Before reviewing my 1Q 2021 and discussing what's next for various asset classes, let's talk about hard things.

Waiting for the opportune time to propose after buying an engagement ring is hard. The ring just starts burning a hole in your pocket. But do you know what's even harder? Writing an April Fool's Day post and not responding to a single comment for two days! I'm sorry for tricking y'all folks. I hope you will forgive me. I'm a jokester at heart.

Ever since I was a kid, I've also been a dreamer. Over time, I've noticed the more you dream, the more good things tend to come true. It must be due to one part positive mindset, one part taking action to achieve your goals. If you go about your day-to-day like a zombie, never dreaming about a better future, I'm not sure anything special will ever happen.

Buying that beachfront dream home in Hawaii costs closer to $15 million, not $10 million as the online estimates say. Sadly, there's no way I can afford it. The funny thing is, one of my good friends can easily afford it, yet he still refuses to live it up!

If the house can earn a $900,000 a year net operating income, a 4% cap rate would give it a valuation of $22,500,000. But it probably earns closer to $500,000-$600,000 a year as the house sits empty most of the time when asking between $85,000 – $250,000 a month in rent.

When in doubt, follow this real estate investing rule: Buy Utility, Rent Luxury. It's much cheaper to rent a luxury home than to buy one. The ongoing maintenance costs are a killer.

1Q 2021 Review Overall: 3.75/5

1Q 2021 went by quickly! Overall, it was a hopeful time due to better-than-expected progress with the vaccine rollout. For example, in San Francisco, everyone is eligible for a vaccine starting April 15, 2021, versus the former expectation of May or June 2021. Now we just have to wait for the vaccine trial data to come out for young kids sometime towards the end of the year.

Financial Samurai is humming along as usual. My wife and I updated another 200 posts or so in the quarter. By the end of 2Q 2021, all posts on Financial Samurai should be fully updated. It's been a blast to revisit some of the older posts from 2012-2015. The key recurring theme is sticking with things for the long term. Good things tend to happen if you keep at it.

On the family front, the kids are doing well. Our daughter is walking all over the place now so we've padded all the floors and corners. She is such a joy to hold every day. Our son got into a language immersion preschool that goes through the 8th grade starting this August. It's nice to look forward to some changes. It's also time for him to meet some friends his age.

1Q 2021 Stock Portfolio Review: 1/5

1Q was pretty volatile. My growth stocks like Tesla and Netflix got HAMMERED as investors rotated into old economy stocks. What's annoying is that I had felt there was a 65% chance tech stocks would underperform. However, I didn't do anything about it because I didn't want to create any capital gains tax liability.

When my growth stocks were getting pummeled, it didn't feel as bad this time because they had all risen so much. All the gains since March 2020 really feel like funny money. Thankfully, many of these growth stocks began to rebound towards the end of March. Let's hope it continues.

After the sell-off, I decided to buy $30,000 in ARKK, Netflix and Tesla towards the end of March. I figured if I'm going to hold many of these names for the long-term, I might as well continue to buy after a correction.

For solely S&P 500 index investors, 1Q 2021 was a fantastic quarter, up about 5.8%. But my portfolio underperformed and closed up only 2.53% due to my heavy tech weighting. Further, bonds had a terrible quarter as well.

Therefore, stock pickers, be careful what you wish for! Sometimes you win, sometimes you lose. In this case, I'm a loser. Notice the widening gap between the orange line and the blue line in my Personal Capital portfolio tracker.

1Q 2021 Real Estate Review: 4.5/5

As more time goes by, it is becoming clear buying real estate in the summer of 2020 and holding onto all real estate assets until now has been a shrewd move.

Demand for single-family homes is strong in San Francisco and all over the country. My tenants have continued to pay on time as they are all gainfully employed. There were no maintenance issues. Further, there is a revival in commercial real estate underway.

The only blemish to an otherwise 5/5 quarter is that my rental property remodel is still lagging. I finally got our remodeling plans approved on 3/9/2021 after 2.5 months of waiting. However, supposedly, the Building Department has not called back my contractor to schedule the inspections despite repeated inquiries.

