With stocks again at or near record highs, it's a good idea to find ways to spend some of your stock market gains. Owning stocks provides no utility or inherent joy (unless you're a lover of money itself), so we must sell on occasion to capture its benefits.

When I first began investing in stocks in 1996, my freshman year in college, I invested for the sake of “getting rich.” Then I changed my purpose to learn as much as possible about the stock market to get a job in finance.

Over time, the goal of “getting rich” through stocks became meaningless. Instead, my goals for investing shifted to become highly specific after losing lots of money in stocks from 2000 – 2003 and again from 2008 – 2010.

The losses reminded me about the importance of selling stocks once you've made enough to buy what you want. Do you know what you're saving and investing for? Stocks are expensive nowadays. Might as well use some of your gains to buy something enjoyable just in case there's another correction.

Best Way To Spend Your Stock Market Gains

It's great to celebrate the good times, especially after a bear market. Here are eleven ways to spend your stock market gains in no particular order. I'd love to hear more ideas from you.

1) Fertility treatments

If you don't have a child and want a child, you may want to sell some stocks to pay for egg freezing or IVF treatments. Insurance generally does not pay for these costly treatments.

On average, the cost of freezing eggs can be anywhere from $10,000 to $15,000 per cycle. More than one cycle may be needed, which can make the total cost about $40,000 or more.

IVF can cost between $15,000 – $40,000 per cycle, depending on where you live. Unfortunately, there are no guarantees a mother will get pregnant and stay pregnant after each treatment. Hence, the cost of fertility treatments can go way up.

The younger you start, the better your chances and the more you'll potentially save.

2) Your child's college education.

Figuring out how to pay for college is a major stressor for many parents. Despite tuition costs soaring, you can’t expect children to make pragmatic choices about higher education or be brilliant enough to land rare full scholarships. Consequently, parents often remain unhappily employed at jobs they dislike for longer than they’d prefer in order to finance their kids’ degrees.

Why not use some of your stock market gains to eliminate some of that college tuition stress? When it's time for your kid to go to college, use your 529 plan, Roth IRA, or UTMA to pay for their college education. It matters less what the balance is in these education accounts.

You must spend when it's time to spend because getting a degree isn't an endless effort. Trying to make future gains in your education accounts once tuition needs to be paid is pointless. This is the moment you've been waiting for.

3) A house you'll live in for 5+ years

Taking stock market gains and converting them into a house is by far my favorite choice. We spend 12 or more hours at home every day. Those who work from home easily spend 20 or more hours at home on average. As a result, our home is a primary consumption.

However, unlike selling stocks to pay for something that no longer provides a potential return, a home does. Selling stocks to buy a house is simply an asset transfer from a more volatile asset to a usually less volatile asset.

Real estate has also traditionally appreciated over time, just not in as great of a magnitude. As a result, depending on the amount of leverage you take to buy a house, your net worth may not fall as far behind as if you had stayed invested in the stock market.

In fact, due to most people taking on a mortgage, while also having a larger absolute dollar exposure to a house, most people will build more wealth through real estate than through stocks.

To be able to make more money from real estate than stocks, experience less volatility, and enjoy your house is a triple win. Trying to buy the dream house now after massive stock market gains is a worthwhile endeavor.

Bought My Forever Home By Selling Stocks

I took my own advice to heart and sold stocks and bought a home with cash in 2023. In retrospect, this was a suboptimal move because stocks kept marching higher. However, I also used a lot of Treasury bonds to buy my home, and the home has likely ticked up in value since 2023.

Even though I climbed to the top of the property ladder and am not happier, I am more satisfied. As a father, it is my duty to provide for my family. I think the best time to own the nicest house one can afford is when the kids are living at home.

The home is incredible and it feels great to enjoy my wealth. In addition, if the home came on the market today, I don't think I'd be able to buy it for the price that I did. With tech and artificial intelligence on fire, more people will be looking for these types of luxury homes.

4) Remodeling your home

If you don't want to move, you may want to parlay your stock market gains into remodeling. Make investments to improve your home, like remodeling the kitchen and bathroom or finishing the basement. This also typically increases the value of your home.

The lowest hanging fruit is changing the fixtures in your home – door knobs, faucets, lights, and window treatments. They are relatively easy and cheap to do. The next easy remodel is installing Toto washlets. They will change your life for the better. Also consider buying a new dishwasher and washer and dryer.

If you're over 45 years old, I don't recommend you do a complete gut remodel. Maybe remodel a bathroom and a kitchen one at a time. But going through an entire gut may not be worth it due to the amount of stress and time involved.

