To outperform the masses, we must take more risk than average. One way to do so is to invest in venture capital. However, venture capital is a form of patient capital, and patient capital requires time. That is the one resource older investors have less and less of.

At 50 in mid-2027, I'm entering the old man phase of my life. It's sad, but the average 50 year old American male is roughly 65% of the way through his life expectancy. The time horizon math starts working against you in ways that are easy to ignore until you sit down and actually do it.

As someone who allocates up to 20% of investable assets into alternative investments including venture capital, venture debt, and commercial real estate, I'm finding it increasingly hard to justify committing to a new venture capital vintage.

Since 2018, I've invested with a traditional VC firm that recently raised a new AI dedicated fund in 2026. I have the option of investing between $100,000 – $1 million in their friends and family round. The question is whether I should at my age, and if so, how much.

Maybe you're older and facing this same dilemma right now. You see SpaceX finally IPO and don't want to miss the next rocketship. Because what's the point of building more wealth if you can't enjoy it for the next 10 or so years?

The Difficulty Of Investing In Venture Capital When You're Older

If I invest in a traditional venture capital fund in 2026, the timeline looks like this:

- Meet capital calls over the next three to five years: 2026 through 2030

- File K-1s for my taxes for the next 8-11 years

- Potentially receive all capital back plus profits somewhere between year 8 and year 11

If the 2026 vintage successfully returns capital and profits in 11 years, I'll be 60. So the central question becomes: will I actually be around, and healthy enough, to enjoy it?

I'd like to think so. But I'd assign roughly a 10% probability I won't be alive at 60, and an additional 20% probability that I'll be alive but dealing with a health issue that makes money less useful than time. NASCAR legend, Kyle Busch, unfortunately died at just 41, so you never know when your last day will be. Please make the most of each minute.

All my discipline of meeting capital calls for five years and delaying gratification for 11 years may ultimately benefit my children, who will be 20 and 17, and my wife, who will be 57. That's a good thing given I'm the main financial provider. However, it also means I won't be able to spend it on them in the present.

Note: If you're looking to get an affordable term life insurance policy, check out Policygenius. Both my wife and I got matching 20-year term life insurance policy and felt a tremendous amount of relief afterward. Protect our children and their futures. Policygenius provides you no-obligation, competitive, and customized quotes all in one place so you don't have to shop around.