Each month that goes by is at least $1,500/month in lost rent. I never plan to do another major remodel again. Remodeling is a young person's game.

1Q 2021 Net Worth Review: 3/5

Due to sluggish stock market performance and not changing any estimates on my real estate holdings, business holdings, or alternative investments, my net worth grew 3%. Talk about unexciting. Perhaps if I mark to market all investments, my net worth might be up closer to 6%.

Since leaving work in 2012, my target net worth growth rate has been 10% a year. My goal is to beat nominal inflation by at least 5% a year and to grow my wealth in a less volatile way.

Formerly, in my 20s and 30s, I used the S&P 500 as my net worth growth benchmark. Today, I feel ecstatic if I can reach 10%.

I seldom update my real estate holdings because I'm focused on the cash flow they generate. Net worth is nice, but it is the passive income to pay for our living expenses that counts the most. Further, I like to be surprised on the upside years down the road if I ever want to sell.

As for my investments in alternatives, they are hard to measure because they are mostly in 5-10 year funds. As for my online business holdings, I don't care because I don't plan to sell.

What's Next For Stocks, Real Estate, And Bonds?

At the beginning of the year, my crystal ball had the following estimates by year-end:

- S&P 500: 4,088 (+8% YoY, $170 EPS estimate, 24X P/E)

- US Median Real Estate: +5% YoY

- 10-Year Bond Yield: 1.25% average (started the year at 0.91%)

All three estimates are currently looking to be too conservative given the S&P 500 is already at 4,019. The US median home price is up 11% as of January 2021, the fastest clip in 15 years. Meanwhile, the 10-year bond yield is at ~1.7%.

Stocks

There is still a chance all my predictions could come true. However, 4,200 – 4,300 now seems more likely on the S&P 500 by year-end due to a robust earnings rebound and an accommodative Fed. Instead of the S&P 500 earnings growing by 30% YoY to $170/share, we could perhaps see $180-$190/share. Using a 23X multiple leads to 4,140 – 4,560 on the S&P 500.

At this rate, it is really hard to see the Fed wait until 2023 to hike rates as it indicated during its last meeting. The market is basically giving the Fed the green light to raise the Fed Funds Rate by a total of 0.5% without negative repercussions.

Real Estate

Can real estate continue to go up by double digits year-over-year? I doubt it as 2Q, 3Q, and 4Q comps get harder. With interest rates ticking up, higher prices, and tougher comps, the US median home price growth will likely decelerate. I'm now estimating a 7% YoY price change for the entire 2021, up from 5%.

Historically speaking, anything above 2-3% is a fantastic year for real estate price growth. Thanks to leverage, the cash-on-cash returns will be tremendous.

Supply should increase in the second half of the year, making it easier for homebuyers. If you want to buy property, I would focus on deals in big cities like New York. I'm very confident there will be a huge snapback in demand. Personally, I am looking for a pied-de-terre in Manhattan.

The real estate freight train has a ton of momentum for several more years. The millennial generation is in their prime home buying years. Therefore, I am still a buyer.

The other attractive real estate asset class is hospitality commercial real estate. So far, there are few sigs yet of distressed property sales, except for Hotels. But with so much pent-up travel demand and travel volume surging right now, investing in hospitality commercial real estate that is in need of capital seems like a smart bet.

Check out Fundrise, my favorite real estate crowdfunding platforms to keep track of such opportunities. You will be notified via e-mail when deals or funds come up. However, demand is very high now and deals are getting filled within 48-hours.

Bonds

There's now probably only a 30% chance the 10-year bond yield will average 1.25% for the year. Risk-appetite is too strong as the economy roars back. Therefore, I'm raising my 10-year bond yield average to 1.75% for the year.

