The definition of a middle class lifestyle has been consistent for over 50 years. Yet, for some reason, there is still debate on what consists of being middle class. Being middle class isn't about how much money you make. Being middle class is about what type of lifestyle your money can afford.

Whenever I publish posts with six figure household incomes and detailed expenses my comments section and social media light up with displeasure.

Instead of accepting the fact that higher income leads to higher taxes and that living in large metropolitan areas result in higher expenses than in less densely populated parts of the country, there is denial.

There's also a segment of people who display hatred for high income earners. It's as if living in a three bedroom house and wanting to eat healthier in order to be around to see their children grow up is an affront to their way of life.

Pushback Against Middle Class Definitions

Based on my observations, here are the types of people most outraged by others paying a lot of taxes while also trying to raise kids and save for retirement in an expensive city:

- People who don't live in an expensive coastal city.

- People who don't have kids.

- Students who haven't even gotten a job yet.

- People who see a $1.5M house price tag and scoff, but don't understand that if the median house price is $1.5M, then the house is quite average.

- People who work 40 hours a week or less and think they should be far ahead of the game compared to their peers who work 60 hours a week or more.

- People who are too afraid to make a change in their career or are too afraid to move for an opportunity.

- People who don't tell the full story of how they make ends meet e.g. a reader claims to save $200K on a 300K income without explaining his taxes and housing situation.

- People who have a tendency to discriminate against others, otherwise, they would be more accepting of other people's situations.

- People who feel their reality is the only reality that counts.

What the heck is going on folks?! It’s OK to be skeptical and disagree, but to hate is unbecoming.

If you are easily triggered in a personal finance context, I've got a solution for you. Focus on achieving equality instead of being mesmerized by the numbers.

A Middle Class LIFESTYLE Is All We Want

People who see others making $200,000, $300,000, and $500,000 a year are too caught up in the numbers. Instead, focus on the lifestyle.

If a household making $300,000 in New York City is living the same lifestyle as a household making $80,000 living in Des Moines, Iowa, why are the two any different?

There is no hate against the $80,000 household living in the Midwest. So why is there hate directed at the $300,000 household who is stuck living in New York City due to their jobs?

We've been fighting discrimination in America since the Civil War folks. Is there any wonder why Stealth Wealth is alive and well? Let's be more accepting of others.

Middle Class Income And Middle Class House

We all know what a middle class INCOME is. That's easy to find out from the government. The median household income is roughly $75,000 in 2024. Therefore, if you make +/- 50% of $75,000, or $37,500 to $112,500, you have a middle-class income.

The median home price in America is ~$420,000. Therefore, if you make +/-% 50% of the median home price, or $200,000 – $600,000, you likely own a middle-class home. Obviously, you want to take the median income and median home price of your city to get a better idea of whether you are middle class or not.

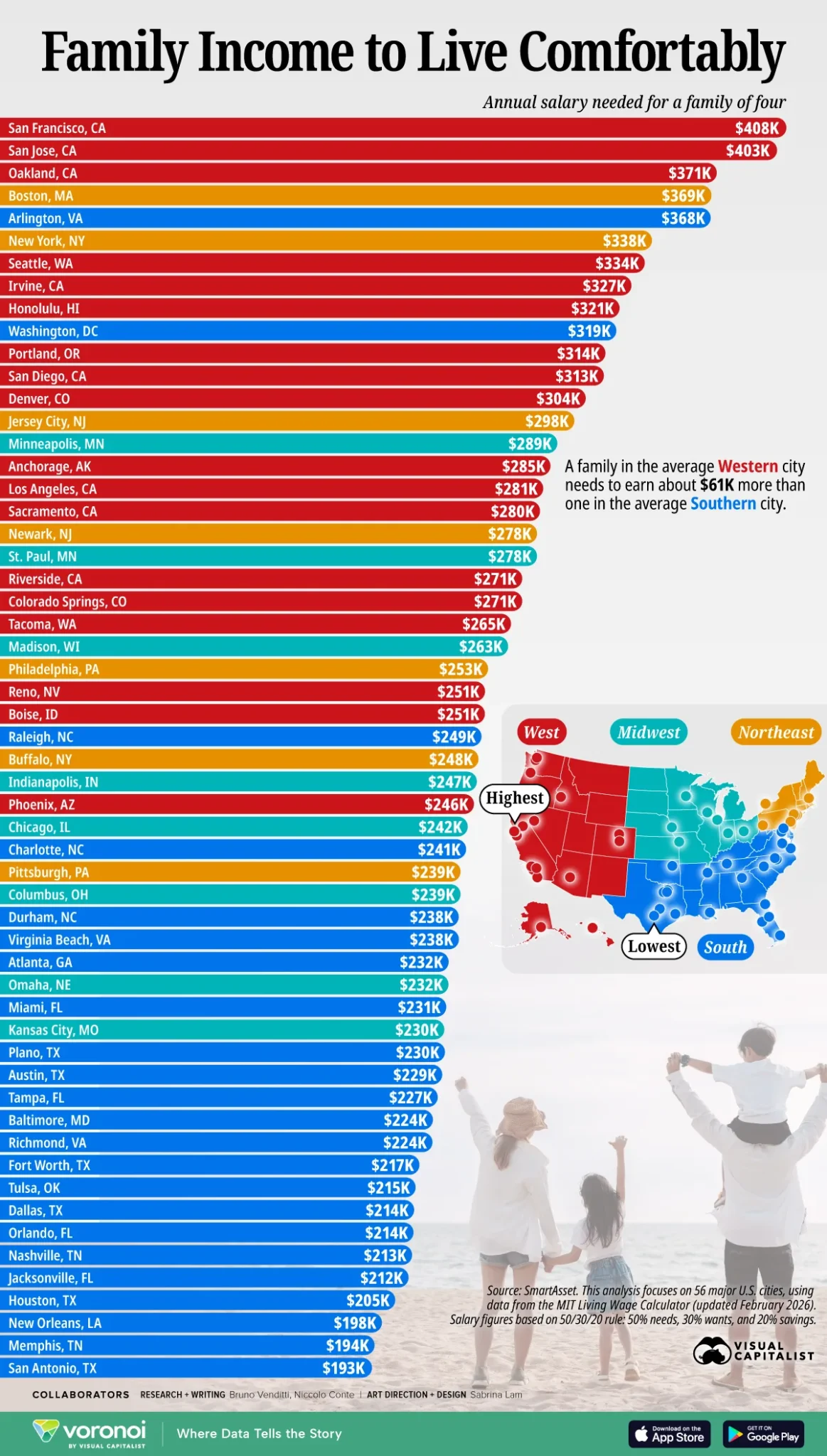

The below chart defines five social classes by 2014 incomes from the Urban Institute. Thanks to inflation, you should add 25% to every income figure.

