“What happened to your friend who bought Tesla stock on margin,” a reader asked. He likely lost a lot of money, but I haven't asked for details. That would be rude.

On March 31, 2021, I published a post entitled, Buying Stocks On Margin Is A Bad Idea: You Could Lose Big. I wrote the post because I was alarmed by my softball friend’s excessive risk-taking.

When compared to what he was earning as an educator, his position was a huge red flag. Given he also wanted to start a family, I tried to encourage him to be more conservative during 2021's stock mania.

I learned my lesson during the 1999 – 2001 dotcom bubble collapse while working at Goldman Sachs. Fortunes are easily made and lost, which is why I encourage readers to regularly convert funny money into real assets. This way, you increase your chances of protecting your gains.

Unfortunately, my advice fell on deaf ears. In his eyes, I was a lazy softball player who didn't dive for balls, slide, and run at 100% speed. No matter how many times I explained to him I didn't want to injure myself as a dad to two young kids, he continued to chide. So he’s not really a friend, but let’s call him one anyway.

What I realize from writing this post is that losing all your money may not be the worst thing when buying stocks on margin. Let me explain.

Betting Big On Margin At The Top

Here's a portion of what I wrote in the post,

My friend makes roughly $70,000 a year as a preschool teacher.

As we got to discussing the future of Tesla one day, he revealed to me he had bought more stock on margin. Given the rise in Tesla stock, I thought he had about a $250,000 position in Tesla, which was already a lot based on his income.

When I asked him how many shares he owned now, he said, “Over 1,000!” In other words, at one point, he had over $900,000 worth of Tesla stock!

I'm not sure how he keeps getting new funds or how he was able to borrow so much. However, he did say he “only has to pay a 7% interest rate on his margin.”

No matter how hard I encourage him to de-leverage, he won't. He's adamant Tesla will continue to fly to the moon. He wants to get rich. At 38, he wants to achieve financial freedom now!

Losing Lots Of Money On Margin And Then Some

Unfortunately, since March 2021, Tesla stock is down about 40%. As a result, he may have lost a maximum of $630,000. He should have used a stop loss to protect some of his gains.

Since March 2021, he has gotten a new job with a raise. But even if he now makes $100,000 a year, based on my FS-SEER risk tolerance methodology, after taxes and expenses, he now has to work at least 10 more years to make up for his losses.

Having to work at least 10 more years to achieve financial freedom is kind of like Elizabeth Holmes going to jail for 10 years. OK, it's not that bad. But during the back end of his life, I'm sure he'd rather be playing softball, spending time with his daughter, and traveling than working.

Losing money is ultimately losing time. And losing time is more costly as you enter the second half of your life.

Worse Than Losing Money Investing On Margin

Besides going on margin to buy Tesla stock, he may have borrowed money from his parents to buy Tesla stock too. He helps manage his immigrant parents' rental properties. When you come from an immigrant family, money tends to get pooled together for the greater good.

It's one thing to lose all your own hard-earned money. It's another thing to lose your parents' hard-earned money. The shame can feel unbearable. As an immigrant, losing the respect of your family is the worst.

I remember getting my brother-in-law into a stock that I thought looked promising. Goldman Sachs had just taken the stock public and it was trading 10% below its IPO, so I told him to buy. But the stock kept going down by another 20%. Ugh. Sorry, Steve!

Losing Years Of Progress

Losing ~$630,000 is a lot for anyone. But if you lost $630,000 on margin going all-in, the $630,000 likely means your entire net worth has vanished.

In other words, at 39 years old, he may have lost 17 years of savings post-college. Losing 17 years of savings and investing progress feels worse than having to work 10 more years.

Any self-respecting person would be willing to work hard to rectify their mistakes. But to wipe away years of financial progress based on inappropriate risk exposure is a killer.

Losing The Respect Of Your Peers

When you're making money from your investments, there's a propensity to brag. And brag he did on Facebook about how much money he was making from his Tesla stock.

Just like on the softball field, there was little humility when it came to his investments. Now that Tesla stock is down so much, he no longer has the status of the “preschool teacher investing guru.”

When it comes to investing, please stay humble. If you invest long enough, you will eventually lose money. Ideally, you want to feel little emotion while you're making lots of money and losing lots of money.

