With stock market volatility back, interest rates elevated, and high valuations, lower expected returns are a good possibility. Since 2009, investors have been able to make lots of money relatively easily. However, to expect double or triple-digit annual returns going forward is not wise.

In August 2020, when I came out with the Financial Samurai Safe Withdrawal Rate Formula = 80% X 10-year bond yield, I was largely ridiculed (review the 390+ comments).

As someone who went through uncertainty and doubt after I left my finance job in 2012, I encouraged new retirees to play it safe the first couple of years as they got used to change. The change can often be very jarring as you search for a new identity and adjust to a new routine.

A guest post I had written about my new safe withdrawal rate formula for another site was taken down as the host was pressured by his readers because my suggestion was considered too extreme. Meanwhile, another blogger called me unflattering names in his rebuttal.

I was disappointed, yet fascinated at the same time about how difficult it was for some people to think differently. As an investor and financial freedom seeker, it is always good to think about multiple scenarios. Here's a case studying using my dynamic safe withdrawal rate between 2020 – 2024. Since then, the market has continued to rebound.

The base case scenarios should be: Realistic, Blue Sky, Bear. From there, you can model out your finances to increase your chances of living your best life.

Lower Expected Returns Going Forward

A year after I introduced my FS Safe Withdrawal Rate formula, in August 2020, Vanguard came out with its 10-year forecast for stocks, bonds, and inflation. Essentially, Vanguard agreed with my thesis that retirees should lower their safe withdrawal rate in retirement or accumulate more capital before retiring.

The Vanguard Capital Markets Model calculated only a 4.02% annual return for U.S. stocks, a 1.31% annual return for U.S. bonds, and 1.58% for inflation over the next 10 years. That’s more than a 60% cut in expected returns.

Therefore, if you have a portfolio mix in retirement of 60% stocks and 40% bonds, your portfolio may return just 2.93% a year if Vanguard's forecasts come true.

Plenty of people, including myself, have their doubts about Vanguard's lower expected returns forecasts going forward. After all, the frenzy of 1999 is back in a big way with AI, Bitcoin, and accelerating adoption and growth. The inflation forecast looks especially low during this high inflation environment.

However, during a stock market correction, I've noticed the rebuttals have stopped. Not only has Vanguard come out with lower expected return assumptions, so have GS, BoA, and a bunch of other investment houses.

If the S&P 500 is down 10% for the year, maybe my safe withdrawal rate formula of 80% X the 10-year bond yield might actually be too aggressive! After all, when your $3 million retirement portfolio is down $300,000, you tend to fear it might go down further.

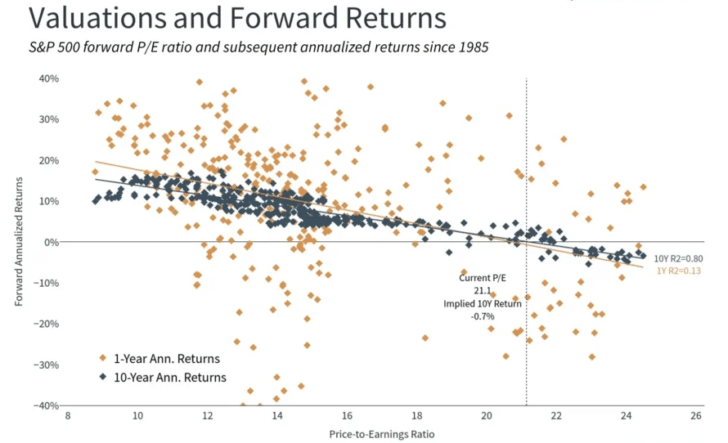

Expected Forward Returns Are Highly Correlated With Valuations

Here is a fantastic chart that plots the S&P 500 forward P/E ratio and subsequent annualized returns since 1985. Notice how the higher the valuation, the lower the expected forward returns. So please take not as you asset allocate appropriately during different valuation scenarios.

Today, the S&P 500 is trading around 22X forward earnings, therefore, expect lower returns going forward.

Things To Do In A More Difficult Return Environment

No matter how stupid you still think I am, we should agree that over the long term, our investments in stocks, real estate, and even bonds should provide positive real returns. However, we live in the short-term. And the short-term, here and now, is where plenty of unexpected things can happen.

You might think you can withstand a 35% drawdown. However, what you might not expect is losing 35% of your portfolio's value AND being out of work for 18 months.

