There’s an endless debate over whether real estate or stocks are the better asset class. Although I'm a fan of both, I just realized the feel-good wealth effect adds another feather to real estate’s cap.

In my post about avoiding the real estate frenzy zone if you want to get the best deal, I highlighted a home that sold 60% over asking, jumping from $2.5 million to $4.05 million. It was an astounding close that genuinely surprised me. I walk and drive by that house all the time and think nothing of it.

After checking in with my real estate agent for some color, she explained that early-year inventory is extremely tight, so demand is massively outstripping supply. The home was remodeled and well-located, so it deserved a strong outcome. Still, it’s not a house I ever imagined breaking the $3 million barrier this year, let alone crossing $4 million.

When I walked by the home again on my way back to the auto mechanic to pick up my car, something funny happened. I no longer felt bad about paying more to fix a coolant leak. I’d already spent about $1,000 replacing the water pump a couple of years ago. Normally, that would’ve irritated me.

After paying the auto mechanic $415 for the oil service and coolant leak fix (replaced a hose for $225), I treated myself to a $10 milkshake, something I never do when getting a burger. Objectively terrible for my weight-maintenance plan. Subjectively? I felt richer so I figured why not YOLO.

That massive house overbid created a real, immediate feel-good wealth effect. $10 for a milkshake after spending another $225 on my car suddenly felt like chump change.

Why the Wealth Effect From Real Estate Feels Stronger Than From Stocks

Since the beginning of 2023, we’ve had a phenomenal stock market run. The S&P 500 is up roughly 80% over the past three years, creating a meaningful positive wealth effect that has translated into higher consumption. I’ve even argued that housing affordability is better than it looks thanks to equity market gains.

Excess stock returns above historical norms have effectively bought us more time, our most valuable asset.

And yet, I’ve come to believe that the positive wealth effect from a huge real estate sale is stronger, deeper, and more durable than even a tremendous stock market rally.

Here are the reasons why.

1) Real Estate Gains Feel More Permanent Than Stock Market Gains

Real estate moves like an armored super-tanker. Even in rough waters, it doesn’t sink. It just keeps chugging along toward its destination. Stocks, by contrast, behave like jet skis: thrilling, fast, and exciting, but one unexpected swell can throw you off and let a great white shark take a bite.

Stocks have no intrinsic utility. They are “funny money.” A stock’s value can get cut in half overnight after a single earnings call. Or some random exogenous shock that causes demand to fall off a cliff could cause years of turmoil.

Real estate provides essential utility. We all need a place to live. In fact, when the world feels like it’s falling apart, housing demand can actually increase. In the extreme scenario of a zombie apocalypse, you’ll crave a defensible home base. Your stocks aren't going to do jack shizzle to prevent you from getting bitten.

Rental income also doesn’t reduce the value of the underlying property. Dividends, on the other hand, are paid directly out of a company’s balance sheet. As a result, the value of the company actually goes down my the decline in cash paid out. Therefore, rental income is superior to dividend income.

The Buoyancy Of Real Estate

We’ve seen how fleeting stock gains can be. In 2021, easy money and massive stimulus sent equities to nosebleed levels. Meta went from about $270 to $376, then collapsed 73% to $99 in 2022, wiping out years of gains in a short period of time. Thankfully it came back.

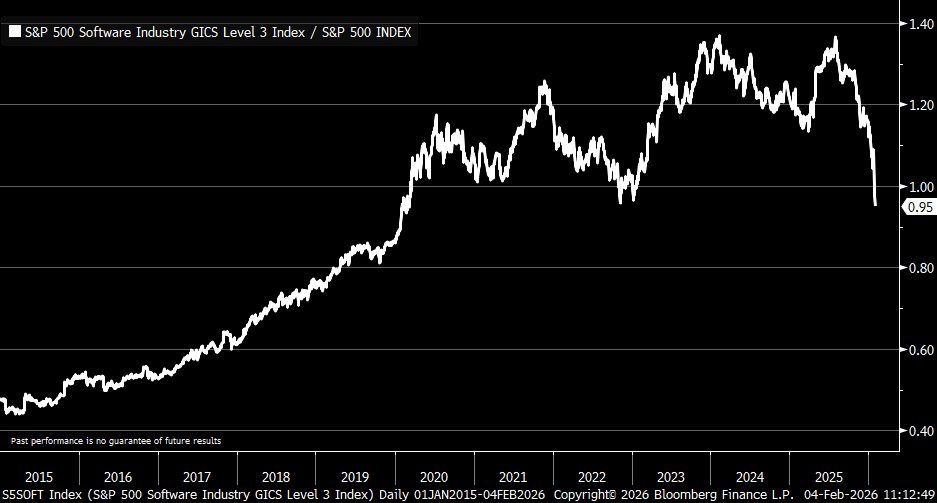

But now software companies in just six months have lost over 6 years of gains relative to the S&P 500, due to fears AI will make SAAS companies and the like obsolete.

