If there's a car in your blind spot and you swerve suddenly, there's a good chance you'll get into an accident. Your accident will not only cost time and money to fix, you might also suffer an injury or even die. If you have financial blind spots, the consequences can be just as severe.

I can't teach you how to be a better driver except to encourage you to slow down. But I can point out some financial blindspots to allow you to live a better life.

Here are five of the most common reoccurring financial misses that I've observed over and over again. For reference, I helped kickstart the modern-day FIRE movement in 2009, when I started writing about my escape from finance. In 2012, I retired at age 34 and haven't been back.

Common Financial Blind Spots To Financial Independence

1) Comparing someone's middle to your beginning.

Some of the most clueless people about money are in their 20s. Yet ironically, some of the most vociferous people who think they know it all also happen to mostly be in their 20s. Fascinating!

They rage against the people who bought their own house by 28, accumulated a million dollars in after-tax investments by 35, and started making over $100,000 a year after going to graduate school.

Yet, they haven't given their life enough time to compound. It's as if they want to get ahead but refuse to work more than 40 hours a week. If you want to be average, work the average number of hours a week and be happy. But if you want to be above average, you just might have to put in more time.

I've noticed through thousands of comments over the years that this rage starts dying down after someone hits 40. By 50, there is much more harmony and agreement. For example, check out my post Here's How Much You Should Have In Your 401(k) By Age. See for yourself by reading how the angst fades the older the commenter gets.

Repercussions for this financial blind spot:

Resentment, anger, and bitterness towards a large swath of people. With so much resentment, you end up going to your local hardware store and buying a pitchfork to stab anybody who has more than you.

Instead of taking action to improve your financial situation, you use your negative energy to attack others and try to bring them down to your level. It hardly ever works folks!

If you compare yourself too much with others, you may also develop money dysmorphia. This is where you think you're doing much worse than you really are. Over time, this warped sense of reality may negative affect your mental health and happiness. Beware.

2) Thinking parenting is easier and cheaper than it is.

For those suffering from this blind spot, they either don't have kids or are a parent working outside the home.

Being a full-time parent is harder than almost any job I can think of. It is 24/7 and the stakes are so high. One look away could mean a bloody bonk on the head or a drowning, the #1 cause of death for children under four. As a result, when looking after a child, you can never mentally or physically relax 100%. Over time, your nerves will begin to fray without relief.

For 13 years I worked in finance, including three years where I also attended business school part-time. I can state unequivocally that being a full-time parent is harder than working 80 hours a week in one of the most cutthroat industries.

I've met so many working dads who think raising a child is easy. Why? Simply because they don't take care of their kids most of the day! It's either their spouse or daycare that takes care of the child. The working spouse tends to take the stay at home spouse for granted. And then the relationship begins to break down.

I've also encountered childless couples who criticize stay-at-home parents for hiring help. They think it's nuts for a stay-at-home parent to hire relief for several hours a week so the parent can take a shower, exercise, and spend quality time with friends and loved ones.

At least consider having a net worth goal before having kids.

Repercussions for having this blind spot

Resentment, fighting, unhappiness, neglected kids, rebellious kids, divorce, financial ruin, and many more years of work. Think about it.

Despite loving their kids more than anything in the world, parents still get divorced, even though they know that having two supportive parents is better than one. They didn't anticipate or appreciate the strains kids put on a marriage and on their finances. If you can't comfortably take care of yourself, consider postponing having kids until you can.

I've been a full-time father since 2017. It's been the toughest job in the world hands down. I seriously didn't realize how difficult it is to be a full-time father. And the challenges have hurt my happiness and relationship with my wife at times. I completely understand why so many couples divorce after having kids, even though a divorce might not be best for the children. Prioritizing your marriage and working together will take extra effort and time when you're already tired. But, you owe it to yourself, each other, and your little ones to give it your best shot.

See: How To Retire Early With Kids: A Nearly Impossible Situation

3) Thinking everybody can just move to a lower cost area of the country and be happy.

Everybody knows the Midwest and South are lower cost areas of the country than the coasts. Investing in non-coastal cities is a no-brainer in my opinion. Therefore, one of the key financial blind spots happens when some people who have no problem blending in tell people in HCOL areas to just relocate.

Here are some responses from a couple readers who are minorities addressing one reader who had asked, “Do people really care about diversity?” after I discussed one of the positive attributes of living in LA.

Mercury: Yes, not just diversity of race, sexual orientation, etc, either. Diversity of thought, travel, differentiated industries, food, cultural options, hobbies, etc. I lived in the midwest most of my childhood. Almost the entire male population spends its weekends only watching sports. Live in NYC now and don’t have to deal with that, can find plenty of people doing interesting things outside of watching other men play sports because there is a diversity of viewpoints.

A large amount of the increased real estate prices in places like Manhattan or SF are actually due to diversity. In my case, I’d rather pay $5k per month for a 1-bedroom in a large vibrant coastal city than live for free in the midwest.

Lilia: YES, that is a big part of why I live where I live!

I used to live in Central Ohio where the #1 and #2 hobbies seem to be drinking and watching football. I don’t enjoy either of those activities.