If you find yourself constantly bragging over social media, find the root cause of your problem. Is it loneliness? A lack of recognition from your parents growing up? Or maybe you need to confront your grade school bully who said you were never going to amount to anything. Figure it out.

Whatever the case may be, practice stealth wealth. You don’t want to lose money on margin and also lose the respect of your peers.

A reputation can take a lifetime to build and a minute to destroy. How much is your reputation worth to you? Good thing society likes redemption stories.

Unlikely To Have Lost Everything On Margin

Good news! Thanks to margin calls, it is unlikely my acquaintance lost 70% of his $900,000 position in Tesla.

A margin call is a demand from your brokerage firm to increase the amount of equity in your account. You can do this by depositing cash or marginable securities into your account or by liquidating existing positions to generate cash.

Given he went on maximum 50% margin, he was likely forced to sell some stock once Tesla declined by 25% to maintain his 50% margin ratio. Further, Tesla's stock price has rebounded. Let's hope he held on!

FINRA Rule 4210 requires that you maintain a minimum of 25% equity in your margin account at all times. In practice, however, most brokerage firms have stricter requirements that demand you maintain at least 30% equity—and in some cases—significantly more.

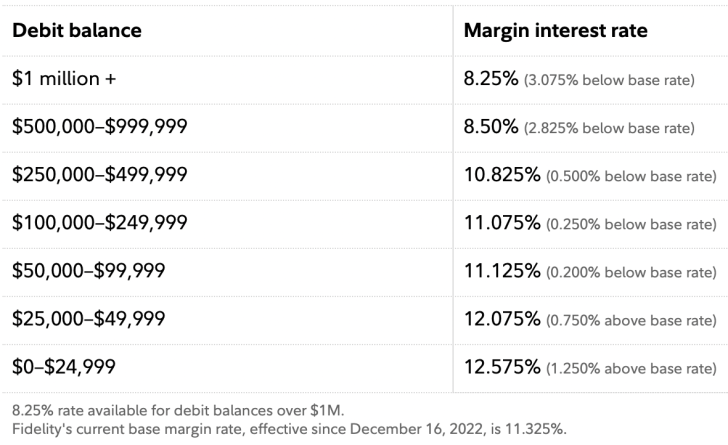

Therefore, instead of losing $630,000 in Tesla, he may have only lost ~$300,000. Check out the latest margin interest rates from Fidelity. Losing money on margin plus paying a 12% margin interest rate is a bad combination!

Lose Less And Outperform

Even though the first rule of financial independence is to never lose money, it may be impossible to adhere to during bear markets. The larger your investments, the harder it will be for you to make enough money from your day job or business to keep your net worth positive.

Hence, the second-best thing you can do is to lose less money than the average person. If you lose less than the average person, then you're actually winning. Because when it comes to personal finance, everything is relative.

At Financial Samurai, we're all about having a risk-appropriate asset allocation so that no matter the economic environment, we'll likely be OK. We logically invest based on how we value our time.

We are willing to feed our investing FOMO by allocating at most 10% of our capital to the riskiest assets. Even if 10% of our speculative capital declines by 100%, we'll still have 90% of our remaining capital left.

Stop Buying Stocks On Margin

If it's not clear by now, please don't use margin to invest in stocks, especially growth stocks. Not only will you be paying margin fees, but you may also lose all your money. Then there's the loss of progress, time, and respect.

There's a reason why bond companies and banks usually only accept real assets as collateral. Funny money can disappear overnight, as it did with the bank run on Silicon Valley Bank.

Going on margin to buy funny money assets is like playing with a live grenade while walking through a minefield.

Being 40 years old and having the same net worth as when you were 23 is depressing. The regret you will feel for confusing brains with a bull market may only grow. And if the regret grows too much, it may ruin many other aspects of a perfectly fine life.

Recommendations To Build More Wealth

Invest in private real estate with Fundrise, my favorite real estate platform. Fundrise enables all investors to invest in residential and industrial private real estate for just $10 minimum. Fundrise has been around since 2012 and primarily invests in the Sunbelt region where valuations are lower and yields are higher. It currently manages over $3.5 billion in assets for over 400,000 investors.

