A forced savings account will help make you rich over time. It forces you to save versus relying on your own discipline to save. A mortgage is exactly this, a forced savings account where the homeowner pays down principal each month and builds equity.

One of the main reasons why the average net worth of a homeowner is 25-40X greater than the average net worth of a renter is due to forced savings. People think they can consistently save and invest the difference while renting. The reality is, unless the savings is forced and automatic, it's hard to sustain the discipline.

There are simply too many temptations and too many “emergencies” to spend our free cash flow on. This “economic leakage” acts as a huge drag on wealth creation over time. As a result, I believe investing in real estate is the best asset class to build long-term wealth for the average person. The combination of rising rents, rising property values, and paying off debt is powerful.

Recommendation: If you're looking to invest in residential and commercial real estate passively, check out Fundrise, my preferred private real estate platform. It focuses on residential and industrial properties in the Sunbelt, where yields are higher and valuations are lower. I've invested over $500,000 in Fundrise products so far, and they've been a long-time sponsor of Financial Samurai.

Mortgage As A Forced Savings Account Builds Wealth

Back in 2000 and 2007, many investors were cocky, much like investors were in 2021. Then, of course, a bear market wiped out tremendous gains, reminding my why I prefer real estate over stocks.

I remember asking my Director at the time what he thought about the concept of the mortgage as a forced savings account? At the time, as an investor, it appeared he could do no wrong.

He said, “I don't need no forced savings account. Only irresponsible people who don't have the discipline to save every month would consider their mortgage as savings. I'd rather have as big of a mortgage as possible so I can make money in the stock market!“

My Director ended up losing millions when the dotcom bubble collapsed. He no longer looked down on people who slowly grew their wealth. At least, unlike most people, he had millions to lose!

A traditional mortgage that pays down principal and interest “forces” you to save. Simply, if you want to keep your property you are forced to pay your mortgage every month. A percentage of each mortgage payment goes towards principal, which can be considered savings.

I'm also in the camp that it's better for most people to receive a tax refund. Although it's like giving the government an interest free loan, because most people can't save for crap!

A Forced Savings Account Saves You From Yourself

After paying off $460,500 in mortgage debt in 12 years, I've had time to reflect on whether a mortgage can really be considered a savings account. If this rental property was all I had, I'd be considered “house rich, cash poor” because my ratio of home equity to liquid cash would be around 10:1.

The reality is my physical property portfolio accounts for less than 50% of my total net worth if I exclude my online business. If I include my online business as part of my net worth, then property accounts for less than 25% of my net worth. Contrast this to the average home-owning American who has a scary 80% of net worth in property.

Let's ignore my property's appreciation over the past 12 years. Instead, let's solely focus on the $460,500 in debt I paid down compared to whether I would have been able to save $460,500 during the same period. The easiest comparison is principal pay off vs. 401k savings.

401k Versus Savings

If I maxed out my 401k from 2003 – 2015, I would have saved $204,500. That's exactly what I did. Remember, the maximum contribution limit in 2003 was only $12,000. It slowly rose by $500 to $1,000 increments to the current $23,000 maximum in 2024.

Contributing to a 401k is just as easy as paying a mortgage once you make 401k contributions automatic. The money is deducted pre-tax from your gross income so the hit doesn't feel as bad and you never see the money in the first place.

The issue is, saving $204,500 in my 401k is still $256,500 less than the mortgage debt I paid off during the same period. Even with stock market returns, profit sharing, and company matching, my 401k only grew to a little over $400,000.

Where did the rest of the money go?!

This is the question I think most people have. We spend years making all this money and wonder why we don't have much money to show for all our efforts. Ever wonder where all the cash you withdrew from the ATM went? I do!

The simple reason for not being able to accumulate wealth as prodigiously as expected is because money is like water. We're a leaky ship sailing through an unpredictable storm. Some expense or desire always seems to come up. As a result, most people don't end up saving as much as they should or think they can.

A mortgage as a forced savings account protects you from spending your excess cash flow on wealth-destroying items or experience. You may do so intentionally as you wish to enjoy life to the maximum. But for most people, their money simply disappears over time due to a lack of discipline.

We can plan all we want for how to consistently invest our savings and financial windfalls. But because life has so many distractions, we just don't do so consistently. If you want to make big money, you must consistently invest aggressively, which is why I have an auto-debit each month for an open-ended venture capital fund I'm investing in.

Whole Life Insurance Is Like Forced Savings Too

If you've ever considered life insurance, a whole life insurance policy is also like a forced savings account. The premiums are higher because you're building “cash value,” like home equity if you purchased a house. Over a 20-30-year period, your cash value will grow, providing you financial security and liquidity if necessary.

In other words, you can make money from a whole life insurance policy. Conversely, a term life insurance simply expires once the term is over, leaving you with no equity.

A Mortgage Is Dumb And Easy At The Same Time

A mortgage really does save people from them selves. I'm not sure if there is any better forced savings account than having a mortgage.

Below is a chart that shows the value of a rental property I own and the mortgage value. Notice how the mortgage was eventually paid off about 12 years of ownership. I didn't pay down too much extra principal.

Most people responsibly pay their mortgages through the good and bad times. If you don't, your credit gets crushed and you won't be able to borrow at normal rates for years. Then, you'll ultimately end up losing your downpayment and perhaps more if you purchased in a recourse state.

Given the bottom 90% of Americans have had an average savings rate between -3% – 5% over the past 20 years, it's clear that most Americans don't have the capacity and/or discipline to save. We're bombarded with aspirational ads that make us want to spend.