Notice how the Urban Institute says a family of three who earns up to $349,999 are still considered middle class? And that was in 2014! Now in 2026, cities such as San Francisco and San Jose require a family of four to earn about $400,000 to live comfortably.

It's nice to know a Washington D.C. based think tank founded in 1968 agrees with my $300,000 middle class lifestyle assessment.

Definition Of A Middle Class Lifestyle

- Having a job that can comfortably, not extravagantly, support a family.

- Being able to afford a safe car to commute to work and reduce injury and fatality from accidents.

- Being able to take 2 – 4 weeks of vacation a year with the family.

- Being able to retire when Social Security kicks in at 62, at the earliest.

- Being able to save enough in your tax-advantaged retirement accounts in order for Social Security to be enough.

- Being able to send your child to college, since college is fast becoming a minimum educational requirement to get many different types of jobs.

- Being able to go out on dates and see friends once a week without feeling immense financial strain.

- Being able to care for aging parents when they need assistance.

- Being able to eat healthy foods to avoid being one of the 45 percent who are obese in America.

- Being able to pay no more than 5X your household income for a two bedroom house.

If you'd like to argue why one of the bullet points shouldn't be part of a middle class lifestyle, please feel free to elaborate. I firmly believe that every decent human being who works hard deserves a middle class lifestyle.

Do not accept the pitiful deflationary state of the average American with $5,000 in retirement savings.

Confused About What You Don't Know

Here's Frank, a renter, who cannot see the $19,200 in property taxes and $3,600 in property maintenance expenses when he pokes at Catcoder for rounding up $24K in taxes. This is a discussion about my $300,000 household income budget.

I can promise you that if you are a homeowner who has to pay $24,000 a year in property taxes and maintenance expenses every year, you will know! In other words, judging people without being in their shoes isn’t productive.

Since we obviously don't all live in the same part of the country, it's logical to assume that different levels of income are required to provide for a middle class lifestyle. Yet for some reason, people don't accept this logic.

If you define yourself based on an income or a net worth amount, then you either have low self-esteem or have a completely backward view about money. A middle class lifestyle is about living.

Geo-Arbitrage Is A No Brainer

Despite clearly stating that $300,000 is equal to $100,000 – $150,000 in non-coastal cities, some folks still cannot accept the equation. The national ideal income is around $125,000 based on the student loan forgiveness income threshold.

Here's one viewpoint from a reader who also believes living in a lower cost area of the country makes sense.

Perspective From Singapore

“I lived in Singapore for 5 years (consistently ranked no 1 in total cost of living worldwide). I came away from that (pricey) experience telling myself I will never live in a high COL area again if given the choice.

It’s incredible how many people in other countries have no choice but to live in their country’s high cost of living areas due to various factors outside their control. Geo-arbitrage is truly one of the mightiest tools in the US that many people elsewhere simply do not have, or not to the same degree.

Some people are forced to go where the work is. But is the quality of life in the expensive coastal cities so great to offset the total life cost? I’ve seen that lifestyle and for me it’s simply not worth it.

The number of life options given to me in a lower cost of living area far outweigh the downsides. If I reach financial independence far faster living in flyover country for a few years, I can then spend my time visiting expensive areas and enjoying their amenities.”

Earn your fortune in a city that pays you more and move, because you can. If you cannot, enjoy your low cost lifestyle and be happy with what you have.

A Higher Income Is Required To Live A Middle Class Lifestyle Due To Inflation

Below is a great chart that shows the rise in cost of goods and services since 2000. If you want to live a middle class lifestyle and own a home and send your kids to college, you're going to have to get long real estate and save aggressively in your 529 plans.

Take Action To Improve Your Life

Please do something about your life if you are not happy with it. Hating on people who make and spend more than you is a waste of time. Your feelings will only make you more miserable.

Save aggressively, invest aggressively, take more calculated risks, and get neutral inflation by owning your own home. The animosity renters have towards homeowners and the real estate market will simply grow.

If you are easily offended by anybody for any reason, ask yourself the following questions:

- Do I hate them because I hate myself?

- Do I hate their achievements because I'm unwilling to work as hard as them?

- Do I hate them because I'm prejudice against certain types of races, sexes, and cultures?

- Do I hate them because I wish I had what they have?

- What actions should I take to change my life?

Once you get down to the real reason for not being able to understand the difference between middle class income and middle class lifestyle, you can take purposeful steps to improve your situation. The only people who fail are those who take no initiative to change.

Long Live The Middle Class, Lifestyle!

For good measure, here's the updated spreadsheet for a $300,000 a year household of three after listening to everybody's feedback. Major changes include swapping out a Volvo for a Toyota Highlander, reducing the food budget from $2,100/month to $1,650/month, including a mobile phone family plan, and increasing charitable givings and 529 contributions.

Surely after making the changes, no one can argue that this is now a “more true” middle class lifestyle.

Related: How To Convince People You Are Middle Class When You're Actually Rich

Rise Above The Middle Class By Order My New Book: Millionaire Milestones

If you are ready to build more wealth than 90% of the population, grab a copy of my new book, Millionaire Milestones: Simple Steps to Seven Figures. With over 30 years of experience working in, studying, and writing about finance, I’ve distilled everything I know into this practical guide to help you achieve financial success.

Here’s the truth: life gets better when you have money. Financial security gives you the freedom to live on your terms and the peace of mind that your children and loved ones are taken care of.

Millionaire Milestones is your roadmap to building the wealth you need to live the life you’ve always dreamed of. Order your copy today and take the first step toward the financial future you deserve!