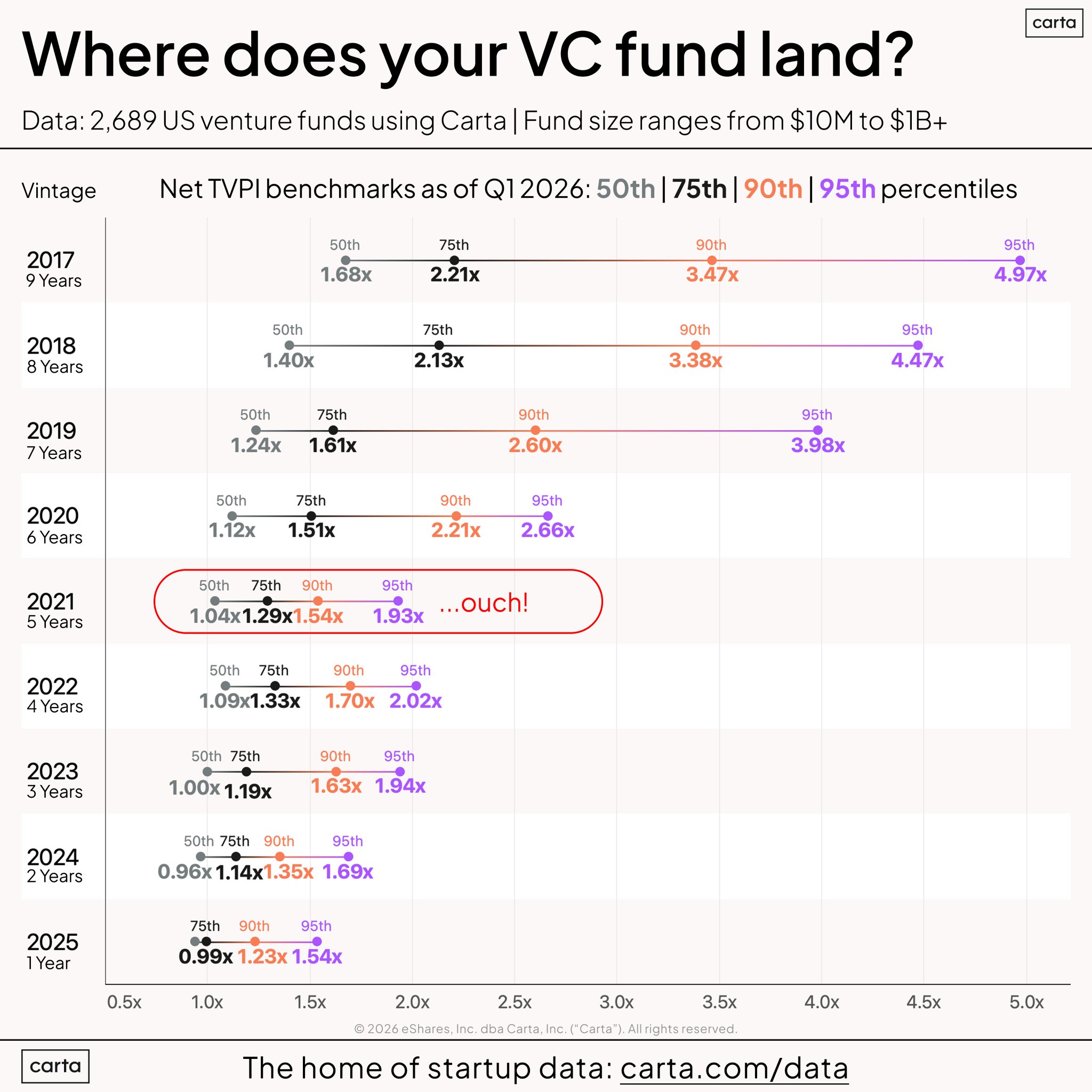

What VC Returns Actually Look Like, And What They Don't

Before deciding whether to invest in VC at any age, it helps to be clear-eyed about what the asset class actually delivers.

The top-quartile VC funds, the ones you read about and the ones everyone wants access to, have historically generated net IRRs of 20 to 30%+ over a full fund cycle. The median VC fund? Roughly 8 to 12% net IRR, which is similar to the S&P 500's historical average of around 10%, and that's before accounting for illiquidity.

In my own experience since I started investing in venture in the early 2010s, my returns have ranged from 8% to 40% IRR across funds. But in aggregate, they haven't dramatically outperformed the S&P 500. Few asset classes have given what a heater the S&P 500 has been on since 2012.

The fact is most people who think they're getting access to top-tier VC are getting access to median-tier or lower-tier VC. And median-tier VC, after 10 years of illiquidity and K-1 headaches, is a questionable trade. Meanwhile, the NASDAQ is up 6.5X net in the past 10 years with 100% liquidity.

