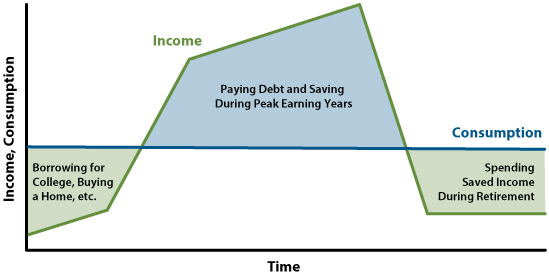

Decumulation is the process of spending down your net worth so you don't die with too much money. If you die with lots of money left over, you've essentially wasted all the time and energy it took for you to accumulate that money.

At the same time, nobody wants to run out of money before they die. Given our health and energy tend to decline as we age, we may be less capable of earning money in the last quarter of our life. Therefore, it's best to die with at least enough money to cover all our death-related expenses.

To live our best lives, we should ideally have the smoothest consumption curve possible. However, I have a feeling as personal finance enthusiasts, most of us will end up working for too long and saving too much.

Therefore, let's discuss the best age for decumulation. This topic is important to me because I decided to enter the decumulation phase in 2022 at age 45. It's been hard to switch from being an aggressive saver and investor to a spender, but it must be done.

Why I'm In The Decumulation Phase

Ever since I was in middle school I've frequently thought about my mortality.

When I was 13, my 15-year-old friend, Mark, died in a car accident. His death sliced open the security I felt as a kid. I was looking forward to skateboarding with him after I returned from summer break. But when I called his house, his mom picked up and solemnly broke the news.

Ever since that day, I've felt some level of survivor's guilt. It became harder to be lazy because that would mean disrespecting Mark, who never even got the chance to try.

Partially out of fear I wouldn't even make it to age 60, I decided to “retire” at age 34. This way, I could improve my odds of living a better life with fewer regrets. Essentially, early retirement was a hedge against an early death.

With about a $3 million net worth I decided to forsake more money to gain back more freedom. Luckily, due to a bull market since 2012, my net worth has grown with the markets.

Even with a wife and two young children to support, based on our current and projected expenses, we have over-accumulated. Specifically, our net worth equals about 80 times our annual expenses. Aggressively, 20X our annual expenses is now good enough according to Bill Bengen, and his updated 5% withdrawal rate recommendation.

If we add 80 to our ages, 48 and 45, we get 128 and 125. Sadly, no matter how healthy we eat or how often we exercise, we will likely not live past 110. Therefore, decumulation is in order.

The Best Decumulation Age To Live Your Best Life

Given the median life expectancy is about age 80, the best decumulation age is somewhere between 40 and 60 years old. The younger you can decumulate, the more enjoyable your life may be because you get to do more fun things with your money when you're healthier.

However, decumulating at age 40 is riskier as it means you may have to plan for at least 40 years of spending. Whereas decumulation at 60 is less risky because you may only have to plan for at least 20 years of decumulation.

Why Decumulating Between Age 40 and 60 Is Ideal

Between the ages of 40 and 60, your health is usually still quite good. Further, you're relatively wealthy after 20-40 years of saving and investing. This combination of good health and high net worth is the optimal combination to better enjoy your money.

At this age range, most people can still walk five miles to play Pebble Beach golf course, walk up the 600 steps in Santorini, or hike the 26-mile Inca Trail over several days. OK, maybe you'd rather take a bus to get to the top of Machu Picchu instead.

Decumulating between age 40 and 60 is also in the ideal retirement age range to minimize regret and maximize happiness. I say 45 is the ideal age to retire given the optimum combination of good health and good wealth. But it's different for everyone.

Meanwhile, if you die relatively young (<70), then you will have better maximized your wealth and time spent making money. In the old days, people retired around age 65 and then died a few years later. How sad is that? It's especially terrible if you spent your entire career working at a job you disliked.

Decumulating before age 40 may be a little too risky if you are in good health. It's better to let as much of your investments stay invested so they can compound. Further, retiring before age 40 is also not the ideal age for retirement. Your earnings power usually goes up in your 30s and 40s.

