be more easily content. I was the case and left with about $3 million at age 34 because I felt lucky and felt like I had enough. That’s about $5 million in today’s dollars.

You think you might end up retiring early instead and forsaking the $15+ million in the future?

Time will tell. I don’t know that I’d ever fully retire. I’d like to work 10 months out of the year and hang out in Spain 2 months of the year in the future. We will see.

We purchased our home for $320K but the value has increased to $1.2M, so it made us feel extra wealthy on paper but simultaneously increased our illiquid percentage. We have over $1M in investments but 80% of that is in retirement accounts. We feel wealthy but I suspect we’d fall in the poor millionaire category.

Sam, just a thought for a future post as I know you have kiddos that are the same age as my own: how do you respond if your kids ask how much money you have? My eldest (7) is very entrepreneurial and interested in money. My answer has always been “we have enough money” but he’s growing impatient with that answer. I love his passion but fear he’ll grow up entitled or telling people we’re millionaires. I’d be curious to hear your thoughts on the topic.

lol I totally relate to this! Our 5 year old started to ask us how much money we have – I also told him we have enough but he’s pretty persistent:)

Amazing property return! When, where, and what did you buy?

My kids haven’t asked us how much money we have yet. We just talk about saving, working, and investing to beat inflation, so far. Just the other day in the car to school, I told him that we invested $10,000 into his investment account in April during the tariff debacle. I’m not sure if that was wise or not, but the numbers are at least normalized as I explained why I did so. So maybe that has given him enough info not to ask how much money we have.

I just try to explain economics and investing to them in day-to-day conversations.

I had the same dilemma at home, my son kept asking how much money I make. So one day, I posted my Schwab IRA statement on the fridge showing a balance of $0.03. I told him, “That’s all I’ve got. Everything else goes toward food and clothes for the family.”

A few months later, while we were vacationing in Hawaii and staying at Hapuna Beach, he noticed construction on a new home next to the resort and asked, “Dad, can you buy that with your three cents?” I told him, “Almost there… maybe next year.” Then he offered to use his piggy bank money to help me buy the beach house.

I think your primary home has at least as much to do with psychology as finance. I live in a city where it’s very expensive to purchase an apartment and moderately expensive to rent. From a purely numbers perspective, the main pull towards ownership is because prices keep going up.

My wife grew up with low-income divorced parents who constantly moved. As a result, she always wanted to own her own place. My family moved once growing up, from a smaller single-family home to a larger one. Though I lived in a number of apartments in my 20s and 30s, I never had a sense of housing fear. I would have been content to rent more or less forever as long as I felt our money would do better elsewhere.

She convinced me to buy a place in mid-2021. At that point we were worth about $1.4 million and we bought an apartment for $1 million. It’s a great apartment and we intend it do be our forever home. My wife wanted to buy it for cash because it would give her a sense of security. I wanted to take as large a mortgage as possible because I was convinced our money would do better invested in the S&P over the long term. We were only able to get a mortgage for 60% LTV so had about $1 million in liquid investments and a $1 million apartment with $400,000 in equity. Since then the real estate market has shot up. The apartment is now worth about $1.85 million and we have $500,000 left in the mortgage, leaving us with $1.35 million in equity. Our other investments are now at $1.8 million and we make about $200,000 per year.

According to a dry evaluation, we own far too much home. But we love the apartment and we all derive a lot of happiness from it. When we look at our net worth, we ignore our primary residence. I hope to FIRE within the next 2-3 years, and we prepare our numbers very conservatively to include the mortgage.

Home comprises 16% of total assets. I live in a slightly lower real estate city market compared to Vancouver (something like San Francisco or NYC) and Toronto. However over 100,000 more people have moved into our city in past 12 months which has until recently, pushed home prices up in past few years. Only know 1 person who has 2nd home as vacation home. Everyone else does live in their own paid for home. No one else has bought a 2nd place.

Late in life to seriously pay attention to building liquid investments. Not until 17 yrs. ago meaning in my late 40’s. Partially because earlier I had lived in another city in my lst home where paid mortgage, then sold before relocating to another province. Simply lucky to barely make just few thousand when sold.