You might think you'll happily live until 90 years old. However, you might not anticipate having a medical issue for you AND your aged children.

The more we can plan for suboptimal situations, the smoother our existence. Therefore, here are some things all of us should do if the Fed doesn't save us.

1) Lower personal expectations

Happiness is about beating expectations. If you only expect a 5% return on your investments but return 8% for the year, you're thrilled! However, if you expected a 15% return on your investments, but only returned 10%, you're disappointed. Funny how our minds work right?

If you graduate from Harvard and pay full tuition, your expectations of doing great things will go way up. If you end up doing what every non-Harvard graduate does for a living, you might be sorely disappointed.

The key here may be to NOT believe the lower expected returns to the same degree. For example, if stocks are expected to return only 4.02% a year for the next 10 years, your 30-year-old self may want to dial back your stock exposure from 90% to 70%. Why risk so much exposure for a measly 4.02% return? Your stock portfolio could easily correct by 10% or greater.

But instead of reducing your exposure, you maintain your 90% exposure to stocks because you are young with plenty of income upside. You expect lower returns. However, you also secretly hope returns will be higher. If the returns are terrible for a year or two, you won't be as disappointed.

2) Accumulate more capital before retiring

After accumulating 25X your annual expenses, please don't stop or start taking it easy. 25X your annual expenses based on the inverse of the 4% rule is seriously outdated. Think about the multiple as a minimum.

Instead, shoot to accumulate 50X your annual expenses or 20X your annual income. Sure, this may require you to work longer and save even more. However, make it a fun challenge. Once you've reached 25X your annual expenses, the incremental jump to 50X your annual expenses isn't as difficult.

The same thing goes for reaching about $300,000 in investments, the approximate level where the feeling of financial freedom begins. Once you get to $300,000, getting to $500,000 or $1,000,000 won't seem as daunting.

3) Generate supplemental retirement income

There is nothing more stress-relieving in retirement than generating supplemental retirement income. The extra income helps keep you busy while also erasing your doubts about your new life.

The fear of running out of money in retirement is overblown, especially the younger you retire. You will naturally gravitate towards doing something you enjoy that likely makes money because we all seek purpose.

If you're still on your financial independence journey, then it behooves you to make side income to boost your investment contributions. If returns are indeed going to be lower going forward, you will need to shovel more capital to get to your target at the same time.

Consult or do something entrepreneurial. Some people actually work two jobs from home because they now can. Without Financial Samurai, I'm not sure what I would do with all my free time. It feels good to be productive.

In fact, one Financial Samurai reader decided to go back to work two months after he resigned! Why? Sequence of returns risk. When he retired at the end of 2021, his net worth was about $6 million. Months later, it had dropped to only about $5 million. As a result, he decided to do some part-time work for his employer to make extra cash.

Three years later, his net worth made it back to all-time highs and he's doing great!

4) Delay your target retirement date

Each year you delay retiring provides a double benefit of saving more and having one less year of expenses to provide for. Therefore, it's like getting a two for one special. And who doesn't like to get a good deal?

By delaying your retirement target date, you lower your expectations. When the year comes to finally take a leap of faith, you can then make a more precise decision.

Maybe you'll discover that work isn't so bad if you've only got one more year to go. Letting go of the desire to get promoted is a powerful feeling. So is working when you don't really need to work.

Or maybe you are presented with an opportunity to get laid off with a severance. Ultimately, the severance accelerates your timetable to leave. My severance made it seem like I was leaving work behind at age 40, even though I was only 34 because it bought six years' worth of living expenses.

Finally, you should probably delay your decumulation phase for a year or two. In a downturn, it's more prudent to spend as you normally have.

5) Boost your spending and live a little

Instead of always being so conservative with your time and money, you may want to spend even more money. If your investments aren't going to provide you solid returns going forward, then you might as well spend more of it on living a better life today.

With lower expected returns, your opportunity cost of spending money has declined. The Porsche 911 you've been eyeing while driving a Honda Fit all these years… go for it! The first-class seats you walk by on your way to an economy class seat that doesn't recline next to the toilet…. time to live larger!

Aggressively find ways to spend your money before the stock market flushes your gains away. There is logic to spending more money during bad times to help make bad times better. It's during good times when you want to invest more so you can potentially make even more money.