Related: Venture Capital Investment Terms, Like TVPI, You Should Know

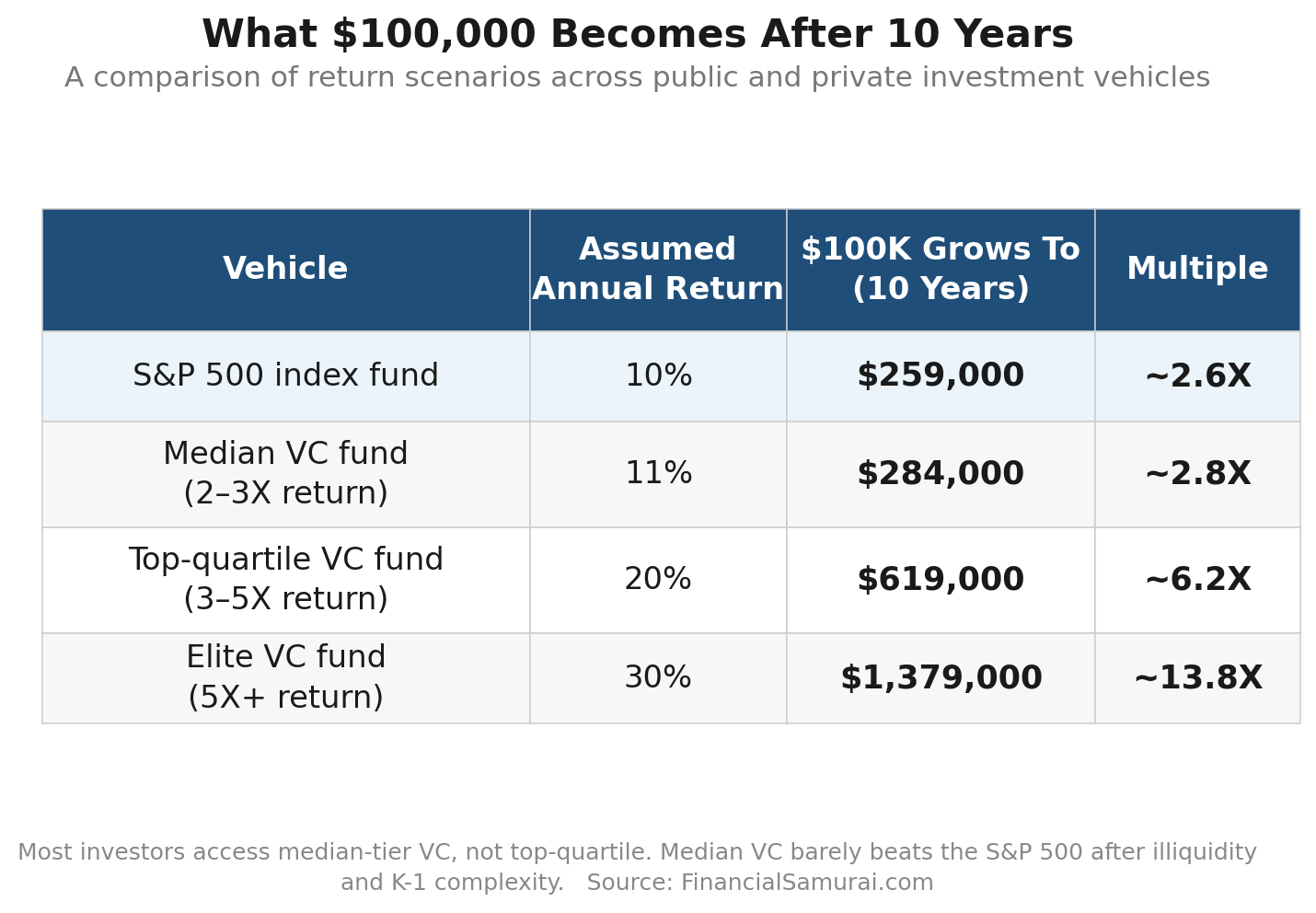

Future Returns Of Venture Capital Performance And The S&P 500 Over 10 Years

Here's a rough comparison of how $100,000 compounds across different return scenarios over 10 years at various annual return percentages:

The S&P 500 number is available to anyone, liquid at any moment, with no K-1s, no capital calls, and no lockup. The top-decile VC number is extraordinary but requires access most people simply don't have. It's invite only, and you and I are almost always never invited.

The realistic VC scenario for most investors sits in that middle band, where the illiquidity premium is thin.

This is why access matters so much in venture. If you can get into the top 10% of funds that have access to the top 1% private companies, the illiquidity is likely worth it at almost any age. These firms include Sequoia, Benchmark, Founders Fund, Thrive Capital, Accel, a16, Bessemer Venture, Greylock Partners, Kleiner Perkins, Greenbacks, Index Ventures, and several more.

If you're in the middle of the pack, the case weakens considerably, especially as you get older. Hence, you may want to scale down your allocation.

