The marriage penalty tax is discrimination. But given the marriage penalty tax doesn't hit everybody, there hasn't been enough uproar to make it go away. Thankfully, the marriage penalty tax has been abolished for 98% of households.

In the past, I used to wonder why two individuals with high incomes or two individuals with a large income differences would ever want to get legally married. Paying thousands of dollars in marriage penalty taxes didn't make sense. It seemed obvious that the government wanted one spouse to give up his or her career to stay at home, even if there were no children to raise.

Otherwise, before the Tax Cuts And Jobs Act Was passed in 2017, why would the top tax rate of 39.6% for a married couple not kick in starting at a combined income of $836,802+? Back in 2017, married folks began paying the 39.6% tax rate once their combined income surpassed only $470,701.

In the eyes of the government, 1 + 1 literally only equaled 1.12. This is blatant anti-marriage discrimination. Discrimination is not OK even if you aren't being discriminated against.

Marriage Penalty Tax Income Threshold 2024

For 2024, the marriage penalty tax income threshold starts from $731,201. In other words, couple's with a combined income of $731,201 or more will save on taxes if they stay single.

Below are the 2024 federal marginal income tax brackets. Notice how income thresholds are double until you get to the 35% tax bracket. Look at the 35% rate on $609,350 for singles. It doesn't double to $1,218,700 in the married filers column. Instead, the 35% married income threshold only goes up to $731,200. Married couples making $731,201 or more have to pay the 37% tax bracket.

Example #1: Marriage Penalty

Below are historical examples that demonstrate the marriage penalty tax that used to occur under the old tax structure. I used the Tax Policy Center Calculator. The point of these examples is to give you an idea of when the marriage penalty tax would kick in under various permutations.

For 2025, you can add about 20% to all the example numbers below.

In example #1, each person makes $200,000. They don't own a home, and have two children. The results are the same if they have no children. They pay a whopping $15,162 marriage penalty tax.

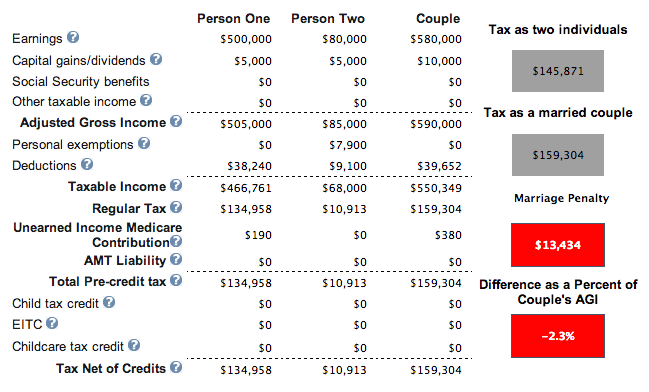

Example #2: Marriage Penalty

One person makes $500,000, the other person makes $80,000. They own a home with a mortgage and have one child. Lucky for the person making $80,000 to marry the person making $500,000. Not so lucky financially for the $500,000 income earner.

After 20 years, this person will have paid $270,000 more in taxes than if they stayed single or unmarried. Marriage forced this person to pay an average of $13,434 more in taxes a year. Think about what this couple can do with all this money!

Example #3: Marriage Tax Credit

One person makes $60,000, the other person makes $40,000. There is no mortgage and zero kids. We have a winner! Because the combined income is under $110,000, the couple can have a kid and claim $1,000 per child to lower their taxes even further to $10,638 from $11,638.

Example #4: Marriage Tax Credit

Here is the real humdinger. One person makes $300,000 and marries another who makes $0. They pay $35,000 in State taxes, $25,000 in mortgage interest, $2,000 in charity and have a child. The $300,000 a year earner saves $11,162 a year in taxes. I tried higher than $300,000 a year and the marriage tax credit starts to decline.

Based on the above historical examples, from a tax perspective couples should only get married if their partner made a similar level of income up to around $100,000 a year or if one spouse had zero income. If both made much more than $100,000 a year, they would pay a marriage penalty tax. How much would depend on the number of kids and deductions. Given most $100,000+ a year jobs are located in high cost of living cities where housing, education, and taxes are already high, paying a marriage penalty tax was infuriating.

