Market timing is the strategy of making buying or selling decisions of financial assets by attempting to predict future market price movements. By timing the market, the hope is to make an eventual profitable decision.

Market timing gets a bad rap partially because it's difficult to do consistently to profit. Active fund managers consistently underperform passive index funds. However, I mostly believe the act of marketing timing is misunderstood.

In reality, every investment decision you make is market timing. As rational human beings, we are always attempting to make the best decision possible based on the information we have and the situation we are in at the time.

A profitable decision generally means buying at a time before future prices go higher or selling at a time before future prices go lower. But a profitable decision can also mean buying or selling to help improve the quality of your life. After all, the ultimate goal of investing is to provide us returns to live a better life.

Here are some common examples you might not think of as market timing, but in reality, they are.

Examples Of Market Timing

You are timing the market if you are investing a fixed percentage of your paycheck in your 401(k) each month. Why not front load your 401(k) contribution so you're done by mid-year? Or why not wait to max out your 401(k) with your year-end bonus?

If you decide to replenish your cash hoard until you have 12 months of living expenses before you invest, you are market timing. Why not wait to start investing in stocks once you have three months of living expenses instead?

If you decide to use 100% of your monthly cash flow to pay extra towards your mortgage instead of follow my FS-DAIR framework, you're market timing. Why not pay down debt and invest at the same time?

If you decide to sell some of your S&P 500 holdings because valuations are 50% above the historical median valuation, you're timing the market as well. Or are you making a disciplined decision?

If you decide to sell one of your rental properties because you don't want to manage tenants anymore, you're timing the market. The decision is based on your inability to endure dealing with tenant issues.

Investing For The Long Term Is Optimal

We all know it's difficult to consistently buy or sell at the bottom or top of the latest market cycle. You could sell near the top, but then you have to time your purchase near the bottom correctly. Then there are tax implications when buying and selling investments in taxable accounts.

Therefore, when it comes to stocks and real estate, the best holding period is usually for as long as possible. It's much better to identify long-term investment trends and asset allocate accordingly. Focusing on the minutiae to outperform the broad trend is often a poor return on effort.

However, whenever asset allocation percentages get out of whack you should buy or sell accordingly. Further, whenever you have new capital to deploy, you should always have an opinion about each investment before purchase.

Market Timing The Real Estate Market

In order to write, The Best Time To Upgrade Your Home Is Coming, I had to have a view on where the real estate market was headed. My conclusion was to buy your move-up property roughly 18 months after the latest peak in the real estate cycle to get the best deal possible.

In other words, I was practicing real estate market timing. When I first wrote this post, I didn't want to buy a new primary residence because I felt there would be better deals in the future.

I had the capital to put 20 percent down to buy a nicer property, but I didn't think it was prudent just yet. The economic landscape changed since the beginning of the year, hence, I adjusted my outlook accordingly.

My decision to wait to buy a new property in one-to-two years would prove to be a suboptimal decision if prices zoom higher and if inflation suddenly collapses.

However, I felt willing to time the real estate market based on my experience investing in a couple of cycles. Further, I'm governed by our desire to enjoy our forever property for longer since we just purchased it in 2020.

Now that we're hopefully more accepting of market timing, let me share why I think it's easier to time the real estate market versus the stock market. The greater ability to time the real estate market is one of the main reasons why I prefer real estate to stocks.

Why Timing The Real Estate Market Is Easier Than Timing The Stock Market

I've been investing in stocks since 1995 and bought my first property in 2003. Hence, I've had a long-enough period of time to make a lot of mistakes. But I've also had a long enough time to be able to hone my investing acumen to make better-than-average decisions.

Timing the real estate market to make more money is easier than timing the stock market for the following reasons.

1) The Real Estate Market Moves Much Slower Than The Stock Market

Largely due to technology and globalization, the stock market corrects and rebounds much quicker than the real estate market. Real estate agents, on the other hand, are still able to charge a 5% commission while stock trading is now free for everyone.

When I published How To Pick The Stock Market Bottom Like Nostradamus on March 18, 2020, I wrote in detail why the bottom of the S&P 500 was around 2,200 – 2,400. At the time, the S&P 500 was trading at 2,304.

I planned on backing up the truck if the S&P 500 got to 2,200. But in three weeks, the S&P 500 had already rebounded to 2,800. As a result, I only ended up investing about 35% of my intended capital instead of 100%. At least I didn't sell any stocks.

The speed and magnitude of price movements in the stock market is the main reason why market timing stocks is so difficult. It's much easier to catch a snail than a sparrow.

