The maximum amount of earnings subject to the 6.2% Social Security payroll tax climbed to a record $176,100 in 2025, up from $132,900 in 2019 for reference. As a result, your goal should be to increase your investment income so you can earn more tax efficiently.

In other words, those lucky enough to have jobs and earn $176,100 or more will have to pay $10,918.20 a year in Social Security tax. This tax would be fine if Social Security was fully funded. However, at the current rate, retired citizens will only get about 75% of the expected payout by 2040.

But of course, you can't forget about Medicare, which is 1.45% of all income earned. And Medicare doesn't have an income cap. So the reality is that a $176,100 a year laborer will have to pay $10,918.20 in Social Security tax plus $2,553.45 for a total of $13,471.65 in 2024. The maximum income for FICA tax will continue to go up each year.

Entrepreneurs Have To Pay Both Sides Of Social Security Tax

If you are “unlucky” enough to be your own boss, you've got to pay the 6.2% Social Security tax + 1.45% Medicare tax times two (employer plus employee)! In other words, a self-employed individual making $176,100 will now have to pay over $26,943.3 a year in Social Security + Medicare tax. That's nuts!

And the great irony is, good luck trying to collect unemployment benefits if your business goes bust.

If you want to save on taxes, earn less W-2 income and more passive investment income. Investment income is taxed at a more favorable rate.

Social Security Is Not In Good Shape

Out of the estimated 173 million workers who will pay Social Security taxes in 2021, about 12 million (7%) will be paying more. But as I've shown you before, anybody who makes between $100,000 – $200,000 and lives in a large city is considered middle class. Therefore, we can conclude the middle class is getting punched in the face even harder.

Don't forget, there's also the 0.9% Additional Medicare Tax on employees that went into effect in 2013. If you make more than the below thresholds, you've got to pony up 2.35% in Medicare taxes (1.45% standard + 0.9% additional).

The semi good news is if you're self-employed, the employer Medicare rate stops at 1.45% and is exempt from the additional 0.9% even if you make more than these thresholds. The bad news is these income amounts aren't being adjusted for inflation, so more and more people are getting subject to the additional 0.9% every year.

- $250,000 for married taxpayers who file jointly.

- $125,000 for married taxpayers who file separately.

- $200,000 for single and all other taxpayers.

Related: The Best Time To Take Social Security

The Positives Of Higher Payroll Taxes

It's important to always look at the bright side of higher Social Security and Medicare taxes.

1) The more taxes we pay in, the higher the chance we'll actually receive the full amount of Social Security and Medicare promised to us. Hopefully most of us have already completely written off any sort of Social Security benefits by the time we reach our 60s and 70s. It's always good to have low expectations of government promises.

2) We insure that more working people pitch in to pay for our great country. It's very hard to avoid payroll taxes. Yes, if you do the math, 173 million workers who will pay payroll taxes equals only 54% of the estimated 319 million people in the United States. But 54% of the nation paying taxes is better than a sharp stick in the eye! The other 46% of the population are too young, too sick, too poor, too unwilling, or too old.

3) The government controls more people by making them afraid of becoming free thinkers who are independently wealthy. Why do you think the first thing Chairman Mao and Fidel Castro did when they got into power was confiscate land from the wealthy and send them to farm?

Having to pay 7.65% in payroll taxes as a laborer is already painful. To pay 15.3% in payroll taxes as an entrepreneur is oppressive. The less people realize the massive upside of being an entrepreneur, the less people will threaten government.

4) Higher taxes encourage people to make a whole lot more than $132,900 to get a “bargain” on every incremental dollar earned. The tax cuts that went into effect in 2018 have practically abolished the marriage penalty tax, eliminated the top 39.6% tax bracket, and raised the income threshold for the highest 37% marginal tax rate. The only problem is that SALT deductions have been limited to $10,000, which is a blow to expensive coastal city inhabitants.

Ways To Counteract Higher Payroll Taxes

Now that you realize Social Security is kind of a rip off, you should understand the income types not subject to Social Security tax. This way, you can save money.

If you're stuck in the rat race, there's really no way around paying Social Security and Medicare taxes. If you're earning close to the maximum income of $142,800 subjected to Social Security taxes, it's not like you're going to tell your boss to give you a pay cut.

Instead, you're going to continue kissing butt in hopes of getting that amazing 3% pay raise next year just so you can afford to pay for the tax hike!

If you're self-employed, you've got more flexibility. You could choose to pay yourself a lower wage and give yourself more in distributions, which aren't subject to payroll taxes. For example, let's say you brought home $200,000 in operating profits (revenue – operating expenses) before taxes.

You could theoretically pay yourself $30,000 in wages and give yourself a $170,000 distribution so you're only paying $4,590 in Social Security and Medicare taxes ($30,000 X 15.3%) versus taking home $200,000 in wages and $0 in distributions and having to pay $15,772.80 SS ($127,200 X 12.4%) + $5,800 Medicare ($200,000 X 2.9%) = $21,572.80. That's a huge $16,982.80 in tax savings!

The Self-Employed Pay More Taxes Than W-2 Employees

If the $200,000 entrepreneur was a W2 employee instead of being self-employed, his/her tax bill would be $7,886.4 SS ($132,900 X 6.2%) + $2,900 Medicare ($200,000 X 1.45%) = $11,40. So it's hard to call $16,982.80 a complete “savings.”