Related: Scraping By On $500,000 A Year: Why It's So Hard To Escape The Rat Race

There's Hardly Any Marriage Tax Penalty Anymore

Fortunately, with the passage of the Tax Cuts And Jobs Act, the marriage penalty tax is now practically abolished. Based on the new federal income tax brackets below, there is tax EQUALITY up until $365,600 per person.

In other words, two individuals who make $365,600 and get married for a combined income of $731,201 will pay roughly the same amount of tax (35% marginal tax rate) as if they were single. Not bad given that in the past, they would have had to pay a 39.6% rate on any income above $470,701.

There are many income permutations to consider when calculating whether or not there is a marriage penalty tax or bonus. However, the key math to consider is at the 10%, 12%, 22%, 24%, and 32% tax brackets. There is a logical doubling of income thresholds if individuals get married. It's within the 35% tax bracket that a marriage penalty can occur.

Thankfully, I no longer have to spend hours to figure out when tax penalties start hitting. I can just tell based on looking at the marginal tax rate table. Perhaps this is why the tax industry is so afraid of streamlining the tax system. When things are easier to understand, they lose business.

Almost Everyone Should Rejoice

We know that the top 1% income earner makes roughly $650,000 a year. So, it's safe to say that less than 1% of Americans will still pay a marriage penalty tax. Therefore, you shouldn't have to worry about how getting married will affect your taxes. If the marriage penalty tax ever gets reinstated, you can always get a divorce on paper but stay together.

The only clear financial benefit I see for getting married is Social Security survivor benefits. Under current law, if your spouse dies, you get to keep all the accrued benefits. If you are not legally married, the government gets to keep all the taxes you've paid into the system if you have no children. Talk about a bad deal for the American people.

The Ideal Taxable Income For A Married Couple In 2024: $383,900

Since everyone believes in equality, everybody should be rejoicing at our new federal income tax rates. I personally believe that a married couple earning up to $383,900 after deductions for 2024 is the ideal income for maximum happiness.

You're paying a 24% federal marginal income tax rate, a reasonable rate. At $383,900 you can live a comfortable life anywhere in our great country. There's really no need to slave away to try and make more. Today, $383,900 provides for a healthy middle-class lifestyle in an expensive city. If you live in the Sunbelt, Midwest, or an 18-hour city, $383,900 should provide for a rich life.

Before you get married, run your combined incomes through a marriage penalty tax calculator. See whether it's worth it from a financial perspective or not. If the tax rates are not in your favor, you can still have a ceremony and just choose not to sign an official marriage license. Talk through the options with your partner and decide what makes the most sense.

Here's a budget I created based off a married gross household income of $458,100 and the ideal taxable income of $383,900 to pay a maximum 24% federal marginal income tax rate. If both my wife and I were working full-time jobs, a combined gross income of $458,100 is what we'd shoot for.

Marriage Penalty Tax Threshold Begins At $731,201 For 2024

Notice how $383,900 is exactly double the single filer threshold for paying the 24% federal marginal income tax rate. In fact, every income threshold is double for the same tax rate for married filers except for the 35% and 37% federal marginal income tax rates.

In other words, there is no marriage penalty tax for two singles who individually earn up to $365,600 in taxable income, get married, and file as a married couple.

Single filers who earn between $243,725 – $609,350 pay a 35% federal marginal income tax rate. However, married filers that earn between $487,450 – $731,200 also pay a 35% rate.

In other words, the government doesn't believe in equality between spouses after each earns more than $365,600 ($731,201). If the government did, the income range for married filers at the 35% rate would be $487,450 – $1,218,700, or exactly double the single filers income range threshold.

How Not To Pay The Marriage Penalty Tax

If you don't want to pay a marriage penalty tax, then limit your earnings to a combined taxable income of $731,201 or less. You'll still be paying an onerous 32% marginal federal income tax rate on earnings between $383,900 – $487,450 and 35% marginal federal income tax rate between $487,451 to $731,201. However, at least you will be treated fairly by the government.

Alternatively, if your combined taxable income is greater than $731,201 and are still single, don't get legally married. Over a thirty-year period, you may end up saving tens or hundreds of thousands of dollars in taxes.

Finally, if your combined taxable income is looking to surpass a taxable income of $731,201 in 2024, one spouse can make less or even retire early. For example, one spouse could earn the entire $731,201 while the other spouse earns $0 to keep their federal marginal income tax rate at 35%.

