The average interest rate by debt type is important to know to utilize debt more efficiently. This article will look at the average interest rate for auto loans, credit cards, and mortgages.

We are an indebted nation thanks to our desire for more and our financial system's ability to grant us more. When used appropriately, debt can help provide for a better life and make us wealthier. When used indiscriminately, however, debt can destroy our financial dreams.

Below is a list of the most indebted nations according to Trading Economics. Currently, America is at ~106% debt-to-GDP and historically ranged from a low of 31.7% to a high of 122%.

Whenever your country's debt is greater than its GDP, it's probably a good idea to encourage your politicians to exercise fiscal restraint lest they take your country to hell during the next financial crisis.

Notice how many of the most indebted countries such as Greece, Italy, and Portugal continue to struggle since the 2008-2009 financial crisis.

Let's review the following types of consumer related debt and rank them from worst to best. We'll also take a look at the latest interest rate by debt type.

Average Interest Rate By Debt Type

The average interest rate by debt debt is ranked from highest to lowest.

1) Average credit card interest rate.

The average APR on a credit card is 17% as of mid-2020. Some go as high as 29.99% if you've got terrible credit. This is such a ridiculously high interest rate which not even the annual returns of the great investor, Warren Buffet, can match.

If you carry a balance, credit card companies are ripping you off. They're secretly hoping you spend more than you make or forget to pay off your balance each month. No Financial Samurai should ever have revolving credit card debt. Use a credit card for rewards points, insurance, a free 30 day loan, and concierge service, but that's it.

I highly recommend reducing the time spent playing the 0% APR balance transfer game. Instead, focus on making more money instead. Don't use the credit card as a crutch to support irresponsible spending habits.

2) Average interest rate for automobile debt.

Borrowing money to buy a depreciating asset is a really bad move. Some people justify their auto debt by saying it's so low at 1.9% or whatever. But 1.9% is still too much when you're losing money on a vehicle every month.

If you are able to spend 1/5 – 1/10th of your gross income on a car, then you shouldn't have to go into automobile debt. If you buy a car that's 1/5 – 1/10th your gross income and can get a 0% loan so you can invest the difference, then fine. Otherwise, just say no to automobile debt.

3) Average student loan interest rate.

The average student loan interest rate is about 4.5% heading into 2021.

The older I get, the more I realize how vitally important education is for achieving financial freedom and happiness. When you have the knowledge and skills to make things happen, life gets so much easier. That said, there's nothing you learn in college that you can't learn for free on the internet. Therefore, skyrocketing college tuition seems more like a scam, especially since higher tuition doesn't guarantee you a well-paying job upon graduation.

Unless your family is rich, choose a college that provides enough free grant money so that you'll be able to pay everything back within four years of graduation. I'm highly biased towards state schools having attended The College of William & Mary for undergrad and UC Berkeley for business school. You can deduct up to $2,500 of student loan interest paid in any given year if your modified adjusted gross income is under $80,000 or $160,000 for married couples filing jointly.

I suggest refinancing your student loan debt with Credible. Fill out your information and get real quotes from up to 10 qualified lenders all competing for your business. Credible is the easiest way to compare the best rates and lenders to make an informed decision.

4) Average mortgage interest rate.

The average 30-year fixed rate mortgage has plummeted to around 2.78%. The average 15-year fixed rate mortgage is 2.32%, which is the best bargain right now. And the average 5/1 ARM is at 2.89%.

Mortgage debt is considered the least egregious debt because it's tied to an asset that historically appreciates. Not only that, the American government allows you to write off all mortgage interest on debt up to $750,000 plus the interest on $100,000 of a home equity line of credit.

The government allows for tax free profits of up to $250,000 for individuals and $500,000 for married couples if you live in your property for two out of the last five years. Finally, the government allows you to defer taxes by allowing you to use the sale proceeds to buy another property under the 1031 exchange program.