Personally, I've decided to permanently boost my spending by 20% starting this year and decumulate. It'll be a challenge, given over two decades of frugality. But gosh darn it, money is meant to be spent!

The Best Insurance Policy Against Poor Investment Returns

Losing lots of money in your investments feels bad. I get it. But the best way to feel better is by living a good life.

If you've got no friends in real life, no family, work a crap job, and spend lots of time venting on social media, you're going to really feel it when your investments take a hit. Your self-worth is too wrapped up in your money.

But if your life is diversified with meaning, then I dare say you'll start looking at ANY investment returns as a bonus. Your awesome job you never want to quit is already providing you the money you need to live a comfortable life. Your friends and family that provide you the most joy trumps any amount of investment loss.

Find ways to use your money to improve the quality of your life. And if you can't, there are a plethora of free things you can do to live well.

We must learn to live with dead money for a while. With black swan events like a pandemic and now a war, our money might not provide us any returns for years.

I'm off to go for a stroller walk and to play some tennis now. How about you?

Diversify Your Investments Into Real Estate

Stocks are very volatile compared to real estate. Therefore, if you want to dampen volatility, diversify your investments, and build wealth at the same time, invest in real estate. Real estate is my favorite asset class to build wealth, especially during times of uncertainty.

The combination of rising rents and rising capital values is a very powerful wealth-builder. By the time I was 30, I had bought two properties in San Francisco and one property in Lake Tahoe. These properties now generate a significant amount of mostly passive income.

My favorite real estate investing platform is Fundrise. With over $3 billion in assets under management and nearly 400,000 investors, Fundrise is the leading, vertically integrated real estate platform today. Investors can invest in their diversified real estate funds with as little as $10.

Fundrise primarily focuses on single-family, multi-family, and build-to-rent properties in the Sunbelt. With lower valuations, higher yields, and strong demographic shifts, Fundrise investments are in the sweet spot of a positive long-term trend. Come check out what they have to offer.

Invest In Private Growth Companies

To potentially boost expected returns, invest in private growth companies instead of public companies and public investments. One of the most interesting areas where I'm allocating new capital toward is public venture capital. Private companies are staying private for longer, so I want to participate in their gains.

Roughly 90% of VCX, listed on the NYSE, is invested in artificial intelligence, which I'm extremely bullish about. In 20 years, I don't want my kids wondering why I didn't invest in AI or work in AI!

Financial Samurai is a six-figure investor in Fundrise funds and Fundrise is a sponsor of Financial Samurai.

For more nuanced personal finance content, join 60,000+ others and sign up for the free Financial Samurai newsletter. Financial Samurai is one of the largest independently-owned personal finance sites that started in 2009.

I am 28 years old and I have an annual net salary of 24,000$CAD (LOL). I studied for many years hoping to get into medicine, but never quite succeeded. I decided to let go and work a simple government job at $22.50 per hour telecommuting. I manage to save about $800-$900CAD maximum per month. I feel like the road to wealth will be long and sometimes, even though it’s wrong to think like that, I feel like I was born to live a hard life. My mother died when I was 17 of a medical error and my father when I was 20. Anyway, maybe one day I will get over it.

I still have a bitter taste in my mouth from my school career and the thousands of hours of effort that I have made to become a doctor without succeeding. Which means that currently, I no longer have the energy or the desire to embark on such a time-consuming project. Maybe one day it will come back to me. But for now, the flame in my heart is extinguished and I’m doing a low-paying job that I don’t really like.

Supplemental income is the way to go in this environment. Anyone can get a part-time job easily and the pay is trending up. Working part-time after retirement is good in many ways. It keeps you occupied. You can make new friends and you make some money. Working keeps your brain active too.

Another option is geoarbitrage. Why not travel around in lower cost of living countries for a few years while the stock market is stalling? Well, it’s kind of hard due to Covid right now, but things are loosening up around the world. Save money and see the world.

Hi Sam,

I’m concerned that for the next several years there will be some form of lockdown as governments, in general, do not want to relinquish the power/control that they have attained. Therefore, if lockdowns continue, would this cause you to revise significantly the withdrawal rate?

Hope all is well and look forward to your next newsletter.

Semper FI,

Luis

What does everyone think about this total net worth allocation:

25.0% – Cash

17.5% – US Bonds

2.5% – Int’l Bonds

21.5% – US Stocks

6.0% – Int’l Stocks

17.5% – Primary Residence

7.5% – US Real Estate (AcreTrader)

2.5% – Int’l Real Estate (REET)

Very risk-averse. I would say very appropriate for someone over 65 years old or who has already amassed a large fortune and doesn’t have to work again.

