If you're looking at buying a house in 2024, I believe a window of opportunity is open. I had originally written this post discussing buying a house in 2023, which turns out to have been a great time to buy. But now that it's 2024, I've updated it. You want to be buying before mortgage rates come down and bidding wars resume, not during or after.

In my 2023 housing predictions, I forecasted an 8% decline in the national median home price by around summer. The reasons include:

- Higher mortgage rates

- The Fed's insistence to hike the Fed Funds terminal rate to 5.25% – 5.5%

- A bear market in the S&P 500 and NASDAQ in 2022

- A potential recession

Update: Buying a house in 2024 was a great move as prices have moved since then. With so much uncertainty and chaos in the economy and stock market, more money is moving to real estate for more stability and security.

What Happened To Housing Prices In 2023

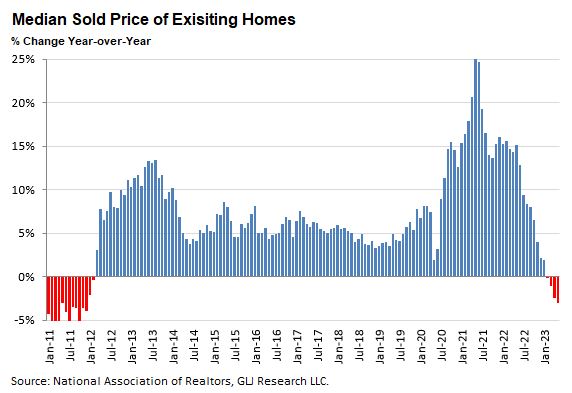

Due to the above factors, housing price appreciation has indeed slowed. In fact, the median home price declined by 8% according to the St. Louis Fed. So I was spot on.

According to Redfin, the median U.S. home sale price fell 3.3% in March to $400,528, the largest year-over-year drop since 2012. That follows February’s 1.2% dip, which was the first annual decrease since 2012.

The slowdown in housing price depreciation was an inevitability given how aggressively homes appreciated in 2020, 2021, and 1Q 2022. A 4%-5% annual housing appreciation rate is more par for the course.

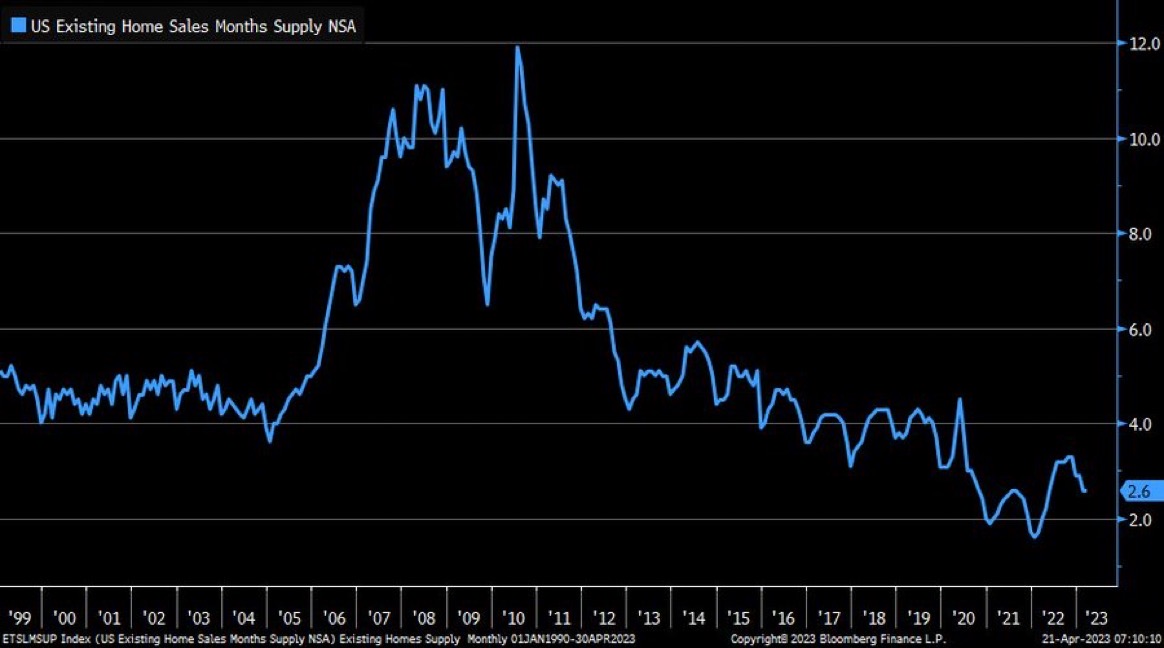

Below is data from the National Association Of Realtors confirming the median sold price of existing homes is finally down.

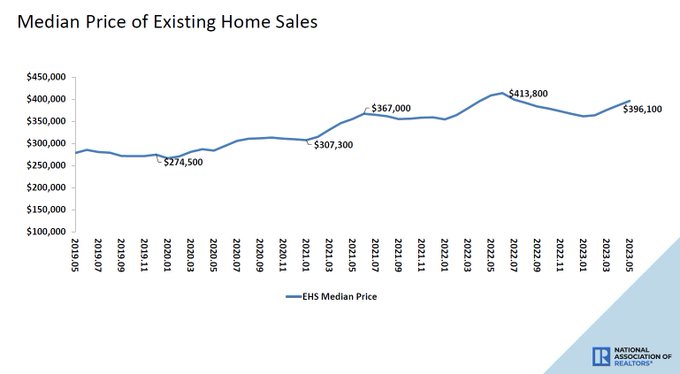

New And Existing Median Home Prices

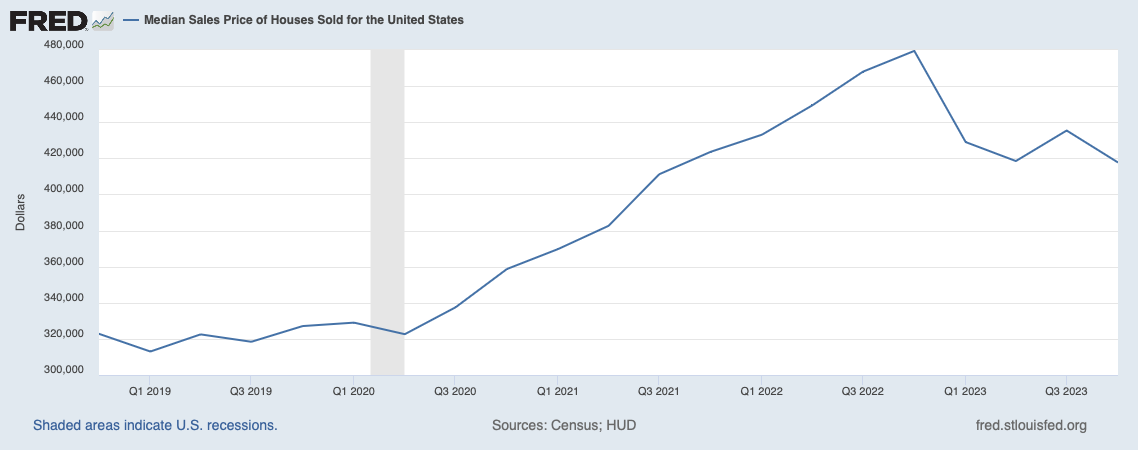

Here is the latest St. Louis Fed data, which has latest data through 4Q 2023. The median sales price of new houses sold declined to $420,800 in April 2023 from $496,800 in October 2022. That's an impressive 15% decline.

According to the National Association of Realtors, as of June 2023, the median price of existing home sales is $396,100, down 4.3% for the year. The bottom line is that prices for new and existing homes have declined in 2023, hence the opportunity in 2023 and in 2024.