Bellwether Microsoft, a company I own, has lost almost 20% of its value in just one month. Meanwhile, Amazon, another stock I own guided for $200 billion in CAPEX in 2026 due to extraordinary demand and the stock was down as much as 11% in after hours.

These sector by sector cuts due to AI is exactly why I've been aggressively investing in private AI companies through Fundrise Venture. I want to own all the main disruptors, such as Anthropic and OpenAI. My problem is not having a large enough position (~$770,000) compared to my public equity holdings.

Housing also surged in 2020 and cooled in 2022 when rates spiked. But unlike the 20% S&P correction or the 25% – 70% drawdowns in tech stocks in 2022, national home prices largely stalled. Even in harder-hit regions like Texas and Florida, declines were around 15% after 50%+ gains. You rarely see housing corrections that erase years of appreciation so rapidly the way stocks sometimes do.

In economics, permanence matters. If a gain feels temporary, you save it. If it feels durable, you spend it.

A classic example is not spending more if you think there will be tax hikes after a year of tax cuts.

2) Real Estate Wealth Is More “Visible,” Which Makes It More Spendable

Stock gains live on a screen. They’re abstract numbers that flicker up and down every trading day. You know they can disappear just as quickly as they appeared, so you subconsciously treat them with caution.

Real estate wealth is physical and visible. You walk by it. You sleep in it. Disrespectful neighbors let their dog's poop on its front lawn, unless you have a rare enclosed front yard. Comparable sales confirm it. A $4.05 million closing across the street feels real in a way a brokerage balance never does.

This visibility makes the wealth easier to mentally access, even if you don’t plan to sell your own home. It creates confidence, and confidence leads to spending.

That’s why a neighbor’s record-breaking sale can make you feel richer. The comp just reset your internal reference point. You can't help but compare your home to theirs and bump up your net worth in the process.

3) Real Estate Provides Stronger Social Proof And Validation

When a house sells at a new record high, it becomes a public event. Agents talk about it. Neighbors gossip about it. Appraisers recalibrate their assumptions. Lenders, insurers, and future buyers quietly update what they believe the neighborhood is worth. Price discovery happens in the open, reinforced by multiple independent third parties at once.

This kind of validation feels amazing. Real estate appreciation isn’t just reflected on a private statement; it’s embedded into comparable sales, listing prices, and neighborhood narratives. One sale can re-anchor an entire block’s perception of value. The gain feels real because it reshapes what others are willing to pay in the same physical space you occupy every day.

Stock gains, by contrast, are lonely and abstract. Nobody throws a block party because the S&P 500 hits a new high. There’s no shared acknowledgment, no communal recalibration of worth. If you mention a big equity win, people tend to assume you either got lucky or took reckless risk. And since nobody likes a braggart, most stock gains stay quietly hidden behind a login screen.

With real estate, your wealth becomes socially validated without self-promotion. After all, the point of investing in stocks is ultimately to turn paper gains into something tangible and meaningful. For most people, that means buying a home, aside from funding retirement. In a world where most financial wins are invisible, this quiet recognition dramatically amplifies the feel-good wealth effect.

4) Real Estate Gains Take More Effort, Stock Gains Far Less So

Because real estate isn’t a 100% passive investment – normally a negative variable in my passive income rankings – its gains ironically feel more earned. If a remodel was involved, even more so given its one of the most painful processes a person can go through. Real estate rewards patience, discipline, ongoing maintenance, and long holding periods. There’s real work behind the outcome, both physical and psychological.

Climbing the property ladder takes decades. Along the way, you usually save aggressively for a large down payment, then summon the courage to take on a massive amount of debt to buy an extremely expensive, illiquid asset. Portions of your house will break and need to be fixed. That’s commitment, plain and simple.