Further, we compare ourselves to our neighbors who make us feel less worthy unless we spend as much or more than them. Credit cards make instant gratification so much easier. And the vast majority of car buyers spend way more than 1/10th of their gross income on a car.

Saving money is hard because society makes spending so easy!

Of course there's no free lunch given a mortgage requires an interest payment. But statistics don't lie. The net worth of homeowners is about 40X greater than renters partly because of the forced savings component of paying down principal. The other reason is obviously the appreciation of property over time, even if the appreciation is just due to inflation.

It's hard enough to save an amount equal to the amount of mortgage debt being paid off. It's even harder to save an amount equal to the total value of the property's equity thanks to capital appreciation.

What started off as a $120,000 downpayment has now turned into a paid off asset that if sold, would provide over $1,000,000 in cash after commission. I almost don't care about the 730% increase in equity from the initial downpayment. All I care about is that 12 years later, this property is a wholly owned asset in my portfolio.

If you don't have the down payment to buy a property yet, check out Fundrise. Fundrise is a private real estate manager that manages around $3 billion. Its investments are mainly in the Sunbelt regions where valuations are lower and yields are higher than in the coasts. I've personally invested over $300,000 in Fundrise to earn more passive income and diversify my holdings. Fundrise is also a long-time sponsor of Financial Samurai.

The Mortgage Payment Expense Declines As A Percentage Of Income Over time

Another wonderful think about having a mortgage is that it generally has a fixed rate for the life of the loan. Even if mortgage rates surge higher, as they did in 2022 – 2024, the homeowner's mortgage payment stays the same.

Meanwhile, as the homeowner tends to earn more money over time, their mortgage payment as a percentage of income gets smaller and smaller. With a smaller percentage, there homeowner feels less financial stress and more financial security. If you got an adjustable rate mortgage right before the pandemic, there's no urgency paying it down either because your principal balance will be lower upon reset.

In contrast, the renter likely has to pay ever-higher rents over time thanks to inflation. Finally, the home value as a percentage of net worth declines as well as the homeowner gets wealthier. As a result, the home also feels like less of a financial burden.

Make Savings Automatic With A Forced Savings Account

Many renters like to tell me that they “invest the difference” by not owning. It's a good idea in practice. Yet, we all know the temptation to splurge tends to derail us from financially wise decisions. A mortgage truly is a forced savings account that has helped many middle class people build wealth over time.

Whether you pay your mortgage, contribute to a 401k, enact a dividend reinvestment plan, or invest in an after tax investment account, make your contributions automatic. If they aren't automatic, it's just way too easy to cheat by contributing less or not contributing at all.

A mortgage as a forced savings account is the best thing ever. It feels great knowing that usually within 30 years, you'll have built up a tremendous amount of savings through home equity.

Invest In Real Estate More Strategically

Real estate is my favorite way to achieving financial freedom because it is a tangible asset that is less volatile, provides utility, and generates income. Stocks are fine, but stock yields are low and stocks are much more volatile.

The combination of rising rents and rising real estate prices builds tremendous wealth over the long term. Meanwhile, there are more ways to invest in areas where valuations are lower and net rental yields are higher thanks to crowdfunding.

Consider Fundrise, a platform that allows you to 100% passively invest in residential and industrial real estate. With over $3 billion in private real estate assets under management, Fundrise focuses on properties in the Sunbelt region, where valuations are lower, and yields tend to be higher.

I’ve personally invested over $500,000 with Fundrise (my investment dash, and they’ve been a trusted partner and long-time sponsor of Financial Samurai. With a $10 investment minimum, diversifying your portfolio has never been easier.

To increase your chances of achieving financial independence, join 60,000+ readers and subscribe to my free Financial Samurai newsletter here. Financial Samurai began in 2009 and is the leading independently-owned personal finance site today. Everything is written based off firsthand experience.

Another big factor here is that you lock in a monthly payment. The P&I on our 20 year mortgage was around 25% of our gross income when we first purchased. 15 years later after raises, promotions and job changes the P&I remains the same but is now roughly 10% of our gross income. Renters have to contend with semi regular increases.

It is beautiful the payment as a percentage of income and the home as a percentage of your net worth becomes smaller and smaller overtime.

Having a mortgage does help with financial discipline! I have my automatic monthly payments include extra principal to keep myself disciplined. After I refinanced, I increased my principal amount on the auto pays too. I’ve never regretted paying down a little bit extra each month.

I was not feeling totally doomed about my home going into foreclosure. After reading these comment, looks like I may as well give up.

My husband and I built our house in 2004 with a construction loan, which we had to refinance once built. We refinanced and had a mortgage of about 350,000, Lender convinced up to borrow up to the value of property for my husbands business (General Contractor). We got burned with a Revere Interest, thought we had a 4.5% rate, found out 3.% was also being added back to the mortgage so we were paying 7% and our principle was going up!

Used the money to purchase 2 lots to build 2 homes. Had a plan of 2 homes a year to pay down the mortgage. One house partially built, bubble popped in 2008, buyers pulled out in fear, had to use the money slated to build the second house and finish the first one, to pay on the mortgage. My husband now had no income.

Lost about $120,000 on the house we started, had to sell it for $35,000 to pay taxes as not to loose our other land we had bought and paid for 20 years prior.

Got a loan modification (2011), lender put a $50,000 balloon at the end. Payments were $2500.00 interest only. (Adjustable)

Fast forward (2016) payments just went to $4000.00, we are unable to do this any longer. Tried to hold on to the house to see if the market went back up and sell.