You can play with this marriage tax calculator by the Tax Policy Center.

Recommendations

1) Negotiate a severance package. When it's time for you to live the good life and pay less taxes, negotiate a severance instead of quitting your job. Pick up a copy of How To Engineer Your Layoff to learn how. It's been updated again for the post-pandemic work environment.

Use the code “saveten” at checkout to save $10.

2) Invest in private growth companies. Invest in private growth companies in the artificial intelligence space, check out Fundrise Venture. It's an open-ended venture capital fund that invests in AI, proptech, fintech, and more. IT holds leading AI names such as OpenAI, Anthropic, Databricks, and Canvas.

What's unique is that you can analyze the fund's investments first before making an investment. And the entry point to invest with Fundrise is only a $10 minimum. In contrast, traditional venture capital funds typically require $150,000+ minimums and you must commit capital before knowing what the funds will be invested in.

In 20 years, I don't want my children asking me why I didn't invest in AI near the beginning of the revolution!

Manage Your Wealth Wisely

Sign up for Empower the web’s #1 free wealth management tool to get a better handle on your finances. Run your investments through their award-winning Investment Checkup tool to see exactly how much you are paying in fees. I was paying $1,700 a year in fees I had no idea I was paying.

After you link all your accounts, use their Retirement Planning calculator. It pulls your real data to give you as pure an estimation of your financial future as possible. Achieving financial freedom is worth it!

If you have over $100,000 in investable assets—whether in savings, taxable accounts, 401(k)s, or IRAs—you can get a free financial check-up from an Empower financial professional by signing up here. It’s a no-obligation way to have a seasoned expert, who builds and analyzes portfolios for a living, review your finances.

A fresh set of eyes could uncover hidden fees, inefficient allocations, or opportunities to optimize—giving you greater clarity and confidence in your financial plan.

Subscribe To Financial Samurai

The Marriage Penalty Tax Has Been Abolished is a Financial Samurai original post. Join 60,000+ others and sign up for my free newsletter for more financial insights. I’ve been writing about financial independence since 2009.

Note: I'm not a tax professional, only a tax enthusiast. Consult a tax professional before making any tax decisions. If you see something wrong with the numbers, feel free to point it out and I'll correct it.

Hi,

I am in a situation where couple both are remote working but primary residence in CA and with 2 kids. Is it make sense to married file separately for a couple where one makes below $150k and other makes $400k? High earner spouse shows residence in no state tax to avoid state tax?

Looking forward for some basic guidance. Thanks in advance!

How about if I’m making 78,000 and my finance is making $650,000?

Sam,

I was wondering if the SALT deduction capping at 10k includes Sales tax too or if that is a separate deduction all together? Thanks!

One of my favorite topics, thank you for addressing!

I remarried a couple of years ago and we chose to not legalize our union specifically because of the marriage penalty. I learned the first time around.

We weighed our marriage penalty (~$30k/yr) vs the economies of scale of shared health insurance ($3500/yr) & gym membership ($2k) and calculated we could come out $25k/yr ahead by not legalizing our marriage. $25k/yr after-tax money!

The new changes do help some as you note but taxing 100% of my husbands income at 37% (vs 24.85%), removing his $10k salt etc is still a $25k+/annual tax penalty for us.

Never the less, we were UP financially in 2017 by not making our marriage legal and will be up in 2018 and we are happy as clams to have a “private marriage”. It’s interesting however that despite how happy we are personally (and satisfied with our legal dodging of the marriage penalty) some people we know question the strength of our marriage because it isn’t legal.

Unfortunately, our culture can’t yet seem to effectively separate a private/religious/personal matter with the legal/tax system. And our tax system cant seem to keep it’s judgments (benefiting the primary wage earner type family) out of our personal lives.

Social/cultural acceptance of the privatization of marriage in the US would go a long way to giving tax payers more choice over their financial and tax situation.

Why is his income taxed so much higher than before now?

In 2017, 100% of his income would have 39.6% plus state of 9.9% because my income would put all of his income at my highest marginal rate. This is in contrast to the ~27%ish federal he would pay as single HoH- he earns about $200k.

