To celebrate Millionaire Milestones: Simple Steps To Seven Figures making the USA TODAY national bestseller list, I want to share how you might feel and what you might do as you hit various levels of wealth (net worth). Perhaps by sharing, I'll motivate you to save and invest more aggressively. We'll start with reaching your first million, then move on to $5 million, $10 million, and $20 million.

I stop at a $20 million net worth because once you surpass that threshold, there's not much left you can spend money on to meaningfully improve your lifestyle. Beyond a $20 million, building more wealth simply becomes a game, a personal challenge, or an exercise in greed.

As the Chinese philosopher Lao Tzu once said, “A journey of a thousand miles begins with a single step.” When it comes to building wealth, you must be intentional. Treat managing your finances with the same passion and precision you give to your favorite hobby.

Those who wing it will wake up a decade from now wondering where all their money went. But those who stay intentional—reviewing their finances regularly and investing in their financial education—will build lasting wealth. More importantly, they’ll unlock the freedom to live life boldly, on their own terms.

1. Reaching Your First Million: Relief, Validation, and a Sense of Real Possibility

When you hit your first million dollars in net worth, you’ll feel an overwhelming sense of relief first and foremost. You’ll think to yourself, “Finally, all those years of saving, investing, and grinding have actually amounted to something tangible.” It's a huge milestone you should be proud of.

It’s like crossing the finish line of a marathon where the prize isn’t just a medal, it’s the ability to breathe a little easier. You won’t necessarily feel rich, especially thanks to inflation, but you will feel validated. You’ll realize that as an employee, building wealth is not just for other people or institutions, it’s for you, too.

Your first million will also give you a huge psychological unlock, if most of it is liquid. Suddenly, you’ll see possibilities everywhere. The fear of financial ruin won’t vanish, but it will shrink given you'll be able to generate $40,000 – $45,000 a year in passive income, risk-free at today's interest rates. You’ll start to imagine what life might look like if you really ramp things up.

Most importantly, the first million is where you internalize a crucial truth: the snowball gets bigger on its own. Saving that first $250,000, as I write in my book, might have felt like climbing Everest. But once you have $1 million compounding at 5%–10% a year, you're talking about $50,000–$100,000 a year in passive growth without lifting a finger.

You can aggressively play offense now, not just prevent defense. You can afford to take more risks, something I wish I did more of when I was younger.

Common Pitfalls Getting to $1 Million:

- Lifestyle creep: As income rises, spending rises even faster for the undisciplined.

- Investment FOMO: Chasing the next hot trend (and blowing your finances up) instead of sticking to a plan.

- Quitting too early: Giving up on saving or investing because the early gains seem too small.

- Buying too big of a house: A nice house is great for lifestyle, but make sure it's manageable to not drag down your net worth growth too much

2. Reaching The $5 Million Milestone: Confidence, Options, and a Taste of True Freedom

Once you reach the $5 million milestone, a quiet but profound confidence starts to settle in. You no longer have to calculate whether you can afford the organic blueberries at Whole Foods. A $7,000 unexpected home repair or even a $50,000 investment mistake that plummets 20% soon after no longer feels like a big deal.

You also start to realize you have options. A $5 million net worth can throw off $150,000–$300,000 a year in passive income, depending on how it’s invested. That’s enough to exceed the median American household’s entire pre-tax income of ~$80,000 without working another day in your life.

If you’ve been stuck in a soul-sucking job or run a business that gives you ulcers, $5 million lets you walk away. But of course, try and negotiate a severance package so you have an even greater financial cushion when you do. If you’ve been dreaming of living abroad, working part-time, or starting your own business, $5 million gives you the luxury of choice.

Unfortunately, you’ll still worry about your finances.What if the stock market crashes? What if rental income dries up? What if health care costs explode? But you will rationally make contingency plans if any of these things happen.

Overall, your anxiety will diminish because you know you have true staying power. In a previous Financial Samurai poll, $5 million was the ideal net worth to retire with, followed by $10 million. You are set for life if you remain vigilant with your finances.

What Happened To The $3 Million Net Worth Milestone?

Some readers have asked why I skip the $3 million milestone, given the jump from $1 million to $5 million is large. I agree it’s a notable step.

Hitting $3 million is a solid financial feat. It can free you from a bad job or open new doors, but it doesn’t feel much different from $1-$2 million. I chose to highlight $5 million because that’s when the sense of freedom and financial security starts to feel exciting again, much like hitting your first million.

Common Pitfalls Getting to $5 Million:

- Overleverage: Taking on too much debt or trading on margin thinking it’s a shortcut.

- Burnout: Pushing too hard at the expense of health, family, and happiness.

- Status signaling: Overspending on cars, homes, watches, and jewelry to “show” you’ve made it. It's interesting, but some of the most insecure people I've met are also those with net worths close to the $5 million mark.

Here's a fun clip from one of my favorite TV shows, Succession, which pokes fun at how $5 million is barely enough if you live in an expensive city like New York. You may not feel rich with $5 million in NYC, SF, LA, Seattle, or Boston, but you should feel comfortable enough.

Looking Back At Retiring With $3 Million In 2012

I left my banking job at age 34 with a net worth of approximately $3 million. Adjusted for a 4% compound annual inflation rate, that’s about $5 million in today’s dollars.