To make long story short, I’m in a better spot.

Sure am aware of some poor seniors who had a valued, fully paid home years ago but living low-income. Enough of them in Toronto and Vancouver. If not also in my present city.

We have our home that we have owned for 25 years at 5.74% of assets and non-income depreciating assets at .24% of assets. No debt. Don’t feel wealthy but do feel financially independent/secure. 94% of assets in marketable securities and just .24% of assets not working for us whether by being income producing and/or appreciating. We could purchase a larger home but being empty nesters don’t need the space we have now. Could purchase second home but rather rent and have the flexibility of where to go for vacation. Being frugal and having simple needs helps in the wealth building process.

I’m surprised you don’t feel wealthy with a home that’s under 6% of your assets/net worth given you have no debt.

I’m assuming you are a millionaire? If so, can you give some guidance on your net worth Range?

What do you think is making you feel not wealthy? Thanks for any insights as I’m trying to offer the best guidance possible for people to feel wealthy.

$9.250 million net worth. $20 million is the feel wealthy spot for me. Another $4.1 million inheritance expected. The real issue is despite the current financial situation and expected inheritance when you grow up feeling poor even though middle class with depression era parents who understandable managed every penny to ensure college education for their kids, you have to overkill the financial side to feel wealthy when you felt financially poor growing up. Age 62 now. However, I do feel fortunate and financially secure just not wealthy.

I identify with this. Home is paid off and only 10% of a 10 mill net worth. Other 9 mill in investments. At 61 and soon entering retirement I don’t feel at all certain we not run out of money. Most software says we will be fine spending about 200k a year, but all have a ton of variables and I don’t do well with variables.

You’re spending too much on unnecessary sofrware.

I think once you have 100% time freedom, you will feel wealthy. You’re also going to discover that supporting a retirement lifestyle is CHEAPER than you expect. The freedom more than makes up for a loss of income.

9M/200k = 45 years. If your non house assets just hung with inflation so you could pull an inflation adjusted 200k each year, you’d make it to 106, and still have the home for 5 more.

This seems to be a “you” problem. If you don’t already have enough to feel wealthy now I’m afraid you may never feel that way.

Thanks for sharing. I guess it’s different strokes for different folks. I felt wealthy with $3 million in 2012 (~$4.8 million today after inflation), so I left work behind.

How do you know you’re expecting a $4.1 million inheritance, and from whom? I don’t like thinking about inheritance at all. It’s an uncomfortable feeling and I expect nothing.

I hope you will feel wealthier sooner. Are you retired or working?

Not sure I ever wish to feel wealthy, just wish to be wealthy and have some level of generational wealth for my 2 daughters.

Doug & ASH01, My 2 cents, admittedly worth less than that…

Using Doug’s numbers, because you two seem close enough in levels…

Forget the inheritance piece for now, it is not real until you have 100% control of whatever is left after reality strikes.

What am I missing? Short of a drug, gambling, or massive spending problem, you seem to currently have about $8.7M available, beyond your primary residence. $8.7M should be throwing off about $392,000/year @ 4.5%, more or less risk free. That is money paid to you monthly if you get out of bed or not, it is of course, also taxable. But, that means you can spend (including tax bill) over $32,000/month, every month, for the rest of time, and your current net worth will stay flat (or go up! if the house appreciates). So even if you live to be 150yo, this leaves your entire net-worth as generational wealth already available to transfer to your daughters/whomever. Fact is your spending will go down as you age, not up. You will become less active, not more active. No matter how much the last 3-6 months of your life costs in medical bills. So, some portion of your $32k monthly income will also continue to compound, forever….you are ~62yo.

You officially have the Universe’s permission to enjoy what you have built, so please do.

The only definition of wealth I ever heard that makes any sense is this: Wealth is the ability to do whatever you want, for as long as you want, with whomever you want. All the rest is BS.