Recommendation To Build Wealth

Sign up for Empower, the web’s #1 free wealth management tool to get a better handle on your finances. In addition to better money oversight, run your investments through their award-winning Investment Checkup tool to see exactly how much you are paying in fees. I was paying $1,700 a year in fees I had no idea I was paying.

After you link all your accounts, use their Retirement Planning calculator. It pulls your real data to give you as pure an estimation of your financial future as possible.

I’ve been using Empower since 2012. Since then, I have seen my net worth skyrocket during this time thanks to better money management. Empower has definitely helped our family live a solid middle class lifestyle.

Build A Better Middle Class Lifestyle Through Real Estate

Real estate is a core asset class that has proven to build long-term wealth for Americans. Real estate is a tangible asset that provides utility and a steady stream of income if you own rental properties. If you want a middle class lifestyle, own your primary residence and invest in real estate.

By owning your own home, you will have covered one of the foundations of living a middle class lifestyle. To get to upper-middle class, you must build a solid investment portfolio that produces passive income.

Take a look at Fundrise, my favorite private real estate investment platform. Fundrise wisely invests in Sunbelt real estate with lower valuations and higher cap rates. The demographic trend toward lower-cost areas of the countries is here to stay.

Technology, WFH, and the pandemic ensured this. Fundrise has been around since 2012 and has over $3 billion in assets under management and over 350,000 investors.

My real estate investments account for roughly 50% of my current passive income. As a result, my family of four can comfortably live a middle class lifestyle without much difficulty.

In addition, you can invest in Fundrise Venture if you want exposure to private AI companies like OpenAI, Anthropic, Anduril, and Databricks. AI is set to revolutionize the labor market, eliminate jobs, and significantly boost productivity. We're still in the early stages of the AI revolution. I want to ensure I have enough exposure not just for myself, but for my children’s future as well.

I've invested over $400,000+ in Fundrise so far. With a $10 minimum, it's easier than ever to dollar-cost average into residential commercial real estate and venture capital. Fundrise is a long-time sponsor of Financial Samurai as our investment philosophies are aligned.

Subscribe To Financial Samurai

For more nuanced personal finance content, join 60,000+ others and sign up for the free Financial Samurai newsletter. Financial Samurai is one of the largest independently-owned personal finance sites that started in 2009. Everything is written based off firsthand experience.

I must say that I’m more of the British mentality that class is largely a cultural phenomenon; two families with the same income and the same number of children might spend it in very different ways; one might be affluent working class whereas the other is lower middle class because of culture.

Hi Sam, small nitpick…your chart has a math error for the “car insurance and maintenance,” – $150 per month is $1800 per year (not $1200).

Incidentally, I think the $1800 figure is more accurate than $1200. Insurance will be $700-800, and then we typically see about $100 per month on maintenance.

Also, I don’t see a line item for parking! Did you include that in “gas”? Parking can be $200-400 or more per month in most large cities, especially if you have to commute in to work in the downtown area. Most of the time, because of unpredictable work schedules and child care requirements, taking public transportation is either impossible or impractical for these families.

I wish I would’ve read this post earlier! This sums up my in-laws! We live in DC, and we make 270K per year, but we pay high property taxes, 2 car payments, a high mortgage, etc. Every time my in laws visit, they make infuriating comments about how we “pay too much” for things like hair cuts or a cleaning service. I’ve repeatedly told them that you can’t compare the prices they pay in AZ to DC, because of the higher overhead here, but they just give me blank stares. They also refuse to listen to a point where it’s sad, because they are so closed off, they will never learn anything new or fun. They think they know it all and give snippy responses to any new suggestions like online shopping! God forbid! They don’t understand that that’s the way most young people shop. Being around them is like being in a time warp.

I’m in a similar financial situation to you but I live in a location where everything is nice & cheap. So while I’m feeding my retirement, my children’s education funds, and my belly you’re feeding the system. Good job. Keep hemorrhaging that cash!

$76k fed+state+FICA total on $300k gross sounds extremely low to me. Are you using 2018’s tax bracket?

Heck, I just finished my tax return, need to triple check if I’m paying way too much…You are making me nervous…

I’m using 2018’s federal income tax brackets.

“Low income” in SF for a family of 4 is earning less than $117,000. “Very low income” is less than $73,000. If you don’t live here you probably don’t get it. You really can’t compare SF and Omaha.

https://www.sfgate.com/expensive-san-francisco/article/low-income-families-sf-bay-area-hud-statistics-13024580.php

Reality is if you live in a city where you make 300k ask around and you will see that the other 80% it’s making less than half of the 300k guess what they are doing just fine…. in San Francisco is no different, you wont die making 80k or 100k now if you make 300k and want to spend more than that person who makes 100k then to them you are doing 3 to 4 times their money what does that make you in their minds? Let’s compare this the 100k in Sf cant but you a property so if you make 300k it does… in the past few years you could have made 1 or 2 million dollars if you sell today? What does the 100k maker has? Exactly nothing. The person making 300k even if they spend everything but sold the property today and move out to the midwest could potentially retire if they want to in just the 6 years of appreciation in sf housing market. Also, to banks 300k would loan you whatever you want, and the 100k woulnt get the same advantage… I mean, what you are saying Sam it’s the same thing as someone making 1 million a year buying a 10 million home and they too potentially live pay check to pay check…? Why isn’t that person be referred as middle class even living pay check to pay check? It’s the same thing if you leave pay check to pay check making 50k or 150k? Or maybe 300k? Then it’s safe to call it low, middle and higher… it’s just decicions.

How does someone buy a $1.5 million median price property making less than $100,000 a year? His stork all definition of a middle-class lifestyle is owning your property and paying it off through your career, and not paying $5000 a month for a two bedroom apartment for life. This is a big predicament for many people who live in expensive cities who want to raise a family.

Hi, Thank you for this article. I really enjoy reading your blog posts. The one reason that I would dispute you assertion that this is a middle class budget is that it contains few tradeoffs. This hypothetical family can fully fund their 401k, pay for private school, and take 3 weeks of vacations. You might say they are not flying first class everywhere they are going and that’s a tradeoff, but I don’t think you would try to make that argument. Without a hard definition of middle class, we could probably argue this point forever. But for me, the lack of a need to make truly hard decisions is a luxury that puts this kind of income into the wealthy category.