Bullish On Real Estate

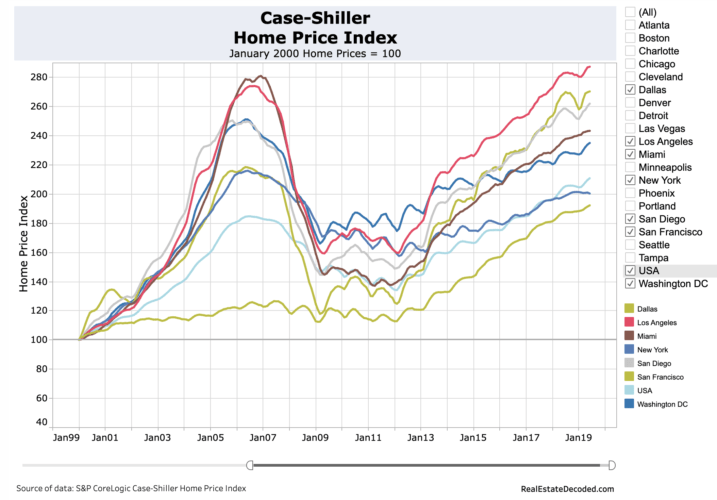

Take a look at this US housing price chart. The clear trend is up and to the right with some cyclical downturns along the way. The gap in price performance between cities like Dallas / Houston and other major cities is one of the biggest reasons why I've been buying heartland real estate. With the remote work trend, technology, and strong job growth, I believe the spread will narrow.

You want to be on the right side of a tank, inflation, the Fed, and the government. The government is pro-housing so you might as well take advantage. You'll want to pay off your mortgage before you no longer have the desire or energy to work. For those of you who've been waiting to refinance or take out a loan, now is probably time to inquire about the latest rates.

I recently refinanced my primary mortgage to a 7/1 ARM at 2.625%. Not only did I not pay to refinance my mortgage, I was given a $500 credit to refinance! It's hard to believe I now pay 30% less a month to own my home than I did when I bought it in 2014.

Debt Is A Tool For Financial Freedom

For those who don't have debt, I commend you for living so fiscally responsibly. The feeling was incredible when I paid off one of my rental property mortgages in 2015. Despite a further rise in the stock market since, I have no regrets.

But to shun debt completely when you're still trying to build your financial nut is a sub-optimal move. If you can borrow for cheap and earn a greater return on your money, such arbitrage should be pursued until you have enough.

Wealth Building Recommendations

Explore real estate crowdsourcing opportunities: If you don't have the downpayment to buy a property, don't want to deal with the hassle of managing real estate, or don't want to tie up your liquidity in physical real estate, take a look at Fundrise, one of the largest real estate crowdsourcing companies today.

Real estate is a key component of a diversified portfolio. Real estate crowdsourcing allows you to be more flexible in your real estate investments by investing beyond just where you live for the best returns possible. For example, cap rates are around 3% in San Francisco and New York City, but over 10% in the Midwest if you're looking for strictly investing income returns.

Sign up and take a look at all the residential and commercial investment opportunities around the country Fundrise has to offer. It's free to look.

Refinance Your Expensive Debt. Now that you know the average interest rate by debt type, you should highly consider refinancing your expensive student loan, mortgage, or credit card debt with Credible. Credible is a top lending marketplace that provides real quotes, all in one place. They have highly qualified lenders competing for your business. It is the efficient way to get the best deal out there.

Updated for 2021 and beyond.

Definitely agree with you on the rankings. Revolving debt not attached to an appreciating asset is deeply unpleasant.

“Borrowing money to buy a depreciating asset is a really bad move.”

This is such an easy concept to understand but I argue tooth and nail with peers who are absolutely stuck on having cars. I have lived in San Francisco for most of my life and I know for a fact that a car in San Francisco is not a necessity for those under 30 and without kids. I did the math over dim sum while my friend spent 20 minutes looking for parking in Chinatown. Basically a low/mid range car with expenses (gas, insurance, parking) cost at least $500/month — and that’s if you kept it for 10 years and paid for it in cash!

I rather have that $500 smackeroo in my pocket every month!

