If you want to get rich or simply just grow your wealth, first you have to be willing to save more money. Then, you have to be willing to smartly invest that money to beat inflation and benefit from compounding returns. But, perhaps you're in need of motivation to save more money. Funny or not, a great motivator is to visualize your broke-ass lonely self.

Ever since I was in the 4th grade, I've had this mild obsession with staying in shape. There was this girl I liked in gym class that I so wanted to impress, but I already had a gut as a nine year old!

So, imagine my dread when it was swim season and I had to sit down next to her in only my trunks. I couldn't wait for the teacher to blow her whistle so I could jump into the pool and exhale. Even at such a young age, I was always so envious of the bony kids who didn't have to suck in their guts.

Get In Shape Physically And Financially

I never did get the girl. I blamed genetics and my lack of courage to say, “Wanna get an ice cream sandwich during recess?” All throughout secondary school I decided to get into better shape. I knew I couldn't be poor and out of shape at the same time. That would be a disaster.

Nowadays, I'm focused on staying healthy so I can live as long as possible to support my family and watch my kids grow up. I try to play tennis 3-5 times a week, and get in at least some type of low impact exercise on my off days. A buddy of mine has a great motto, “I make it a goal to sweat every day I eat.”

For those of you single folks, I'm sure you've all seen the online dating profiles of people who look amazing in their photos. But, then when you meet them in person it turns out he/she is actually 30+ pounds heavier. Or maybe that's what you've been doing for your own profile. In any case, being overweight isn't a great way to make a first impression when you're looking for love.

If we can't stay fit, then we must be able to at least generate enough wealth to provide. Being unfit in wallet and in wealth leads to loneliness. This is our curse from society, which I'll discuss more in an upcoming podcast.

“No money, no honey,” as the saying goes.

Save More Money By Being More Mindful

Losing weight and saving money are perhaps the two most difficult things to consistently do. But we try because we believe one or both of these activities will provide us with greater happiness.

If you read my blog regularly, I also hope my articles also help motivate you to save more money. I feel it is my duty to help spread financial knowledge, and am always trying to encourage people to think about money in new ways.

I recently got back from a three day trip to New York City to cover a couple events held by Empower Personal Capital. The main event was the revealing of a study conducted by Yaron Levi, a Finance PhD at UCLA and Shlomo Benartzi, Co-Chair of the Behavioral Decision-Making Group. They found that spending decreased by 15.7% on average for those who download and use the free Empower financial app. Talk about improving the balance between spending vs saving.

To put 15.7% into context, a household making $50,000 a year will end up saving an extra $150,000 in a 20 year time frame. Given the overall 401k average balance at the time of the study is roughly $101,650 and $150,000 for those 55 and over, average 401k balances could theoretically double over the next generation if everybody adopted a financial app to help manage their money.

Utilize Technology To Save More Money

Let me address the skeptics head on by saying it shouldn't come as a surprise that an event hosted by Empower should have a positive finding about Empower’s financial app. Furthermore, I'm a consultant of theirs. But it makes sense that a financial app can help curb spending and increase investing.

As soon as I started typing out my budget in Excel and creating pro forma calculations of my net worth circa 2007, I became much more sensitive about my spending habits. I didn't want to see a negative number in each month's spreadsheet, so I did everything possible to save more money. Before then, I didn't know exactly how much I accumulated by age 30.

By publicly highlighting my passive income activity annually, I feel more pressure to not mess things up because I know many are expecting some progress in my next update. The more you hold yourself accountable, the better your chances to save more money and grow your wealth.

The Empower Personal Capital financial app helps me visualize where I want my net worth to go if I continue to invest X amount of my income and achieve Y returns. It's addicting and fun if you've never tried. And you don't have to use Personal Capital's app either. There's Mint, Quicken and several other free financial tools out there. The internet has eradicated all excuses as to why someone can't better manage their money.

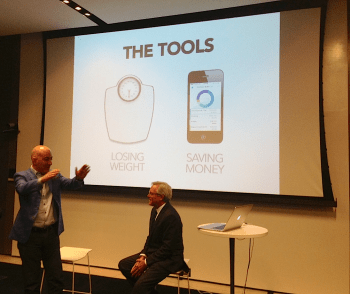

A Portable Financial Scale Holds You Accountable

The analogy Dr. Benartzi used for describing why he believes a financial app helps people spend less is that of a portable scale.

If your ideal weight is 160 lbs, but your portable scale is blinking 185 lbs right before you eat, there's a good chance you won't stuff your face as much. You might skip the cheeseburger and order a salad with a glass of lemon water instead. I know I would. (Related: The Ideal Weight Pisses Me Off)

A portable financial scale helps modify behavior in a similar manner. If your net worth is going down or hasn't changed much for months, then you might be better motivated to save more money. It's good to be aware of the pain!

Every time I log on to check my net worth, I'm more motivated to pay down debt. It feels great updating the figure with a smaller and smaller number. On the flip side, if the financial app is saying my net worth is skyrocketing, then perhaps I'll be a little more adventurous and get some new shoes.

Empower Can Help You Save More Money

Now imagine if a financial app could show a broke old you in the future if you continued with your existing financial habits. That's exactly what Empower’s app does with its Investment Checkup feature. Surely, your behavior will change for the better at the margin.

Finally, if you really want to save more money don't live in New York City. It's the greatest city in America for six months a year, but the city will bleed you dry. Even the most standard hotel rooms costs over $400 a night during the week. Let's not mention the $66 dollar cab or Uber ride into the city, ubiquitous $12 cocktails, the daily $25 lunches, the $2,000/sqft condo prices, or the $50,000 a year private school tuition either.