The risk of paying only 15% of your operating profits as a salary is that you might get audited. How much an entrepreneur with an S-Corp can pay himself in income and distributions is a gray area. I've argued for a ratio of no greater than 50/50.

Finally, the absolute best way to counteract ever-rising payroll taxes is to simply earn income that is NOT subject to payroll taxes! What types of income are not subject to payroll taxes? Here's a list.

Investment Income Not Subject To Payroll Taxes (FICA Taxes)

Here are the Income Types Not Subject To Social Security Tax:

- Dividend income

- Rental income

- Venture debt income

- Private equity income

- P2P income

- CD interest income

- Capital gains

- Student income, ministerial income, exempt wage income

- Real estate crowdsourcing income – I've personally invested $810,000 in real estate crowdfunding to invest in lower valuation, higher net rental yield properties across the heartland of America. There is a multi-decade trend of workers and companies moving away from the expensive coasts thanks to technology and the rise of remote work.

Tax Cuts For The Middle Class And Retirees In 2025 And Beyond

Thankfully, the Trump administration has proposed tax cuts for middle class and retirees. It wants to eliminate tax on Social Security benefits, overtime, and tips. That's huge for the typical American. Here are the list of tax cuts proposed:

- No tax on tips

- No tax on Social Security benefits for seniors

- No tax on overtime pay

- Renewing the Trump Tax Cuts from the 2017 Tax Cuts and Jobs Act

- Adjusting the SALT cap

- Eliminating special tax breaks for billionaire sports team owners

- Closing the carried interest loophole for hedge fund managers

- Tax cuts for Made in America products

On July 4, 2025, The One Big Beautiful Bill Act passed and will provide tax relief for millions of Americans. It extends the 2017 Tax Cuts and Jobs Act and raises the SALT cap deduction limit from $10,000 to $40,000. Hooray!

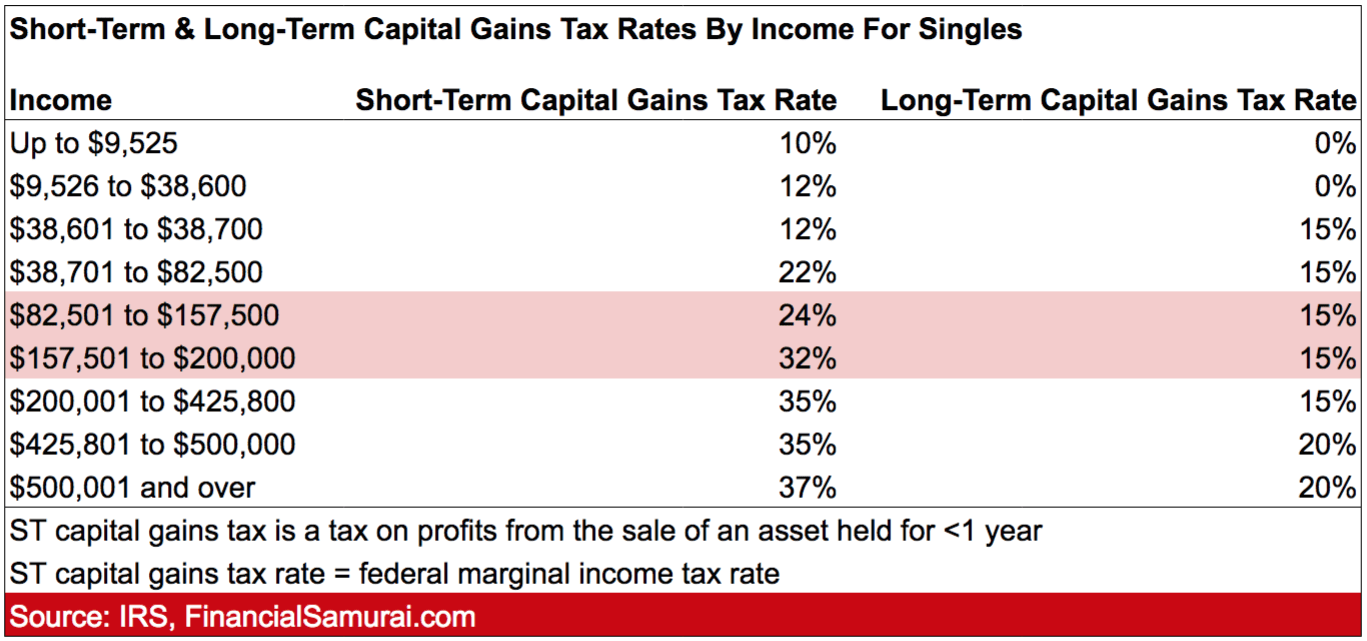

Capital Gains Tax Rates

What's also good about investment income is that you may get some tax breaks on income and capital gains. The tax rate on long-term (more than one year) gains is 15%, except for high-income taxpayers ($400,000 for singles, $450,000 for married couples) who must pay 20%. High-rate taxpayers will typically pay the healthcare surtax as well, for an all-in rate of 23.8%.

Qualified dividends have a tax rate of 15%. Meanwhile, there are no federal taxes due on income produced by municipal bonds. For those who invest in their own state's municipal bonds, there isn't state income tax due either.