The Value Of Liquidity Goes Up As You Age

Liquidity is not a fixed value. It is worth more as you age, not less. Here's why.

When you're 30, an emergency like a job loss, a health scare, or a market crash is painful but survivable. You have decades of future earnings ahead. The illiquidity of a VC fund is a manageable constraint. It could actually be a positive feature as it forces you to invest over the long haul through down cycles.

When you're 60 and facing an aggressive cancer diagnosis, illiquidity isn't a feature. It's a cage. The money you'd most want to use, to take your family on a once-in-a-lifetime trip around the world while you still have the strength, is locked inside a fund you can't access.

Or consider a less dramatic scenario: your child needs emergency surgery abroad. Your elderly parent needs expensive full-time care. You want to help a spouse pivot careers, which may mean no dual-income for a year or two. These are real situations where tappable equity matters enormously. With traditional venture capital, that equity simply isn't there.

Therefore, for traditional venture capital, you must only invest money you don't need for 10+ years.

The alternative, investing in publicly traded vehicles with private company exposure, closed-end funds, or individual stocks, preserves optionality. Yes, there's more day-to-day volatility in public venture capital funds like VCX. And you must be careful with your entry points. But the equity is yours to deploy when life actually happens.

After all, the purpose of investing is to actually spend it on something that improves the quality of your life. If not, investing just for investing's sake is useless.

