I recently realized something that completely reframed how I think about income in America: a $200,000 household income is no longer middle class. Instead, under increasing college financial aid formulas, earning up to $200,000 now qualifies as low income or even poor.

Being labeled “poor” or “low income” doesn’t sound great. But if $200,000 is the new poor according to these elite universities, there are suddenly real advantages to earning less for families. I'm amenable to this new label, as that's all it is. The key is to understand what these changes mean for your family and how you can prosper because of it.

I’ve long believed the middle class is the best class in society. You’re not attacked for being greedy like the rich often are, and you’re not dismissed as lazy like the poor sometimes are. Politicians chase you because you’re the largest voting bloc. As a result, middle-class earners can move through society with fewer judgments and less friction.

There’s power in being part of the majority. That’s why if you earn a middle-class income, rejoice! You are loved and protected. And if you earn a high income, pay massive taxes, and grind through endless hours at work never seeing your children, you should seriously question whether the tradeoff is still worth it.

When I went from a high income in finance to zero active income in early 2012, I became poor. Yet it felt like an enormous weight had been lifted. I was burned out and desperate for a break. No longer working five months of the year just to keep a dollar of what I earned after sixty-hour workweeks was liberating.

Today, I wonder whether being “low income” might actually be better than being middle class, thanks to expanding benefits, less social pressure, and the possibility of a healthier work-life balance.

Once your basic needs are covered, extra income adds surprisingly little to overall happiness. A $200,000 household income should be enough to meet most families’ needs. And clearly, $200,000 is a great income if you live in a low cost area of the country.

$200,000 Is The New Low Income Limit According To Yale

On January 27, 2026, Yale University announced it will offer free tuition to students from families who earn less than $200,000 a year. For students from families earning under $100,000, essentially all costs associated with attending Yale (room and board) will be covered.

Although roughly 96 percent of students who apply to Yale will not be admitted, this is fantastic news for those who are and whose families fall under these income thresholds.

In effect, Yale has determined that any family earning up to $200,000 is low income, or poor. I am sure Yale will also consider family size and adjust thresholds accordingly. After all, it is far easier to support one child on $200,000 than it is to support four.

At the same time, Yale is implicitly signaling that families earning less than $100,000 are considered too poor to afford even one dollar toward college. After spending eighteen years providing food and shelter for your children, Yale now believes it is their responsibility to cover your adult child’s living expenses for four or five years. Awesome!

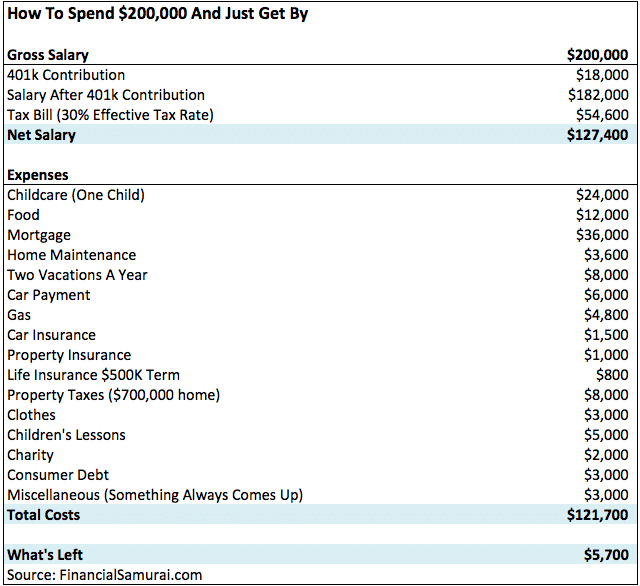

While it may sound strange to describe a six figure income as low income or poor, I have written several articles with detailed budgets showing how difficult it is to get ahead in major cities earning $200,000 or even $300,000 a year. Many readers objected to my conclusions, but it is validating to see the institutions closest to the money agree that $200,000 isn’t that much money for a family to survive on.

How Assets Are Considered By Yale And Other Institutions Is Unclear

Even though a disproportionate number of students at Yale and other Ivy League universities come from high income households, this move is still a generous gesture and brilliant marketing. Most people will be surprised to see $200,000 defined as low income.

As personal finance enthusiasts, however, we understand that net worth and investments matter far more than income when it comes to achieving financial freedom. We also know that where you live matters for how far your income goes.

The definition of FIRE I proposed in 2009 when I launched Financial Samurai is simple. The ability to generate enough passive income to cover basic living expenses. If you can live off $25,000 a year in passive income you are financially independent. If your passive income is $300,000 a year but your expenses are $400,000 a year, you are not.