Havent been able to make the payments since July 2016. Forclosure starting

Dec 31 2016. So it sounds like, I am in a non-recourse state (AZ), but my modification will cause it go be a recourse. I will loose my land, Only have one vehicle, my employer provides me with a vehicle. My husband has cancer and is trying to do small jobs to contribute. So I may be seeing my wages garnished?

I am 58 and was hoping to retire in 10 yrs, doesn’t look like that will happen now. Any advice?

.

[…] Be under no illusion that you will make money off your property for at least a decade if you buy. The only thing that’s probably going to help build your net worth is some good old forced savings. […]

[…] Mortgage as a Forced Savings Account to Build Wealth by Financial Samurai. An interesting way to think about your mortgage is as a savings account that you absolutely have to put money into. An upside to buying a house is that your asset will probably appreciate as you’re saving, but the downside is that your savings account probably isn’t very liquid. […]

[…] if you end up paying off your $1.2 million house within 30 years through forced savings, you’ll end up with at least $1,000,000 in cash after commission and taxes. With the $1 million […]

I think ultimately it all boils down to the question whether one is disciplined in saving or not. Fully agreed that a mortgage can be a fantastic way to commit yourself to saving.

That said, I personally have never had problems with savings discipline. My savings rate has gone up over the years as I earned more income and has now reached 50-60%. I do not own property because I live as an expat in Belgium, where one-off fixed costs of buying a home are huge (15% of property value) and I cannot say with any degree of certainty whether I will still be here some years down the line.

When one has a disciplined approach to saving, however, I find many of the usual claims made for home ownership (some of which are reflected in the comments here) rather odd. For instance, the statement “I buy property because I don’t want to pay off someone else’s mortgage” doesn’t make much sense. Once one considers opportunity costs (the fact that money invested into real estate cannot be invested anymore in alternative investments), it is pretty clear that you are not “paying off somebody else’s mortgage”.

Living in a home is CONSUMPTION, whichever way you put it. And it costs. Now one can purchase the property one lives in as an investment, and that’s just fine. But from a financial perspective the question only is whether the investment into the property will yield a higher return/lower risk than alternative investments.

I will likely purchase a home sooner or later. Essentially for the following reasons:

(a) Diversification to have less exposure to the stock market

(b) Reduction of risk

(c) It will feel nice and warm that the house is “my” home and I can do with it whatever I please.

That said, this purchase will likely only come in a couple of years, when I hopefully have a family and hopefully am financially independent (or very close to it).

Without family and with a net worth below financial independence (as now), the risk/reward profile of real estate is not overly attractive in my view. At least in Belgium, property prices are currently such that you can get a decent return on investment only if you leverage substantially, which in turn makes the whole thing a lot more risky. In short: I will stay with a net worth allocation quite heavily tilted towards stocks for now. But I’m also looking forward to buying real estate in the future once I have a family to fill the house.

This is an interesting twist. And I agree with it. Of course, it assumes that your home is an investment. I don’t, but I do consider it a ‘back-up, emergency, worst case scenario investment.’

Your idea is also a great concept for rental property. Who cares if the cash flow is break even or even at a slight loss? The renters are paying down your mortgage.

By the way, I constantly get into arguments with people who say that real estate is a bad investment. They say real estate only returns 4% on average per year historically, and that stocks return 9% or 10%. Let’s say that is true. No one, except the very rich, pay all cash for a house. Almost everyone puts down 10% to 20%. Yet, for stocks, not many people buy on margin; they put 100% down. So looking at these two investments from an original cost standpoint, and assuming a conservative 20% down for real estate, the return for real estate historically on average is 20% per year.

That’s correct from a leverage standpoint. Eventually, I think we should all pay our properties down by the time we no longer want to work.

Good point on getting a renter to force save for you.

Sam,

I like the photo you put on this post!

“Saving money is hard because society makes spending so easy!” – this is so true. It can be way too easy to spend. It’s sad that some people flock to casinos on pay day and others get so caught up in material wants that they get super buried in debt.

Having a mortgage has definitely helped me be more disciplined with my money, but I wouldn’t say I was reckless without one either. I know someone who has a mortgage and has always paid on time, but has gotten into bad financial shape using her heloc way too much. Having that credit line has done bad things for her finances. I wonder if she never had one in the first place if she would be much better off because she was always good at making mortgage payments.

Ah yes, the dangers of a HELOC. I need to write about that in a future post.

I haven’t been tempted to use one b/c HELOC interest rates are much higher than normal mortgage rates.

Graduated 3 years ago and still renting. I guess I am one of those atypical people who has not purchased a home yet while investing most of my savings. I did recently sell quite a bit of stocks for a possible down payment on a house. Right now Seattle housing market is on fire and a lot of the brand new builds are very pricey. Not San Fran like but I am starting to see $500/ sq foot now which is pretty ridiculous.

Comparing myself with my college friends who have purchased a house. My net worth is triple theirs, and on top of that I started 3-4 years later working. Why is this? My savings % is much higher compared to them. Currently my fiance and I average 65-70% monthly savings. In the long run however I do plan to buy a home. Personally do not feel great about trying to purchase a house during a bidding war in Seattle with 100-200k over listing prices.

It’s all relative. $500/sqft sounds dirt cheap here in SF!

I wouldn’t say not buying a home 3 years out of college is abnormal at all. I think the average first time home buyer is closer to 30.

I personally look at a mortgage as just another bucket for money to flow. I of course maximize all my tax advantaged accounts first before I throw any additional principal at the mortgage.

As we have talked about on your blog before, I have a plan to pay off the mortgage on my primary residence before I turn 35. Today my homes equity only makes up about 16% of my total net worth.