Based on my home price analysis, real estate prices tend to slowly fade in a down market due to reluctant and sticky sellers. During an up market, prices tend to spike quickly due to the emergence of bidding wars.

Hence, you can time the real estate market easier by buying property after a one or two year decline. Then hold on for the inevitable upturn.

Real Estate Market Timing Example

Although timing the stock market was difficult in 2020, I was able to time the real estate market well and get 100% of my intended capital invested during that year.

In the spring of 2020, I published the post, Real Estate Buying Strategies During The COVID-19 Pandemic. I had just stumbled upon a dream property and wanted to write out my thoughts on how to get the best deal possible.

Public showings were canceled during lockdowns. Only private 1X1 showings were available and limited to two people per showing. Many people were also too worried to consider buying property during this time.

I didn't want to miss out on touring the gem I'd stumbled upon. So, I attended a private showing and instantly saw the benefits the property could provide my family.

Slow Motion Real Estate Market

After six weeks of discussions and negotiations, I got into contract. The offer was for six percent below asking and a 30-day close. But out of fear and my desire to get a better deal, we closed 55 days later.

The sellers weren't happy that I asked for a price concession after getting into contract. But this period of the pandemic still had me quite nervous about our economic future. I had just bought a fixer in 2019 and now I was upgrading to a home 57% more expensive.

Despite all the technology in the world, the real estate market moves at a snail's pace compared to the stock market. Pricing whiplash is uncommon in real estate. As a result, it's much easier to make more optimal buying decisions.

Market timing a real estate sale, on the other hand, is more difficult due to the preparation required to sell a home. Moving out, staging, asking your tenants to move out, painting, and fixing things usually takes months.

I believe dollar-cost-averaging in private real estate funds, like the ones offered by Fundrise, is one of the easiest ways to invest in real estate. Fundrise focuses on residential property in the Sunbelt, where valuations are cheaper and rental yields are higher. The minimum investment is also only $10.