The goal is to make your money work for you so you have the option not to work. Further, investment income is generally taxed at a lower rate than W2 income, as it should be, since that money has already been taxed.

When I read Yale’s announcement, I could not determine how assets factor into financial aid decisions. At some institutions, a primary residence is counted towards contribution. At others, it is excluded.

What about parents who diligently saved into a 529 plan for eighteen years and accumulated enough to pay for all four years of tuition while earning “only” $160,000 a year? Do their admitted children get free tuition or should they be expected to pay something? The questions are endless as Yale uses the vague words “typical assets” next to families who make under their new income thresholds for financial aid.

Below is an excerpt from Yale’s announcement that offers broad statements but few specifics.

By raising the threshold (for zero parent contribution) to $100,000, nearly half of all American households with children ages six to seventeen would now qualify for a financial aid package that does not require parents to contribute anything toward a student’s education. Under the new policy for families earning under $200,000, more than 80 percent of American households would be eligible for a Yale scholarship covering at least the cost of tuition.

Today, more than 1,000 Yale College students receive a zero parent share award, and 56 percent of all undergraduate students qualify for need based aid. The average grant for students receiving aid this academic year exceeds the annual cost of tuition.

Yale also provides additional grants for winter clothing, summer experiences abroad, and unexpected financial hardships.

Lucky for you, I have two comprehensive articles that explain how to pay for college and how to get free money for college. If you do not have the time or patience to navigate it on your own when the time comes, there are also consulting firms that help families save money or maximize their college financial aid offers.

Focus On Building Net Worth, Not Income

If you can find clear details on how assets are treated under these new income thresholds, I would love to see them. I could not find any. If you are a college financial aid officer, please share your insights!

What is clear is that Yale and other elite private universities emphasize income over assets when defining financial need. The same framing dominates political discussions around taxes. Income is easier to grasp and easier to message. But if we must continually trade time for money, we will never be free.

That is why I believe focusing on building a high net worth is far superior to chasing a higher income. As income rises, taxes rise under a progressive system. Once you reach a marginal federal rate of 25 to 30 percent, you may begin to question whether the extra effort is worth it. And if you disagree with government policies or see waste and fraud in your community, your motivation to work harder just to pay more taxes may fall even further.

If your family earns less than $200,000 a year, feel good about your future. You are earning enough to raise a couple of children comfortably in most parts of the country. Even earning $150,000 – $200,000 with two kids in New York City or San Francisco is manageable if you avoid private school tuition.

And if your children happen to be exceptionally talented or gifted, they may even attend a top university for free, tremendously alleviating your financial burden. Although, some say this new announcement is simply a play by Yale to virtue signal and admit more students who can pay full tuition .

Attracting Top Talent Is Competitive For Colleges Too

While many families fixate on how hard it is to gain admission to top universities, from the schools’ perspective, competition for the best students is intense as well.

With Yale offering free tuition up to $200,000 of household income, other top universities will almost certainly follow to remain competitive. Less competitive private colleges will need to offer even more generous incentives to attract top students. This is great for all middle-class and low income families.

Within the higher education ecosystem, the universities with the largest endowments will continue to dominate. It is impossible for a fantastic public institution like The College of William and Mary with a $1.5 billion endowment to compete with Yale’s roughly $40 billion endowment. In a final twist of irony, the rich get richer. And that is likely how it will remain unless someone or some institution deliberately intervenes to level the playing field, if only for a little while.

Readers, do you agree that $200,000 is the new threshold for what constitutes a low income, lifestyle, or family? Is a household income of $100,000 effectively poor when compared with $60,000 plus in annual after tax tuition at private universities? And do you agree that the middle class is the best class in the world?

Stay On Top Of Your Finances To Comfortably Pay For College

To maximize your college financial benefits, you need to start planning by your child’s freshman year of high school, if not earlier. Colleges will look back at your family’s financial history for at least two years, and sometimes longer.

One tool I’ve consistently relied on since leaving my day job in 2012 is Empower’s free financial dashboard. It remains a core part of how I track net worth, monitor investment performance, and keep cash flow honest. If your child does get free college tuition, you can likely retire earlier.

Through Empower, you can also get a complimentary portfolio review and analysis if you have more than $100,000 in investable assets linked. You’ll gain clearer insight into your asset allocation, risk exposure, and whether your investments truly match your goals for the years ahead.

Small improvements today can meaningfully compound into greater financial freedom over time.