In 2018 100% of his income would be at 37% as opposed to an est of ~25%. In both instances he would also lose HoH status (we own 3 residences and each have children), his child tax credit, and my ability to consider our 3rd residence where we support grandma a “2nd home”. We both itemize.

2018 limitation of SALT in our high SALT state causes further insult to the marriage tax rate.

I had our CPA run the numbers for 2016 and 2017 so I’m confident in what would be our personal net marriage penalty. I think the tax foundation calculator underestimates the marriage penalty but I’m not sure exactly how.

Ok. Not sure how 100% or his income could be at 39.6% or 37% since that’s the highest marginal income tax rate, but if you or your CPA say so, then that’s all that matters since you’re filing your returns.

You know what, you are right, I was totally wrong on the 2018 scenario and using 2017 assumptions. Look at me, jumping on my soap box before I looked close enough at the 2018 table.

Last year for a married couple, 100% of income over $470,700 was taxed at 39.6%. There wasn’t much of a difference in total taxes paid between married vs. head of household up to $470k. So if one spouse already pushed past $471k, 100% of the 2nd spouses income was taxed at 39.6%. I was placing that assumption on 2018.

You are right, the tables impacting the penalty are really different in 2018! Wow. Different game. We’ll have to have our CPA run it again for 2018.

You fail to factor in how higher income families got screwed. I would posit that most higher income dual earning families live in higher tax states on the cost. With the recent changes to the tax regulations, we lose the deduction for state income tax and the majority of the deduction for the property tax. So, our AGI will be higher, pushing us into brackets that will make the changes essentially a wash.

Check out: Why I’m Investing In The Heartland Of America

The heartland is not necessarily low tax. We are high income in KS and pay over 6% income tax. We also pay very high property tax. So now we are looking to leave the Midwest.

“ I personally believe that a married couple earning up to $315,000 after deductions is the ideal income for maximum happiness” – Samurai

Oh… being in the top <5% of households in one of the wealthiest countries in the world is ideal?!?

I don’t really see how a tax break for the wealthy is such a good thing, especially with the fiscal situation… the wealthy already get a disproportionate amount of special tax breaks (e.g. retirement accounts, lower taxes on capital gains, capital gains exemptions with the sale of a home, caps on inheritance).

You mention several times that you want the government out of deciding people’s lives…do you want to lose all of the tax advantages you have used to accumulate wealth in favor of a flat tax?

Yes, up to $315,000 for a couple is ideal, depending on where you live. What is your ideal couple income figure?

Are retirement accounts like the 401k only available to the wealthy? I’m not sure companies with 401(k)s can discriminate that way, same with the house sale proceeds Etc.

If you have been discriminated against with these things, I would definitely bring it up. Always got to fight for equality.

One of the reasons we married back in the day, in spite of the marriage penalty, is because there were no “but we’re in looooove” green cards.

Rights and responsibilities often balance each other out. One of my frustrations is hearing people talk only of the rights that go along with being married without also discussing the responsibilities. If the marriage penalty has really been eliminated, should we also eliminate spousal social security benefits?

I think the correction to the marriage penalty is good. I also think the $10K maximum for Property Tax is a step in the right direction and it should be further reduced over time to a $0 deduction. In fact, I am in favor of simplifying the code and get the Federal Government out of the “deduction business” and tax income without all deductions which are based on peoples’ choices. So, remove the personal deductions based on number of dependents (personal choice), remove the deduction for charity (personal choice), remove the deduction for sales tax (personal choice available to those in states with no state income tax), remove the state income tax deductions (personal spending choice), etc. etc.

Taxes are created to influence our choices. Everything is a choice. If you drive a car, you pay gas tax. Unless you’re talking about specifically deductions? IA that simplification of tax code. What about education deductions? Is education a choice in today’s world?

Yes, taxes have been created to influence the choices but I was just talking about income taxes and the simplification of that code. I feel if the name is “income tax”, then it should just be on “income”.

As far as education, the type of education is a choice and should not be in the income tax discussion. Too many people assume they need 4, 6 and 8 year higher education degrees in fields that are not in demand and when they get out of school, they are in deep debt and can’t find a job in their field that pays well. There are many skilled trade/technical/vocational careers that pay well with less full time educational requirements.

well said. i support the “choice” thought process above.