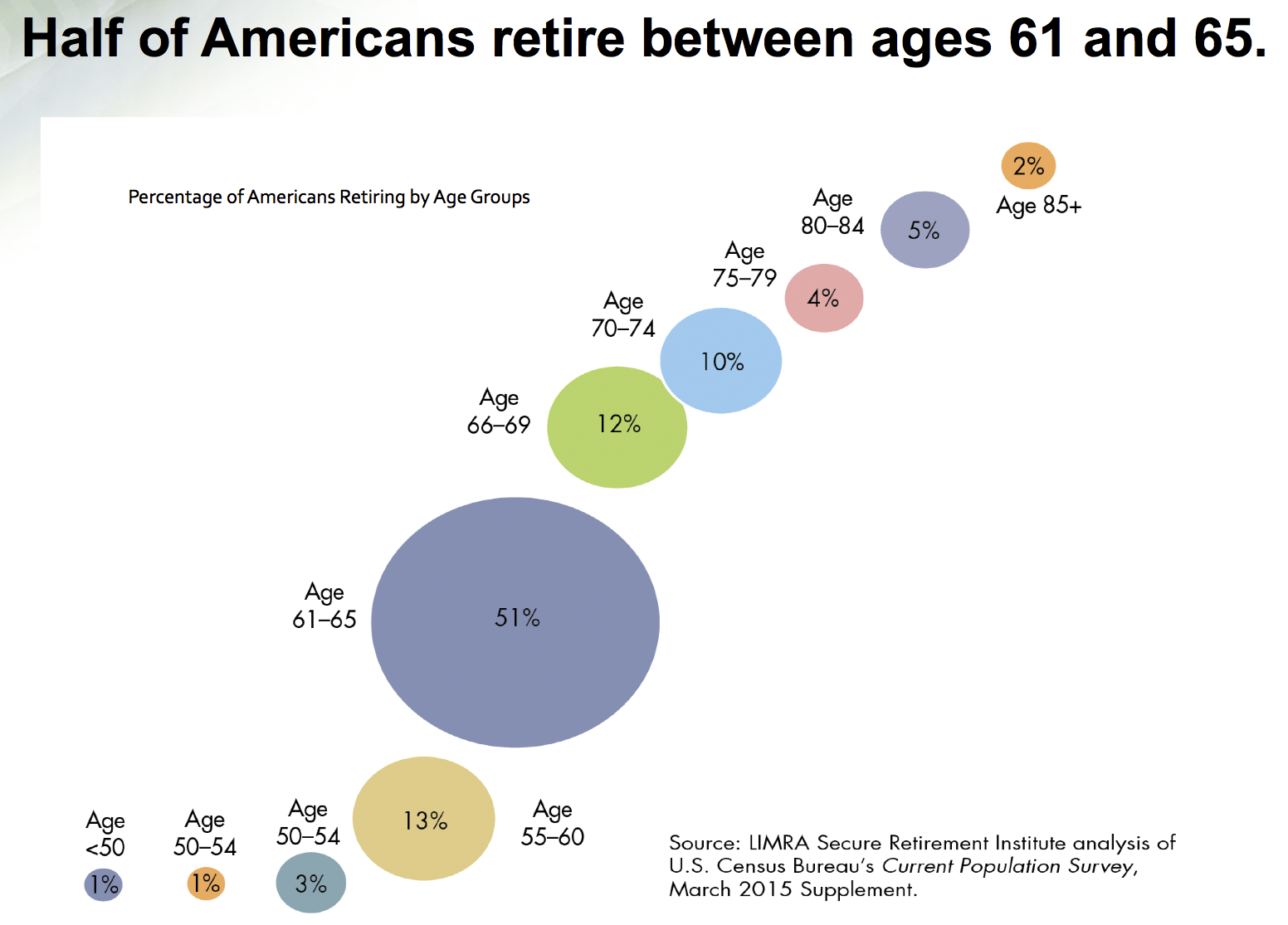

Waiting until after age 60 to decumulate is what most people do. After age 59.5, Americans can start withdrawing from their tax-advantaged accounts tax-free. Meanwhile, most Americans retire between 61-65, partially because Social Security can start being collected at 62+.

Easiest Way To Calculate The Ideal Decumulation Age

Although I've suggested the best age range to decumulate is between 40 and 60, everybody is different. Therefore, here's an easy way to calculate your decumulation age.

1) Decide which retirement philosophy you follow. There are two general retirement philosophies. The first is dying with as close to nothing as possible, i.e. the YOLO retirement philosophy. The second is dying with money left over to help others and keep your legacy alive. Most people are somewhere in between.

2) Once you've decided on your philosophy, take 80 minus your current age to see how many years of expenses you need to cover. If you subscribe to the YOLO retirement philosophy, use a small number, like 70 minus your current age. Your goal is to spend more money while living. If you subscribe more to the Legacy retirement philosophy, use a larger number, like 100 minus your current age. Your goal is to have money left over after you die.

For example, given I'm slightly in favor of the Legacy retirement philosophy, I'll use the number 90. Subtracting my age, 45, from 90 equals 45.

3) Once you've calculated how many years left you have to live, compare that number with the number of years of expenses you have accumulated. If your expense multiple is far greater than the number of years you have left to cover, then decumulation is in order.

Given my family has a net worth equal to about 70 years of expenses, we need to get cracking on decumulation since we've only got about 45 years left to live.

Although getting old can be expensive, health insurance, long-term care insurance, and life insurance should cover most health expenses. Therefore, make sure you have these three types of insurance if you're worried about a disaster. After we both renewed our life insurance policies recently, we felt even more at peace.

Case Study For Decumulation

To figure out how much you want to decumulate, you must first decide how much money you want to die with. I'll start with myself as a case study for determining when to start decumulating.