Empower is a long-time affiliate partner of Financial Samurai. Further, I did some part-time consulting for them in person from 2013-2015. Click here to learn more.

To expedite your journey to financial freedom, join over 60,000 others and subscribe to the free Financial Samurai newsletter. You can also get my posts in your e-mail inbox as soon as they come out by signing up here. Financial Samurai is among the largest independently-owned personal finance websites, established in 2009.

Seems like Yale alludes to assets a few times in their financial aid page so it sounds like they definitely take it into account –

https://admissions.yale.edu/affordability-details

Doesn’t seem like a situation where those cheap FIRE people get subsidized healthcare with all growth stocks!

Yeah I’m relatively pessimistic on this, seems like a way to keep increasing tuition for people that diligently saved for college. I guess it’s like a progressive tax. I doubt Yale will admit more higher income students since they don’t need the money.

Consider this from Yale’s progressive politics perspective. Charging $70K per year for tuition when the median US Household income is about $80K is simply obscene. This is the ratio the administration is trying to obscure with this proposal.

I appreciate you outlining how families are impacted by the new lower-income criteria. Seeing the actual figures and comprehending the implications for various household sizes is beneficial. This kind of clarity makes it easier for consumers to plan and modify their budgets in light of growing expenses and shifting economic situations. Do you believe that more conversations about financial assistance programs will result from this change?

Absolutely. More conversations, GREATER aid by a larger number of colleges to stay competitive, and more financial planning that could ultimately reduce the number of years a parent has to work if they can get more free money for college.

As a parent, I’m 100% focused on generating enough money to pay for college and hedge against college not being enough to land my children jobs 15-18 years due to AI and globalization.

So seeing this news, and then forecasting greater aid from colleges to students is a great positive.

It definitely depends where you live. Homes in the $200k range and under are common in my small Texas town. That means earning $200k per year would make you rich… And it’s possible, with doctors, lawyers, business owners, and even trades working enough overtime (or two earners). But I know if you live in a city that people in other countries have actually heard of (NYC, LA, Chicago), you probably are not as rich even with such a high income. That’s the truth of it!

For sure! Which is why it is amazing that Yale University and other similar universities are offering full tuition now if you can get in.

More trategically, if you talk to the finance departments of these universities, they will likely also admit fewer children from this income group and admit more children whose parents can afford to pay full ticket.

So there is a chance that the middle class, which is definitely between $100,000-$200,000 income, gets squeezed the most.

A great PR move by Yale. But they will essentially accept fewer middle class kids from families making under $200,000 and MORE wealthy families who can pay full tuition.

Same thing is happening at Harvard, Princeton, and MIT.

Yes, I think the middle class, which is really this income level, will actually get even fewer opportunities.

If universities like Yale and other private universities, consider me low income or poor, and unable to pay for tuition, food, and living, I’m all for it!

Maybe with the universal basic income and more generous private school support, life really will get easier for families.

Good initiative, but also a form of virtue

since nobody can get into the university and 15% of its students come from the top 1% of income.

$40 billion is a huge endowment. This is the least they can do. But if they really wanna help society, they can stop gatekeeping and expand the number of seats available.

So a $700K house in IL is paying $15K in property taxes sadly, in a great school district an hour outside of Chicago. I wish $8K was more like it!

Sam – stunned by the “fact” that $200k per year qualifies as low income (perhaps a stretch in my view). Correct me if I am incorrect but the median HH income in the US is approximately $83k. I am unclear on what percentile $200k places a family in but – perhaps to 10%-ish? 5% – ish? Thus, 90% of the US is poor? Seems off in my way of thinking.

No questions that a family of 4 in SF/NYC and other locations would “need” $200k to pull off middle class. Midwest? $200k is a healthy take home but your detailed family budget is legit. In mid America, $200k is big money that allows for an accelerated savings program and upper middle class lifestyle. Agree that this is not the case in larger coastal locations.

Thanks for your note. Yales and other schools with larger endowments are going to be able to offer this kind of assistance but many other colleges will struggle to buy admissions this way.

Thank you for your always wonderful perspective.

Assigning the word “poor” to Yale’s definition of household income qualifying for full tuition just reinforces how you are out of touch with mainstream America.

With US median household income now around $80k I think you have insulted over 50% of your potential readers.

While working I managed to reach the 2% income band and was blessed to know many folks living happily making less than $100k. So I’m not just some “poor” offended Midwesterner.

If your intended audience is the top 5% of earners then I apologize for the rant. But if you wish to grow your viewership I suggest you step away from your California bias and take a look at the ~80% of Americans working hard to save while making near median incomes.