How old are you and what is your situation?

39, spouse 38. One child. Just over $2 million net worth. ~ $250k household income in relatively low cost area.

Why so much in cash? You are losing money on that 25% of your portfolio. Maybe move some to I BONDS paying 7.12%

I have $20k in i bonds. It’s included in my US Bond allocation. Yeah, I’m going to work to a 22.5% cash (checking, savings, CDs, etc.) allocation and maybe even a little lower over time.

Are you planning to retire soon? If not I think this is way too conservative, especially having that much in cash.

All this talk about “risk” and “avoiding loss” is not really applicable unless you (1) want to retire soon (in under 5-10 years) or (2) feel like you may need to convert some of the investments to cash soon (e.g., to buy a house). Otherwise, it makes sense to stay long in the market knowing that historical returns are ~10%. Sure, this next decade may not be projected to meet that growth, but if you’re not going to retire in that time frame it’s really rather irrelevant. Even a 4% return in the market is more than a 0% (or negative, after inflation) return on cash.

Maybe retire in 12-15 years. Yes, I’m going to work towards a 22.5% cash allocation and maybe even lower over time. It’s currently even higher than 25%. Thanks for the comment!

I’m assuming you sleep pretty well at night then, which is important at the end of the day!

If there’s ever another bear market, you’ll be good and have plenty of cash to deploy.

Yes, I’m currently even > 25% cash. I’ll work towards 22.5% and maybe even lower over time. Thanks for the comments!

With retirement, drawing down assets, safe withdrawal rate, etc. the financial planning part is important of course, but don’t forget the emotional and psychological element. Having ‘retired’ once and then decided to work again for a while, I can say that the financial math ceases to be theoretical, and becomes very very real. And market events like March 2020, or January 2022 can be very emotionally stressful if you don’t have a lot of financial cushion. For me, if my target retirement net worth number is X, I will wait for 1.2X, to have the peace of mind in situations like this.

There are soooo many variables to figuring out whether you will outlast your money and to be honest a lot of it is out of your control.

Sequence of Returns Risk is just like a casino. You never really know when is the right year to retire.

From a Kiplinger Article –

$1 million portfolio 20 year time period. 3% inflation. taking out 50K per year to start.

1989 – 2008. End value $3 million.

Now just reverse the returns

2008- 1989. Run out of money in year 19. End Value $0

50X expense obviously takes out most of this risk as the above example is 20X expenses.

I am a credentialed 80 year old teacher. And I love my job!

My career advice has always been “do what you enjoy”.

I worked till I was 75, so that I have a good social security. No one has ever advised me, but I tried to do what made sense. As a woman, I found very little help out there, my mother was the best for giving advice. I also maxed out 403b and then found that I could contribute to a Roth IRA. I also put inheritances to our mortgage.

After I retired, I was passing the District office and went in and they signed me up for substitute teaching immediately. I did about 2 jobs a week and we found that it stretched our retirement money in addition to me enjoying myself.

During the pandemic, the District helped me with unemployment (!). It also helped me train for online learning and Zoom. Now the District is short of substitutes and I do as many jobs as I can ranging from TK to 8th grade. We also received a substantial pay increase.

My main point is Please have a career that you LOVE! Women are still handicapped in the retirement area, no one helps us at all. I have seen women refuse to open retirement accounts “because their families need the money”. Who will look after them when they are old?

My second point is “get qualified”. Leicester University in the U.K. and CSULB helped me get credentialed at minimal cost. I am still using those qualifications.

Then please make sure that you spend wisely. We are still in the same SoCal house after 40 years, with minimal house taxes. We also buy preowned cars. We eat out minimally. We live well.

Thank you!

The problem with volatility is that when the prices veer down, the people who can least afford the losses (i.e. the small investors) tend to panic and sell. Probably because they think they can’t afford to keep losing money.

What they do, of course, is lock in their losses.

Those lower priced equities then get snatched up by bigger investors. When things go up (volatile means up and down, not just down), the rich have gotten richer and the less rich have gotten even less rich than they were.

A conspiracy theorist could even speculate that the wealthier investors might deliberately create volatility when they can.

Volatility by itself is not a problem if you don’t feel compelled to sell when things drop.