5) A mid-life crisis car

Stock market gains are like funny money gains. You don't do anything to make money. You don't do anything to lose money. As a result, it's sometimes nice to turn funny money into splurges you don't need. And one such thing is a mid-life crisis car.

My Range Rover Sport is coming up on 10 years old in 2025. As a result, I'm beginning to research what our next family car should be. I like the look of the redesigned Range Rover. It's larger than the Sport as well, which works well as my kids grow larger.

However, I also just bought a house that has a Tesla charge. By 2025, even more car brands will have adopted the use of the Tesla charger system. Therefore, I'm leaning towards finally getting an electric vehicle.

It's going to be fun test-driving all the options, such as the Cybertruck. Maybe a Range Rover EV will be the final choice. But I'm always wary about getting the first or second-year model after a redesign due to all the bugs.

6) A sports / health club

Mental and physical health are more important than money. Hence, if you have stock market gains, you might as well use some of them to join a private sports club.

You'll be able to exercise, play sports, and make friends. If you're feeling lonelier than normal, joining a sports club will do you wonders.

In February 2023, I joined a club to play tennis and pickleball indoors during the rainy season. I'm less happy and grouchier when I don't get my sports in. The extra $185/month has been well worth it.

7) To charity through a donor advised fund

Consider donating some of your stock market gains to charity through a donor-advised fund. The recipient gets the fully appreciated value of the stock and you don't have to pay capital gains.

If we're lucky enough to make money doing nothing from the stock market, we should share our good fortune. Giving feels great which is one of the reasons why I've consistently published and recorded on Financial Samurai for free since July 2009.

8) Pay off annoying debt

Pay off any outstanding debts like high-interest credit cards, auto loans, or student loans. This is like giving yourself a guaranteed return equal to the interest rate and frees up cash flow.

Even if the interest rate on your debt is 0%, for example, like if you got an interest-free loan from your parents, paying off the debt feels wonderful. The less money you owe to people or institutions, the more free you will feel.

I have never regretted paying off a mortgage, even if I could have made more money elsewhere. Each time felt like a tremendous victory given the average duration of having each mortgage was 15 years.

When you're young, you may enjoy taking on debt to supercharge your net worth. When you're older, you may enjoy paying off your debt to feel more secure.

9) A new fancy wardrobe

As someone who likes to wear inexpensive comfy workout clothes, owning a fancy wardrobe is foreign to me. I have the same suits, shirts, and pants I bought from 2000 sitting in my closet. Hence, if you want to find a way to save money on clothes, stay the same size for as long as possible.

However, now that I'm mingling with other parents more often due to my children's school events, I should probably get some new clothes.

Well-tailored clothes help you leave good first impressions. Beyond buying clothes that fit well, you can also consider accessorizing with jewelry and fancy watches. For those into luxury watches, you'll be pleased to know luxury watch prices have come down since early 2022.

10) Your loving parents

If your parents are still around, it's worth spending some of your stock market gains on them. Being a parent is the hardest job in the world for the first 18 years. But we tend to take our parents for granted over time, especially if we are not parents.

Wouldn't it be nice to send your parents on a nice cruise? Or how about a two-week vacation to Paris and Italy? For parents who are extra frugal, spending money on them is a great way to get them to change their financial habits.

Enabling our parents to live it up during their golden years is something we'll never regret. Neither will they. I've been trying to get my parents to travel now that COVID is over. However, it's been harder than expected.

Maybe the ultimate: On freedom to do what you want

If your stock market windfalls are sizable enough, you may finally feel emboldened to negotiate a severance package and bid work farewell forever.

Take your total gains and divide them by your annual living expenses to determine if you have adequate nest egg sustainability. If your stash can provide for you until average life expectancy, you're set to escape the corporate grind.

Realistically, amassing the funds to sustain you decades into the future may be overkill. You really only need your investments to bridge the gap until age 70, when maximum Social Security benefits kick in.

At 59.5 you’ll also gain penalty-free access to 401k/IRA savings. In addition, you may have other sources of passive income streams you’ve developed could support you as well.

Having the freedom to retire early thanks to runaway stock success may be the ultimate prize. When work becomes optional, you tend to only expend effort on passions—creativity unburdened by what pays the bills.

If you have smaller stock market gains, here are some cheap, fun, and practical things to buy for less than $100.