Stock investing, by comparison, is intentionally frictionless. You click, allocate, rebalance, and wait. That efficiency is financially optimal, but psychologically it dulls the payoff. Returns feel closer to luck or market tides than personal sacrifice, resulting in a thinner, less durable feel-good effect, even when the numbers look great on paper.

Get Neutral Real Estate As Early As You Reasonably Can

If the feel-good wealth effect from real estate is stronger than stock market gains, the logical takeaway isn’t to speculate harder. It’s to get neutral real estate as early as possible.

Getting neutral means owning your primary residence so housing inflation no longer works against you. Instead of rising prices making life more stressful, they begin working quietly in your favor through:

- Inflation protection on your largest recurring expense

- Forced savings through principal paydown

- Long-term appreciation supported by rising replacement costs

You don’t need a portfolio of rental properties to benefit. Owning just one home already changes the equation. By locking in your housing costs, you hedge the single largest expense in your budget. For many households, that alone justifies ownership—even before appreciation or rental income enter the picture.

The psychological payoff is immediate, especially as a parent. When shelter is secured, everything else feels more manageable.

Stocks are essential for liquidity and long-term growth. But relying solely on stocks while remaining fully exposed to housing inflation as a renter is an underappreciated risk.

Real Estate Quietly Wins

The biggest misconception is that stocks alone deliver financial security. They don’t, at least not to the degree people expect. Stocks can grow your net worth on paper, but their volatility makes that wealth feel fragile and reversible.

Real estate works differently. Owning your home converts your largest recurring expense into an asset and turns housing inflation from a threat into a tailwind. Over time, it replaces financial anxiety with a sense of control that portfolios alone struggle to provide.

With real estate, it’s not just about returns, it’s about permanence. No matter what the market does tomorrow, your family still has a roof over its head. That stability creates a confidence that quarterly statements rarely match.

Both stocks and real estate generate wealth effects. But real estate wealth feels more durable, more visible, and more real. As a result, people are far more willing to loosen the purse strings when their housing situation feels secure.

That’s how a record-breaking home sale down the block suddenly makes a pricey car repair feel acceptable, an indulgent lunch feel earned, or even a completely unnecessary $10 milkshake seem like a reasonable life choice – perhaps followed by a $250-a-month gym membership to burn it off.

Readers, which creates a stronger feel-good wealth effect: a big real estate sale or stock market gains? If you disagree with my thesis, I'd love to know why.

Participate In The Feel-Good Wealth Effect Of Real Estate

Rising real estate prices don’t just make people richer on paper. They make people feel more confident, more secure, and more willing to spend.

If you want exposure to that positive wealth effect without buying another property, one option is Fundrise. Fundrise lets you invest passively in diversified residential and industrial real estate across the country, so you can participate in real estate’s long-term, confidence-building upside without the hassles of direct ownership.

I’ve invested over $500,000 with Fundrise, and they’re a long-time sponsor and trusted partner of Financial Samurai. With a $10 minimum investment, it’s a simple way to tap into real estate’s feel-good wealth effect and balance stability with growth.

In addition, pick up a copy of Millionaire Milestones, my instant USA Today bestseller. The book helps you build more wealth so you can break free sooner.

For more nuanced personal finance content, join 60,000+ others and sign up for the free Financial Samurai newsletter. This way, you never miss a thing.

I own real estate and ETFs and would hands down liquidate my real estate in favor of ETFs. RE is minimal to no returns with on going headaches and risks. One bad tenant can mean loss of an etire year of returns. One big repair can wipe your profits out. Not to mention dealing with on going issuss even when you are on vacation. ETFs allow flexibility of immediate purchase/ sale of exact amount you desire. What if I want to trim like 5% of my porfolio due to my preferences/ needs, no can do with RE. Not to mention the headache of showings and RE fees and taxes. Its nto even close. Invest in doversified portfolio and live your life. I invested in RE due partially to advice from this site and regret all my purchases. Same amount in the market would mean no tenant hassles, better returns, and ability to sell whatever portion of my porfolio I want, immediately.

Perhaps we feel what we don’t have, whether it be stocks or real estate investments, would make us feel more financially secure. My investment journey started off all real estate. I now have several million worth of equity spread across multiple properties. For the past several years I have been trying to find more balance and have been investing in index funds. If I was given the choice today, I’d gladly swap my real estate equity for liquidity to invest in stocks/bonds.