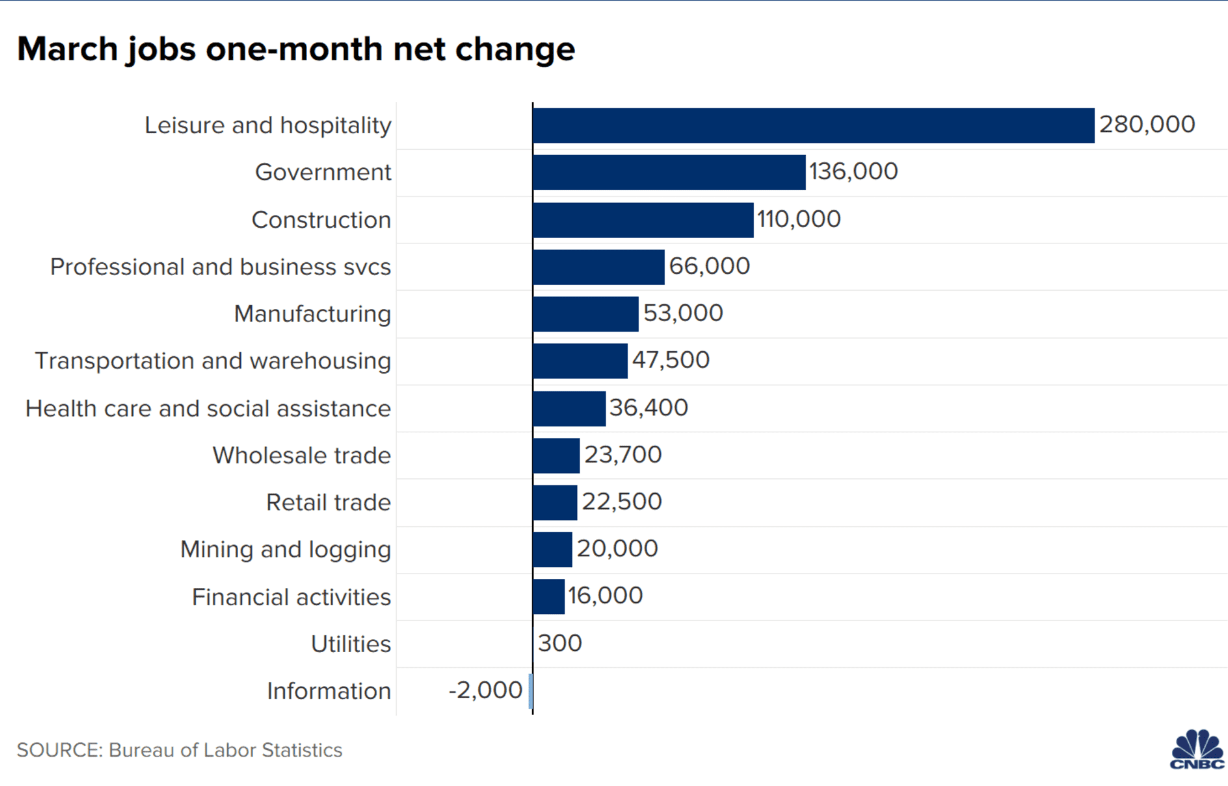

The US added back 916,000 jobs in March, the strongest gain in 7 months and better than expectations. The official unemployment rate is now 6%, down from 6.2% in February. Overall, the US has now gained back 13.7 million jobs (62%) of the 22.2 million jobs lost since the start of the pandemic.

Check out this chart that shows where job gains were highest: leisure and hospitality.

There's now a higher likelihood the 10-year bond yield will hit 2% versus go back down below 1%. So far, the stock market and real estate market are taking higher interest rates in stride. ~3% for an average 30-year fixed-rate mortgage is still cheap, especially if you've kept your job and have seen your stock portfolio balloon by 20%+ over the past 12 months.

If the 10-year bond yield hits 2%, I'll be buying bonds again. I just hope we don't hit 2% until the very end of the year. If we hit 2% by the summer, I expect to see at least a 5% correction in the S&P 500 as the risk-free rate alternative will look to be relatively more attractive.

If you have debt, the higher interest rates go, the less inclined you should be to pay down debt. Your existing debt interest rate becomes relatively more attractive. In other words, the value of your debt with a locked-in rate has gone up.

Getting The Direction Correct Is The Most Important Thing

As an investor, in order to make money, your main goal is to get the direction correct. It's very difficult to pinpoint exactly where something will end up. My direction-calling (stocks up, real estate up, bonds down for 2021) has led me to keep my positions the way they are. I've just been adding to some positions with new capital.