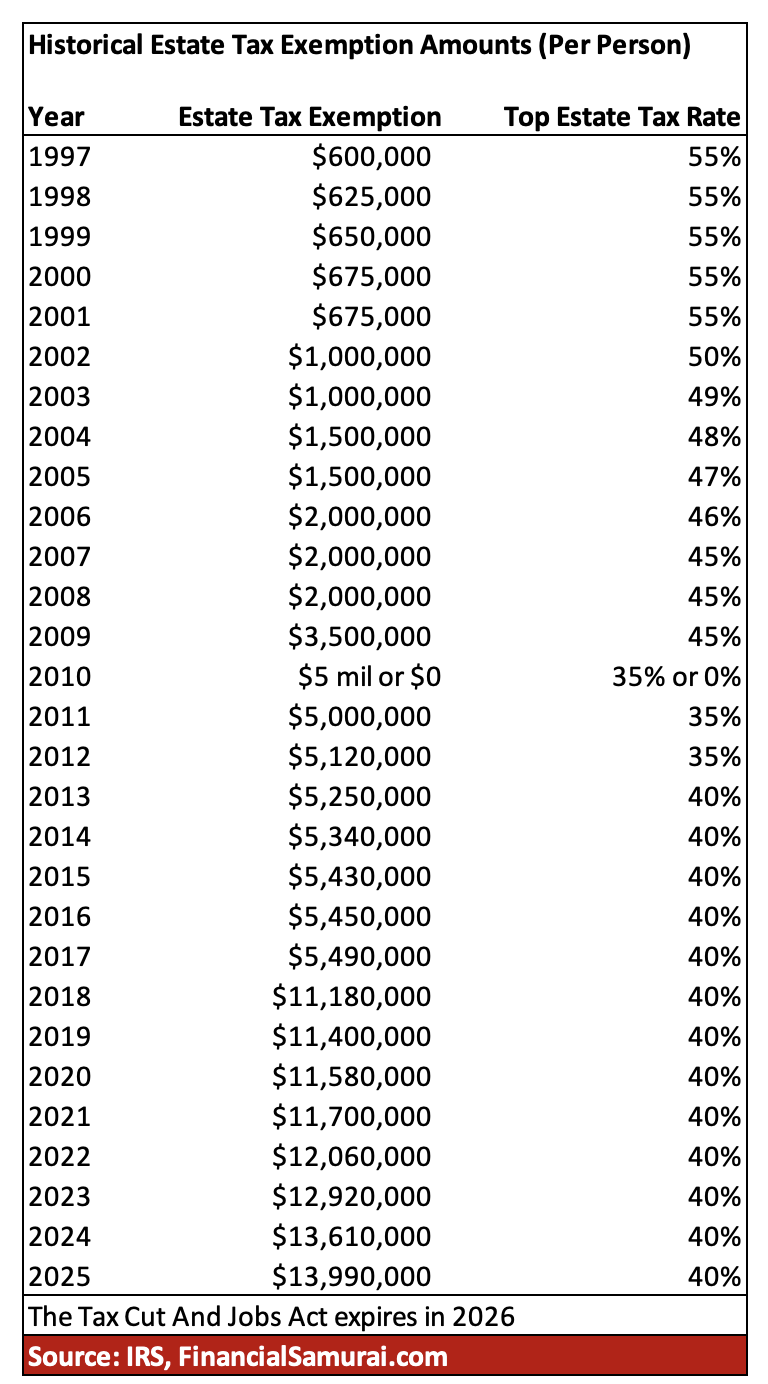

My most recent net worth goal was to accumulate the maximum estate tax threshold as a couple to leave to charities, my children, and relatives. We would then spend and give away every dollar over the estate tax threshold instead of paying a ~40% death tax.

However, the estate tax threshold has gone up quickly every year, especially in 2018 when it doubled. The latest threshold is at $27.22 million for a couple in 2024 and $27.98 million in 2025, which seems incredibly generous.

I feel like dying with that much money is a waste, even though plenty of truly rich people set up trust funds and die with way more. Therefore, I've decided to decumulate well before hitting $24.12 million.

I'm assuming the estate tax threshold will eventually go lower. But who knows given how high inflation is now. For now, I think dying with $5 million, or whatever the estate threshold is expected to be at the time, whichever is lower, sounds reasonable.

How To Decumulate Excess Wealth

Here's an applicable way to decumulate excess wealth. It is most appropriate for those who've hit their financial independence number or who have retired. Remember, you are free to spend more or spend less whenever appropriate.

Take the difference between your annual expense multiple and the estimated years you have left. Multiply that figure by your ideal annual expenses. Then divide that figure by the remaining years you have left to calculate how much more you have to spend a year.

Let's look at an example. A reader who recently contacted me has 55 years of annual expenses saved and roughly 38 years left to live, 55 – 38 = 17. His annual gross expenses are $135,000. So he should calculate 17 x $135,000 = $2,295,000. Then he should divide $2,295,000 by 38 (years left to live) = $60,395.

In other words, under these assumptions, he would need to spend an extra $60,395 a year or $5,032 a month to ensure he doesn't die with an excessive amount of wealth.

To make sure you decumulate the right amount, run this formula at least once a year. Your expenses and your net worth are always changing.

I like this method of decumulation the best because it is the most realistic solution that doesn't feel too drastic. This formula is based on the money you already have, therefore, it is more effective.

You can also simply increase your safe withdrawal rate in retirement as you see fit. But it becomes an even bigger guessing game as to which rate is best.

How To Decumulate Excess Wealth Part Two

Another way to decumulate your wealth is to calculate what your expected net worth will be when you die minus how much you want to leave when you die. You would then take that amount and divide it by the number of years left you plan to live and spend that much each year.

This formula is riskier because it is based on money you don't already have. A lot can change over the years, including lower investment returns. However, playing around with the numbers at least gives you a rough estimate of how much you can reasonably spend a year, pre-tax.

For example, let's say you want to die with $5 million. Your current net worth is $1 million and you plan to live for 45 more years. If you save $20,000 a year and return 5% a year on your entire net worth for 45 years, you will end up with $12,338,711. Subtract $5,000,000 from $12,338,711 to get $7,338,711. Now divide $7,338,711 by 45 (number of years left to live) to get $163,082.

To properly decumulate, you would need to spend about $163,082 a year starting this year while also contributing $20,000 a year to investments that return 5% a year for 45 years. See how this is a riskier strategy? most would wait until after they have $5 million before decumulating.

This formula is most relevant for those who are still working or who have not yet reached their financial independence number. Obviously, if you decide to spend less a year than what the formula spits out, then you increase your chances of dying with more money than you want and vice versa.

The Problem With Decumulation

There's one big problem with decumulation. After decades, many of us are already satisfied with our spending and lifestyles. We might be set in our frugal ways and don't want to change. Therefore, decumulation may feel like a big waste of money!

Personally, I like our 7-year-old car and forever home. I could easily drive Moose for another five years given he only has 35,000 miles. Meanwhile, we plan to live in the home until 2038, or when our youngest potentially heads off to college.

