I made a mistake with both my children's 529 plans in 2017 and 2020, when they were each born. Instead of investing in equity index ETFs or funds in the S&P 500, I invested in target date funds (TDF). Both target date funds have significantly underperformed, costing my children $40,000+ of lost profits in just a few short years. Instead, I should have invested the 529 plans in an S&P 500 index fund. If I had, their balances would be much higher today.

A target date fund – also known as a lifecycle, dynamic-risk or age-based fund – is often a mutual fund designed to provide a simple investment solution through a portfolio whose asset allocation mix becomes more conservative as the target date approaches. The target date is usually retirement, but can be for any upcoming expenses such as college tuition.

Target-date funds offer a lifelong managed investment strategy that should remain appropriate to an investor's risk profile even if left unreviewed. The strategic asset allocation model over time is known as the glidepath.

Let me share why investing in target-date funds in a 529 plan or retirement plan may not be the optimal move. I'll share why I made the mistake and what I plan to do about it.

Superfunding With A Target Date Fund

When our son was born in April 2017, I decided to superfund his 529 plan by the end of that year. In retrospect, I should have opened up his 529 plan in 2016 and then changed beneficiaries when he was born. However, better late than never.

By mid-2018, my wife also superfunded our son's 529 plan. We had now contributed $150,000 between us and couldn't contribute more for the next five years. As first-time parents, we wanted to get the college savings aspect out of the way so we could focus on being good parents.

Since 2017, my dear mother also generously contributed $66,500 to our son's 529 plan as well. With a total of $206,500 in contributions through 2021, you would think the 529 balance would be well over $300,000. After all, the S&P 500 is up about 70% since mid-2018.

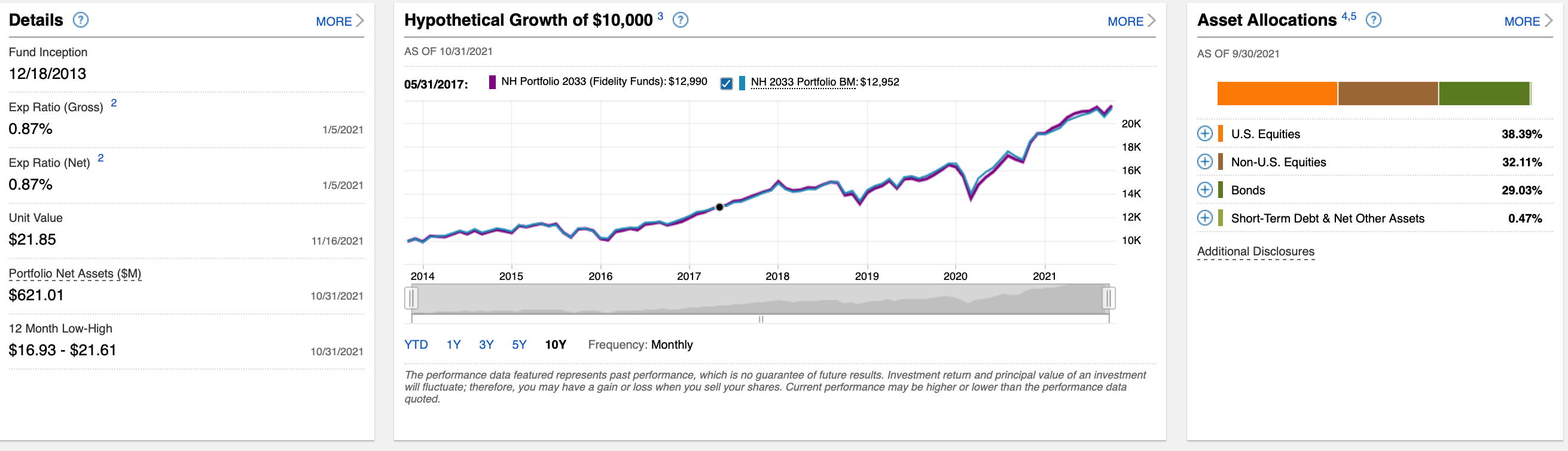

Unfortunately, that's not the case. Due to investing in a target date fund instead of a S&P 500 ETF, our son's balance was only $299,640.29 through October 2021. The dark line below shows the balance. The light blue line shows the contributions since July 2017. The difference is the profit, which stood at $93,140.29.

If I had invested in an S&P 500 index ETF instead, our son's 529 balance would be about $30,000 higher to ~$330,000. $30,000 could easily pay for one year of public university tuition. Damn.

Target Date Fund Severely Underperforms In A Bull Market

Below are the returns by period. The fund's 3-year return is only 14.55% versus a 21.48% 3-year return for the S&P 500. What's worse is that the YTD performance through October 2021 was only 10.85% versus 24.04% for the S&P 500 index.

Of course, target-date funds should underperform the S&P 500 in an equity bull market. After all, a TDF is a mix between equity and fixed income. To be fair, target-date funds should be compared to more balanced funds, such as 60/40 funds. However, I did not anticipate such tremendous underperformance so early on.

The NH Portfolio 2033 TDF I invested in has roughly a 30% weighting in bonds, 38% weighting in U.S. equities, and a 32% weighting in non-U.S. equities. The bonds and non-U.S. equities have really dragged down the performance.

I'm not sure what non-U.S. equities the fund invested in, but the U.S. has been one of the best-performing countries in the world since the pandemic began.

What Else Went Wrong? Being Too Conservative To Start

In 2017, when I was deciding between target-date funds in the 529 plan, Fidelity suggested I invest in the NH Portfolio 2035 fund. 2035 is the year our son turns 18 and potentially goes to college.

However, back in 2017, the real estate market and the stock market were feeling frothy. I was also in protection mode as a new father. I traded in my Honda Fit for a safer SUV, sold my main rental property to buy back more time, and became slightly more conservative with my equity weighting. Instead of taking more risk, I focused more on capital preservation after a nice recovery since 2009.