Thanks for this article. I live in a high cost of living area, Wash DC, with some of the highest per capita income state in the world. As someone who follows quite a few FI blogs, I had started to get the impression that every family in the FI community lives off of $30-$40K per year. I was sort of bummed out that our family of four was able to pull off a similar lifestyle for $107,000 per year. So this makes a perfect bookend. I think it would be kind of a cool idea if you could create some sort of survey where everyone could fill in their basic expenses and it would kick out an average that could be sorted by geography. I’ve found that once you solve the real estate issue, either by house hacking, owning your home outright, or staying in one place for 20 years it’s easier to manage the other costs like groceries, automobiles, education regardless of where you live.

Sam,

I have liked your blog for years. Aside for the fact that I live in MN in a McMansion and that you call where I live “fly over country” this is insulting. Call it the Midwest please.

Separately, I think that it does not matter if you are part of the 2% at $300k or the median US resident at 50% with 40k. It’s just irrelevant. One chooses the weather and the beach, the other the low crime rate, or the quality education. It does not matter in the big picture.

There is a great article by a California professor that showed that the 50% people are servants to the 1% people taking care of their food via restaurant or their kid’s day care or schooling as teachers… but those 1% people are themselves servants to the Uber rich. The $30M UHNW families which are 80,000 big. Those use private jets with net jets. Then there are the 100M class of a few thousands that have a plane, and finally the billionaires that are controlling the way the country functions.

So, in the grand pictures it is sad to watch the poor servant arguing with the priciledged servant. They are both servants fighting over the crumbs.

By we way, I am happy with the crumbs. I know where I belong. But it seems not every one here does.

An analogy would be the average NFL fan complaining about the salary of the wide receiver that makes good money for only a few years and is judged while the franchise owner is accepted for his net worth. Very hypocritical.

Hi FranceUSA – Thanks for sharing. I used “non-coastal city” in my article, not fly over country. But speaking of the name, can MidWest be used to identify states in the South or SouthEast? Or does one have to say “MidWest, South, Southeast, etc” to identify non coastal states?

The NFL analogy runs true. Sorry about the Vikings last year. Go Niners and Raiders!

First time reader and commenter here. Truly an interesting subject.

A little background: I grew up poverty level poor in rural Maine in the 70s/80s. Neither of my parents finished HS. I was the 7th of 7 kids, and only the second to get a 4 year college degree–a BS in nursing. I married my husband (he’s a HS teacher) during college, and we were able to graduate with only $1800 in student loans, which we paid off very quickly. He grew up middle class midwest, but neither of us had parents who paid for college, and we both worked 2-3 jobs each while attending full time to pay for our own schooling. We proceeded to have 4 kids in 5.5 years and lived in a small city in North Carolina for the next 16 years. While our kids were home, I only worked part time with the exception of 3 years. For the first 12 years of our marriage, we never made more than 35K net between us, and never more than double that for the next 7 or so. I homeschooled for the early years, and then our kids attended the private school where my husband taught. We have always lived below our means: buying fixing upper homes, brown bagging lunches, cooking at home, shopping yard sales and thrift stores, saving to buy used vehicles, never carrying credit card debt, taking vacations that mainly consisted of visiting family and friends and staying local, doing our own routine car maintenance, etc, etc. We also always paid into our 401Ks to get the match from our employers, which obviously wasn’t a huge amount, but it adds up. Neither of us have ever felt deprived or jealous of those who make more, nor have we aspired to make a lot of money. We were/are pretty content with what we have, and also happy for those who choose to make more.

Fast forward to 2012. We decided to take the plunge and work overseas at an International School. My husband applied and got several offers. At this point, our oldest was in college and our 3 youngest were in grades 9, 10 and 11. We ended up choosing Hong Kong, which consistently ranks first or second as the city with the HCOL in the world. When we moved, we sold our home in NC and paid off our family cabin in rural Maine. We came to HK with zero debt. While we moved for my husband’s job, after we arrived, I was able to work as the school nurse, but I get paid on a secretarial scale as I do not have a HK nursing license. Since arriving, we have been able to live very frugally, while still traveling extensively. Our school pays a housing stipend, and if you do not use it all, you can keep the difference, so we have always found the cheapest apartments available–we currently pay $1700 USD for 400sf, while many routinely pay 5-10K or more. We pay nothing OOP for health insurance, and our kids, (who have now all graduated and are in college) were able to attend a top notch high school for free. The school also pays to fly us home every other year, and we have very low commuting costs as we have chosen not to have a vehicle here. We have been able to save/pay for kids college/buy real estate with approximately 50% of our income. We still have zero debt, and we still barely cross the 6 figure theshold between us. We still cook at home most nights and brown bag lunches. I buy most of our clothes at thrift stores.

I say this to say that no matter where you live, there are choices. I also understand that while most people who make a lot of money want to live a lifestyle that is equal to that choice, there are always ways to save more. Growing up amongst the poorest in the US, I rountinely saw people waste money on booze, cigarettes, and lotto tickets all the while collecting food stamps and disability checks. The choices that the rich make can sometimes seem equally puzzling to me, but we all have our reasons for doing what we do.

Like you, what I have noticed is that the general population tends to blow off (or get downright ugly!)about any ideas you have about frugal living if you exhibit even a modicum of wealth (like traveling), little realizing that most of us who “make it’ do so through a series of choices. My only beef is with people who claim they can barely get by on $x, but choose to spend money on things that truly aren’t necessary for living. If you want a 80K vehicle, private education, 3 vacations a year, fancy meals out—great!! But please just own it, and don’t tell me how hard your life is.

Just thought I’d share my story. Thanks for a great blog!

Thanks for sharing! Having your kids attend the private school where your husband taught is truly one of the best benefits of teaching. I’ve thought about this for my son, I really have. And I probably will apply to be a teacher in Honolulu somewhere. My good friend got to go to Georgetown for free b/c his mom worked there! Not bad!

HKIS? HK is so expensive… I couldn’t live there. But I did visit 11 or so times for the HK Rugby Sevens. What a blast! Where are your kids going to college?