We are still better off not marrying, financially. SALT is one reason. 2. My itemized deductions were $24,000 last year so now the two of us together get my itemized deduction and his standard, so that’s 32% of $12,000. 3. This isn’t directly connected but the Administration’s FY19 budget would change the student loan income based repayment program so that you can no longer choose married filing separately and only count the borrower’s income. If I’m grandfathered in, I’m in the clear but some college aged readers wouldn’t be. If we could commit 15% of his income to pay my loans, that would be nice for me, but we can’t for a few reasons. Plus, in some marriages, people keep their finances and obligations separate and that’s okay.

Would I say no if he really wanted to get married tomorrow? No, I wouldn’t because I do love him, we have a son, and I’m somewhat traditional, but it’s certainly a reason I’m happy with the status quo now.

Thanks for sharing your example. I hope you put that marriage penalty tax savings to good use!

I think you’d like this post: Financial DEpendence Is The Worst

Also, it can be interesting to compare on how it is in other countries.

For example in France, people prefer to avoid the marriage and go for a pacs which gives more tax advantage and less hassle than a marriage.

This is such great news! I got married last year 2017 and currently doing my taxes. I was so mad to find out I got hit with the marriage penalty tax. At least its only for 1 year…. I did get hit pretty hard with the 10K property tax limit.

I am SO glad that you pointed this out! I completely agree with you that this been completely overlooked by the media. I just got married last year and we are most similar to Example #1. For 2017, we will be paying ~$20k extra to the government for the privilege of having a piece of paper with our names on it. Had the tax change been announced earlier, we probably would’ve delayed getting married until 2018.

In other countries like Canada, taxes are paid individually. The tax bracket doesn’t change based on your marital status. I’m glad the US is finally modernizing its tax code (with respect to marriage).

It’s great to see things have pretty much equalized in terms of taxes due for married folks versus single filers. Hopefully the tax rules will maintain this going forward. They needed to be adjusted forever. Your line about getting a divorce if the old rules ever get reinforced made me laugh. It’ll be interesting to see how much tax laws change in the second half of our lives. I sure didn’t care or know much about taxes when I was younger but now I do my best to keep up with the big changes to minimize how much I owe every year.

There is one marriage tax penalty that hits married homeowners very hard: SALT deductions. If you are single, you can deduct up to $10k in SALT. If you are married, you can still only deduct up to $10k in SALT. This really hurts married homeowners who live on the coasts, especially when those areas already have high state income taxes.

True, but who’s fault is that? Fed doesn’t make some states have high state taxes.

Honestly, it’s “generous” that the Fed cares at all how much you pay in state taxes. Logically, it doesn’t make any sense for there to even be a deduction. Why should Fed get less money because a state decides it wants more? Or vice versa in an alternate universe.

Great comment. I am tired of media portraying Federal Gov’t as some sort of Pariah for restricting a “Loophole” that favors intrusive progressive liberal, inefficient coastal state gov’ts a free pass to continue excessive anti-American tax and spend policies. It should have been eliminated, not just restricted.

I live in the corrupt state of Oregon. OR hates it’s working citizens and puts them below everything else. This state is looking to make healthcare a “right,” cares more about salmon and trees than citizens and makes me pay for abortions for all, including illegal aliens.

If changing federal tax code can put some pressure on these insane hard blue states than electing Trump was awesome. MAGA!!

Coastal states (in general) incur greater costs to keep government working. People on top of people is always expensive to manage.

Is it excessive? Perhaps.

Hard to imagine people revolting and fleeing major metropolitan areas with whole foods and local fast casual dining at every corner for rural america but maybe Amazon and others can even the playing field a little.

Personally – I’d love to recede from coast if I could still get my gourmet food delivered and get my kids into good schools.

I think it’s great that their is tax equality for married couples for the ones that make $300K each, always nice to have equality in any level.

In terms of getting married or not based on the tax penalty, I don’t think it’s a huge factor since other ones like personality and be compatible are probably more important.

There are still marriage penalties on deductions for IRAs and eligibility for contributing to a Roth IRA.

I believe most of the other deductions phase out at levels that do not double for couples. So the marriage tax lives on in the phase out limits. But I agree it is much better than it was. Still need to get rid of amt though.