I’m willing to consider, however, that the extended bull market we’ve experienced since 2009 is creating a cognitive bias. We’ll see how I feel about my asset allocation if we enter into an extended bear market.

Well said. We are all biased towards the Investments that I’ve treated us the best. And then the bull market in stocks has truly been amazing for us.

I’m just narrowing in on that feel good feeling when a property in your neighborhood sells for way over asking and you weren’t even thinking about it on the other hand, we pay attention to stocks at least every week and can see huge rises that make us feel good. Then one bad man, wipe out years of games which feels horrendous and reminds us of the tenuous nature of stocks.

Good article Sam. I think though it is important to parse out “real estate investing”. I think most of us think about primary home and a few “investment” rentals to gain passive income, principal appreciation is OK but secondary.

I have worked in NVA – very hot housing market – for 30 years and done engineering that supports builders – home and commercial. Incredible amounts of money to be made – and lost. I know someone who bought 30 acres in 2020 for 5 Mill and just sold it to a data center builder for 65 Mill. However, alot of things had to come together such as having it rezoned. When he bought it it was residential and no guarantee county would rezone it. If he put that money in S&P it would be about 15M now. So in this case it was hitting the lottery and worked out well. Many people invest in real estate and lose everything because zoning doesn’t work out, or utilities won’t support development, or whatnot.This is more what risks you face when investing in “real estate” through crowdfunding platforms. Your money can being going into projects that will lose everything.

My Dad tried a real estate venture when I was young and lost a considerable amount of Money. Still can remember he and my Mom arguing over it when I was in bed. In this case it was like a stock that went to 0. It is possible to buy a piece of land and it never appreciates, or you lose a ton of money because of just mistimed loans.

Just saying real estate investing can be very speculative. Much more speculative than buying some individual stocks like XOM and AAPL.

Great distinction in Potts. Thanks for sharing. This article is primarily focused on owning your primary residence. However, the feeling of a comparable property near your rental selling for big bucks also has the same powerful feel-good Wealth effect.

“Nobody throws a block party because the S&P 500 hits a new high. There’s no shared acknowledgment, no communal recalibration of worth. If you mention a big equity win, people tend to assume you either got lucky or took reckless risk. ”

My suspicion of why this is true is due to far more people owning houses than stocks. Almost everyone who gets money buys a house, sometimes merely because it is part of the Life Script(TM) our society gives us. Stocks are owned by a smaller percentage of people than houses. Because of this, people have far less direct experience with stocks than houses.

What about retirement funds? From many interviews I’ve done over the years, most people think of their retirement accounts as black boxes if they give them much thought at all. Also, far too many people treat their retirement accounts as emergency funds alienating them from compounding simply because they kill their account before they reach takeoff. All of this tends to make stocks seem alien (and worse, random) to people compared to houses. So people who do well with stocks can only be “lucky.”

Interesting. My wife loves real estate, but if it was up to me i wouldnt even own a primary home. To me, its just a big headache. So, atleast this helps me understand her point of view a bit more…though I’ll still try to avoid owning real estate as much as possible. As for the “wealth effect” of a primary home appreciating, I’m not sure I really get that either though tbf I”ve never lived in a place that appreciated by $1M+. In order to access that increased equity, you’d have to be willing to move to a lower cost area or take out a HELOC…. OTOH, stocks are liquid and any gains could readily be coverted into cash to fund whatever purchase you fancy from milkshakes to mansions… As for the social proof, I like “stealth wealth” and wouldn’t want people to know i lilve in a $4M home if that were the case.

Glad I’ve helped you understand your wife more!

The Median single family home price in SF is almost $2 million, so $4 million isn’t outrageous. But it still is a lot for this home.

I think you are spot on here. I grew up seeing my parents benefit directly from well-timed real estate deals. I’m sure most of it was a bit of luck sprinkled with being in the right market at the time (California). Anyways, I have far more wealth, but all of it is on paper, and not in physical form, which makes it seem less real. Strange, but true!

True indeed. Can be up one day and down a lot tomorrow with stocks and other funny money assets.

“Real estate wealth is physical and visible. You walk by it. You sleep in it. Disrespectful neighbors let their dog’s poop on its front lawn.”