We don't need to spend more money on food because we want to maintain our body weight. In fact, we should probably spend less money on food to eat less and stay fit. However, I did try spending more money on food to decumulate for three months. It was fun to splurge, but after three months, my wife and I got sick of everything!

We've also budgeted our children's educational expenses for the next 20 years. Any excess money left over in their 529 plans will be transferred to a new generation.

The most reoccurring “luxury” expenditure I have is buying new tennis shoes every 8-12 months. But, even the most expensive tennis shoes will only cost $160. Then I like to buy new rackets every three years, which now cost about $300 each strung. My softball glove and bat last forever.

Except for flying first-class and spending obscene amounts on family vacations, there aren't any other possible big expenditures on our wish list. Do I really want to spend $120,000 to fly private to Honolulu from San Francisco and rent a beachfront property for $150,000+ a month? Not really.

Spending Too Much While The Kids Are At Home Is Dangerous

Here's another point worth mentioning about decumulation. You might not want to spend too much money on a house, transportation, and food when you're raising kids.

It's important to practice what you preach and if they see you spending so much money, they might develop bad money habits before accumulating their own fortune.

Therefore, consider spending more money before having kids. Once your kids are three years old, then you can cut down on your spend ways. Setting our kids up with good personal finance habits will help reduce parental anxiety and set themselves up for a better life.

Taxes Is A Cost To Decumulating

Finally, in order to decumulate, I may have to sell down assets and pay taxes. Sure, that's what investing in a Roth IRA all those years is for, tax-free withdrawals. But, unfortunately, I don't have a Roth IRA. It feels bad to sell down assets to pay taxes to buy things and experiences I don't really need or want.

Therefore, if you're already happy with your spending level, then the best thing to do would be to set up a donor-advised fund (DAF) and donate your investments. Make donating money to those in need the default beneficiary of your decumulation spending.

Spending More Money Won't Make Us Happier

You've got to find your ideal spending number that makes you happy. You don't want to let your super-frugality lead to lifestyle deflation.

Based on my experience living in expensive cities like NYC and SF, spending more than $150,000 a year per adult (~$200,000 gross income) doesn't make me happier. As a result, I tend to save most of the overage if any.

There's a study from 2012 that says earning more than $75,000 doesn't bring more happiness. Thanks to inflation, that level is now about $100,000 today. I think $100,000 in annual spending, where there is no more additional happiness, is about right for the median household in America.

I've tried to spend more money on my parents, but they refuse to accept anything. They are also set in their ways. So that leaves helping my cousins, who don't keep in touch. Therefore, it's time to reach out to my relatives on my mom's side. I've lost contact with since we've been on other sides of the planet for decades.

Decumulation for us will center more on charitable giving. I also want to spend more time volunteering at the foster youth home I volunteered at pre-COVID.

Decumulation is tougher than it sounds. After a lifetime of building wealth, it feels uncomfortable to go in the other direction. However, we should try our best to consumption smooth for everybody's own good.

Related: Why Everybody Needs To Create A Death File

The Best Way To Spend Down Your Wealth Responsibly

I've been in decumulation mode since mid-2023 when I turned 45. I definitely think 45 is a great age to start spending down your wealth.

I tried my best to spend more money on food, clothing, sporting equipment, and trips, but the spending didn't make a dent. Part of the reason why is I couldn't get myself to spend enough on things I didn't really need. The other reason is because of the bull market boost stock and real estate prices since 2023.

However, I did discover the best way to spend down wealth in a responsible and enjoyable manner. That is by upgrading to a home you don't really need.

Buying A Nicer Home Feels Great

In 2023, I decided to take advantage of a weakness in the real estate market and buy a larger home on a triple-wide lot. The home is situation on the robust west side of San Francisco, where I think economic activity will continue to grow.

Although I climbed to the top of the property ladder and don't feel happier, I feel more satisfied. The satisfaction comes from doing everything I can to provide for my family.

A home is a great way to decumulate wealth because you get to enjoy it for 18+ hours a day on average. If you have a partner and children, they can enjoy it as well. In addition, with all the ongoing property taxes and maintenance expenses, a home will continue to cost money for as long as you own it.

If you buy too expensive a home, you may end up feeling house rich cash poor. And that's not a great feeling to have if you're always tight on cash flow. Hence, make sure you buy within your means by following my homebuying guidelines.