At the time, $3 million felt like enough because I only had myself, and eventually, my wife to take care of. My investments were generating around $80,000 a year in passive and semi-passive income. Combined with a severance package and the support of my wife—who was 31 then and willing to work for another three years—I felt it was time to peace out.

Still, I was nervous and insecure about leaving my day job so young. Looking back, I probably should have worked for another three-to-five years to further solidify my finances. With $3 million, I was much more argumentative in the comments section too. Now I’m not. If you plan to start a family, then getting to that $3-$5 million net worth range is important.

That said, everything has worked out because I found purpose. I found something I love to do that generates supplemental retirement income, and, more importantly, I became a father. In the end, retiring early gave me the flexibility to build a more meaningful and fulfilling life.

3. Reaching The $10 Million Milestone: Abundance, Status, and Subtle Shifts in Relationships

At the $10 million milestone, your world view may shift again. Scarcity thinking—the nagging belief that there’s never enough—starts to dissolve, but never truly goes away.

With a $10 million net worth, you'll feel an underlying abundance mindset take over:

- You can generously tip service workers without thinking twice.

- You can say yes to experiences you once would have passed up because of cost.

- You can invest in your health, relationships, and personal growth without financial hesitation.

- You can eat wagyu steaks and toro sashimi until you're sick of them both.

- You're part of the richest rich class who didn't get rich through index funds

- Upgrading to Economy Plus or even first class is no problem

- People don't piss you off as much anymore

- You can more easily migrate to another country to save on taxes

- Perhaps best of all, you can easily speak your mind and stand up for yourself without fear of financial ruin

Being A Multi-Millionaire Can Have Its Problems

At this level, status becomes more visible, whether you like it or not. People may treat you differently once they know—or sense—your wealth. Friends and family might ask you for favors, loans, or business investments. You’ll need to develop a thicker skin and clear boundaries.

With $10 million, you'll probably embrace Stealth Wealth like a secret agent trapped behind enemy lines. You didn’t spend all these years building your fortune just to get hit up for handouts, judged, or peppered with investment pitches every time you leave the house or turn on your laptop.

As a millionaire ten times over, people will be quicker to judge your actions and far less sympathetic when you're feeling down. Even though millionaires need love too, people may simply not care if you're feeling down and out. Hence, you purposefully become more guarded with your friends and acquaintances.

Thankfully, some of your relationships will deepen. You'll naturally gravitate toward people who genuinely don't care about your money.

No longer will you feel the need to maintain relationships just because someone holds sway over your financial or career future. Instead, you'll start surrounding yourself only with people you truly enjoy being around. Say goodbye to toxic relationships!

Having A $10 Million Net Worth And Children

If you have children, reaching $10 million also changes how you think about legacy. How do you empower your kids without spoiling them? How do you prepare them for a world where they don’t have to struggle financially the way you did?

Fat FIRE parents might worry even more because they no longer have traditional day jobs that force them into the office 40+ hours a week. At least if you have a day job and a $10 million net worth, your children will know that you are working hard.

As a result, FIRE parents will likely have to make up a “trust fund job” to demonstrate their work ethic and purpose to their kids. Otherwise, they might ruin their perspective on life and money.

At the same time, with so much wealth, you may naturally start toying with the idea of making your kids millionaires too. You know firsthand how hard it was to get here, so it’s only natural to look for ways to help them shortcut the journey.

Just be careful. Taking away your children’s drive to become financially independent could end up being one of the greatest disservices you do for them. As you know, one of the greatest feelings is achieving something mostly on your own.

Common Pitfalls Getting to $10 Million:

- Neglecting tax efficiency: At higher wealth levels, minimizing taxes becomes just as important as investing well.

- Poor estate planning: Without smart legal structures, you risk losing millions to taxes or probate.

- Not cashing out or diversifying into safer assets: Outsized income and company valuations do not last forever. Without diversification, your net worth swings can be huge.

4. Reaching The $20 Million Milestone: Peace, Purpose, and a Reduction In Material Desires

Crossing into $20 million territory feels less like a major “event” and more like an arrival. You realize there’s almost nothing left to buy that will materially improve your happiness.

A $50,000 watch won’t make you feel better than a $500 one, so you don't get one. A $200,000 car won’t make you happier than a $50,000 one, so you drive your current car until it breaks. You could buy a third or fourth home, but would you even have time to enjoy them? You can't because you can only live in one place at a time.

The only real splurges you can enjoy with a $20+ million net worth are flying private, renting vacation homes for $50,000+ a month, and paying for $60,000+/year private grade school without worry. You could do these things with “only” a $10 million net worth too, but you'll feel the expenses more acutely.

But even with $20 million, will you really be willing to spend $120,000 on a roundtrip private jet flight from San Francisco to Honolulu when four first-class seats cost just $10,000? Probably not. The more disciplined you are with your personal finances, the less likely you’ll be to splurge on such unnecessary luxuries.

You might also finally feel like you’ve won the lottery, as you could easily generate $1 million a year in almost risk-free income for the rest of your life. The happiest people with this type of outsized wealth recognize their luck and never forget it.

You start thinking about legacy in a more profound way:

At the $20 million milestone, the real luxury becomes time, health, and relationships.

- How can I make an impact beyond myself?

- Who can I help with this abundance?

- What institutions or causes will outlive me?

- Will my children grow up to be outstanding citizens who make something of themselves?