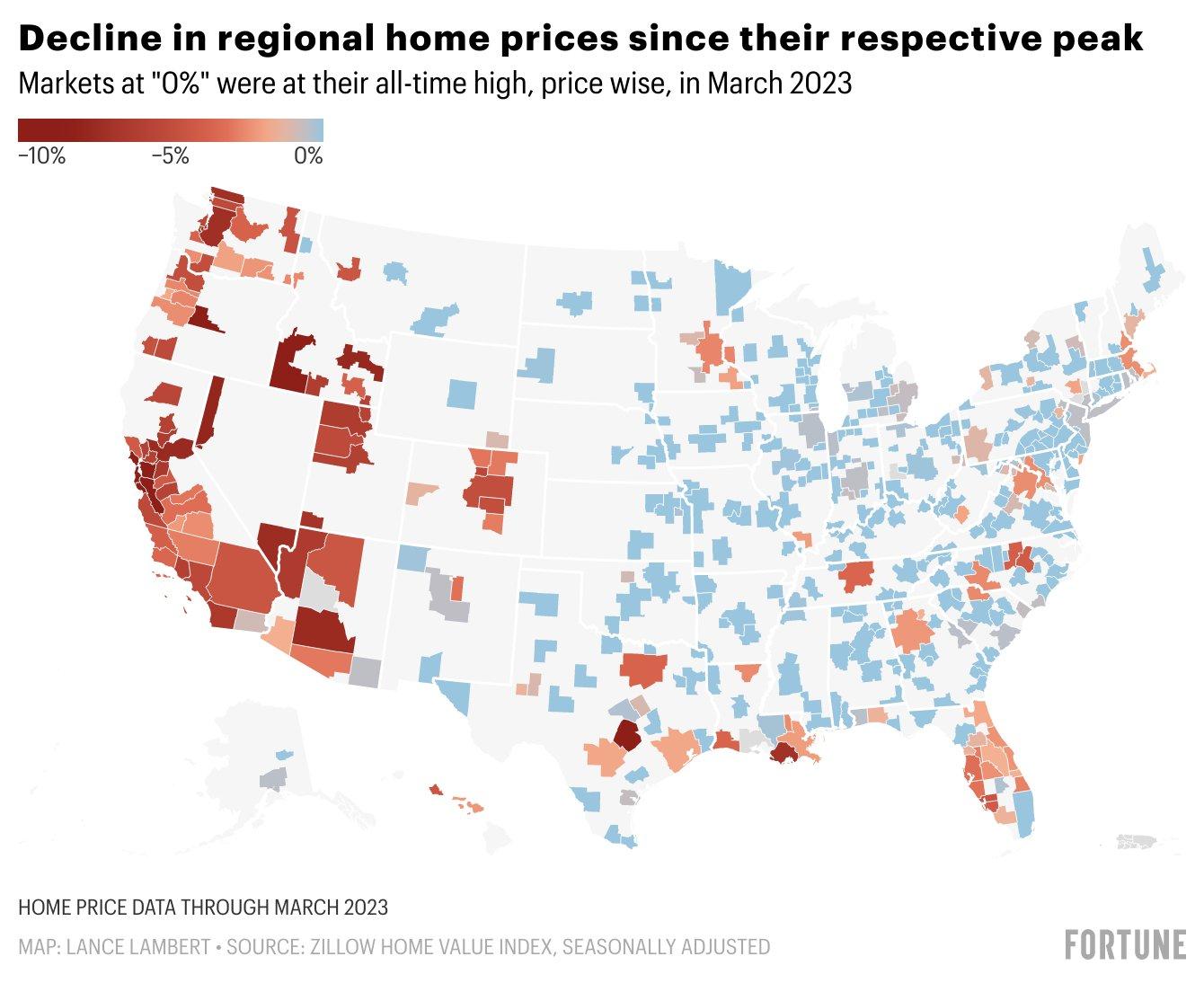

Home Price Changes By State In America

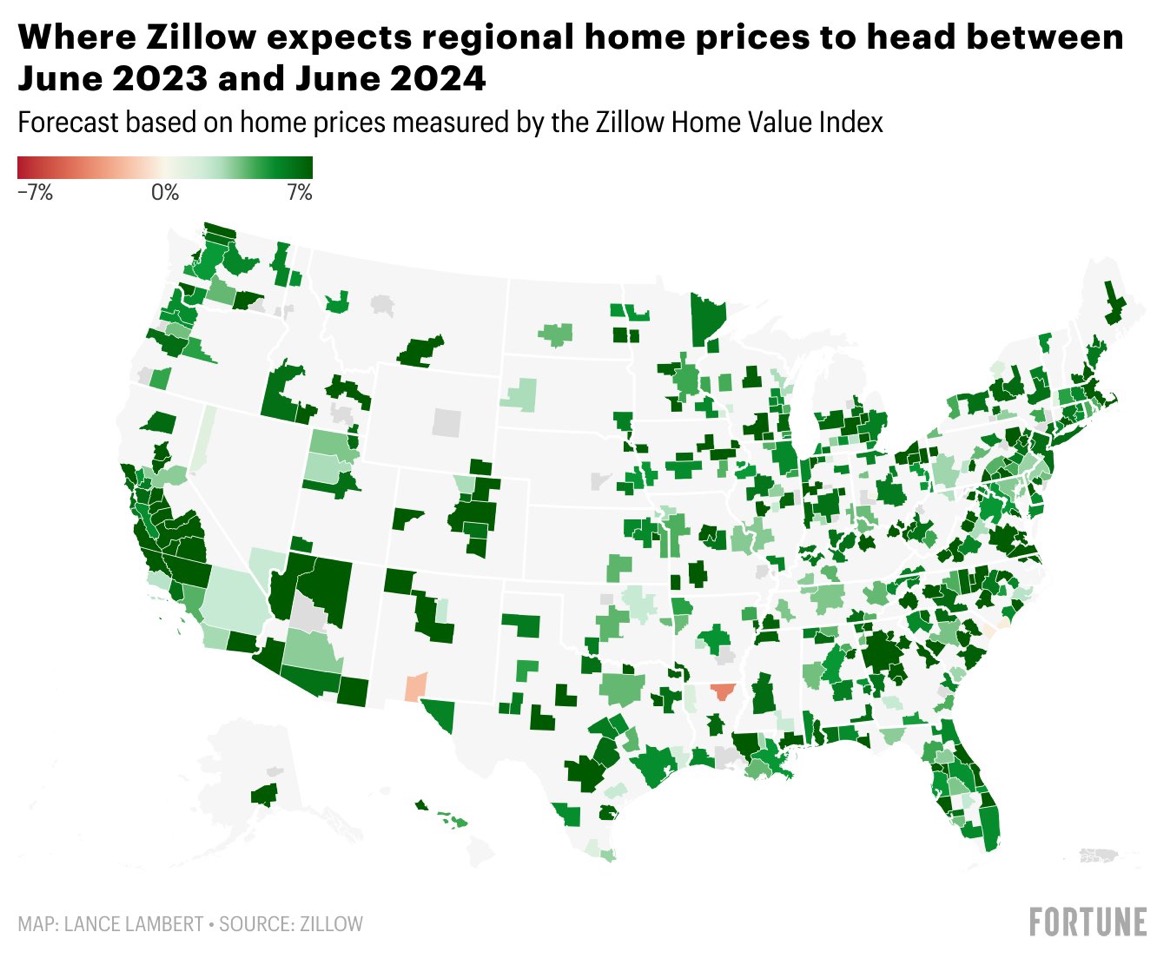

Based on the Zillow Home Value Index, home prices have declined the most out west, but have stayed stable or even increased slightly out east.

Given I live in San Francisco, I may be seeing more deals than those of you who live in Virginia, for example. More deals will, therefore, bias my outlook about buying a house in 2023. So please take this situation into account.