Invest In Residential Real Estate More Strategically

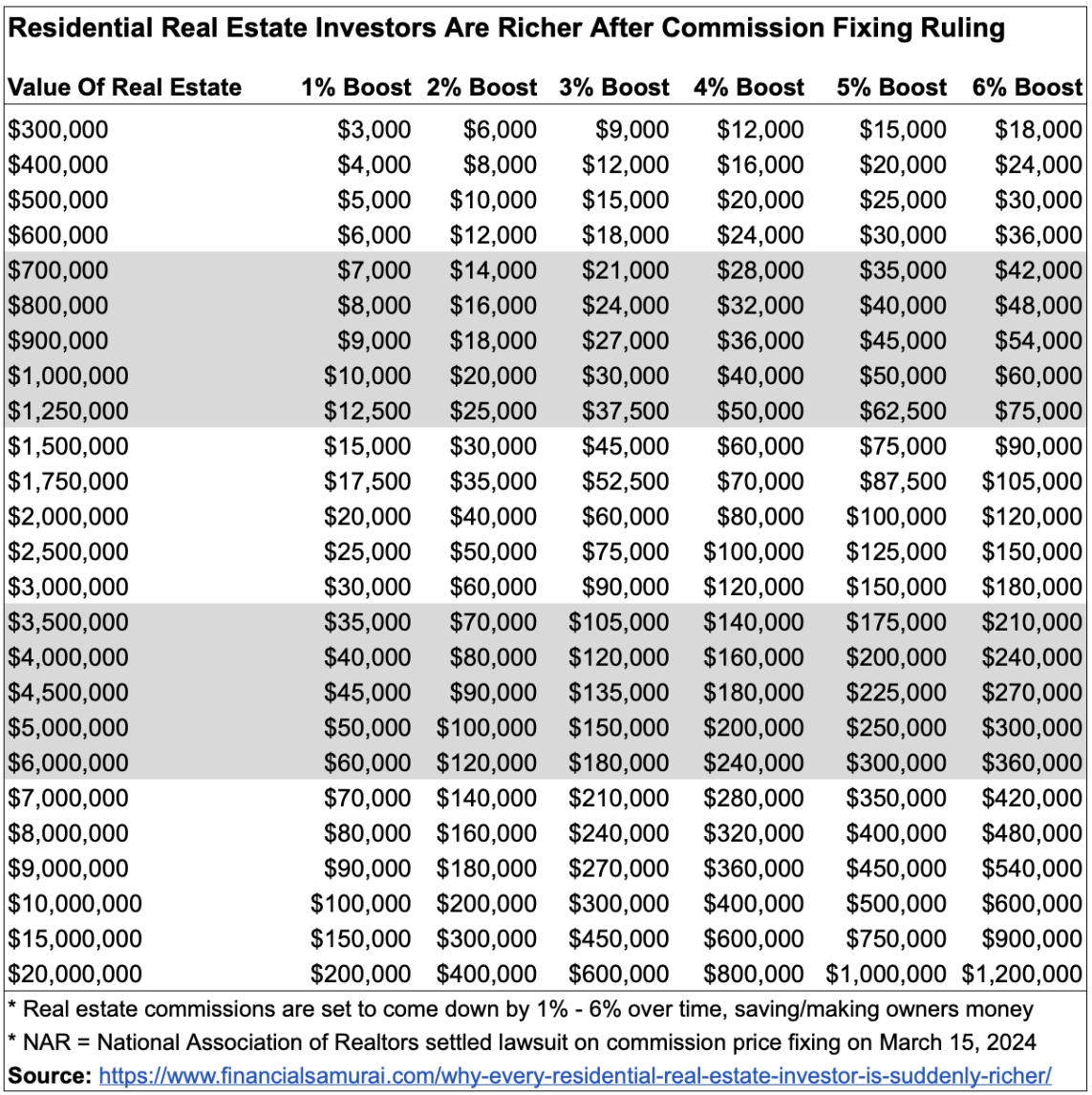

After the National Association Of Realtors price fixing settlement, residential real estate owners are now wealthier because commission rates will come down. Sellers paying less in commissions means more money in the homeowner's pocket.

To invest in residential real estate more strategically, I'd look into private real estate funds and individual deals.

Take a look at Fundrise, my favorite private real estate investing platform. Fundrise was founded in 2012 and manages around $3 billion with over 350,000 investors. The firm focuses on residential properties in the Sunbelt, where valuations are lower and cap rates are higher. For most investors, investing in a diversified private real estate fund makes the most sense.

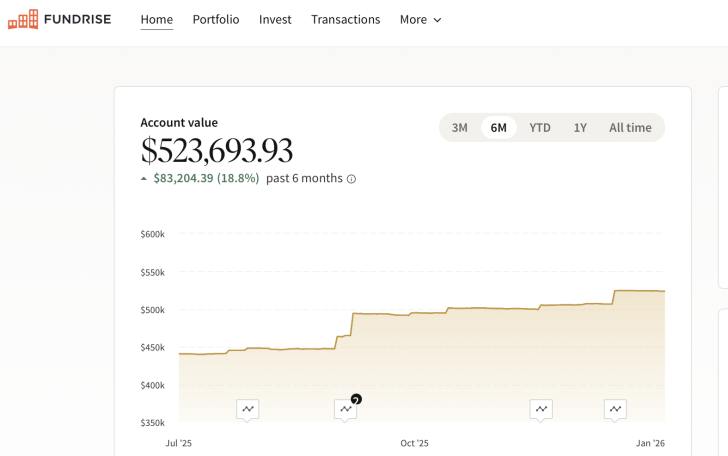

Personally, I've invested over seven figures in private real estate since 2016 to diversify my exposure and earn more passive income. Although we're supposed to be spending down our wealth, we also want to feel good continuing to invest our wealth too. After all, we got to this stage of thinking about spending down our money thanks to diligent investing.

For those interested in long-term innovation, Fundrise Venture also provides access to private AI companies like OpenAI, Anthropic, Anduril, and Databricks. AI is reshaping productivity and employment at a massive scale, and I want to ensure my family’s portfolio has sufficient exposure to this transformation.

I’ve personally invested over $400,000 with Fundrise. They’ve been a trusted Financial Samurai partner for years, and with a $10 minimum investment, diversification has never been easier.

Subscribe To Financial Samurai

Listen and subscribe to The Financial Samurai podcast on Apple or Spotify. I interview experts in their respective fields and discuss some of the most interesting topics on this site. Please share, rate, and review!

To achieve financial freedom sooner, join 60,000+ others and sign up for the free Financial Samurai newsletter. Financial Samurai is one of the largest independently-owned personal finance sites that started in 2009.

Hi Sam!

I enjoy your post and look forward to it every week.

I believe I am qualified for the revenge spend. And, I also decided to start decumulation.

So… here is what I am going to do this summer.