2) You Can Better Control The Length Of Transaction With Real Estate

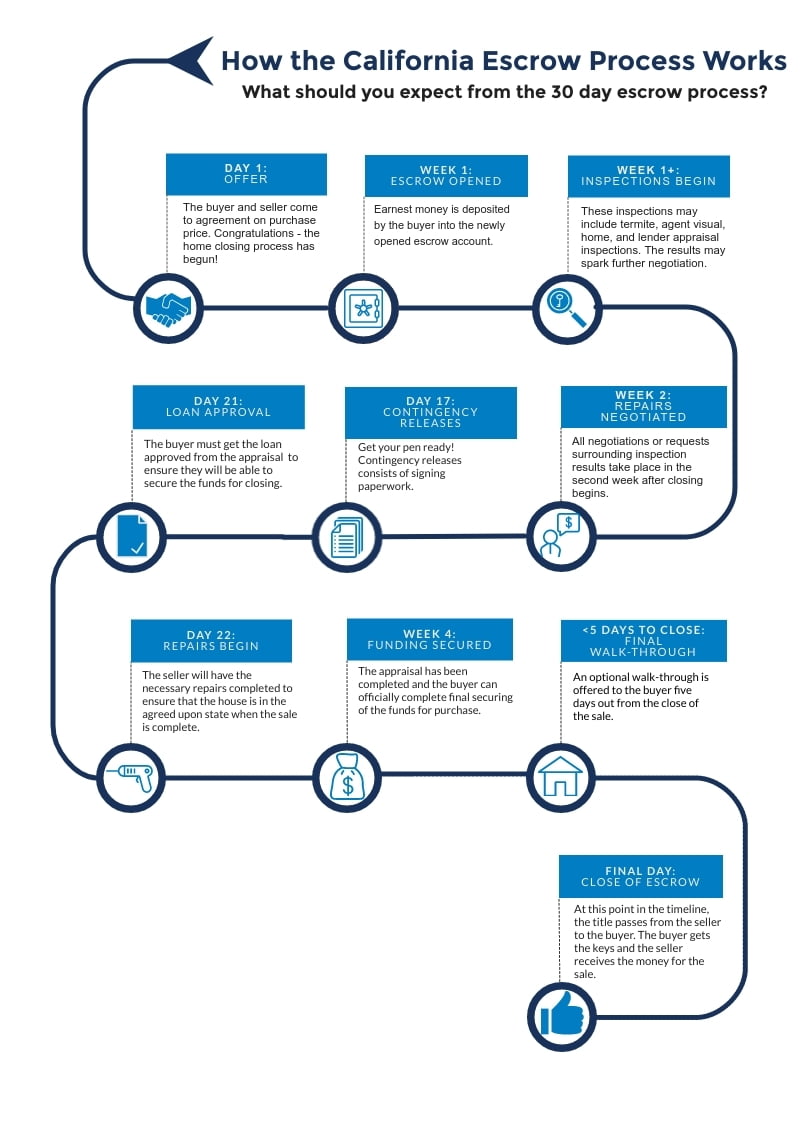

When it comes to buying and selling stocks, once you press the button, your transaction is complete. Your stocks or cash will settle in a couple of days. However, when it comes to buying and selling real estate, the average time in escrow is around five weeks. And during this time in escrow, anything can happen.

Below is a great graphic that shows the various steps of a escrow process. This process excludes all the time you spent house hunting and getting your offers rejected.

Get Into Escrow And Then Negotiate

The escrow process can be delayed mainly due to inspection contingencies and financing contingencies. As a buyer, you have the right to delay closing until all inspection issues are fixed or agreed upon. As a seller, you can drag your feet to accommodate the buyer's wishes or counter.

If you have a financing contingency, as a buyer, you also have the right to delay closing until you can get your financing. Worst case, you can also back out of the deal if you have a financing contingency.

During the escrow period, anything can happen to make you want to back out. Maybe the S&P 500 tanks by 30% during escrow. If so, you have real-time data to help you argue for a lower price.

Conversely, if the S&P 500 zooms higher by 20% during the first half of escrow, you may want to accelerate your close to lock in your price before the seller changes their mind.

Therefore, with real estate, you can better control the timing of the transaction. It's almost like having the ability to bend time and space. Some escrow periods last six to twelve months!

To learn more, read my tips on how to delay close of home escrow to gain more time and money.

3) You Can Negotiate Price With Real Estate

Unlike with stocks, you can negotiate your real estate purchase price. There are also many tactics to deploy as well.

Before submitting a written offer, you can tell your agent to tell the listing agent you're thinking about X price. This whisper price may sway the seller your way. You can also submit low-ball offers across multiple listings to see if any bite.

Once you're in escrow, you can further negotiate on price based on the inspection and financing contingency. Finally, you can always ask for a pricing concession for whatever reason. A price concession can include having the seller pay for closing costs.

Make A Connection With The Seller Or Buyer

Let's say you believe the real estate market will decline by 10% over the next 12 months. But given you would rather buy a home today, you craft a real estate love letter to get your foot in the door.

Once you're in deep discussion then you write a real estate breakup letter to try and get a discount. If you can convince the seller to sell at a 10% discount immediately, then you've successfully bent the market to your desires.

As a minority stockholder, you have no say on price whatsoever. But as the potential sole owner of a property, you have tremendous power to get a better deal.

As a real estate investor, you could come up with an all-cash offer and a quick close to entice the seller to get you a deal. Whereas with stocks, you're almost always paying cash with an instant close so it doesn't matter.

Thoughts On Properly Timing The Real Estate Market

Timing the real estate market is still not easy. But at least it's much easier than timing the stock market given how much slower the real estate market moves.

The key is to know where you are in the real estate cycle. Once you have a good idea, you can make an educated guess on how long the current situation will last before making a move.

Below is the classic real estate cycle that is divided into four phases: Recovery, Expansion, Hypersupply, and Recession. Each real estate cycle will be different than the next. Some will have much higher amplitudes than others. Other cycles will be much shorter.

But based on history, real estate tends to move in 7-10-year bull runs followed by 1-3-year bear runs.

Once you make an appropriate estimate of where you are in the cycle based on supply and demand figures, you must estimate how much time is left until the next phase and so forth.

If you get your timing wrong, it's easier to estimate how much you could lose or gain given the price moves are less dramatic. Historically, real estate prices move up and down any given year by +/- 5%, similar to bonds. Hence, the beta is lower.

The Current Real Estate Cycle

The United States just went through a 10-year real estate bull market (Phase 1 and Phase 2). Supply is still well below the pre-pandemic average, however, demand has declined given a significant rise in rates.

We could say we are at the end of Phase III, despite supply not being in hyper supply. However, what's more likely going on is that both supply and demand have pulled back.

If you own a property with an attractive mortgage rate, why would you sell and buy a more expensive house with a higher mortgage rate if you don't have to?

Given the magnitude of price appreciation and the duration of the real estate bull market, a recession could easily occur for two or three years until recovery.

Buying Real Estate

If rich Fed Governors are emboldened to inflict pain on the middle class to protect their legacy, it's best to accumulate cash if a recession has to work itself out.