As a result, I invested in the NH Portfolio 2033 fund, which assumed our son would go to college in 2033. As a result, the fund had a greater weighting in bonds than the 2055 fund. The difference in percentage points was ten percentage points if I recall correctly, e.g. 80/20 vs. 90/10 to start.

S&P 500 Historical Returns

It turns out, being conservative paid off in 2018. The S&P 500 finally had a down year, -4.38% after the following huge years:

2009: +26.46%

2010: +15.06%

2011: +2.11%

2012: +16%

2013: +32.39%

2014: +13.69%

2015: +1.38%

2016: +11.96%

2017: +21.83%

2018: -6.24%

Put yourself in my shoes. Would you have dared invest $75,000 after such a long winning streak? Further, 2017 was one of the hottest years for the stock market. It felt risky to dump $75,000 in July 2017, so I didn't.

Instead, I contributed $15,000 to start and then just kept on contributing more as the year went on. In the end, I decided that since I had an 18-year investing time horizon, I might as well superfund.

To feel better about investing so much after such a large run, I was more conservative with my asset allocation. It was a fair compromise at the time.

Did Not Adapt After 2018's Decline

After a disappointing 2018, I decided to leave the funds in the NH Portfolio 2033 TDF. My wife was in the process of superfunding in 2018, which felt appropriate. Our decision was for me to superfund in 2017 and for her to space out the contributions to hedge against a market downturn.

In retrospect, if we had a crystal ball, we would have invested 100% in an S&P 500 index at the end of 2018. Here's what happened in the S&P 500 after:

2019: +31.49%

2020: +18.4%

2021: +25%+

2019: +28.88%

2020: +16.26%

2021: +27%

2022: -19.6%

2023: +24%

2024: 23% (amazing back-to-back-years)

2025: +16% as bonds finally came back

2026: +10% YTD so far, with bonds struggling again

After 2018, the S&P 500 has mostly done very well, except for in 2022. As a result, being too conservative with a target-date fund has cost me and others tremendous performance.

At Fidelity, you can rebalance your 529 plan twice a year. Check your plan’s rebalancing limit a year. Here is my 2022 stock market forecast if you're interested. If it comes true, investing in a target date fund will probably be good. So far, having a more conservative asset allocation is working out.

Target-Date Funds Asset Allocate In The Opposite Direction

Not only did we not change our asset allocation to more equities after a negative 2018, due to the nature of target-date funds, our equity allocation declined even further!

The idea of a TDF is to continuously increase the fund's allocation towards bonds each year as one gets closer to the target date of college or retirement. This makes sense. However, the biggest drawback is that the fund does not change at all based on equity or bond performance.

For example, if the S&P 500 goes down 35% one year, I will be rebalancing more towards equities and away from bonds. I did so in March 2020 when I wrote, How To Predict A Stock Market Bottom Like Nostradamus.

However, target-date funds will just operate like zombies based on a set target date with preset allocation weightings. The automation of these types of funds makes me wonder why there is even a fund manager getting paid to run these funds at all!

Take a look at my son's 529 plan's performance in 2023. It was only up about 10.8% while the S&P 500 was up 24%. That is some serious underperformance, making me believe a 529 plan is not enough to pay for college.

Target Date Fund Fees Are Relatively High

Not only has my TDF significantly underperformed the S&P 500, it also has an expense ratio of 0.87%. In comparison, the expense ratio of the Vanguard Total Stock Market ETF (VTI) is only 0.09%.

Over a five-year period, I will have paid about 4% more in fees. And over an 18-year period, I will have paid 13.86 percentage points more in fees. Those fees may amount to tens of thousands of dollars that could be used for education.

Imagine your 529 plan growing to $500,000 when your child is 18. $500,000 X 0.87% = $4,350 a year in annual fees. Instead, you could have paid $450 a year in fees by holding index ETFs. What a waste, given by then, the target date fund will likely have a very conservative weighting and hence, a lower return.

Active Versus Index Target Date Funds (A-Hah Moment!)

After comparing my daughter's target date fund to my son's target date fund, I realized I had picked an “actively run” target date fund for my son and not an index target date fund. My daughter's target date fund says (Fidelity Index) next to it and only has a 0.14% expense ratio.

I now remember the Fidelity rep in 2017 telling me the two choices on the phone. He sold me on the actively run target date fund without mentioning the higher fees. I was under the assumption the fees were the same. If I knew the fee difference was so large, I would have certainly gone the index route instead. But I was probably sleep-deprived and not thinking straight back then.

Therefore, before investing in any fund, please always ask about its expense ratio! Don't just assume you will be investing in an index TDF with lower fees.

It's amazing how it's taken me writing this post to realize the type of target date fund I invested in for my son. I wonder how many other unsuspecting investors don't realize this as well.

No Wonder Why Target-Date Funds Were Created

Target-date funds are an amazing money-maker for the firms that create them.

Over time, target fund creators make more from their clients as balances grow. Meanwhile, the fund managers don't have to generate any alpha for charging high fees. Instead, the clients are OK with declining returns, making it even easier for the fund manager to do their jobs!

How cool is it to be rewarded for consistently underperforming your respective indices? Because busy parents have so much going on, they often don't bother to do a deep-dive analysis of their returns. Parents end up “setting it and forgetting it,” which is music to a target fund manager's ears.

For the first three years of our son's life, we worried constantly about his vision and health. We also seldom had a good night's sleep. Although I'm on the ball with regards to our investments, I wanted to forget about his 529 plan so I could focus on other things. That was the point of me investing in a target date fund in the first place.

But now that I've been able to slowly come up for air, I'm thoroughly disappointed in actively-run target-date funds and my decision to invest in them. Its lagging performance has been bugging me since 2020. However, I was hopeful that the fund would narrow its underperformance in 2021. Unfortunately, its underperformance widened.