With greater diversity, you’re more likely to meet people who have interesting hobbies. More likely to meet people who were born in other countries and share their experiences and perspectives.

Also, being non-white, you’re less likely to get the “But where are you REALLY from?”, “Where did you learn to speak English?”- type questions. Because even the white people around here are used to more diversity.

Not saying people from racially homogenous areas are inherently bad or racist. They were just raised where everyone looks the same, which is part of the problem.

Repercussions for this ignorant financial blind spot

Uprooting your entire life to save on costs only to move back because you couldn't comfortably assimilate. Racial tension online and offline. Homogeneity in the FIRE community where the majority comes from low cost areas and all looks the same. A widening cultural gap between HCOL and LCOL residents. Bigger and bigger echo chambers.

The best way to understand what it's like to be a minority is to live for several years in a foreign country whose main language is not English and whose dominant racial lineage you do not share. Hopefully, most of your experiences will be positive, but there will also surely be some bad experiences which may be great for better understanding.

4) Underestimating health care costs in retirement.

Because employers subsidize most and sometimes all of their employees' health care costs, employees either don't know what their true health care costs are, or they take these benefits for granted.

It's the same reason why so many freelancers get into trouble when it comes time to pay their taxes. When they were working as full-time employees, their employer facilitated the payment of an estimated tax from each paycheck. If the government didn't require this practice, it would have difficulty collecting the majority of its tax revenue.

Here's one reader's questionable response to my article, Why $5 Million Is Barely Enough For A Family Of Three To Retire Early On where he criticized the featured couple's budget:

“Our healthcare costs are a rounding error and not even worth mentioning, we are both healthy young 30s.“

Commenter Sean and his wife are 31, don't have kids, and think the profiled couple's budget is ridiculous. Sean does not seem to realize that his healthcare costs are a rounding error because his employer pays for most of the cost!

Sean also seems to have a double blind spot. One, he does not recognize that healthcare costs rise with age and family. Two, he erroneously equates better health with lower premiums. In America, the richer and healthy subsidize the poorer and less healthy. This is the law.

Repercussions for having this blind spot

Having to go back to work with your tail between your legs because you underestimated the cost of health insurance. $20,000 a year is at least $25,000 in gross income that must be earned to pay for such cost.

Alternatively, you need $625,000 in retirement capital at a 4% rate of return to pay for this cost alone. Needing over $1,000,000 in after-tax investment accounts to live comfortably in retirement doesn't seem as far-fetched anymore.

Another thing is, you might not be able to find a job after years of being retired. And if you do find a job, you might find it difficult to last given you're not used to schedules and people telling you want to do. As a result, you could put your finances and health at risk if you don't have proper affordable health care insurance.

I decided to go back to work, consulting part-time for a fintech company from November 2023 through March 2024. Unfortunately, I could only last four months because of all the micromanagement. I was miserable and just had to leave, even though the pay was good. The job didn't pay any benefits, including health care insurance.

5) Believing the only path to financial independence is through a high income.

Obviously the higher your income, the more you can save. Just don't tell this to the countless high income earners who have blown away all their money and have nothing to show for decades later. It's often harder to stay disciplined financially if you have a higher cash flow. Why do you think the majority of Americans are overweight? It's because when the cookie jar is in front of you, you tend to eat more cookies.

If you believe the only way to wealth is through a high income, then you've already defeated yourself. You'll believe working on a side hustle, like driving a car, assembling furniture, or flipping burgers is beneath you. You probably won't be willing to put endless hours in an online entrepreneurial endeavor because you think only special people with money can do something unique.

Besides building more income streams through entrepreneurship or side-hustles, you'll also neglect the extremely obvious method of building wealth through investing or real estate. Risk must be taken to receive reward.

Repercussions for this financial blind spot

Not living your best life. The reality is, many people from all types of occupations and incomes can achieve financial independence. You don't have to be a techie, banker, doctor, or burned out lawyer with a high salary to reach FIRE. You just need to save and invest as much as possible.

In addition, by thinking you need a high income, you might also end up developing an unhealthy case of money dysmorphia. If this obsession with a high income as the only way lasts for years, you may risk damaging your mental health.

6) Investing in value stocks as a way to get rich quicker

After investing in public equities since 1996, I can firmly tell you that investing in value stocks is a waste of time if you want to FIRE. Value stocks are often value traps that stay suppressed for a long time. Instead, it's better to invest mostly in growth stocks, which increases your chance of building your capital basis larger and quicker.

Once you actually reach financial independence and want to protect your wealth, can you invest in dividend stocks and value stocks. With so many companies around the world growing quickly, I wouldn't focus on turnaround stories at all. Focus on growth stocks instead.

Curing Financial Blind Spots Is Hard

Nobody's situation is the same. Some will have more financial difficulties than others based on their abilities and circumstances. However, I firmly believe we can all make financial progress, no matter where we start off. If we have the opportunity to help others, all the better.

The easiest way to shine light on a blindspot is to listen to those who've been there before. Plenty of people have already achieved financial independence, so you might as well take in what they have to say.