Ironically, at $20 million, if you’re not careful, you risk losing your edge. The hunger that fueled you to work harder, save more, and invest smarter might start to fade. That’s why having a purpose beyond money becomes so crucial.

In addition, once money is no longer a problem, all your other problems come into sharper focus. Neglected your spouse and children on your path to multi-millionaire status? That regret may now feel overwhelming as you can't get that time back. Prioritized your career at the expense of your health? Suddenly, nothing seems more important than getting fit so you can live longer now that you've won the lottery.

If you ever reach this level of wealth, never voluntarily reveal how much you have. Let others guess, but never confirm. Instead, throw them off the scent by looking and acting as normal as possible. Your health, happiness, and safety depend on staying humble and low-key. If you must share something, let it be your generosity.

Your Financial Worry Might Actually Rebound

Ironically, reaching higher levels of wealth can bring back financial anxiety. The more you have, the more there is to lose. A 20% decline could erase $4 million to $16 million. It's a gut-wrenching amount, even if you're still financially secure. That’s why your mindset naturally shifts toward capital preservation, all while trying to stay ahead of inflation.

One reason real estate and private investments become more appealing is that you don’t see the daily price swings like you do with public stocks. With your money locked up for 5 to 10 years, you're less exposed to the emotional rollercoaster of market volatility. As a result, you are more likely to feel at ease.

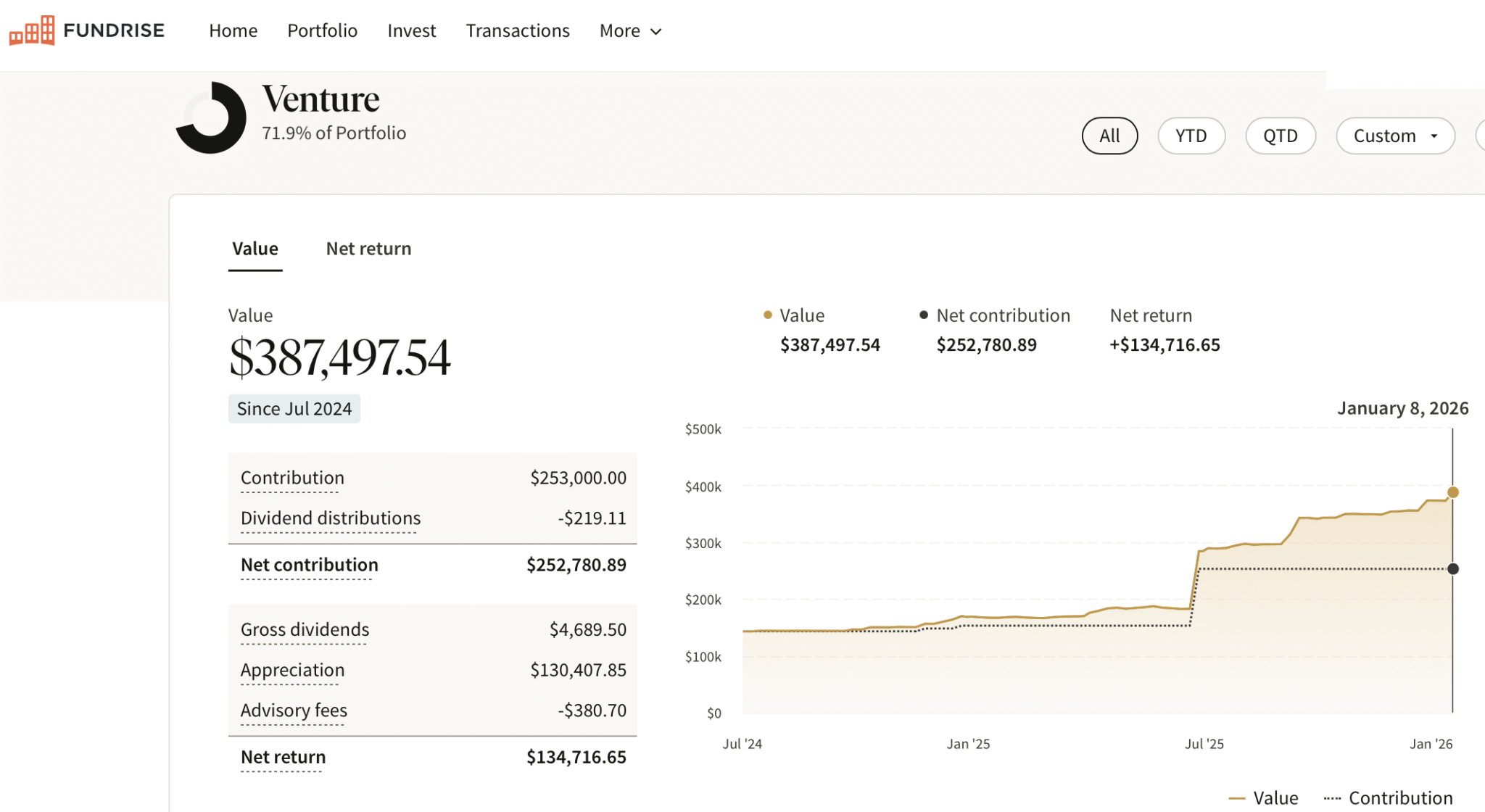

If you're looking to diversify your real estate investments and generate more passive income, check out Fundrise, my preferred private real estate and venture capital platform. Fundrise manages around $3 billion in assets for over 380,000 investors. I've personally invested over $400,000 in their commercial real estate and venture capital offering. They've also been a long-time sponsor of Financial Samurai.