If you can’t “feel wealthy” with no debt, and effectively a $32,000/month lifetime annuity already in your hands, then there is no number. Why even mention $20M, make it $100M, make it $1B…it won’t matter. Figure out your spending, do the math for yourself, and go forth with confidence. It’s not that complicated, and none of us are going to live forever.

The only thing you are missing is that randomly posting their net worth for others to see is what gives them a nice tingly feeling. If that is what it takes then we should let them do it with no questions.

Hi. At the end of 2024 we moved from North Carolina to Alabama to live in the same city as our daughter and grandkids. We sold our home and paid cash for our home in AL. It is 12.6% of our net worth. We are both retired and underestimated the lack of social life in rural Alabama. We are considering buying a condo in Destin, FL where I grew up. Our price range is 250 to 300k. I plan on using a credit line against one of my brokerage accounts that is a little over $1.3 million. Is that too risky? Can I spend more? We plan on using it part-time but will try to rent it when not using it. I am not expecting to make money but hope to offset insurance and HOA costs. Our overall net worth is about $3.4 million. I am 59 and my wife is 65. Any input is appreciated. Thanks!

Relocating and purchasing a $300,000 home at $3.4 million net worth is not risky at all, even if you borrow.

The condo could decline by 50%, and it would do nothing so negatively affect your lifestyle.

But if you want to discuss in more detail, check out my personal finance consulting page. It’s hard to give specific advice without knowing more.

Technically we are rich millionaires- primary residence is 19% of net worth, but I still feel like a poor millionaire since the ‘liquid’ part of our net worth is in stocks, ETFs, and retirement accounts. In other words, I don’t have as much truly liquid cash as I think I need to feel like a rich millionaire. I’m 54 and have just come to accept this feeling.

Can you share your net worth amount? I’m assuming the closer you are to a $1 million net worth, the less rich you feel relatively.

But having about 81% of your net worth that can be easily sold in case of emergency should provide relief.

Total net worth $12m. Between our primary residence and vacation property we have roughly $3.5m in real estate. This is mainly a psychological issue because I tend to view things through the lens of liquid cash, meaning when I have a good amount of cash I feel rich, but when I don’t have a lot of cash I feel like a poor millionaire!

Sam

Longtime follower, and occasional poster to your comments section. I have been a big fan for a long time. This article hit home for me.

In October of 2020, my wife and I purchased our dream/forever home (we wrote the sellers a love letter and we try to always follow your guidance as best as possible). At the time, we had 2 daughters in highschool and one in junior high. It was the height of covid, and we locked a 30 year fixed at 2.5%. We currently owe 419k on this mortgage, the home value is probably 1.1m.

Other than our home, we are pretty frugal. I am self employed. My wife is a teacher. We have no other debt (cars, credit cards, etc). I have paid cash for all three of my kids to attend school in our home state. The youngest, will be done in May 2028. Our networth is about 3.5 million. This includes 3 paid off single family rental homes and a small (850 sf) office building. Quick math tells me, my principal residence is 31% of my networth. I am heavy real estate. My retirement funds (pre tax and after tax brokerage) are approximately 900k of my networth. My wife has Public Employee Retirement Account (PERA) that will be available to her in about 6 years. We are both 50 years old. I cannot seem to shake this uneasy feeling of being so illiquid and nearing retirement. The rentals cash flow, my wife has an average income, and my income is pretty solid right now. However, reading this, makes me realize that if I had more liquidity in my networth, I’d sleep (better) at night. Thank you, once again, for coming through with a great article at just the right moment.

Jim

Jim, you’re welcome! Great to hear from you and thanks for being a longtime reader. You’ve done an amazing job — paid off rentals, a dream home, no debt, and all three kids’ college tuition covered. That’s the kind of financial foundation most people only dream about.

At this stage, it’s more about fine-tuning for peace of mind and freedom. You’ve clearly put in the work, and you can always raise liquidity by selling off some assets. But since you and your wife are both working, you might as well build your liquidity through increased savings. Gradually, that uneasy feeling gets better!

Thanks again for sharing your story.