Knowing the government will never efficiently manage other people's money, I started building a passive income portfolio in 2000 so I could have more of my money back. As soon as you can make enough passive income to cover all your living expenses, you are not only free to do whatever you want, you're also free of the 7.65% payroll tax for employees and 15.3% payroll tax for the self-employed!

Wealth Is More Important Than Income

Because the government is always going after income, wealth is much more important for financial freedom. For example, you could be worth $10,000,000, the ideal net worth for retirement, and not have to pay payroll taxes or income taxes since you can live off your investments.

You could also partake in subsidized healthcare under the Affordable Care Act. Further, your kids could get 100% of their college tuition paid for by universities given they determine grants by income and not by wealth.

The more you work, the more you have to pay in taxes. Instead, work smarter by focusing on building more investment income or equity in a business, especially as corporate taxes are getting cut. You can build wealth up to $13.61 million as an individual or $27.22 million as a married couple before the estate tax kicks in in 2024. It changes every year.

From now on, really think about how all your income sources are taxed. Do you really want to work all day for the privilege of paying federal income tax, state income tax, city income tax, Social Security tax, Medicare tax, and so forth? Just like inflation, tax increases will never end.

If you are starting to make a high income, I'd strongly consider trying to relocate to one of the nine states with no income taxes. For example, if you make $500,000 a year and relocate from California to Nevada, you save over $40,000 a year in state income taxes. Now that sounds worth it to me!

Free Financial Analysis Offer From Empower

If you have over $100,000 in investable assets—whether in savings, taxable accounts, 401(k)s, or IRAs—you can get a free financial check-up from an Empower financial professional by signing up here. It’s a no-obligation way to have a seasoned expert, who builds and analyzes portfolios for a living, review your finances.

A fresh set of eyes could uncover hidden fees, inefficient allocations, or opportunities to optimize—giving you greater clarity and confidence in your financial plan. Empower helps their clients optimize on their taxes as well.

The statement is provided to you by Financial Samurai (“Promoter”) who has entered into a written referral agreement with Empower Advisory Group, LLC (“EAG”).

Earn More Passive Income Through Real Estate And Venture

Stocks and bonds are classic staples for retirement investing. However, I also suggest diversifying into real estate—an investment that combines the income stability of bonds with greater upside potential.