At this stage, the real battles are psychological. You may find yourself wrestling with how you should feel about having outsized wealth. How dare you feel sad or ungrateful, but you sometimes do. Guilt is an emotion that sometimes emerges as you wonder why you?

In time, you might even downplay your financial success, convincing yourself you’re not as rich—or as lucky—as you truly are.

Common Pitfalls Getting to $20 Million:

- Losing your drive: Without new goals, it's easy to plateau since nobody needs more than $20 million.

- Isolation: Wealth can unintentionally distance you from old friends and even family. Stay grounded, unless you proactively seek out friends who also have a similar level of wealth.

- Might get trapped in a bubble: Your expectations for how to spend, earn, and think about money can run completely counter to the 99.5% of the American population who have less.

Wealth Is Built on Thousands of Micro-Decisions

Each millionaire milestone you reach brings a sense of satisfaction. But it’s the $3 million, $5 million, $10 million, and $20 million marks that tend to feel the most significant.

None of these feelings—relief, confidence, abundance, joy, or peace—happen by accident. They happen because you took thousands of intentional steps over years, sometimes decades.

Remember:

- Every $100 you invest instead of spend

- Every hour you spend learning and creating instead of mindlessly consuming

- Every risk you take to level up your skills or career

It all adds up.

Time To Focus

Building wealth is a straightforward formula, but sticking with it takes resilience. Inflation will keep shifting the targets, and today’s milestones may look modest in thirty years.

But with enough discipline, patience, and purpose, you can achieve more than you ever imagined. The real reward is not just reaching a number, but growing through the process—learning, adapting, and gaining the confidence that comes from doing the work.

If you want to create a life of freedom for yourself and your children, take the first step today. You may find that the journey itself becomes the greatest part of all.

Recommendation To Build Wealth

Stay on top of your net worth with Empower, the web's #1 free financial app. Track your cash flow, x-ray your investment portfolio for excessive fees and inappropriate risk exposure, and use their retirement calculator to plan for the future.

If you have over $100,000 in investable assets—whether in savings, taxable brokerage accounts, 401(k)s, or IRAs—you can sign up for a free financial check-up from a professional at Empower. It’s a no-obligation opportunity to have a seasoned advisor—someone who analyzes portfolios for a living—take a fresh look at your finances.

A professional review can help you identify hidden fees, inefficient allocations, or missed opportunities to grow and protect your wealth. More importantly, it can give you the clarity and confidence to know whether your current savings and investment strategy aligns with your long-term financial goals.

I've taken advantage of three free consultations with Empower over the past decade and they've been great. There's no rewind button in life. Make the most of everything, especially things that are helpful and free.

The Next Million Dollar Windfall: Investing In AI

One of the ways I plan to make another million dollars is by investing in private AI companies. Since private companies are staying private for longer, more of the gains are accruing to early, private investors. It only makes sense to allocate more capital to this space.

I believe artificial intelligence will significantly disrupt the labor market in the future, potentially making it harder for my kids to find fulfilling careers. To hedge against this possibility, I’m investing in both private and public AI companies. That way, if AI does end up reshaping the job landscape over the next 20 years, our AI investments could perform exceptionally well.

Check out Fundrise Venture, an open-ended product accessible to all. It invests in the following five sectors:

- Artificial Intelligence & Machine Learning

- Modern Data Infrastructure

- Development Operations (DevOps)

- Financial Technology (FinTech)

- Real Estate & Property Technology (PropTech)

Roughly 85% of Fundrise Venture is invested in artificial intelligence in some capacity. In 20 years, I don't want my kids wondering why I didn't invest in AI or work in AI!

The investment minimum is also only $10, making it accessible and easy to dollar-cost average in. Most venture capital funds have a $250,000+ minimum. You can see what Fundrise is holding before deciding to invest and how much. Traditional venture capital funds require capital commitment first and then hope the general partners will find great investments.

I've invested $253,000 in Fundrise venture so far, and plan to keep investing until I build a $500,000 position to hopefully make another $1+ million return within 10 years. There are obviously no guaranteed returns when it comes to risk assets, so invest according to your risk tolerance and goals. Fundrise is a long-time sponsor of Financial Samurai. Our investment philosophies are aligned.

Pick Up A Copy Of Millionaire Milestones Today

As I wrote in my USA TODAY national bestseller, Millionaire Milestones: Simple Steps To Seven Figures, “If the direction is correct, sooner or later you will get there.” Make sure you have the right resources to point you in the right direction.

Good luck on your financial journey. If you want to become a millionaire or multi-millionaire, my book will help you get there. You can pick up a copy on Amazon, which has the best sale.

For those of you who’ve reached these millionaire milestones, how did you feel after hitting each one? Which financial milestone had the most lasting impact on your lifestyle and happiness? I’d love to hear your story—what changed for you, and what did you do differently afterward?

Subscribe To Financial Samurai

Listen and subscribe to The Financial Samurai podcast on Apple or Spotify. I interview experts in their respective fields and discuss some of the most interesting topics on this site. Your shares, ratings, and reviews are appreciated.