For that reason, avoid funds that leverage returns, avoid puts and calls, and nearly anything that locks you into doing anything when you might otherwise choose not to.

Sun Tzu warns about not making your move in a place or time not of your own choosing. That’s solid advice both in war and in peace, especially with lots of volatility. Don’t let anyone else force your hand on when (or what) to sell.

Hence why we should follow a investing allocation framework through thick and thin. Of Sun Tzu advice.

Best hedge is to really live a great life or the best life possible each day. Bc that is the end goal, not money.

Only person I know on margin is a educator who makes less than $100K. It is concerning, but everything is rational.

Is the educator still all in after the last couple of weeks?

Yes. Went on more margin to buy more TSLA. Everything is rational in the end. So he must have the money to take the hits.

When I was 22 I worked for a broker, Marty Finn who was about 60. He pulled me aside and said “Never ever buy on margin.” Then proceeded to show me the carnage from margin calls in a client’s accounts.

On our way to an ice hockey game the other week I said to my son, in reference to tactics to use in his upcoming game, “You know what you shouldn’t do?” My wise-guy answered “Buy on margin.” Smart alec

I have a great life. I’d wish one for everyone. But is is kind of hard to have one without the money as, sooner or later, someone needs a operation, or maybe just orthodontics, or a car needs to be replaced, or whatever. I’ve been poor and in debt, too, and living a great life then was hard.

Now, when the only thing stopping me from eating all of my meals out at nice places is time, calories, and Covid, it is easier for life to be good. Ditto on, when the wife’s car goes kaput, going down to the dealer and writing a personal check for the full amount to get a new one, without even a concern about the checking account balance. That also makes it far easier to have a great life.

On the other hand, I could increase my salary by at least 50% if I was willing to walk down to the train station (a block away) and go into Manhattan every day. But I do not and it is because, despite the money, that would be a big hit on my quality of life.

I see my neighbors run for that train at 7AM and get home around 7PM. While I went to work at 8 and was home before 5 (providing I didn’t just work from home), having already gone to the gym and had dinner before they even get home.

I do expect lower rates of returns with stocks and bonds over the next 10 years, at least real returns. Higher than normal in RRE though. For that reason, 4% SWR may be too high for most early retirees. Probably still OK for regular time period as long as some flex to cut back on expenses as needed. Main reason I think the SWR is higher than Treasury flexibility on spending and always the ability to go work part time or side hussle for $ as needed. My rental properties fortunately have cash yields well over 4%, not counting principal paydown and appreciation, so for those willing to manage their own properties in higher cap rate areas, can still safely expect 4+% income from that. Of course, cap rates have come down in much of the country in the last 2 years but we’ll see what happens from here!

There should be more RE investment opportunities as rates rise and cap rates tick up.

Heartland real estate has done crazy well since 2016. Is I wonder what’s next.

The biggest elephant in the room is not being addressed here.

It all depends on how long you want to live.

For me, I have no desire to live past 50-55 years old. The pains, ailments, and disadvantages that come with aging don’t make life worth living. Deceive yourself all you want, but the quality of life just isn’t there in those advanced ages.

That’s my rationale for having a high withdrawal rate. Once you get to a certain stage, it’s better to face the music and end it.

Sorry you are in so much pain :(

50 years old is only 4.3 years away for me. But I’m really focused on trying to live until 65, until my kids are independent adults.

I hope you will find better health!

Take good care of yourself, eat healthy foods (have you tried keto?). I know many, many folks into their 70s that are very healthy, active and traveling all over the US and the world.

I’ve got to say that at age 61 I COMPLETELY disagree. To be honest, the best years of my life have been the last 10 years, and I may have “lost a step” with my age, I still enjoy every part of my life, including all the golf and tennis I play.

And, since this is a blog about finances (one I’ve read dutifully for the last several years), I now have more money than I’ve ever had to spend on my family, great vacations and overall lifestyle. I get YOLO, but for your sake I hope you get to my age and see there’s still so much more life to be lived.

One thing that might be missing from the equation is whether the person has a chronic illness or something we don’t know about. We just never know the full story unless told.