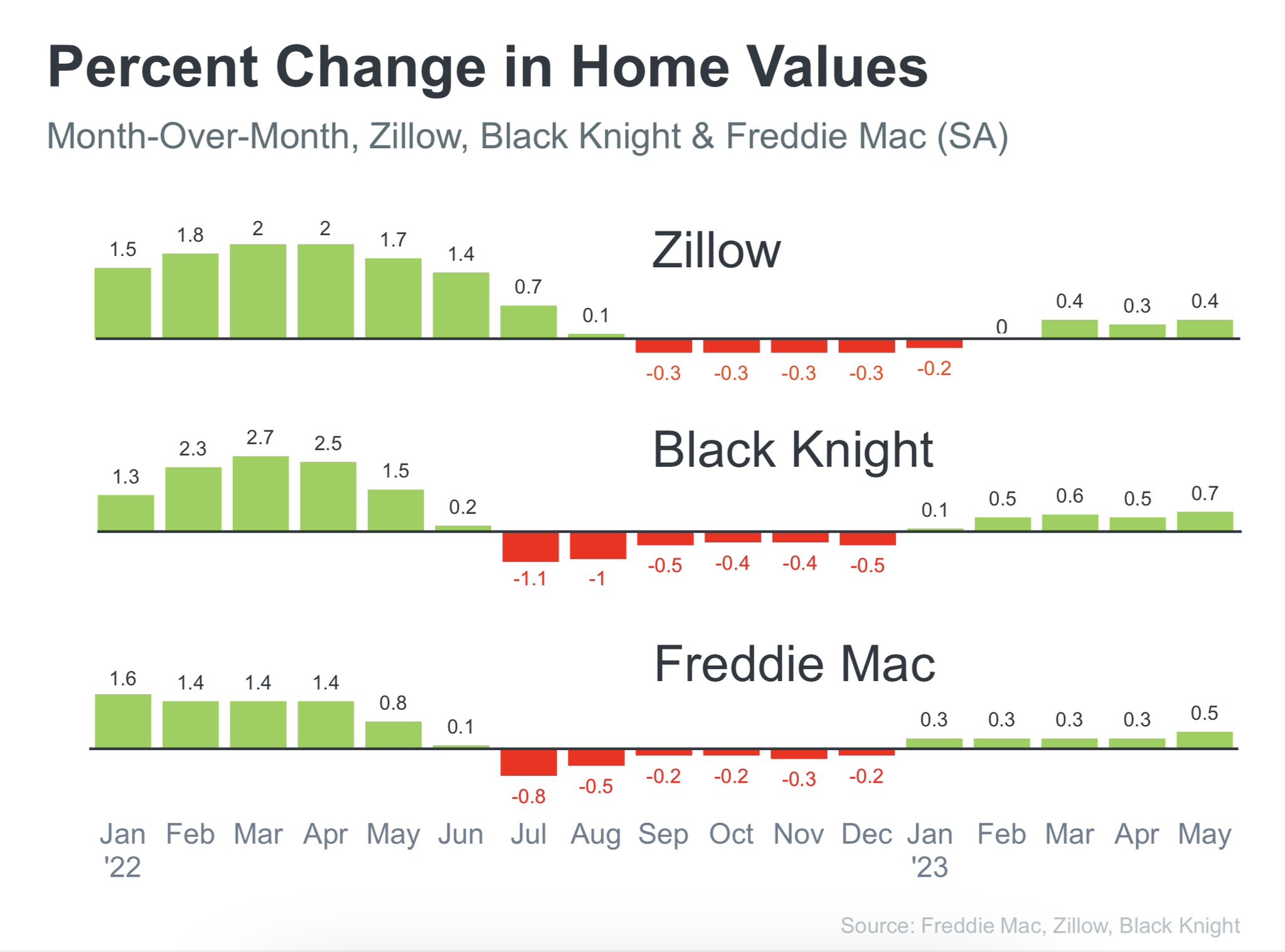

The below chart shows the month-over-month percent changes in home values as tracked by Zillow, Black Knight, and Freddie Mac.

The housing market saw price declines in the second half of 2022. But since January 2023, prices have been inching up. There is seasonality at play here with second half usually weaker.

In addition, Zillow is now forecasting roughly a 6.5% nationwide rebound in home prices from June 2023 to June 2024. The thinking is that mortgage rates have peaked and will head down. Demand will increase as a result, outstripped the increased supply of homes. Although, Zillow has since decreased its forecast, but is still calling for appreciation in home prices in 2024.

The Default 10% Discount Mentality When Buying A House

Whether you're buying a house in a bull market or a bear market, your default mentality should always be to try and get a discount to market. My mentality has always been to aim for a 10% discount and settle for at least a 5% discount.

A saying that captures this mentality well is, “Money is made on the purchase, not on the sale.” The ability to negotiate is one of the main reasons why I like buying real estate versus stocks.

Here are some strategies I've written about on Financial Samurai:

- You can write a real estate love letter to get the seller to accept your offer.

- Then you can even write a real estate breakup letter or price concession letter as a polite way to walk away if you don't get a price discount.

- If you have cash, you can make a no-financing contingency offer to beat out the competition.

There are so many things a real estate investor can do to get a better deal. As minority stock investors, we can't effect change. However, as real estate investors, we can also remodel, expand, market, and find new tenants to enhance the value of our properties.

If you want to buy a house in 2024, start with a 10% discount mentality from last year's prices and see what you can find. It's no different than in 2023, starting with a 10% discount mentality to 2022's prices and so forth.

A 10% discount mentality is the sweet spot because it's not so low as to insult the seller. It's also low enough to make the buyer feel like they've gotten a good deal. To make a successful transaction, all parties must feel good about their decisions.

Over the long run, home prices, like stocks, tend to go up.

Why A Buying Opportunity Window Is Open In 2024

To quantify my buying opportunity conviction, I give 2024 a 6.5 out of 10, with 10 being the highest conviction score. In comparison, my buying opportunity conviction in mid-2020 was an 8.5 out of 10, which turned out to be a 10/10 in retrospect.

In other words, 2024 is not a table-pounding buying opportunity, as we used to say on Wall Street. But my conviction is strong enough that I do think buying now will lead to a positive outcome a year from now, especially the greater the discount you can get.

I'm personally on the hunt for a nicer home because I have children. And the best time to own the nicest house you can afford is when your children are living with you. But I'm not going to buy another home unless I feel like I'm getting a good deal.

Here are the reasons why homebuyers should have more confidence in buying a house in 2024. Buying in 2023 was a great time to buy a house, but it was also much scarier and riskier then.

These are my reasons why I feel it's safer to buy a home in 2024.

1) Pent-up Demand And Growing Cash Balances

Thanks to a surge in mortgage rates, the housing market has essentially been frozen since October 2022. As sellers don't want to give up their sub-3% mortgage rates and buyers didn't want to pay 7%+ mortgage rates, both parties decided to take a wait-and-see approach.

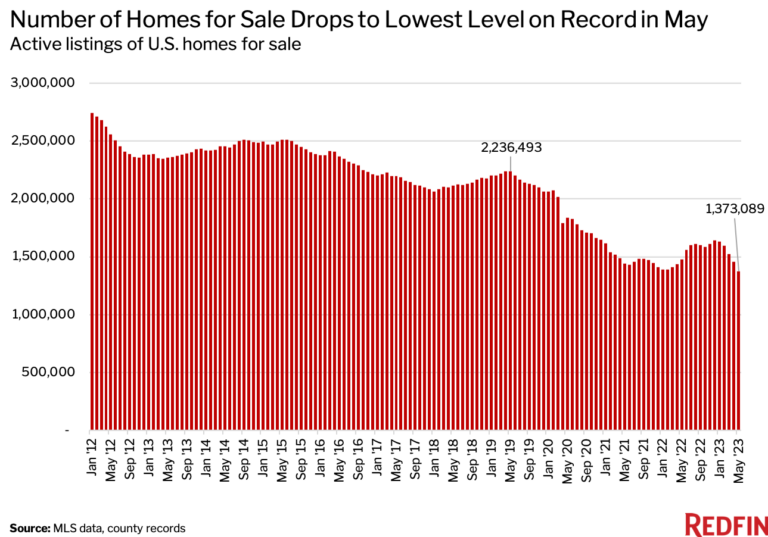

Eight months of lower-than-average monthly transactions ultimately leads to pent-up demand for housing. Housing inventory in 2020, 2021, and 2022, 2023, was already tracking below pre-pandemic levels each month. The longer there is pent-up demand, the more capital will ultimately be unleashed into the housing market.

While potential homebuyers wait, they've been buying 3-month Treasury bills and earning higher money market deposit rates. But the good times for high risk-free rates is ending. Hence, money will start looking for new investments.

Meanwhile, people were still getting married, babies were still being born, and families were still relocating for jobs as they waited for the economy to settle. Therefore, the “need to buy” has been building as well because life goes on!

Personal situation on cash

Since the beginning of 2022, I've been increasing my saving rate in preparation for another recession that no longer seems to be coming. Further, I've invested the majority (60-70%) of my cash flow and savings into Treasury bonds as rates went higher. The lure of 4% – 5%+ risk-free returns has been too great to ignore.

With the remaining 30% – 40%, I've been buying stocks and private real estate funds. In general, I am always dollar-cost-averaging into risk assets every month. It's just the percentage split and the amounts that change.

As a result, I've accumulated the most amount of cash plus Treasury holdings I've had in the past five years. This large cash hoard enables me to be a competitive buyer for another home. Meanwhile, I can easily dollar-cost-average into Fundrise and public REITs in the meantime.

Homebuilding stocks like DR Horton, Toll Brothers, and KB Homes are significantly outperforming the S&P 500. Another indicator of the strong demand for homes this year. However, VNQ, the Vanguard Real Estate Index Fund has lagged.

2) The Stock Market Has Rebounded

The S&P 500 has rebounded by ~17% and the NASDAQ has rebounded by ~35% for the first half of the year. As a result, investors are feeling richer. 2023 ended up a banner year with the S&P 500 up 24%. So far so good for stocks in 2024.

After closing down 19.6 percent in 2022, plenty of investors and Wall Street strategists were worried about 2023. The median S&P 500 forecast was ~4,033 on the S&P 500, while many strategists predicted 3,900 on the S&P 500 or lower. Today we're almost at 4,600.

With better-than-expected stock market performance so far, not only are stock investors feeling richer, but they are actually richer on paper. As a result, there should be a higher propensity to buy real estate given stocks and real estate are correlated.

Real estate prices generally lag stock prices by about six months. And the Oct 12, 2022, bottom of 3,577 in the S&P 500 was a little over six months ago. Although there are doomers like Mike Wilson from Morgan Stanley who believe the S&P 500 will collapse to 3,000, I think this scenario is unlikely to occur.

As a result, buying real estate from here onward is looking like a safer bet. You get the benefit of being able to buy at a 5% – 10% discount, despite the S&P 500 having already rebounded by ~18%. If the S&P 500 stays flat, six months from now, you may experience real estate price appreciation as the real estate market catches up to the stock market.