Just to clarify, you can only use a 1031 exchange for investment property. Therefore, if you’ve used a home as your primary residence you will need to establish your former residence as a rental property for a period of time before you can do a 1031 exchange. It is usually better to take advantage of the $500K or $250K exclusion that applies to personal residences assuming the requirements are met. Also, to deduct the $100K equity line, the loan proceeds are supposed to be used to purchase, maintain, or upgrade your home. It is not supposed to be used for consumer purchases like buying a car (at least if you want the interest deduction). However, money is fungible so try to make sure you can verify how the equity line was used in relation to your primary residence, even if you are buying other things at the time the loan is taken out. I’m not aware of much enforcement by the IRS regarding this issue, but you never know when they may target it as an area of abuse.

I generally agree with your ranking, but as one or two other commenters mentioned, I’m not sure that anyone should care too much whether the asset is appreciating/depreciating in terms of whether the debt is viewed as better or worse. The asset itself may be worse from an investment standpoint, but the interest rates are relatively low.

I have a car because I need one to get around (work and personal travel), and if I don’t plan on paying cash upfront for everything, then it makes sense to take on the cheapest forms of debt possible.

A very strong post. Debt, when used correctly can be a positive. I think of my brother who does everything wrong with debt.

On credit cards, he makes impulsive purchases. His card charges 18.99% interest with no real benefits. He is deep in debt. I blame the credit card company because he filed bankruptcy 6 years ago. For them to provide him with a $10,000 line is laughable. My wife and I put all of our spending on credit cards designed for travel credits since my wife likes to travel. Last year, these cards paid us $2500. We incurred no interest. When I was working as a travel warrior, I estimate I earned about 10K per year in economic benefit between cards and loyalty programs.

On the other hand, I know many who could be taking advantage of using credit cards in a smart way but refuse to do so. They are stuck on the credit cards are evil sort of thing.

On auto debt, I am coming more towards Sam’s point of view. I have always leased because I drove only 5-6K mikes per year (my travel was on airplanes) and I only wanted to pay for my depreciation. I was fine with giving the car up and starting over. I always negotiated strong deals. Now that I have exited corporate life, my thinking is that I will keep my current car. It should cost 1/9th of our yearly income off lease.

As for student debt, this hits home since I have 2 teenage daughters who will both be entering college over the next few years. We have saved for this since before they were born. If they are wise we will have enough for 4 years. If not, they should only need small loans, I hope. The mistake I see friends making is that they raid their retirement or take home equity loans on their houses. Unless their kids are going to fund their retirement, I think that makes no sense. I am also against putting your house at risk for that purpose. Loans are the better way to go. Colleges and universities have done next to nothing to control costs on their end. A day of reckoning must happen at some point.

Obviously, mortgage debt is the most sensible debt you can incur. Without it, most of us would never be homeowners. The rates are usually low and the debt is tax friendly. It also allows for leveraging a real asset. However, I only need to look at my brother again for the downside. In 06, he purchased a house for 300K! On his income I didn’t know how that would be possible. As it turns out, it wasn’t. It was an interest only, adjustable rate loan. After the lockup ended, his payments more than doubled. Combined with some shady private loans from his tech school (forgot to mention those above), his monthly outlay by 09 was 4K per month just on those 2 items. He only cleared 2.8K per month after taxes. He begged and borrowed for everyone he knew (I mean everyone) for 2 years before the water finally circled the drain. Lost the house, lost his car, lost his job in the recession. The problem of dream living on borrowing crushed him.

Sadly, he is repeating the same pattern again, albeit with a few differing details this time. In short, debt can be a real tool or your worst enemy.

Regarding your brother, sounds like he is living the American dream actually! So long as he doesn’t lose his job, all will likely turn out OK right? Worst case, he has you to borrow from to bail him out :)

Yes, I would not raid my retirement account to pay for college. I would have my kids go to a cheaper college! 2 years community college, then transfer. I love that method.

The only debt I have left is mortgage debt. And that’s because I just can’t find the checkbook to pay it off. Where did I put that thing?

Seriously? I got stung on all three, and remember when the only debt left was my mortgage. That was a party day!

Hey FS,

Thoughts on the housing market right now? In the market for Fremont ~$1M, but curious what you think the future outlook is like and if you’d buy in this environment or wait it out.