Recently, I learned about one of my many blind spots from a reader. Against the herd, he felt the budget for the LA couple with $5 million in after-tax- investments was not only fair, but even a little modest.

$5 Million May Not Be Enough For Some People

He wrote, “No matter how disciplined you are, you always want the best for your children. It hurts to see other kids have more than yours and get to experience better things in life. This is much more so when you have $6,000,000+ in the bank. You know you can ‘afford' to give your kid anything. You are choosing not to. It seems selfish at times even if you know in the long run it may be the right thing to do.

For men, this is also true for our wives. I know many on this site have frugal spouses and they don’t ‘want' the finer things in life. Mine is certainly willing to live without. But, I don’t like seeing my wife do without, knowing I have millions in the bank. All within reason of course.“

I replied, “It’s interesting, but I’ve never thought about it being painful to not get my wife the finest XYZ because we have money. It’s probably because she's thrifty and hardly ever shops or wants anything.“

A Financial Blind Spot Of Not Recognizing My Wife's Desires

He responded smartly, “It might be that your wife wants more than you think, but she loves you and wants to support you in your FI goals. Her desire to make you happy may easily outweigh her desire to spend money. Took me awhile to figure that one out. Doesn’t necessarily mean she wouldn’t prefer the finer things in life if she genuinely believed it wouldn’t bother you. Could also be she is wired exactly like you. In that case, congrats on winning the spouse lottery.“

Ah hah! I've known my wife for 20 years now and I've always assumed she was super frugal and thrifty just like me. She tells me she doesn't like shopping, and her favorite store is Target and not Gucci. But I also notice her glee when she shops for little things online like a childhood Swatch she once had and lost.

My wife is definitely suppressing some of her consumption desires because she knows as the one in charge of our family investments and keeping us from not having to go back to work with the continued operation of this site, life can sometimes get stressful.

Life is so much better when we're able to listen to what other people have to say, and then share our own thoughts and solutions. So long as we have an open mind, I don't see why we all can't keep progressing.

Best Tool To Track Your Finances

To make sure you have no financial blind spots with your finances, sign up for Empower, the web’s #1 free wealth management tool to see where all your money is going.

With the Investment Checkup tool, you can elucidate any risky allocations you aren't aware of. The more you can stay on top of your finances, the better you can optimize your wealth.

Diversify Your Retirement Investments

One of the common blindspots renters have is believe they will always save and invest the difference to build more wealth. Unfortunately, the net worth data on the massive differential between renters and homeowners shows this not to be true. Investing in real estate is one of the best ways to build wealth long-term.

Consider Fundrise, a platform that allows you to 100% passively invest in residential and industrial real estate. With over $3 billion in private real estate assets under management, Fundrise focuses on properties in the Sunbelt region, where valuations are lower, and yields tend to be higher. As the Federal Reserve embarks on a multi-year interest rate cut cycle, real estate demand is poised to grow in the coming years.

In addition, you can invest in Fundrise Venture if you want exposure to private AI companies like OpenAI, Anthropic, Anduril, and Databricks. AI is set to revolutionize the labor market, eliminate jobs, and significantly boost productivity. We're still in the early stages of the AI revolution, and I want to ensure I have enough exposure—not just for myself, but for my children’s future as well.