Decumulation + Revenge Spend = US Open Hospitality Package

I just purchased the Hospitality Package and a couple of Authur Ash and Louis Armstrong tickets in the middle area for 3 days (I didn’t have the courage to buy the courtside…yet). And reserved the hotel within walking distance of the stadium.

90 days to go!

An awesome way to spend your money and enjoy a great experience! Can’t believe they seeded Nadal 5th in this years French Open. The disrespect!

Love this post! First time on the page but struggling with what you mentioned towards the end. How after being so thrifty are we supposed to just change 30 years of spending/savings habits?

I also recently bought a new tennis racquet and instead of grabbing the newest and best, I found a lightly used racquet that was last years model. Old habits die hard!!

Looking forward to reading some of your older posts!

We’ll start splurging more when our son goes off to college. We’ll be about 55 by then. Life is good now so why make any big changes. Who knows? Spending more might cause some unforeseen problems. Also, I want to be more conservative and don’t really mind leaving some money behind. I prefer to err on the side of caution.

This article waaay over simplifies. Superficial really. You didn’t spend nearly enough time on inflation, recessions, and potential medical costs (you will get sick before you die).. I say, figure out how much you think you will need, then double it. If there is money left over, fine. That’s what Wills/Trusts are for.

Feel free to complicate figuring out the best way to decumulate and share what you’ve been doing. Use some numbers in an example to help illustrate the point.

I’m always open to suggestions as I begin my decumulation phase. Thanks!

Great article! Lifetime spending calculations also puts “fear of running out of money in retirement is overblown” into perspective. I’m a personal trainer with a net worth of 2.7 million at age 36. You don’t hear that one every day. Since it would be hard to fuck this up at this point, I have been able to justify silly purchases(that seemingly actually add value to my life) like my dream car for $650/month, a boat for $200/month and our safe family mobile for $550/month. We also have our forever home. So, my only unintentional decumulation as far as I can tell will be home improvements and kid’s college. My net worth target ever since I was 22 and read “think and grow rich” was 10 million so I will try to get there before active, intentional decumulation.

Would love some insights on how you got to $2.7 million at 36 as a personal trainer!

$10 million is a good goal to have. It’s the ideal net worth to retire with based on my survey of tens of thousands of readers.

But definitely keep enjoying the journey and your wealth as you get there!

I started personal training in 2008. Bought half of the failing business in 2011 for 10k. Turned it around to be profitable. I was still only making 46k/year but my girlfriend(now wife) was making almost double that so our debt to income was favorable. We saved up for a 16k FHA downpayment on a 2 family right outside of Boston in 2012. The property exploded in value within a year. We refinanced out of the FHA and took out a Heloc again for a 4 family with 18k down. That property also shot up so we took a larger heloc for 20% down on a 2 family. Did a triple cash out refinance and bought a vacation rental on a lake. Then used savings for a single family to give my in laws a home to live in and build equity in case they need long term care. Then a single family/forever home where we are now. The first property was 500k in 2012 and is now 1.4, the 4 family was 550k and is now 1.2, etc etc. We were lucky to buy 5/6 houses at a great time.. the 6th is yet to be determined, but has seemingly shot up since June ’21 because of low inventory. Still a personal trainer but now own the whole business.. it just so happens to clear 200k a year profit. So… not just a trainer I suppose but that’s where it all started. I have loved reading your posts over the years.. so much so that it has convinced me not to blog haha.

I loved this article, Sam. Very nicely put on so many dimensions. It’s impressive how you think these issues through so clearly. I’m looking forward to reading your book this summer!

One thing that’s not talked about much is climate change. I think in the next 20-30 its going to really impact people and in some places it already is. People may have to start migrating to other areas of the country. Things like water shortages, fire, extreme weathre etc. how will that impact us financially? Just some food for thought.

Going inland lowers your cost of living. So it’s a net positive if one moves. But I’m always an optimist.

Related posts:

https://www.financialsamurai.com/how-climate-change-may-affect-real-estate-values/

https://www.financialsamurai.com/problem-with-owning-beachfront-property/

I know this can be a hard topic to discuss, but I wonder if dealing with early death leads to the pursuit of economic freedom earlier in life. For example, many of my male family members died in their 40s or 50s (heart disease and accidents), so I always wanted to enjoy whatever time I got – and of course take care of my cardiovascular health with lifestyle choices.

With that said, this article is good to keep in mind. While I don’t need to start wealth decumulation soon, it’s good to know. I could retire, at my current rate, in my 40s (although I don’t think I’ll fully retire until I’m unable to work for health-related reasons). I am interested in pursuing other options – related to charity – as I think that will be a good use for whatever wealth I build (beyond what my family needs).

As a bit of a sidenote, regardless of my family history, I plan to live well into the twilight years. It’s better to plan with a bit of a cushion after all!

In terms of legacy, what about funding a second to die life insurance policy for your kids. This way when you and your spouse pass your children will get a base amount. Anything over can be gravy for them and you can more aggressively decumulate knowing you set a floor for their inheritance.

I’ll have to do some research on that and write a post! Thanks for the suggestion.

Love this post, Sam. So timely (for me, anyway) and the formula for decumulation is extremely helpful, even if you have to fight your own psychology/relationship to money issues. Other bloggers speak to the topic but practical examples and benchmarks are what draws me to your site time and time again.

I saw my parents save throughout their lives and while they splurged on us, they really didn’t go over the top with themselves. Mom had her chincilla and jewelry, but in later years, I feel like they could have enjoyed more rather than leave us what they did, although I’m super grateful.

Now I’m wrestling with that legacy but the anxiety of decumulating. All models are good as their inputs, and it feels like there are too many variables (spiraling health care costs, taxes, inflation etc.) in play to fully let go of worries. Our spending has never been consistent year to year, nor have our earnings, or returns.