I was immediately reminded of an article I saw a while back on EarlyRetirementNow–the title was “This place has extreme wealth inequality, yet everybody is happy!” The author was, of course, talking about the world of personal finance bloggers and those who are striving for early retirement.

A nice counterpoint to the experiences you’re relating here, Sam. Just remember that not everyone is a hater! :)

Okay, I’ll be honest: I was an avid reader of Financial Samurai for years. But then I started feeling like I couldn’t relate to the numbers. As more articles started referencing “above average” people, I kind of checked out. I’m not at a point in my life where I’m pushing myself work/earnings-wise, and I’m okay with that (right now).

Our Next Life got me thinking about “middle class” when she pointed out that the median household income in the US is $57,000. There were some comments that pointed to this blog, which piqued my curiosity. Reading the comments here has really gotten me thinking. So:

I live on the outskirts of Indianapolis, Indiana. I’ve never looked in to where we rank cost of living wise, but I know where you are in the city and outlying areas makes a huge difference. Regardless, MUCH lower than coastal areas.

I have a salaried income of $56,000/year. My fiancee is hourly, in a weather dependent job. He usually earns in the low 50’s, although this year is looking better.

He has adult children that we don’t support; I have no children. We do provide minimal financial support for his mother.

We bought a fixer-upper house at the end of last year, rolling the major renovations in to the mortgage. We bought the house for $55,000. With renovations, the mortgage is for $88,000. It originally appraised for $105,000. Property taxes are around $1,200/year. Our house is a 3 bedroom, 1.5 bath ranch, with a full basement, and large two car attached garage, on an acre of land.

I drive a 2014 Ford Escape, that is paid in full. My fiancee drives a 2014 Chevy High Country, which we bought used a few years ago, and have a $639/month payment on.

My first thought on the breakdown was that some of those expenses are high. But, that’s the same thought I have when I’m looking at our spending. We take 1, maybe 2 “real” vacations a year, spending $2,000-3,000 each. We don’t spend a lot at the grocery (>$100/week), but spend way too much at the bar (Not even gonna go there). I calculated a few weeks ago that we spend $50,000 per year to cover our basic lifestyle. That doesn’t include extra debt repayment (we’re working to pay off all credit card debt), home improvement projects, vacations, clothing, etc.

If we’re trying to compare apples to apples, I might be “better off” than someone making $300,000/year in a HCOL area. I could see trimming some things from the breakdown above. But, I could equally trim things from my own budget.

Of course, if we both contributed equal %s to investments, Mr. $300,000’s investments are going to grow much faster than mine, due to the larger dollar amount. But, then, if he stays in a HCOL area, he’d probably have similar buying power. So that’s probably a wash?

Point being, I definitely don’t feel “rich”, or even “upper middle class”. So, by comparison, I guess I could understand the same for $300,000 in a HCOL area.

Cindy – Is Our Next Life the couple that wrote a hundred blog posts telling their readers when they were going to reveal themselves like a count down? If so, it got very annoying and off putting, much like Lebron James trying to hype up when he was going to Miami. Like they are all egomaniacs or something.

From their blogger manifesto, did they reveal how much they earned? I don’t think so.

They don’t have kids either, which makes early retirement much easier.

Bloggers who blog about blogging and incessantly promote themselves are incredibly banal. But that’s just my own opinion.

They aren’t for everyone. I personally find that different blogs appeal to me at different points in time, depending on where I am financially/emotionally, and what the blogger is focusing on at that point. And I like varying points of view, even if they don’t match my opinions or situations.

And the kids thing… I understand that kids have a huge impact on finances. I don’t have any children myself. I based my life around the fact that I would, but it turns out that I can’t. I’m kind of in between though, since my fiancee has two children in their twenties. So, we’ll still have weddings and grandkids and other costs associated with having adult children. A lot of personal finance blogs deal with having children, so it’s nice having some variety out there, for people who aren’t in that situation.

I hope my comment didn’t come across as bashing Sam. I’ve always enjoyed his writing. It’s just that, for a while, I couldn’t relate. Sam concentrates on “above average” earners/savers. I’d end up feeling bad that I wasn’t even trying to be above average. That’s on me. Sam writes to a certain niche, and he’s very good at it. No blog can be everything to everybody.

Fair enough. There definitely is no one site that fits all. But when a blogger writes incessantly about themselves, and then writes a blog manifesto telling people to be more transparent without even sharing their income, that is hypocritical and annoying.

Do you really not think they are full of themselves?

I don’t feel bad, I feel motivated. And that’s just two sides of the same coin.

Isn’t every blogger kind of full of themselves though? I mean, really, blogging is a platform where you write about your life (or something that you consider yourself an expert on), with the idea that others will find it riveting enough to spend their time reading.

And I say that with love, since I have my own little blog, where I write about my money life.

I share my income a lot on my blog. I share my net worth numbers. I used to share my monthly spending; I might go back to that. It’s a little embarrassing lately, if I’m honest.

That’s my choice to share all of that. I can read other blogs and gain a lot from them, even if they choose not to share all the details. I completely understand the reasoning for not sharing all of that information.

All that being said, I can kind of agree with you.

The thing I’ve always liked about Financial Samurai is that he’s always been very honest about who he is. He writes for a niche in the financial community. I know that I’m not his target audience (again, totally on me), but I can still gain valuable information from him. I know exactly who he’s writing for when I read his posts, and he doesn’t try to say otherwise.

I think sometimes that blogs like Our Next Life (and many, many others out there) try too hard to be inclusive. While it’s great to acknowledge that your situation may not apply to everyone, if you spend too much time on that, it becomes a lot harder to handle the posts that definitely don’t apply to everyone.

It’s great to acknowledge that a lot of retirees have to work, because Social Security won’t cover the bills. But that’s way different from choosing to work to pad your retirement, and finding freelance gigs that will take up less than 10% of your time, but cover all your expenses. Equating those two things comes across as a little tone deaf.

And, there’s a lot of money to be made in successful blogs. I don’t always agree with the “high and mighty” attitude of not monetizing a successful blog. Call it a hobby all you want, but there’s still a lot of work that goes in to it. There’s no shame in making money off that work. And, if you’re a successful blogger, you most likely have other financial opportunities that are coming about because of your success on the blog. Maybe not making money off the blog itself, but definitely making money because of the blog.