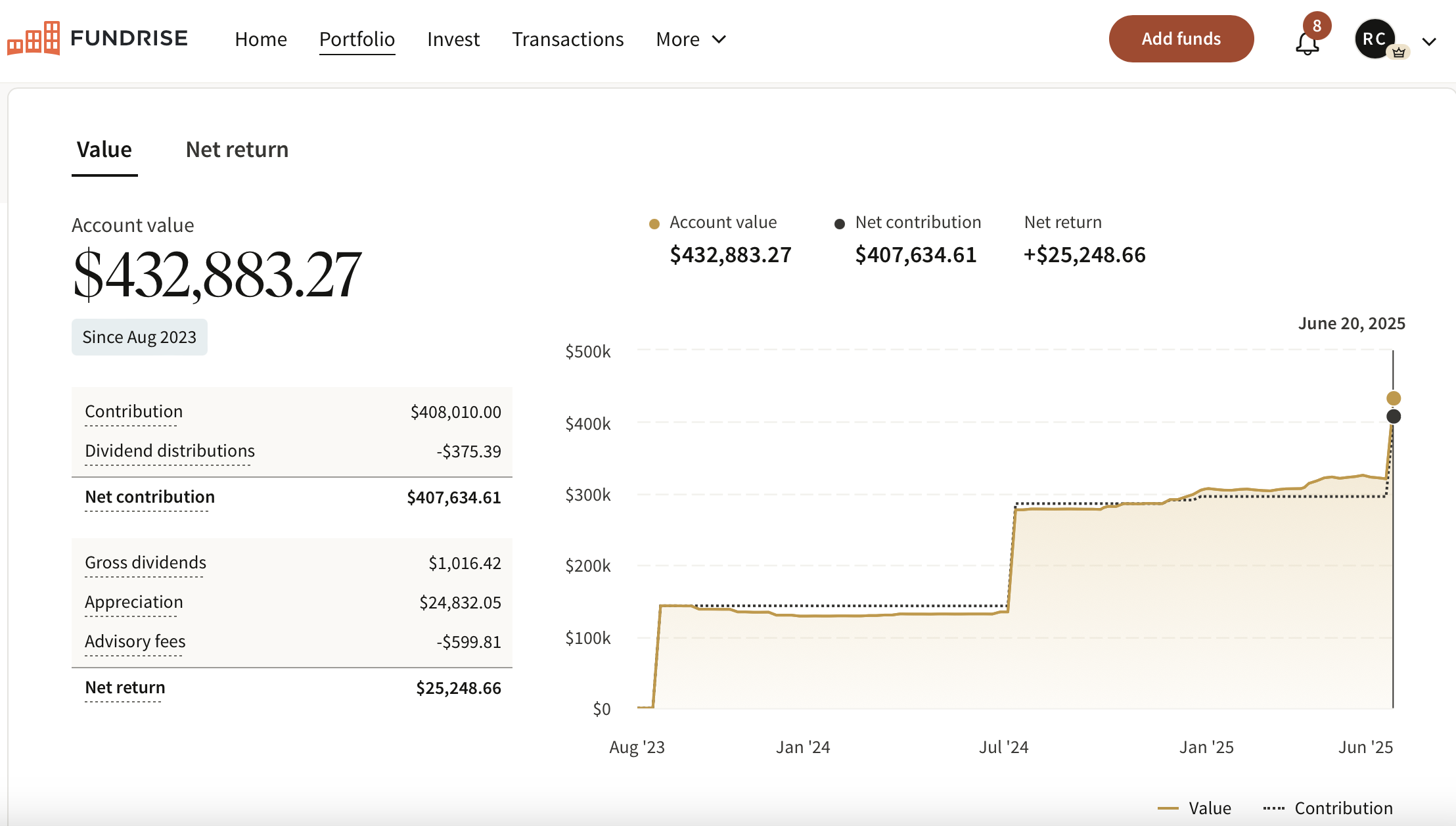

Consider Fundrise, a platform that allows you to 100% passively invest in residential and industrial real estate. With over $3 billion in private real estate assets under management, Fundrise focuses on properties in the Sunbelt region, where valuations are lower, and yields tend to be higher. As the Federal Reserve embarks on a multi-year interest rate cut cycle, real estate demand is poised to grow in the coming years.

In addition, you can invest in Fundrise Venture if you want exposure to private AI companies like OpenAI, Anthropic, Anduril, and Databricks. AI is set to revolutionize the labor market, eliminate jobs, and significantly boost productivity. We're still in the early stages of the AI revolution, and I want to ensure I have enough exposure—not just for myself, but for my children’s future as well.

I’ve invested over $400,000 with Fundrise, and they’ve been a trusted partner and long-time sponsor of Financial Samurai. With a $10 investment minimum, diversifying your portfolio has never been easier.

Subscribe To Financial Samurai

To increase your chances of achieving financial independence, join 60,000+ readers and subscribe to my free Financial Samurai newsletter here. Financial Samurai began in 2009 and is the leading independently-owned personal finance site today. Everything is written based off firsthand experience.

Income Types Not Subject To Social Security Tax is a Financial Samurai original post.

Husband and wife are flipping houses. What deductions for income tax can we claim? Can we claim our own labor for the work we have done in the house?

suppose instead of working for an S-Corp, you work for a C-Corp. there are any number of executives (Steve Jobs was one) who paid themselves $1 a year. So all the work you do becomes corporate profits instead of wages. Under the new tax law, that means you pay 21% Federal taxes.

As I recall, the first 90k or so of dividend payments are tax free for married low-income workers. If you lived in an income-tax-Free State, this would mean that, on corporate income of about $115,000, you’d pay the Feds about 24k in total taxes. Run some numbers through TurboTax and check it.

Pros should look up Subchapter T.

A bill being considered before the House Ways & Means committee right now proposes to hike the social security tax significantly by (1) increasing the total burden from 12.4% to 14.8% and (2) subjecting high earner wages to the SS tax for all wages in excess of $400,000. The second one will put a lot more pressure on the meaning of “reasonable compensation” when using the S-Corp tax savings strategy!

When my S corp’s earnings were growing quickly, I had to figure out the magic annual salary where individual 401k employee and employer’s were maxed out relative to employee and employer social security “contributions.” That annual salary was $60,000. I was previously paying myself $160k and contributing $40k to a SEP IRA. With $60k, I could contribute $15k as an employee and $15k as an employer. I believe the wages cap was $92,000 at that time. It would be interesting to re-do that analysis now with a higher cap.

Well done. So important for people to understand that paying into the social IN-security program is voluntarily and can be avoided by the type of income in which you obtain. This is a very strange thing the government did. I have to wonder why they did it. Is it because they believe that a person who has a job rather than being an independent self employed person is less likely to need social security? I retired at the age of 46 with enough rental income to meet our nut, but I live in Orlando Florida. When I tell people I no longer pay social security or medicare taxes, most people don’t understand it. It is sad we have become so uneducated in the United States on the nature of reality that we just accept slavery voluntarily to the US government.

A majority of people can’t afford to live off rental income.

Diversifying into more tax efficient investments would still be beneficial, though.

I think it would be a mistake to assume you have to live entirely off of one, or even multiple, “tax efficient” income source(s). I think the takeaway message from this article is to spread your income sources out into more tax efficient vehicles to reduce your overall tax burden and expedite your financial independence.

congrats on the early retirement!

if you stop working at 46 how does that affect the your social secuirty benefit? will you get a lower monthly SS payment when you start collecting. I was under the assumption you need to work like 30 years to get the max payout

Maybe I can get some advice from readers. I am 46 years old. I retire from the Army next Aug. My retirement pay will be 3500/month (before taxes) and is not subject to FICA tax. My disability will be another 3600/month all tax free. I own 8 rental properties that generate 6400/month after expenses which is also not subject to FICA and with depreciation, makes the tax impact negligible. My take home pay now is 8700/month with an additional 15k per year bonus. My son is using my GI bill which pays me his BAH living expense of $10,400/yr (I get paid for my son to go to college!). I will go back to work as a physician assistant in the civilian sector overseas on a one year contract making 13.4k/month. My monthly living expenses are 6K/month including a 2k/month mortgage (small farm with 20 acres). I have 100k in physical gold/silver that doesn’t earn squat. I have not invested in any stocks, bonds, or 401Ks due to piling everything into getting my rental properties paid in full. I plan on purchasing 2 more rental properties upon return from the contract for a total of 10.