To expedite your journey to financial freedom, join over 60,000 others and subscribe to the free Financial Samurai newsletter. Financial Samurai is among the largest independently-owned personal finance websites, established in 2009. Everything is written based on firsthand experience and expertise.

How You'll Feel Reaching Various Millionaire Milestones ($1-$20M) is a Financial Samurai original post. All rights reserved.

The biggest change at $10M is the.sense of how much portfolio gains overtake your earning.capacity. Simply increasing your portfolio return from 10% to 12% is equivalent to a good salary. Life becomes more about managing portfolio returns than worrying about W-2 employment (if you still have a job).

You’re absolutely right. See: When Investment Returns Overtake Active Income, Work No Longer Matters As Much

I’ll be writing a new post about this subject and how our investment returns help us buy back TIME soon.

I’m one of the exceedingly rare breed: W-2 deca-millionaire. No entrepreneurship, no IPOs, no inheritance, no leveraged bets – just a moderately high non-FAANG W-2 income and two decades of SPX & chill. It’s a low risk path to sustainable generational wealth.

Good stuff! How old are you? And when do you think you’ll eject the corporate life? Cheers

Late 50s. My advisor is telling me to hang it up and enjoy life before I get too old. I’m still feeling like I’m the most innovative person in my group so the place would come apart without me.

If you feel that importance and that innovation, then keep going. Once you’re out, it can be very tough mentally to handle.

See: The Negatives Of Early Retirement Nobody Likes Talking About

Thanks Sam, learned a lot from your site, it set me on the path to FI.

Current age-53, ~3.5M in assets besides home equity.

Plan on working in my current job until age 58 (another 4.5 yrs) and then would like to keep working if possible because I want to, but only with a different job arrangement if I can do that

Goal is to replace my salary which is ~200k, so I a shooting for 5-6M by age 58 with having all debts paid off by then.

I think the truly rich in this world make a million or millions per year USD, so I feel the entry point for that would be about 20M+

-Elliot

Maybe some others have mentioned this, but I was confused for a while in this article as to whether you were talking about X million in liquid assets or net worth. These are not the same, and the feeling you get reaching each milestone for each would be different depending on your situation. As I read further, you began saying net worth more often and that’s what I assumed this was attributed to. Anyway, an edit or two would’ve helped the reader a bit.

I like the idea of this article, however, I believe that only once you reach the 20 million mark, does everyone seem to fall into the same pattern for your suggested mentality. At that point you have so much that you are thinking multigenerational. Before that however, you may have different situations as another person with the same net worth. Health conditions, kids, divorce, business, obligations, etc. can really impact those on lower milestones.

You’re the first person to mention this, but I’m talking about net worth. Happy to clarify in the article and in this comment. You’ll feel similar feelings with these amounts in Investments as well.

Is what you’re saying how you felt once you achieved the $20 million net worth? If so, did you do anything to change how you feel and how you invest for the future? How long did it take you to get to a 20+ million dollar net worth and what are some of the things you did to get there?

I’d love to get some perspectives from as many readers as possible. Thanks.

I’m right with you, I was confused too, so I reread 3x time. It’s the even difference between an lottery winner with enormous of liquid assets a one time, contrary to an investor with big net worth with less liquid in bank. The feeling is totally different.

This is great feedback, thank you. I will try to simplify my writing more so it is more understandable to more people, including the French, which I assume you are based on your email address.

Can you share your net worth and age? I’d love to know more about how you don’t feel the same or how you feel much different with a $5 million net worth at $5 million in investment assets etc.

Most people I know with five, 10, and $20 million feel the same. And most people I know don’t spend more than 30% of their net worth on their primary residence. So what’s left over is still significant.

But having a nice primary residence also provides a great sense of satisfaction and security as well, which is correlated with net worth amount and how nice the house is. And of course, real estate also has the potential to appreciate and build more Wealth as well.

Thank you for this article !

Becoming rich requires ambition and hard work, but your social background… and also your country of birth and its intrasec opportunities also play a very important role.

Hitting your first million feels different from two, five, or ten — each changes how you see risk and opportunity. Watching $SCHD, $AAPL, $NVDA for steady growth into the next milestone.

This is an interesting topic and great ideas in the comments.

In mid 40’s, live in SoCal, $3.1 mil total invested NW: $2.3 million invested and a pension worth $800k. Sam, your blog is probably the only reason I’ve thought that $5 million is a worthwhile goal, however, I’m not sure it’ll change anything (I’ll be sure to confirm when we get there in the next few yrs). With expenses at $81k, and an eventually taking on a low primary hm mortgage, the drive to strive has begun to diminish.

Currently, $3.6mil invested NW (I say invested NW cause primary home equity doesn’t really do much) seems like Fat FIRE, cause it allows us to pay off the mortgage loan of the hm we inherit and divert all assets to vacation and charity.

Our CFP just asked us to spend $24k more on top of the $81k to have experiences while the kids are still young. This has really helped us begin to relax with spending and why I appreciate meeting with him every few years. Next year we will begin to withdraw from assets, but it’ll probably only 2%.

The lack of motivation to work is kinda a bummer. Might take time off for a month to see if there are more worthwhile ways to fill up the time.

In the end $3mil vs $5 mil depends on lots of things including spending and what you value.