In total Real Estate makes up about 30%.

The goal is to keep Real Estate to 40% or less of my net worth. Long-term I would aim for something around 25%.

Cheers!

Sounds good to me Dom. 25%-30% is what I’d recommend as well.

Mortgages are a necessary evil. You actually give a bank a mortgage, they give you a loan secured by the mortgage…

In investment property, it’s probably a good thing. If not for mortgages, property would likely be MUCH cheaper.

Having said how great mortgages are, I have 5 properties free and clear.

Indeed. Without dual income earners and credit and generational wealth transfers, everything would be that much cheaper. How long did it take you to pay off each one of your mortgages?

While I don’t like getting a refund, I think mortgages as a forced savings works in the US. If everyone automated the rest of their choices (401k, auto savings transfers, etc) and learned to live off the rest, then the -3 to 5% savings rate would be a lot higher!

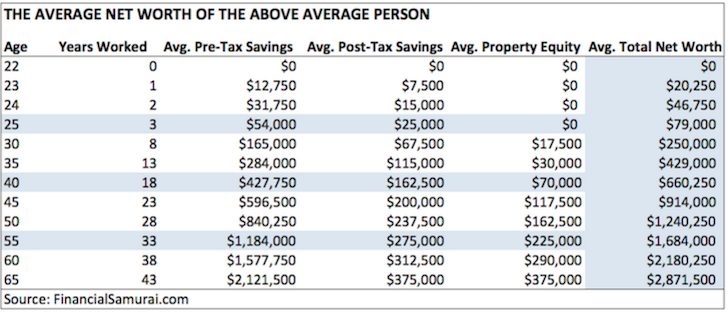

I was surprised that 80% of the average homeowner’s net worth was their house. Mine is about 25% (and falling since my savings rate is quite high recently).

Call it forced savings, call it an investment, call it home.

I don’t care what it’s called as long as I have it.

After a decade or more of paying someone else’s mortgage for them as a renter, I was ecstatic to buy my first property over a decade ago.

I’m fairly disciplined but even I have difficulty sticking to a strict budget and planning every purchase. So anything that let’s me automate my savings and investment is a plus in my book. 401k. IRA. Direct deposit plus automated transfers. And my mortgage.

Given today’s stock markets, I’m glad to have money in something physical that provides me a vital service – shelter.

BINGO Jack! Your comment is spot on.

My perspective changed a lot once I went from renting from 1999-2002 to buying in 2003. But, I’m drinking the gov’t kool-aid b/c I want their subsidies after paying so much in taxes.

If you don’t need the forced savings of a mortgage, I am not convinced buying your own home is the best investment. I own plenty of investment property, but still rent.

I like to live in newer downtown apartments. Every time I move, I look into buying vs renting, and buying always looks to be a gamble.

The downtown condo prices are driven up by people buying the dream, and new buildings go up every year of apartments keeping a cap on rental prices. Rents gross approximately 7% on downtown condos here, but gross closer to 15% on lower end (working class / student class, crime free) housing.

I much prefer to rent and then deploy funds at the 15% growth rate. Easier to sleep at night relying on yield, as opposed to praying for capital growth.

May I ask where you are getting a consistent 15% growth rate?

I guess you do not subscribe to my suggestion of buying real estate for lifestyle and not for income or capital appreciation?

Sorry, that was incorrect. I meant to say 15% GROSS RENTS, not growth rate. These are easy to find in middle class areas are easy to find in the flyover states. Indianapolis, Chicago, Kansas City, etc. The gross rents are different to the cap rates. A 15% gross rents has a cap rate closer to 7-8% long term (or a cap rate of 12% if you ask a real estate agent who doesn’t understand roof replacement, vacancies, etc.).

I like to invest to make money, and rent for my lifestyle. The A-class property I want to live in, just doesn’t yield.

Gotcha. 15% gross rental yield makes sense.

I’ll tell you this though… property becomes MUCH MORE meaningful once you can find a place you enjoy to live. Otherwise, it’s just a cold asset there to make money. And making money gets old after a while.

I’ve been a homeowner for over 20 yrs. You don’t consider the expenses of home ownership in your equations above. Sure, after 12 years you may have built some equity in a home, but you have also spent about 1% of the house price on taxes, maintenance, etc., as well as another 4% on mortgage interest. In your example above, a quick estimate means about 5% a year, for 12 years on a 500k house, that’s around 250k +/- pretty much out the window. So, in order for a house to be a good “investment”, the prices need to rise faster than 5% a year just to break even. If you rented a place for the amount of your mortgage, and dollar-cost averaged the tax and maintenance money, you’d be in pretty decent shape over a 12 year period, and make up most if not all or more of the deficit in your above example. No, it’s not automatic, but I think anyone who is capable of home ownership and automating mortgage payments is capable of automating a savings program.

My perspective after years of home ownership..Buy a house so you have a place you can call home, not as a wealth building strategy.

Have you tried to find a place to rent for the cost of a mortgage? The landlord rolls all of the mortgage, taxes and maintenance into the rent price and still makes a profit. In addition, most of the small maintenance is the responsibility of the renter. I think if you do the calculations with real life examples you will see that there is more financial benefit in the forced savings of home ownership vs renting + savings.

Hi Mike, I just posted a longer response below showing real life examples. Funny you mention rental costs, my wife and I are considering whether to buy a vacation house, versus just renting. When we do the numbers, the price to rent a place monthly all year roughly equals the dividends and interest of just investing the purchase price of the house. It seems many real estate investors look to rent their house to cover the carry costs, write off some expenses, and sell it for a profit as the market price moves up. Again, I’m not saying you can’t build wealth owning a home, I’m just arguing that there’s about 25-30k per year in carry costs (see below) that need to be considered in those calculations.