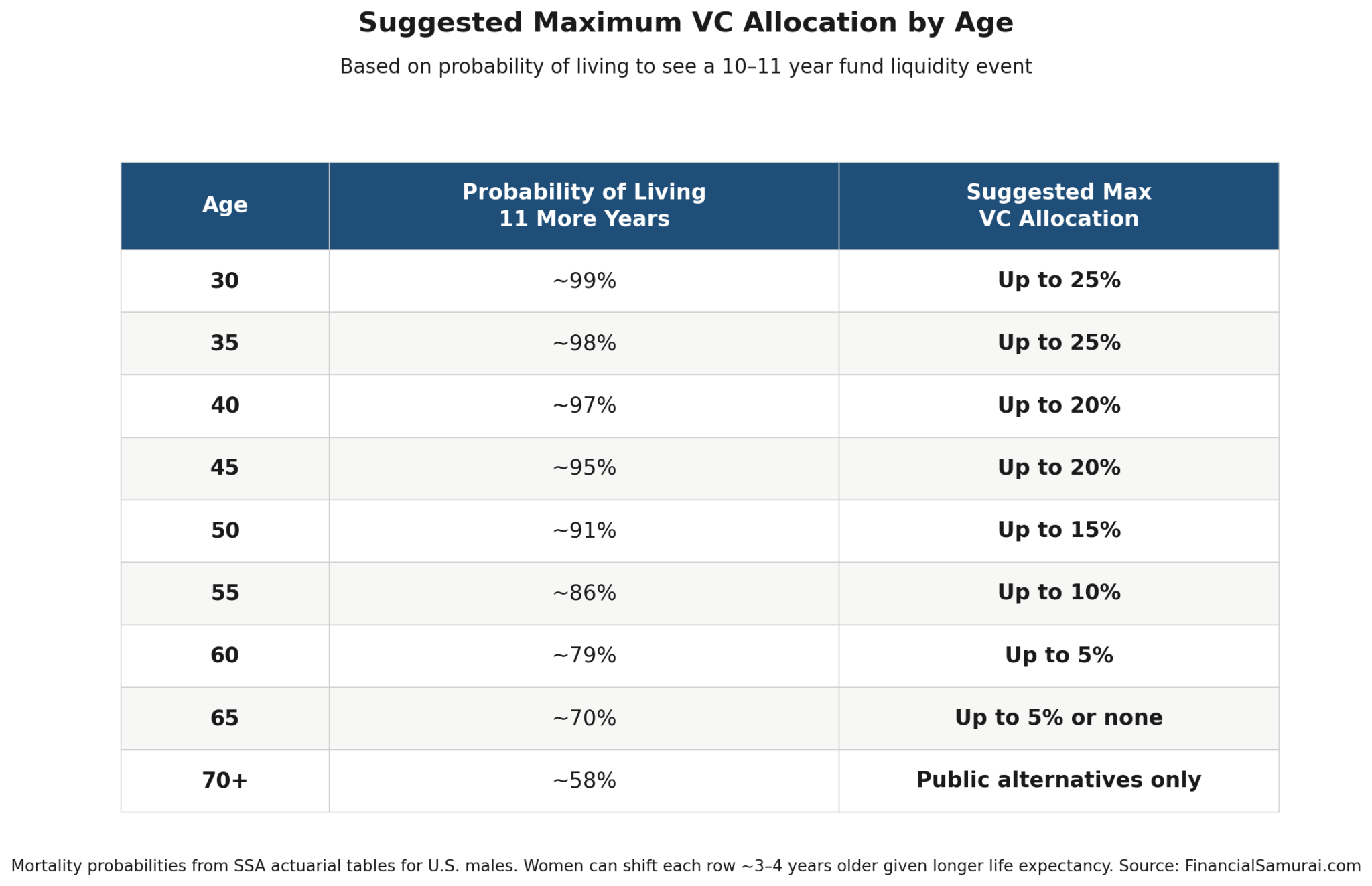

A Guide: How Much VC Should You Hold At Each Age?

Let me offer a practical framework for thinking about your private fund allocation as you age, grounded in two variables: your remaining life expectancy and the probability you’ll live to see liquidity from a given vintage. We're going to assume you can get into a mid-tier venture capital fund or higher.

Given companies are staying private longer, with more gains accruing to private investors and employees, it makes sense to allocate more capital to private investments.

Further, if your goal is to outperform the S&P 500 and achieve financial freedom sooner, you must be willing to take more risk for potentially greater returns. There are two levels of rich, and the richest didn't get there by investing in index funds.

The Core Principle: Your VC Allocation Should Shrink As Your Time Horizon Does

A standard VC fund has an 8 to 11 year expected hold. If your planning horizon is 30+ years, a 10-year lockup is a minor inconvenience. If your planning horizon is 12 to 15 years, a 10-year lockup consumes most of it.