Here's To More Stock Market Gains In The Future

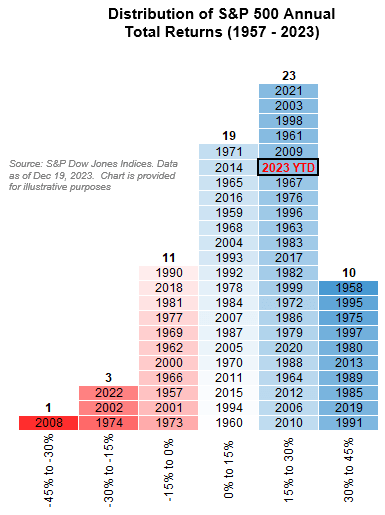

After the stock market’s dispiriting losses in 2022, we should revel in our current gains—who knows their staying power amid an unknown future. Sure, the Wall Street forecasts for the S&P 500 are for another 7-8% return in 2025. But you never know. Rather than endlessly chasing more or fretting through the ups and downs, let’s appreciate windfalls when they arrive.

Occasionally taking chips off the table to fund lifestyle desires maximizes the purpose of investing. Here’s to celebrating gains as we go!

How are you spending your stock market gains? The more ideas the merrier.

If You Want To Continue Investing

After years of investing and seeing our net worths grow, it came be hard to take profits and enjoy life. Therefore, if you can't help but invest to potentially make more money in the future, continue to dollar-cost average into the S&P 500, real estate, and private growth companies.

To invest in real estate more strategically, check out Fundrise. Fundrise runs around $3 billion in assets under management for over 350,000 investors. It invests primarily in Sunbelt residential and industrial real estate where valuations are lower and yields tend to be higher.

I've personally invested $400,000+ in Fundrise funds so far and my investment outlook is well aligned with the CEO. Plus, I love the transparency and easy of entry they provide. You can get started investing with only $10, making it easier than ever to invest in real estate.

Plus, they also offer venture capital exposure. You can invest in private growth companies, with Fundrise Venture in the artificial intelligence, prop tech, fin tech, and datacenter space. Private companies are staying private for longer, meaning more gains are accruing to the private investor.

We have the opportunity to invest in great public and private AI companies at the beginning of this revolution. Fundrise Venture is open-ended with only a $10 minimum investment as well.

When my kids are adults, I certainly don't want them asking me why I didn't work in AI or invest in AI near the beginning.

Disclosure: Fundrise is a long-time sponsor of Financial Samurai and Financial Samurai is a multi six-figure investor in Fundrise funds. Financial Samurai only works with the best companies that can provide the most value to its readers.

You have a good list. Your “spend” articles don’t get a lot of attention, but I love them. Maybe most people have no problem finding a way to spend their money, but it’s a big problem for me.

Since the beginning of the pandemic, I’ve bought a new sports car, dishwasher, washer/dryer, all interior door knobs(silly, right?), taken pricier vacations, contributed more to my DAF, and am paying for two private high school tuitions (my biggest expense). The kids also have paid activities and lessons, coaching/tutoring, college counseling, summer programs, medical needs, etc. My wife started pilates. I wish there were more things I could spend on my wife or me that would bring us joy.

We have no use for fancy clothes, purses, cars, etc. because we both work from home. I only get dressed up to attend school events, and I never take the new sports car. I prefer to drive my 30 year old sports car. Even among other wealthy people, I practice stealth wealth.

I cannot bring myself to remodel due to the hassle, and I cannot upgrade my house because my current home has a super low mortgage rate and property taxes (Thanks, Prop 13).

Equities were never our thing & over the years we did hear the concerns, from many of our friends, who invested traditionally & are still working in their late 60’s. Some took out mortgages to pay for their kids college education, with many of their kids still paying off other loans. Ours all used passive income, that the wife setup, as well as scholarships & owned their own homes within 5 years of graduating.

But we are selling off most of our free & clear properties & holding the notes @ 9.75-12% on most. Seller financing helps spread the massive capital gains that we have earned over 40+ years, but depreciation recapture is now the silent killer. We have been debt free & all cash on everything since ’98.

40 years ago the original 0-5% down/leverage to get in, the tax advantages of passive income over W-2, (retired very early) & the massive tax deductions against income, have all generated more wealth for us than anything equities could have done.

To visit our out-of-state kids we live between three very nice homes that we have updated & paid cash for. Thankfully we are still in great health, BUT having lost a few close friends during & since Covid my wife found this quote insightful …

“the older we get the more I realize that the ultimate luxury is not wealth, but TIME” !!!