You could get the direction correct and go on massive leverage to get rich quicker like Archegos Capital. However, you just need to also be aware of the consequences. I really don't recommend stock investors go on margin.

Today, I'm slightly bullish on stocks, bullish on single family homes and commercial real estate, and still slightly bearish on bonds.

My existing net worth allocation, excluding business equity, is about 30% stocks (70% index funds, 30% mostly in tech stocks), 40% real estate (includes real estate crowdfunding), 20% bonds (mostly CA munis), 8% alternatives (venture debt, private equity), 2% risk-free.

If I had $1,000,000 to invest right now I would:

- Invest $200,000 in hospitality and industrial commercial real estate deals

- Invest $200,000 in a diversified private eREIT to take advantage of the overall real estate trend

- Invest $200,000 in my favorite tech stocks or funds that have corrected by 20%+

- Pay off $150,000 remaining in a vacation property mortgage that is stuck at 4.25%

- Sit on the remaining $250,000 until there is another 5%+ correction in the S&P 500 or another 10%+ correction in some of my favorite tech stocks. Manhattan real estate is also really calling to me. I don't mind holding a good amount of cash here.

Overall, 1Q 2021 was a good quarter. I continue to expect 2021 to be a profitable year. By June 1, 2021, everybody I know will be fully inoculated. Then, I think it's really time to enjoy our wealth more.

Related posts:

1H 2021 Financial Samurai Review

Readers, how was your 1Q 2021? What are your forecasts for the rest of the year? Do you think the good times can continue? How would you invest $1,000,000 right now? Disclaimer: Invest at your own risk. There are no guarantees. The investments made in this post are mine alone.

You can sign up for my free weekly newsletter here. I've been helping people achieve financial freedom sooner since 2009.

I enjoyed reading today’s newsletter. You said you invested 30% of equity proceeds into bonds. Is this still individual Cali muni bonds, if not, what bonds are you buying? All individuals or ETF’s/mutual funds? A new post on bonds would be great! Thanks for your work.

If you had $1 million to invest, none of it would go into farmland through one of the platforms?

Sam,

Firstly you totally got me with the April Fool’s post. Showed my girlfriend and everything so well done.

Broadly I agree with your forecasts.

I’m long equities with an overweight in tech and will top up on pullbacks. I think the long duration/inflationary argument makes sense but I think these stocks will continue to grow into their multiples. Not to mention that they’re basically defensive stocks now anyway. If QE turns into QT then that would be the catalyst for a bear market in my opinion but just can’t see that happening this year.

I don’t own any property (aside from my house) but think that RE outside of cities will continue to narrow the gap to city RE as the majority of companies make flexible working part of their norm. Agree there’ll be a bounce back in city RE, but I think the fundamental requirements of a home have changed for a lot of people. They want space, gardens, a dog etc not a 500 sqft apartment. Also, I live in the UK and young people are obsessed with owing RE unlike in Europe where they rent forever. That tail wind will keep prices moving up for a long time (unless we start seeing rates head above 2/3%).

Underweight bonds on the basis that central banks will raise rates sooner or later (most likely sooner). Plus just don’t really see the point for a sub 2% yield apart from the lower vol and hedging properties.

I also have a small % holding of crypto. I agree this is classic late stage bull market stuff with all the SPAC talk and hunts for yield, but there seem to be a lot hedge funds and institutions adding this to their asset allocation which makes me think that we may be looking at something that is more credible than just retail investor mania.

Your posts are great btw, keep up the good work.

Ben

Lol! You really got me with this one :)

BTW thank you for your analysis, I really enjoy your blog posts!

I am worried about another housing bubble. I know interest rates are low and fixed but, I worry about all the millennial’s purchasing out of their price range and not being able to afford it. With all of the bidding wars happening, I feel like people are jumping into something without doing the appropriate homework. On top of that the govt won’t be able to bail out people forever.

Is there a chance that in 6 -12 months we start to see the housing market collapse again? If that is the case, I think I would want to hold some cash and purchase something after the bubble bursts.

cheers,

s

Always a possibility. I wonder whether there will be a flood of supply one forbearance is over end of this year and whether there will be enough demand.