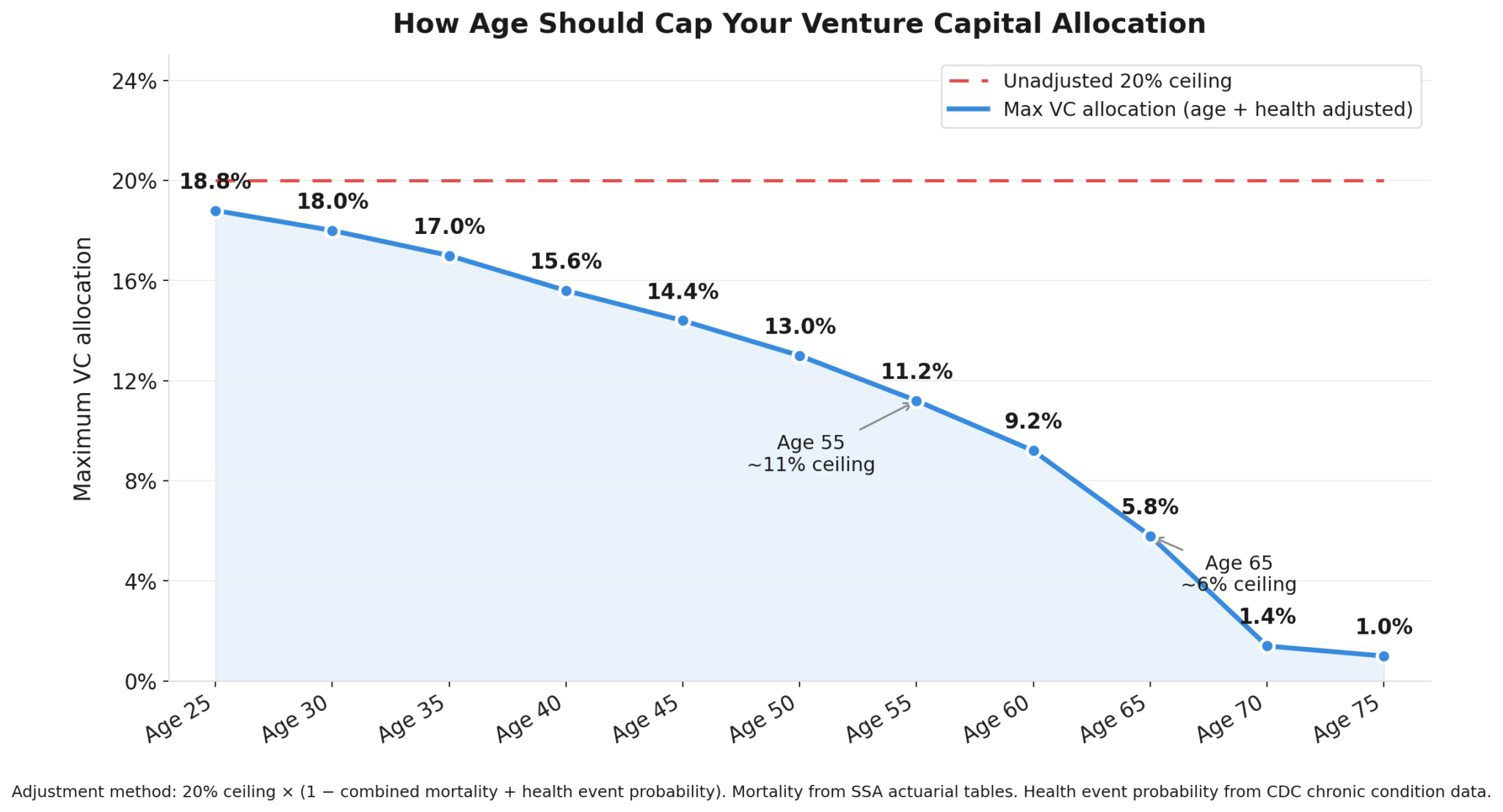

Here's a suggested maximum traditional VC allocation of investable assets by age, assuming a 10-year fund:

*Mortality probabilities based on SSA actuarial tables for U.S. males. Women can shift each row roughly 3 to 4 years older given longer average life expectancy.

Lower Traditional VC Exposure The Older You Get

The logic is simple: your maximum VC allocation should roughly track your probability of living to enjoy the returns. If there's a 9% chance you won't be alive in 11 years, it's hard to justify locking up 20% of your portfolio on that bet, regardless of the projected returns.

The great irony of venture capital is this: access is hardest when you're young, hungry, and have the longest time horizon to benefit from it. By the time you've built the connections, the reputation, and the capital to get into the best funds, you may be too old to want the lockup. That's not a solvable problem. It's just the way it works.

This is why the creation of public venture capital funds like VCX has created a good alternative for younger and older investors alike who want exposure to venture capital without sacrificing liquidity.

The Second Variable: Health-Adjusted Liquidity Needs

Beyond mortality, factor in the probability of a major health event that would make liquidity valuable even if you survive. By age 60, roughly 40% of Americans are managing at least one chronic condition with meaningful out-of-pocket cost. By 70, that figure climbs above 70%.

This is why I do not recommend allocating more than 20% to venture capital in general. For most investors, the real ceiling sits lower once you account for age.

The rule of thumb: start with your 20% maximum, then haircut it by your combined probability of dying or facing a serious health event over a typical 10-year lock-up. The riskier your personal situation, the more you trim the illiquid position.

Example VC Asset Allocation As You Get Older

Here's how it works with a $3 million liquid portfolio and a 20% VC ceiling, which gives you a $600,000 starting point:

- Age 25: Minimal mortality and health risk, so you barely haircut at all and can approach the full $600,000.

- Age 45: A roughly 10% combined risk trims you to about $540,000.