Sam, How has your experience been with RR over past 8 years from reliability standpoint? We just bought the 2024 RR LWB SV last week using some of the stock gains (Meta/MSFT) this year. I am not big on cars and was a bit concerned about land rovers reliability scores but couldn’t resist the design, luxury and isolation (air tight cabin) of 2024 RR.

Loved the article, as always!

Hey Sam,

I’ve read your post about paying all cash for a new home. Would you take on a mortgage to buy a second home in another state (not a vacation property) even if you could pay cash without selling any other assets? This could be a long term relocation play, though we plan to keep our current home which is fully paid for. It’s worth about $750k and we’re planning a slight geo-arbitrage play in a lower cost (much lower tax) market. I’m trying to think strategically here.

I wouldn’t if I could pay all cash without selling other assets. I’d use the power of all cash to get a better price. You always have the option of doing a cash-out refinance if you want.

I just don’t know your cash flow, net worth, or future plans for funds.

We’re looking at a cash-out refi as an option.

A year ago we sold our business to private equity, but retained a modest equity stake in the company that acquired us. I’m 57 with a goal to “retire” at 60. Cash flow is good, with cash equivalents currently at about 20% of total net worth (about $5.2M)

The rest is across real estate (passive & active), stock market and the private equity stake.

A new home would represent about 12% of our current total net worth in the price range we’re considering. That would weight our “active” real estate holdings at about 40% of total net worth overall.

An eventual PE sale could increase net worth by an additional 45% within 3 years, but that’s not guaranteed.

Likely overthinking this… but nice to have options!

Todd,

I like Sam’s all-cash/refi idea. I’m looking at similar situation for a Utah SFR LT rental. Plan on using HELOC & Cash proceeds. I’ll just keep rolling my 4 week T-Bill until I find something. Goal would be to put enough down to cash flow a bit while taking some gains off the table. You’re in an awesome position w/ options. – Sky

I’m putting in a votes for the Tesla and the wardrobe!

Happy holidays and best wishes for the New Year.

Where would you recommend going to buy men’s clothes?

I’m definitely no expert on clothes. When I was working in finance, I liked getting tailored blazers in Hong Kong and tailored shirts from Thomas Pink, which can be found in the U.S.

Oh yes, tailored clothes from Savile Row in London is a great experience. https://www.gq-magazine.co.uk/gallery/savile-row-tailors-london

Half the battle is being fit and getting fitted clothes.

I spent 5 years in London UK back in early 70’s (worked for Australian Trade Commission) & had several suits hand made on Saville row, also had a couple made in Austria from Italian cloth. Amazing Merino wool material, just sad that I outgrew the girth of them all. Sadly I now just wear Carhartt as it’s more functional.

As usual, you are spot-on with what’s on my mind, especially #10. With several our uncles/aunts in poor health but parents still healthy, my sister, wife and I decided to send our parents to Australia this spring. We have some recently discovered relatives (thanks ancestry.com) that we have never met in person and realized that time was running out for our parents to be healthy enough to make the trip.

They always did so much for us growing up and it feels good to give them a trip they may not have otherwise taken.

Thanks for the reminder that we are earn money and save for a purpose.

Happy Holidays!

Awesome! I might have to check ancestry.com out. Seems like the easiest way to prove Polynesian/Hawaiian ancestry.

I’m in saving mode for the next 3-6 months and then I have some deferred shopping I want to do. Nothing major as I’m a bargain hunter, but some new wardrobe pieces would be nice. My whole wardrobe could probably use an entire overhaul but I want to get some classic pieces I can hopefully get a lot of mileage out of. And planning a nice summer vacation to a resort would be my other big splurge for next year.

Bucket list! Number 1 on mine is flying private. It might be time to pull the trigger.

It’s worth trying once. You may never go back. Or you may find flying First such a great bargain after! That’s what I discovered compared to flying private.

But I don’t fly more than once a year anymore. Easy splurge.

See: The Cost Of Flying Private

Would you agree that investing ‘for the sake of getting rich’ is somewhat similar to investing ‘so i don’t have to continue working at XX age in the future?’

At the time, when I was in college, no. I had little concept of what being rich really meant and what early retirement was. Instead, I wanted to get a job to make money, buy a car, travel, go out, etc. Now rich to me is family, health, and freedom.

What are ways in which your spending your stock market gains?

Nice fun article, Sam. I’m thinking of buying an electric car but not sure yet. Can you do a post on car buying? Wanted to understand your car buying research process.

Happy Holidays!