I definitely don’t recommend people buy a vacation house vs. renting, as a vacation home owner myself. I’ve got a post on this topic in the queue. Stay tuned!

Looking forward to the post!

I agree. Landlords are in the business of making money. If you have a really good landlord and your time is more valuable than his/ her time, then it is probably in your best financial interest to rent; if your landlord is not particularly good or if you would consider it extravagent to hire a person to be on call to take care of maintenance when it arises, it is probably in your best interest to buy. All of this assumes you are comparing apples to apples in what you would buy versus rent and that your housing needs are expected to stay the same for a good long while. The one big financial benefit of renting is flexibility.

I am a homeowner and consider it a good financial decision for me, but I wouldn’t describe the benefit as forced savings. We could have taken out a bigger mortgage on a larger house and had more forced savings, but it would have been a bad decision financially because it also would have been more forced taxes, interest, heating, etc. on something we don’t need. So, I guess what I am saying is that a mortgage *for the sake of* forced savings can just as easily turn into forced waste. What I love about homeownership is the HUGE benefit (in the form of equity) I get from cutting out the middleman (landlord) on a piece of property that is well-suited to my long term needs.

I believe you and Sam agree on the benefit of home ownership then. The HUGE benefit that you call equity, is indeed the same thing that he describes as ‘forced savings’. You are forced to pay that money to the lender, which is actually the building of equity in your home/property.

Take off the “forced” from “forced savings” and I would agree with you. If you keep the word, “forced,” though, it makes it sound like having to pay yourself (in the form of principal reduction) every month rather than having the option to spend that money on other things you might want is a benefit, and I disagree. If I could rent a place equivalent to mine for what I currently spend on interest, taxes, and upkeep (not principal, since that isn’t an expense), I would do it in a heartbeat. In other words, given a choice between (1) housing expenses of $X per month plus a requirement that I personally sock away an additional $Y per month and (2) housing expenses of $X per month with no requirement that I save anything, I would go with option 2–the option that allows me flexibility, even if I know full well that it’s possible I will abuse that flexibility by spending money I really should be saving. In my area, though, nothing remotely close to option 2 is available. Renting (the only non-forced savings option) costs way more than owning because landlords essentially want (and can get) double-profit–long term equity building (principal reduction) plus extra monthly cashflow.

You are correct Rich, which is why I differentiated between trying to save the amount of mortgage pay down of $460,500, and trying to save the total value of the property 13 years later. But, like you said, I don’t include the COST of renting the place. I’ve conveniently crossed the cost of renting the place and the cost of owning the place out.

But if you were to do that calculation now, the cost of renting the place is about $4,000 – $4,400 in today’s market. The cost of owning the place is about $1,000 a month w/ no mortgage due to property taxes and HOA dues. In other words, the annual net rental yield is only about 3.6% – 4.1%, but, that still compares favorably to the 10-year yield of 2.1%, and the potential for such an asset to keep on appreciating.

I think San Francisco is one of the cheapest international cities in the world. Let’s see in 10 years whether this is true or not!

The final key is “investing the difference” is not as easy as just paying your mortgage. The data shows this. And intuitively, we know this.

I’m not saying that owning a house, with a “forced” mortgage won’t help you build wealth, I just think the numbers aren’t always as great as people think going in; partly due to the unpredictability of markets that others have discussed, but also the need to spend money on a house on a regular basis. I built a quality new home just over 20 yrs ago, and there just seems to always be some kind of maintenance that needs money. That doesn’t include inevitable remodeling that occurs long term in a house.

I agree with your 1000. per month value as a “maintenance” allowance. Dollar-cost averaging that over 10 yrs at a modest rate and your talking around 200k +/- which should be realized when calculating the financial pros and cons of home ownership. Let’s add in the interest cost on a modest 300k mortgage at 4% (say, 10k+/- per year average over 10 years) on a 500k house and you’ve just added another 100k in expense. Taxes are going to be another 50-100K over 10 years. All that adds up to around 30k a year for maintenance, some remodeling, taxes, and debt interest. Your house value would have to go up by 6% per year just to break even. Since you do get tax breaks, let’s call it 5% per year break even rate. Since long term, most housing markets move with the inflation rate, unless you’re bringing in rental cash, you’re kind of treading water.

As I mentioned, I own a house to live in and call home, not as an optimal wealth building vehicle.

A big x factor is where you buy, just like what stock you buy. Where do you own?

Absolutely. We live in New England, which has had it’s share of booms and busts the last 30 yrs. We had a real estate bubble in the 80’s many of the country didn’t experience. After 2 of them in my lifetime, you realize anything can (and will) happen!

I think the big mistake people make is assuming that just because the real estate market growth rate was X over the last Y years, that it’s going to continue. Nothing could be further from the truth.

You are dead on. 29 years of homeownership has taught me that all homes become obsolete, and are eventually in the wrong location. When the replacement cost of materials exceeds your sales price, it’s an easy conclusion.

I own a house(s) because I have animals and more than one child, and hobbies, and I detest multi family housing. The same economic problems with ownership apply to small scale landlording unless you’re in a hot location, rents can’t keep up with maintenance, unless you are in the slum business. Ownership is a slight hedge against inflation, but mainly a lifestyle choice.