Personal situation on stocks

My stock portfolio has rebounded along with the stock market. As a result, I feel calmer and richer. I now want to convert more funny money stocks into real assets to better preserve my wealth. It feels like I've been given a second chance.

I have reduced my public stock exposure from ~30% to 25%. For the past 10 years, my exposure range has been between 25% – 35%. I will reinvest the 5% into real estate, other hard assets, and Treasury bills yielding 5%+.

There is an artificial intelligence boom happening in the SF Bay Area which will bring in more homeowner demand again. The earnings results from big tech have been coming in better-than-expected. Stocks like Apple and Nvidia are close to their all-time highs again.

As a semi-retiree, my ideal scenario in retirement is conservative returns with steady income to pay for life.

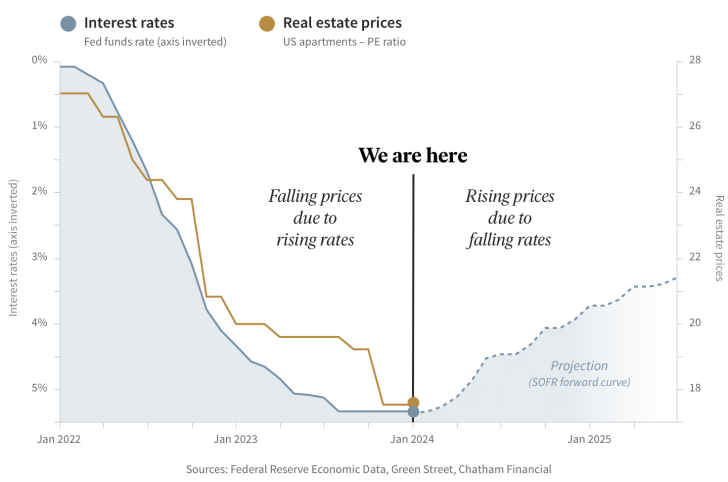

3) Mortgage Rates Have Peaked And The Fed's Rate Hikes Are Coming To An End

It is clear, summer 2022 was the peak of this recent inflation cycle. After another 0.25% rate hike in July, the Fed Funds rate is now at 5.25% – 5.5%, what most market forecasters believe is the peak. We are past the bottom of the real estate cycle.

Now that homebuyers have greater confidence the Fed rate-hike cycle ended in 2023, the housing market will see a wave of pent-up home buying demand get unleashed. No longer is there fear of an accelerating increase in mortgage rates.

In fact, the Fed finally cut interest rates in September 2024.

As a savvy homebuyer, you don't mind paying a higher mortgage rate if you can get a greater discount on the purchase price. After all, you can always refinance your mortgage but you can never change your purchase price. As mortgage rates continue to decline in 2023 and beyond, there will be more purchase and refinance opportunities.

By buying a house in 2024, you get ahead of the curve if mortgage rates do indeed continue to decline. Because you know that bidding wars will return once mortgage rates come down. Buying a home with contingencies is a smart move.

Personal thoughts on mortgages

I believe the long-term inflation and interest rate trend is down. Therefore, I expect CPI to get down to about 3% at the end of 2024 and hover there for the next couple of years. With declining inflation comes declining Fed Funds rates and mortgage rates.

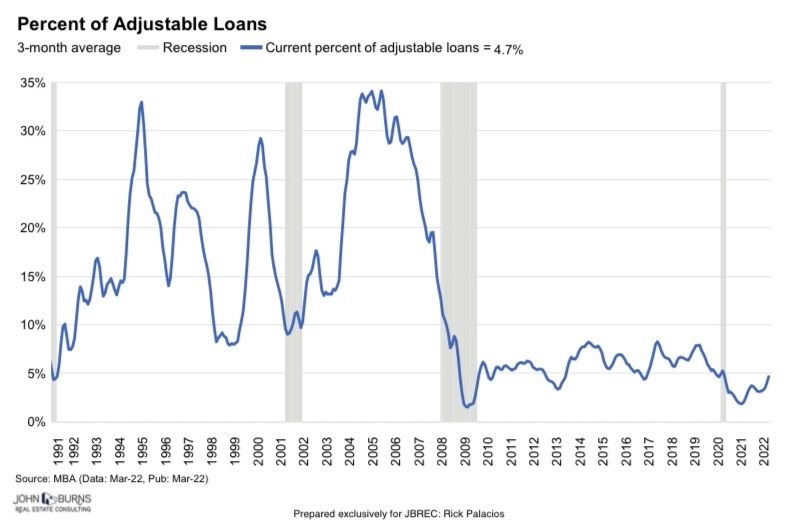

Longer duration bond holders will profit. Meanwhile, the vast majority of homeowners who took out Adjustable Rate Mortgages from 2019 – 2022 will see insignificant upward adjustments in mortgage rates once the fixed-rate period is over.

For example, my 2.125%, 7/1 ARM I took out in June 2020 will reset in June 2027. I have zero worries about a potentially higher monthly mortgage payment. By 2027, at least 15% more principal will have been paid down to help buffer against potentially higher rates. By then, my total income should be higher as well.

Risks Of Buying A Home In 2024

Although a window of opportunity to buy a house has opened, there is no guarantee buying in 2024 will be profitable for you when you finally sell. Always do your own due diligence as investing is your decision alone.

My base case assumption is to buy now with prices down 5% – 10% and then ride a 5% – 10% recovery over the next twelve-to-twenty-four months. Here are some risks to buying a home in 2023.

1) The Risk Of Another Recession

A deeper-than-expected recession will likely cause further declines in housing prices. But even the definition of a recession seems to be fluid. We technically already had a recession in 2022 with two consecutive quarters of GDP declines. We also had an earnings recession with two consecutive quarters of declines in earnings in 4Q2022 and 1Q2023.

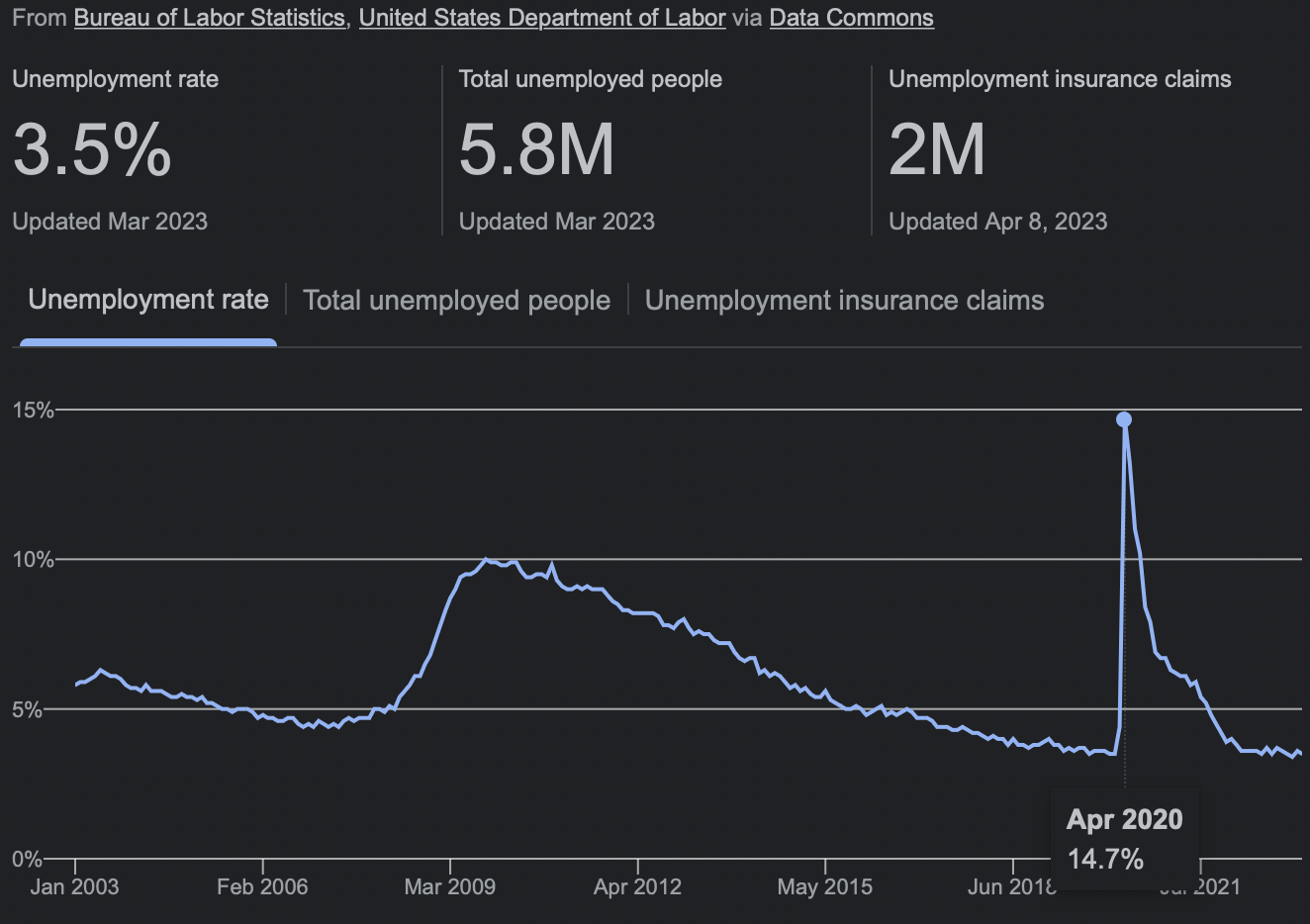

To me, the key economic variable to look out for is the unemployment rate, which currently stands at 3.5%. If there are mass layoffs by year-end that bring the unemployment rate above 5%, then housing demand will likely soften.