“Discrimination” is really not a useful lens to look at this through. Coming up with uniform tax rules that make people pay their fair share without inflicting undue hardship on too many people is difficult. Different people are situated differently and the tax code necessarily “discriminates” (i.e., applies different rules to different situations) in some respects. It’s unavoidable, even when the goal isn’t to do social engineering about the “best” kind of living arrangements.

The old system implicitly subsidized families on a model that was more socially normative half a century ago, one primary breadwinner (usually dad) married to a spouse who’s either not in paid employment or in lower-paid employment (usually mom). Really not that different from allowing a dependent exemption for a non-disabled, non-working spouse, like the tax code does for children.

Conversely, the old system tended to push one half of dual-income power couples out of the workforce. “Sure, you’re a doctor, honey, but I’m making $500K a year at my law firm, so the taxes on your $100K salary are at the top marginal rate from dollar one, then we need childcare, you need a work wardrobe, you have to commute to work, and when you get right down to it, on an hourly basis, you’d basically be working for less than minimum wage in a high-stress profession, so why not just stay home with the kids, do volunteer work and pursue your hobbies?” (The status rewards to Doctor Mom staying home with young children have changed a lot in the last half-century — absolutely obviously the right thing for any decent mother to do in 1960, a very low-status thing for a woman with an MD to do today, because shouldn’t she at least put all that knowledge to work, even part-time? Some people think that’s a good thing, others don’t, YMMV.)

The new system still shafts that doctor-lawyer power couple due to the top bracket ending for singles at $500K and marrieds at $600K, but the “discriminatory” judgment there is that couples who are making that kind of coin can afford the tax hit. It also creates new incentives around the margins for married couples at lower income levels to have both spouses working, because the tax “roof” before their combined income puts them into a higher marginal rate bracket jumps up higher, which effectively means the second working spouse’s after-tax wages are higher. In that sense, the new system “discriminates” against one-income families and subsidizes (“discriminates” in favor of) two-income families. Subject of course to Sam’s very correct disclaimer that it’s complicated, and incentives work at the margins rather than in every case.

One can spin all kinds of tales of moralizing resentment about how the old system “punished women who work” or the new one “pushes women out of the home” or it’s “discrimination” against somebody. Treating what is unequal as if equal is bad, treating what is equal as if unequal is bad, the problem is you’re never going to get agreement on what’s equal and what’s not.

I think it’s great that the marriage tax has been remedied. Now we should actually take it a step further and offer a increasing scale of credits based on years married. At the end of your podcast, you asked if we want the gov’t getting involved in our personal lives. I think it’s inevitable that they do and will continue to do so. I think it’d be better for the gov’t to encourage citizens to get married and stay married …. and have children (as they already do with the child tax credit). The more robust our natural growth rate and the more financially stable and strong American family units are, the better our economy will be. I think there’s lots of other benefits to local communities and society at large from this too.

Sam,

I think it was in one of your email newsletters that you mentioned you seeing the stock market continuing to go up this year because the only thing that had changed at that moment was a higher bond yield. It looks like you were right since the market is soaring from a week ago. When I saw the stock declines, I didn’t think they would stay down for long either but my reasoning was based on the tax cuts that the middle class received. Most people saw their paychecks go up by 3%-4% which means more money in their pockets for spending. A single middle income earner would have anywhere from $117-$467 more per month for spending. As I learned from my college economics class, it’s consumerism that keeps the economy healthy!

Too early to tell whether I’m right or wrong. But over the long term, I hope I’m right.

Hopefully American laborers really are seeing a difference in their paychecks now with tax cuts. The Michigan consumer confidence index surged to 99, from expectations of around 95-96 for February. Not bad!

I’m not sure I agree with you that a couple making $315,000 a year is the ideal income for maximum happiness. Why would you be less happy if you made more than that? Say you make $500,000 instead. You’re only going to pay an extra 3% on $100,000.

Are you saying that you’re less happy paying higher marginal taxes? It’s not like your entire income would be taxed at the higher bracket. You would have more disposable income with a higher salary even if you are paying a little more in taxes.

Jeff, I think the rationale Sam is using is the point of diminishing returns. He is not saying you will be LESS happy if you make more than 315K after deductions; he is saying you just won’t be that much MORE happy by making more because, on average, most of what you would want can be acquired at the 315K income level living in most parts of the country. Sam’s conjecture, the amount of additional happiness you acquire does not correspond 1:1 with the rising level of income beyond this point.