Here is the question, at that point, I will have $16k/month in passive income with no FICA taxes and negligible income taxes. I don’t have health care costs due to military retirement. What should I be doing now as far as other investments such as stocks, bonds, TSP, 401K that would make more sense than my current plan or in addition to it? Once my house is paid off, my monthly living expenses will only be 4K. Smart people here so I appreciate any feedback.

Focus on acquiring more cash flow rental properties for the long haul.

The stock market will be heading south fairly soon, maybe buy into it after it goes down 15%.

Hey Sam, this is by far the most detailed post I’ve ever seen on payroll taxes. I love that you not only explain what they are, but also how to avoid them by earning income sources that are immune to FICA! What I found especially intriguing is that the US Gov. elected to raise the income taxed by social security by much more than the rate of inflation. My guess is that they are choosing to tax the wealthier more and leave people who make less than 120K alone. To be honest though, I think this trend will continue, and FICA taxes will not only cover a larger range, but will also take a larger % of your income. The best thing we can all do right now is switch our income sources so that we can keep more of it for ourselves.

Thanks for the great article!

Yes I plan on building dividend, municipal bond, and rental income to reach FI in 8 years. I hope the IRS will make no changes to that type of income in the tax code. You make 200K in passive income and still work or are you FI?

Still work by writing content on Financial Samurai and doing some occassional corporate and private 1X1 consulting. My ideal number of hours to work to week is around 15-20.

It’s really fun working when you don’t have to work!

One thing I’ll never understand is the fixation most people have on gross income rather than after-tax income.

Depending on:

– which country you live in;

– what tax breaks you are able to utilise;

– how you earn your money; and

– the split of income from you and from your partner,

The amount which hits your bank account can vary widely.

Vanity asside, it is only really the money that actually hits your bank account which is even remotely relevant!

I’m still figuring out what business expenses I want to undertake in December rather than January for efficient tax-planning. I need to save some write-offs for 2017 because that will be the year I hopefully switch to FT at my personal business. Controlling my AGI will be imperative.

There was a research study done by economists showing that the per capita G.D.P. has grown by almost twice of what it was in the 1980’s but the average American hasn’t benefitted from G.D.P. growth because the wealth has gone disproportionately to the affluent. I say, if you can’t win, then join them. Invest in the companies that are doing well and take your share through dividends and like FS mentioned, you won’t have to pay payroll taxes on the earnings.

The New York Times wrote an article on the study: https://www.nytimes.com/2016/12/08/opinion/the-american-dream-quantified-at-last.html?emc=edit_ty_20161209&nl=opinion-today&nlid=70074107&te=1&_r=0

So most people want to pay less taxes. What else is new?

Take a look at USA total share of GDP paid in taxes versus other developed countries and you will see we are at the low end. Given that, the logical discussion is who pays what share, not lowering the total.

My personal view on this is corp and wealthy America have snookered everyone into making their share lower than it used to be and frankly I think their share should increase. But reasonable people can disagree on that.

There is really no debate that the corporate contribution has been cut dramatically for several decades, and that the 0.1-0.01% have as well. They just prefer we not mention it.

Luckily I have a gov job that has a great pension program, and I max out my 457(b) plan (18k a year) but I”m trying to find the right timing to get into the double tax free VCIX fund. I”m

typo VCITX. Was going to try to build that up, but at only 3% dividend payback, I’d have to have a huge golden egg to have that make it worthwhile. Was going to try and wait until interest rates jumped up even more to buy the fund at a low low price, or dump everything extra into a high yield vanguard dividend fund. When I retire I’ll have my pension plus my 457(b), plus any passive income streams i’m able to come up with. Currently trying out realtyshares and lendingclub. So far happy with both but I’m having trouble focusing on which to build up higher faster. Also started my own website to see if I can build some more passive income (readysetfive-0.com). Thanks for your blog, learning a lot every time I come here.

This topic has been on my mind this week as well with the increase in the Social Security tax cap and essentially getting a pay cut for 2017. I just actually posted this morning about how most Americans, including myself, are actually paying MORE in FICA taxes than they are in Federal income taxes.

I don’t believe that most Americans pay too much in federal income tax, I think most pay too little and aren’t covering their portion of defense, education, infrastructure (etc, etc) costs. Everyone’s so focused on the federal tax rates being “so high” that they don’t actually know what percentage they are paying in reality if they were to look at their tax return and compare it to their gross income.

I DO believe millennials are currently paying too much for FICA taxes because our future benefit is very uncertain. I personally will be taking many of your suggestions to increase passive income and gain the benefit from decreased FICA taxes as well as more favorable federal tax rates.

Great post, I touched on some of the same topics in my post about SS tax this past October. As some others commented it is essentially forced saving on the working class, which has positives and negatives but the doubling of the tax for entrepreneurs is just not fair. It creates a huge incentive to build up passive income through wealth as you pointed out.

For the gentleman who lost his $5000 a month annuity, my understanding is that insurance company annuities may be backed by the state depending on where you live. In New York the state guarantees them which gives the state reason to highly regulate the insurance companies. One strategy people have suggested is to buy a long term bond of an insurance company instead of an annuity because you get the same counterparts risk but with a likely higher return if held to maturity. Just a thought for the long term planning types.