Building up a cash hoard now for this potential event is a good idea.

I think you understand how powerful the gov’t is at bailing people out forever.

I think the government is only bailing the banks through the people.

Nice post! I really appreciate your quarterly reviews.

Too bad the post on April 1st was but a joke. I guess there’s always next year!

Ok, where’s the April Fools post? I must have missed it and don’t see it under the Latest Post section!

If you click the link in this post in the intro, you will find it.

Hmmm… makes me wonder about whether readers see my link placements now in my post! Any tips? I always include relevant links in all my posts.

And here it is again.

Here is also my e-mail list for posts and my e-mail list for newsletters.

Thank you! And lol at the post. That beach house looks very dreamy though…

Anyway, the link is there! Sorry, I just overlooked it.

I’m curious to know where the stock market estimates come from. Predicting 1 year returns is notoriously difficult but most analysts that I read predict long term returns well under historical averages due to sky high valuations right now. Are you predicting strong long term returns with this year just being part of that trend or are you predicting strong performance in the near term which eventually comes down to earth?

I’m predicting returns based on more than a 30% EPS rebound in the S&P 500 for 2021. Starting in 3Q I will make my best guess assumptions for 2022 earnings and valuations, depending on multiple factors. Predictions are hard, but work best one year at a time.

What are you predicting for this year and how are you positioned? I’m hoping more people can share their analysis as well.

Check out this post I wrote in March 2020 on how I went about predicting a stock market bottom. It has more bottoms up analysis.

How To Predict A Stock Market Bottom Like Nostradamus

I posted a response earlier with my analysis, but they don’t appear to be making it through. Not sure why.

Not sure. Maybe got caught up in spam and then flushed out by mistake. Feel free to repost.

Short-term stock market predictions are notoriously difficult to make with any accuracy, so I do not even try. I look at various valuation metrics to try to gauge return expectations over a 10 year time horizon and then shift my asset allocations accordingly. For example, in 2017 the Shiller PE ratio went above thirty, which pushed 10 year return expectations into the low single digits. At that time rental properties in my area still hadn’t recovered from the housing crash, so I sold some of my position in domestic equities in favor of rental real estate. As it turns out, the stock market has done very well since 2017, but my rentals have done even better. There are still 6 years left before I can tell if the shabby ROI predictions for the S&P in 2017 come true, so I guess I’ll have to wait and see, but either way I won’t be upset.

Now that all valuation metrics (Shiller PE, PE, market cap to GDP, Average Investor Asset Allocation, etc.) Are at or near historic highs and projected returns are even lower, I have sold nearly all of my position in domestic equities in favor of international equities with more attractive valuations relative to their sector weights. I will consider buying back into domestic equities if/when the Shiller PE goes below 30 and other valuation metrics return to something approaching normalcy. Until then its international and emerging markets, real estate, and perhaps a dabble in alternative investments for me.

Reading your article on your method, it appears that you are assuming that the PE ratio will remain relatively steady and that the recovery in earnings will drive shares higher. This could be true, but I am curious to know how much of that recovery you believe is already priced into the PE ratio. In that case, even a fairly large earnings recovery could result in a reduction in the PE ratio rather than an increase in share price. Also, that analysis is pretty short-term. I am still unsure as to whether or not you think that the high valuations endanger long-term returns, but you think the short-term is positive or if you think valuation concerns are overblown.

Sounds good to me. At the end of the day, you’ve got to investment in a manner that’s best for you and nobody else.

For us, we are shooting for a 10% annual net worth increase in as low-risk a way possible. As two stay at home parents, we want to stay at home until both our kids start attending school full-time. That means 3.8 more years. We are going to try and do everything possible NOT to have either one of us go back to work for income, healthcare subsidies etc.

Related: Focus On Trends When Investing

There was a nice WSJ article today in which DR Horton made a 50% GM selling an entire 120 home subdivision to Fundrise. In other words, Fundrise is one of the firms pricing out traditional real estate firms / individual buyers in the housing market.

Why should an individual who invests on the platform expect their returns to track the real estate market when Fundrise is over-paying? I’ve always believed that you guarantee your outcome based on buying right…is this not the case anymore?