In addition, one of the most interesting funds I'm allocating new capital toward is the Innovation Fund. The Innovation fund invests in:

- Artificial Intelligence & Machine Learning

- Modern Data Infrastructure

- Development Operations (DevOps)

- Financial Technology (FinTech)

- Real Estate & Property Technology (PropTech)

Roughly 35% of the Innovation Fund is invested in artificial intelligence, which I'm extremely bullish about. The investment minimum is also only $10, as Fundrise has democratized access to venture capital as well. Most venture capital funds have a $200,000+ minimum.

For more nuanced personal finance content, join 65,000+ others and sign up for the free Financial Samurai newsletter and posts via e-mail. Financial Samurai is one of the largest independently-owned personal finance sites that started in 2009.

I technically invest with borrowed money by selling deep out of the money Puts on S&P at the amount of my available heloc credit line. I figure I am willing to get exercised and borrow money (via the heloc at prime rate) to buy stocks if SPY is down another 20% from where we are (so 40-45% down from peak). Historically, you make your money back after peaks in <10 years for the S&P (so on net I get a positive return if I can hold on to the shares long term), so I make a small amount of money if market doesn't tank, and buy at a steep discount if market does tank. Anybody see issues with this strategy? I have enough cashflow to cover the interest on the helocs.

Good luck! So long as your returns are greater than your interest, you will make money. You just have to last longer than any period of irrationality.

I think in general everything you are saying is correct.

That said, margins are made for the arbitrage, where you have identified specific patterns, and if you have a situation that produces 30-100% gains annually, why not increaset that ratio.

I would never margin to 50% of holdings, and typically sit around 20-30%, but I have turned 10k into 150k over the last two years, buying and selling certain stocks, never and holding for more than 90 days at a time. Get in, clear 7-10%, sell. Wash and repeat.

I would also note, margins account spending should be done at better interest rate institutions, think IBKR, M1.

Going from $10K to $150K is great. What percentage of your net worth or investments is $150K?

With those type of returns, I would seriously consider starting a hedge fund.

150k is around 8% of my networth.

I would never pretend to be good enough to start a hedge fund, nor would I want to put anyone else money at risk. I mean if what I did was risk free, I would bet more than 8% of my networth.

Also by definition, these investing situations (arbitrages) are by definition, usually not indefinite, someone else will figure it out and remove your advantage.

I mean SBF at FTX (then Almeida research), capitalized on the small differences between Western and Eastern BTC exchanges. He wasn’t a master day trader, he just patiently took advantage of the market inefficiency as long as possible, but eventually that evaporated and he had to move on to other things.

IMO, His problem was he thought he was smart enough to start a “hedge fund”, FTX, and lost everyone’s money. Also probably some stolen, probably by him in that “hack”.

Honestly, with those type of returns I would invest more than $150K id your net worth is $1.7 million. You are in the top 0.001% of investors in the world.

If I had those investment skills, I would invest at least $500,000 of my $1.7M net worth and try to turn it to $5-7.5 million in two years.

You may be underestimating yourself and your skills. But only you will know.

Once you hit a net worth of $5+ million, financial stress really begins to decline.

How do I reset

I had to sell because I had 90 % in tesla

I regret not selling in November 2021 when I could have paid my margin of and be left with $390 k but hung on and paid off margin when stock declined and now have less than 15 % left in my account ..my regret is huge fortunately my wife has 300 k and I have ss and work a side job and she is in Real estate ww now intend to increase real estate portfolio carefully

Sam, loved hearing your podcast on this article this morning as I was exercising at 5AM. Albeit he seems like he has little to no humility, I feel bad for the Softball guy. Hopefully his steep losses teaches him some humbleness, but I likely doubt it.

Keep on with the great work!

Thanks for listening. Yeah, not humble. His constant chiding and harping made playing softball less fun. He would criticize me and many others for an error. But he’d frequently make errors himself. So eventually we just poked back.

Dunning-Kruger is a scary disease. It’s one thing to think you’re an amazing meetup softball player. It’s another thing to think you’re an amazing investor. Losing all your money and progress is devastating.

Thanks for leaving a review on the podcast.

I’m just glad I have rental property and a full-time job. 5 grand in margin should be easy to knock out!

I now believe there is no such thing as “investing.” If my money is used to buy bonds, stocks or real estate, I am “betting” in the future these things will be worth more than I paid. I do not know this will happen. I guess it will happen. I believe it will happen.