Sam,

You stated “Further, your kids could get 100% of their college tuition paid for by universities given they determine grants by income and not by wealth.”

As a professor with college age kids, I can tell you that income AND wealth are taken into account when determining financial aid at most universities and colleges in the US. While there are scholarships (mostly merit-based) that do not take ability to pay into account, need-based financial aid, Pell grants, and student loans generally rely on the FAFSA (https://fafsa.ed.gov/) to determine an Expected Family Contribution or EFC. A higher EFC means that you will offered less (or no) need-based financial aid. The FAFSA determines your income from your Federal Tax Return and also requires the disclosure of assets not including the equity your primary residence or retirement savings. Assets in the students name count more when calculating the EFC. There are plenty of online calculators that will estimate your EFC (e.g., .

There are games to play to manipulate the EFC to be lower, but it requires multi-year planning. Under a recent rule change, your Federal Income Tax return filed during your child’s junior year in high school will be used in the EFC calculation for his/her freshman year of college. And, in most cases, to continue to qualify for need-based financial aid, you must submit a new FAFSA each year that your child is in college. Additionally, keeping most (or all) of your assets as equity in your primary residence or in retirement plans can substantially reduce your EFC, but for FI/RE folks, this may be challenging.

As a professor, don’t professor’s kids get to attend your university for free? My friend went to Georgetown U for free. Lucky guy. Now he’s an ortho surgeon.

Is it not much easier to manipulate/hide wealth than income? Income is always reported to your name, unless you earn cash.

But yes, start making less income 2-3 years BEFORE college dear parents! Be wealthy, earn poorly.

My kids get free tuition if they choose to attend the where I work. Unfortunately, my kids want to be engineers and I teach at a liberal arts university. There are programs that can get free tuition with other universities, but the number of available slots is rather limited.

The only ways I have found to legally “hide” wealth wrt to FAFSA is as equity in your home, cash value of life insurance (not generally a good investment), in retirement plans or a family business. 529b’s, brokerage accounts, savings accounts, vacation homes, rental properties, etc. must all be declared as assets. N.B. While a family business may be excluded if it meet certain legal requirements, rental properties cannot be treated as small business ).

A couple good articles for those interested in this topic (as well as other details about how colleges determine need-based financial aid): https://www.forbes.com/sites/troyonink/2014/02/14/how-assets-hurt-college-aid-eligibility-on-fafsa-and-css-profile/#54fd4e2453bb

https://www.forbes.com/sites/troyonink/2014/11/04/consumers-beware-the-truth-about-life-insurance-annuities-and-college-financial-aid/#130116373ead

The bottom line is exactly what you stated–start preparing well before you kid(s) are college age.

It’s tough to avoid those payroll taxes. I know that with my own little side hustles, I save the entirety of that income into a Solo 401k, which saves me at least 30% in marginal taxes, but I can’t seem to avoid that ~15% SE taxes, which is a bit of a bummer. But I do like being able to save that extra money away.

I do pull in some solid rental income by renting out my guest room on Airbnb, and it’s nice to not have to pay the SE taxes on it, but then I’m stuck paying a high marginal tax rate on that income. I can’t really think of any way to get that money into a tax deferred account. Would almost prefer having the Airbnb income as 1099 income that I could put into a Solo 401k, even if I had to pay the SE taxes on it.

Any ideas on how I can reduce my tax liability on that Airbnb income?

I haven’t ventured into Airbnb yet b/c I’m afraid of the occassional ax murderer. Also, SF is totally clamping down and want all this information about the host. It’s MORE BIG BROTHER that I don’t want. I already experienced that w/ Uber when Uber leaked all our information to the city, which turned around and required us to pay a $91 registration fee or else face fines.

Is it really true your kids can go to college for free even if your net worth is 10 million? with no income??

I am 30 now… I plan to have kids in a few years, so when I’m around 48 years old I should make sure my income taxes are near zero so they can go to school for free. That is very interesting…

Yes. Here’s a blurb from Stanford’s financial aid site. The income hurdles will obviously change (go up) in the future due to inflation. It’s all about INCOME not WEALTH.

Zero Parent Contribution for Parents with Income Below $65,000

For parents with total annual income below $65,000 and typical assets for this income range, Stanford will not expect a parent contribution toward educational costs. Students will still be expected to contribute toward their own expenses from their summer income, part-time work during the school year, and their own savings.

Tuition Charges Covered for Parents with Income Below $125,000

For parents with total annual income below $125,000 and typical assets for this income range, the expected parent contribution will be low enough to ensure that all tuition charges are covered with need-based scholarship, federal and state grants, and/or outside scholarship funds.

Families with incomes at higher levels (typically up to $225,000) may also qualify for assistance, especially if more than one family member is enrolled in college. We encourage any family concerned about the ability to pay for a Stanford education to complete the application process. If we are not able to offer need-based scholarship funds we will recommend available loan programs.

These levels have been set based on typical cost of living in the United States. These same levels may not apply to families living outside of the United States; aid eligibility will be determined based on individual family financial circumstances.

“…and typical assets for this income range” makes me think that they look at your net worth as well. Seems that $10MM wouldn’t qualify as “typical” for somebody earning no income…

The key is, they will never know you have 10 million because there are plenty of ways to hide your wealth. It’s income that’s hard to hide.