As a buyer during any recession, your goal is to try and get a discounted price equal to what you believe will be the bottom of the cycle. This way, you won't have to compete with frenzied buyers during a recovery.

In other words, let's say you believe the bottom of the real estate cycle is June 2025 down 10%, you want to buy at a purchase price down 10% before June 2025. Because if bidding wars were to return by the fall of 2025, prices will move far ahead and you might miss out.

Buying when nobody else wants to buy always feels off; it always does. But it often turns out well given real estate always eventually recovers.

Of course, if moral suasion by the Fed changes, so will our market timing forecasts.

Be A Good Negotiator to Better Time The Real Estate Market

Stocks are a great way to invest passively. No effort is involved once you own stocks. However, there's no way to get a better price at the time of purchase. The only thing you can do with stocks is wait for a better entry point, if it ever occurs.

With real estate, there are so many tactics to deploy to improve your transaction price. If you are an experienced negotiator who can recognize potential, then you should much prefer real estate over stocks.

Eventually, you can amass a large enough physical real estate portfolio and no longer want to do more work. When that time comes, you can then invest in real estate online for 100% passive returns.

Letting a professional time the market and negotiate better terms for a fee becomes more attractive the more valuable your time.

Reader Questions And Recommendations

Readers, what are your thoughts on real estate market timing? Do you think it's easier to do than timing the stock market? If you zoom out far enough, isn't every investment decision market timing?

If you want to dollar-cost average into a weak real estate market, take a look at Fundrise. Fundrise primarily invests in residential and industrial properties in the Sunbelt, where valuations are lower and yields are higher.

Fundrise is long-time Financial Samurai sponsor and Financial Samurai is a multi six-figure investor in Fundrise funds.

We recently closed on a townhome in the Bay Area. Paid 50k more than what the seller’d paid 5 years ago for the property (and the seller has done some remodeling). Similar square footage for SFHs in our area goes for twice as much as our home. Desirable homes in good school districts still gone within a week despite the rate hikes. We’re a little worried that we bought the home at peak, but hopefully things work out as we do plan to stay in this home for 10+ years.

It doesn’t seem like an overpay after five years. Especially if they remodeled the place as well. But over at 10 your time., You will most likely make money.

I try to front load my roth IRA. i don’t really do it to time the market as much as i do it to get the extra quarters of dividends that i would miss out on if i slowly bought in throughout the year. i guess technically that’s timing though. haha

2023-3Q will be a good time to buy real estate. Also, you cannot use love letters anymore on offers. Market timing is super difficult. You know this better than us Financial Samurai – you were in Wall Street. Diversification and dollar cost averaging is key. That goes for real estate too.

I don’t understand how your examples in the beginning are market-timing related.

“Why not front load your 401(k) contribution so you’re done by mid-year?”

Generally people can’t afford to do this so for budgeting purposes they set a percentage of their paycheck to goto their 401k. It’s about cashflow management, not timing the market.

But yes real-estate prices definitely move slower, but you gotta have a lot of cash to pounce on these, again generally speaking.

I can’t speak for other people, but I’m providing an example of what people have done. Let’s say you make $100,000 a year. Instead of allocating 20.5% of your monthly paycheck to maxing out your 401(k) each month, you might jack it up to 41% for your first six paychecks to max it out by July 1.

When do you think the s&p will bottom this time and how low will it go.

3,666 on the S&P 500, potential rebottom mid-October.

“ Why not front load your 401(k) contribution so you’re done by mid-year? Or why not wait to max out your 401(k) with your year-end bonus?”

Because your employer may match a certain amount as a percentage vs. pay, and it is possible to contribute so much early enough in the year to lose out on matching funds.

There are employers who would stick to only percentage match instead of override based on the total dollar amount? You’ll have to give me a numerical example to better illustrate the point. Thx

Sam, I couldn’t agree more. Every time you choose to invest (or not invest) you are making a time bound money decision. I think stock picking and listening to blowhards with “secret” buy level price information for certain stocks is why “market timing” is such a dirty word.

The reality is all money decisions are time bound. Really appreciate your recent efforts to advise us less versed in real estate to view its cycles like we do stocks. Will be interesting to revisit this in a year to see where real estate cycle lands.

They may be time bound based on your personal financial situation. But that’s not the same as market-timing.

Very true points. I’m not a great negotiator, but I do like how there is wiggle room with real estate vs stocks. I also gave up on getting my stock investment “timing right” a long time ago. Now I just try and leg in several times a year and call it a day.