Check out this response from Fundrise on the purchase and why they bought.

You got me real good on the April fools post. I thought you’ve finally decided to live large

Sorry. Pauper for life! Don’t want to get too soft before herd immunity. Less than 12 months to go before we can really live it up. So let’s rock before then!

I’m similarly conservatively positioned when it comes to equities and have high cash as I dumped all bonds. I also have a health chunk in illiquid startups.

A single digit allocation to crypto in prior years has driven outperformance for me in 2020 and ytd. Let’s see where it goes from here.

Congrats on your crypto holdings and hopefully your angel investments hit it big!

Hi Sam,

Totally agree with you buying a good primary residence last summer was the best financial decision ever! I bought a 1.2m 5000sqft sfh in your home town McLean VA last August. Now six months later, similar homes nearby are selling for 1.4-1.6mn. It’s def gone bananas!

Now there are a lot of FOMO going on in the RE market. People have become very irrational, offering 100-400k over asking, waiving all contingencies and often side unseen… Do you think this is still good time to buy more properties? Thinking about getting more sfh rentals in NoVa areas, but the craziness feels scary…

Thanks for your insights!

Maria

I sold my house in NOVA in November. I listed it on a Thursday, had 25 showings by Friday, and received multiple full ask offers. I had a couple with full ask plus escalation, and all of them were received with zero contingencies. I ended up selling the house on that Sunday night of the weekend at well over asking. Went under contract, and then received two additional backup offers at above ask as well. The DC/NOVA market is definitely insane, and it felt great. The flip side of course, I went to buy a house in NH and I had to beat out 11 other offers on a property that listed on a Friday night, with a all offers due by Saturday night, for an owner’s sell decision by Sunday. Luckily I won the house, but I too had to buy with no contingencies and over asking as well.

Looking back I kind of wish I kept the house in NOVA as the property value has risen again, and I could have probably got another $50-100k on the sale. Oh well, on to the next one.

At least you bought another! My goal has always been to hold onto my real estate holdings for as long as possible. But when my son was born in 2017, I just didn’t want to deal with five unruly guys anymore.

So the key is really to almost always reinvest the proceeds. And that’s what we’ve done!

Makes sense. Part of my issue for not holding was the distance. I didn’t want to be 8 hours away from a rental unit. So selling it off eliminated the fear of having issues so far away. I’m now looking for another lake house closer to me in NH and will definitely rent that one out and hold forever once found as well. I’m down to only 4 properties currently, and at least they are all in the same 4 hours radius now. No longer having units in NOVA will be a change but at least I can always rent luxury when I visit as needed.

Good old McLean Virginia. I think it’s always a good time to look. There are often times anomalies where you can get a relatively good deal. We are also so many ways to negotiate but I should probably bring those up again in a future post.

The thing is, I think it’s going to be a multi year trend in housing. Institutional investors are gobbling up neighborhoods. Maybe there might be better deals when the moratorium and later this year.

Every real estate transaction is different. It is always worth looking in my opinion.

Generally agree with your thoughts, but I think residential real estate will be up at least 10% this year…many markets might achieve that by the end of this month(4/30/21 vs 12/31/20) plus more, if slower, appreciation after that. I’m estimating 15% nationwide on RE this year (20-25% on the lower end and 10% higher end with middle in between those two). Normally you’d see a large increase in construction starts to sell into this demand environment for housing but construction costs are going up faster than prices are and labor is very tight. And spring buying season is just getting started. One of the townhome communities near me the 3 bedroom 2 bath were selling for $175k in October are going for $220k now as an example.

My Networth (NW) has increased by roughly 5% in the first quarter. This put my number solidly over my year end goal of 2 Mil that I set out to accomplish in Dec 2019.

My goal for Q2 2021 is to complete payoff of rental home number 2, leaving a final single family home rental with a mortgage of 3.25% and my principal residence at 2.5 %.

My wife and I purchased our dream home in Oct 2021, so we’ve been sorting out/updating some items and getting accustomed to a larger home, larger lot, and all things that come with it. Overall, we are enjoying the time with our daughters still in the home for a short while.