Related: Recommended 529 Plan Amounts By Age

Choose A Index Target Date Fund Instead

With inflation and upcoming Fed rate hikes, having a 30% weighting in bonds seems like too much. Further, there are still 14 years left before our son potentially goes to college. As a result, our son's 529 plan can afford to take on more risk.

Even if we keep the 70/30 equity/bonds allocation the same, I'll just buy low-cost ETFs to recreate the allocation and save 0.78% a year in fees (0.87% – 0.09%). I'm unwilling to pay $2,300+ a year in fees for a actively run target date fund I can easily create myself. Or, I'll just switch to an index target date fund with much lower fees. Check your 529 plan provider to see what’s possible. Fidelity only allows you to choose between active and index target date funds.

If you must own a target date fund, then own one during the first several years of your child's life. That will be when the expense is most worth it. You're busy and need all the help you can get. Further, you aren't paying a high absolute dollar amount in fees because your balance is still low. Even if you lose a lot of money in a bear market, you won't be too pissed either.

Three Years Or $100,000 Until You Create Your Own Fund

Three years after your child is born or a $100,000 balance, whichever comes first, creating your own target date fund with index ETFs is probably the more optimal way to go. You are a more experienced parent so you will be more relaxed. Further, you may also have more time because your child has started attending preschool or daycare.

If you create your index target date fund, you just need to be careful with your asset allocation. Every six months to a year, you should revisit your asset allocation to ensure it corresponds with your objectives.

The easiest thing to do is to follow the asset allocation path of a target date fund you could have invested in. Alternatively, you can asset allocate based on age or just stick to a fixed asset allocation.

If you can’t create your own fund with ETFs, then invest in an index target date fund with a lower fee. Again, my daughter’s index target date fund only has an expense ratio of 0.14%.

Love And Worry Is A Profitable Industry

The money management industry, like the higher education industry, smartly takes advantage of a parent's love and worry for their children. Love and worry are why colleges can continuously hike tuition much faster than inflation. Worry and love are why active target-date funds can charge a high fee, when little investing acumen is required.

And let's be fair here. If the S&P 500 would have continued to struggle after 2018, I would have felt relatively better about investing in a target date fund. The fund would have outperformed the S&P 500, which would have made paying an 0.87% expense ratio more palatable.

However, even still, I would have eventually woken up to the fact that I was paying more in fees than I had to. It was kind of like my epiphany when I ran my 401(k) through Empower's 401(k) fee analyzer. I realized I was paying $1,700 a year in fees I had no idea I was paying! The main culprit was also a Fidelity fund with a 0.74% expense ratio and 95% turnover ratio.

Paying a fee is absolutely fine for something you can't do or don't want to do on your own. But when it comes to a 529 plan or retirement with a long time horizon, we can all construct a simple two or three ETF portfolio and save.

Who Should Invest In Target-Date Funds?

Target-date funds can definitely help investors who want a simple and risk-appropriate way to invest over time. Having an automated glide path is assuring if it fits your objective. However, fees need to come down.

Here's who I think target-date funds are appropriate for:

- First-time parents who want to get their 529 plan investing out of the way

- People who have no interest in staying on top of their investments every quarter, six-months, or year

- Busy professionals working in an industry other than finance and who have little knowledge about investing

- Investors OK with frequently not beating the S&P 500 index in exchange for less volatility

Again, if you do invest in a target date fund, invest in an index target date fund with lower fees. Outperforming a respective index over the long term is hard to do.

Related Post And Questions

How To Reduce 401(k) Fees Through Portfolio Analysis

Different Investment Strategies For Different Life Stages

Roth IRA or 529 Plan To Pay For College

Being Unwilling To Use 529 Plan Funds When The Time Comes

Update: Due to the passage of the SECURE Act 2.0, starting in 2024 unused 529 plans can roll over to Roth IRA for the student. The annual limit is $7,000 or whatever the limit is during that time. The lifetime rollover limit is $35,000. Not bad! You just need to have your 529 plan open for at least 15 years.

Diversify Into Real Estate To Help Pay For College

Instead of investing in bonds, I prefer investing in real estate. I consider real estate a “bonds plus” type of investment because it has greater upside, and potentially less downside. Real estate is a stable asset class that tends to return a couple of percentage points above inflation. But it also generates steady income as well.

Invest in real estate without the burden of a mortgage or maintenance with Fundrise. With over $3 billion in assets under management and 350,000+ investors, Fundrise specializes in residential and industrial real estate. I’ve personally invested $150,000 with Fundrise to generate more passive income. The investment minimum is only $10.

I also think there's a lot of value in residential commercial real estate with prices declining almost as much as they did during the 2008 global financial crisis. Yet, the economy and household balance sheets are much stronger today.

Invest More Aggressively To Pay For College

Contributing to a 529 plan is essential for covering college expenses. However, if you aim for better returns than a target date fund, consider more aggressive investments outside of it, possibly focusing on the S&P 500.

Apart from the 529 plan, allocating a portion (10% – 20%) to venture capital funds for investing in private growth companies is a strategic move. It is part of my dumbbell FIRE investing method I recommend. With companies staying private longer, investing in them can yield significant gains. Considering your extended time horizon for saving, the investment duration aligns well.

Explore opportunities with the Fundrise and its venture product, which is reloading with VCX 2. Its Innovation Fund successfully listed on the NYSE in March 2026 under the ticker VCX, so Fundrise has filed to launch a second venture fund.

Roughly 90% of VCX is invested in artificial intelligence, which I'm bullish about. When my kids are in college, I don't want them asking me why I didn't invest in AI near the beginning.

The investment minimum is also only $10. Most venture capital funds have a $250,000+ minimum. You can see what Fundrise is holding before deciding to invest and how much. Traditional venture capital funds require capital commitment first and then hope the general partners will find great investments.

I've personally invested $253,000 in the venture product, and plan to continue building my position to $500,000 to invest in private AI companies. AI growth is accelerating, and I want to ride the wave. Fundrise is also a long-time sponsor of Financial Samurai.