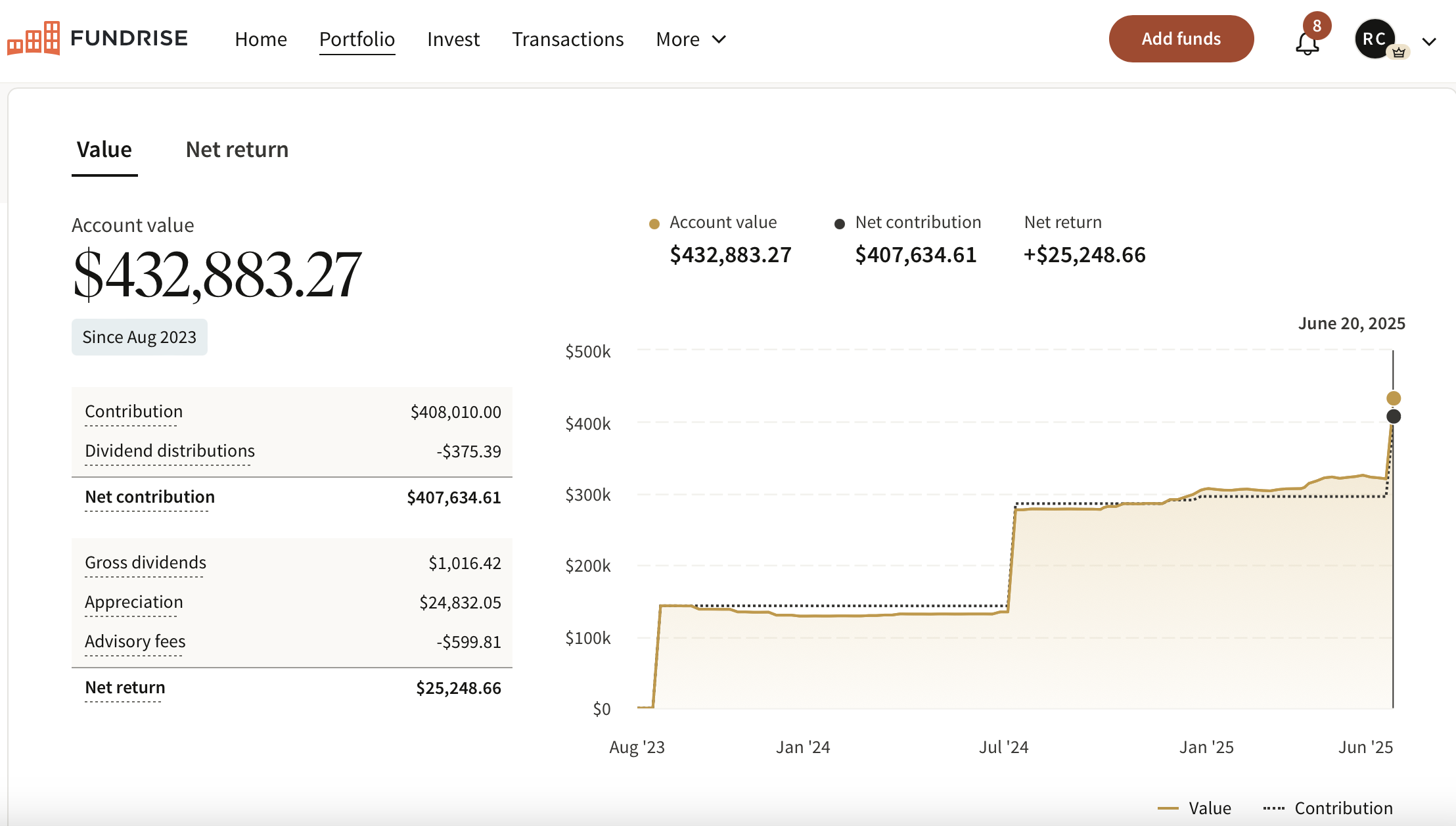

I’ve invested over $400,000 with Fundrise (my dashboard above), and they’ve been a trusted partner and long-time sponsor of Financial Samurai. With a $10 investment minimum, diversifying your portfolio has never been easier.

To increase your chances of achieving financial independence, join 60,000+ readers and subscribe to my free Financial Samurai newsletter here. Financial Samurai began in 2009 and is the leading independently-owned personal finance site today. Everything is written based off firsthand experience.

Common Financial Blind Spots On The Road To Financial Independence is a Financial Samurai original. Financial blind spots are more common than you think. Please be cognizant!

I have to say the last portion of this article was kind of insulting to women/wives. I am not a wife but I am a woman and am frugal, just like your wife. That isn’t to say I don’t want some of the finer things in life but I fall into the belief that frugal does not equal cheap. So when I look at items that are expensive and choose not to buy them it is because that item, while appealing, does not appeal enough to me for that price. I learned this behavior from my mother. I know she actually gets upset when my father attempts to buy her expensive things such as jewelry because generally she had looked at similar items in the past and dismissed them as not being something she wishes to spend the money on.

Yes your wife probably is partially frugal in order to “support you,” but she likely would be making similar decisions if she were single because it sounds like she and you are married because you have many similar values, to include being frugal. To imply that she wouldn’t serves to perpetuate the idea that women are always “spenders.”

Basically, If you suppress your desires for frugality, why wouldn’t your wife as well?

There’s a lot in this world to be insulted about, but coming to a realization that perhaps my wife is being more frugal on purpose to be supportive during difficult times is not one of them.

Relationships take a lot of work and communication, especially with a life partner. I wish you good luck in finding yours!

PS not sure who is suppressing their desires for frugality. We’ve been able to naturally suppress our desires to spend more out of habit.

Sam,

Here’s a comment and suggested future blog post regarding the blind spot you accurately identify: “Thinking everybody can just move to a lower cost area of the country and be happy.”

It’s totally true that it is hard to live in close-minded or culturally devoid places, especially when you are not the dominant race/class. That said, I think it’s important to highlight that high-income coastal cities are homogenizing at an alarming rate. You can get the same Intellengetsia coffee with the same well-educated, well salaried crew in SF, DC, NY, LA, Seattle, and soon Denver. The experience of working professionals in those cities an exceedingly narrow experience; the big coastal cities are all starting to look and feel the same. When they were in their “growth” periods, things felt alive, vital, diverse, open, and exciting. But they have simply reached a plateau of homogeneity that comes with wealth. Individuals who are reaching for new ideas, new businesses, are priced out. Thus, the coastal city experience feels uniformly slick and uninspired– only the big and corporate businesses can survive.

Howover, there are numerous open-minded, diverse places that are still in their “growth” phase — affordable and in the middle of the country, but building open minded, creative city experiences with the enthusiasm of Seattle in the 1990s – 2000s. FOR EXAMPLE:

Atlanta — I moved to Atlanta after living in Seattle, then DC, then Los Angeles (Santa Monica). I find Atlanta to me the most diverse, open-minded, and culturally interesting of all them. Businesses are still independent. The food scene is off the chart because creative chefs can afford to start restaurants — they don’t have to wed themselves to a corporate restaurant group. There is a true commitment to diversity and actually living among different races in a real way.