As for the 2nd half of 2021, I remain cautiously optimistic. I’m going to increase my cash savings through the end of the year with the deletion of the second rental mortgage, continue to Max my retirement savings account, and hope to travel a couple of times by year end.

Still bummed you didn’t buy that dream home, Sam. Lol

Nice! And congratulations on buying your dream home.

The funny thing is, we are living in a really nice home we bought last summer. So I won’t be itching for a dream home for a while, maybe if ever. It’s always fun to look though.

Hey Sam congrats on a solid first quarter. 3% when it’s nearly double the risk free rate is nothing to sneeze at!

As a NY metro resident who’s been loosely keeping an eye on Manhattan real estate, your comment caught my eye. Just wondering if you’re looking at it from a crowdfunding standpoint or potentially buying something that could possibly be managed at an absentee owner?

Actually, 3% is ~7.5x the risk free rate (1.03^4 – 1 vs 1.7%) since you have to annualize the quarterly gain vs compare the full year on the 10yr treasury

Good point Rob, thanks. Even more reason to be grateful!

I mainly looking to buy a pied-à-terre two bedroom condominium in a prime neighborhood like the UWS or Greenwich Village.

I think it’s really great that so many people have fled the city to give people who have stayed and investors and opportunity to buy up real estate at a discount.

I started my career in New York City, and the opportunities are just so amazing there. Therefore, I have this dream that maybe my kids could find opportunities there as well one day. By buying in New York City, I will have two of the greatest cities in America covered with regards to housing.

Besides, I just love New York City for six months a year. It’s truly the best city in the world. And I hope the people who stayed back during the entire pandemic all get raises and promotions.

Looks like they are about to get another large tax increase instead (see WSJ article). I’m not sure NYC is going to come back this time between taxes going up + more remote work flexibility. 60%+ marginal top tax rate if this goes through, and it will get worse if federal taxes go up again as well. Detroit was once one of the richest and most powerful cities in the country….now…. I think NYC could end up being the Detroit of the 21st century or at least a repeat of the 70s-80s.

I’ll definitely take the other side of the bet that NYC will end up being the next Detroit! Ah, I love the markets. So much opportunity!

I think the banking centers will continue to move to lower cost but similar power cities like Charlotte (Truist, BAML, WF) and I just don’t see the other industries coming back. NYC is too expensive, the new taxes make it even more expensive and white collar workers like working remote. Add on to that a 65% marginal tax rate and a long commute to do NYC, I’ll happily take the other side of the bet, and I’ve been to NYC probably 60 times in the last 6 years (NYC doesn’t even make my top 20 places to visit of places I’ve been to, much less like to visit).

Maybe it won’t be Detroit (although Detroit likely didn’t see it coming either – people today forget Detroit in 1950s was dominant) but it could very easily be a repeat of the 70s and 80s, which were very difficult years.

NYC also has a huge problem that 5% of their workers account for 60% of their tax base, and that has grown over time and the new tax proposal makes it even worse. If a decent percentage of those are gone for good, or leave after the tax increases, they will have to make significant cuts to spending or keep raising taxes, both of which have a lot of issues.

Lastly, NYC has a ridiculous amount of hotel inventory and airbnb inventory, no real reason to own there when you can invest in much higher cap rate markets and rent when you want to visit. As you say, rent luxury (NYC)

I’ll join Sam on the other side of that bet. Obviously different circumstances, but I remember many predicting the demise of NYC (who would ever live/work in a skyscraper again??) after 9-11. Opportunity knocks..

Congrats on getting son into language immersion program. Must be a load off.

Looks like you picked up some ARKK near its lowest in Q1. Well done. I’ve stayed away thus far but contemplating putting a little in myself — do you think it’s too late if I haven’t already been in?

Personally, on the RE front, I’m still dealing with a tough time renting one of my 1BR units in prime Dolores Park, it’s been 2-3 months and other properties have been hit with some vacancies in SF which need updating, so I’m personally a little over RE problems at this moment to appreciate the long game.

Lastly, if you’re predicting S&P 4200-4300 why wait for a 5% correction at this point? What if it never goes on sale more than in 1-2% dips?