Hi Sam,

Only about 50% of Stanford undergrads receive need-based financial aid. The rest are supposedly on athletic scholarships or are paying full fare.

Stanford does take into account “your family’s assets, including home equity, savings, investments and real estate, but not retirement accounts.”

https://financialaid.stanford.edu/undergrad/how/parent.html

So, if you hid your wealth well enough that it wouldn’t show up in these categories (or you simply weren’t truthful on the form), you could get a full ride. But it seems that about 50% of Stanford’s students receive no need-based aid so those families are failing to hide their wealth well enough.

Regardless, if you have enough wealth to hide it well, I’d hope you’d be willing to invest 70k/year into your child’s education.

Hi Sam

Off topic from this post but based on your Venture debt investing posts, I decided to contact a few firms that may be currently raising funds. Can you share your due diligence process when you invested in venture debt? it’s an entirely new concept for me and I would like to know how you did your due diligence. The company i am looking at is Trinity Capital Investment. Thank you!

Completely agree Sam … which is exactly why I focused on building income from stocks, REITs, bonds, and preferred shares.

Why work harder just to get taxed more? Work smarter! Earn income from places taxed at lower rates!

Great idea about earning via distributions instead of self employment income…but why not pay yourself only $1 and then “distribute” the rest? I suspect there’s bound to be limits on how this is done.

It’s a nice idea in theory to pay all but $1 of your operating profits in the form of distribution. I’m sure there are business owners who do that, but it’s a red flag. The IRS says you have to pay yourself a “reasonable salary” you would pay someone else to do the job and generate that income. So at the very least, you’ll probably have to pay 70% of the median income of such a job.

Once you get to bigger operating profit numbers, there’s really no escape. But there’s also safety too b/c let’s say you make $1,000,000 in operating profits. If you pay yourself a $127,200 salary, the IRS gets MAX Social Security tax from you, so what do they care if you pay yourself a $872,800 distribution. But there is Medicare tax you get to avoid.

Check out: What’s The Right Ratio Of Salary And Distribution To Avoid An Audit

Hi Sam,

That is the exact strategy my accountant has me follow. Whatever the SS cap is, that’s how much I make that year. The rest is distributions. I could probably pay myself a little less and take more distributions but feel its just not worth risking an audit to save a couple grand a year.

Thanks, Bill

Great post on the benefits of creating more passive income. Especially investment income since it’s taxed at a more favorable rate in addition to not being subject to payroll taxes.

I also love the line “It’s always good to have low expectations of government promises” in regards to social security. Although I believe it will still be around when I’m old enough to take it, I’m not counting on it at all. If it’s there, great. If not, no big deal. Just count it as another generous contribution to the government.

I am concerned about the potential for a wealth tax down the road, this is one reason why the hype around the shift to a cashless, digital currency that is NOT P2P / blockchain-based / decentralized but instead centralized / transaction traceable is such a scary proposition. Another risk is the form of a property tax rate increase here in CA, although fortunately there are a lot of real estate rich blue state liberals who may oppose this since they want to fund all these programs accessible to the entire world’s citizenry with other people’s money – i.e. Republicans. However, all these unfunded pension obligations for stressed out government workers like the janitors making $276k are certainly not going to pay for themselves.

Maybe a solution is to spend all of one’s wealth before death! Then, who can take anything away anymore?

I think it will be pretty cool to see the BART train service workers start reporting $350,000 – $500,000 a year incomes. At the end of the day, everything gets normalized.

Nobody in SF cares how much anybody makes for what type of job they do. One love!

As a high wage earner, I’d actually be fine with the government taxing ALL income (wages, capital gains, dividends, etc.) for Social Security/Medicare, particularly if doing so (a) drastically improved the solvency of the programs, and/or (b) cuts could be made to the rates to make them more progressive. As of now, they are an incredibly regressive tax (if you’re making more than $127k, you pay 0% on anything above that amount, whereas someone who’s supporting a family on $40k a year has every penny they earn taxed for Social Security/Medicare), and the safety net of Social Security/Medicare are INCREDIBLY important.

We often talk about how 47% of Americans pay no income tax….but we ignore the fact that many of those 47% pay Social Security/Medicare taxes (which are by far the biggest government outlays), and the fact that the rich (i.e. anyone who makes more than $127k in wages, or who makes millions in non-wages) pay ZERO (or zero on anything they earn above $127k) for Social Security/Medicare.

Its a very progressive tax. Those that paid the least get the most, its the definition of progressive.

Not sure if you remember that if you make any more than 127k then federal/state brackets start to rise rather dramatically as well, and you will pay a significant amount of taxes period. Its not as if taxes just magically disappear above this point. Just the SS tax, and it should as those people contributing are basically subsidizing those who will receive it. The max payout is low enough you’re unlikely to recoup what you even put in, let alone the opportunity cost, and there are phaseouts. You’re doing a service, which is fine, but dont get crazy and try to fully pay for someone elses safety net dollar for dollar from someone elses pay.

SS is not that hard to fix, and will probably be totally fine with very minor adjustments or simple demographics. You’re requiring zero thought from your legislators and politicians and far too comfortable with doing the lazy thing and just taking from others. Those in higher brackets are the most able to adjust their working hours/income to outside factors and I guarantee people would be less productive if that were the case.