Hey Sam, just out of curiosity where did you get the $8,400 annual (employer subsidized) healthcare number? Reason I ask is because my wife and I (with a little one on the way) pay roughly 3k a year through her job. She won’t be heading back after the baby is born so I researched Obamacare unsubsidized plans and I’m looking at 8-10k.

Yeah, $300k in NYC, SF or the like is decent money, especially with no residual debt (student loans, credit card debt, heloc etc) or if you bought your place more than 10 years ago, but its certainly not going to be luxurious living either for a family (maybe as a single person would be good $).

I live in CLT & my income in NYC would need to be ~$700k to match what I make here (bit over $300k assuming bonus and RSUs at target). I’d label my family as lower upper-class by income but just upper middle class (but rising quickly) by wealth. In NYC the same salary we’d be just into upper middle class at best.

It’s all about putting things into perspective. If there is a surgeon making $500k a year, well he’s studied his butt off, works crazy hours, nature of work has a high amount of risk and therefore pays a lot in insurance and other expenses too.

In terms of coastal cities, I know people that work in DC and commute 2+hours to live in burbs for less. There are always trade-offs and you have to be willing to sacrifice for example time, money, family, etc.

In the end, I think there is a big distinction between middle and upper middle class. UMC should be retitled as affluent. Think about the range the term “middle class” covers. It is way too wide. I believe that is part of what drives the emotional reactions. I have a unique perspective because I have been in all 4 ranges at some point in my adult life. Now, we are in the mid range of affluent (upper middle class) and I am out of the corporate rat race at least for now.

I see no issue with Sam or anyone else driving a 60K car if they can afford it. Why pass judgement on anyone? In Sam’s case, he made a lot of money in Finance and still makes a great living. I did think contributions to charity could be higher and he clearly agrees with that.

Also, the middle class (not the affluent/Upper mid class or high class) are getting squeezed. If they own their own business, the cost of health ins alone can be a back breaker. Then you have out of control (until recently) education expenses. 2 huge rocks that can kill any budget. These people do not believe that their concerns have been addressed. That leads to anger which leads to emotional reactions against “rich” people. It goes a long way towards explaining some of the politics in the country today.

On the other side of the equation, nothing drives me more insane than the articles on the internet which state “Family of Four Survives on $12,000 a Year”. I guess it is technically possible if you have free housing but who in the world wants to live that way? I have seen other sites where the site own admonishes people who like to have a dinner out once in a while. He stated that he makes “delicious food at home”. Well, good for you. I am sure he is a blast to hang out with.

Anyway, I get both sides of this since I have been on both sides. My advice to people is to work hard, take the role that looks hard but can be rewarding if you are tireless and smart, get the proper certifications and licenses for your profession and do NOT give up. If you do those things there is a very good chance you will be able to write an article like Sam that inspires emotional reactions as well.

Mental point of origin and how it relates to lifestyle inflation certainly needs to be taken into account in everyone’s situation. I have the advantage of having been raised in a small midwestern town with a divorced family; financial struggle was a daily reality that felt impossible to overcome at times and certainly shaped my world view. Visiting family that lived in the nicer suburbs of cities such as Columbus and Indianapolis created the idea that living in a place with more than a Subway restaurant and around people who could consider flying for vacation was flabbergasting to me in my youth (I’m a millennial).

The most challenging jobs I’ve ever had in my life were those in my teenage years, roofing, warehousing, masonry. I was paid no respect and the money was $8 per hour at best. Now my family’s hh income of $225k seems surreal. So does living in the Denver metro area in a suburb full of services seem like rich people stuff :). I literally make more while using the bathroom than I used to during the time it took me to carry 60 10” cinder blocks to the basement wall that I was building.

Home costs-$24000 per year all utilities included. Value $465, mortgage balance $170k

Cars-cash, 3600 for insurance, $300 maintenance (I do my own). No car loans. Gas paid by employer.

Childcare-$12,000 for high quality pre-K, costs will soon be $6,000 for charter school

Phone-paid by employer, $120 as gf is on family plan

Food-$12,000 groceries and out for 3 people. No restaurants as my girlfriend’s cooking is the best meal of my life each time. We both grew up where there was only a subway so home cooked meals are the only way to go for our tastes.

Vacations-two flying week long vacations per year paid in points from extensive work travels. No international, we like US destinations.

Alcohol-$100 per year, barely drink

Clothes/home furnishings-$2,000 per year, half come from goodwill.

Gym-$0, built home gym from scrap wood and bar from Lowe’s.

Hobbies- $500 for shoes and firewood- camping/hiking

All this and we feel amazingly rich while saving 60% of take home pay. I travel to expensive coastal cities often for work and I can’t believe people agree to live there regardless of their financial situation. I’m not saying my mental point of origin is “right”, but I’m sure glad I have the one I have so I can feel rich while living the way I do.

I agree that $300,000 per year in an expensive coastal is very fair.

Here’s how my middle class situation fits your definition with a $70,000 income in the expensive eastern panhandle of West Virginia (still not expensive).

* Having a job that can comfortably, not extravagantly, support a family.

No problem here especially since we haven’t had to pay for child care for the last 15 years. We decided both of us working wasn’t worth the expense. Full time minimum wage barely covers the expenses it generates when you have 2 childcare age boys.

* Being able to afford a safe car to commute to work and reduce injury and fatality from accidents.

We have a $6000 used commuter vehicle and a $20,000 2016 family vehicle. The number one safety factor is the driver.

* Being able to take 2 – 4 weeks of vacation a year with the family.

We take 2 weeks of vacation in the states totaling around $4000.

* Being able to own at least a two bedroom, one bathroom home or apartment.

Own a 4 bedroom, 2.5 bathroom home at a cost of only about $85/sqft.

* Being able to retire when Social Security kicks in at 62, at the earliest. * Being able to save enough in your pre-tax retirement accounts in order for Social Security to be enough.

We’ll actually retire at 49, but could easily retire at 62 with only a 5% savings rate for 40 years at our current income level (at 8% growth it would be worth around $1mil)

* Being able to send your child to college, since college is fast becoming a minimum educational requirement to get many different types of jobs.