1 million is always going to be a hot market segment. Prices above 2 million have cooled. I think prices will continue to cool for another year or so. Before Uber or Airbnb go public. Don’t be in a rush.

One question on the car thing.. how do you feel about car leases? It’s not a debt per se, but it is a cash outflow. On a standard gas powered car, I’d think it’s not a great idea, but with the new tech like hydrogen cells, all-electric, etc, the tech changes so rapidly, that purchasing the vehicle seems like a poor option. A 3 year lease would generally allow you to reap the benefits of the tech improvements, and not get locked into a car that may not age well after 5-8 years (since the aging bugs may not be worked out of the system). Please note, I’m not talking about Teslas or BMW i8’s, but something along the lines of the Nissan Leaf or Volkswagen e-Golf. (I suppose if a Tesla’s leases is 1/10 of your income, it’s a moot point anyway).

I actually lease my Honda Fit for $235/month after tax after trading my 14 year old car in 2.5 years ago. The $235 is a business expense that comes out to about $155/month after deductions. I leased b/c it was cheap, the buyout of my Fit is only $12,600 after 3 years so I was only paying about a $800 premium to lease for the optionality of returning the keys when done. I’m all into a simpler life now.

I’ve been thinking about going back to Hawaii for a while too.

Related: Buy Or Lease A Vehicle?

The decision to finance a car, all else being equal, still depends on opportunity cost. If the loan rate is 1.9% and you are using money that is earning more than that, taking a car loan is not a bad choice. The same goes for college financing. Of course, more should go into trying to calculate the cost-benefit of the education choice to begin with, which is not always so easy.

As a aside, I had a offspring in graduate school who borrowed the maximum subsidized loans available that did not start accruing interest until the degree was completed. He took the money, invested it, then paid back the prinicipal 6 yeasr later upon competing the degree. In his case he was able to live (and save) on just his stipend so he started work without debt and a chunk of change in the bank.

Wow, I’m just glad that no one got on your case about auto loans and limiting the amount of your gross income you spend on cars. That always seems to hit a soft spot when you advocate spending no less than 10% of your income on a car.

As for credit card debt, I would advocate young people who are starting out to get one and use it build credit. Not saying they should carry a balance, but that they should simply use it and pay it off to build credit. I always advise my younger customers to never spend more than they can comfortably pay off each month.

I wish the government was as fiscally responsible as we are. I don’t get too mad at the idea of government shutdowns because I believe the most mind boggling thing is that we still even have a government. Politicians literally hold THEMSELVES hostage just so they can increase a debt ceiling and spend more non-existent money and no one can figure out what the problem is. And these politicians think they can tell people the best way to spend their money.

Sincerely,

ARB–Angry Retail Banker

Don’t worry about the politicians. Even during government shutdowns, all the Congressmen and women and the President still gets paid.

I tolerated debt early on for education and my first car and home. Now at middle age, the only debt I have is rental property.

I greatly dislike being in personal debt. I feel I have so many more options when I am debt free. The crash of 2008 wasn’t that bad for me because I didn’t have debt to pay so I didn’t have to firesell anything.

However, I am comfortable with cash flowing rental property mortgage. But I am always going back and forth on whether I should pay my existing loan off or use my cash for another leveraged property. On one hand I despise debt. But on the other risk is limited. Worst case is selling investment property out of need which isn’t that bad because it doesn’t affect my day to day.

My aunt told me as kid to never pay credit card interest…that is why i haven’t paid interest in over a decade (ok, i was a little bad in my 20’s)…my wife and i recently got married and thankfully she is on the same page with me in regards to credit card debt…we pay them off every month

Not sure if I get the point of mortgage vs car loan. Shouldn’t the decision only depend on the after tax deduction effective rate? I don’t see how an asset being appreciative or depreciative has much to do with what kind of debt to take out, unless the decision to buy a car vs house is also part of the decision.

No. But that’s cool if you want to just look at the effective rate and not associate it with the asset.