For more nuanced personal finance content, join 60,000+ others and sign up for the free Financial Samurai newsletter. Financial Samurai is one of the largest independently-owned personal finance sites that started in 2009.

Just saw this today, but wasn’t sure where else to post it…

starting in 2024 unused 529 plans can roll over to roth ira for the student. interesting…

There are a few limitations to the new rollover measure, including:

The 529 account must have been open for more than 15 years

The eligible rollover amount must have been in the 529 account for at least 5 years

The funds must be rolled over to a Roth IRA owned by the 529 account beneficiary (student)

There’s a $35,000 lifetime cap on Roth IRA rollovers for each 529 account beneficiary

Definitely an added benefit! But man, 15 years is a long time. Hence, parents gotta start funding ASAP if they want this additional benefit.

Financial Samurai,

Good post but I somewhat disagree with you my friend. Going all equities on a 529 plan runs an enormous sequence of returns risk. What if your kids were starting college at the start of a bear market, such as 2008? A 40% equities decline coinciding with when they need to use the 529 funds would be devastating. A target date fund, by comparison, would only have a fraction of the portfolio invested in equities during such a time and would have done much better during a bear market.

Hindsight is always 20-20 and given the long bull market, with the brief exception of the 2020 correction, you could have done even better in leveraged bull etfs -were they available in your 529 plan, but there’s no way for you to have known that when you started. Diversification is the only free lunch in town.

Sounds good. How are you investing for your kid’s education? And how many years do they have left until college begins?

When my kids are within 5 years of college, I will lower their risk exposure.

Is it better to superfund a 529 or get the approx. $600 per year state tax deduction?

Most states let you roll over the deduction. In VA as an example, you can deduct $4k per beneficiary per account. So married couple with 2 kids each opens an account for each they can deduct $16k per year. If you superfund, you just take $16k per year until you are done with the total value of deductions.

This is a pretty disappointing column because 1) I don’t believe it for a second and 2) it now makes me wonder how much fiction is in the others.

I can’t believe that you of all people didn’t spend the 15 seconds to check the fee structure when investing 75,000. You, who spend 1000x more time negotiating refis in the same time frame, who has been in the managed investing world for decades. You who absolutely knows the difference between active and expensive management versus passive indexing, along with the ‘scams’ of passive indexing with active management fees. And it shows in the column, which is muddled and contradictory at times because it’s not your actual experience.

This was written for an audience, who may not know these things.

There’s nothing wrong with a Vanguard or Fidelity TDF. I prefer VG because they are transparent with their component percentages, and the cost is the same as buying the subcomponents directly. No one should be paying 50-100 basis points for a TDF. Just as no one should be paying that for an S&P500 fund, but you still come across them in 401k offerings.

There is a great deal wrong with comparing S&P 500 performance to TDFs. This is commonly done since in the last decade it has outperformed everything, most recently because of the big tech giants that dominant this market cap based insex. But if you believe in the principles of MPT or diversification in general, you don’t presume this will remain true, or you accept that you’re engaging in a small bit of market timing.

I don’t like the inefficiencies that come from companies entering or exiting the 500, so I’d prefer the total market index. In the short term I like the US prospects coming out of Covid better than for the EU or the developing world, so the timer in me would want a higher domestic ratio that is seen in many TDFs. As one other commenter mentioned, you can cheat a little by allocating 20% to a second choice, perhaps a small and midcap index.

Like I’ve written in my previous posts, I am a perpetual failure, which is the main reason why I continue to save so much.

But I do like to use my mistakes and failures as a case study to help others avoid making the same mistakes. It makes me happy to help others.

At what age or after how many years were you able to rid yourself of financial mistakes?

Also, you can listen to the Dec 3, 2021 podcast episode about a surprise find on this TDF topic.

If someone doesn’t read your column carefully or past the first half, their takeaway is that TDFs are bad, when it should be that overpriced funds are bad.

And as your recent “Best Asset Class Performers” article showed, the S&P500 was not the top performer over a 20 year span, it was terrible in the first decade, and the prospects for the next decade are somewhat lower. The correct (read: safest from risk adjusted standpoinjt) college investment choice for someone with a toddler is going to be a blended portfolio of multiple asset classes. International could finally snap back (or lose less than US), and substituting REITs for bonds is another topic you’ve put out there that could be attractive for this 20 year investment.

as for mistakes I’ve made – most of them are about selling losers.

I sold Amazon around 2003 for $11/share. It has been underwater for years, I was still recovering from the dotbomb, and per the classic thinking “Would you buy it today? No? Sell,” no reason to keep it.

At another time, I sold off a more substantial stake in CompUSA just about 6 weeks before Carlos Slim acquired it for a substantial premium. I had thrown a bit of good money after bad trying to DCA my way to a positive result, and could have make a profit had I still be in. But had that buyout not occurred, the company would have just drifted to zero like Sears or Kmart.

I feel like my timing is better on buying, though I haven’t rigorously tried to back test. Mostly I’ve shifted to more sector ETFs like VIG over individual stocks. That removes a lot of the decision paralysis on buy/sell decisions as the probability of a big miss and regrets is quite low.

I have some old chunks of PMI/MO that have been dripping their way for 20+ years, but like with Exxon, I should be looking for a proper exit point. Given my past history, and its recent returns, it still seems better to let the dividends accumulate.

Bringing it back to the 529 topic, investors who want to diversity but not be stuck by the decisions of a fund should look to an account that offers automatic rebalancing when the percentages drift too far. Then they can have their cake but not have to keep doing market timing calls of when to correct or when to let it ride.

Selling Amazon at $11/share is tough. Reminds me of being able to buy Netflix at $10/share pre-splits in 2006 given Reed Hasting spoke at my business school graduation ceremony. But at least I’ve held onto most of my FAANG stocks since 2012. It’s been a good ride and enough to pay for our kids tuition through college and then some in 14-16 years.