- Age 55: A combined 44% risk (say a 14% chance of not being alive in 11 years plus a 30% chance of a major health event) cuts your adjusted ceiling to about 11%, or $330,000, roughly half the theoretical maximum.

- Age 65: A 26% mortality probability and 45% health-event probability produce a 71% haircut, dropping your ceiling to around 6%, or $180,000.

The upside potential of venture capital does not change with age. Your ability to wait it out does. The younger you are, the closer you can responsibly get to the 20% ceiling, or maybe even beyond it. The older you are, the more a rigid illiquid position becomes a liability rather than an opportunity.

More VC Asset Allocation Examples By Age

Here's how hypothetical portfolios might be structured with appropriate VC exposure at different life stages:

Age 35, $1M Portfolio

- $200,000 traditional VC / private funds (20%)

- $700,000 S&P 500 index funds (70%)

- $100,000 Treasury bonds / cash (15%)

Age 45, $2M Portfolio

- $340,000 traditional VC / private funds (17%)

- $1,260,000 S&P 500 index funds (63%)

- $400,000 Treasury bonds / cash (20%)

Age 50, $3M Portfolio

- $390,000 traditional VC / private funds (13%)

- $1,860,000 S&P 500 index funds (62%)

- $750,000 Treasury bonds / cash (25%)

Age 58, $5M Portfolio

- $400,000 traditional VC / private funds (8%)

- $3,100,000 S&P 500 index funds (62%)

- $1,500,000 Treasury bonds / cash / liquid alternatives (30%)

Notice that as VC allocation shrinks, the freed capital moves toward liquidity, into bonds, cash, and liquid alternatives, not just into more equities. This reflects the rising value of accessible money as your life circumstances become less predictable.

Slowing Down My VC Investments Post 50

In 2027, I'll start slowing down my VC investments to match my mortality.

I'll make these investments through my revocable living trust, as I always have, so my wife and survivors can manage the assets smoothly if I were to die prematurely. Then I'll meet capital calls as they come and hope for the best.

After roughly 20 years of VC investing, I've come to genuinely appreciate the capital call structure. It kept me disciplined through the 2008 financial crisis, the 2018 correction, COVID, and the 2022 downturn, forcing me to deploy capital at moments when I might otherwise have frozen.

Investing for the long run is generally a good thing. Unfortunately, as economists love to say, in the long run we're all dead.

Weighing The Cost Of Illiquidity

As someone who has lived in San Francisco since 2001 and loves the startup ecosystem, there's something uniquely energizing about investing in creators as a creator myself.

There's also less investing FOMO when you're already a venture investor, because you're in the game rather than watching from the sidelines.

That said, the VC outperformance has been real but not transformative. As the years pass, I have to weigh that modest premium against the growing cost of illiquidity. Increasingly, that tradeoff makes less sense.

My hope and expectation is that Fundrise, which is back to focusing primarily on real estate, eventually launches VCX II following the success of VCX I. Ideally one that raises capital privately, deploys it over 2-3 years, and then lists on the NYSE. If that happens, I'll be the first to commit. Fundrise is a long-time sponsor of FS.

Being able to invest in venture capital while maintaining liquidity is a powerful combination. Here's hoping the asset class keeps evolving in that direction. But for now, let's enjoy the SpaceX IPO for those of you got in directly or through a VC fund!

Reader Questions And Author Background

Readers, what do you think about investing in private funds after age 50 with a 10-year or longer lockup? Is there an age at which you'd stop committing to venture capital or other illiquid private funds? And for those of you who've been in VC for a decade or more, has the illiquidity ever cost you in a moment when you genuinely needed the cash?

Background: I've invested in venture capital funds and private companies since 2006. I've loved entrepreneurship since elementary school, and ultimately became an entrepreneur myself with Financial Samurai in 2009, after 10 years in finance. This passion is one of the big reasons I've continued to live in San Francisco since 2001, despite reaching FIRE in 2012. Two of my venture capital funds own SpaceX, and every portfolio company that IPOs is exciting. But not all IPOs are successes.