Maybe it’s my INTJ personality, but I can’t relate to the mindset where home ownership is needed as a forced savings. I got a mortgage so I could invest more money in the stock market, and I actually follow through with that. Other than a small, fixed allowance I give myself for discretionary spending/unexpected expenses, every last dollar remaining after paying monthly bills goes directly into the stock market. By structuring my budget this way, I have incentive to continue finding ways to reduce my monthly expenses. 75% of my take home pay YTD has been invested and I expect by the end of year it will be 80%. To me, it is just simple logical math. My finances aren’t influenced much by emotion, other than I want FI asap :)

It’s not needed, but it’s going to be a nice paid off asset as backup if needed.

How long more towards FI? What wealth amount would allow you to pull the rip chord?

I’m INTJ, too – but have a different perspective. I feel like the most logical choice is to establish multiple forms of forced savings, home ownership included. The bottom line is that regardless of how disciplined we are, we’re still human. There are certain emotional choices that could detract me from savings (not talking about material things, but other choices that might pull at my heart strings but not be in my best interest). I chose a 15-year term because I like the idea of forcing myself to pay it down as quickly as possible (but not at the expense of investing in the market, which I also do). The tax savings are also very real, as is the peace of mind knowing that I’ll be mortgage free on a nice place at around age 40 with passive income to cover expenses. I do agree with you on allocating out savings until you have to live pay check by pay check until you meet your goal.

That’s exactly right BH “we’re still human!” I get lured by things to buy all the time. I’m actually trying to force myself to spend more money now, hence the planned 3.5-4 week trip to Asia (here in Seoul now, thank goodness for wifi).

I KNOW with high certainty, that if I successfully pay off the other three mortgages, regardless of any capital appreciation, there’s going to be a huge accumulated paid off asset. What’s great is that everything is automatic, and paying off those mortgages doesn’t negative affect my life at all b/c I don’t even feel it.

I’m all for having a mortgage. Especially in this low interest rate environment. Young adults need to learn the power of leverage. There is “good debt” and “bad debt”. Of course, the previous commentor is correct, if you coming at the high and unreasonable housing market of 2005-2007, a lot of people are still under the water, and it might look pretty depressing. However, in the longer term – force saving win.

In states like Texas, it’s not a great savings because your tax burden is basically on par with historic inflation (2.5-2.9% prop tax in cities).

The math from this article suggests that you value your online business as about a 60% increase to your overall net worth. I am curious if you make that valuation based on a simple annual multiple or more involved DCF. IMO I believe it’s hard to value a business like this at greater than 3x, especially considering that the tribe revolves around your personal touch.

That’s a huge property tax rate vs. 1.2% here in San Francisco. At least you guys have no state taxes.

For my business, I’m just estimating its value, and on the low end. I’m buying business based on 3X earnings all day long b/c I can sell businesses for 6-10X earnings. Just gotta know where to look!

If I die today, 75%+ of the traffic will continue because 75%+ of the traffic is from search engines. I’ve got some contingencies in place too.

That is a good point. Much of it is evergreen. But, over time algorithms would penalize the site becoming “stale” (no updates).

I am confused on whether your saying that you’re actively buying and selling businesses right now.

Appreciate the concept and the comparison of renters to home owners. There are two data points that are crucial; how much interest you will dish out to lenders in achieving a mortgage payoff over time and what percentage of income one should have in regards to a mortgage. Too many people believe lenders that they can afford more mortgage than they really can. Moreover, our government (and others) actually promotes debt; both in how they run our government and in how they give tax breaks to those with a mortgage. One of these was highlighted in this week’s Economist (e.g. http://www.economist.com/news/leaders/21651213-subsidies-make-borrowing-irresistible-need-be-phased-out-great-distortion ).

The key imo is to not use debt after you own your primary home to buy other real estate; save for it and then pay cash when there is a solid investment opportunity. Understand that in our current culture that this is hard to do; however, it is a must if you really want to get ahead by making great investments. Don’t short the real estate investment by borrowing.

Hope you enjoy your vacation and learn from the cultural adventure!

I think they key is to use everything the government subsidizes to your advantage! For example, I’m managing my income to make not much more than $250,000 a year b/c I’ve run the analysis for years on what income level per person is optimal for a good lifestyle, and the most fair tax burden imo. If my income mid way through the year is looking to annualize much higher than $250,000, I simply WORK LESS and enjoy life more.

The ideal mortgage amount on the ideal income I’ve calculated is also $1,000,000. And whaddaya know, that’s the maximum mortgage indebtedness for interest deduction the gov’t allows.

Don’t fight the government. Join them by understanding their rules and play by them.

Agree that we should understand the government rules to get ahead individually or we will lose out; this is exactly why lawyers are a must for businesses to succeed. However, to me (working in strategic policy) it’s also key to know the laws and policies can be altered to effect strategic change for the better of the entire country. This area/topic, along with taxing money at a high rate for U.S. companies on income made overseas are two terrible laws/policies for the future of the U.S.A.. We shouldn’t care where the money is legally made, as long as they bring it home.

Could you comment on what the optimal annual income is for a married couple, and why? Is your estimate of $250,000 for an individual pretax from all sources?

Looks like Dan (and the Economist) got his wish with the new Trump tax plan now that you cannot combine the mortgage interest deduction alongside large state and local tax deductions (SALT). The mortgage interest deduction is still there, but 80% of taxpayers that used to deduct now no longer have a financial incentive to do so (according to what I read from Intuit/Turbo Tax). So the incentive to borrow big and write off all the interest has gone away for most.

Have a great trip, Sam!

Hey Sam,

Here in Belgium, just like in the US, it is often promoted in the media that home ownership is a good thing. The focus is that having a paid off home in retirement lowers your cost of living in retirement. (if it is well maintained).