Local college will only cost us about $8000/yr after financial aid. We have some savings for this, but most will be paid as we go. Our kids (14 and 17) have seen that a comfortable happy life does not require a huge income, so they aren’t that motivated to make big money (this could be good or bad – we’ll see in about 10 years I suppose).

* Being able to go out on dates and see friends once a week without feeling immense financial strain.

We usually see a movie or go out to dinner as a family once a week. Most of our adult friends are online and we spend a few hours a week with them for basically free.

* Being able to care for aging parents when they need assistance.

Kids should be done with college before this happens.

* Being able to eat healthy foods to avoid being one of the 45 percent who are obese in America.

No problem. We eat at home 95% of the time and spend about $600/month on groceries.

* Living in an area where the median home price is between 4.3X-6.3X your household income given the national median multiple is 5.3X.

The median home price in my area is about $175,000 which is only 2.5 times our household income.

We are doing very well on $70,000 for two reasons: low cost of living and being financially responsible. The only debt we have is our mortgage which was only $90,000 because we rolled our equity from a previous home into this one. Unfortunately, most people in this area making $70,000 are struggling even though the cost of living is so low.

Wealth, and what it means to be middle class, is relative. It reminds me of the joke involving two runners out in the woods jogging when they come across a bear – which immediately starts chasing them. One runner says to the other, panting – “Can you outrun a bear?”, and the other says, “I don’t have to outrun the bear. I just have to outrun you.” What often makes the difference in our happiness is how well the person running next to us is doing (and how we define that person). Is someone living in SF really running against someone in Biloxi, MS? Choose your race, run it well, and finish strong. Measure your goals and achievements by your circumstances and opportunities, wherever you live or choose to live. Otherwise, you run a pointless race – and the bear wins.

Hi Sam,

I thought I would offer some real life examples of low-cost coastal living. I live with my wife in West LA (almost Venice but not quite, ~2 mi. from beach). We just had a kid. We are both 30 years old. Our monthly expenses are low.

Rent for 1br $1,595

Rent. Ins. $32

Auto Ins. $30

Umbrella $15

Health/Dental $255

Groceries $220

Utilities $25

Charity $100

Other Stuff? $300

We don’t own a car because everything is close and Uber is easy to use. I keep non-owner auto insurance for the one weekend a month that I need to travel for work or if we need to rent a vehicle for other reasons. Our kid is a recent addition, so we will play things by ear. My wife is stay-at-home. We still save a lot, we live close to the beach where I can surf and workout for free, and we are pretty damn happy. My situation probably needs more context but a low-cost, fulfilling life is indeed possible in expensive coastal cities.

I don’t know that you would call this middle-class, but then it seems that the middle (or maybe upper-middle) is most easily characterized by some kind of neurotic status anxiety which I try not to have (I’m not always successful) and a mostly-fruitless overinestment in their children’s development. I would read “The Nurture Assumption” by Judith Rich-Harris (http://a.co/4bbgiZn) or “Selfish Reasons to Have More Kids: Why Being a Great Parent is Less Work and More Fun Than You Think” by Brian Caplan (http://a.co/7XQNCdJ) for explanations as to why. In short, above a certain very low threshold like making sure your kids are fed and not locked in a closet, the shared environment (think your home life or upbringing) explains almost none of the variation in some of the common metrics we use for success. It does correlate a little bit with how much your kids like you and some short term impacts, but nothing long term. Genes play a big role.

Overall, I think the lower, middle, upper class division have become pretty meaningless. It’s kind of crude and not clearly defined. Hence the hundreds of comments arguing back and forth. I do think people get overly hung up on the money dimension of class. You are probably a little to blame for the misunderstanding because the numbers play such a central part of your post. I think this generates clicks and conversation, so there’s a tradeoff being made here.

If I can recommend one more book, Paul Fussell in “Class: A Guide Through the American Status System” (http://a.co/4fGJyVI) divides people into 9 classes: Top Out-of-Sight, Upper, Upper Middle, Middle, High Proletarian, Mid-Proletarian, Low Proletarian, Destitute, Bottom Out-of-Sight. These classes are defined not just by wealth, but by dress, patterns of speech, and even the way people decorate their bathrooms. A person can be upper class without having a lot of money, and a person with a lot of money can still be high-prole. The book is about 25 years old and a little dated but still insightful.

Thanks for sharing. How is it like with a newborn and living in a one bedroom? Where does the baby sleep and how is he sleeping? I found that if the baby is not sleeping, it’s important for the income producer to find a way to sleep because of lack of sleep really impacts the cognitive function.

How long would you like to live in a one bedroom with a baby? And if you do decide to get a bigger place, how much does it cost to rent a two bedroom or three bedroom 4 x 2 or three bedroom house or apartment in Venice Beach nowadays?

I think the majority would say that a middle-class lifestyle is living in a two bedroom apartment or house or larger once you have a kid. If you disagree, let me know why.

Sorry for the slow response.

In short, no. Whatever I’m doing is probably orthogonal to the middle class. I think maybe there is a market for class or status signals just like there’s a market for bonds or homes. I try to put money and effort into the things that provide both the greatest return to me in terms of goals, principles, or values and provide the greatest improvement in class or status in so far as I care about that, which is honestly a little but not a lot. Some people worry about the “optics” of their actions (or how other people will perceive them) but I’ve found not worrying about this too much to be a good way to save money and do the things I care about.

Newborn was in the NICU for a bit as he was slightly premature but is now home. It’s only been a few nights. I sleep in the bedroom (with earplugs) and my wife in the living room with him. We switch for a couple hours in the morning so she can get more sleep, and I’ll look after him. Then I do some work which is easy to do remotely either from home or a coffee shop nearby. The amount of data is too limited to call this a “routine.” Things will adjust I am sure.

Intend to stay in LA for at most 2-3 more years. Wife’s family is from the upper midwest and we will go there. The difference in value is just too stark. I can buy a beautiful, old house for cash in a nice neighborhood. In 2012 I would have picked Boise to move to, but I’m now reading that Californians are invading that and driving up prices. No one is fleeing to Milwaukee (knock on wood), so we’ll go there. Being near family is good too.