I’m fascinated by someone worth 10M or 20M not feeling wealthy. Are they hanging out with nothing but billionaires? The only other explanation is a scarcity mindset. But I suppose that mindset got them to where they are. They need to now learn to spend! Once we hit $5M, there will definitely be a silly 150,000-200,000 car happening. I think staring at a Porsche or Lamborghini logo will help with the not feeling wealthy thing

Yes. For example, 50% of NVIDIA employees are worth $25 million or more. Which means you’re often bumping into colleagues worth $50 million or $100+ million.

My friend who joined Figma in 2019 is probably worth $30-$50 million. But the co-founders are worth $4-6 billion.

It’s all relative! Living in San Francisco, the competition is fierce and so is the wealth. Best to relocate to Honolulu instead.

And I put the odds of you blowing $200,000 on a car once you hit $5 million at less than 50%. When you know how long it took to get there and the risks involved, you might be more judicious with how you spend.

I can’t get myself to replace my 10-year old Range Rover Sport with a new one for about $120,000 out the door, despite having over $5 million in investable assets. Why? B/c I bought mine for $60,000 out the door and it still runs fine! $120K seems like an outrageous sum for a car that depreciates. I’d rather invest the $120,000 in the Fundrise Innovation fund that owns OpenAI, Anthropic, Anduril, Ramp, and Databricks for my children.

The opportunity cost not to invest in private AI companies today is too great when you have children to care for.

You’re right. I’ll probably keep it reasonable and just get a gently used $100,000 Porsche at that time. Meantime 2019 Audi A5 for another few years.

It’s not so much about not feeling wealthy. . .it’s more about not wanting to divert assets from generating returns and continuing to grow the pile. At what point is it OK to actually splurge on things that aren’t about the future but about the now?

Wife and I are both 38 with a 7 month old. We live in So Cal, just hit 3m NW earlier this year. I completely agree with you skipping it. I thought when we hit it, after setting out on this journey a decade ago, it would be a great feeling. It truly isn’t.

No debt besides mortgage debt, make combined 400-500k +/- 50-100k a year depending on bonus’ etc.

Childcare is expensive (we have a in home nanny 3 days a week and have some fantastic parents that each help a day a week, their choice, we don’t ask them)

You are spot on skipping 3m NW. 3m sounds like a lot, but it isn’t.

Where do we find ourselves with 3m NW?

500k in retirement accounts (401k)

150k in equity in a rental property

250k in private equity deals

1.6m+ in equity in our primary residence

550k in cash/treasuries (1/2 of this came from recent rental sales, we have yet to redeploy into other investments)

100k in other misc small investments (stock account etc)

Does this create financial freedom? Nope, not at all. We aggressively save, max out my wife’s 401k annually, contribute to mine as necessary to max out tax savings but her match is better, and live within our means.

After having 550k liquid, I’m realizing you need 2-3m in investable after tax assets to create true financial freedom, where you could explore a different career, open a consulting business, etc.

Key to freedom is creating that 100k+ of income that will allow change. My new goal is to work on an investment account, post tax to create that freedom. Tough part is being in a burnout business, with a baby, I’m trying to find that balance between time and money these days, where it use to be all about the $.

We reached $20m 10 years ago when we were in our early 50s but have chosen to continue to work. As immigrants, we suffer financial insecurity and felt the need to continue to work for as long as we possible could until corporate layoff. We are just two W-2 employees without any stock options but have been very frugal for the last 30+ years.

We live a simple life, still fly economy, drive a13 years old car. No fancy furniture, no luxury goods but just enjoy simple happy life.

I lost my job 3 years ago and my spouse still works and hope to retire next year.

Do we feel wealthy? Not really because money has not changed our life style.. However, it is good to feel free of any financial worries.

Congrats! What is it that you two do for work and what was the average income? How was most of the savings invested for those who want to follow your path?

Frankly, we have been very lucky! We are just two professionals working for private corporation (without any stock options) for about 30 years. Pay was ok then became great but we didn’t upgrade our life style. While i was also working, our combined income was over $1m+ annually in the last 10 years

We didn’t start investing until early 40s because we didn’t know much about investing and have had very demanding jobs working very long hours. I wish we had started investing much earlier!

We bought some rental properties between 2010 to 2019 and also invested money in US stock market.

$1+ million income is great! What is it that you two do? Not easy to get that income level.

Especially without stock compensation

I think I was the one the mentioned a while back in your comments that you should of worked a few more years, maybe even till 40 or even to see how high you could get.

You’d be over 20 million easy if you did, possibly more. I forgot the excuse you gave back. I remember the story you told of a female friend that made director and was having trouble finding a partner, having family etc.

I feel like both of you should of switched how your careers ended. She should of retired early to start family etc. (Since she is female). You should of tried to get as high as you could till 40.

Could’ve been good! Working until 40, or 5.5 more years would’ve been the more prudent move. But then, I might not have ever been able to start a family due to all the stress and work. And I would give up everything to have them.

What did you end up doing with your career and how’s your net worth now?

Other than moving to a bigger house and being able to pay cash for it, or perhaps upgrading our 6-yr old Nissan Rogue in a couple of years to a new Toyota Highlander I am not sure if I am willing to change anything when I reach 20M. Flying first class most likely will not be on our bucket list (although buying extra leg space could be an option). We are used to living a middle class lifestyle and adding few millions to our net worth will not change anything. The most important thing moving forward will be legacy and charitable work.

at $20 million, I think you could comfortably afford something much nicer than a Toyota Highlander, which is nice. It just doesn’t have that soul IMO.