Other flyover cities that are affordable and open-minded:

Nashville

Chicago

Asheville

Charlottesville

Houston

Chattanooga

Truth be told, there is now an open-minded / proto-yuppie/hippie enclave in just about every small city in America. What’s more: they actually have independent spirit, single-owner operated stores, and are more invested in diversity because their states have historically lacked it. I think this is the holy grail for people looking to early retire who seek diversity and open-mindedness, yet did not work in finance like you and thus cannot even consider SF or even California at large.

I think a post on this from your blog could be really influential.

Great feedback. Part of the reason why I want to leave San Francisco because it is feeling very homogenous nowadays.

I do want to profile more people and their finances from various parts of the country. It’s gonna take a while, but if Rieder’s want to take a proactive measure, I’m welcome to more guest posts.

Healthcare costs can be hugely mitigated if you qualify for subsidies. You probably won’t be able to pull in your $200k/yr target, but you can get quite a high quality of life on $100k in actual spending while paying zero income taxes as a married couple if you can stack your capital gains and dividends in the right way. In a very simplified example, take $20k from principal contributions not counted as income, $60k from LTCG and taxed at a 0% rate, and $20k is from dividends which is erased by the standard deduction. Then just live in a no-income tax state. Overall taxable income flies just under the 400% FPL rate for subsidies and now your health care premiums are cut by 75%.

Also, with a kid you’ll get money back from the government since child tax credit is refundable.

It’s amazing how cutting income down below these critical barriers (0% LTCG bracket and 400% FPL) provides enormous financial benefits, easily as much as another $25k in income a year.

“In America, the richer and healthy subsidize the poorer and less healthy. This is the law.”

-This is true in every advanced country.

In other nations, you pay 20% sales tax for “free” healthcare.

In America, we pay hideously inflated hospital bills to pay for the people with no insurance, inflated insurance premiums to pay for the people in our insurance pool who are sickly, and about 10% (including both your contribution and the employers) in income tax to cover free healthcare for old people and desperately poor people (Medicaid).

At least socialized medicine is more straightforward about the costs.

That being said, I think unless you live in a big city, you probably won’t have medical costs of $20k a year until you’re old, at which point you’ll have Medicare to help you. 50 year old me who is in early retirement (and freed from the stress of work) ought to be just as healthy as current me (23). And finding an affordable healthcare plan isn’t hard for a healthy single man in early retirement.

[i]What would you recommend we spend more money on?[/i]

4X4 (overlanding)

motorcycle (street)

motorcycle (off-road) or ATV

boat

plane (light-sport)

Two blind spots I found were a lot of relatives and friends have this idea you have to invest a lot of money up front to make a difference and because of that they become overwhelmed and don’t even try. They would assume some massive number, typically a million or more, that they had to save. Or they would hear they had to save 10-20% of their salary and figured they couldn’t possibly afford that as they lived paycheck to paycheck. Then because they couldn’t see saving that number or percentage, they chose to save nothing because what was the point? They would fail anyway so in their eyes why start a path to failure?

I’d tell them I started my kid’s college fund with $20 a paycheck when each was born, and they’d laugh and tell me my kid wasn’t going to college unless they got a free ride.

I’d tell them I started my retirement fund with just enough to get the matching and they said I might as well spend it because I’d have to work until I’m 80 to be able to retire on that.

Their problem is two fold. First they assume “start” equals “always” and fail to understand that starting is harder by far than piggybacking onto something already moving. Second, they totally overestimate what they really need and become overwhelmed without considering their own situation.

It took ten times the effort to open and set up automatic deposits to a 529 from my bank account for each kid’s college account back in the day than a phone call (and later on a click on the computer mouse) to increase the amount saved once a year or when I got a raise or promotion.

It took more thought and effort and mental worry determining how we were going to make ends meet without that initial 3% of salary than taking 1 or 2% out of a 4-6% raise or promotion multiple times over the years and putting it towards retirement.

Starting not only got us into the habit of saving and not touching certain accounts, it allowed us to add to those accounts painlessly and seamlessly to both grow our amount annually saved and the amount in the accounts.

The second part of their problem was overestimating what they needed based not on running the numbers themselves, but on what they heard typically from friends or bylines on articles meant to make you read them.

For example, you don’t NEED $200K or more for a college education. $4K local community college per year and $21K per year for a kid staying at a in-state college or university will do the job in many states. Total, $50K or so per kid. That’s paying for it all, excluding scholarships, work study, etc. Most any other “costs” you’re already likely paying or making them pay for (car, spending money, etc.) while they were still in high school so it’s not an “increase” to you.

Also consider almost none of my relatives would even NEED a million in assets for retirement. $500K with a safe withdrawal rate of 4% or $20K a year plus their SS of another $10-15K a year at 65 would cover the majority of my relations who don’t earn more than $35-45K a year, many earn less so they could have gotten away with $200-300K in retirement. But because many were so focused on the big numbers, they never thought to think that even having something would be better than having nothing.