Sounds like you are over 50. So hopefully, despite the sales, you have done quite well.

I cannot control how much of my article someone decides to read. I try to be thorough. It’s up to the individual to decide how much water to drink.

How much did you invest in your 529 plan and how much did it have when it was time to use it for college?

No, not quite 50, but close enough to get harassed by the AARP.

No kids here, I was drawn to the TDF in the title. But if I were funding a 529 with 75k for a newborn, I’d likely take the Vanguard TDF route.

Netflix in 2006 was a hard buy. It was good enough to clobber Blockbuster, but hard to see it ever having the margin to be worth more. It was the shift to cloud based streaming, enabled by AWS, that changed the scene and the potential profitability.

The big change in tech between the dotcom era and the past decade is how much lower the costs are to run a startup long enough to see if it will be a hit or a flop. IAAS removed so much wasteful capital spending. In 2006 I spent a couple hours with 4 others debating how to spend 10k for a backup site we would normally never use. Amazon or Azure will give you that capability for pennies on the dollar. And if your busiess takes off, you don’t have to wait 8 weeks for a shipment of servers from Dell or HP.

Curious, as a n almost 50 yo with no kids, how do you spend your fortune?

I’m not sure what I would do with my stock gains if it weren’t for my kids. I am donating to two main charities right now and plan to donate a good portion of my book proceeds to charity.

But my kids give my money more purpose. After you have a house, car, food, clothing, there’s not more you need.

Are you thinking of kids given your decision to read and comment on this post about 529 plans? Or perhaps set up 529 plans for relatives?

Hypothetically, what would you do with $5 million in equity gains at your age.

Here’s who I think target-date funds are appropriate for: sheep.

The chances of one actually precisely fitting your needs and risk acceptance are vanishingly small. Plus, the management fees are unacceptable, even if one did.

It seemed like such a good idea at first blush.

Think you are too busy to look in on how your retirement funds are invested? For most people, you’ll spend a lot more of your life standing at gas pumps or waiting in checkout lines at the grocery store. It doesn’t take much to get minimally informed (financially literate), at least not on the minimal levels needed to give your hopes and dreams a little due diligence and a common sense check from time to time. The information you need is all on the web, for free. You don’t need an MBA for this.

Pretty strong words. Not everybody has the time or desire to mange their money. So a TDF fits this need/demand. A TDF with a 0.14% expense ratio is much better than leaving investing to someone who does not want or know how to invest IMO.

Lots of people have just held cash over the years b/c they didn’t know what to do with it.

Maybe a bit strong but I was considering the audience.

There are a lot of sheep. Heck, I’m related to some of them, as are we all. There are always going to be a lot of sheep, so there are always going to be products for them. And that’s a good thing if it keeps them out of stuff that is even more problematical.

But, unless I miss my guess, the sheep are not frequent readers of your blog.

I certainly hope no one with gumption to even come here in the first place is keeping everything in cash, or else won’t be for much longer.

Thanks for this article. Certainly learned more about TDF. I’m certainly the set it and forget it type. Now that I have a toddler and a baby, this is something I’ll need to look into!

Do you see a benefit in combining 529 plans via roll over?

It seems most of the posters have 1-2 529s, (or similar to number of kids). I currently have 3 529 plans each kid – or 6 total.

Initially I did one for each kid in VA for the matching tax deduction of up to $4k per year per beneficiary. Then my wife did the same. We put in enough to at least get the $16k tax deduct each year for VA. There are also some family members who likely have 529 plans for our kids as well.

When we moved out of VA, I shopped around again to see if there were better 529 plans because we were no longer getting the tax deductions. I have kept those accounts though and still contribute to them, as there is always a chance we move back to VA some day and the plan allows tax deductions to roll over indefinitely.

So, now I have 6 accounts, and I’m trying to see if there is really still a benefit or not. Perhaps I should just roll them into 2 accounts?

I have also recently found out that one of my siblings intends to make large contributions to her nieces and nephews as graduation gifts. She just gave my oldest nephew $100k for his graduation to help with his college expenses. My father in law is also gifting around $15k per year per kid as well. However, his contributions are randomly applied throughout the year, and sometime he forgets. I’m never one to ask him because it’s odd to tell someone giving free money to their grandkids that he forgot to make his regularly scheduled deposit. I originally talked to him about super funding but he declined at the time. He thought rolling it in slowly was better, however he would revisit at a later date. My mother also has a large amount of funds set aside for the kids education as well, but I haven’t seen the recent numbers. I know at one point she set aside $450k, but that was to split across all her grandkids, unfortunately she has had health issues and those funds might be needed elsewhere.

So, I’m also on the fence about saving so much if there are other willing parties. Then again, I’d hate to bank on someone else to only find out they gave all their money to a sea turtle refuge. So, I guess I will keep saving as we go.

**As a side note, I haven’t been getting notifications of post responses for the last few months despite the selections made for replies to comments or all comments. Its hard for people to stay engaged if they are not getting the comments. FS, perhaps something to look into…**

Good post! Wow, it’s amazing that even you got taken in by the active fund. It really shows the power of index funds.

My son’s 529 is up about 19% this year. It underperforms because there is a big chunk in international index funds. It’s all equities at this point. I plan to allocate some to bonds when he is in high school.

Maybe something like this.

9th grade – 80/20 stocks/bonds

10th grade – 60/40

11th grade – 50/50

12th grade – 40/60

We’ll see how it goes.

That’s good performance! The funny thing is, after I wrote this post, I called Fidelity to make the switch. And they said I was already in the index target date fund. I guess I looked up the wrong fund or it auto-populated the active fund when I searched.

Regardless, the performance has still been disappointing.