I can bet the next roll of the dice will be 7. I can bet at 16 the next card is 5. I can bet my horse is the fastest in the race. It is all gambling.

As you have said plain, dumb luck is the reason some people get rich.

By the way, will the market open higher on Monday?

That’s why we can’t forget to spend our money and enjoy life! This way, we’re always winning.

The only difference is, no ammount of research can change the odds on a dice roll.

I agree stocks and real estate is still gambling, but you can affect and reduce the risk with proper research, resources and timing. You can still lose, but at least you know you did your best.

Contrary to not doing anything, where sometimes it will inevitably lead to loses, like having all your cash under the mattress

To some degree this is true, but statistically, gambling you will lose money – the house always wins in the long run due to the odds. Stocks – collectively – nearly always go up over time – in fact they’ve averaged 10% CAGR over more than 100 years (and they are aided over time by inflation). Investing in individual stocks is a loser. Empirical evidence has long shown you can’t beat the market in the long run, just buy something like VTI and forget it. Bonds are different beasts, but they are backed by real assets in most cases. If all the stocks and bonds go to zero, just remember it means no job and no government, so you’ll have bigger issues to worry about than your investments. I prefer owning individual bonds over bond funds, especially at low levels of interest.

Sam is absolutely right though – do NOT go on margin for stocks (or bonds) – certainly not a concentrated position of size relative to your income and net worth. The only thing I have leverage on is some of my rentals, and the cash flow is way in excess of my full carry-cost on every single property, plus a handful with no leverage.

Vow

The money you invest is used by somebody to create productivity and generate more money – that’s how you get returns

I hope that was a sarcastic comment about investing

You need Buffett

My dad lost $400k during the 1987 crash…he was on margin. The Dow(and other indexes) during that time were not nearly as volatile as what we see today, so I would NEVER go the way of margin in today’s markets. Total insanity and will invariably end in ruin and great pain.

Hi. thanks for this information, im sure many of us have been tempted to do this at some point.

Right now i have been tempted to do it, but on real estate. and instead of betting on stocks i decided to bet on myself. Apparently last year i probably got too greedy:

As of 2022 i had 5 rental units, 3 of them paid and the other 2 on mortgage. Also had a cash reserve of about 12 months, waiting for some good investment to come around (i had it in stocks, but got out the moment i heard about Russia intentions).

After much despair on what to do i decided to sell the first property i bought, an apartment, which i finished paying 2 years ago. The building was very old, not a single dime has been spent in its maintenance in the last 20 years, and while the value had tripled in the last 14 years, the rent had stayed basically the same, and i began to see decay both in the neighboorhood and the quality of tenants in the past to years. So i decided to sell.

After some consideration, i decided to use 40% of the sale money to give the down payment for 2 units on a “pre sale” price in a new susteinable developement. I gave 10% and i will be paying another 10% for about two years until the building is finished, then i will have to pay the remaining 80% anyway i can. I also negotiated an exit clause, so i can transfer one or both properties before its finished should things go awry, with the ability to reap off the profits from the increase in value, which is expected to be quite high. My original plan was to eventually sell one of the units and roll the money to the other one and then finish the purchase taking yet another mortgage in about 2 years.

But then i said “hey, i should keep both units!”

with the other 60% of the sale, i decided to built on top of one of my other units which is an old downtown house, in a zone with lots of demands for either cheap offices space or apartments. The idea is to built 2 double height small units on top while adding the ability to divide the ground floor in two units instead of one.

So far so good.

fast forward 6 months.

The lost rental income from the apartment i sold and the ground floor of the house im expanding is already hurting a lot because i cant rent it until i finish it.

the monthly payments of the 2 units i gave the downpayment is hurting even more, eventhough on paper they increase in value by the day.

It turned out the foundations needed a lot of reinforcement so a lot of the money was spent there. there is still a long way to go to finish everything and the money from the sale is already spent. my business is scrapping by right now because revenue generating projects i expected to close at the end of last year didnt go through, so yeah!

I already dug about 60% of my cash reserve.

I just secured a loan (kind of like a HELOC) that will allow me to finish the proyect. Once i finish it, and hopefully rent it, it will generate enough cash to cover for the payment of the 2 newer units and the some, but until then im on my own.