Next to that, you have indeed a pile of cash saved up in the home equity that enables you to sell and go live smaller, or sell and go to a retirement home. There is even some reverse mortgage you could look at.

For me, wanting to FIRE at one point in time, it reduces the build up of assets that can pay my monthly expenses. This is somehow a downside. But it is a downside for a very lucky bastard, as I am able to save on top of the mortgage.

On the other hand, I also consider it a safety net that I can use if really needed. I do not take it into account when calculating net worth or a FIRE date. But it is there, as a hidden gem.

Amber Tree

To be able to save on top of paying down your mortgage is a winning proposition over time.

This post discusses the baseline effect of what if someone didn’t save anything, but kept paying off a mortgage over time. The home becomes a defacto savings account that can be liquidated or turned into a rental. That’s a good safety net for many people, b/c savings rates are so piss poor low.

Hi I’m Margaret and currently live in the UK but as a dual UK and American citizen, I know that homes and land are wealth. My rental property has given me gross revenue in three years at 482% in cash flow, and that’s just one property for now. I came to UK where I was born, to work and give myself rental income. My property went down in the 2008 crash but I enjoyed not paying a lot of taxes and had no intention of selling. It is my forced savings and how I can build wealth for me and my daughter.

Hi Amber,

Can you please expand the term FIRE for those of us who aren’t familiar? Thanks :-)

Financially Independent Retired Early

Thank you, Matt!

Interesting perspective. I believe if you buy a property at the right price, finance at a good rate, and maximize investing and saving outside of the mortgage, the mortgage can be another means of forced savings. We’ve all heard many horror stories recently about how people have been burnt by real estate, but we conveniently omit details that are relevant. For instance, a friend of mine bought a home for nearly a million dollars (in a neighborhood where the median price was just over half a million) just before the real estate bubble burst. He said it was an investment. I remember looking at him, cocking my head to the side, but not asking for an explanation as to how it was an investment. I didn’t want to offend him. At the time, I only had a sole condo in my real estate portfolio, so I considered myself unqualified to question him.

Stocks and real estate are not so different. An investment is rarely, if ever, good if we buy at or near the peak.

True. I guess it depends on time frame.

Buying a house 100% higher than the next highest priced house in a neighborhood is a bad move.

Don’t count on appreciation. Buy a home for life!

https://www.financialsamurai.com/invest-in-real-estate-for-capital-appreciation-rental-income-or-lifestyle/

“Mortgage” come from the root words “mor,” meaning death, and “gage,” meaning gamble or wager; thus, a mortgage is a death wager. A mortgage might not kill you, but it’s a gamble, often but not always a smart one.

When you buy a home with a mortgage, you’re gambling on several things:

First, that your home will appreciate. Lots of folks learned the hard way that housing values can collapse, even if the neighborhood stays otherwise healthy. I have relatives in a nice part of California’s Inland Empire whose houses are still worth less than they were in 2007. Some of my relatives were very lucky that they sold at the top of the market.

Second, that your neighborhood won’t get worse. Buying a home in downtown Detroit in 1960 might’ve seemed a good idea at the time, but given the mess Detroit is now, it would’ve been a bad investment.

Third, that local government won’t start gouging you. Many states assess home values every so often and they raise taxes accordingly. A friend of mine saw his property tax triple after the improvements he made.

Forth, that your job is secure enough for you to keep paying the mortgage, and that if your company goes under, you can find work with a commute that won’t kill you.

I’m not a homeowner yet, but if and when I do buy, I don’t plan on depending on my home’s value to get by. Depending on a home’s value is a sign that too much of your portfolio depends on your house. A house was never designed to be a route to wealth; it’s meant to provide shelter and a be good place to raise a family. As a savings account, a home isn’t good: it’s illiquid, equity loans are a rip off, and you may well have to pay capital gains taxes when you sell the house.

The only form of savings is actual savings. I’ve found it best for me to automate as much as possible: money from each paycheck goes to the savings, HSA, and 401(k) automagically without me worrying about it.

Thanks for sharing your thoughts.

What are your thoughts on the enormous difference between the net worth of renters and homeowners?

Do you think your perspective will change once you buy?

Will you consider paying cash for your first property in order to help solidify the housing market? I’ve written that it’s probably best for all homeowners to only sell to cash buyers from now on. Less headache, less heartache, less disappointment, less waste, and a quicker close.

What are your thoughts about the government canceling home buying support programs and homeowners only selling to cash buyers only for the great financial good of America?

Oops, I saw your comment, tried to approve at the Inchon Airport in Seoul, and it got lost Hubbard. If you can repost, that would be great!

Ok, trying again.

What are your thoughts on the enormous difference between the net worth of renters and homeowners?

Let’s try a quick thought experiment about two 70 year old men. The first bought a home in San Francisco in 1970 and paid off the mortgage, but did no other saving and now relies on Social Security. The second man moved every few years and never bought a home but consistently socked away 15% of his salary into savings for four decades. Given how much the San Francisco real estate value grew, the San Franciscan probably has a higher net worth than the renter, but the renter probably has more flexibility with his money. Indeed, the homeowner may well be living on rice and beans–ask social workers in San Francisco and I’ll bet that they can find you some examples of guys who did more or less what I’ve just described.