Yet, they would argue with me about it and how saving was a waste. Or at least they argued until they began hitting their 40’s and 50’s.

OFF TOPIC ALERT

In a recent email you said that you were going to lighten up if and when the S&P reached 2850 – it was right near there at about 2800 when BAM a 2.5% decline today to about 2720 at this writing. What do you make of it?

I’ve been on the receiving end of someone else’s blind spot. During Thanksgiving, I mentioned to my sister how I just got a new car and have been driving for Uber for a couple of months now to cover the car loan that I didn’t want to have (despite being within the 1/10 rule). My sister calls me a couple of days ago to tell me that she transferred money to my bank account to pay off the car loan because she didn’t want me driving for Uber because of safety concerns. I tried to assure her that I’ve never felt even slightly threatened by any of my riders, but she insisted that I shouldn’t be spending an extra 10 hours a week doing Uber in addition to my full-time job. Granted, I do give off the image that I don’t have much money with the various ways I try to save (earning money with gas and shopping apps, saving 3-7% with discount gift cards for stores I need to shop at anyway, riding a bike to work for 6 months before getting freaked out after being hit by a car) and make money (side hustles doing wedding flowers, baking cakes, Uber). However, I don’t have a lot of liquid funds since I invest most of it with every paycheck, so I do feel “poor”, which is good because it keeps me from spending on things I want but don’t need. My sister’s blind spot is assuming that I don’t have money due to the lifestyle I lead. My blind spot is assuming that everyone is trying to reach FI or at least hoard as much cash as they can. My sister insisted I take the money because in her words “it’s not as if I’m going to miss it.” The funny thing is I’ve mentioned the FIRE concept to her on multiple occasions and she doesn’t seem to have any interest in it even though she has the six-figure income to easily achieve FI.

Your sister seems to be very kind hearted.

I’ve always been grateful that I don’t have sisters because that would’ve meant I would’ve had to share my stuff growing up but every now and then a story like yours comes along and makes me wish I did!

My sister is a sweetheart. She’s complex though. She’s quite ambitious and has never let anything stop her from achieving her goals. While growing up she claimed that she was the least intelligent out of the four of us siblings yet she is making more money than two of us; our other sister is an ER doctor. If you asked me, I’d say she has a better quality of life compared to the ER doctor. It goes to show that persistence and determination count for a lot.

While I assume most of us are talking about healthcare/insurance costs in early retirement (FIRE) it’s important to note once you DO hit 65 or are eligible for Medicare, your premiums and costs drop dramatically. Assuming you’ve worked 40 quarters in the US, you’d get Medicare Part A for “free’ and your 2019 Medicare Part B premium would be $135.50. Monthly. It’s means-tested (more expensive) if you’re making more than $170k annually but tops out at $460 per month if you’re making more than $500k per year.

I point this out, because too often media outlets (looking at you here, CNBC) put up huge, 6-figure numbers needed for “healthcare” in “retirement.” It’s just not true.

Example: If you want to close the 20% coinsurance gaps in Original Medicare Part A and Part B, you only need to look at a $0-monthly premium (HMO, PPO) Medicare Advantage plan with a prescription drug card embedded. They look, feel and walk like what most employer coverage looks, feels and walks like – copays for physician visits, fixed costs for hospital visits… they’re comprehensive and MUST cover everything Original Medicare covers. It’s estimated 50% of all Medicare beneficiaries will be on these things by 2030. They’re all over the place, in plenty of primary, secondary and tertiary markets across the US. And, every one of them has an annual out-of-pocket maximum ($6,700 or below) so once you hit that number (think: horrible plan year) you’re done spending for the year. That’s the BIG potential pitfall of staying on Original Medicare Part A and Part B – there is no maximum annual out-of-pocket. If you get really sick, you could just keep spending and spending and spending…

Sure, you could buy a Medicare Supplement policy that will mostly fill in all the gaps, too. Those will cost you $150-$250 per month, plus a Part D card at $15 in addition to your Part B premium.

This isn’t an ad in any way… I just want to give those of you in your 50’s the perspective that yes, you will have to figure out your health insurance until you hit Medicare age. BUT when you do, your out-of-pocket costs can drop dramatically. Still way less combined expense than most take into account in their “retirement” spreadsheets. Don’t let those news outlets scare you off. They don’t get it.

Anyone who thinks parenting is easier and cheaper than it is, is probably walking around with their eyes closed and this is coming from someone with zero kids!

Even the easy kids like my brother and I (who didn’t demand toys and things) were probably a huge financial drain on my folks just with our basic necessities of food and clothes.

A few years ago, I learned boarding schools for boys are more expensive than for girls because of the food bill! My brother was and still is a food vacuum cleaner growing up.

I don’t think I’ve ever had any of the financial blind spots listed above. My blind spot was lifestyle inflation too early on in my career but then I didn’t know better or that there was another way to live.

Regarding #3 – I’m glad you included the ‘diversity as amenity’ discussion because I also thought it was quite an interesting point.