Great article! My youngest’s 529 plan is 100% equities but my 9-year old is in a relatively conservative target index fund because his account already has enough to pay for any school he wants to attend, so I just want to preserve capital and keep up with inflation now. I don’t want to take unnecessary risk with college accounts since it’s not that far away, especially relative to retirement.

Can you share how you were able to get your 9-year-olds 529 plan to be so large? Are we talking $500,000+ level due to superfunding 9 years ago? It’s always good to see real life examples to motivate folks to save and invest.

What plan did you use to let you go 100% into equities?

I use Utah for my kids’ 529 accounts, and Utah has good options including a “customized static” option. I don’t work in finance and haven’t spent a lot of time on this. It just made sense to me to take some risk in a tax advantaged account when my kids are young, and then once I felt like I have enough, to take some risk off the table. My 9-year old has almost enough pay for an Ivy priced school for 4 years in today’s $$, so I switched to a target date fund for him, because again, I don’t work in finance and creating a balanced fund on my own is outside of my wheelhouse. For each of the last 10 years, I direct deposited into his 529 plan via automatic paycheck contributions an amount equal to the annual gift tax limit because it was the right amount for my budget, but more recently, I invested a couple large work bonuses because I’m finally in a position to do so comfortably. Now I am shifting my focus to my toddler’s account. I plan to stay in at least 90% equities while I’m trying to get that account to a similar place, then switch to a target date fund, and retire!

Good stuff. Hope our 529 plans appreciate at least faster than tuition appreciation rates!

Thanks for this article! I’m definitely the set it and forget it type of parent. I even forgot the login to my son’s 529 account! Will need to login and check the expense ratio for whatever fund I selected.

We didn’t set up any savings plans for our three kids’ college expenses, we planned on cash flowing college for them, which we could have done since we were only going to pay for an in state public university, which are still relatively affordable here. As it turned out there were no college costs as they all got totally free rides for their four year degrees. We didn’t help out with graduate degree costs or medical school.

As the parent of a HS senior and sophomore that has saved for college via target date 529s, this hit home. I’m always fine tuning my other retirement & brokerage accounts but for some reason I just left the 529s alone. That was a mistake! To parents of younger kids, pay attention now, be smart, and add a little more risk/return. I now have to cover more college expenses out of pocket because my 529 returns were weak. Wish I read something like this article 17 years ago.

I have my share of regrets as well as my oldest started college this year. Had I been more aggressive and paid more attention, it could have meant she can likely get through undergraduate studies without any loans. But perhaps having a bit of skin in the education funding process is not completely a bad thing. My goal for all three of my kids is to help enough so they can graduate with at most their 1st year salary.

Interestingly, I’m very aggressive in my portfolio 90%+ stocks but in my kids 529 ( split between 3 ), I played safe and put it on moderate risk age based autopilot mode. I felt like I can always work longer if I need to but my kids’ timelines are fixed. I was certainly not in the financial situation of being able to super fund 529s when my kids were young.

FS super-funded 529 so perhaps there’s different mindset that goes into that with 17-18 year horizon plus the possibility of even paying for his grandchildren’s education with that fund. I definitely agree that more aggressive approach is the right thing if you can invest large amount early on.

“ My goal for all three of my kids is to help enough so they can graduate with at most their 1st year salary”

Could u clarify what you mean?

We decided to superfund bc we had cash and were investing in the stock market anyway. So it was basically carving out what we were going to invest for retirement for our children’s education instead.

Wanted to get it out of the way bc we felt already so overwhelmed as first time parents.

Congrats for investing in your 3 kids to have enough to pay most of the tuition!

A rule of thumb that I’ve come across many times while researching college financing is that if you can keep student loans under what the student might earn as the first year salary out of college, it will be a manageable amount that can be paid back in about 10 years. For each one of my kids my plan is to use that as the maximum loan limit since I will likely not be able to pay for all of the cost at the current projection unless they are able to get substantial scholarships or we get a windfall.

1st year salary could be different for each child as they will want to pursue different careers. So in my case I set my maximum loan target of around $40k for 1st, $50 for the 2nd and $60k for the 3rd. The differences are to account for tuition increases and inflation as they are 3-4 school years apart. Salary expectation is at the low end of the spectrum to be conservative as well as to keep my possible expectations in check on their choice of major/career.

My real working projected numbers are to limit their loans to federal loans only (max $25k total for 4 years right now) if they go to a in-state university and not take out any private loans for undergraduate studies. If there’s any fund left over in their 529 at the end, it will go to pay off the capitalized interest and some of the principle amount. With multiple kids, there is a juggling act to make sure I’m contributing fairly across all three account not just from contribution amount perspective but also based on what the balances are projected to be when they start school.

If they decide that they really want to go to an out-of-state or a private school, they will have to take on more of the burden. Any scholarships or income from part time jobs will not reduce my contribution. I tried to tell them about these things time to time but it’s hard to tell if it means anything to them right now. Hopefully, it will factor in to their choices. Only exception I told them is if they get into an elite university, I will contribute more. Since probability of their success is likely higher, I’m willing to sacrifice more as odds of them coming back to live with us as an adult child would be lower.

Well, that’s sort of our plan. Super funding 529 makes so much sense for anyone who can. I wish I had contributed more earlier rather than some of the dumb things I had spent my money on in my 20s and 30s

Thanks for all the articles you post and update. They have been a great resource for helping me think through my financial plan. Your site is one of the reasons I created a detailed plan last year to become financially independent in the next 10 years or so by the time my youngest is out of college.

It’s not the be-all, end-all solution, but Paul Merriman’s “Two Funds For Life” is one solution that attempts to address the lack of aggression in a TDF (recognizing that a TDF is over-allocated to bonds in the earlier years). His solution is to put 70% in a TDF, and 30% in a more aggressive fund, such as a Small Cap Value fund.

Hey Sam, this is my first time posting but definitely not my first visit! I consider myself pretty savvy when it comes to picking low-cost funds and I completely overlooked the active versus index fund selection for both my sons/daughter fidelity 529 accounts also in the NH funds. I just changed them over to the index age-based funds to keep it simple. I am going to have my kids email you in the future to thank you for the extra college money you just made available to them, thanks again!