To continue building your wealth and navigating an uncertain future, subscribe to my free weekly newsletter. Join 60,000+ readers who get my latest insights on investing, real estate, financial freedom, and more, sent straight to their inbox.

Longtime reader, really appreciate your content.

Does your perspective on time horizon and allocation change based on investment vehicle? I am in a couple of VC deals through a Self-Directed Roth IRA. This capital is already locked up until retirement (illiquid even if in S&P 500), and it is tax free given the Roth dynamic. I have about $300k available inside my SDIRA and have considered allocating most of it to VC as attractive deals show up.

I just turned 60 this year with about $1.5M invested in VE/PE type investments, about 25% of our net worth. We are overweight in this type of investment, but about half was unavoidable; it came through the sale of my tech services business in 2022 to a PE firm that required a 25% rollover of funds. We’re waiting for the coveted “2nd Sale”. Another piece of this is Fundrise, and I hold about 11,000 of VCX… lol we’ll see how that lands in a few months. In any event, another insightful article, Sam! I’ll probably read this one again a couple of times over the weekend. Cheers!

First time, long time here. And always enjoy the posts; I’ve learned a lot. Any addendums to this post given the slide in VCX shares lately?

Not really. I’ve maintained my same stance since listing and my podcast episode on the subject. I think VCX’s NAV grows to $40 – $50 by the end of the year, which is its fair value.

The best part of the article is the reminder that money is a means to improve quality of life. If investing prevents you from living with dignity when the need arises, it has lost its purpose.

What are your thoughts on using “annuity like” ETF funds that have 100% nominal downside protection (in their yearly reset version or laddered) as part of the larger liquid assets requirement you suggest in retirement?

I feel 50 is really not that old. I’m 61 and have 12% of net worth in VC and private companies. This feels comfortable to me. My goal is to leave at least about 25% to my children, based on how much I inherited. It is in 2 Australian VC funds, Angellist, and a couple of private Australian companies. The first VC fund investment I made was in 2018 when I inherited the money. It has made some distributions, has one major company left, which will hopefully become liquid in the next year or two. One of the private companies also wants to IPO soon… When I officially retired at the end of last year, I stopped investing in a rolling fund on Angellist but I have committed to a third Australian fund, but less than I committed to the second fund. So, I am trying not to tie up too much money in this, while being exposed to the asset class. I don’t like investing in stock index funds, so this is my major way to be exposed to tech companies. I invest in other PE only through listed funds.

If I live until 61, I’m sure I won’t feel that old either. But over 50 is about 65% of the way through life already. Is there anything you would’ve done differently if you rewind time back to 49 and 50 years old?

It sounds like you inherited a lot of money when you’re 54. Was that 25% of your net worth post inheritance? And if so, did inheriting that money at that age make a difference to your life at all? This is something that I think about more as I don’t wanna die and then leave my middle-aged or later kids any money because it doesn’t seem like it would be that helpful to them by then.

Awesome perspective, as always, Sam. Just curious… did you get in on the SpaceX IPO? Or did you just accept exposure through different funds you own? I was considering buying some IPO shares, but didn’t want the lockup and figured I could get them later at a comparable price to the IPO. Personally, I’m buying whatever Elon is saying. If I could invest in all the naysayers he’s proven wrong, I’d have been retired 10 years ago!

Thanks for all the years of great advice… enjoy your wins!

I did not. I’ve got enough exposure through two different funs. Check out my post on not wanting to be exit liquidity.

But I also want to look for the NEXT SpaceX. Too bad my money is quite finite!

Good perspective as always. However, an alternative approach is not VC allocation by age, but by net worth. This likely gives completely opposite recommendations, since older people tend to be richer. As an example, a 30 year old might need all the liquidity they have (and then some) to put a down payment on a house in San Francisco, in which case investing in a VC fund wouldn’t make sense. In contrast, a 70 year old centimillionaire could easily put half their money into VC funds knowing they could living comfortably on the rest.

Sure, it is a variable that I use in the examples in the post. But my general guideline is 20% of net worth or investable assets.

What percentage of your net worth or investment assets are you investing in venture Capital?