You should always invest in the stock market or even bonds (but I hate bonds) before paying down your mortgage. I totally agree with you Sam. Its a simple rate arbitrage. The not so simple thing is that the return earned in equities is over the long-term and most people hate that. I don’t mind it because I’ve seen how the non-linear returns work over time. Its feast or famine. When you’re nominal rate is like 4% and your after-tax rate is about 2.5% why would you ever give up 8% in equity returns?!?!?! That’s a 5.5% delta that is being flushed down the toilet. And I would argue equities return closer to 11% on a nominal basis.

Great article – avoid all credit card and other silly debt.

If you are using debt to buy a car that is not only a waste of 1.9% interest but it also indicates that you are buying a car that is too expensive for you – hence the use of debt. Buying a car for $30,000? You must be crazy.

We just bought a car for our family for $4,000 and paid in a rolled up wad of cash. No interest, no payment, and we will get more than $4,000 in value out of it. I’m astounded that Americans are paying 30, 40, 50, and 60K for automobiles!!! Its not even an asset people![pardon the hysteria]

PWB, your first comment and second comment are totally at odds. I, too, agree that rate arbitrage is a good thing if used wisely. So why wouldn’t that same rate arbitrage apply to a car loan? Lots of people can use Sam’s 1/10th rule for car buying and still pay $30,000 (or more!) for a car. We could have easily paid cash for our car, but chose to finance it for 1.9% for the very same kind of rate arbitrage you’re advocating. That cash we didn’t spend upfront on the car is now earning us 15% via a private loan.

The trouble would have been if we’d chosen to finance the car so we could splurge on a vacation we wouldn’t have taken otherwise. Many of the people who frequent finance sites like this one have enough financial discipline that a choice to take on debt (even auto debt, and heck, perhaps even credit card debt in the right situation) can be the rational and prudent decision.

First post. Similarities are interesting…..IB for while, MD for awhile, 5.0 tennis player, lots of connections to the Bay Area…. First time I have felt you are off the mark. Debt/leverage compounds timing issues. The ‘itch’ can apply to FIRE as well as greed. I very much realize the potential positive impacts of ‘good’ debt leverage but the reality is people are just spinning that to themselves.

What are your thoughts on where I am off the mark exactly? Are you saying that all debt is good? Please elaborate. Thanks

Agree with your ranking, disagree with your premise….is there really ‘good’ debt. Fundamentally, all debt starts a time clock which people feel they can control but sometimes they can not. Again, realize the power of leverage but the goal should be no debt not ‘good/bad’ debt. I am ready for the replys where people need it but I will still disagree…see the Steve Martin YouTube on debt/Saturday night live.

Sounds good. What is your history with debt and when did you become debt free and did you also retire early? Our paths must have crossed because there aren’t that many, if any 5.0s who aren’t MDs here in SF. We should play some time!

The Debt/GDP ratio reflects national/federal government debt, not private debt. It’s used as a heuristic politically for the point where so-called “insolvency” is supposedly reached, but you cannot compare a cash flow item with a balance sheet item as that ratio is doing. A proper method would be debt payments as a percentage of income (tax revenues), since income (tax revenues) is what pays down debt, not GDP. Most of us have debt several orders larger than our incomes… so its not the size of the debt that is a problem per se; its whether or not you have the cash flow to pay it down. The PIIGS countries do not have the tax revenues nor do they have a central bank willing bail them out nor control their own currency to devalue the real value of their debts, so they’re in a real pickle.

As far as real estate goes, the USA is at the bottom of the barrel in terms of overvalution compared to other countries such as Australia or Canada. I do now know (since I haven’t looked yet) if this is due to increased subprime lending and/or loosening of mortgage restrictions that we haven’t really done again (but certainly have in autos and education).

Related: Why Is United States Property So Cheap Compared To The Rest Of The World?

I struggle with the mortgage being good debt.

In rental property I think it certainly is an I’m in no hurry to pay it down. The leverage is helpfull at least in a generally up trending market, the interest and depreciation turns a gain into a loss (initially) and eventually into a break even for tax purposes.

For a primary residence it gets hazy.