Many of those people who dont make enough money to pay much in taxes get some back at the end of year, and some even get more than they would have been liable for by way of credits, etc…

It’s not progressive at all. Poorer workers pay a greater proportion of their income in Social Security taxes than richer workers — i.e. if you make over $127k in your job, you are paying less than 7.85% or whatever of your income in Social Security taxes.

Yes, richer workers keep paying taxes about $127k, but you can’t have your cake (segment off SS taxes to its own world as “progressive” since those who pay the least get the most) and eat it too (segment all other taxes off as their own thing apart from Social Security). Ideally, ALL taxes would be progressive (i.e. the richer you are, the higher a percentage you pay) including Social Security taxes (and, for that matter, dividends/capital gains taxes, etc…..I’d just treat all income as income, regardless of source, and tax it progressively).

And there is ZERO proof that tax rates play much if any role in individual determinations of how productive someone is going to be or how much they earn — I’m not going to give up earning an extra hundred thousand dollars if I get to keep, say, 55% of it vs. 61% of it. I’m still up $55k, which is better for my wealth/financial picture in the long run.

I get what you’re trying to say, but they receive a benefit that is disproportionate to their contribution, so very hard to be regressive on net, as on whole. Not simply compared to their income. Especially after considering actual net taxes paid which is low for the majority. Its basically a strawman argument to attempt to divorce the payroll tax from overall tax burden and effective overall rates.

Define poorer, then show what they actually pay overall in effective taxes. The median income in the US is about 52k. Many many people make far less than the median, and even though SS taxes are collected, many get a partial or even full to over 100% of their taxes returned so they have a negative tax rate. The bottom 20% have a negative tax rate, its the definition of progressive, no matter how you slice it. You can argue its your opinion its not progressive enough, but its not regressive.

We even have data for all this of course. For all workers/returns less than 50k, the effective average tax rate was 4.3%, this comprises 63% of all returns. I dont think that is an onerous rate or could be described as “regressive” at all. Higher income filers are also more likely to be self employed and pay 15.3% up to the limit, which is most people.

There is not zero proof of that, just look at any finance forum, people do less than they can at top rates for just that reason. In reagans large cuts from 91% marginal they did show an increase in amounts earned which showed there could definitely be suppression of productivity. Now, Im not arguing the marginal rate needs to be reduced or anything, as we are not anywhere near that kind of context anymore, nor as progressive as then. The debate is not about is it progressive or not, but is it enough and what are the effects? You have to balance productivity and receipts, incentives, and how it affects inequality. These are separate but important issues. Everyone here seems focused on the working rich, when its really the 0.01% that have had the largest tax breaks (from 74 to 34 effective).

As for the disincentive to work, unless one has a spending problem I (and many people I know as well) have no desire to work beyond what I can keep my effective tax rate around 35%. After maxing out all my retirement and tax advantaged space I’d simply rather spend time with my family than wander into the 60% marginal rates (Cali). No thanks, I dont need it and enjoy time with the family. Sometimes Im thankful for the rates so that I do not just become a crazy workaholic and enjoy life, and Im certainly not the only one.

Im also not against paying my fair share or really care that I wont even come close to getting a return on SS, its my patriotic duty and its fine. However, when people say “its not progressive at all” its really annoying and has to be brought back to reality. It may not be perfect, but unless you talk about things in a real way you arent doing your particular sides point any good.

Social security payouts are HEAVILY subsidized by middle class and wealthy taxpayers. Low income earners get back way more than they pay taxes for.

There are 3 income bands that are taxed.

In the first, lowest $ earner band, people receive 90% of their monthly income.

In the middle $ earner band above that, people receive 32% of their monthly income in that band.

They only get credit for 32%! Where does the 90%-32% = 58% go? It goes to subsidize low income earners.

In the high $ earner band above that, people receive about 15% of their monthly income in that band.

15%!!! Where does the 90% – 15% = 75% go? It goes to subsidize low income earners.

And now you want to tax high earners EVEN MORE? How is that fair?

Isn’t a 75% tax on their high income contributions high enough? 75%!

Here’s a link from Social Security that explains exactly how to go about calculating benefits. https://www.ssa.gov/pubs/EN-05-10070.pdf

I don’t follow you at all!! Mitt Romney had an effective tax rate of of around 12%, that means he got 88% to play with. As for S.S. Lets take your 127,000 cap wage at 7% for ease (127,000 * .07 = $8,890) say you paid that for 40 yrs. = 8890 * 40 = $355,600 then lets say you retired for 30 yrs. 355,600 / 30 = 11,853 / 12 = $988 mo. and using your S.S. calculator I am sure you will find that you will get 3 times that amount per month. So even large income individuals come out doing very well. And yes there is the opportunity to loss it all if you didn’t have S.S.

Hi Sam,

Great advice! This makes me wonder if I should not maximize my 401k contribution and instead take some money each pp to purchase dividend & interest paying investments to build up more passive income for 2017.

Always max out your 401k contribution and then invest extra money after. The key is to make it a habit and live within your remaining income.

Related: How Much Should I Have In My 401k By Age?

Can’t say I see myself every applying for a government job, no matter the benefits. My plan is to work hard, efficiently, save and then retire early. Accumulate wealth young, let it compound and then wipe out most of my income taxes. As you stated, live off my investments.