I do question the justification for costs though. I am white, male, late 20s, English is my first language. However, I’ve lived in Korea since 2016. While there are certainly uncomfortable moments, if I were saving significantly more (as an absolute number or as a percentage) I would stay in a heartbeat. In general I would say Koreans are much less understanding of “foreigners” (as we are all collectively called here), being one of the least diverse countries on the planet; however, there is of course an element of idealization of white people/western culture in some situations. Balanced, in my opinion, by demonization or disregard in others.

I can understand those people’s comments. There are also some westerners here that become resentful and bitter but stay for financial/cashflow reasons. But I question the idea that that is an inevitable downside of living in a homogenous society. It seems that it’s an issue with the minority of people who get incredibly angry about ignorant/naive questions and comments. I actually find them to be the intolerant ones, as they cannot accept folks who are less worldly, experienced, or understanding than they think people should be. I think this is simply an excuse to continue living in expensive metropolitan cities where things are generally more interesting.

Really like this post Sam!! These blind spots show that their is more than just numbers especially with moving to a LCOL area. Sure moving from HCOL area to a LCOL area sounds logical because you are able to save more but you have to think of the emotional impact it will have. Will be able to adapt to your new location and enjoy it? Will be sufficient to make this move with the people that are moving with you(really crucial for a family doing this)?

Some of these financial blind spots is beyond the numbers and that is something we all have to seriously consider when making decisions.

Excellent list of blind spots! And a great motivational read. It’s easy to get sucked into spending mode at this tome of year with all the retailers going on full blast to lure us in. What helps me is sending in my estimated tax bills and property tax bills. No quicker way for me to feel like a grumpy gus about money outflow and make time to give thanks about what I already have. For me the cost of kids and healthcare are prominent. I just hope I don’t have the quantity and frequency of health issues as my parents do when I’m older. I gotta take better care of my health now and live as long ad possible at a high quality of life!

Great article! As a parent of 4 children (22-11) there are a few financial issues I have recently seen first hand with my friends, or my children’s friends that will ruin them.

1. College – Letting the little darling spend whatever they want to go wherever they want. Some parents looking at 200K or more for undergrad. Some parents even borrowing for Grad school or Med/Law school.

2. Weddings – Parents spending upwards of 50k or more for one day.

3. Adoption/IVF – People in their 40s desperately trying to build a family. IVF isn’t covered by insurance and can take multiple times at 15k each try. Adoptions can be over 25K easy.

4. Buying homes/Lifestyle payments to children. You have mentioned this one in the past, but the stories of late 20 children needing a handout from the parents is getting to become rampant. Several co-workers delayed retirement because they couldn’t say no to their kids.

Kids are expensive when they are young, but the cost NEVER goes away.

Under estimating healthcare costs now and in retirement will be a blind spot for most. Until recently we were not a big consumer of healthcare. That all changed with one diagnosis. For the first time in our adult lives we have hit our health insurance out of pocket maximum with less than 3 months since diagnosis.

Even if you have employer sponsored healthcare you need to educate yourself on prices in the market. It is gradually becoming more transparent – but you have to work hard on it and shine the light on the issue.

Ask what the cost will be. Cost being what the insurance and you will personally pay – not the gross charge a healthcare provider will submit to your insurance.

Most people have no idea that a prescription drug picked up at a pharmacy can have different prices at different pharmacies. Don’t just ask your pharmacist what the clinical side effects are, ask your pharmacist the more difficult question about what your cost will be!

C’mon man…. What’s the issue with Ohio State football? Please come to Columbus for an OSU game eventually. You’d love it. So much fun!!! Thanks for the post.

Europe wants to settle energy transactions in euros. Looks like Saudia Arabia has been selling oil for RMB, just not announced it.

Big step functions could be near.

I’ve lived in Southeast Asia as a white America for 15 years. I have never had a single problem tied to race or nationality. Truth is, most “minorities” don’t have them in America either. Being offended is a part of life, and it’s nothing like red lining in real estate or lynching. I laugh when I see an Asian crying about racism in America, since Asians are the richest and most educated ethnicity in the country.

This is a great blind spot as a white man living in Southeast Asia, not realizing that the average American is way wealthier than the average Southeast Asia. When you’re wealthier and come from a wealthier nation, do realize you get treated better.

Also, great blind spot about not granting resilience, work ethic, and perseverance to Asians getting ahead in America. And also disregarding other minorities.

Thank you!

Where exactly did he say that Asians don’t have those qualities? Or are you just assuming his perspective so you can feel indignant?

I think the point is there will always be off-color comments and awkward moments. It’s not worth throwing a tantrum over, since at the end of the day the only person upset by it is yourself.

The problems will vary by location and race and situation, but you can always choose whether you let it get to you.

Not sure who is throwing a tantrum? The post was pretty measured in my opinion.

Thanks for bringing attention to some of the issues of living in LCOL midwest. Definitely a true blind spot as most people don’t realize what is important to them until it’s gone.

As an Asian American currently living in the midwest (raised in LA), I can now see a clear value of having diversity in a coastal city. And, like you said, it’s not just racial diversity, but one of different backgrounds, thoughts, and interests.

I live in Chicago, there’s plenty of diversity here! Just curious Jas..where do you live in the midwest?