Good to hear Matt! The fees really add up over time, especially if our 529 plans continue to grow.

Better we catch our suboptimal decisions earlier than later and make a change!

Sam

My MFS 529 snuck in 5+% load fee without telling me when I opened the account AND have expense ratios near and over 1% with no index fund options. I bout lost my mind when I figured it out. Needless to say I’ve transferred my 529 to another provider scholarshare and am much happier, F MFS stay away!

Wow! That’s a lot. Glad you changed, but the front load is gone forever right?

Scholarshare has no load, much happier now in a 100% US equities TIEIX fund (for a 9 y/o so still have some time for risk) with a .05 expense ratio (lowest fee I could find in a fund I liked). When I confirmed there was no load I superfunded it last year.

But still kicking myself for paying the load with MFS, should’ve sniffed that out with more investigation before contributing. Similar to your on boarding agent not disclosing the ‘extra’ fee for the active fund. Good lessons on asking all the questions at the front of the relationship…

As always great insight for and against 529 target date funds. Just as you stated if the market went down your sons 529 account would have done better aka felt better. Since your son is so young I agree with taking more risk. What really surprises me is that you didn’t look into Nevada’s 529 or Utah’s 529. You should really look into Utah’s 529 customizable index 529 funds (low cost) with all your investment acumen. I have 2 kids and I used Utah’s 529 customizable low cost index funds and target date fund. It’s really interesting how timing of investments matter a whole lot more than what you invest in. For example if the older kid 529 was invested in a target date fund during lower valuations (higher bond allocation) vs a customized allocation (higher stock allocation but rising market) result in widely different returns. My older kids 529 value is much higher than my younger kids even though my younger kids allocation is a lot more aggressive and I also dollar cost average at a rate of 50% more in my younger kids account.

I’m not sure if I had a choice with Utah’s 529 plan, but I’ll ask next time.

Can you share some performance numbers of your Utah plan and expense ratio? At the end of the day, those are the numbers that really matter.

We’ve all got analyze the hard numbers.

Thx

I went with Utahs 529 too. I chose to do a self designed glide path using their Vanguard and dimensional funds. This article prompted me to go check performance. I did 80% US and 20% international, all equity with tilts towards small cap and value. It stays equities until 3 years before college, before shifting to 50/50 allocation. YTD is 24% return vs 26% on S&P, tough to beat S&P the last decade. I just worry about the overconcentration among the top holdings now.

They add .14 in fees to self directed portfolios on top of vanguard fees that avg under .1. So it averages about .2% in fees

As always great insight for and against 529 target date funds. Just as you stated if the market went down your sons 529 account would have done better aka felt better. Since your son is so young I agree with taking more risk. What really surprises me is that you didn’t look into Nevada’s 529 or Utah’s 529. You should really look into Utah’s 529 customizable index 529 funds (low cost) with all your investment acumen. I have 2 kids and I used Utah’s 529 customizable low cost index funds and target date fund. It’s really interesting how timing of investments matter a whole lot more than what you invest in. For example if the older kid 529 was invested in a target date fund during lower valuations (higher bond allocation) vs a customized allocation (higher stock allocation but rising market) result in widely different returns. My older kids 529 value is much higher than my younger kids even though my younger kids allocation is a lot more aggressive and I also dollar cost average at a rate of 50% more in my younger kids account.

Ive looked at target date for both 529 and retirement plans, and have found them to generally be under performers vs the s&p or a total market index fund(vtsax). So I just buy both s&p and totals and call it a day. Yes they have more volatility. A down year just means stocks are on sale so just buy more. Warren Buffet said it best; 10-20 years from now stocks will be cheap! (Loosely quoted). To be fair, my investment horizons are long 35ish till retirement and 15-18 years for kiddos. Great article, love the content you provide it gets me thinking about many things. Thank you Sam!

One thing to check is if the state you live in you can deduct your 529 contributions. Where I live in New York, families can reduce their tax liability by $5,000 (individual filers) or $10,000 (married joint filers) when they contribute to a 529 plan. Fidelity doesn’t have a NY State 529 plan so I went direct with the NY state plan. BTW, California does not allow families to deduct their contributions to qualifying 529 plans.

Don’t feel too bad. I had a similar experience. My wife and I starting automatic contributions to a 529 for our future kids in 2008. Since we didn’t have any kids at the time, we put it under my name and let it invest in target date fund. I didn’t give much thought to it for 8 years as it continued to grow automatically and incrementally increase contribution amounts.

When my daughter was born in 2015 we didn’t even think about changing the beneficiary. Unfortunately the fund you were invested in was based on the age of the beneficiary and instead of using a newborn (aggressive portfolio) it was using a 36 year old (conservative portfolio). I didn’t actively look at the account so I didn’t really notice until 2017 when I saw the error.

So did I immediately switch the beneficiary and/or the fund/risk? … well no… I decided to go against my long term investment philosophy and assumed their would be a downturn after so many years of a bull market. Talking about adding insult to injury. It wasn’t until earlier this year that I finally corrected the mistake. I don’t have the heart to calculate the loss in potential earnings but know that when only 30k of a 165k 529 plan come from earnings, I clearly made several errors in judgement.

Thanks again for all your postings. I always enjoy reading them.

Doh, But I am super impressed you guys had the foresight to invest 7 to 8 years before your daughter was born. Shortly, you are doing way better than the average person. There’s a plan to do much better.

Great insights thanks! I remember considering a target date fund when I first opened my 401k account. But then I decided against it and ended up going with several different funds to diversify my exposure. I had to create regular calendar reminders to rebalance and monitor performance but it wasn’t too much hassle once I got the hang of it.