One consideration is a comparison to the risk free rate of return. Generally you’re about even with treasuries even when accounting for interest deduction. If the standard deduction goes up this may be even more close.

Second consideration for me, at least in my state, is legal protection. In the case of a lawsuit (my kid runs over a jogger) my house it protected…my brokerage account is up for grabs.

I’ve come down on the side of paying it off. I realize I’m paying for peace of mind and “insurance” in a way.

Credit card debt? There’s just no excuse for that. If you’re paying interest on a credit card you’re a sucker. But thanks for subsidizing my rewards! I love traveling for free.

The irony is to really enjoy the mortgage interest deduction, it’s best if you make ~$200,000 – $250,000 and can afford a $1,000,000 mortgage.

See: https://www.financialsamurai.com/the-ideal-mortgage-amount-is-1-million-dollars/

Sam – couldn’t agree more with your debt order. A lot of credit card debt makes it almost impossible to get ahead. You’re better off owning that debt (being the lender). Another thing to think about is tax deductibility of debt. If it is tax deductible and cheap then debt (if used wisely) can really help towards wealth building.

Great info Sam. When things get uncertain domestically and/or internationally, I always get the urge to back off my 401k contributions and focus on getting rid of debt.

I’m finally seeing some light at the end of the tunnel of my $150K student loan debt. I calculated that if I put just $200 extra a month in extra payments I can have the loans gone in 2 years. Needless to say I ramped that up right away and hopefully I can get it paid off sooner! I can’t wait for the feeling of finally being debt free.

Your interest rate is either astronomical or your balance is no where close to $150k anymore if an extra $4.8k will pay it off in two years.

It sounds like he has been paying for years on what started as 150k and is now approaching the end.

Six figure student loans are no joke, especially when you are a five figure earner.

They should make it a rule of sorts, that you don’t have to start paying back loans until your annual salary exceeds your total loan amount.

I would hope someone who takes our six figure student loans plans to actually make six figures, and in a hurry.

Debt is a tool or tactic that can be useful. I was once able to use the zero interest balance transfer to tread water for a month until a bonus came in. Taking the max student loan at the start of the semester and paying back what wasn’t used was again useful as I was able to account for emergencies with a little additional flexibility.

My wife and I definitely got sucked into “too much house” early in our lives. The struggle to maintain ownership of the property defined many following hardships. We still own it, but it was a neat thing and we had to get weird several times.

When my wife was in the Air Force and sent out of state, she lived in a coworkers basement and I lived at he police station in between visiting her and working. Meanwhile the house was rented out. Like many aspects of my life, I wouldn’t recommend it, but it can be done!

Very interesting, especially the different rates for credit card debt.

While I’m 100% anti-consumer debt for things like credit cards, student loans, and auto loans, I can definitely see where having debt for things like rental real estate would be beneficial if you’re able to earn more than you pay in interest.

If I were to buy rental real estate (and I DO want to do this when I’m financially able), I think I’d still have a hard time getting over my debt-aversion.

Great post Sam! It is good to break up the debt like you have. We paid down credit card debt, then auto debt (even though it was 0%). Now it is student loans and mortgage, but they still fall at 3x my annual salary combined.

We are an indeed a country of indebtedness and I am not sure how that is going to get better in the near future.

Paying off a 0% loan doesn’t make sense, mathematically.

Thank you for taking the time to compile all of this information. America is built up on debt, and at some point everything has to either get paid or fall down. My only debt is a car loan at 2.79%. It isn’t terrible, but you are absolutely right: why should I pay 2.79% for the privilege to own a depreciating asset? I shouldn’t.

My student loans had an APR of 7.4% which was a killer, I paid those off as quickly as possible. It was painful seeing so much lost to interest every month. But there are people who owe more than my student loans at much higher APRs. If they don’t find a way to get out (such as the Debt Snowball), then they’ll probably never get ahead on anything in life.

Looking forward to seeing what sort of optimal debt structure you suggest. De-risking your personal balance sheet by having no debt whatsoever is generally under appreciated. If you lose your job and a tenant moves out in the night, you will not be happy about your debt or care about ‘optimizing’ your debt load. Great post.