I was wondering if i should ask for more money on loan to PAY the remaining 10% of the 2 newer units. I would still have to make monthly payments but lower.

Another option is to just sell one of the units and keep the other one, and i wouldnt have to make another payment in 20 months.

Or simply just generate more income from my business.

If nothing else happens, i have 2 projects in my business that will cover my expenses for 5 months. Assuming i use the loan to finish the building, i would have a cash reserve for another 6 months.

should i still bet on my self? when enough is enough?

technically this is the time where my on paper networth has been the highest in my life, yet ive never been so stressed about money. Maybe its just the hardships of building something.

Any advice or admonition would be gladly heard.

As a side note, instead of doing all the aforementioned stuff, i could have just paid off nearly 90% of my remaining mortgages with the sale. Also, im aware my situation is not exactly what i would desperate, but still it has been quite the distressful experience.

Sounds like a complicated situation. I don’t know what your interest rates are or your cash flow is.

But I expect real estate prices to decline this year by 8% and get attractive again by the middle of the year. Depending on where are mortgage rates for, real estate could do better than down 8%.

The solution seems to be to generate more money from your business to alleviate the pressure and to hang on until the properties done so you can rent it out.

Wow! thanks for the response!

that seems to be the most logical solution before panic come in.

I dont live in the US. The interest rates here (Latin America) would be scandalous for you guys in the US, but its our reality. My income adjusting for purchasing power parity is around 130-160k after tax (as per the info of some dedicated sites) with expenses to match. But due to a couple of non paying clients last year i was around the red, which happenned just after i began construction.

Right now im implementing almost maximum reduction on expenses and looking for more work like crazy, because im of the idea that having too much cash sitting around makes you lazy (i recently found out you have an article about this). Ill try to protect the assets and investments as much as i can for as long as i can. Thankfully i negotiated that exit clause on the 2 units. But its not on the plan to use it. If anything, i will end up with better discipline.

Also, i wanna thank you for all the hard work and advice you write on this site

I just read your article on cash flow vs net worth… You are absolutely right

Thanks Sam. I know what to do now.

The vast majority of preschool teachers in the United States make under 25k per year which is in my opinion criminal.

Stands to reason that they would make 70k in San Francisco where people earning 300k per year probably live worse than those making 100k per year in most other US cities.

So sad

Do you have a source for this claim on $25,000 a year or less?

$300,000 a year is a nice middle-class lifestyle here in San Francisco.

The great thing about knowing what you know is that you can make a difference by donating money to your preschool teacher. That’s what we do and other parents to help them make more money on the side. They should make more.

one benefit of margin can be it forces you to sell a stock you should sell instead of holding forever thinking it will come back. so you may have been forced out at 100 cause of margin but if you aren’t on margin it is now 22 and you still own it. loss in second scenario might be more in actual dollars than the first scenario.

Sure. I’m sure the margin calls saved my fellow softball player at least $200,000 in losses. He had absolute faith in Tesla and Elon.

Regarding middle class, CNBC recently posted an article detailing the household income ranges necessary to be considered middle class in 20 US cities. In San Fran/Oakland/Berkley it’s $77K-$232K. Near me in the Denver metro it’s $60K-$181K. I find it accurate in my metro.

Good to see the data as a friend recently tried to sell me that he’s middle class, but their household income is 60% above the top range in the article and in the top 15% of earners in their zip code per IRS tax filers. Lifestyle creep can be sneaky!

Recently watched a documentary on Netflix about a Canadian bitcoin exchange startup (Quadriga) that went bust when the founder died. Turned out it was a ponzi scheme. Some heartbreaking stories of people who lost their life savings.

It’s interesting Ponzi schemes are revealed, and the government goes after them during a bear market. But not in a bull market because everybody is happy.

Kinda makes sense because Ponzi schemes fall apart when lots of people try to withdrawal the money the think they have..which is more likely to happen in a bear market or recession.

We could probably use more stories of people losing a lot of money (or even a little) buying and selling or even holding individual stocks. Even the most devoted index fund investors (myself included) fell prey during the last bull.