Go with Vanguard 529 the fees are .14% for the target funds. They also let you self adjust your account with multiple cheap stock and bond index funds. I put my money years ago there because the state run plans were a complete rip off (2% fees) and all managed accounts. I adjusted my account stock/bonds balances because like you I think the target funds are too conservative. Once my child hit 18 I did put in a target fund, so I didn’t lose principal. If you want cheap with good service I would go with Vanguard.

0.14% must be the magical number for index target date funds, as it is the same with Fidelity’s index target date funds.

Our 529 has very limited options. As I only put in the optimal amount in MN per year ($500) between the 2 kids, I don’t have a large enough balance to worry about it.

The reason I’m not superfunding the 529s is that I’m not sure what the future will hold. Our kids could get full ride scholarships, they could end up going into a trade, or some political swing may make college much cheaper.

How do you decide that $500 is the optimal amount to contribute?

Unfortunately, we are an overrepresented minority, and I dare not think my kids will be smart enough to go for scholarships.

I’m much more conservative, and would rather save and invest too much then have too little.

Related: Recommended 529 Amounts By Age

In MN there is a 50% tax credit up to $250, so contributing $500 provides the maximum “return”.

My strategy does have risks, but if you save too much in a 529 there is a 10% penalty and you have to pay income tax rates on any growth. So you have an investment vehicle that is funded post tax, and potentially taxed at income rates +10% instead of capital gains. Another strategy is to use Roth funds to pay for college, which is a qualified distribution.

I really wish the government would allow 529s to be rolled over to Roth IRAs for the beneficiaries, or at least taxed at capital gains rates if there is overage.

Gotcha. Check out these two posts:

Using The 529 Plan For Generational Wealth Transfer Purposes

Roth IRA or 529 Plan To Pay For College: Pros and Cons

I would contribute more to the 529 plan if I were you. You can always change beneficiaries in the future with money left over.

Why do you say you wish you’d set up the 529 before your son’s birth?

More time to compound in a tax-efficient manner. I should have open end one in 2012 under a different beneficiary and then named my son the beneficiary after birth. But I didn’t 100% I was going to have a child in 2017 back then.

But in 2016, I had high certainty I was going to have a child in 2017. And if not in 2017, then by 2020.

***

The IRS requires that a 529 account be opened for a living beneficiary who has a Social Security Number. This requirement rules out opening a 529 account with an unborn child as the beneficiary. However, 529 plans offer the flexibility to later change the beneficiary. For example, a parent may open an account and initially list him or herself as the beneficiary, and once the child is born, change the beneficiary to the child. Before choosing an initial beneficiary, you should be aware of potential tax consequences of later changing the beneficiary.

Is your issue with all target date funds or ACTIVELY MANAGED target date funds (w/high expense ratios)?

I don’t really have issue with the equity/bond allocation of target date funds (and I expect performance to lag an equity index because of this). But I mostly don’t like how much they usually allocate to non-US equities. It’s past performance bias, but they generally have not performed as well as US equities the past decade. And that drags down the target date fund performance. Of course, if we have a market correction, maybe ex-US equities will then outperform? Who knows.

Actively managed with high expense ratios and target date funds in a bull market.

Index target date funds have reasonable expense ratios. But you have no control over the asset allocation.

I have 4 of 5 grandchildren in Fidelity 529 Target Date Fund Plans and I am overjoyed with the annual ROR. I see the annual ROR declining over the last 8 mo but was surprised to see how well they were doing. I contributed $900 to each this year and they are all nearing $10,000 now with appreciation between $1500-$1800 in addition to my contribution.

Fidelity NH Portfolio 2030 12 mo ROR 03/31/21 37.54% 11/21/21 22.95%

Fidelity NH Portfolio 2033 12 mo ROR 03/31/21 46.04% 11/21/21 28.52%

Are they the Fidelity Freedom (active) or Fidelity Index TDFs?

Makes me feel I did something right! For my oldest daughter, now 10, in the Virginia 529, I used the James Madison fund, which is a target fund. My parents own it and my dad doesn’t like 529s, so I stopped investing in it years ago. When I opened Florida 529 years ago for her, I split it 60, 30, 10 or something like that between large, international, and small. I think it has done OK. For my other 2 kids, she 3 and 4, when I opened their Pennsylvania 529 (managed by Vanguard), I invested 70% in the Total stock index and 30% in the Total int’l index. Those have done very well. The only thing I think I still need to fix are my old Roth IRA, which is in Fidelity 2030, which I haven’t contributed to in years.

Have you compared the actual performance numbers? I’m curious to know the exact results.

I think we go too much on “feel” where we “wing it” with out investments. That’s what the fund management industry hopes more people do. We need to look at the relative returns and fees more.

WOW! Based on your request to compare Target fund vs Closer to Index funds, I did. I had to first enter in a lot of the historical price data into my Quicken. YTD, the 529s invested in 70 Total Stock / 30 Total Int’l (Pennsylvania) is netting 25%, as is the one split with US, Small Cap, and Int’l (Florida). The Target 2030 fund (Virginia), with 50% equities and 50% fixed income is at 8%. With 0.39% in fees. And the kid just turned 10 years old yesterday (about when I opened it). If I look at 2020, it is 17 – 20% vs 11%. If I look at 2019, it is 23% – 27% vs 16% for the Target 2030 fund. The only positive is that I stopped contributing to that Target fund in 2017, as I was funding her Florida one, which did the best. With that said, in 2018, they all lost money, but the Target 2030 one lost the least. I just took a look at my IRA and Roth IRA, the former in an index fund, the latter in a target fund. WOW again, YTD 30% vs 13%. Though 2020 was comparable with 18% vs 15%, but 2019 was 31% vs 21%. Luckily the IRA has 4x the Roth IRA in dollars. And in 2018, the Target lost far less money. Maybe for retirement, it is OK as it is a form of diversification. Looks like I switched my wife’s retirement from Target to Index fund in early 2017. Should have done it earlier, but at least not too bad.