Hi Ben:

$1600 for rent in West LA seems like a great deal. I remember paying about $2k 15 years ago for a 2-bedroom in West LA, although it was more than 10 miles from the beach and it was spacious. I can’t imagine what it goes for now.

Just some thoughts from someone with a preschool-age toddler:

1. You will find that you start spending more on food once the baby starts eating real food, not just formula or breastfeeding. When is a baby is trying out different foods there is going to be wastage.

2. Even with a SAHM, there may be some times in the first few years that you will want your child to socialize with other kids, which may involve preschool or other costs. Even meeting for playdates will cost you something usually, whether it’s for a cup of coffee somewhere or transaportation costs to someone’s house.

3. Don’t forget to look at your local public schools and see what they look like. Time flies and before you know it the time for kindergarten will be upon you.

4. Your travel budget (under Other Stuff?) will most certainly increase when it comes to getting on a plane.

5. If you want your kids to be exposed to museums or other cultural artifacts they will start costing you as well.

Basically the bar for happiness goes up a little more than just keeping the kid fed and out of the locked closet.

I would be surprised if you considered any of these items products of a neurotic status anxiety. I classify them as pretty middle-of-the-road expenses for a middle-of-the-middle-class family.

Best of luck

Exactly BigJimDallasTexas, net worth rather than yearly income determines class. I’m not sure when people started using “yearly” income to determine class.

The wealthy own assets that provide cash flow that is used to pay for their liabilities while a W2 workers exchange their time for money to pay for their liabilities.

Someone can work to make $300k a year and have so many liabilities they have a negative net worth, if they become ill, they could lose everything. I wouldn’t consider this person rich. Even someone who considers themselves middle class may actually be poor. They may be living the middle class lifestyle but on borrowed money and no savings and investments. They have a negative net worth (they are poor).

People who judge others based on one tidy number without considering COL and net worth imho shows their ignorance in financial matters. Worse, when anyone uses that lack of understanding to manipulate the masses shows their true colors.

John… this is an excellent way to describe people’s mindset toward others and money…. (Quoting his post below).

“Two guys riding in bus. They look out the window as they bump along and see a beautiful Porsche go by. The one guy says, ” someday I am going to get one of them and not ride the bus” and the other guy says ” I hope that someday that porsche owner rides the bus just like I “have” too.”

People should really think about it and determine which of the two men they are. The first guy is positive and his mind is working trying to find a way, while the other guy who hopes the drive is on the bus is the naysayer, negative, who’s angry, I was in the I’m going to get one someday camp and that mindset was part of the reason I was able to move out of lower class. The ladder will stay in the same class they are in.

To me, the distinction in class here misses the point. One’s net worth should determine class, not income from work. This is how “class” started. The landed gentry were the upper-class, and really did no “work”, they just owned things.

Who would you rather be: a 62 year old teacher making $60,000 a year who invested diligently for 40 years and is worth $4,000,000, or a 62 year old doctor making $600,000 a year who blows it all/made bad investments/multiple divorces and is worth $500,000.

Frankly, for purposes of FIRE and this blog, net worth as “class” should be the focus. It’s not what you make, it’s what you save.

Sam,

Great article I think people perspective and experiences will never change, I’ve spent 30 years in the military and travelled around the world and met people on both ends of the spectrum; from billionaire sheik to people who make as in much in a year as I made in a month. Unless you can walk in the other person shoes no matter how hard you try to explain your position to many $300k will never be middle class. Between my current job working for Air Force in Japan and my pension I make around $150k and when I explain to some how tight our budget is I get that look, can’t imagine making twice and still trying to get people to understand depending on where you live what you make do equal….being rich.

Great article Sam. I certainly see your points. Our nation is so divided, whether socially, politically, racially or classes (hence your article, middle class). So divided that I’ve put much thought into whether it was worth it to start my own financial blog.

I reside in TX and plan to sell my home in the next couple of years (as TX residential home prices, at least in my area, are getting “bubbly!”) and relocate to Arkansas where cost of living will be greatly reduced. Property taxes alone!

I think the real problem is not income inequality… it is financial literacy. There is no doubt that if everyone was paid the exact same amount in the same cost of living area there are some that would end up much better off. Those are the ones that can delay gratification, the ones that understand time-value of money, the ones that plan for the future. The ones that spend in the now would be just as bad off as they are now…

I know anecdotal evidence doesnt prove anything… but a co-worker of mine is paid the same as everyone else in the same position… is in serious debt and knows it a problem… asks for help but ignores all advice… “now” is more important than any future… we all got a significant raise… i suggest that they put it towards paying down they debt since they were living paycheck to paycheck and this could be the shovel they needed to get out of debt. Instead…. they still live paycheck to paycheck and dont live any differently now than they did before… hard to tell where the extra money even goes…. to make matters worse for them/better for me… we all got ANOTHER large raise (we are talking over $5,000 a year for each of these raises in a LOW Cost of living area) … and STILL lives paycheck to paycheck… and STILL has nothing extra to show for it…

While seemingly unrelated to this post… my point is… people that look at other peoples earnings and wealth dont understand how money works. I am better off because of people like Elon Musk and Steve Jobs and Bill Gates… they have a ton of money… but i live a better live because i use their products… if wealth was a pie and everyone got a slice… we would all still be living on farms and growing our own food… people are not poor BECAUSE other people are rich…. anyone that thinks this is the case simply doesnt get it… and probably will continue to be envious their whole lives and work into their 70’s because they arent financially literate…

sorry for the rant…

Thanks for sharing! I don’t think people are poor because others are rich either. I hope FS readers abolish welfare mentality and know they deserve to find their own gold too.

Related: Getting Rich Is About Willpower: Why Give Up When You Can Keep On Going?

While many things are more expensive in certain locations, not everything and not to the extent that $80,000 in Iowa is truly the same as $300,000 in SF. Just ask any Iowan who has to save for several years to afford that DisneyLand vacation that costs her the same as the San Fran family but represents a much larger percentage of her income. Unless your local sales tax in SF is 200% then the same is true for anything purchased online, which these days is almost everything.

True, but I hope people don’t get hung up on the $80,000 Des Moines, $300,000 SF example. Maybe the real level is $100,000 – $120,000 in Iowa.

The point is to stop focusing on a middle class income, and instead, focus on a middle class lifestyle.