This made me rofl. Don’t forget that dogs pee all over the front lawn too. Brown spots for days and expensive boxwoods that won’t grow because they are pee’d on all day and night.

Got to love it! I always wonder why dog owners don’t pick up after their dogs or just have their dogs poop on their lawns?

Bow hunting is quiet and off to the swamp for fertilizer a country boy will survive !

Alternative call the dog warden to write up the clueless.

Warden went to neighbor found 3 dogs & 2 cats no vax result $500 fine, LOL

Dog Warden NEVER talk with your neighbor about their dog CALL ME !

Net result no dog and no ken & no karen will ever tell again.

My solitude is priceless.

Yeah, the whiplash in stocks is definitely no fun, especially this week. Years of gains have been lost and just shut a short period of time. Stocks love to do that, to test your resolve and see if you can hold on and buy the dip for a better future. With real estate, you don’t even think about the value of your house changing until there is some sale close by that makes you stand up and go wow. And often times, it does make you go wow because inflation just sneaks up on you over the years without you even paying attention.

Over the long term, stock market investing has generally produced higher returns than real estate, especially on an unlevered basis. While real estate can provide rental income and tax advantages, its price appreciation tends to be modest compared to the growth of equities. Stock market investing benefits from higher historical returns, powerful compounding, broad diversification, superior liquidity, and very low effort through index funds. Unlike real estate, it requires no active management, maintenance, or tenant risk, making it a more efficient and scalable way to grow wealth over decades.So yes, real estate may “feel good” but stocks have better results in long run….

Sounds good. So from your point of view, the feel good wealth effect from stocks is higher? Have you been able to make more from stocks then real estate?

Yes, it’s not just the feel-good factor, the actual returns and ease have been significantly higher for me with stocks. While my father ran a real estate business, I’ve personally focused only on stock market investing, and over the last 12 years my experience has been very positive. The combination of stronger long-term returns, liquidity, diversification, and minimal hands-on effort has worked really well for me.

I’ve made a ton more from stocks than I have from real estate (I live in the midwest) but real estate losses (gains) bother (excite) me a lot more than they should. Lately, house values have dropped a little bit and I have to remind myself that the amount of the drop is less than the monthly fluctuation in my stock allocation. Similarly, when house prices went up 20% here, it felt AMAZING even though we had gained a ton more in stocks in half the same time period.

So I guess I’m agreeing with you both. For me, stocks are the clear winner but losses and gains in real estate have a much bigger psychological effect on me.

That makes sense and thanks for sharing. It is an interesting and different scenario. You’re in with me regarding the housing market since it is so expensive to live here in San Francisco. At the same time, it doesn’t matter where you live, you can invest in whatever stock you want, and we have obviously both benefited from stock investments.

I failed to mention in the post that losing a lot of money very quickly later than global financial crisis was traumatizing. And I also bought a single-family house in 2005, and went through the financial crisis, but it was less traumatizing because I just continued to own and limited. I didn’t need to sell it really and I didn’t have daily reminders how much the house was going down in value. And then ultimately, in 2017, when my son was born, I decided to simplify and sell it. I walked away with almost $1.8 million in profits and Principal pay down. So that is a bigger investment amount and return I’ve ever had compared to stocks and all I did was just live my life in it and then rent it out for several years.

Perhaps we feel what we don’t have, whether it be stocks or real estate investments, would make us feel more financially secure. My investment journey started off all real estate. I now have several million worth of equity spread across multiple properties. For the past several years I have been trying to find more balance and have been investing in index funds. If I was given the choice today, I’d gladly swap my real estate equity for liquidity to invest in stocks/bonds.

I’m willing to consider, however, that the extended bull market we’ve experienced since 2009 is creating a cognitive bias. We’ll see how I feel about my asset allocation if we enter into an extended bear market.

for me yes. houses are a pain in the behind. I can see the appreciation any minute on my phone of my equities. and the only reason I managed to put 20% down payment to buy my house was selling shares of equities.

Good points. I do feel richer for longer when a comp in my neighborhood sells at a big price. The latest carnage in software stocks is a great reminder to not only diversify in your stock portfolio, but diversify in your asset allocation as well!

Crazy how software stocks have gotten wiped with 6 years of gains lost, and also with Bitcoin down 40% in a couple of months and Silver Gold imploding. Easy come easy go!