A 5% unemployment rate will likely spook homebuyers into waiting again. Inventory will likely also increase given more people will need to sell their homes to pay their bills. If the unemployment rate gets above 6.5%, expect to see home buying demand dry up as budgets get cut.

2) The Risk Of Another Stock Bear Market

It feels great to have rebounded off the October 2022 bottom in the S&P 500 and NASDAQ. Stock investors all feel better as a result. We feel we can spend more and buy more things we don't need.

However, if the S&P 500 gets back to its October 2022 low of 3,577, then housing demand will likely stall out once more. And if the S&P 500 declines by more than 20% to 3,000, we can expect median home prices to decline by 10% – 15%.

I only assign a 10% probability the S&P 500 gets back to its October 2022 low of 3,577. But there is certainly a risk that it does. The bank runs provided a big scare and I'm sure there are plenty more banks with precarious loan books.

The positive of a much higher unemployment rate and another crash in the stock market is that Treasury bonds will get bid up. As Treasuries get bought, Treasury yields decline, and so will mortgage rates.

Hence, there is a counterbalancing mechanism during difficult times. There may also be a flight to safety as investors buy more real assets like housing as well. After 11 Fed rate hikes, eventually, higher interest rates with slowdown the U.S. economy.

3) Inflation No Longer Declines

CPI peaked at around 9.1% in June 2022 and has since come down to 3% as of April 2024. There's a risk CPI stays stubbornly higher-than-desired given anything can happen to energy prices and consumer spending remains strong. This is actually happening right now, which is pushing out Fed rate cut expectations.

If CPI stays sticky from here, average mortgage rates will likely also stay range bound as well. Without the average 30-year-fixed-rate mortgage declining below 6%, there won't be a tailwind to bring in more homebuyers.

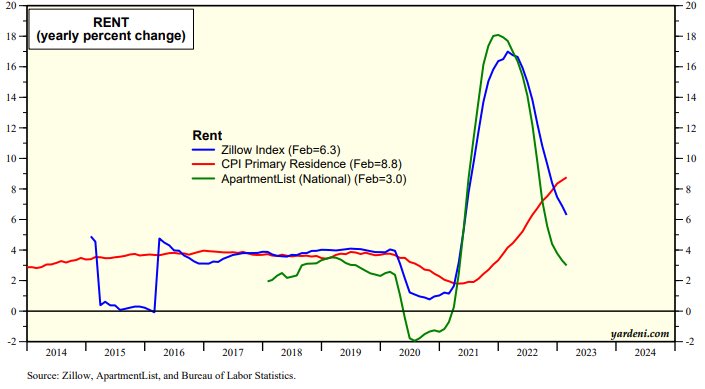

But I assign only a 15% chance CPI doesn't decline below 3% over the next 12 months. The biggest reason why is due to national rents rolling over.

Shelter accounts for about one-third of the CPI index and sixty percent of core CPI, which excludes food and energy. Given the CPI index is a lagging indicator, we can expect CPI and core CPI to come down even further.

Below is a chart that highlights rent growth compared to overall CPI. Where the Zillow Index and ApartmentList lines cross the rising CPI line shows that rents will bring down CPI in the coming months.

4) Risk In Commercial Office Buildings

The return to work movement is progressing, but it may not be as strong as commercial office building owners and lenders like.

A survey by Kastle Systems, a security company, found that the average occupancy rate of offices in 10 select cities was 50.4 percent on Jan. 25, 2023, the first time that occupancy has been more than 50 percent since March 2020. The cities surveyed were San Jose, Calif.; Austin, Texas; San Francisco; Washington, D.C.; Dallas; Los Angeles; Houston; New York City; Chicago; and Philadelphia.

Austin had the highest occupancy rate last Wednesday at 67.7 percent, followed by Houston with 60.3 percent. San Jose had the lowest with 41.1 percent and Philadelphia was second lowest with 42.7 percent.

Given more commercial office loans are floating, there is a risk some commercial office building owners will default on their loans if mortgage rates don't decline far enough. More defaults mean more downward profit pressure on lenders. A wave of commercial office building defaults could cause more bank runs and tightening lending standards.

The acquisition of First Republic Bank by JP Morgan on May 1, 2023 is a positive sign for the banking system so far. We don't want contagion to spread and cause lending standards to tighten too much.

X Factor That Could Be Good Or Bad For Home Prices

Government regulation is an X factor that could positively or negatively affect home prices.

For example, starting May 1, 2023, homebuyers with higher credit scores now must pay a slightly higher mortgage fee. This higher fee subsidizes homeowners with lower credit scores who now get to pay lower mortgage fees.

The idea behind this regulation change is to give more lower credit score borrowers an opportunity for homeownership. They've largely been shut out from the real estate boom since 1990 because they could get or afford mortgages.

This new regulation may increase demand, which would boost home prices. On the other hand, if there are too many lower credit quality buyers, during the next downturn, the housing market might experience a higher rate of foreclosures and short-sales.

Student loan repayments are set to restart in October of 2023 as well. As a result, disposable income for potential homebuyers may decline, bringing down demand.

A Buyer Of Real Estate In 2024 Too

In conclusion, I believe there is a favorable risk-reward ratio to buying real estate in 2024. The rebound in real estate prices won't be as quick as the stock market, but I do believe median home prices will be higher by the end of 2025. There is a structural undersupply of homes in America that is simply getting worse.

A housing crash is unlikely given the high percentage of homeowners who've locked in low mortgage rates or own their homes outright. The home equity cushion is massive compared to 2007. Almost half of mortgage borrowers have 50% equity in their homes. Meanwhile, roughly 40% of homeowners have no mortgage.

If you're waiting to get a steal in the housing market, you could end up waiting a long time. I know plenty of renters who've been waiting for 20 years now!

Bargain aggressively and be willing to walk away from a deal. Don't get emotionally attached to a home because there is ALWAYS another great home around the corner.

Follow my 30/30/3 home buying guide so you minimize your chances of blowing yourself up. Run a realistic worst-case scenario to see if you can truly withstand future downturns. Having buyer's remorse feels terrible. I know after buying a vacation property in 2007.

If you plan to live in your home for at least five years, preferably ten, I think you'll do fine. And if you don't end up making money on your home, that's OK too. At least you will have had a nice place to live all those years.

Check out the 2024 housing price predictions. Most industry experts are calling for an increase. With pent-up demand, mortgage rates coming down, a strong labor market, and a bull market in stocks, I can see home prices performing well in 2024, 2025, and beyond.

Reader Suggestions

Take a look at Fundrise, my favorite private real estate investment platform with almost $3 billion under management. Fundrise invests in single-family and multi-family homes in the Sunbelt, where valuations are lower and rental yields are higher. It's easy to dollar-cost-average into Fundrise given the minimum is only $10.

For more nuanced personal finance content, join 65,000+ others and sign up for the free Financial Samurai newsletter and posts via e-mail. Financial Samurai is one of the largest independently-owned personal finance sites that started in 2009.

I am still trying to wrap my head around the new normal when it comes to prices. Everything has pretty much shot up from the price of milk to houses, but I still do a double take when a house that was sold for $800k few years ago are now selling for $1.2 million.

I bought my current place as a “starter” home 4-5 years ago with the plan to sell it in 7. I’m still passively looking around my area to move to a bigger place, but being locked in at a low rate, and my monthly payment being far less than what I could potentially rent it out for, now I’m leaning on keeping this starter home as an investment and buying another place. I’ll just have to save up more to put down a big down payment.

My neighbor right across from me used to rent his SFH for less than $3k a month. Now it’s listed at just under $4k. Crazy.

It’s definitely hard to give up a low rate. The fear is that massive pent-up demand builds, and by the time rates decline, demand will be robust and mega bidding wars will return.

So much better to buy when things are more normal than crazy.