Great insight in this article. I love the concept of financial blind spots.

I agree wholeheartedly about the challenges of reaching financial independence with kids. We have four (!) and it definitely requires a much higher degree of effort to break free above and beyond the expenses that our children need to thrive. Then, it’s a tricky circle because you’re working hard to save, but that necessarily takes time away from the kids. From a distance, I am fond of Sam’s approach of reaching independence before having kids, but on the other hand I wouldn’t change our situation for anything. It’s complicated! :)

This blind spot exists, I think, for precisely Sam’s explanation: people underestimate how hard and expensive parenting is. Parenting also more rewarding than people think (yay!), but the overall commitment is definitely underestimated.

People who do well with career and family embrace the high energy it requires. Just go all in and do your best with the energy you have (and hire help, if you can afford it!).

Thanks for the great article, Sam. Really made me think.

The biggest blind spot of all is the ignorance of sovereign debt cycles.

Great point about the kids. Help is definitely needed sometimes. I will add that if you have family close by willing to give a helping hand that is a BIGTIME bonus.

Lots of food for thought here. Definitely appreciate the acknowledgment of the full time parents!. A couple items:

1) Moving to a LCOL area only helps if your income stays the same(ish). If a teacher moved from the coast to the midwest, they’d likely be just as bad off if not worse because salary, benefits and workplace support scale by local tax base.

2) Young people today aren’t just too ignorant to realize accomplishments grow as you age. The workplace is very different now than it was when 50-60 year olds were in the same place. Expenses like housing, food, education are significantly higher while it’s harder to get a steady job with benefits. There’s some of that lack of insight, sure. But their reality and the future they have to look forward to is not the same.

I respectfully disagree TR.

Young people have more opportunities than they ever had thanks to technology. They also have more BS to deal with, again thanks to technology but I feel the positives far outweigh the negatives.

It goes back to Sams number 1 blind spot.” Comparing someone’s middle to your beginning “ I also think it works in reverse. “Comparing someone’s beginning to your middle”

It’s a mixed bag. Part time positions, lack of benefits, and importing temporary workers/outsourcing to other countries are much more of a factor. Wage inflation and the decline in quality of jobs is a real and widespread problem.

However, the ability to create income outside of a job is much more accessible. I feel the younger people who really suffer are the ones trying to live their life as if it was still 1970 — faithfully following the ‘1) college 2) long career at one company 3) ??? 4) profit’ model.

“My children the only true technology is nature. All the other forms of man made technology are perversion. The ancient dictators used technology to enslave the masses” 1977

Number one. It’s always number one for me as of now.

However, at 34, a number of friends are beginning to have, or recently had, kids, so I can see the parenting blindspot continuing to grow (and then change) for those that I know.

– Mike

Underestimating health care costs in retirement.

True true true !

Especially in the USA….

Dear Sam

regarding the point:

“Thinking everybody can just move to a lower cost area of the country and be happy.”

do you really think (based on your experience as Asian American) there might be racial tension in Central USA (non-coastal cities?)

thanks

I am an Asian American living in the Central USA. I am in my early 40s (immigrated when I was young).

I look back at elementary yearbook pictures, The majority of the time, I’m the only non-white in my class. At the school level, maybe we were two dozen or less.

Up through college, I frequently did get “your English is really good.” Even to this day (though less frequently), I will be asked where I am from, my presumed assumption for that question is that if you’re non-white/african, you have to be from somewhere other than the US.

I live in a college town, so there are many areas of diversity and we’re definitely able to find “like” minded people.

However, when I go into work – there still aren’t a lot of people that look like me.

That’s not a unique problem to the midwest though. Even working at a CA tech company, if you’re Asian – you’ll see others like you, any other ethnic minority – not so much.

I am happy with my MCOL area, family is close by and am happy to use the $$ we’ve saved to go visit the coasts and come back home to space and fresh air!

We each do what makes us happy!

You know I hear the where are you from thrown out as a racial perception thing a lot, but I think there is more to it then that. I live in Delaware. Almost no one is from Delaware. So the first question I’m ingrained to ask is where are you from to anyone I meet, regardless of race. ( I’m not a native of the state either)

Conversely, I’m white living in Asia — and get the same type of questions/assumptions. People refer to me as “American” or “foreigner” and I’m often complimented on my language skills after literally only saying “hello”. There are 2-3 white people in my neighborhood and it’s only me at my workplace. But to let those minor annoyances dissuade you from living where you want to live is absolutely insane in my opinion. I can’t imagine placing surrounding myself with ‘my tribe’ above my own success.

How old are you and you have a family? Maybe you are getting surprised out in Asia and you don’t even know. Asian wages and salaries are generally much lower than here in the United States.

Like Sam, I found that younger people tend to be much less empathetic until they have seen more ups and downs.

It’s definitely not somewhere I would be if I had a family. Society can be crushingly conformist at times and the pressure on students to be socially accepted and academically excellent is too intense. It creates a lot of good kids but also a lot of suicides and people dropping out of society entirely. So, I will be returning before that stage of my life. For now, it’s a good way to save money, gain skills and make memories in the process.