It’s hard to pony up for first class tickets that are three times to eight times more expensive, given you still get there at the same time.

I don’t know about the average total net worth for middle class Americans. But in Canada, NW @$1 million is probably best or slightly less. And especially living in a home that is warm and doesn’t leak in a big Canadian city.

The problem is thinking $1 or $2 mill is fantastic –except in Vancouver and Toronto a home is shockingly high and even if one owns it, the asset is not liquid. Because one lives in that home. The smallest condo in Toronto is at least $600,000. A detached home @1+ million is very common in both cities.

Are you referring to brokerage accounts or overall net worth. My net worth is a little over $2m at 46yo but my investment accounts just hit $1m and living in Charleston Sc in an expensive neighborhood is still leaving me feeling poor.

Sam,

for purpose of discussion above, would you include home equity or 401k/ira accounts that either can’t generate income or inaccessible until later in life.

Absolutely for net worth calculations.

Hi Sam, Do you think in 15 years 20MM investable with no debt will still be a lot of money? Also, with this nest egg can someone still fly private and have a 2nd home?

Sure, it’ll still be a lot of money. If inflation runs at 3% a year for 15 years, the purchasing power of $20 million falls to about $12.9 million. Still pretty good. Is that what you are shooting for, $20 million? If so, how much do you have now and how old are you?

I’m 41 and currently have around 8.5MM investable no debt. I would like to retire at 55. You think 20MM is reasonable by 55?

I think so. 14 years is a lot of time to compound.

How much do you think i could spend a year starting at 55 and never touch my principal?

Depends on the composition of your net worth. Check out my personal finance consulting page (https://www.financialsamurai.com/career-personal-finance/ ) if you want to get into a deeper discussion and analysis. I’m doing a promotion now to celebrate the launch of Millionaire Milestones (https://www.financialsamurai.com/millionaire-milestones-book/).

How about 30MM in 15 years? What is the purchasing power?

Bro, ChatGPT. $19.25 million. Geez, pretty simple.

Very nice article Sam. Thanks

I am perhaps the poorest out here with barely 300k networth at age of 36 and about to loose my decent paying cybersecurity job but my only two dreams in life are one to achieve FIRE and two to create a company thats creates immense value to the world and become really big within next 7 years.

I had a poor childhood so I over realize the importance of money and never tend to overspend it. That said , i also realize the three tenets of life(Wealth , heath,Relation) needs to be balanced and money is not essential for happiness so i want to Atleast retire from job before 41 and work for self fulfillment and hapiness rather than money .

Hi Sam – first time commenter, long time reader. Wanted to say a big thank you. Coincidentally this post has aligned with our household hitting the $1M NW mark with us in our mid-30s. Granted it’s spread across different asset classes but your writing inspired me to save aggressively in order to get us here and has me motivated to go well beyond. I remember reading your writing back in 2012 and feeling like something unlocked in my head. Along the way I’ve been called cheap or worse by friends/people who spend everything and drive much nicer cars and live in bigger houses. But I’m feeling incredibly proud to be here, just as you described above, and your writing has me motivated to achieve even greater freedom. Thanks and keep up the great work – all the best to you and your family

Hi Scott – thank you so much for taking the time to comment and share your story. Huge congratulations on hitting the $1M net worth milestone in your mid-30s—that’s an incredible achievement and a reflection of your discipline and long-term vision.

I’m honored to have played a small role in your journey since 2012. It’s never easy going against the grain, especially when others don’t understand the delayed gratification mindset. But you’ve clearly proven the power of consistency, intentional living, and smart financial decisions.

Keep going! you’re building a powerful foundation for even more freedom and options in life. I have no doubt you’ll continue to surpass your goals. Wishing you and your family all the best, and thanks again for reading and sticking with me all these years! – Sam

P.S. I hope you pick up a copy of Millionaire Milestones. It will motivate and guide you to take action to make many more millions after that!

I don’t usually talk about investing outside of a very small circle in real life, but we had an interesting discussion last night. The topic was “when are you going to sell?”

Without even thinking, I blurted out “never.. it always goes up!”

Then the conversation shifted to “what amount is enough?” Are we just treating investing like a never-ending game, constantly chasing a higher and higher score?

It really made me reflect on why I was aiming for a specific net worth. That first million felt incredible because most of it came from what I saved. Delayed gratification. Discipline. And a lot of luck.

But now, most of the growth is driven by the market. I’ve contributed far less compared to the returns and while it’s great, it just feels more like a game than a meaningful goal.

I’m not exactly sure where I’m going with this, but I want to rethink what the magic number is and reassess it every year or so. Even though 2012 was 13 years ago, I think $3 million is still a good target.

The magic number is a moving target, which is part of the reason why it’s so hard to quit the money. $3 million is definitely a fantastic target to shoot for, especially if you wan to feel like a real millionaire.

Gotta love the stock market rebound going on right now!

Well said, Sam. I’ve just reached milestone #2, and you captured my thoughts perfectly. I definitely feel that I have options now. Even though I still have an extremely demanding job, I feel more free and relaxed knowing that I don’t have to continue if I don’t want to. However, I still get nervous about market downturns. Additionally, the dollar’s weakness has really hurt me since most of my investments are USD-based, but ultimately, I will need to exchange my dollars for Euros. Ideally, I would like to build a bit more of a cushion before retiring, as part-time work is not an option in my line of work. However, milestone #3 seems to be too far.