My oldest son who is 20 just went under contract on his first house. You are right, the opportunity matrix is improving. Here’s what helped him: He’s been preparing for 2 years. He’s worked the same job and has been banking 80%+ of take home while living at home since the start of his senior year in high school. He graduated last year. Because my wife and I have been rehabbing houses for the last 5 years he has learned some useful skills and he has parents who can help rehab the property. This year he will earn around $38K.

As far as getting the house under contract, he was willing to see past the mess of this house which is filled with trash and needs a lot of love. The listing agent I feel made a mistake on this house as well. It was listed on Friday night and we scheduled to see it on Sunday. I view the MLS at least 2X a day. They got a cash offer on Saturday that expired Sunday and they were inclined to take it. We were still able to do a walkthrough and make an offer. As the 2nd offer with only a couple hours left in the deadline he made a strong offer. Slightly over 10% above asking, allowing them to leave all of the stuff behind, and a 20% down conventional loan. I think the realtor greatly reduced the opportunities for offers here by not having the listing up for a week +. This is a small rural area. My son has the 20% down payment saved and will end up with a house payment of around $500 a month with taxes and insurance included. We will have a big project to work on, but it is mostly cosmetic. He got this 3/1 house with 1.25 acres, well and septic, 5 year old furnace and central air for $64,000. Meanwhile in the same area the 2/1 that’s right next to us that is in good repair but not updated just sold for $255,000. Lot’s of opportunity to add equity to his house. I will do a post about this purchase once the loan closes and we can get started on the rehab. In 2 years he can do a refi and drop his P+I payment from around $375 to around $270 if rates drop from 8% to 5%.

Sam – Nice article as always. Been a long time follower of yours since 2015 and purchased your recent book. You inspired me to write my own book as I’m expecting my first daughter!

In terms of this article, you bring up couple of valid points. I now own 6 single family real estate investment properties scattered over San Antonio, TX, Southwest Florida, and Los Angeles, CA.

Even though there are some buying opportunities this year, I’m going to slow down on the single family rentals. With a growing family, I want piece of mind. Going to manage by 6 rentals as-is for long term play. Likely parlay my future investments into FundRise and RealtyMogul. Already have some $$ there like your previous note.

Overall, love your content and want to take a quick 5 min to let you know this.

Congrats on your first daughter and writing a book! Please enjoy the moments, the tough ones and the good ones.

Good idea not getting more rentals too. You’ll want to spend as much time with her as possible. All the best!

It seems like the Fed’s attempts at raising rates are having less and less effect on long-term rates (including mortgage rates) and thus we’re not going to get the kind of downward pressure on home prices that was needed after the excesses caused by zirp. This also makes me worry that we haven’t seen the end of inflation.

Hi Sam,

Thanks for another great post. Are you seeing real estate property taxes go up in San Francisco even though home values have declined y/y? Property taxes have shot up in NY, making it very expensive to buy real estate right now on top of high mortgage rates.

Cheers,

Harvey

Due to Proposition 13, property tax increases in California are limited to 2% a year.

San Francisco homeowner here. We actually got a check from the SF controller out of nowhere for a partial refund of property taxes due to a decline in our property value.

Wow! Impressive! When did you buy?

Hey Sam,

A report from your home town NoVa McLean! House prices are going up crazy still… despite the 6%+ interest rate! Why? No idea… Demand is very strong for great schools and large homes. Last year between June to December, there were some softening. But not anymore. The bottom might have already passed…

Interesting how the East coast seems much stronger than the west coast. It sounds like the fourth quarter of 20 22 may have been the bottom for East Coast.

But when you say the prices are going up, do you have an idea of how much in percentage terms versus last year? Thanks.

I would say it is another 3-5% from 2022 peak, making it a solid 35-40% appreciation since the pandemic low (early 2020). This is for decent size SFH (2500sqft+) zoned for good schools only. Not townhomes or condos.

I guess it’s because the East Coast didn’t see too crazy appreciation like 50-100% in some Western and sunbelt cities during the pandemic. So there is still room to grow.

I can confirm this. We’re in the NJ area only 45 minutes by direct ferry to NYC and we have seen the opposite happen where property prices are continuing to rise steadily and no significant price drops occurred. While it’s good for those who have homes, it’s not very good for those who are first time home buyers.

The job market is also awful, and many people in tech were let go and competition is high. Salaries are coming back down to pre-pandemic standards as well as pre-pandemic working conditions where jobs are mainly in-office.

We also see a lot more developments going up but not for houses, rather for condos and apartments.

Therefore, it will be interesting to see where things go from here for the north east.

Why do you think property prices are going up in the NJ area if the job market is bad and with high mortgage rates?

Demand is low/moderate, but supply is very low (because nobody wants to sell and get a new mortgage at double the interest rate). Thus home prices appear to be stable to slightly increasing over the past 2 months.. Job losses may force people to sell though.. particularly in tech heavy locations… if interest rates get down to 4% there will likely be a lot more activity, but pent up demand will swallow that up.. People are also sitting on a lot of equity in their homes. So taken together I think housing prices will rise slowly but steadily over the next 2-3 years..

I have a question for you regarding selling investment properties. We have (4) SFH left in heartland (TN) where values have gone sky high- rents have increased and cash flow is decent. However due to ongoing maintenance, and the values having gone up so much, if we sold them, took our gains, paid our capitals gains taxes, we would cash flow at 5% (treasuries) more than what we cash flow now on a monthly basis due to the increased values and equity, without even factoring in repairs etc. Our cap rates are 8-9% off our initial investment, but with rising insurance costs, and property taxes those numbers are being consolidated. We have owned all of them for 3-5 years. (We had 6 at one point but ended up flipping 2).

They are all financed at low rates, 3.3-4% on 30 year fixed, and we don’t live on the cash flow for anything- but the large sum of cash we would walk away with would give us more life choices as far as freedom and flexibility. (Career’s, etc)

What’s more important? Letting it continue to grow for the future- or being able to have more time and freedom now? We are DINKS, mid 30’s, and live in a high cost of living area, So Cal. I will say after a health scare last year, our thought process has changed a lot. It use to be all about budget and accumulation of investments and properties, now it’s trying to find a balance of enjoying some of the fruits of our labor. We don’t know if kids will be an option or not at this point.

I’m really torn on to sell them or not. Thoughts?

How about split the middle and sell 2 out of 4? As a real estate investor, the ideal holding period is forever IMO.

Financial Samurai has previously mentioned the value of interest rate arbitrage. with your 3.3% rate range, you are 3% below current owner occupant rates and at least 4% under investor rates. With your 4 homes, I’m thinking you have $600k + of debt with a great arbitrage. Although you can generate more cash flow today, you will sacrifice quite a bit of wealth liquidating the properties through realtors and taxes. You don’t need the money, let it ride. Hope all is well with the health scare

Sam,

Unfortunately for my family, we’re still 3ish years from buying another home. We’re fortunate to live in a desirable neighborhood in Denver, with no intention of moving far. Currently homes are going quick, especially anything reasonably priced. What to you anticipate as annual price gains after the ‘bottom’? Trying not to FOMO into buying something before we meet 30//30/3 rule. We can only save $4k a month so need some runway

I don’t think the real estate market will run away from us on the upside. I’m thinking 8% down from peak in 2023 and perhaps a 5% – 10% grind higher in 2024/2025. You’ll always be able to find deals.

Further, you own a home that will ride the wave. And you can invest in real estate through public REITs or private real estate funds to ride the wave as well.

Sam, I’ve been slowly building my cash position in anticipation of purchasing a new home for my family with the intention of converting our current home into a rental property. With the cash I have on hand that I plan to use toward a downpayment on a new home, do you recommend keeping the cash in a high-yield Cash Management account (like Empower offers) or investing in something like Fundrise? My purchase horizon is 12-24 months. Thanks.

With money market funds and Treasury bills (1 year or less), yielding ~5%, I’d mainly park my money there.

Given you’re 12-24 months away, I would also invest 20-30% in some real estate related in case the real estate market takes off. You don’t want to be left behind.

For Fundrise, you need to be willing to invest for years. Hence, with your time frame to buy a house, it wouldn’t be appropriate. A public REIT or real estate ETF would be more appropriate.

I just checked Zillow and there aren’t many houses for sale. The inventory is low so it’s hard to find the right house. If you can find the right one and get a 10% discount, that sounds like a good deal. Not a bad time to buy if you can.

Yeah, high quality inventory is still lacking. But I did just notice the number of HOT-labeled homes on Redfin has spiked way up. Very interesting.

Sam,

What is your perspective on holding on to real estate if it isnt cash flowing at this time and only have a small amount of equity in it right now? Do you weather the next few years waiting for more buyer demand / better market to sell? Or do you cut losses now and focus on finding investments where your money will perform better and can find a property that actually cash flow? Or just investing in anything that will perform better than having to contribute $450 extra a month to a rental property payment. Bought a rental property recently (1 year ago) and switched strategy from airbnb to long term. My initial airbnb projections were off. Thank you and I am a long time subscriber and purchaser of your amazing book!