I retired 4 months ago a couple years after selling my tech business to a PE backed IT firm. My family is about $5.5M in net worth with zero debt. I just checked and our primary home is 15% of net worth. We’re planning to purchase a second home soon in a tax favorable WY and establish tax domicile there because I still hold a “small” equity position in the company that bought mine. That position is currently worth about $750K. We currently live in WA and there’s a new excise tax that would add 9.9% in addition to the federal 20% and the federal 3.8% “windfall tax” for a whopping 33.7% tax hit probably within the next 2 years when PE sells the company. We can’t avoid the 23.8% tax, but the 9.9% would be add $75K at current valuation (which could could lower or much higher). We intend to hold our WA home and the two homes combined value would be 25% of our net worth. We also have a rental home that generates $20K annually after taxes and insurance, so theoretically that would cover the mortgage payment on the new house after a large down payment. We listened to your latest podcast with Bill Bengen on the drive home yesterday – it was great and very reassuring!

Thanks for sharing your story and for listening to the podcast with Bill Bengen. Sounds like you’ve made some excellent moves! Congrats on selling the business.

Having only 15 percent of your net worth in your primary home is low, and holding two homes at 25 percent still keeps you diversified while giving you flexibility in where you live.

I don’t blame you at all for looking into Wyoming for tax reasons. That extra 9.9 percent in Washington is tough to swallow, especially when you’ve already got the 23.8 percent federal hit coming. Sounds like you’re thinking several moves ahead, which is exactly what experienced business owners tend to do.

I just wonder whether you’ll be able to adjust to a new environment at this stage in life. Have to find new activities and friends. It could be easy or maybe it won’t be.

Honestly, we’re looking for a slower pace. We really enjoy hiking, kayaking and being outside. Our WA property is fantastic and on 7 acres next to wetland area and nature preserve. It’s also only a 15 minute drive to “civilization”. Our visit to Montana and Wyoming last week was amazing. Absolutely stunning beauty. Yellowstone was awesome and hardly anyone there this time of year. I’m excited about a new adventure and living 7 or 8 months in an area I’d never even visited before. A friend from college just moved there and she recommended my wife and I check it out. She wasn’t wrong! We lived in Santa Barbara for 11 years and moved back to WA. We’ve been here for 21 years. Time for a change – YOLO! Plus, we can afford to keep both properties so we’re free to go back and forth (as long as we’re domiciled in WY for 183 days a year. We’re planning to visit relatives in Germany and visit Spain and Portugal in 2026 (hope to see the total eclipse in August 2026). We’re never bored, always keeping busy. And Cody, WY is a major tourist destination in the summer (we’re looking at Powell, about 25 miles east. You should check it out – a hidden gem!

We are poor millionaires because we have all the liquidity zappers – over 90% of our NW is tied up between our home, venture capital funds, rental properties, qualified retirement accounts, and 529 accounts. I don’t mind it because illiquidity has prevented us from overspending on other things (inevitably, whenever we have a liquidity event, even a great bonus year, the money gets spent); however, I am focused now on building up a taxable brokerage account so we can retire within the next 5 years. I will feel comfortable once we have $3m liquid between a taxable account and other cash equivalents.

Liquidity certainly does have its benefits of staying put and investing for the long term.

Thanks for reminding me of this post I wrote, which I will now update: Higher Returns With An Illiquidity Premium

This makes total sense. I definitely have felt more at ease over time as my home has taken up less of my overall net worth. My anxiety also tends to go down when I am more liquid and running higher on cash and vise versa. I try not to sit on too much pure cash so that it can work for me but there definitely is a balance especially when unexpected expenses pop up.

Sam,

I wonder how many “poor millionaires” have pensions? Using your tool to calculate their value and adding to net worth changes things dramatically for millionaires with net worth under $3 million.

Also, not having a mortgage is a huge rock off your back. Expenses for owning a house drop dramatically and you reach the minimum passive income threshold at a much lower value. That has a positive psychological impact as well and makes you “feel” rich (or at least comfortable).