So here’s a little story about losing a little. I bit on Tesla after what I thought was a hearty correction only to watch it drop another 50%. Small position is what saved me. Only 5k. Same for coinbase. I was too scared to mess with crypto so I thought if I couldn’t win buying something whose utility seemed spurious with every explanation, maybe I could win with a broker. Wish I hadn’t done that either. Again it *only cost me me 4k. Tesla might come back one day. Coinbase probably not. Losing most of $9000 and knowing it could take years or decades to get it back or that it might not come back at all sucks. But it could have been worse.

The good news is most of my investments are in indexes. This is my 4th major recession and I am not worried about my index positions. The odds my indexes won’t come back are much lower. I’ve got more tech and growth exposure than I will want for the next bear market, but let’s get through this bear and have another bull first before I start worrying about the next bear.

Buffet’s first rule “Don’t lose money” has been the basis of one of my life’s guiding principles, which is: Every winning strategy begins by specifying how not to lose.

It’s important to ask yourself honestly: What if this fails? And can I deal with the consequences?

I only have margin on my accounts so I don’t have to wait for a trade or ACH transfer to settle before making another purchase.

Yeah, if you want to go on margin, you really need to know what you are doing and buy the right stocks / investments. Take a look at Charlie Munger at The Daily Journal : he is on margin, but doing pretty good with his position in Alibaba.. Tesla was not the stock to buy in 2021, whether on margin or not.

“Readers, have you ever confused brains with a bull market?”

It’s very hard to distinguish when you are right vs when you are inside a bubble. Tesla was only one example of “bubbly” stocks in 2020/21. Amazon, Facebook, Paypal and so many more were bid up only temporarily.

Even good old Clorox was cough in a frenzy. Remember cleaning in 2020 ? Everybody was looking to get their hands on their products. The stock almost doubled in a few months. If you had the stock before the pandemic started, you believed you were a genius ! Now Clorox is trading the same price as it did before the pandemic. Nobody is cleaning anymore I guess ..

“Do you know of friends who suddenly believed they were investment pros despite being in a different field?”

All the time. It’s very common. Something we call the Dunning-Kruger effect.

It’s like in music : there’s nothing more annoying than somebody who is tone-deaf and tell they are great at singing. Since a good hearing is essential to know if you sing well, if you can’t hear well, you can’t know you’re off tone. That creates an endless loop keeping the person in mediocrity.

The same goes in finance and investing.

“How can we better help people invest more responsibly? Or is investing FOMO just too great of a feeling to overcome?”

I think the appropriate way to be good at investing is having a good knowledge and always keep things rational. There’s nothing worse than acting on emotions with your finances.

Most important is understanding the basic financial math, reading a lot of information about investing from different sources, and then finally have enough experience – good and bad – to be prepared for many different situations.

I think it’s possible to do it for anyone. The problem is that many people are not interested or willing to improve, whether it’s by a lack of interest, overconfidence or just being overwhelmed with everything in their daily life.

This is sad. I wish there were more people taking their responsibility and improving their financial skills. They would benefit more than they can even imagine…

At least, you are trying to do your part, Sam, with this blog. I wish there were more people like you writing quality content about finance and investing. And .. most important .. more people reading financial content. We would all benefit from it, as a society.

Oh boy, that’s a hard story to hear. How unfortunate things turned out for him. But at least this should be a big enough learning experience that he won’t make the same mistake again. Hopefully his losses were not as big as his entire net worth prior. Oh man, his experience is just so painful to think about.

I’ve never had the risk appetite to go on margin. I can see the benefits, but the risks just largely outweigh the gains for me. I definitely wouldn’t be able to sleep if I was invested big on margin. Thanks for the insights!

Don’t confuse brains with a Bull Market is the best advice and age-old advice. Also, don’t invest what you can’t afford to lose. Lastly, BUY when others are fearful and sell when others are buying or something like that in the Warren Buffet school of Investing. Here is to the market rebound in 2023!

I also got margin called on tesla stock on the way down! Much smaller amount but still 6 figures but it still hurt. The mistake I made was selling covered calls instead of just selling stock. I started getting margin calls around 200 and sold 2025 calls against them to hold my shares.

I also invest my mother’s money Luckily her cost basis of tesla is 220 and only 10 percent of her portfolio.

Everything hurts. But hopefully, we use this pain to better calibrate, our risk exposure and risk tolerance.