Hi Brett – Thanks for picking up a copy of Buy This, Not That. I’d appreciate a review on Amazon.

Because I believe the real estate market will rebound by mid-2024, I would hold on for better days if you can. I just don’t know enough about your finances to understand how painful $450/month is to you or what percentage loss is it.

I buy property with the intention of owning for 10+ years. In SF, the first two years is often hard to cash flow.

Perhaps this post will help: When To Sell Your Rental Property. I just remember I wrote it and should update it. Google “topic + Financial Samurai” and I’m sure something will pop up!

aloha sam from taipei – thank you for your timely and generous insights and congrats on the book launch here (i bought the english version awhile back). i have been researching fundrise but am a bit concerned about their large number of holdings per fund (77 properties for flagship fund and 52 for income fund) that may end up diluting return and their foray into silicon valley venture investing that may take the focus away from sunbelt. what is your take? i’m also looking into individual projects on crowdstreet but feel a bit underprepared to build a portfolio and avoid analysis paralysis per deal. given real estate is the long game, would you have advice on how to incrementally commit, ‘learn while you invest’, while keeping enough chips in your pocket to see the end? warm regards.

Hi Angie – The venture fund is separate from the real estate funds. Have you seen otherwise? If so, let me know and I’ll double check with them.

I would just dollar-cost average with money you are comfortable with and go from there.

I think the nature of work and the need for office space has permanently changed and will never go back to previous occupancy rates for commercial real estate. Add to that the impact of AI and the reduced need for human resources and the concept of large office skyscrapers will be obsolete. Companies can increasingly leverage leaner workforces and increasingly powerful distributed software services. The few remaining employees can work remotely or occasionally meet in colocated workspaces at fractions of the size of previous offices. We’re already seeing big companies not renewing leases or even getting out of leases. What this means is previously safe commercial real estate portfolios will have to be drastically written down and it may be even sooner than people realize; banks stand to lose substantially. Sam, I’m curious about your thoughts on this subject as you may have some interesting insights about how much banks may have allocated to commercial real estate in their portfolios, how much of that was leveraged, and the potential that this could result in something similar to what we saw from the residential real estate debacle in 2008. I have a feeling this will start to snowball as more banks realize this and nobody wants to be left holding the bag.

I agree office buildings have seen a likely shift down in the demand curve with WFH. Maybe more will be converted into residential.

The decline might be slower than expected due to workouts, a decline in mortgage rates, and a growing percentage of return to offices.

Regional banks also have a larger percentage of their loan book exposed to commercial office buildings. But the Fed has demonstrated it will be a backstop.

Thanks Sam. I certainly appreciate the analysis. I’m extremely grateful that I didn’t succumb to the very real temptation to sell my home or any of my rentals. I’ve owed nothing on any of them for years so that would be a huge (to me) amount of cash even after Uncle Sam got done putting me through the wringer.

Naturally the overall rate of return has diminished as the value has skyrocketed but not in on the ground terms. Rents have steadily risen. Compound this with the fact that real estate is the only investment strategy that I’m very experienced in (Other than stuffing money involuntarily in a state pension system) so I feel comfortable with it. Yes, I’m glad I stayed.

Nonetheless I think you are correct in your assessment. The only thing I worry about is that as a nation we are increasingly turning into less homeowners, with more renters and inescapably landlords. I wonder how that will play out if the trend continues

Your worry is also a worry of mine. What if those rents, which as you mentioned have steadily risen, don’t come down? I would say that would surely impact inflation. The Fed needs inflation to come down and will do what it takes for as longer as it takes, or so seems the message that I have been hearing.

Median rents have already rolled over a lot. You’ll see the results in this summer’s CPI.

Yes, with real estate, it’s a war of attrition. Whoever can own their real estate holdings the longest generally are the wealthiest.

As many renters tell me, they enjoy renting and believe there’s nothing wrong with renting. As a result, I say it’s a more win-win scenario where both landlords and renters win. Hooray!

Hey Sam, good insights, I’m reading “Buy This, Not That” right now too!

I’m actually on the seller side of things right now, would love your perspective. My husband and I bought a single family home in La Mesa, CA back in late 2019, it’s an older home and we spent a lot of time/money fixing it up. We’re still dealing with frequent repairs, a pool, canyon land to maintain, lifestyle creep we don’t want anymore… we miss our simple condo lifestyle and want to sell the house, move back to the condo (it’s rented now), and invest the nice profit from the last few year’s appreciation into index funds. We’re close to reaching our FI number (learned tons from Kristy Shen/Firecracker, Vicki Robin, and you), selling this house will let us reach it and we’ll be able to quit our jobs in ~2 years to travel the world full-time (our life dream).

We want to sell our house now in June 2023 to hit the peak selling season, but do you think it’d be worthwhile to wait until Spring 2024 instead? I’m seeing lots of corporate layoffs, if interest rates come down I imagine more houses will go on the market and prices could soften (right now inventory is nill here in SD). I’m just not sure the payoff of waiting to sell til ’24 is worth the risk of the housing market stalling or reducing then. Thanks in advance

Hi Jess,

Thanks for picking up a copy of my book. If you enjoy it, I’d appreciate a review on Amazon.

As for your question, to stay consistent with my thesis, I think waiting until 2024 will get you a better price. If you list now or this summer, you may be contending with buyers like me and thousands others who are looking to get a great deal. Because buyers feel that those who list now must be more motivated given rates are still high and most people don’t want to give up their low mortgage rates.

At the same time, you bought at a great time and are probably up a lot. One of my other themes of this post is that people are sick of putting their lives on hold. So you can certainly try this summer and see if you can get a price that you would like. If not, you can always try again.

All the best!

Sam

PS I can’t believe Kristy and her husband have been so anti real estate for the past 10 years! If they bought in Canada, they would have made way more money than the Canadian stocks. Oh well.

Sam, thank you for your work, I have gained so much insight from your writing and I always look forward to these real estate updates.

My wife and I (both 35) just purchased our first home in Placer County, we closed Christmas weekend 2022. We negotiated a 10% discount + 3% cash back from seller to cover closing costs. No other buyers in sight, no competition, it was during the 30 days of rain we had here in Northern California.

We knew it might not be the best time to buy but we were really nervous of having to buy among the “wait and see crowd”, who typically have tons of equity/cash ready to scoop up deals. Plus, our rate of 6.25 isn’t really that bad, historically.

I absolutely agree with you that millennials want the same things as previous generations. Every one of my friends (all in our mid 30s) had kids and bought homes the past two years. These are college educated people with high credit scores and stable jobs.

As for the future, I work in residential construction and people seem to feel positive in our area, work is steady, I feel very lucky. I’m not positive it will stay that way, but it seems like people have a psychological obsession with doom and gloom, and predicting collapse- I have been hearing talk of economic collapse for years. In our area I just don’t see it happening, it could! No one really can predict the future, but there has been a massive influx of people to Placer County, we just finished a new construction home for a customer who moved from Encinitas- crazy! Lots of Bay Area folks discovered this area during the pandemic and I believe it will never be the same again. This is good for everyone, a rising tide lifts all boats in my opinion.

So I just hope things remain good for people, and we make it through the correction and recession without too much catastrophe!

Ah, nice job buying property during my favorite time of the year. Good job getting that 10% discount too.

I was just in Tahoe two weeks ago with the kiddos. They sledded for the first time and had a blast.

I’m not looking to buy but I am in the process of doing some major renovations to my current home. I know what you said about renovations being a PITA, but I’m in no rush. As long as they don’t try to rob me, I can be patient. I’m doing add-ons, so it won’t affect my current living space that much.

I do have a question. You said you plan to convert your stocks into real estate and “other hard assets”. Can you give me some examples of hard assets that you like?

I fully expect a real estate crash, Sam!

Most likely not residential but commercial is looking bleaker every month.

I definitely increased my house buying target year to be ~2027. ’08 took ~5 years before housing really bottomed. It just takes forever before housing prices come down.

I personally believe landlords in my town of Austin, TX just doesn’t get it’s not 2022 anymore. I got a renewal offer for $1415/mo (from $1375/mo). I asked to renew at $1375. They said no. So I moved to a much better place (20% bigger and 20% cheaper).

The prior landlord now has 6 vacant units, about to be 7 with mine on the market.

I am willing to rent for the next 4 years!

Sounds good to me. Your new landlord is probably appreciate of your 4 years of stability as well. Everybody wins.

The question is, how much percentage down is a crash? And when will you know when it’s time to buy?

I want to get people to be more analytical about their viewpoints to build more wealth and make better decisions over time.

I agree. I love my new landlord and I want to do everything I can to keep the place in great shape.