My only debt is my mortgage. 15 year @ 3.0%. I always struggle with paying it off or investing.

I know the math says you should put the extra money towards investments because you can average 7% return and inflation makes the payment go down.

But, the same argument could have been made for our student loan debt that we paid off as fast as possible and that felt absolutely amazing to get rid of. Would the mortgage feel the same?

Also, would you ever consider taking cash out against your home to invest it? I know I wouldn’t but the math says you should.

Interested to see the new post on Debt Optimization.

As for your last question, all I would say is to never invest whet you can’t afford to lose. If you are borrowing against your home, them that’s money you can’t afford to lose. The whole point is to be able to invest your excess cash, not to create another inescapable financial obligation.

Those are just my personal thoughts on the matter.

Sincerely,

ARB–Angry Retail Banker

Paying off the mortgage feels the same. It is a terrific feeling.

I’d never take out home equity to invest. Don’t co-mingle the funds. Lots of people did this during the last bubble and not only lost on their investments, they also lost on their homes.

Related:

Why I’m Paying Off My Mortgage Early And Why You Should Too

Pay Down Debt Or Invest? Implement FS-DAIR

Agreed Sam, even though my student loan debt was originally above 6% (some up to 10.25%) and our car is .9% – the ability to deduct interest and the increased earning power makes student loans less evil than car loans.

We never got into a bad credit card situation, I think I had around $1,500 when I graduated from college and haven’t carried a balance in the last 5 years.

Samurai –

Looking forward to the debt optimization post. Fricken hate automobile debt and am actually just about to put to rest my small amount remaining (i.e. getting rid of it earlier, as opposed to 22 months from now). Debt can be very useful, as you’ve stated, for rentals, as well as the tax advantages of real estate, agree completely.

Thanks for sharing this, talk soon.

-Lanny

im glad you added in the bit on using debt to maximize return and even using a zero percent car loan to get ahead. We fit this description where we have a low dollar zero percent car loan on my main car. That money is invested either in the market or arbitrage into my mortgage which is three percent. I do so based on my asset allocation as I view a fixed rate loan after the fact as part of a sort of bond allocation ( when taking the debt it’s a depreciated expense obviously.

I definitely agree with your debt rankings. Credit cards are the worst if you’re carrying a balance month to month. Now if you are travel hacking they are awesome, especially if you’re using them correctly. However, sadly most people don’t travel hack and lose the rewards associated with their cards.

This is a great analysis and an interesting post. My husband and I have had all four kinds of debt. We eventually got rid of #1-3 and currently have only the mortgage on our house. But we’re also aggressively trying to pay it off soon.

I definitely agree with your debt rankings. Credit cards are the worst if you’re carrying a balance month to month. Now if you are travel hacking they are awesome, especially if you’re using them correctly. However, sadly most people don’t travel hack and lose the rewards associated with their cards.

2 Year Old Triplets – no revolving debt, 1 auto loan (I had to buy a mini-van and didn’t want to spend all of our savings), 1 3.5% APR 30 Year Fixed. Doing it on 1 income, and still saving some (not as much as I want to, but some) towards the future. When the wife goes back to work, we’ll be able to just save/invest her entire income.

It can be done – but you have to be disciplined and disregard the easy spending that comes with having a credit card. It’s a mindset change to say the least.

Wow. You must be busy! Long road ahead of you!

While student loans are evil, they are also unique in that their rate sometimes changes during the life of the loan. For example your SL provider might knock off 0.25% for auto-payment, and the loan might have a clause where the rate is reduced by over 2% after 36 on-time payments. I make this note not just as a correction to the student loan caption, but also so people don’t fail to take advantage of these benefits. It would suck if missing a payment kept your loan at 5.16% instead of dropping to 3%, like ours has.

Why are student loans evil? Sure taking out 150k in loans for a degree that will net you a 40k/year job is a bad financial decision, but evil? Selling someone on the idea that that same degree will be a good idea could be called evil, but the loan itself is an amoral financial product. A hammer is not evil for breaking into a car, the person wielding the hammer is to blame.