Kudos to you for not giving to lifestyle creep! Having spent a lifetime in aesthetics/design/luxury goods/social sphere, it’s hard not to want to be surrounded by beautiful things and experiences.

Funny, but we had a chinchilla as well for many years! He died of old age, but lived a good life.

It’s hard to decumulate, which is why I think the first formula works:

Take the difference between your annual expense multiple and the estimated years you have left. Multiply that figure by your ideal annual expenses. Then divide that figure by the remaining years you have left to calculate how much more you have to spend a year.

This way, the spending is more incremental, rather than all at once.

If you have any lifestyle inflation spending ideas from the aesthetics/design/luxury goods space, please share them! I was talking to a wealthy friend about what we should buy, and we couldn’t really think of anything. We came up with a beer maker and new tennis rackets.

I’m going to guess that the chinchilla C M Cal’s mother had was the type she wore! :)

Wealth taxes have been mooted in Australia, but at present do not exist. The Greens, the most anti-capitalist, un-Australian party wants to impose a 6% wealth tax (not a death duty) on billionaires of which we have a handful.

My wife and I are in our mid-70s (I turned 75 yesterday) and spend what we like, when we like. We have everything that opens, shuts, and beeps.

Our challenge, as I see it is not worrying about how much cash we leave, but the material “stuff” we have accumulated that we need to decumulate. I tell my wife I don’t want her to die before me because she has a truck load of craft equipment, machinery and fabrics etc that fill a whole bedroom and more.

I dread the though of our two adult children having to dispense with what is left when the last of us takes that trip to the crematorium. I’m actively trying to declutter/decumulate whatever I can.

Interesting, if not sobering logic. Does algorithm take into account the amount of the desired estate one would want to leave behind? Perhaps I missed it.

I’ve been trying to decumulate for the last couple years now. I quit putting new money into the stock market. I bought a vacation property and remodeled my primary residence. I’ve cut my work schedule down to roughly 8 hours a week. I gave more to charity than anytime in my life. I raised the pay for all my employees far above market rates. The end result my net worth increased a couple million dollars.

This is your fault Sam! Saving, investing, real estate, multiple income streams and a Stealth Wealth lifestyle all contributed to my failure.

It sounds good, but I have to consider a few things.

1). I think oldster healthcare costs will explode as the biggest cohort of Boomers (born ~ 1960) need it. And like the value of an annuity when the insurance company that owns it goes under, I’m skeptical that long term disability/care/whatever insurance will be honored after that phase change simply because the companies that have these policies will simply die under the weight of claims.

2). If we live longer in better health, that’s the best case scenario. If you can still work, then you don’t have to be retired in the “worst” case scenario. I remember that reason I started aggressively spending more money to travel was when I met the Man on the Bus in Stockholm. He was in his nineties and could barely move and our tour bus had to do much to accommodate him (as it should). The fact he waited so long to start traveling (according to him) made me sad but also made it clear that waiting too long to travel was a bad idea. If traveling is important to you, don’t be the Man on the Bus.

Great post. Tough to put into action though. My struggle with alot of these projection based scenarios is having to “trust” that the market will return 5-10% on average per year – historical averages. If it is flat or slightly negative for say a 10-year period, then alot of the wealth/early retirement theories go bust. Add in a potential new era of high inflation and this seems like a difficult time to start decumulation. Or at least get a handle on projections.

I understand that is why you recommend only a 0.5-1% withdrawal rate. But that puts early retirement (and I mean true retirement, not quit job and do side gigs) out of reach for many or would have to live very meagerly, which isn’t alot of fun and not most people’s goal for retirement.

With 4.8 million of investible assets, 1% withdrawal is 48k, then another say 90k on dividends (Assuming 1.8% yield), and take-home is about 108k (after taxes on the dividends). Our current spending is $160-200k. 2.5% withdrawl rate about gets us there.

Thank you for acknowledging my proper safe withdrawal rate post! Dang, I got so much backlash for recommending a much lower withdrawal rate using my formula. I guess it’s nice that after the current turbulence, maybe my reasonings were reasonable.

I actually only recommended a 0.5% withdrawal rate when the 10-year bond yield fell to 0.59 during the first ~8 months of the pandemic. My withdrawal rate recommendation is based on the formula: 10-year bond yield X 80%.

So the bright side is, as the 10-year yield has risen to ~2.75%, my dynamic safe withdrawal rate is now ~2.2%. I truly believe my safe withdrawal rate formula is the smart way to go for changing times. And notice how the current 2.2% is close to your 2.5% withdrawal rate to get you there.

Not bad at all.

but isn’t that the problem? The stock market is yielding negative returns this year. Doesn’t that exasperate the issue by increasing the withdrawal rate? Your are withdrawing more of your assets and assets decreasing in value at same time. 30-year at 5.25% – will see housing cool dramatically as well

Higher inflation should equal higher profits for companies should equal higher stock prices. However, not happening. Companies are having to pass higher profits on products back to workers as wages and for supplies. High inflation environmental requires a rising stock market to protect portfolios.

Yes and no.

On the one hand, lowering your safe withdrawal rate is better when you’re losing money in the stock market.

On the other hand, if your focus is on retirement and earning retirement income, your retirement income will go up. Therefore, it is safer to increase your withdrawal rate to earn more income.

As a retirement practitioner, the main thing I care about is income. I care about my net worth amount, but mostly in relation to how much income it can safely generate to provide for my lifestyle.