For your April 1 post, I caught on fairly quickly but I was still hoping to see a real listing so I could make I own $2M below list price bid. ;)

Personally I’m 50% stocks, 5% cash/ultra short term bonds and 45% real estate. I don’t see the point of bonds since my real estate serves a similar purpose of cash flow and reduced vitality.

I update my real estate valuation once a year with a conservative number because like you, I’d like to be surprised on the upside. Unlike you, I’m very much for used on appreciation as opposed to cash flow because I like to minimize taxes.

Ideally I want to generate just enough income to cover my expenses. I cash out refi my equity quite regularly to keep leverage and interest expenses up and use the proceeds to rebalance my portfolio.

My bond position is almost entirely California municipal bonds that I’m just holding individually until maturity. There are no taxes on the interest payments, so it’s really nice, especially if Biden raises taxes. That’s something to think about as well. The value of municipal bonds will go up relative to other bonds in a higher tax environment.

Real estate just has been going absolute BONKERS. I don’t understand it at all. I keep wondering if it was like this during 2005 – 2007 when real estate was absolutely booming.

Hey, even if it was an unexciting 3% growth, a 3% net worth growth is better than a 3% net worth decline.

I can’t believe there’s an actual possibility that the S&P will return another double digit growth this year. That’s just insane. Even after so many double digit growth the past years. I don’t know how to make sense of this market at all.

That makes total sense that real estate is doing well and will continue to do well. Rates are low, we’re all spending more time at home, the demographics friend is hugely positive, and some people have saved so much money and have made so much money since the pandemic began.

This time around, it is much much much harder to get a mortgage then in 2005 in 2006.

Any thought on Bitcoin as a store of value/diversification tool? I suppose if you own Tesla that gives some exposure to it indirectly.

I think it’s worth speculating on with a small percentage of your investable assets. As a store of value, that’s pretty good because who wants to spend it if it has the chance to go up further?

But in a bull market, such alternatives I think will lose its luster as there is more joy and trust in the system when it’s working.

I’m looking to cash out refinance in 2022. I

Can’t right because my mortgage company says I need two years of rent income. Will interest rates still be low in 2022?

That is what I had done. A week back my cash out refinance was closed and I have $500k in my account. It is 30 yr mortgage at 2.69% rate. I am planning to invest the amount in robo advisor platforms like Betterment account, REITs and Growth stocks/ETFs.

In 2022, My crystal ball says the average rate for 30 year fixed mortgage will be 3.65%. That’s about 0.3% higher than it is today, and still low by historical standards.

What a clever April Fool’s post! haha I love your wit and creativity. It certainly is fun to dream about a house like that. More fun to visit for vacation then to actually own and maintain it though I’m sure. I have a hard enough time keeping my current house clean, I can’t imagine trying to keep a mansion that size clean. haha

Thanks for the Q1 recap. I can’t believe it’s April already! I gotta get back to work on my goals. Here’s hoping for ta great Q2!

“ More fun to visit for vacation then to actually own and maintain it though I’m sure”

I think that is probably correct! And again, if that was our main home that we could live in all day, I think it would be really really nice. We just need to have a lot more money to be able to comfortably spend big bucks on maintenance and stuff.

Manhattan RE is coming back fast! You may have missed it as inventory is low

It is indeed, but there still a ways to go.

I was able to use the tech stock downturn to harvest some losses and am going to shift my active stock picking into my IRA after 30 days.

Glad to see your take on bonds. I had been avoiding earlier in the year, holding cash and alternatives instead and that trend will continue.

One strategy I’d highly recommend is selling OTM puts on things you’d be happy to buy at a certain price on a pullback. Think of it as a limit order where you get paid to wait. If you’re worried about a tail event, also buy a lower strike put for downside protection (bull put spread). Easy to do well over 1% per month with this strategy. I target 2-4% per month.

I think that’s a good strategy. And I should probably spend more time on it. So far, my strategy has been to focus on Financial Samurai and focus on asset allocation and buy the dips.

Great April Fool’s joke!!! You had me dreaming!!

January my S&P prediction was 4050. . . .it’s 4250 now. The higher, the better!

Thanks for all you do for us!

Sounds like a reasonable target to me!