Yes, this is true. However, of all the people I have known who have lived to advanced ages, I’ve found that quality of life is based more in the mind than it is in the physical body strength. I’ve seen people close to me who have had many physical challenges (including full paralysis) live happily late in life with their mental abilities staying strong. I have known many close friends and family who were physically strong but lost their mental capacities (dementia) and had a very rough road. I know the two can be linked at times (meaning physical ailments can lead to mental ailments), but if I’ve learned anything about quality of life through my own first-hand experience is that the mind is more important than the body.

Hope all this writing keeps my mind healthy then! One of the reasons why I’ve asked my dad to edit my posts is to keep his mind sharp too. He loves to take out the red marker!

Nice post. Regarding your first point, about lowering expectations, one thing to keep in mind is your expected time horizon. For example, let’s say you are 30 and have a goal of retiring by 55–you have 25 years of saving ahead of you. Year-to-year returns, or even a full decade, are not the most relevant time frames for you. Rather, you’re interested in what’s going to give you the best return by the end of that 25 year window. And that means staying invested in the markets, continuing to build your investments, and not panic-selling when the market dips. After all, barring some kind of extreme event without historical precedent in U.S. markets, the market will grow at the end of a 25 year period. Even a 4% return is better than most alternatives, and the “risk” of losing money in the short or even medium term can be (almost) entirely discounted if you are staying in the market for the long haul

On the flip side, if you’re 5 years away from retirement you need to set very different expectations. In this case, downside risk is very real and it makes sense to lower expectations and plan accordingly.

True. One of the most common mistakes I see retirees make is miscalculating the cost of living as they get older. And it is largely due to medical issues that are difficult to forecast.

But other random things happen all the time as well. A natural disaster crushing your home or car. A leaky roof which causes rot and forces a gut remodel.

Anything and everything can happen.

At the same time, there’s more opportunity to make money than ever before.

There seems to be something very odd in your NW target by age after 35 y/o. From 35 to 40 you have net worth double and increase more in real dollars than net worth from 40 to 45. Is your target person retiring or significantly cutting back at age 40? I understand how your net worth can go up at a higher percentage in the younger years (since savings accounts for larger portion of the growth), but how does it go up faster in real dollars?

Higher absolute dollar amount invested, higher income, and returns.

If you disagree, all good. Feel free to share why and your situation. There is not right answer. It is a guide using assumptions as wealth tends to accelerate the wealthier one gets.

I agree, the higher someone’s net worth, the greater gains in absolute dollars, hence my confusion. On your table, someone making 200k should increase their net worth by 1,000,000 from 35 to 40 but only increase NW by 600,000 from 40 to 45.

I’m happy we have a correction now in the stock market. This will flush a lot of people out of the market. This is sad. But this is a very healthy and necessary process for a well-functioning market. Margin accounts were rising too rapidly and options trading was going crazy. We should come back to a more normal stock market after that bout of volatility.

For the withdrawal rate, another way to look at it is 25X expenses should last … 25 years, assuming no return but also no loss of purchasing power (aka negative real return).

Using that logic, 50X will last … 50 years. Obviously :)

And 1% withdrawal rate should last 100 years. Probably more than enough for most people, unless plans include multi-generation trusts.

This is oversimplified, but this simple math shows a very obvious principle. The withdrawal rate will be exactly inversely proportional to the longevity of the funds available.

The original 25X rule was based on an average 30 years retirement (from 65 to 95). Based on historical data, it concluded that any period of 25 years was able to earn at least an additional of 5 years in returns, or a “total real return” of 25% over the period. This was easier to attain, since bonds were yielding more than 4% before, and that interests was increased when inflation was higher.

I don’t know how this will apply going forward. Fed fund rates are still currently at 0%. And even if they are increased, it seem unlikely they will ever go higher than 2% …

On the other hand, quantitative easing insure that bonds stay below 2% (or 3% at worse) even if inflation runs at 7%.

This seems an impossible fight to win for investors.

Particular warnings should be made to those who retire in their 30s (50 years life-span) and have only 25X expenses in retirement funds … This would require 100% total real return over the next 25 years. I have no idea if this is attainable or not. But this seems to be far-streched from the original study …

But, no matter if we have saved enough for 25, 50 or 100 years, I don’t think any investor should settle to get less in the future (in purchasing power) than what they can obtain today.

This would be an ultimate travesty of finance if “delayed gratification for our future self” became “delayed gratification lost to inflation or market fluctuations”.

The real question become “what is the best course of action to preserve our purchasing power considering current financial conditions ?”

After all, no matter how much we saved and no matter how much we have now, we should never settle for less than we have worked for …

The answer is not an easy one.