Have you calculated your personal inflation numbers? One thing I realized is that our spending has only increased about 3% this year (vs 7% CPI number). That is likely because a) we dont need to buy a new vehicle this year b) we own our home so are not subject to rent increases c) Stuff like gas, food and electricity make up a comparatively smaller part of our budget than what the average basket that they measure inflation against. So overall, my portfolio still had a modestly positive real return this year given that. My guess is that many here are in a similar situation.

Hi Sam,

Thank you very much for the very nice article.

Just curious, do you include your primary residence in your net worth, or should it not be included as it does not provide any income?

My net worth is negative if I do not include it, so I am always in the fence to include it or not.

Hi Hasan, it’s worth including a conservative estimate of the equity in your primary residence as part of your net worth. The down payment, for example, doesn’t just suddenly lose its value once it is used to buy a house.Thanks

We plan to decumulate our investable assets based on a lifespan to 90 years old. If we live beyond that age, we have our primary residence and lake property equity to dive into. Die before 90, the kids get the remaining investments plus the two properties. Die after 90, they get the remaining equity.

We’ve hit our financial goal of 5.5M at age 44, but with the recent real estate price surge, we feel obligated to work for a couple more years to help our 3 young adult children with down payments on their houses. We make more in one year than they will in ten years, so it kind of feels selfish of us to shut down too early.

Sam – appreciate the post. When you talk expenses does that include taxes on income and how do you factor in the fact that (presumably) one’s net worth will continue to grow based on the market.

Easy to just use gross annual expenses as the multiple. That way, it’s more apples to apples.

The formulas should be relatively conservative given they don’t account for any appreciation.

As usual Sam, your post is on the mark. Many of your readers, such as myself, have been following you for years now. So, your A+ “students” need to start hearing about things such as decumulation, withdrawal strategies, etc.., in addition to the accumulation strategies.

I have 4 more years before I hit my decumulation age (which will be 58). If I live to an old age, I plan to do most of my legacy-giving while I’m still alive. That way I know WHERE it’s going and HOW it’s going to get used. If I check out earlier than expected, then the estate-planning that I’ve put in place will kick in.

I don’t know who said it, but some rich fellow said, “I want to leave my kids with enough money to do ANYTHING, but not enough to do NOTHING”. Well, I won’t be that wealthy, so my motto will be, “I want to leave my kids with enough money to do SOMETHING, but not enough to do NOTHING”.

Then I will set up some charitable donations that I haven’t quite gotten around to just yet.

Everything you say is spot on, but it’s still going to a very hard task. How do I go from sacrificing, saving and investing for 30+ years to now SPENDING my savings?

This upcoming chapter of my life will definitely be different. LOL!

Hi Alvin,

May you live long and prosper!

“I plan to do most of my legacy-giving while I’m still alive. That way I know WHERE it’s going and HOW it’s going to get used.”

Makes total sense and what my mom tells me all the time! I plan to do the same.

It will certainly be tricky for us to help our children while ensuring not to demotivate them to make their own wealth. I’m hoping our constant talks about the importance of working for our money will make a difference. It has to.

Nothing is given! Everything is earned. To be able to earn something on your own is one of the greatest feelings.

Awesome article!

It’s like do I take early SS or wait for full? I guess to a degree, we need to play God. My wife are living every day likes it’s our last … within reason. We’ve traveled the world, now, living in Vegas to be a sponge for the entertainment world. Thinking about a foundation or charitable trust, something we can be proactive on while we’re here. Just an fyi, I should have been pushing daisies at age 40 … however my wife and I have been proactive in everything in life, even our health. We get full body scans every five years, it’s a “heads-up” in life.

Cheers!

What happened at 40? I’m gonna have to look into this full body scan. What does that entail and how is that different from a normal physical with blood work?

Here’s a post on Social Security: https://www.financialsamurai.com/when-to-take-social-security/

I work in the medical field. All jokes aside, lifespan has increased. They are already running anti aging studies on metformin. I agree with others one should plan to live longer current lifespans, especially if one is under 40

Consider a Private Operating Foundation where you DO your charitable activity instead of donating to a DAF since many nonprofits that might benefit from your hard work and accumulation will be inefficient, ineffective and not align with your core values.

Please share more. What does a POF entail? Procedures, costs, transmission, etc. thanks

Extremely thought provoking and timely for my own situation. 63 and burned out.

This is one of your best.

Thanks Steve. I hear you on the burnout. I hope you can take things down a notch and enjoy the time more.

Been following this site for a while and appreciate the insight. I’ve implemented a lot of the concepts here over time and its led to far better financial and overall life decisions. Thank you for putting the effort in.

Funny you should post this. I’m reading a book by Bill Perkins called Die With Zero with expands on this very point. The title is a bit misleading…this isn’t a “go light you’re money on fire”-type philosophy; its an extension of living you’re best life now (no autopilot) and not putting things off when you’re too old to move.

You’re welcome Louis. I’ve read Bill’s book too. It’s not bad, but I found it to gloss over the HOW to decumulate. Further, Bill is worth over a hundred million dollars and can afford to decumulate heavily if he wants to. I didn’t find the book as helpful for the mass affluent or middle class.

My wife wants to decumulate. And we are going to live well, with lots of travel and stuff, regardless, so long as we live. We’ve been planning for a long time.

I just keep having this tiny concern that, sometime in the next thirty years or so, someone is going to come out with something to set your clock way on back (some stuff in the news today about epigenetic resets on a woman’s skin cells to deage her many decades, which they think will eventually work on all kinds of other cells).

I’d hate to not have the money left for us to get the treatment, as I very much doubt medicare will cover it.

I know. It seems weird now. But is it?

Sounds like a win-win actually. You decumulate and live it up more. And you find out you get to live longer. If so, you will find away to make more money or make your money last longer.