That is a question that will definitely be hard to answer . Knowing me, I don’t think I’ll buy at the best price :(

I also think I’m a little biased about real estate because I live in Austin .

Buying a house in 2023 definitely could turn out to be a great decision!

I look forward to your deep dive analysis. We are all at least a little bit by us based on our own investments.

Well, I asked why you didn’t buy in Austin in 2020 or before?

Currently in escrow for a home we offered 11% under asking on (seller accepted). It’s an area where tear downs are common. House needs a lot of work but we love the historic feel and have no desire to tear it down, just make cosmetic improvements. The seller ultimately chose us because she heard our story, and loved the idea that we plan to raise our two boys there just as she did hers 20 years ago, rather than flip or merely invest. Feels like a win-win.

Sounds like a win-win too. Sellers love to hear their buyers or on for the long term and rehabilitate their properties after they have sold.

When the sellers would love to rehabilitate as well, but they might not have the time or money or ability.

Would be interested in your perspective on living in SF. You obviously love it yet we read so many articles about crime, filth and homelessness making the city unliveable so wonder how much of that is true and also what effect those things have on real estate values. Realize you live out west so maybe away from the problem areas. But still would think you would experience some effect from these things.

The greater the city, the more heat there is. It’s generally like that with anything. I would encourage you to come over and take a look for yourself experiencing things for yourself. Experiencing something for yourself is generally the best way to know.

Now there’s the AI boom. San Francisco is one of the cheapest international cities in the world, especially when you compare to the income generating potential per capita.

London Breed should hire you as a cheerleader. SF is really bad right now. Elon is very vocal about that. SF would be a great RE market to short. The city needs a Gulianin-type transition but the city is bereft of competent leadership. The chances of being the victim of a random crime deters me from visitng my favorite restaurant Sam’s Grill as one needs to park at 555 CA then walk a block – lots can happen in that block in FiDi.

Where do you live in SF to experience this crime?

If you feel insulated from the crime then I am happy for your luck so far. I would just feel unsafe having my family live day to day in a city that has defunded the police and hosts the biggest open air drug usage forums in the country. And a lottery for high school? I just don’t get it when there are so many nicer places in Norcal let alone Santa Barbara or SoCal. I’m only up here for the job market; we’re back to the beach in OC as soon as I feel comfortable moving away from the security of this job market, probably ~3 years. The Bay area is only good for building wealth – quality of life here sucks compared to South OC or San Diego. But I’ve defintiely built a lot of wealth here quicker than I could in any other job market in the US with a computer science degree.

What neighborhood are you experiencing all this crime though? Strategically, the media or people against SF will focus on the worst neighborhoods and try to make it a reflection of the city. It’s par for the course for an expensive city, where fewer than average people can afford.

If you live in one of the worst neighborhoods, and feel unsafe, but have made a lot of money, I think it’s worth paying up to move away from that neighborhood. No point in making a lot of money to only feel unsafe and in danger.

But I just looked at one of your previous comments and it doesn’t look like you live in SF either.

I understand that suburban living is different from city living. You just have to be comfortable with the pros and cons of each. Everybody is different, and I understand if you dislike San Francisco because of your political views. But I would try not to let San Francisco get to you because it shouldn’t affect your lifestyle if you don’t live here or want to live here.

“ We’re in a big name school district that is super popular with Asian families that can’t quite afford Saratoga/Cupertino/Palo Alto/Los Altos, and we bought an small home below our means which will make it a super attractive well priced rental, and I took advantage of the Dem’s misguided climate policies to take my home off the grid with a 26% subsidy for the full Elon stack.”

But it does affect my lifestyle. I’d like to go to Sam’s and to the Bay Club Gateway to play pickleball/tennis/swim etc on a nice sunny day but the thought of random crime is a real deterrent so we stay comfortably ensconced in the South Bay. My wife and I used to even entertain thoughts of buying a small retirement place there but that SF of 10 yrs ago is a faint memory. Unless SF solves the pervasive crime and quality of life issues via much tougher policing the city will go BK like NY in the 70s as their tax receipts are plummeting.

Got it. Thank you for caring so deeply about San Francisco. And I’m sorry something happened to you during your visit. Leaving in fear stinks.

Funny you should mention Gateway as I just went to a party there play pickleball and celebrate their new 6 courts! We had margaritas in the hot tub after.

But there should be some good tennis courts and pickleball courts an hour south where are you live, ie Broadway, Redwood Shores are good clubs. Palo Alto has a huge public pickleball court area. I was at Menlo Circus Club the other month and their pool and tennis courts are nice.

Personally, I wouldn’t drive more than 30 minutes to play tennis or pickleball.

The constant bashing of SF from people who don’t live in SF is amazing. It’s weird how SF lives rent-free in so many envious people’s heads who also happen to be Republican.

People love to hate on California, our PR is so bad right now haha.

I lived in Nashville, TN from 2016-2020 and the comments people I heard every day about California were hilarious, and those people commenting had never been out west to experience it for themselves ha.

After living in the south, and traveling to cities all over the country I can say this- these “hot” markets like Nashville and Austin are only popular because young attractive hip people made them cool. Take away all the hipsters, all the bars, all the restaurants- and you are left with ugly fly over cities with horrible weather. Their hype and prosperity purely relies on their trendiness.

California on the other hand is the best “raw material” on earth. Strip away all the people and businesses and you have the most beautiful land imaginable, with the best weather. There is no other Big Sur in the world, people all over the world dream about seeing it, or Joshua Tree, or Lake Tahoe. You can surf world class waves and ski world class mountains in the same day. This is the value of California and it doesn’t go away.

California is a great place to live no doubt, but you have to be willing to pay for it, especially if you are high income. California bases its budget on gouging a tiny sliver of high income folks, with the highest personal income tax rates in the country. People voted twice to raise them even higher, but only on high income brackets. This is only going to get worse. If a relatively small number of the very high income people move, it will create havoc for the state. I am one who recently left and moved to a no tax state. My guess is that more follow and this becomes a bigger problem for the state. Good luck.

You’re right. It costs a lot more to live in CA.

But if you’re rich, or you can afford to live in California, many people do due to the higher quality of life.

See: Life Expectancy By State

Sam, love these real estate market updates! My favorite posts by far! Want to shop for an upgrade but would likely only consider new construction. Don’t have the patience for renovations. Want the house to be exactly the way I want it and problem free. Hard to get that with a used home. Contractors are the absolute worst!

Yeah, you might have to pay a premium. I truly do believe remodeled homes will sell for greater premiums now given how much of a pain it is to remodel.

Great article Sam. So thankful to have been a long time follower of Financial Samurai. Your content is the very best out there. You’ve introduced me to the average networth for the above average person (Financial Sam readers), buying my dream home, and so many incredible topics, not the least of which- the now discontinued Rolex Milgauss, which I picked up in October and has now become my favorite timepiece.

Anyways, I feel like 2023 is not a good time to buy a house. As much as I’d like for it to be, to expand my single family rental home portfolio, I’m just not ready to pull the trigger. As an insurance professional, the rebuild cost versus the listing prices in my area (Midwest/West) seem out of whack. Home prices seem to me, to be overinflated, with room to fall. That, coupled with current rates in the upper 6s make me hesitate and take a wait and see approach. Perhaps towards the end of 2023, I’ll feel differently?

Lucky for me, I’ve put your advice to good use over the past decade, and I can afford to “pick my spot” when opportunity re-emerges. Thanks again, for your incredible wisdom and entertaining articles.

Yeah, buying now is not a table pounder. The difficulty is figuring out when. If rates drop a lot by end of 2023, then waiting until then will result in missing out on some price appreciation. So the goal is to buy ahead of the frenzy.

Let’s see what happens!

Didn’t know the Milgauss was discontinued.

The Milgauss was removed from Rolex website March 27th. I visited my local AD teo weeks ago, and got on the waitlist for a steel Daytona… probably won’t happen soon, but similar to real estate, I can afford to wait and if it doesn’t, oh well I’m content with my properties and watch that I have now. The rest will be gravy, I guess.

You truly do, make your money when you buy, not when you sell. Thanks for all the advice. As my daughters have begun to enter adulthood, we’ve established Roth IRAs for them, and I continually forward your work to them. Your book, “Buy this, not that” has been referred to friends and family alike. Thanks Sam.

Ah yes, I got me a white and black face dial SS Daytona from 2008-2009. Keep them unused actually. Same year (2008) I got my black face green Milgauss. Crazy how time flies!

Thanks for referring my book and leaving a review on Amazon. Appreciate it!

As they say in real estate, “marry the house, date the rate…”

Hi Sam- leading economic indicators all point to a recession by late in the year. I think it’s likely we will see a significant decline in the stock market. Your optimism about where the economy will be heading this year is a surprise to me – but we will all see!

Indeed. Time will tell. If you believe we are going into a recession, and the Recession will negatively affect surprises, how are you investing as well as your new cash?