———-

I was supposed to be going to a concert next week (Wagner), but it is cancelled. We are still in full lockdown here. I’m tired of this pandemic. Can’t wait for the virus to be gone !

Expenses will tend to rise. So 25X expenses may really only be 15-20X. Better to be conservative.

“Expenses will tend to rise.”

Do you mean “rise with inflation” ? Or “higher cost of living, like healthcare or other expenses” ?

I try to think everything in “real term”, or “value of money today”. Because it’s really hard to think about how much things will cost in 30-40 years from now.

For example, if I want to buy a car in 2050, it may well cost 150 000$ for a Toyota Yaris if we have 7% inflation per year during 30 years (assuming this car still exist). But if my portfolio didn’t followed the inflation rate, this is entirely my fault for not having made the right investments…

Anyway, I was just wondering. But I agree to be more conservative in anything finance. Mesure twice, cut once. Because life is not a game we can reset if we didn’t like a move we made in the past.

As for the other bloggers, it’s easier to stick to the herd, especially if you don’t have a finance background and cannot think on your own. And when they see someone with a new idea or new logic, it literally short-circuits their brain.

Keep being you! The blogger you are referring to writes the most boring articles anyway. Snooze fest!

Now really is a good time to focus on what matters most. And it’s not money!

I didn’t care for MMM either

I totally get that it’s scary to think differently and put yourself out there. I guess if I didn’t have a finance background, I would just parrot the same talking points too.

But the blogger does have a finance background, yet for some reason, lacks the maturity to have a ration discussion without resorting to name calling.

Maybe it is a complex? I’m not sure.

Thanks for posting this, definitely needed this reminder! Life is so much more than monetary wealth <3

Love this post

Taking a conservative approach to one’s retirement withdrawal rate with the way rates are is very logical to me. I think folks who react so strongly against this are likely doing some from emotions and feeling like their expenses can’t be lowered and/or they haven’t saved up enough. There’s no right or wrong in PF because we’ll it’s so personal lol. So I always try to keep an open mind about different philosophies and recommendations and find those that fit my life the best.

I certainly don’t expect returns to be strong indefinitely and feel that I’m pretty well positioned to handle dips and conservative returns. But if the markets decide to rocket ship and keep going up and to the right that’s fine by me too!

Yes of course.

Working hard and saving all your life.

You have $3m in retirement portfolio and at 4% withdrawal can spend $120K. You feel great and know that you can have a comfortable retirement and do everything you want.

Then someone comes along and says, no you can only do 1.6% withdrawal and spend $48K. Dreams crushed. Your comfortable retirement is gone.

No wonder our guy got ridiculed and the readers lashed out. He just told everyone that they are screwed. Either double your portfolio before retirement or scale back that comfy retirement and your dreams of travel and relaxation are poof.

These types of articles are good and thought provoking which is what I think was the goal. Can your portfolio handle normal and bad sequence of returns.

Curious Jeff. Do you think most people are so fragile as to read something and then get their dreams crushed? Is that how you felt as well? If so, I might be more powerful than I thought!

One of the things I’m thinking about is writing more of what people want to read to make them feel better, even though it might not help them build wealth and happiness long term. Strategically, it saves me time from debate, minimizes hatred, and creates more friends. I think it’s better to be more generic in thought and stick to the status quo.

I’m too old and tired to debate people. Even if my suggestion is for a withdrawal rate to follow during the first year or two years of retirement, some people immediately take the inverse to try and get a multiple of how much capital to accumulate.

I’m 37 and my dad has been telling me since middle school our generation will need a *minimum* of $2m to retire, but probably more like $4m. He never minced words about finances. I think hearing stuff like that growing up helped manage expectations about how much money I needed to save/invest.

Smart dad! Setting expectations to normalize and formalize the goals.

When i came out with the post, $3 Million Is The New $1 Million, a lot of people were unhappy. But i feel it’s more helpful to tell the truth versus telling people what they want to hear.

Sam if you decide to blow skunky smoke at your readers with feel good pieces, what would your value be? We can get that drivel anywhere. Keep writing real articles and you will keep your following.

Best, 30 yr Wall Streeter

People who are easily disturbed with new ways of thinking or who are easily offended generally have the lowest self-esteem and are the lowest educated.

So ironically, they are the ones who need the most help. But they refuse. It’s a sad conundrum.