Finished reading Millionaire Milestones a few days ago. Highly recommend it for anyone inspired by this post!

I forget who said it originally, but “making my first million was the hardest” comes to mind. I completely agree for the reasons you laid out. To get to $1MM, you need to establish sound habits. Cementing a new habit for any pursuit, money, diet, exercise, etc. is not easy.

Once you hit $1MM, that likely means your habits are locked in. You just have to keep doing the same thing to get to $5MM and $10MM. You’ve already done the hardest part. You just need time.

Matt

I’m 59 and hit the $5 mark a couple of years ago when I sold my IT business to PE. I expect another liquidity event in abut 2 years through the equity I hold in the company that bought mine. I’m seriously ready to retire by the the end of the year – facing some burnout issues. We’re currently looking at legacy planning and purchasing 3 rental homes that we’ll eventually gift to our adult children. Just started reading Millionaire Milestones! Will be fun to hit the $10 stretch goal especially with no W2 income. lol

Right on Todd! Huge congratulations on hitting the $5 million mark and successfully selling your IT business—that’s no small feat! Sounds like you’re in a fantastic position heading into this next chapter, especially with another potential liquidity event on the horizon. Burnout is real, especially after years of grinding, so I totally get the urge to step back and enjoy the fruits of your labor.

Love the legacy planning strategy with the rental homes—such a smart way to build generational wealth while still maintaining flexibility and control. I’m honored you’re reading Millionaire Milestones and I hope it gives you some added motivation (and maybe a few laughs) on the path to $10M. Hitting that goal without a W-2 would be be fantastic. Enjoy the ride!

The funny thing is, with a several good years in the markets and economy, you could get to $10 million before you know it. The compounding effect is real and incredible once you have that nut!

When you’re done with the book, if you don’t mind leaving a review on Amazon or wherever you picked it up, I’d appreciate it. Every review counts and means a lot. Thanks, Sam

I will definitely provide a positive review once I’m done reading the the book (I already know it’ll be great!). I’ve followed FS for several years now and consider you a mentor (despite that fact that I’m older than you… lol!) a friend just recommended a podcast entitled “Founders” which I find utterly fascinating. Just listened to episode #384 called, “Ken Griffin: Founder of Citadel and Citadel Securities”. The story about Griffen is interesting to be sure, but the insight and lessons sprinkled into the podcast by David Senra are profound and absolutely golden. This will be required listening for my entire family as we embark on the next phase of growth.

To wait until a net worth of $10M to generously tip service workers is having an extreme scarcity mindset.

Thanks for sharing your sentiment. Yes, if you’re only tipping generously after reaching $10+ million, that may be concerning. But clearly plenty of people tip well before that net worth milestone too.

It also depends on what “generously” means. What does it mean to you?

To some, tipping 25% – 30% is generous, while to others, only tipping 50%+ is generous.

You may enjoy these relevant posts:

Keep Your Donation Amounts A Secret

The Importance Of Stealth Wealth For Happiness And Survival

A Tipping Guide To Counteract Tipflation And Feel Great Again

You never want to share your true income, wealth, or amounts of giving because you will always be judged. And often times, the people who judge you will have less or give less.

We can’t help but judge how other people spend their money. It’s just the human condition. The sooner folks can adopt a low-key, stealth attitude, the better.

I do 25% as the baseline tip for even just average service. 50%-100% would be the generous amount based on certain persons or circumstances. I started doing a lot more of it after crossing 1M several years back. At 10M, I’d probably go around tipping 50% each and every time! LOL

Sounds good to me! Thanks for sharing.

In the tipping article I wrote there are some people who just find tipping to be completely foreign into them. And it really is foreign in many cultures in Asia and Europe to not tip. So to each their own, I say!

Tipping culture in America is completely out of control. 25% for average service?

In Portugal, we offered a $5 euro tip (on an $85 bill) and in a discussion with our server, he kindly turned it down and explained that he appreciated the gesture but says he hopes the American tipping culture never comes to Portugal.

Mike what u dont understand is that servers in the U.S. make 100% of their income from tips. Their hourly pay is literally 2.15/hr and goes all 2 taxes. This is not true in Europe as laws are different.

This depends on the state. Most restaurants don’t pay the federal minimum wage either.

This is just excellent! You nailed all the feelings with welcome words of caution. Thanks again!

$1M is a nice start. $3M…most people can retire happily. $5M….you can retire a couple of decades early. From personal experience.

Only in the midwest. That aint enough in SF, NYC, or Hawaii.

This is cringe worthy to read. At $10 mil you suggest upgrading to economy plus? LMAO. My net worth is less than $10k and I fly business only. Once I have $100k I’ll quit my job and never look back. Moving somewhere to south east Asia where I can live off $1000 a month comfortably. All I need is to generate 1% return a month and I’ll be sorted.

Love it! You’re clearly playing chess while the rest of us are stuck on checkers.

Business class with less than $10K net worth is some real big baller energy—I salute you. And if you can consistently generate 1% a month, forget retiring in Southeast Asia… you should be running your own hedge fund out of Bali with coconut wi-fi and a staff of ex-Wall St. interns.

I see First Class in your near future.