The point of this thought experiment is that net worth isn’t a perfect measure of wealth. Further, home ownership correlates with other factors that increase net worth: marriage, steady work, being older. It isn’t shocking that married fifty somethings have a higher net worth than twenty-something singletons. Your data showing that the average homeowner’s net worth is 31-46x greater than the renters could also be rephrased thus: “One group is younger, less likely to be college educated, and more likely to be a single parent; the other is older, more likely to have a college if not a graduate degree, and is disproportionately married. How shocking is it that the latter generally has a much bigger net worth?”

For that matter, it’d be interesting to see a comparison between lifelong renters and former homeowners who are also renting.

I’m more interested in breaking down things by age and geography. I’m curious as to how, say, a 40 year old homeowner’s net worth compares to a 40 year old renter’s. As I understand it, once you account for inflation, the stock market generally outperforms a home in most of America. Your experience with real estate in San Francisco is atypical of most people’s.

Would Personal Capital’s data be able to break down what’s going on? I realize that their clients skew richer than the average American, but it’d give us some data to understand how people are actually getting rich. Lots of financial advisers tell us that we can retire millionaires if we save so much out of every paycheck over several decades–how many people become rich that way versus owning a good home? And how many people are doing both?

Do you think your perspective will change once you buy?

Centuries ago, La Rochefoucauld observed: To understand matters rightly we should understand their details, and as that knowledge is almost infinite, our knowledge is always superficial and imperfect. I’m pretty sure my perspective will change as I get older, regardless of whether I buy or no, since I’m planning on learning more. For example, I was much more bullish on real estate several years ago, and got less so after seeing several friends get clobbered in the housing down turn. That encouraged me not to trust cliches but to try to understand what was going on.

Will you consider paying cash for your first property in order to help solidify the housing market?

I’ll pay cash so long as it’s in my best interest. The housing market, like any other market, can stay irrational for longer than I can stay solvent. I’ve little interest in solidifying the housing market because I have no control over it; I’m intensely interested in not getting burned in the housing market, which I have some degree of control over.

What are your thoughts about the government canceling home buying support programs and homeowners only selling to cash buyers only for the great financial good of America?

I’m not sure what you’re talking about here. Did the federal government stop the mortgage interest deduction on taxes? Did states stop using property taxes to improve neighborhood schools? Did cities and counties stop using zoning laws to attract good businesses near homes?

The government, at all levels, tries hard to get people to buy homes. I just listed some significant ways that government subsidizes the housing market.

If you’re talking about financial institutions being wary about loaning to people with solid but nontraditional finances (I seem to recall, Mr. Dogen, that you had some issues here), then the thing to do is to remember that big banks are very good at gauging most of their clients. They make policies with the majority in mind. But they’re not as good at dealing with outliers, which you are.

Glad the comment didn’t go to waste! Some thoughts:

1) The average net worth comparing homeowners and renters has a fixed Age variable. They are comparing the average net worth of all homeowners to the average net worth of all renters. The median age in America is 34, so we can assume that figure. Although, it’s likely the average age of renters is younger. As a result, let’s multiply the renter’s net worth by 1,000%. Homeowner’s net worths are still 300% higher.

2) My point is that forced savings really helps people save, whether they are disciplined or not. Yes, housing is illiquid, but it is not unfungible. The homeowner can taking out a HELOC, or sell the home and geo-arbitrage to a different state for retirement.

3) Your point about NOT depending on your home as a savings account is something I absolutely AGREE with. A home is for living if it is your primary. And a rental is for making income, like a business.

After you buy your home, come back to this thread and share whether your perspectives have changed. Fighting the gov’t is futile. If the gov’t is pushing homeownership, then who are we to combat?

We can continue this back-and-forth for a long time, but I think we’re fundamentally in agreement on the big issue—force yourself to save. A mortgage isn’t my preferred way of doing it, but it’s better than what most Americans seem to be doing, which is nothing.

But I do want to contest one final point—Fighting the gov’t is futile. If the gov’t is pushing homeownership, then who are we to combat?

The government also pushed Cash-for-Clunkers, which you correctly panned. Just because the government pushes something doesn’t mean that it’s in anyone’s best interest. You don’t have to fight the government, but you can dodge its bad policies by not playing its game.

Nice job finding my old Cash for Clunkers post! Have you been reading FS since? If so, very cool.

That program was obviously a bomb and a waste of money. But, getting subsidized housing through tax reductions is just too good to pass up, especially the higher the income tax bracket you go.

Excellent comments, gentlemen!

Very good analysis, Hubbard (the intelligent comments are why I keep coming here).

The government promotes ownership because it stabilizes communities (the “ownership society” concept). I think in aggregate this is a positive thing.

I fall in the home ownership is a good thing camp.

Honest to god that was the most intelligent and civil discourse I have seen on the internet, like ever. Thank you gentlemen for your commentary.

That’s how we roll on Financial Samurai! Here’s the FS reader demographic page.

The readers here are great for the most part. It’s a huge difference from the folks you might find commenting on Yahoo Finance articles. But alas, Yahoo Finance is huge :) See this post on Yahoo I wrote.

In Denver a 4-br/2-ba 2k-2.2k sqft home costs around 380k or 2k/mnth for a 30yr mortgage. The same home rented on average for 2.3k/mnth. Already the buyer has $300 more per month that can be put into savings than the renter. 30 years later, the buyer has saved 380k in property equity and 108k in rental savings (assuming they invested that savings) before the renter has saved a penny. If the renter can save 15% of his income and pay rent, the buyer can do so also while also building home equity. If the choice is should I invest this $2500/mnth in stocks or buy a house, absolutely invest in stocks (assuming you already have your own shelter)…. if the choice is I have $2500/mnth for shelter should I buy or rent, the buyer builds wealth while the renter doesn’t.