That’s just my thought, I could be wrong

Just curious, but did you read the post in its entirety? Yale University has decided that families earning up to $200,000 a year are not wealthy enough to afford tuition. They’ve decided earning up to $200,000 is considered low income, or too poor to afford their tuition.

If you apply for financial aid through FAFSA and private applications, there are often income thresholds and contribution formulas that are taken into consideration for how much one can afford to pay for college.

One of the super powers in life is to interpret the data for what it is and not be easily offended. Personally, I’m going to embrace my status as low income or poor. I think it’s great with higher income thresholds for who gets help for college.

Please read or re-read the post. And please share how you and your wife plan to save for your children’s college now with this new information or how you saved for college for them if they are older. Cheers

Sorry if you are having money troubles and feel insecure after FIREing in 2020. To be insulted by what a university and other universities is team as low income to receive for tuition indicate something wrong with your own mental health and finances.

Just know that if you focus on improving yourself bit by bit or finding better companions, things will get better. Hang in there.

oh wow this is fascinating news. And yes, a good signal for more colleges and universities to hopefully follow suit quickly. I agree with you that it also opens up so many unanswered questions. So hopefully we will learn more as this rolls out.

I found the wording that “the average grant for students receiving aid this academic year exceeds the annual cost of tuition” to be insightful as well.

Looks like their posted costs for this academic year are

2025–2026 Tuition and Fees Cost:

Tuition $69,900

Housing $11,550

Food $9,100

TOTAL $90,550

Man that’s so expensive. Glad they’re making it more affordable for the lucky few who get accepted. I certainly didn’t come close to getting in when I was applying to school. But I agree what’s most important here is that their competitors will likely implement something similar which should then trickle down the chain for non-Ivy’s to follow suit as well.

Yes, super expensive to go to Yale, and great they are using their well to help more families.

The main benefit for the rest of us is that hopefully other colleges grow more competitive and offering free financial aid. Which they must in order to stay competitive.

Kudos to you for preparing years in advance for your kids’ futures. It is interesting to think about how the government perceives the importance of assets versus annual income and come up with the Expected Family Contribution for those completing the FAFSA for aid. Have you looked into and/or made any changes in your asset allocation to account for their formulas (https://fsapartners.ed.gov/sites/default/files/2022-08/2324EFCFormulaGuide.pdf)? Thank you for sharing your thoughts on this realm!

So in a way, Yale’s $40 billion endowment is its net worth and it makes enough passive income to subsidize the cost of college for prospective students.

If Yale University and other private universities want to pay for college tuition AND food AND housing when I’m making $200,000 living in Des Moines, I’ll take it!

Realistically, nobody is getting into Yale and this makes competition even more fierce. But I agree that other universities will have to be more generous with financial aid to attract students.

As a result, I’m going to re-run my retirement assumptions and hopefully retire 2-4 years sooner thanks to free college!

Yes indeed. After 18 years of feeding and housing our children, expertly decumulating our wealth, it would be nice if a great university rolled out the red carpet and paid for everything. And it doesn’t even have to be a top 25 university either, let alone top 5. A top 50 university or top 100 all expenses paid for 4-5 years would be great too.

The future is getting a little brighter if this is the trend. But it also makes me hope new legislation is in place to roll over more leftover 529 plan money. Maybe I should have YOLOed and replaced my 10.5-year-old car after all!

Alas, it’s best to expect nothing and hope for the best.

We contributed early in my son’s life to a 529. My income was healthy, and I always assumed my income would go down, so I wanted to save for his education while I could. (My income actually went up, not down, for about ten years after that.) We also were hoping for more children, and I thought I would split it for multiple kids later. After several miscarriages and an infant death, only that one son (and he’s awesome) survived, so we only needed one college fund. With investment return, his 529 grew to over $450K. He then decided on an out-of-state large public university — but then we moved there are now he pays in-state. So my best-laid plans have his 529 still almost $400,000 as he finishes his junior year. It’s good for graduate school, and I guess I can create an IRA for him with about $35,000 of it. Saving it for his children some day seems like a really remote plan (what if he never has kids?). I, too, wish there were a penalty-free way to re-deploy more of the money. Maybe let it go into a Roth or something?

I am so happy your son is doing great. Man, creating life and sustaining life can be hard.

Just tell your son your wishes about keeping the 529 plan for his future kids, and I’m sure he’ll honor it and figure out what to do with it in the future.

Thank you for sharing your story and bless you and your family.