My understanding is the penalty is also still in full effect for AMT.

I want to guess the reason for the penalty was the belief that shared costs are reduced across two people and that people who share costs would ultimately get married. Not saying I agree.

But as I understand, far fewer of us will be paying AMT under the new law. I did a quick check, and about 60% of filers in the $200k-$500k range (ie. my household) pay AMT. I couldn’t find new numbers, but everything predicts it’s going to be much lower.

The major reason for AMT was state and local income/property taxes. Since that deduction is capped at $10,000 far far FAR fewer people will be subject to the bite.

Good Morning Sam,

If you stay single and file separately you both get the 10,000 deduction cap for s.a.l.t. Married filing joint or separate can only deduct 10,000 or 5000 I believe so there is still somewhat of a penalty correct?

Correct. It’s stupid that a married couple doesn’t get $10,000 X 2 = $20,000 of SALT deduction. Not sure what the government’s logic is on this one. Perhaps the logic is now that the marriage penalty tax is abolished, the benefits outweigh the benefits of doubling SALT. Losing $10,000 of SALT deduction is $2,400 for a 24% tax bracket couple, but the income tax savings is greater.

Is there still the marriage tax related to the 0.9% extra medicare tax (single pay over $200k income and married over $250k) or was that modified with the new tax plan?

Completely agree on the 315k maximum hallow was figure. We are switching to a Roth 401k to pull as much income into the 24% bracket as possible.

It wasn’t about logic, it was about a compromise. Remember, the original plan was to get rid of the SALT deduction entirely, because it doesn’t actually make sense for federal revenues to go up or down based on what states decide to do with their taxes. CA deciding they need more money shouldn’t mean the government gets less.

Also it raises more money for the federal government, so I’m sure there were dual incentives to kill it :) How much each reason played in the decision is subjective, but I’d believe the wonks in the GOP were thinking of the former, and the classic politicians were thinking of the latter

Good point about compromise. With a nation divided, compromise is the only way to get things done.

Thoughtful response. We fall into bucket 1. I’m not happy one of us loses our SALT but at least net/net the marriage tax is reduced. Our SALT impact is mainly a loss of deducting state property taxes where we have a home value comfortably above the average. I rationalize it as a luxury penalty and I’m OK with that considering the convenience we derive from the location for both of us to work in very good jobs.

The government got this one right in my book.

Thanks for the analysis, Sam. I don’t remember seeing this highlighted in the media, which is surprising, given I would think the marriage penalty would have been seen by the public as unpopular. Biased media?

This is a big deal to me. We fall somewhere near example 1, and while I knew the penalty was probably large, I don’t think I knew it was quite that large.

More important than just the dollar impact, the whole idea of the penalty is, to me, massively unfair. Much has been written about the societal benefits of marriage (especially on children), and yet you throw a stiff penalty at people for playing by the rules and making responsible choices?

This wouldn’t be highlighted in the media (at least for positive reasons) because look at the numbers used in this post… e.g., two couples making over $200K each. The majority of this country WANTS this exact couple to may more in taxes, not less. Highlighting these examples would garner less support for the tax bill than it already did for ‘helping the rich’.

Yes, I’m in the camp that the government should treat people equally, change their old ways of thinking about how one spouse should always stay at home, and get out of the business of deciding what individuals should and should not do with their lives.

I don’t know why the mass media and more people aren’t talking about the marriage penalty tax abolishment. This is GREAT for equality. Perhaps nobody has come to this logical conclusion about what the new 2018 federal income tax brackets mean? Is it possible folks can’t think in derivatives except me? Doubtful, but maybe! It is Valentine’s week after all.

If one spouse makes 300k and the other only makes 30k, the one who makes 30k is still taxed at the 300k rate…..so why are you saying the “penalty” is gone?

Unless I’m messing up the math, this is the type of couple who would really benefit. The single person earning 300K is taxed at 35% on taxable income from 200K to 300K. When they get married, 200K – 315K is only taxed at 24% and the final 15K is taxed at 32%.

I pay a marriage tax but it’s mostly because I would qualify as a head of household (higher standard deduction/tax bracket threshold than single) and get the full dependent credits.