I'm glad to be back in affordable San Francisco!

Track Your Investments Wisely So You Can Spend With Confidence

The easiest way to know how much to spend on a luxury expense is to know your portfolio inside and out. That means understanding its asset allocation, income generation, and returns. You can do that with Empower and its free investing tools.

Last week, I went to the post office to send out a dozen signed copies of my USA Today bestseller, Millionaire Milestones. If you’re interested in participating in the promotion, you can sign up for a free financial review with Empower. You can read about my experience and the instructions in this post.

Get my posts in your inbox as soon as they are published by signing up here, and subscribing to my free weekly newsletter here. I've been writing about personal finance since 2009, and everything is based off firsthand experience and expertise.

Sure NYC is expensive by nature but there are still ways to achieve financial goals there. Not saying it would be pretty though!

I guess for me, the app would not be helpful because I track my weight by how snuggly my clothes fit. A few years ago, I manually noted my spending and adjusted where I needed to. I have maintained the same lifestyle and this has helped me to save some money. I guess I will be slow to jump on the app bandwagon because I am also not really interested in or good with technology.

Who says you have to spend $66 to get into NY? Take the bus for $2.50.

Or maybe walk to Manhattan from

JFK, since it’s free.

Ha-ha. What a clever snarky comment, that manages both to evade the issue and avoid the validity of my response. You want to be the last of the really big spenders, be my guest. So you’re coming from JFK, take the AirTrain and then the subway, you’ll spend a grand total of $7.50. From LGA, take the M60 bus for $2.50. Anyone who bothers to do their homework will find you can get around and stay/eat in NYC for half your prices and no compromise in quality.

okay okay everyone just calm down.

We need personal capital here in france :-)

Ahh, losing weight and making money. Great analogy on building wealth with a portable financial scale.

I see growing wealth like a game, with the Personal Capital app the game maker. If we can make saving and investing fun, then we’ll do more of it.

Let’s just hope there aren’t as many violent downturns as we’ve recently seen in the markets!!

Thanks for mentioning the app. Will have to check it out and see how it can help us further. :)

I step on the scale and check my net worth every morning for the same reasons! I’m always almost exactly 5% off my target because it just works better to have a target that is slightly unattainable.

I don’t agree with your premise that 8s “settle” for 6s. There was a nicely written article in the Atlantic that described how women on average are better looking than men because we invest more in our appearance. Men on average are wealthier than women because the female-to-male earnings ratio is still about 0.81. In your example of an 8 and a 6, they are probably a good match, assuming of course that he is in fact wealthier than her.

Doesn’t the Atlantic study therefore buttress the likelihood that my friends settled for guys less attractive than them? But from an entire package, maybe they are the same since the guys are financially well to do.

Sam,

That “portable financial scale” has radically changed everything for me. At the beginning of this year, a month after my wife and I purchased our first home at the age of 28, something in me just clicked. I started tracking all my finances and networth in my own built spreadsheets and trackers. Back then it was hovering around six figures. Half from my 401k to date, and half of the equity in our new home. Had no emergency savings, and over 15k in CC debt. Fast forward to now/end of this year and I will have accomplished:

1. No CC debt

2. Net worth will have increased by about 75% from this year alone and will increase more aggressively going forward

3. Change 401k contributions from 6% (to meet full employer match), to maxed out contribution of 17.5k (plus a 7.5% employer match)

4. Traded in car to something more manageable (Audi S4 –> Used Subaru Forester)

5. Added extra mortgage principal payment, which will help us pay off our 30 yr fixed in 20 years

6. Saving $5500 every year and will back door it to a Roth IRA.

7. Poised myself to build my 6 month salary emergency fund over the next 2 years with a savings plan

8. Opened 529 for our little one on the way and will max tax deduction amount of 4k annually at minimum

All of this is due to me tracking everything every month. To your point, I now watch my spending all because i want to be able to see these results month to month on my trackers. What we were spending our money on astounded me! Granted my wife and I are living less spontaneously and well within our means now, but I’ll admit that we were spending ridiculous amounts of money without thinking about it and trying to “live up our 20s” while we could.

Now that it’s out of our system, I feel like we’re on a great track for our future retirement. I will also say, my wife and I have worked really hard to get to where we are in our careers, and our salaries are reflective of that. Allowing us to have a high income, which in turn has made alot of these changes easy to do.

If I can do all this, all of you other FSs should also be able to make radical changes that put you on a great path to a healthy retirement! As always, keep up the great posts, Sam!

-T

This is awesome T! So fantastic of you to be on top of your finances, leverage technology, and make a difference in your financial future!

Your example is the prototype example of how a financial scale can help someone.

It doesn’t surprise me that Personal Capital’s financial app led to lower spending for the people who used it. Tracking spending always helps people be more mindful. This is one of those cases where technology can be used for good- not just for entertainment or something pointless! =)

Yes, I believe that apps help both financially and physically. Anytime I have tracked either calories or expenses, I have always either lost weight or saved money. But the problem is that you really have to want to lose weight or save money and unfortunately I just am not that optimistic about other people wanting to do either.

Knowledge is power. For the vast majority of people, just knowing aggregates of their spending categories can be a wild awakening.

Denial is a big part of the problem too though. I have friends who won’t use Mint or similar because they “just don’t want to know” what their total financial picture is. Hint: They are pretty broke :-)